Introduction

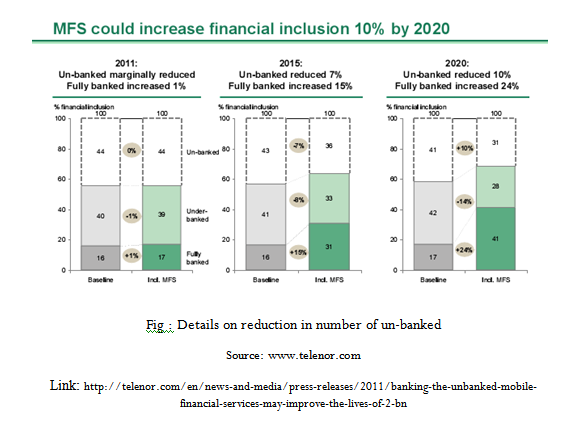

Bangladesh currently has a 55 percent financial inclusion rate. This means that in Bangladesh today, 45 percent of adults have no access to formal financial services. Among the financially included, 16 percent are fully banked, meaning they are able to take advantage of a full range of financial services (including savings, insurance, credits and others); and 39 percent are under banked, with only basic access, such as a savings account. Bangladesh’s inclusion rate, which is extremely high given its current level of economic development, is driven primarily by microfinance, and the percentage of active users of the full range of financial services is probably lower. Furthermore, the penetration of key services—especially insurance—remains quite low, and MFS is nearly nonexistent.

There is strong evidence that financial inclusion—the delivery of affordable banking services to a population—is associated with the attainment of a nation’s crucial economic and social goals. Providing financial services draws credit into the banking system, leading eventually to GDP growth. It increases the formation of domestic capital, spurring entrepreneurship. And it develops the depth of a nation’s private sector, which in turn builds new jobs. These financial developments reduce a nation’s overall income inequality, increase income growth among the lowest paid quintile of the population and accelerate poverty alleviation.

From a social perspective, financial inclusion gives workers the means to make remittances, a key goal in promoting the reduction of inequality. It provides them with a safe way to save their income, increasing the resiliency of the poor to unexpected economic or political shocks and food shortages. And it gives the population access to insurance—a basic safety net for emergencies such as accidents or crop and weather catastrophes—making it possible for families to keep their children in school through difficult times.

Addressing the Un-banked

Mobile financial services lower some of the key barriers to banking inclusion in Bangladesh by reducing start-up costs and service prices, as well as by delivering the banking products that meet the particular needs of Bangladeshis. Widespread network coverage allows for around-the-clock account access and eliminates travel time and costs. Furthermore, mobile banking gives customers access to additional products, such as credit and insurance policies, thereby breaking the chicken-and-the-egg cycle and providing Bangladesh’s population with a much-needed opportunity to build credit histories.

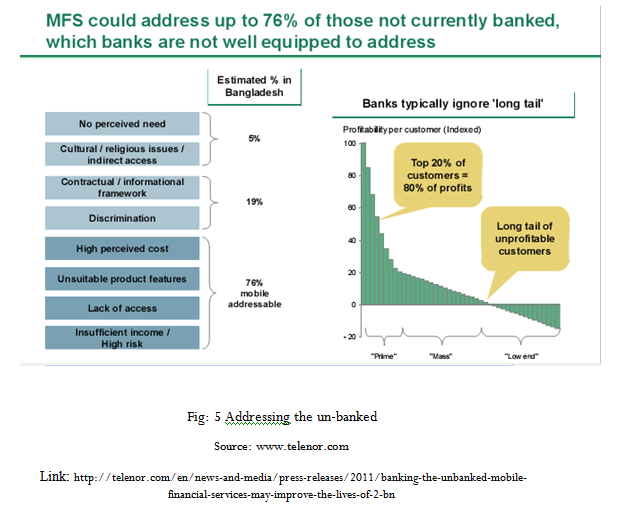

To consider who might benefit from the distribution of MFS, we broke down the Un-banked population into several categories, leveraging surveys of the unbanked in emerging markets. Among those Bangladeshis who do not use formal financial services in any way, an estimated 5 percent are in that position of their own accord—either for cultural or religious reasons, or because they perceive that they have no need for banking services. The remaining 95 percent are excluded involuntarily. This could be, for example, because they face (real or perceived) discrimination or because they cannot get past the information and contractual requirements needed to access banking services.

