This report focuses on the difference between Islamic banking and conventional banking. There are several Islamic banks in Bangladesh. For specific and detailed analysis and comparison for this report I choose EXIM bank Bangladesh LTD which was a conventional bank at past now become an Islamic bank.

The main objective of this report is to find the difference between Islamic banking and conventional banking. I tried to find out what are the difference between an Islamic bank and a conventional bank. What are the different approach /terminology they follow. I also tries know about the Islamic shariah terminology which is backbone of the Islamic economics. The secondary objective is to know how EXIM bank Bangladesh LTD operating their daily work.

Methodology:

As three months internship is mandatory for competition of my BBA program, I work for EXIM bank as a intern. I collect all the information from my supervisors in my three months of internship. At first I went to Mr. Sheik Ishreuq Osman, he introduces me to the bank and their stuff and tell me to work in account opening section. I work at account opening desk under Mr. Monir, he gives me clear idea of necessary papers and rules to open any sort of account. Then I worked at bills and clearing Section under keya madam and sharmin madam. There I came to know about the demand draft, clearing of cheques. Then I work in investment section under Mr Juwel and Mr. Sayeed, they actually show me the actual difference of Islamic banking and conventional banking. They also show me how Islamic banks investments are different from conventional bank. They give me clear idea of profit and interest. They also introduce me to their products. Then I work in foreign remittance section under Shapon sir. He showed me how actually maintain the letter of credit, foreign customers etc. As cash section is very sensitive section to work that’s why intern people in cash section is beyond banks policy. That’s why I did not got the chance to work there. But Mr. shopon also give me a brief of cash section. In this way we collect all the necessary information needed of my internship report.

Islamic banking:

Islamic banking is guided by Islamic law which is known as Shariah principles. In particular, Islamic law prohibits the collection and payment of interest, which is known as RIBA. Generally, Islamic law also prohibits trading in financial risk (which is seen as a form of gambling) that are considered unlawful, or Haraam.

The Islamic capitalism were developed between the eighth and twelfth centuries. Gold dinar was the base of monetary system of that economy. Mirza Basheer-ud-Din Mahmood Ahmad is known as the father of modern Islamic economics. he describe it in detail in his books Nizame Nau in 1942. In his book he proposed a banking system based on “Mudarabah” which is known as profit and loss sharing. Bank Melli Iran is the largest Islamic bank of the world.

Overview EXIM bank Bangladesh ltd:

The full form EXIM bank is Export Import Bank of Bangladesh Limited. The Bank started commercial banking operations effective from August 03, 1999 as a conventional bank. Later it converted its Banking Operations into Islamic Banking based on Islamic Shariah from traditional banking operation in July 01, 2004 after obtaining approval from Bangladesh Bank. They have a strong shariah board to maintain the proper Islamic banking system which consist 11 learned muftis, reputed economist and bankers of the country lead by Professor Maulana Mohammad Salah Uddin. Late Mr. Shahjahan Kabir was the founder chairman of this bank.

Export Import Bank of Bangladesh Limited is a public listed scheduled bank categorized in private sector and established under the ambit of Bank Companies Act, 1991 and Incorporated as a public limited company under the Companies Act, 1994 on June 02. Now it has 67 branches all over Bangladesh. Soon they are planning to open 5 more branches in Comilla, Coxsbazar, Chittagong and Dhaka.

During the span of time the Bank has been widely acclaimed by the business community, from small entrepreneurs to large traders and industrial conglomerates, including the top rated corporate borrowers for forward- looking business outlook and innovative financing solutions. In 30th June 2009, EXIM bank open exchange house in London, United Kingdom in order to deliver remittance services to the NRB’s living and working there. It is the first private bank to do that. They use the world renowned core banking software TEMENOS T24 to provide best IT

service to their valued customers.

With a few of the Company’s activities and program on the basis of Islamic Shariah, within this period of time it has been able to create an image of responsibility for itself and has earned significant reputation in the country’s banking sector. Within an operative period as eight years, the bank has arrived at a strong financial and business position by expanding its market share compared to its contemporaries and to some extent to the 2nd even 1st generation banks of private sector.

