Management summary

As banking service in Bangladesh has been continuously attracting more and more customers because of the packages’ unique and convenient features, this is always a wise choice to launch any suitable product in this sector. Bank Al-Falah, one of the leading banks of Pakistan, is just a little away from the formal inauguration of its operation in Bangladesh. The bank has already got significant amount of success in Pakistan by giving special emphasis on its car loan service. Now in Bangladesh, it is considering the launching of its key elements of success-“car loan” by exploiting its early experience, although achieved under a separate circumstances .To repeat the same success under a different circumstances, the bank officials think that they must prepare a comprehensive and strong marketing plan by giving special emphasis on the factors critical to this countries economy and environment. In its marketing plan, the bank wishes to concentrate on the basic factors involving the marketing of the service next year along with the results expected from implementing the plan.

Economic Projections

The bank wants to evaluate the critical variables of the economy which are likely to affect the marketing of the bank for the product in the coming years. The factors that the bank considers as critical are employment, personal income, inflationary pressure, government regulation .The way in which those factors are expected to affect the marketing plan is described below-

personal income: This is always important to anticipate the average personal income of the prospective customer. This is necessary for the bank officials to identify who the prospective customers are and what their income level is .The company has selected the following sectors of customers.

| Class title | % of people falling in the class | Income level (in BDT) per year | Product for which the loan is offered |

| Upper class | 5% | 600000 & above | Any type of auto that the customer demand |

| Upper middle class | 10% | 300000 & above | Personal car (better) |

| Middle class | 37% | 120000 & above | Personal car (good) |

| Lower middle class | 42% | 72000 & above | Auto for business purpose, i.e. taxi cab, CNG auto rickshaw |

Table : Percentage of potential customers and their respective income level

Table: Income level (amount in lac)

The bank is trying to plan different strategies to be implemented on different level of income holding people. The bank plans to employ its more resources on the sector which is thought to be as more profitable. As the people living at the upper class society rarely need any loan to purchase any car, the bank does not want to focus extremely on this section .Rather, it chooses the middle class people as the most attractive customer sector for their service. According to the bank projection, those people are not having the lump sum amount to purchase a car but they can afford to pay long-term installment amounts to repay their loan.

Employment: The higher employment in the society indicates that large number of people are getting sufficient amount of money to run their life smoothly and thus show much prospect for the bank’s service. The bank is thinking that, as the business environment in Bangladesh is looking prospectus and large national and foreign investment is taking place regularly, the employment rate will be higher in future. Hence, the bank officials are planning to expand their service in relation to the employment rate in the society.

Table : employment rate in the country

Effect of the pay scale: The service of the bank is also likely to be influenced by the government’s announcement of new pay scale. This will enable people to receive and hold more money to pay for the loan and also to pass for the loan initially.

Price range of the car | Initial down payment required to be paid to get the loan | Percentage of potential customers qualified for the loan before the new pay scale | Percentage of potential customers qualified for the loan after the new pay scale |

| 2000000 – above | 450000 – above | 5% | 5% |

| 1000000- 2000000 | 200000-450000 | 7.5% | 9% |

| 500000 -1000000 | 80000 -200000 | 30% | 35% |

| 200000 – 500000 | 50000 – 100000 | 25% | 30% |

Table : Positive effect of the proposed pay scale

Inflationary effects: The bank is also considering the inflationary effect of the economy. Because of the unexpected rise in inflation, the bank may assume substantial loss due to its unadjusted interest rate .It is likely in this society that, inflation has been rising continuously since last few years .And the projection of new pay scale has already caused some inflation in the economy.

Inflation in the economy

Here the bank wants to determine its potential market segmens for the auto loan service. In doing this most important job, the company wants to analysis the customers demography in different zone and in different income level. It also looks into the industry profile to see the trend of customer’s purchasing car by loan.

Customer’s Demography :The managers of the bank see that, people residing in Dhaka, Chittagong, and Sylhet have a growing interest in purchasing the car by taking out a loan from a commercial institutions. The demographic analysis of those zone show the following information.

In Dhaka male population aging between 30-45 have been taking car loan to buy a car. Most of these people are working at mid level position of private organization.