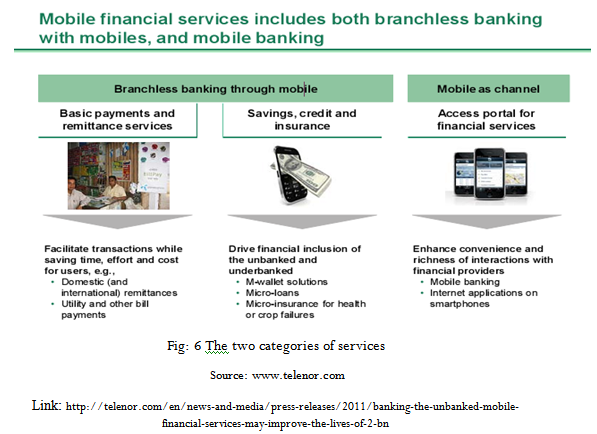

It is estimated that a large proportion, up to 76 percent, are unbanked because financial institutions see their low income as too great of a risk, or because, for these Bangladeshis, the cost of services is too high and the product features that are offered are not sufficiently useful for them. This is the group that MFS is well suited to address. “Mobile financial services” is defined here to include two broad categories of services: branchless banking via mobile phones and mobile banking as a channel for financial services. With branchless banking, users can take advantage of services allowing them to make basic payments—utilities and other bills—and domestic and international remittances. These transactions become fast, easy, and cost-effective through MFS. Users can also participate in savings, credit, and insurance programs. Such services drive the financial inclusion of the unbanked through m-wallet solutions, micro-loans, and micro health and crop-failure insurance.

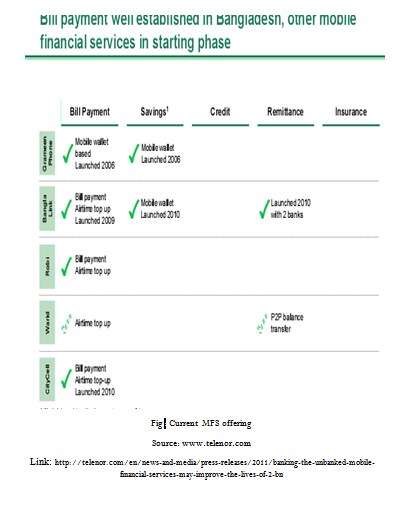

The other side of MFS provides existing banking customers with a highly accessible portal for financial services, increasing convenience. The frequency of interactions between customers and financial providers is enhanced through this mobile portal, allowing for convenient mobile banking and the use of Internet applications on smart phones. Mobile bill payment is already established in Bangladesh, but other types of MFS, including savings, credit, remittance, and insurance products, are just in the starting phase or have yet to begin. Bangladesh, thus, has the potential for great influence by MFS, with a large population in need of secure, convenient, and affordable banking services.

Adoption

For mobile financial services to gain a strong footing in Bangladesh and develop a successful, lasting ecosystem, a number of elements have to be in place. These include regulations, business model planning, distribution networks, and consumer education. Implementing and enforcing regulations of mobile services is a key step in the inclusion process. These regulations must include the structure of the MFS framework for non-banks, guidelines for the use of MFS agents, and a coordinated government initiative. In addition, the establishment of a workable MFS business model will be necessary. Since both banks and telecoms will offer mobile financial services, there must be cooperation and transparency between these different types of players. Profit sharing and pricing mechanisms must also be built into the MFS business model. A stable, reliable distribution network has to take hold before MFS can be successful in Bangladesh. This includes how MFS agents are used, trained, and certified. A strong network must also be set up to manage liquidity, or to guarantee the security and flow of funds. Finally, consumer education is of crucial importance in guiding the success of mobile financial services. Consumers will have to be taught the advantages of becoming banked and begin to understand the importance of moving away from a cash-based economy. This process will also include attempts at establishing trust in MFS as a reliable and useful system, and will likely require the collaboration of all members of the ecosystem, including the regulators.

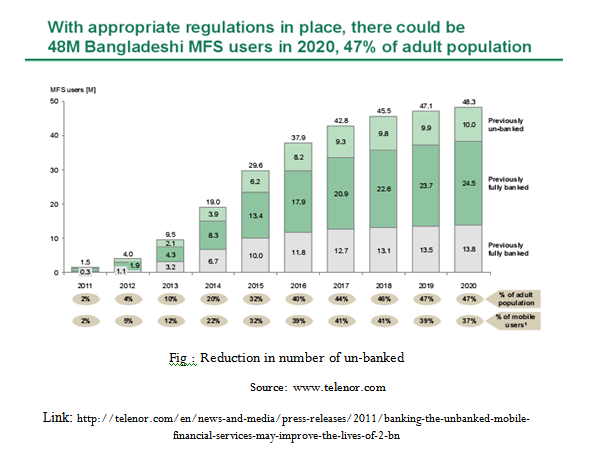

Given that this sort of supportive environment is in place, the potential number of MFS users has been projected until 2020. For more details on the analysis please refer to the appendix. By 2020, 47 percent of all adult Bangladeshis—from the un-banked to the fully banked—could be MFS users, thereby reducing the number of un-banked by 10 percent. While the current financial inclusion rate of 55 percent should gradually increase to 59 percent by 2020, driven by overall development and economic growth, the additional 10 percent inclusion from MFS means financial inclusion in the country could reach 69 percent by that year.

