Chapter-01

Introduction

The internship project is the fulfillment of an active part of the internship program as per requirements for completing the BBA program. As an intern attach with Pubali Bank Limited, naturally the selected project will be related to the area by which the organization can be influenced. Pubali Bank Limited is the largest private scheduled Bank of the country. It is significant part of the Banking and financing sectors of Bangladesh, which is always playing an important role to improve the banking and financing in this country.

Bangladesh is one of the developing countries in the world. The economy of the country has a lot left to be desired and there are lots of scopes for massive improvement. In an economy like this, banking sector can play a vital role to improve the overall social-economic condition of the country. The banks by playing the role of an intermediary can mobilize the excess fund of surplus sectors to provide necessary finance, to those sectors, which are needed to promote for the sound development of the country. In this regard Pubali Bank Limited by dint of rendering the overall banking services has been playing active role in the development of our economy.

This report is an attempt to reflect the position of Pubali Bank Limited in the banking industry of the country in respect of its activities in the arena of overall banking services- General Banking, International Trade and Local Financing.

There are three types of schedule commercial banks are in our country. They are Nationalized Commercial Banks, Local Private Commercial banks and Foreign Private Commercial banks. Pubali Bank Limited has discovered a new horizon in the field of banking area, which offers General Banking, Investment and Foreign Exchange banking system.

So I have decided to study on the topic “An study on Foreign Exchange transaction on export and import of Pubali Bank Limited”.

Because the BBA program is an integrated, practical and theoretical method of learning, the students of this program are required to have practical exposure in any kind of business organization last term of this course. This report on practical orientation has been oriented above thinking. The BBA program conducted by BIU was introduced in order to provide a number of graduates in business sector; this program has been designed to facilitate the students and to provide basic theoretical knowledge and practical in the job activities in the context of Bangladesh. Students are required to work on a specific topic based on their theoretical and practical knowledge acquires during the period of Dissertation Program and then submits it to the teacher. That is why I prepared this report.

This internship report is generated under the supervision of Mr. Shajedul Alam, senior lecturer of USB Department of University of Liberal Arts Bangladesh. It is required to fulfill the BBA. The topic of this report is “A study on the foreign exchange transaction on import & export of Pubali Bank Ltd.”.

To prepare this report I have selected and got opportunity to work as an interne at Pubali Bank Limited, Foreign Exchange Corporate Branch, under the supervision of Ferdousi Jahan, Deputy General Manager, in charge of the Branch. My supervisor duly approved the topic, which was decided for doing the report. The report will definitely increase the knowledge of other students to know the financing institutions i.e. Banking Industry of Bangladesh, and the various services PBL is providing to develop this industry.

The main objective of my study is to gather practical knowledge regarding banking system and operation.

The specific objectives of this study are as follows:

- To acquire some practical experience that will be helpful in the near future.

- To find out the overall picture of Foreign Exchange Business of Pubali Bank Limited.

- To gather knowledge the function and transactions of different type of Foreign Exchange business of Pubali Bank Limited and comparison of practice based on theory.

- To identify the problems related of Foreign Exchange business faced by Pubali Bank Limited.

- To demonstrate their Strength, Weakness, Opportunities and Threats.

- To find out the reasons why people go to Pubali Bank Limited.

The report has been prepared from every day working experience, extensive. Discussion with the concern dealing officer of PBL, Foreign Exchange Branch, Dhaka, and the theoretical learning that I have achieved from library, journal and circular of Bangladesh Bank . It is not possible to pinpoint the each and every aspects of overall banking transaction due to this short span of time.

The study is qualitative in nature. In depth interview of the company personnel, various official documents, study case, circulars were used as instruments to collect information.

Several group discussions arranged with the concern official of the different wing of department of PBL, Foreign Exchange Branch. The study contains a huge amount of data and information. In preparing this report, I had to follow some methods to collect information:

I collect my information through face to face interview and discussion with the officers of different wings of PBL, Foreign Exchange Branch. I have gone through different types of publications. I had also used published data. These are:

- Various publications of PBL.

- Annual report.

- Various reports were collected from internal bodies and library.

- Main papers and documents were collected from different wings and desks.

For the data analysis the following steps are followed:

- Software: Computer software (e.g. Microsoft Excel) is used, which has helped to make the analysis of data collected during the research proposal easier, more efficient, and more effective.

- Tables: Frequency table, data analysis, etc have been used to describe the findings.

- Graphics: Chart wizard, graph different types of figures have been used to represent the findings from the survey.

There were some problems efforts was applied to conduct the orientation program. A wholehearted effort was applied to conduct the orientation program and to bring a reliable and fruitful result.