A significant percentage of these organization’s female executive are also interested in taking auto loan in order to contribute to their family. Following is the table showing the percentage of potential customers in different age group in the total country.

| Age range | %of male executive (expressed as % of total male executive) | % of female executive ( expressed as % of total female executives |

| 24 – 30 | 20% | 60% |

| 30-45 |

65%

35%45-above15%5%

Table: Customers in different age group

In the district of sylhet, the bank has found that, expatriate Bangladeshis are getting back to the country and purchasing here a car for their family. But the more important fact is that, although still a few percentage of these people are taking car by bank finance, the percentage is increasing rapidly through out the last few years. people under those category, invest their maximum amount in business and wants to spend a minimum,initially, in purchasing a car.

| Year | Expatriate people getting back to the country ( in approximate figures ) | No.of expatriates purchasing car for their own or family | No. of expatriates taking car by loan |

| 1998 | 2500 | 375 | 60 |

| 2000 | 3790 | 435 | 110 |

| 2002 | 1560 | 146 | 45 |

| 2004 | 2080 | 249 | 76 |

| Total | 9930 | 1205 | 291 |

Table: Record of expatriate people in purchasing car

Industry profile:This is the most important factor that the bank needs to determine. Fortunately, in Bangladesh this factor is favoring the companies marketing plan to a significant extent.

The industry analysis of recent past shows that ,people’s tendency to purchase car has been increasing significantly during last 5 years. Earlier, people choose to have a recondition car without any loan. But, people began to take the loan when the government imposed a huge amount of duty on recondition car for the preservation of environmental interest. The cost to buy a car has risen to above 6 lac which require a lot of customer to take out a loan.

Analysis of competitors’ Strategy

Competitors Performance : In this section the bank officials want to define their current competition both from banks and nonblank financial institutions.

In this analysis the bank finds that, since last few years, the institutions providing auto loan service have performed with significant success. Al-Falah officials are particularly interested in analyzing the performance of those institutions who have achieved some degree of specialization in this service. They are considering those firms as potential source of threat for their expected business. In this case they have found 3(Three) major Banks who deserve some special consideration as competitors in this business. The banks are- (1)Eastern bank ltd.(2)Dhaka bank ltd.(3)HSBC.

In the analysis of the performance of those particular institutions, Al-falah officials have found that all of those banks have started their auto loan service at a certain point of time.

The similar commencement period of auto loan service by these banks put strong evidence that the market for auto loan service in this country had emerged at a particular recent point of time. The sustainability of their business clearly shows that the market is still prevailing to a significant extent.

| Name of the bank | Commencement period for auto loan service | No. of branches & booths to provide the loan |

| Eastern Bank Ltd | 2002 | 12 |

| Dhaka Bank Ltd | 2002 | 9 |

| HSBC | 2003 | 3 |

Commencement period & no. of operative branches of the competitors

In analyzing the performance of the competitors the bank officials have also seen the amount of services that the institutions have provided to their customers at different years.

| Years | No. of auto loan provided by EBL | No of auto loan provided by Dhaka Bank | No. of auto loan provided by HSBC |

| 2001 | 105 | 75 | 45 |

| 2002 | 230 | 125 | 55 |

| 2003 | 240 | 200 | 70 |

| 2004 | 300 | 220 | 35 |

| Total | 875 | 520 | 205 |

Recent performance by the competitors

Competitors operation in the selected places: Earlier by analyzing the demography of customers from different locations, the Al-Falah bank has selected their possible places of business. Now In this case The company is interested to know about his competitor’s performance in these regions. Therefore following data containing the performance of those banks in the country are very vital to them.

Percentage of customers served by the customers

City | % of customers served by EBL | % of customers served by Dhaka Bank | % of customers served by HSBC |

Dhaka | 6% | 5% | 3% |

Chittagong | 6% | 6% | 2% |

Sylhet | 3% | 1% | 0% |

Total | 15% | 12% | 5% |

City wise performance of the banks

Analysis of the promotional activities of the competitors: For a successful marketing plan ,it’s a must to determine the way in which a particular firm will promote their product to the customers. In order to determine a efficient promotion tool, the bank evaluates the promotional campaign procedures that have been adopted by its competitors. Following table shows in brief the medium and type of promotions that have been undertaken by its competitors at different time.

| Name of the bank | Preferred Medium of promotion | details |

| EBL | Print & Electronic | National dailies, Television |

| Dhaka Bank | Print & Electronic | Bill-board, foot over bridge |

| HSBC | National dailies, Bill-board |

Problems and opportunities

In order to prepare its marketing plan , bank Al- Falah has conducted a comprehensive questionnaire survey on a representative sample of the potential customers. The sample included both group of customers – Those who have purchased an auto by taking loan and those who are likely to take the loan for an auto purchase. The bank officials made two separate form of questionnaire to be asked to the two distinct group of customers.