From MFS to Traditional Institutions

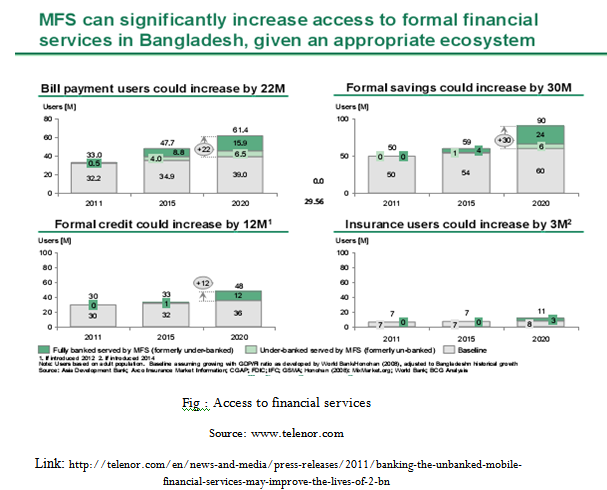

With wide MFS adoption, the number of people with formal savings accounts would probably increase by 30 million by 2020. In addition, 22 million can be added to the number of people using formal bill payment products, significantly increasing total transaction volume. As Bangladeshis adopt mobile financial services, they will also begin to gain access to a greater range of formal financial services. For example, customer relationships will deepen through MFS, with providers gleaning more information about who their customers are and where they live, as well as deeper knowledge of transactional patterns, all of which will begin the basis for building customer credit histories. Given wide MFS distribution beginning in 2012, the number of formal credit service users could increase by 12 million by 2020.

Further, with MFS insurance introduced in 2014, the number of formally insured Bangladeshis could increase by 3 million by 2020. Currently, the limited rural distribution of insurance products makes for high transaction costs. Bangladesh’s poor are also inhibited from gaining access to insurance as a result of their lack of credit history and their general classification as high-risk customers. Many are also without documentation, which makes claim verification difficult. Mobile distribution of insurance policies would introduce products better suited to the needs and payment capacities of a considerably wider range of customers. These products would include health insurance, particularly micro-insurance; crop insurance; and rainfall and weather insurance.

Remittance systems are another key beneficial service that will be much more accessible through MFS and will eventually lead to an increase in formal users. Mobile remittances can be made through a fast, secure channel that would be available to all, with fees significantly lower than the 5 percent to 12 percent of transaction amounts that informal channels often charge. These services are designed to be instant, safe, and secure, which should draw users away from the informal channels many use today. This will likely include those unbanked who do not trust traditional banks, but who would find the brand names of mobile providers appealing. MFS remittance services should lead to an increase of 39 percent in the number of formal users by 2020.

Benefits: From the Individual to Society

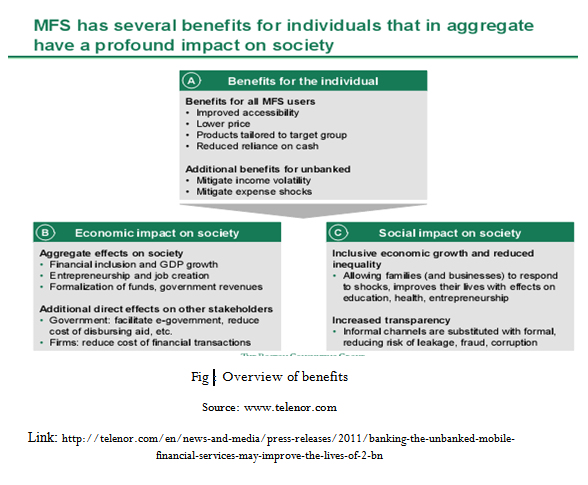

Mobile financial services can offer all Bangladeshis certain benefits. Banking becomes much more accessible and affordable. Products are tailored to customers and are thus more relevant and meaningful. And MFS leads overall to a reduced reliance on cash. In addition, those MFS adopters who were previously unbanked will benefit from an enhanced ability to mitigate income volatility and expense shocks. All of these advantages accrued by the individual will ripple outward and benefit society economically and socially. Economic benefits include the increase in financial inclusion, which leads to GDP growth; the sparking of entrepreneurship and job creation; and the formalization of funds and government revenues. Other stakeholders will feel direct economic effects as well, such as government, through the facilitation of e-governing and the reduction in the cost of aid disbursement; and private firms, through lower costs of financial transactions.