In spite of having the wholehearted effort, there exit some limitation, which acted a barrier to conduct the program.

The study has suffered following limitations:

- Respondents were reluctant to fill the questionnaire, which has impeded the preparation of the study.

- Validity of the study is subject to the reply of the respondent.

- Because of the resource constraint survey as per the sample size was not possible which has restricted the accuracy of the result.

- All the concerned personnel of the bank have not been interviewed.

- Lack of in-depth knowledge and analytical ability for writing such study.

- Lack of experience.

- To analyze SWOT of an emerging market is a wide survey material.

But time constraint restricted the study to specific feature.

Chapter 02

Profile of the Organization

In 1971, Bangladesh, was East Pakistan, emerged as an independent country. In immediately nationalized the entire Banks expanding 3 Foreign Banks, six Nationalize Banks were thus formed. In 1983 a new policy was implemented allowing private sector participation in the industrialization. As a part of this process, two national commercial Banks were against denationalization and a number of Private Commercial Banks were allowed to operate. Among these Pubali Bank and Uttara Bank were the first to be decentralized.

Schedule Banks in Bangladesh

| Particulars | Number of Banks |

| Nationalized commercial Bank | 04 |

| Privatized commercial Bank | 32 |

| Specialize Bank | 04 |

| Foreign Bank | 9 |

| Co- Operative Bank | 01 |

| Grameen Bank | 01 |

Total = | 51 |

Table 2.1: Schedule Banks in Bangladesh.

Pubali Bank limited is the largest Commercial Bank in Private sector. The Bank was incorporated in the year 1959 under the name and style of Eastern Mercantile Bank limited under company Act 1913. After liberation of the country in 1971, the Bank was nationalize as per policy of the Government of the People’s Republic of Bangladesh under the Bangladesh Bank (Nationalization) order 1972(PO No 26 of 1972) and was renamed as Pubali Bank. Subsequently, the Bank was denationalization in the year 1983 and was again incorporated in Bangladesh under the name and styles of Pubali Bank Limited in that year 1984 on May 20 under the license no Bl/DA/1/84. The Government of the People’s Republic of Bangladesh transferred the entire undertaking of Pubali Bank Limited, which took over the same as a going concern. It is listed in the Stock Exchanges at Dhaka and Chittagong as publicly traded company for its general class of shares. In 1983 PBL started their new journey with the deposit of Tk. 645.14 Crore and they sold 16 Lac shares in the market. It has a large asset position comprising of Tk.130, 121.42 million in March 2011. The Bank employs largest in private sector, which stood almost 5600 personnel in March 2011. Presently it has 400 branches in operations Principal branch is one of the big and important branches of PBL.

PBL intendeds to ensure the trust and confidence of the customers through focused customer’s orientation qualities of services and state of art technology. The company philosophy-A Bank for the 21st century has been precisely the essence of the legend of the Bank success.

- To get recognition as a dynamic, innovative and customer supportive Bank.

- To maintain continuous & steady growth with utmost transparency and to diversify development of resources.

- To enhance continuous development of information & technology to meet the demand and challenges of the time.

To hold the position of best private commercial bank in Bangladesh with adherence to meticulous compliance of rules and regulation and strong commitment to social responsibility.

The bank will be a confluence of the following three interests:

- Of the Bank: Profit maximization and sustained growth

- Of the Customer: Maximum benefit and satisfaction

- Of the society: Maximization of welfare

The objectives of the bank are to promote private sponsors to establish joint venture banks, financial companies, branches and affiliates abroad to satisfy their customers. It conveys its objective via their motto:

- Be one of the best bank in Bangladesh

- To establish, maintain, carry on, transact, undertake and conduct all types of banking, financial,

- investment and trust-business in Bangladesh and abroad

- To form, promote, organize, assist, participate or aid in forming, promoting or organizing any company, bank, syndicate, consortium, and institute or any holding or subsidiary company in Bangladesh or abroad for the purpose of undertaking any banking, financial, investment or trust business.

- To encourage, sponsor and facilitate participation of private capital in financial, industrial or commercial investments, shares and securities and in particular by providing finance in the form of long, medium or short term loans or share participation by way of subscription to the promoter shares or underwriting support or bridge finance loans and/or by any manner.