Shariah Board

The Board of directors has formed a Shariah Supervisory Board for the Bank. Their duty is to monitor the entire Bank’s transactional procedures, & assuring its Shariah compliancy. This board consists of the following members headed by the chairman The tasks of the Shariah supervisor in summary is replying to queries of the Bank’s administration, staff members, shareholders, depositors, & customers, follow up with the Shariah auditors and provide them with guidance, submitting reports & remarks to the Fatwa & Shariah Supervision Board and the administration, participating in the Bank’s training programs, participating in the supervision over the AlIqtisad AlIslami magazine, & handling the duty of being the General Secretary of the Board.

Profit VS interest:

To know Islamic banking at first we have to realize the difference between profit and interest. Where conventional bank gives certain percentage of interest to its depositors there Islamic bank share certain percentage of its profit to its depositors. Interest is known as RIBA which is completely forbidden (Haraam) is Islamic terminology. Riba means access increase or addition.

According to Islamic Shariah terminology, riba is any excess compensation without due consideration of time value of money. In our country interest is set at the beginning of the year by conventional bank and it is fixed if any economic disaster does not happened. But on the other hand profit is completely different from the interest. Bank invests its depositor’s money as their fund to a business and earns profit, than share some percentage of this earned profit to the depositors. Profit is also set at the beginning of the years but it is not fixed as interest is. It may change if bank earn more and less. It depends on bank efficiency. Islamic bank in Bangladesh also give the percentage of their profit at the beginning of the year as per as Bangladesh bank rules. But sometimes it changes its percentage due to their profit making efficiency. This is actual difference between the profit and interest.

EXIM bank divides their whole work into 2 parts. They are:

- General banking

- Investment

General Banking:

Bangladesh is one of the less development countries. So the economic development of the country depends largely on the activity of commercial banks. So I need to emphasis whether these commercial banks are effectively and honestly performing their functions, assign their duties, and responsibilities.

In this respect I need to know the general banking function of those Banks as well as the EXIM Bank Limited, is to provide the general banking service. The general banking department does the most important and basic works of the bank. All other department is linked with this department. It also pays a vital role in deposit mobilization

BANK General Banking Investment of the branch. EXIM Bank provides different types of accounts, locker facilities and special types of saving scheme under general banking. For proper functioning and excellent customer service this department is divided into various sections namely as follows:

1. Deposit Section.

2. Account Opening Section.

3. Cash Section.

4. Bills and Clearing Section.

5. Remittance Section.

6. FDR Section.

7. Accounts Section.

MUDARABA savings deposits:

The main feature of this account is depositors can deposit any amount of their deposits as much time they wanted to do but in terms withdrawn there is some barriers. No depositor can withdraw more than 5 lacs in a week or more than twice in a day. Bank provides small amount of profit to this account. Bank has the rights to use the deposits of this account. This is specially designed for the mass people. Normally EXIM bank opens this account not only in the name of individual but also in the name of any organization. Bank has the rights close any account if it has zero balance or inactive more than 2 years.

MUDARABA monthly savings scheme:

Any adult person having sound mind can open one or more account in the same name at the same branch. The maturity of this account is 5, 8, 10, and12 years. 80% loan can be taken after completion one year of maturity. Deposit must be give within the 1st ten day of the month. Charge is taken by bank for late submission of deposit.

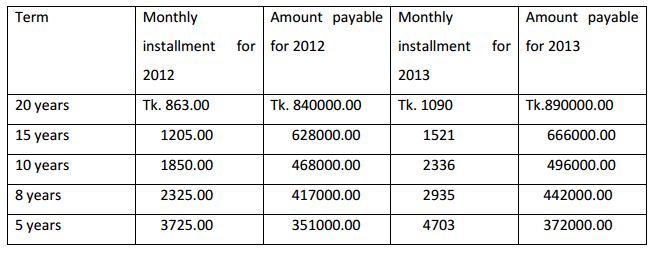

MUDARABA Hajj Scheme:

It is specially designed for hajj. It is actually same as MUDARABA monthly savings scheme but there is a bit difference. Here EXIM bank ask his client when they want to do their hajj. Than the assume the cost of hajj for that particular year and than they set the installment. Suppose two clients want to do their hajj in 2012 and 2013 respectively. Than they have to pay the installment like below:

Education Savings Scheme:

The most gratifying experience for parents are proper education of their children. Educational expense is rapidly increasing and therefore appropriate planning needs to be done by all parents. EXIM Bank offers customer ‘Education Savings Scheme’ to assist customer in financial planning well ahead in time for customers children’s higher education. Deposit of Tk. 25,000/- and multiples there of at a time will be accepted under the scheme. The instrument shall be issued for 7 years, 10 years, 15 years, 20 years term. The deposit is payable at maturity with benefit either in lumpsum or on monthly basis as education allowance for 6 (six) years starting after the completion of respective term.