All of these advantages accrued by the individual will ripple outward and benefit society economically and socially. Economic benefits include the increase in financial inclusion, which leads to GDP growth; the sparking of entrepreneurship and job creation; and the formalization of funds and government revenues. Other stakeholders will feel direct economic effects as well, such as government, through the facilitation of e-governing and the reduction in the cost of aid disbursement; and private firms, through lower costs of financial transactions.

Socially, the impact of MFS will be substantial as well. Inclusion, which leads to economic growth, will also lead to an overall reduction in inequality. Families and small businesses will be better able to respond to shocks, and because of the effects MFS will have on education, health, and entrepreneurship, Bangladeshis will have the opportunity to lead improved lives. Informal channels of financial services—with the inherent risks of leakage, fraud, and corruption—will be reduced, and instead Bangladeshis can begin to make use of the formal, more transparent channels of mobile financial services.

Benefits for the Individual

The practical and attractive features of mobile financial services are a strong draw for individual customers. The accessibility of MFS, for instance, has meaningful appeal. Banking no longer requires the time and cost of travel, and users do not even need a computer to manage accounts and seek information about products. They can conduct transactions of any amount at any time of the day or night from anywhere. And those transactions—such as purchases, personal remittances, and business operations—are completed instantly and at a relatively low cost.

Another key benefit to the individual is how MFS lets users spend less of their time overcoming bureaucratic obstacles. Tailored features, as well as flexible repayment plans and reduced balance requirements, give the previously unbanked the ability to open accounts and gain access to products tailored to their own needs. It also puts them in a position to build up credit histories, an important stepping-stone in individual economic improvement.

Mobile banking reduces its customers’ reliance on cash, a feature that brings increased convenience and savings potential into Bangladeshis’ lives. Cash becomes unnecessary for transferring or receiving money, which reduces the inherent risks of cash handling, such as loss, theft, or fraud. With middlemen squeezed out of the transaction equation as a result of MFS, customers will experience increased transparency. All of these benefits give consumers good reason to adopt mobile banking.

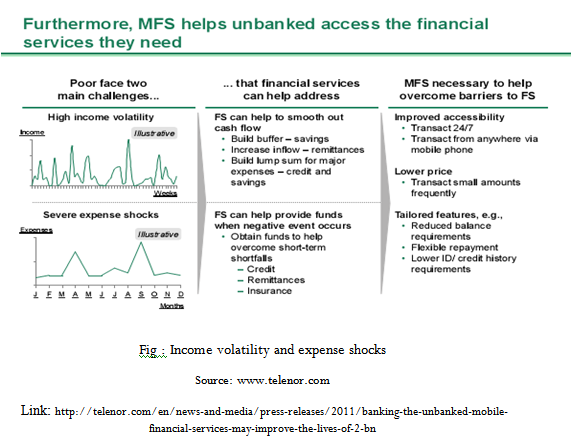

Bangladesh’s poor face two primary challenges that financial services can help address, first, they tend to live with a high degree of income volatility. Financial services can help smooth out their cash flow in several ways: by building a buffer through savings; by increasing inflow through remittances; and by accumulating lump sums of money—through savings and credit—that can be used to manage major expenses as they come up.

The poor also suffer from the severe expense shocks that occur now and then in their lives. Again, access to financial services would help. Customers can obtain funds to help overcome temporary shortfalls through credit, remittances, and insurance, all of which is out of reach for the un-banked, and has served to keep the poor from improving their economic situation.

