Concept of Cost-Volume-Profit Analysis (CVP Analysis)

It is a method of cost accounting that looks at the impact that varying levels of costs and volume have on operating profit. Every firm has a prime motive of not only earning profit but also maximizing it. A profit does not happen by chance. It has to be managed. Cost-volume-profit analysis (CVP Analysis) is a tool of planning for profit. CVP analysis is helpful for developing alternative strategies in the sales planning and cost estimation. A certain relationship exists among the variables like selling price, sales volume, and taxes.

Cost-volume-profit analysis (CVP analysis) is an accounting technique showing the relationship among these variables. The cost-volume-profit analysis makes several assumptions, including that the sales price, fixed costs, and variable cost per unit are constant. CVP analysis, though most often illustrates business cases, is equally applicable for not profit-making organizations to allocate scarce economic resources most effectively among the competing alternatives. It is used to determine how changes in costs and volume affect a company’s operating income and net income. The allocation of scarce resources among the various demanding sectors is the most important issue of national planning. CVP analysis requires that all the company’s costs, including manufacturing, selling, and administrative costs, be identified as variable or fixed.

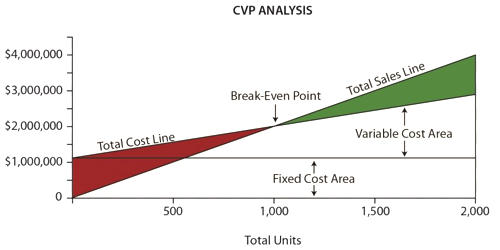

The CVP formula can be used to calculate the sales volume needed to cover costs and break-even, in the CVP breakeven sales volume formula, as follows: Breakeven Sales Volume = FC/CM

Where,

- FC = Fixed costs

- CM = Contribution margin} = Sales – Variable Costs

CVP analysis is the analysis of the relationship between cost and volume of activities and the effect of the relationship on profit. It is an analytic tool based on cost accounting measures. CVP analysis is a framework for figuring out how you get to profitability. Managers can use the concept of cost-volume-profit analysis to forecast the volume of activity at which the firm will break-even or attain target profits. CVP is very useful for making informed decisions and analysis. CVP analysis is therefore, a useful tool that helps managers, business owners and entrepreneurs to determine the profit potential of a new firm or the impact on profit due to changes in selling price, cost, or level of activities of current business. CVP analysis expands on break-even analysis. An important transition point in CVP analysis is the break-even. It helps in understanding the relationship between profits and costs on the one hand and volume on the other.