Time Deposits:

A deposit which is payable at a fixed date or after a period of notice is a time deposit. EXIM Bank accepts time deposits through fixed deposit receipt (FDR), short time deposit (STD) etc. While accepting these deposits, a contract is executed between the bank and the customer. This contract will be a valid one only when both the parties are competent to enter into contracts. As account initiates the fundamental relationship and since the Banker has to deal with different kinds of persons with different legal status, EXIM Bank officials remain very much careful about the competency of the customer. In term of term deposits their product name is:

- MUDARABA term deposit receipt account

- MUDARABA super savings scheme

- MUDARABA multiplus savings scheme

- MUDARABA monthly income scheme

MUDARABA term deposit receipt account:

The main feature of this account is depositor can deposit and withdrawn only for one time in this account. The profit rate is much higher in terms of this account which is 12.5 %( as per as Bangladesh Bank order). Any adult person (jointly or individually) having at least tk. 10000 can open this account. One or more account can be opened in the same name at the same branch. Depositor must have the savings account to open this account in EXIM bank. Depositor can take 80% of their deposits as a loan and pay it in installments or whole at a time.

Difference:

In conventional banking system it is known as fixed deposits. As like other accounts conventional bank gives interest to this account. To open this account in conventional bank one individual needs at least taka 50000. There is no need for saving account or current account to open this kind of account in conventional banking system.

MUDARABA super savings scheme:

Any adult person (jointly or individually) having at least tk. 50000 or multiple of its can open this account. One or more account can be opened in the same name at the same branch. Depositor must have the savings account to open this account in EXIM bank. Tenure of this account is six years. The main feature of this account is bank will double or close to double its depositors money in maturity of this account. Depositor can take 80% of their deposits as a loan and pay it in installments or whole at a time.

Difference

It is known as double scheme in conventional banks. Where EXIM bank do not ensure that they will doubled their depositors money there conventional bank ensure their customer to double their money. As the interest rate is fixed that’s why conventional bank can do that.

MUDARABA multiplus savings scheme:

Any adult person (jointly or individually) having at least tk. 50000 or multiple of its can open this account. One or more account can be opened in the same name at the same branch. Depositor must have the savings account to open this account in EXIM bank. Tenure of this account is ten years. The main feature of this account is bank will triple or close to triple his depositors money in maturity of this account. Depositor can take 80% of their deposits as a loan and pay it installments or whole at a time.

Difference

It is known as triple scheme in conventional banks. Where EXIM bank do not ensure that they will triple their depositors money there conventional bank ensure their customer to triple their money. As the interest rate is fixed that’s why conventional bank can do that.

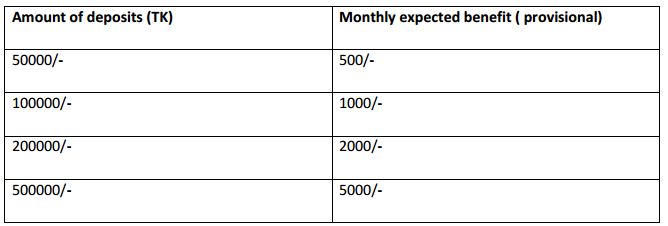

MUDARABA monthly income scheme:

Exim bank designed this product for those who has a lots of idol money or need monthly fixed income. The main feature of this account, here bank promise to give same amount of profit every month to its customers. Any adult person (jointly or individually) having at least TK.50000 can open this account one or more account can be open in one name. Monthly benefit of different amount of this account is given below:

Difference

It is known as monthly income scheme in conventional banks. Where in EXIM bank monthly benefit is not fixed there conventional bank ensure their customer to give certain amount of money every month against their customers deposit. As the interest rate is fixed that’s why conventional bank can do that.

Cash Section:

The cash section of EXIM Bank deals with all types of negotiable instrument, cash and other instruments treated as sensitive section of the bank. It includes the vault that is used as the beyond this time; the excess cash is then transferred to Bangladesh Bank. This section perform the following functions:

Cash Packing:

After the banking hour cash is packed according to the denomination. Notes are counted and packed in bundles and stamped with initial.

Allocation of Currency:

Before starting the banking hour all tellers give requisition of money through ‘Teller cash proof sheet’. The head teller writes the number of the packet denomination wise in ‘Reserve sheet’ at the end of the day; all the notes remained are recorded in the sheet.