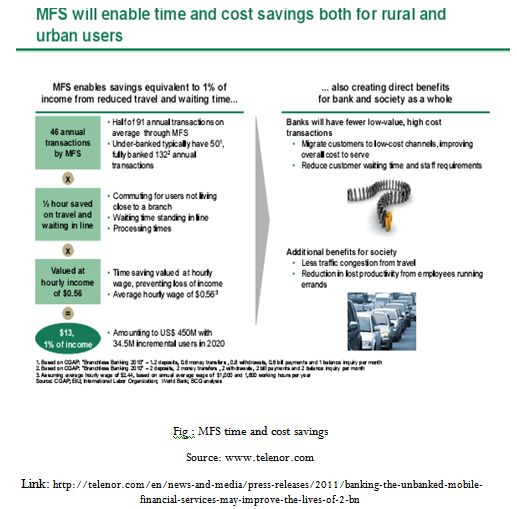

For urban Bangladeshis, MFS could produce a savings equivalent of 1 percent of income as a result of reduced travel and waiting time—including the commuting time for users who don’t live close to a branch, the waiting time involved when standing in long lines, and the transaction processing times. The savings will be significantly higher for rural users, who have to travel farther to get to banks. As MFS does away with these inconveniences, both banks and communities will feel the benefits. Banks will have fewer low-value, high-cost transactions to contend with as customers migrate to cheaper channels—improving the overall cost to serve. The reduction in customer waiting times translates to reduced requirements for bank staff, too. From an even broader perspective, MFS could contribute to a decrease in traffic congestion in urban areas and a reduction in the lost productivity that occurs when workers have to run inconvenient errands.

Economic Impact on Society

Strong evidence indicates that growing financial inclusion increases a nation’s GDP. As entrepreneurs with business ideas gain access to credit, economic activity grows, and new businesses and jobs mean a more productive society. In addition, there is an accounting benefit from the formalization of savings within the banking system, as this will power further credit creation, increasing investments. With mobile financial services adoption, Bangladesh could see a GDP increase of US$6 billion, or 2 percent, by 2020.

New Job Creation

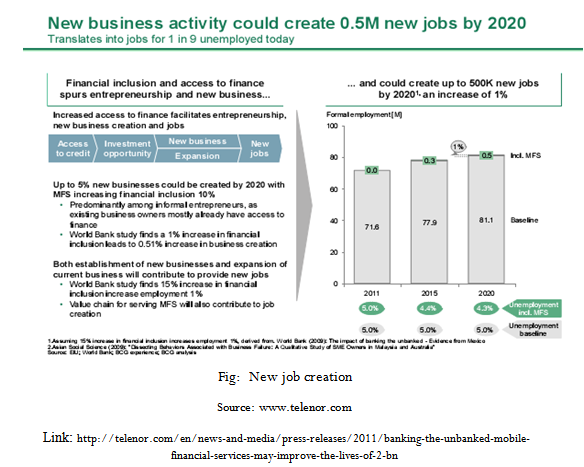

Increased access to finance facilitates entrepreneurship, new business creation, and new jobs. A World Bank study finds a 1 percent increase in financial inclusion corresponds to a 0.51 percent increase in business creation, and a 15 percent inclusion increase leads to employment growth of 1 percent.

By 2020, if MFS adoption increases financial inclusion by 10 percent, there could be an increase of up to 5 percent in new businesses, leading to 500,000 new jobs, or an employment increase of 1 percent. This is the equivalent of new jobs for 1 out of every 9 currently unemployed Bangladeshi.

Tax Revenue Growth

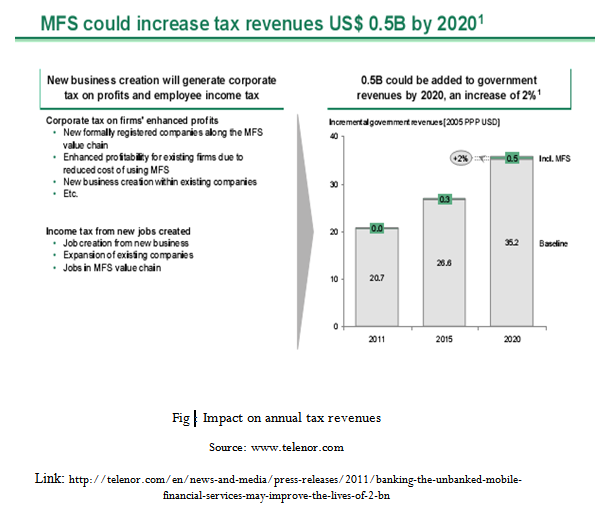

The benefits of the economic growth stimulated by MFS will increase tax revenues, as well. Corporate taxes will grow as a result of new business creation along the MFS value hain, growing profits within existing firms thanks to savings from MFS, and company expansions made possible by MFS. This business growth and creation will generate new jobs, which mean increased employee income taxes. MFS could therefore add US$500 million annually to Bangladesh’s government revenues by 2020—an increase of 2 percent.