The Bank was established primarily as Private Bank. After liberation it was nationalized and it remained so for quite a long period. Though it has been denationalized again and has gone back to its Private norm it could not get rid of all the rules and norms of Nationalized Bank. Like any other business organization, the top management makes all the major decisions in PBL. The Board of Directors being at the highest level of organizational structure plays an important role on the policy formulation. The Board of Directors is not directly concern with day-to-day operation of Bank. They had delegated their authority to the Managing Director who is assist by Additional Managing Director (AMD), Deputy Managing Directors (DMD) and General Managers (GM) to look after the day-to-day affairs of the Bank. The Bank is running by an excellent management team under the direct supervision of a competent Board of Directors. The Board of Directors comprises total fourteen members headed by the Chairman. Mr. Hafiz Ahmed Mazumder is the present Chairman of the Board. The Managing Director (MD) heads management team. Under him a AMD, four DMDs, a GM heads each department of the Bank. Mr. Helal Ahmed Chowdhury is the present Managing Director of PBL. The management hierarchy of Pubali Bank Limited is given below:

Organ gram of Pubali Bank Limited

All activities related to the loans and advances are directed and controlled by this division. This division is presently headed by a General Manager. The credit deals with different types of credit, like, Commercial credit (e.g., Secured overdraft, cash credit, etc.), Industrial credit. For monitoring, follow-up, supervision of the functions and to gather market information, there is a cell in this division.

Credit sector wise as on 31st December 2010

This department is assigned to do the activity related to general administration and development of human resource of the bank.

Human Resources of PBL

This division maintains all sort of accounts of the bank, performs fund management, management information system, expenditure control, budgeting, etc. This department is presently headed by a Chief Financial Officer and General Manager.

International division of Pubali Bank Ltd. performs the responsibilities of foreign trade and foreign exchange and foreign remittance on behalf of the branches. The division deals with the issues regarding opening, lodgment, and payment of import of Credit, PAD, LIM, LTR, etc. This division also relates to export such as advising, negotiating, export documents, etc.

This division is headed by a General Manager and works directly under the control of the managing director. The division is responsible to arrange periodical internal audit, conduct special audit, follow-up and monitor the bank’s overall activities.

This division procures and supplies dead stock such as furniture, machinery, equipment and stationers, vehicles, etc. also renders some other common services and control central dispatch services. The division is presently headed by a General Manager.

The division is assigned to lead the computerization of the bank. It procures and maintains computer hardware and software, conducts computer training for the employee. Operation and maintenance of all electrical and mechanical appliance such as note counting machine, telephone, PABX, FAX, Telex, are usually done by the department. At present the division is headed by Mr. Mohammad Ali, Chief Technical Officer (CTO) and General Manager.

This division sanctions the loans related to household goods, car, flat purchase, educational loans etc. and makes periodical on site and off site supervision and initiate step to recover the loans. Presently the division is headed by a General Manager.

This division is assigned to perform the task to invest in Lease asset-Equipments, Machineries, Pick up Van and son. The division promulgates policies related to Lease Finance and takes all types of supervisory steps together with the Branch.

Conformity with Bangladesh Bank’s regulations, this division is assigned to perform the duty of ensuring compliance by the Branch level to rules and regulations, policies promulgated time to time by the Bank and Bangladesh Bank as well.

This division is headed by a General Manager and works directly under the control of the managing director. The division is responsible to follow-up and monitor the credit at the post sanction stage and to arrange all types of procedures to recover the bad loans.

This division is responsible for all types of legal aspects. This division is headed by a General Manager and he must be a legal representative.

This division is headed by a General Manager and works directly under the control of the managing director. The division is responsible to arrange the bank’s overall development activities such as opening new branch and so on.

This division is headed by a General Manager and works directly under the control of the managing director. The division is responsible to arrange the bank’s overall research and

Development activities such as designing product policy program, controlling product quality, creating new brand product and so on.PBL is the largest commercial Bank in private sector of Bangladesh. The Bank within stipulation lay down by the Bank Company Act 1991 and directives as received from Bangladesh Bank from time to time provide all types of commercial Banking services. It has 400 branches all over the country and among them 205 Branches is online.

Branch Network of PBL

Bank’s Name | Name of Region/Zone | No. of Branches |

PUBALI BANK LIMITED | Dhaka | 76 |

| Narayangonj | 18 | |

| Chittagong | 56 | |

| Sylhet | 48 | |

| Moulvibazar | 33 | |

| Comilla | 28 | |

| Noakhali | 19 | |

| Mymensingh | 27 | |

| Rajshahi | 24 | |

| Rangpur | 18 | |

| Barisal | 27 | |

| Khulna | 26 | |

| Total Branches | 400 |

Table:2.3 Branch Network of PBL

The risk management of the bank covers six core risk areas of banking I.e.