Bills and clearing section:

For safety and security in financial transaction people use financial instruments like DD, PO, Cheque etc. Commercial Banks duty is to collect these financial instruments on behalf of their customer. This process that the Banks use is known as clearing and collection. The mail function of this section is to collect instruments on behalf of the customers through Bangladesh Bank, clearing house, outward bills for collection (OBC), inward bills for collection (IBC).

Upon the receipts of the instruments this section examines the following things:

- Whether the paying bank within the Dhaka city.

- Whether the paying bank outside the Dhaka city.

- Whether the paying bank is their own bank.

Payment Order (PO):

It is process of money transfer from payer to payee within a certain clearing area through banking channel. A person can purchase payment order in different modes such as pay order by cash, pay order by cheque.

EXIM Bank charges different amount of commission on the basis of payment order amount. The bank charges for pay order are given in the following chart:

Demand Draft (DD):

It is an instrument containing an unconditional order of one bank office to pay a certain amount of money to the named person or order the amount therein n demand. DD is very much popular instrument for remitting money from one corner of money to another. Commission for DD is 0.15% of the principal amount.

Foreign Exchange division

One of the largest businesses carried out by the commercial bank is foreign trading. The trade among various countries falls for close link between the parties dealing in trade. The situation calls for expertise in the field of foreign operations. The bank, which provides such operation, is referred to as rending international banking operation. Mainly transactions with overseas countries are respects of import; export and foreign remittance come under the preview of foreign exchange transactions. International trade demands a flow of goods from seller to buyer and of payment from buyer to seller. In this case the bank plays a vital role to bridge between the buyer and seller.

Foreign exchange department of EXIM Bank is one of the most important departments of all departments. This department handles various types of activities by three separate sections:

1. Import section.

2. Export section.

3. Foreign remittance section.

Import Section:

The function of this section is mainly to deal with various components such as :

- Letter of credit

- Payment against document (PAD)

- Payment against trust receipt (PTR)

- Loan against imported merchandise (LIM).

Export section:

The function of this section is mainly to deal with various components such as:

- Export L C

- Loan against exported merchandise

Foreign remittance section:

This section deals with foreign currency. This section actually sells and buys the foreign currency against the taka. EXIM Bank has authorized dealership. Different branches of EXIM Bank such as Motijheel Branch, Panthapath, Malibagh Branch etc. are providing the foreign remittance services to its customers. There are two types of remittance.

- Inward remittance

- Outward remittance

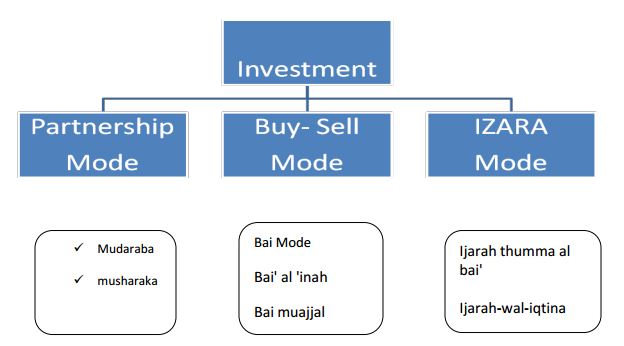

Investment section:

This section is also known as credit section. It is an essential part of any banks revenue. As EXIM bank is an Islamic bank they do not change any type of interest in terms of their loan customer. They try to follow the Islamic rule which is known shariah in islam. Now I m going to give a brief idea about their credit system/ loan system.

EXIM bank Bangladesh LTD. actually divided their loan product into 3 parts. This is known as follow:

- Partnership mode

- Buy- sell mode

- Izara mode

There are certain terms under these modes. This is given in the next graph below:

Partnership mode:

In this mode EXIM bank tries to do business in partnership with their clients. There are 2 types of product offered by EXIM bank in partnership mode. They are:

- Mudabara

- Musharaka

Mudabara:

Mudabara loan system means profit sharing and loss bearing. In this mode EXIM bank give loan to its client for business and take share of the profit gain by their client. For example a company takes loan for its business from EXIM bank. Bank will give them a certain time to make profit. After making profit bank will take certain percentage of its profit as a feedback of their loan. If the company fails to gain profit bank will give them more time to regain it.