Social Impact on Society

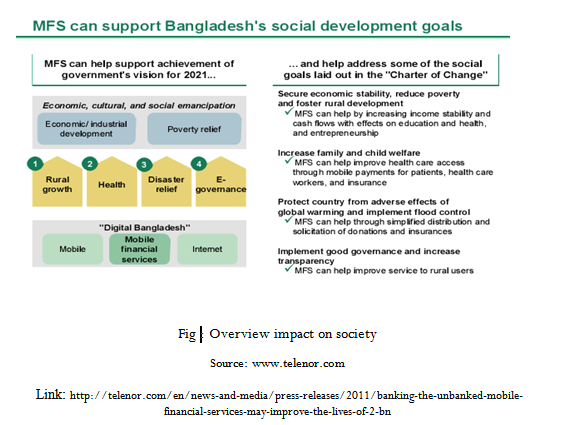

The adoption of mobile financial services can help support the achievement of Bangladesh’s social development goals, including its vision for 2021. The growth of the country’s technological infrastructure—mobile services, broadband, and, thus, MFS—will be at the root of the development of rural society, health care, disaster relief, and e-governance, and will help address some of the social goals expressed in the country’s “Charter of Change.”

For instance, MFS can aid in securing economic stability, reducing poverty, and fostering rural development as it benefits education, health, and entrepreneurship. It can increase family and child welfare as it improves health care through mobile payments for medical workers and patients and makes insurance more accessible. MFS can also serve to mitigate some of the adverse effects of global warming, particularly for the poor, and can help with flood relief by simplifying the distribution and solicitation of donations and insurance. Finally, MFS can help to implement good governance in Bangladesh and increase transparency as it improves service to rural users.

As these improvements occur, Bangladesh will undergo economic and industrial development and poverty relief. MFS can support these changes and help enhance the country economically, culturally, and socially.

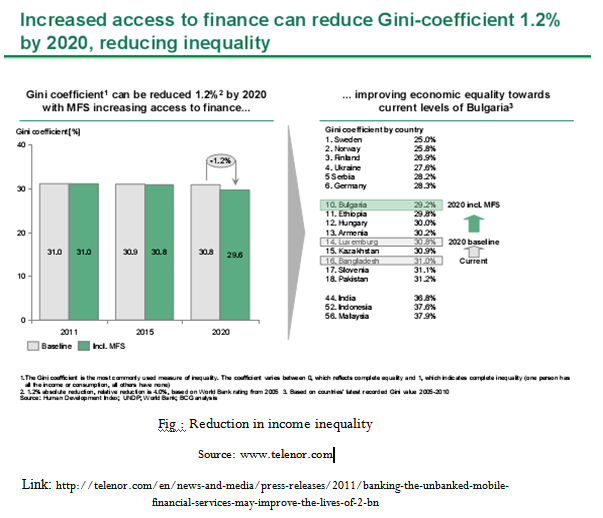

Reducing Rural Poverty

By 2020, with the distribution of MFS having widened access to financial services, the Gini coefficient—the most commonly used measure of inequality—can be reduced by5 1.2 percent. With such a shift, Bangladesh’s economic equality would be roughly equivalent to that of Bulgaria

The current inaccessibility of bank branches is an important reason that the rural poor in Bangladesh remain unbanked. For some potential customers, a trip to the bank could take a whole day, which would mean a day of lost pay, the expense of the trip, and exposure to theft. In addition, paper- and cash-based settlement systems are prone to errors, such as double-billing or charging late fees when bills have actually been paid on time.

Mobile financial services reduce or eliminate these problems. Customers save time and money, potentially 12 times their daily salaries, plus travel expenses. Storing money electronically removes the risk of theft or loss, and customers have the potential to earn interest. Incidences of double-billing and late fees go down. MFS also improves flexibility tremendously, with transactions available at customers’ fingertips at any time of day or night, as well as the use of a wide network of agents, facilitating customers’ access to cash.

Health Care Improvements

In Bangladesh today, serious injuries and funerals can have a devastating effect on the poor. Almost 70 percent of medical payments today are made out-of-pocket. For urban rickshaw pullers, for example, 67 percent of financial crises encountered are caused by health shocks. A study of poor households in Pakistan, a country that is similar in many respects, shows the potential harm of health shocks on the poor in Bangladesh. In the study, food shortages occurred in 35 percent of the cases, children dropping out of school in 10 percent of the cases, resorting to child labor in 11 percent. Fully 60 percent of these households never recovered from the damage caused by health shocks.

MFS will improve overall access to health care and mitigate the impact of health shocks by providing access to three main levers. First, with MFS, the poor have a simple and safe way to save money for future health care costs. Products can even be tailored for this purpose. In Kenya, for instance, women can make mobile micro-payments for a predetermined period to save for childbirth costs.