- Credit risk

- Asset Liability risk

- Foreign Exchange risk

- Internal Control & Compliance risk

- Money Laundering risk, and

- Information technology risk

The bank management is well conscious about its responsibilities and always uses to take calculative business risk with a view to safeguard the bank’s capital, its financial resources and profitability. The bank follows the guidelines of Bangladesh bank and other regulatory authorities in respect of risk management. As per as direction of Bangladesh bank a separate risk management unit has already been formed in the bank headed by deputy managing director (admin), deputy managing director (operation), deputy managing director (general) and all the divisional heads are the members of the unit.

The principal activities of the bank are banking and banking related business. The banking business included deposits taking, extending credit to corporate organization, retail and small & medium enterprises, trade financing, project financing, etc. Some of which are mentioned below with a brief overview of the major business activities:

Retail Banking: As part of risk diversification strategy PBL has expanded the lending activities in this sector since 2003. The loan schemes offered by the bank include Flat Loan, Household Loan, Car Loan, Education Loan, Retired Primary Teacher Loan, Loan against Salary, and Loan against Medical Equipments and so on.

SME Lending: Job creation is essential and it must come from Small and Medium Enterprise that will ultimately dominate the private sector. During 2010 bank’s Strategy was focused on customer convenience.

Corporate Credit: PBL’s strategy is to provide comprehensive service to the clients of this segment who are large and medium size corporate customers with experience in trade finance and related services.

Islamic Banking: for the development of Islamic Banking Business, in 2010 PBL had entered into the vein of Islamic Banking Business. Islamic Banking operation of the bank has been separated from the operation of conventional banking.

Correspondent Relationship or Foreign Exchange Business: Over the years, foreign trade operations of the bank played a pivotal role in the overall business development of the bank The bank has established correspondent relationships with a number of foreign banks, namely American express Bank, Bank of Tokyo, Standard Chartered Bank, Mashreq Bank, Hong Kong Shanghai Corporation, CITI Bank NA-New York And Arab-Bangladesh Bank Ltd. The bank is maintaining foreign exchange accounts in New York, Tokyo, Calcutta, and London. The bank set up letter of credit on behalf of its valued customers using its correspondents as advising and reimbursing banks. The banks maintain a need based correspondent relationship policy, which is gradually expanding.

Merchant Banking: The Bank’s operation in this sector was limited Underwriting, Portfolio Management and Banker to the Issue functions. At present this merchant banking is separated from core banking and it is regarded as the sister concerns of PBL.

Information Technology in Automation and Online Banking: All the 400 branches have been computerized and running successfully with the in-house developed software, PIBS (Pubali Integrated Banking System). Pubali Bank limited has implemented Centralized online Banking system in the year 2008 through its in-house developed software. In the mean time all branches in Dhaka, Chittagong and Sylhet have been brought under online banking system. At present 301 branches are online and it will be increased branches in the upcoming year. The rmaining branches will brought under online banking system gradually. The bank will also extend services to its customers through internet Banking and mobile phone bank phase wise shortly. The bank has developed Islamic Banking Software and 2 (two) Islamic banking wings in Dhaka and Sylhet. The bank has entered into the internet world through its website www.pubalibangla.com and has also been operating Automated Trailer Machine (ATM) and Point of sale (POS) services to meet the demand at the time. PBL also has entered into the payment system of Bangladesh Electronic Fund Transfer (BEFTN) in 2011.

Pubali Exchange and Pubali Money Payment Business: PBL has started the business of Pubali Exchange and Pubali Money Payment to facilitate the process of remittances. PBL in this regard has established 2 Exchange in London and Malaysia and will also establish another one in Italy very soon. Gradually Pubali Exchange will be established all over the world.

Pubali Bank Limited offers various kinds of deposit products and loan schemes. The Bank also has highly qualified professional staff members who have the capability to manage and meet all the requirements of the bank. Every account is assigned to an account manager who personally takes care of it and is available for discussion and inquiries, whether one writes, telephones or calls. The products and services are given below:

Deposit Services:

Foreign Currency Account | Miscellaneous Services:

|

Loans & Lease Services:

| Remittance Services:

|

PBL is one of the largest private sectors Bank in Bangladesh with years of experience. The Bank is on the steady growth considering its financial position which is discussed below:

The Bank’s investment was Tk. 15,943 million as on 31.03.2011 and Tk. 16,516 million at the end of the year 2010. The amount of investment at the end of year 2010 for Tk. 3987 million.

Chart 2.5: Investment

Loans and advances of the bank grew strongly by 20.08% i.e. Tk. 14,903 million in 2010 and stood Tk. 89,106 million. Bills purchased and discounted increased by 74.01% indicating strong growth in export performance. Now at the end of the month of March, 2011 total advances stood Tk. 86,965 million.