If the company fails again then the bank will share the companies’ loss as the agreement of Mudaraba loan system. Since 2006 EXIM bank stopped the Mudaraba loan system as they have bad experience over it. After becoming Islamic bank from conventional bank they had gave loan in this system to 25 companies. Only 2 of them show small amount of profit. Others show loss to their projects. It is big loss for EXIM bank. That’s why they stopped it later.

Musharaka:

This is actually joint venture system. In this loan system bank made an agreement of joint venture with their client, do businesses, and share profit and loss. Suppose a company need a financer of its project. If they go to EXIM bank and then bank approve the project and invest in it. Here bank and its client becomes partner to a project. Bank and its client will share all its profit and loss as ratio. This is often used in investment projects, letters of credit, and the purchase or real estate or property. Many real estate companies are taking this sort of loan to avoid the interest which is prohibited (haraam) in Islam.

Buy- Sell mode:

In this mode bank actually become the middle man to its client. Here bank buys the required product ordered by its client and sells it to its client in higher price. There are 3 products in terms bye- sell mode. They are:

- Bai salam.

- Bai’ al ‘inah

- Bai muajjal

Bai salam:

Bai salam means a contract in which advance payment is made for goods to be delivered later on. The seller undertakes to supply some specific goods to the buyer at a future date in exchange of an advance price fully paid at the time of contract. Here client negotiate with bank to made advance payment to its seller of his required product.. Exim bank sells it to his client in higher price. Various garments use these terms to operate their business.

Bai’ al ‘inah:

Bai’ al inah is a financing facility with the underlying buy and sell transactions between the bank and the customer. The bank buys an asset from the customer on spot basis. The price paid by the bank constitutes the disbursement under the facility. Subsequently the asset is sold to the customer on a deferred-payment basis and the price is payable in installments. Suppose I had a land and I need loan against it. Exim bank will buy the land from me and give me the money. I will pay a higher price for my land and buy it back from the bank but this time I will buy my land in installments. In the mean time I can use my land as like as I wanted to use it.

Bai muajjal:

Bai means bank earns profit margin and muajjal means credit sale. It is a contract in which to pay the price of the commodity at a future date in a lump sum or in installments. Suppose here a client choose a product from a shop. Then apply for loan in EXIM bank I bank thinks that everything is ok than they will buy the desired product of that customer from that particular shop and sell that product to that customer in higher price. The client will receive the product and pay the money in installments. Basically EXIM bank use term of loan in term of car loan, consumer loan etc.

IZARA mode:

Ijar means lease, rent and wage. Here bank sale the benefit of use a product or service to its customers on a fixed price and installment payments. Under this concept, the Bank makes available the use of service of asset/equipments such as plant, office automation, motor vehicle for a fixed period and price to its customers. There are 2types of product in Izara mode in EXIM bank. They are:

- Ijarah thumma al bai

- Ijarah-wal-iqtina

Ijarah thumma al bai:

It is known as hire purchase client enterr into contracts with bank to form a complete lease/ buyback transaction. The first contract is an Ijarah that outlines the terms for leasing or renting over a fixed period, and the second contract is a Bai that triggers a sale or purchase once the term of the Ijarah is complete. For example, in a car financing facility, a customer enters into the first contract and leases the car from the bank at an agreed amount over a specific period. When the lease period expires, the second contract comes into effect, which enables the customer to purchase the car at an agreed to price.

Ijarah-wal-iqtina:

A contract under which EXIM bank provide equipment, building, or other assets to the client. In return EXIM bank receives rent from its client. Here ownership of the product belongs to the bank. At the end of the lease period ownership of the product will be transferred to the client. And client will pay the agreed amount in the agreement to the bank.

Conclusion:

Now a day’s Islamic banking is becoming more popular day by day as more people want to lead their life in terms of Islamic rule. Exim bank is doing excellent job in terms of Islamic banking system. But in my point of view people do not have the clear idea about the difference between interest and profit as banks do not promote this in their marketing strategy. As Islamic banking becoming more popular to the people of Muslim countries, many multinational bank like HSBC, Standard chartered bank now a day’s open Islamic banking section (like AMANAH) in their bank. Even many conventional banks in Bangladesh have already open Islamic banking section. It is become new marketing strategy for banks to attract new customer.

EXIM Bank is playing a leading role in economic development of the country along with maintaining standard level of services. It understands the needs of the customers and thus it understands the needs of the nation. EXIM bank and its contribution to the economy of Bangladesh along with high level of corporate social responsibility are providing it a way to move forward in faster than other banks in the country.