Second, MFS puts insurance within reach by simplifying how premiums are paid and how claims are processed. Micro-health-insurance programs can be targeted at the poor and ultra-poor.

And third, MFS makes instantaneous fund transfers easy for customers, which improves their chances of receiving immediate health care access. An example of such a program already functioning in rural areas of Bangladesh is the DGHS maternal health voucher system, which allows poor women to use vouchers to pay for treatment, with government organizations transferring the money to providers. MFS can spark other such programs, decreasing payment delays and cash reliance.

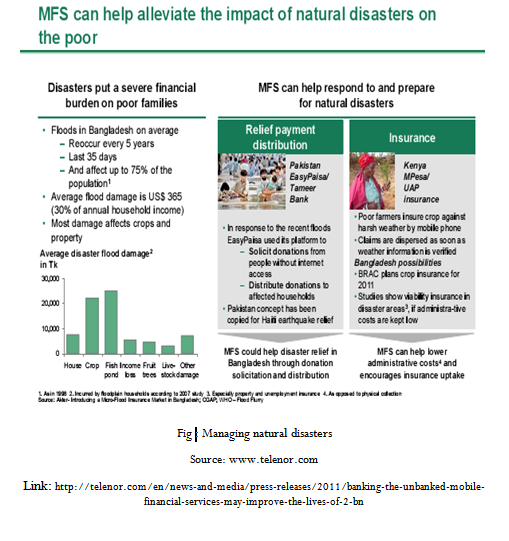

Managing Natural Disasters

Natural disasters such as floods inflict a severe financial burden on poor families in Bangladesh. Floods are a particularly significant threat in Bangladesh, given its geography. Major floods occur on average every five years, last on average 35 days, and can affect up to 75 percent of the population. Average flood damage is US$365 per household, or 30 percent of average annual household income.

MFS can help Bangladeshis prepare for and respond to natural disasters. For instance, mobile donation solicitation and distribution programs can improve disaster relief. In Pakistan Easy Paisa used its MFS platform in response to floods to solicit donations and to distribute donations to households in distress. The same concept was used in Haiti after the recent earthquake. Such services are particularly crucial when no alternatives are available, since it will often not be possible to keep track of potential recipients as they flee the affected areas, or physically deliver cash or other forms or payments to those who need it.

MFS can help Bangladeshis prepare for and respond to natural disasters. For instance, mobile donation solicitation and distribution programs can improve disaster relief. In Pakistan Easy Paisa used its MFS platform in response to floods to solicit donations and to distribute donations to households in distress. The same concept was used in Haiti after the recent earthquake. Such services are particularly crucial when no alternatives are available, since it will often not be possible to keep track of potential recipients as they flee the affected areas, or physically deliver cash or other forms or payments to those who need it.

Mobile services can also be used to encourage the uptake of insurance. Kenya MPesa’s UAP Insurance is a mobile product that has proved successful. Poor farmers there can insure their crops by mobile phone against harsh weather, and claims are dispersed as soon as weather information is verified. In Bangladesh, BRAC is planning a crop insurance program for 2011. Studies show that insurance can be viable in disaster areas—as long as administrative costs are kept to a minimum, an issue MFS is well suited to address.

Institution that provide the MFS

There are four institutions that provide the mobile banking service. These are

- Dutch-Bangla bank ltd

- Brack Bank ltd

- Islami Bank Bangladesh ltd

- Bangladesh Post Office.

DBBL is the first bank in Bangladesh who introduces Mobile banking service to bring poor people form remote area under smart banking service. DBBL is operating this new innovative banking service through Banglalink and Citycell mobile operator and their approved agent throughout the country.

DBBL largest bank has selected Sybase 365 of its mobile banking platform.“Sybase365’’ platform allows us to deliver the best possible mobile banking service to customer.

Bangladesh’s first complete mobile financial service provider, bKash Limited, a BRAC Bank subsidiary, launched its mobile banking operation.

The bkash mobile wallet, a VISA technology platform which is fully encrypted to ensure most secure transactions, will be the customer account into which money can be deposited and out of which money can be withdrawn or used for various services. Customers will be able to receive electronic money into their bKash accounts through salary, loan, domestic remittance, and other disbursements and eventually will cash out the electronic money at any of the hundreds of cash out agents which bKash assign.

“bKash provides a wonderful opportunity for millions of unbanked people who have a cell phone to have a bank account where they will be able to deposit, pay out and transfer funds as they wish safely and securely bkash is designed to provide financial services via mobile phones to both the unbanked and the banked people of Bangladesh. The overall bKash value proposition is simple: a safe, convenient place to store money; a safe, easy way to make payments and money transfer.