Questions for customers who have purchased car by loan:

1.How many years ago you have you purchased your auto?

2.What type of auto you have purchased?

3.From where you have taken the loan for purchasing your vehicle?

4.For how many years you took the loan?

5.What was the amount of down payment for your loan?

6.What rate of interest was charged on your borrowed amount?

8.What percentage of total amount you had to pay as origination fees?

9.Did you prepay the loan and if you did what was the consequences?

10.What was your level of satisfaction regarding the service that your bank provided to you while taking the loan.(The respondent was asked to express his level of satisfaction on a scale ranging from 1 to 5).

For the customers who have not yet bought a car by taking loan but are very much capable of having a car by taking a loan, the bank Al-Falah officials have prepared some critical questions to be included in the questionnaire form. The major questions include-

Prospective customers who are likely to take the loan:

1.What type of auto you would like to purchase?

2.What amount of money you want to borrow in purchasing the auto?

3.Are you satisfied with the service of the current auto loan provider or you are looking for some other institutions with some special features?

4.If not satisfied with the present service provider , what are the reasons of your dissatisfaction?

5.What beneficial features would you like to suggest to any auto loan service provider? (This is a subjective question where Al-Falah officials want to know about the customers, choice regarding the service.)

The Al-Falah officials are now in a strong position to determine both the short term and long term objectives for its business. The bank has first tried to settle its long range goal within the country context and then translated the goal into short term objectives which are to be implemented in the coming years. The objectives that the company has set forward are detailed as below-

Qualitative aspect: Here the bank officials want to disclose the reason why they are intending to start this business and where they want to go after a certain period of time. After considering all the analysis stated above , the think tank of the bank wants to conclude that Bangladesh is having a huge prospect for their auto loan service. Analyzing the market, they firmly believe that their auto loan service will get the similar success in Bangladesh as it does in their home country – Pakistan. Hence their primary long range objective is to capture the maximum possible market share in this country by outreaching its competitors in 5 years.

Quantitative aspect: Here the bank wants to translate its long term plan into achievable short term objectives which will be implemented in the very recent future. Analyzing the existing market from all possible dimensions, here the bank wants to determine some exact figures which will help them to design the organizational day to day activities. The bank has extracted the following expected figures for different variables-

Expected Market Share: In the analysis of the competitors’ performance, the bank has found that there remain a huge percentage of customers who have not yet been served by any of the competitors.Hence the major concentration for the Al-falah officials is to capture the maximum of hose customers. Following is their expectation in relation to the total market-

| Name of the banks | % of customers captured by the bank |

| EBL | 15% |

| Dhaka Bank | !2% |

| HSBC | 5% |

| Potential customers | 68% |

| Expected target for Bank Al-Falah | 50% (in next 5 years) |

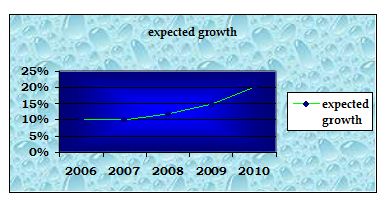

Expected growth: Analyzing the growth pattern followed by the competitor firms and analyzing their performance in their home country, Bank Al-Falah is expecting to attain 10% growth in their business in the first two years and 20%+ in the next 3 years.

Table: expected growth for bank Al-Falah

| Bank | Growth in first 2 years | Growth in later period |

| EBL | 8% | 16% |

| Dhaka Bank | 6% | 14% |

| HSBC | 4% | 12% |

| Bank AlFalah(expected) | 10% | 20% |

Action Programs

Given the past history, the economy, the market, competition, the bank officials now want to set the action programs to reach the goals they have set for this service.

This section will be a description of specific actions they plan to take during the coming years to ensure reaching the objectives they have set forward for their service in he earlier section. These would include Advertising and promotion, Location of the branches who will principally focus on the auto loan service, the procedures to be followed by the customers to acquire the loan, required down payment and interest rate to be charged.

