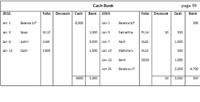

Cash book is most significant accounting book of opening as transactions relating to currency are recorded here. The balance of cash wants to determine every day to tally it with the accessible cash in hand. For big enterprises, though, it may not be probable until next day to locate out the cash transactions for the prior day as entries can be prepared at a later stage also until the day is closed.

Accounting Cash Book