In February 2011, mobile operator Robi Axiata Limited signed a partnership agreement with bKash to provide access to its services for Robi subscribers and extend the distribution of the service. bKash’s other distribution partner is BRAC which provides a local presence to offer the bKash service at the vicinity of the beneficiaries.

The directorate of Bangladesh Post Office (BPO) will introduce a banking service that allows people to make transaction over a cell phone. The service, titled post e-pay, will be launched in all the 9800 branches of the post office in phases with the help of the mobile operator country with network.

This is the first time that mobile banking services have been launched in the country. However, these new services introduce a person to person transaction without going to post office and charges are 3 tk. The service can be utilized for the payment of bills. The Govt can also pay salaries to employees through the service.

Initially so post offices in the capital, Dhaka, have been developed for the service and four districts will be prepared each month for the service.

Two types of technology will be used for the service SMS, and internet.

Islami Bank Bangladesh ltd has introduced its SMS banking service by mobile phone operator. The services that provided are

- Multiple Account Registration.

- International push-pull facility

- Account Balance

- Mini Account Statement

- Account Information.

| Institution | Mobile Financial Services |

| Dutch-Bangla Bank Ltd |

|

| Brack Bank Ltd |

- The bkash mobile wallet, a VISA technology platform which can be used for money deposit and withdraw

- Uses Robi mobile operator

- Provide SMS banking and SMS bill payment

- Customers will be able to receive electronic money into their bKash accounts through salary, loan, domestic remittance, and other disbursements.

Islami Bank Bangladesh Ltd

- Provide SMS banking And internet banking

- Multiple Account Registration

- International push-pull facility

- Account balances and account information

- Mini account statement

Bangladesh Post Office

- The post e-pay allow people to make transaction

- Introduce a person to person transaction without going to post office

- Charges is minimum

- Utilize in payment of bill, Govt can also pay salaries

- Provide SMS banking and internet banking

Here we see that different institution provide the mobile financial services by different way. They uses various mobile operator among them Bangladesh post office provide the services by minimum charges and set up a country wide network. On the other hand Dutch Bangla Bank provides various services with securities. It provides the services by citycell and Banglalink mobile operator that is available. So Dutch Bangla bank is best.

CONCLUSION

The emergence of m-banking/m-payments systems has implications for the more general set of discussions about mobile telephony in the developing world. For example, it underscores the way the device blurs the domestic and the productive spheres, the social and the transactional. Each transaction is influenced by (and reinforces) the structural position of people in broader informational networks (Castells, 1996). The latest case of m-banking/ m-payments systems is a reminder that an understanding of the role of the mobile in developing societies must include its role in mediating both social and economic transactions, sometimes simultaneously. Existing theory about the significance of mobile communications in the developing world has focused on voice and text messaging (Donner, 2008). This focus is appropriate, but the emergence of mobile banking also underscores how, occasionally, innovations emerge from unexpected places and have the capability of reconfiguring the significance of a technology to its users. Mobile theory must keep pace, accounting for m-banking/m-payments systems along with other capabilities enabled by this increasingly flexible technology.

REFERENCES

Anyasi, F.I. and A.K. Yesufu, 2007. Indoor propagation modeling in brick,

zinc and wood buildings in????

Anyasi,F.I., P.A. OTUBU and F.E. ISERAMEIYA, 2008. The Merging of Telecommunication And Information

Arumugam, S., T. Jebarajam and Joy Winnie Wise, 2008.

Congestion Control Algorithm In Computer

Barnhart, C.L. and R.K. Barnhart, 2000. The World Book

Dictionary. Sixth Edition. ISBN: 0-19-431538-x

Wikipedia, the free encyclopedia, http://en:wikipedia.org/wiki/mobilebanking- 7/16/2008

Wikipedia, the free encyclopedia, http://en.wikipedia.org/wiki/smsbanking-7/16/2008

Wikipedia, the free encyclopedia, http://en.wilipedia.org/wiki/online,banking-7/16/2008

Wikipedia, the free encyclopedia, http://en.wikipedia.org/wiki/telephonebanking-7/16/2008

Wikipedia, the free encyclopedia, http://en.wikipedia.org/wiki/automated-teller-machine7/16/2008

www.telenor.com; visited on 10th February, 2012; Link: http://telenor.com/en/news-and-media/press-releases/2011/banking-the-unbanked-mobile-financial-services-may-improve-the-lives-of-2-bn