Advertising and promotion: Although the bank officials has compared various method of promotional activities adopted by the competitors and thus determined the best promoter, the bank wants to bring some unique features in their promotion procedure. The major 3 banks have been continuing their promotion through newspaper and gigantic billboards. This is still an uncommon practice in Bangladesh to choose the electronic media as a medium of promotion for the auto loan service. Still then the Al-Falah officials are highly interested in launching large amount of advertise on electronic media. They are planning so because they have received huge amount of success in this way in their home country. By conducting an extensive market survey in Bangladesh they have found that electronic promotion, although a bit expensive , exert much more influence on the customers’ mind if they are aired in the right time and in the right sequence. Therefore, it has been very crucial for the bank to determine the right slot for their advertise in the right channel .

In this regard the bank has found the following data-

| programs | Viewers watching on Channel i | Viewers watching on NTV | Viewers watching on ATN Bangla |

| News | 40% | 25% | 15% |

| Dramma | 20% | 45% | 20% |

| Talk show | 50% | 10% | 20% |

Programs that are watched by the most no. of customers in the private electronic media.

The bank has also found that a significant % of population ,who fall in the prospective customer group for the auto loan service, are weak to the international channels. Hence, the bank has planned for signing contracts with those foreign media as well. The bank has planned to capture the following schedule in the prospective channels

| media | programs | Average time allocation per day in the first 6 month |

| espn | Cricket gold, highlights of Bangladesh’s cricket matches, Live cricket match of Bangladesh | 3 to 10 minutes depending on the popularity of the daily programs |

| Ten sports | Popular historical matches of Bangladesh, Pakistan & India | More than 5 minutes as the bank enjoy some rate benefit here |

| others | Other popular programs | Depends on the seasonal popularity |

Location of the branches who’ll focus on the service: Although as a bank , Bank Al-Falah will have to concentrate on other typical financial activities , its primary emphasis will be on the auto loan service. This is considered as the principal profit generating service of the bank. Therefore, its very crucial for the bank to determine the location of the branches from where it will operate the business.The bank is also considering the establishment of some small booths in some very special places like the big showroom premises to provide instant services to the customers.

By considering the early analysis of the cities of prospective customers, the bank Al-Falah has planned to set up two small booths initially in each prospective cities except Dhaka.However in Dhaka the bank is considering to establish more than one branch which will put emphasis on the service of auto loan besides doing other day to day activities. The place selection process here in this case is influenced by the auto loan service to a less extent than it is influenced by other variables. The places which are generally suitable for establishing branches for banks like Motijheel, Dilkusha, Gulshan, Mohakhali, Karwanbazar, Dhanmondi, etc are also considered as the most suitable places for providing the bank loan. The bank has already started its operation in its Head office on the Rajuk Avenue of Motijheel C/A. Primarily the officials are planning to inaugurate 2 more branches at Dhanmondi and gulshan where the tendency of purchasing auto among people is higher.

Besides establishing the branches, the bank is also considering the establishment of some booths in some crucial places in order to provide auto loan service instantly to the customers. To establish the booths the bank has chosen some places where there are more than 10 showrooms within a distance of 2 km.The bank has found 2 such places at Purana paltan and Dhanmondi Sat Masjid Road.The bank has also planned to set up another booth in Mohakhali where there are grand showrooms of some giant companies of the world.

So, the auto loan service of Bank Al-Falah will be operated from the following locations-

| Branches & booths | Locations |

| Head office | Rajuk Avenue |

| Branch-1 | Dhanmondi |

| Branch-2 | Gulshan |

| Booth-1 | Purana paltan |

| Booth-2 | Dhanmondi Sat Masjid Road |

| Booth-3 | Mohakhali |

| Booth-4 | Sylhet |

| Booth-5 | Chittagong |

Procedures to be followed by the customers to acquire the loan: The Bank Al-Falah is committed to serve the customers in a way that is most convenient to the customers. Hence the bank requires the customers to follow the least amount of formalities. The bank is trying to structure its service in a way so that customers needs to do nothing except making a phone call to the bank officials. The bank has already purchased 20 telephones which will act as the hot line for the customers.

Required down payment and interest rate to be charged: After the completion of the survey on the prospective customers, the bank has come to know that customers at present are little dissatisfied with the amount of down payment required by the existing banks. Hence, the bank has determined to demand a lower amount of down payment from the customers. They will demand 25% of the borrowed amount as the down payment instead of 30% of the competitors.

In disclosing the interest rate, the bank officials want to stand on their famous principle of expressing real interest rate which includes all types of cost of the loan for the borrower. Any additional service charge, origination fees are subject to be included in the expressed interest rate. In Pakistan, their add on car loan has been revolutionary because of its expression “ 9.5% means 9.5%”