Loans & Advances and Deposits

Total Liabilities of the Bank are increased by Tk. 16,013 million during 2010 due to incensement of deposits. At the end of the March 2011, it stands for Tk. 115,286 million.

The authorized capital and paid up capital of the bank stood at Tk. 10000 million and Tk. 4968.60 million respectively in 2010. Out of total 86200 shareholders, Bangladesh government held 72 shares of Tk. 7200 while taka remaining shares of Tk. 2939.99 million where held by various shareholders.

Capital Structure

Value added to the bank stood at bdt 7097.53 million as of December, 2010 as against bdt 5406.44 million in 2009 registering a growth of 31.28% over the previous year. The highest percentage of value added statement went to the shareholders stood at 30.14% in 2010 as against 22.32% in 2009. The share of government of Bangladesh decreased to 24.62% in 2010 against 29.17% in 2009. The depreciation, repairs and maintenance of fixed assets decreased to 2.15% in 2010 as against 2.20% in 2009 and statutory reserve value added stood at 14.03% in 2010 from 13.58% in 2009.

Chart:2.11

Net Profit before Tax stood at Tk. 4,980 million and Net Profit after Tax had become Tk. 3,233 million. Thus the growth rates of the Net Profit before and after Tax were 35.73% and 54.54% respectively than that of previous year. At the end of the March 2011, Net profit before Tax and after Tax stood for Tk. 949 million and Tk. 457 million respectively. By the end of the month of June 2011 the profit of PBL stands for Tk. 280 Core.

| SL No | Particulars | 2006 | 2007 | 2008 | 2009 | 2010 |

| 1. | Deposit | 44443.03 | 48675.93 | 57996.82 | 73016.51 | 98850.49 |

| 2. | Total Loans & Advance | 32639.68 | 40386.65 | 50549.16 | 61788.15 | 89106.21 |

| a) Unclassified | 24747.48 | 35208.44 | 46006.8 | 57450.27 | 84192.11 | |

| b) Classified | 7892.2 | 3206.82 | 2514.90 | 2219.31 | 1047.60 | |

| 3. | a) Required amount of Provision | 289.22 | 104.97 | 113.98 | 137.82 | 3866.5 |

| 4. | Net Profit/Loss | 875.53 | 1353.51.3 | 1515.23 | 2092.23 | 3233.09 |

Overall Performance of PBL

Not surprisingly, in the competitive area of marketing are SWOT analysis is a must based on product, price, place and promotion of financial institute like private bank from the SWOT analysis we can figure out ongoing scenario of the bank. So to have a better view of the present banking practices of Pubali Bank Ltd. SWOT analysis is very necessary.

Strength:

- Brand Value.

- Product Rang

- Low Interest rate @ 13% than foreign banks

- 400 branch all over the country

- Effective human recourses

- Minimum service charge

- Large number of customers

- No additional service charges impose

Weakness:

- Poor Que. Management

- Less superior service quality

- Lack of technology

- Minimum customer care

- Minimum use of advertising

- No use of ATM

- Less contribution of management with employees

Opportunity:

- Large number of share and paid up capital

- Several segments in investment

Threats:

# Local Private Banks

- PBL Vs Dhaka Bank

- PBL Vs Eastern Bank

- PBL Vs IFIC Bank

- PBL Vs Mercantile Bank

# Foreign Banks

- PBL Vs standard Chartered Bank

- PBL Vs HSBC

- PBL Vs American Express

| SL. | Particulars | 2008 | 2009 | 2010 |

| 1 | Authorized Capital | 5,000.00 | 5,000.00 | 10,000.00

|

| 2 | Paid-up capital | 2,940.00 | 3,822.00 | 4,968.00 |

| 3 | Reserve fund | 4,606.82 | 5,687.25 | 9,411.27 |

| 4 | Total Deposits | 73,016.51 | 88,466.46 | 98,850.50 |

| 5 | Total Advance | 61,788.15 | 74,203.33 | 89,106.21 |

| 6 | Total Investment | 8,375.59 | 12,168.65 | 16,516.39 |

| 7 | Import Business | 58,009.10 | 60,493.85 | 85,683.53 |

| 8 | Export Business | 24,795.65 | 24,739.65 | 33,909.78 |

| 9 | Bridge Finance | 6.89 | 6.89 | 6.89 |

| 10 | Total Income | 9009.25 | 10,663.81 | 12,828.53 |

| 11 | Total Expenditure | 5563.39 | 6824.34 | 7343.48 |

| 12 | Pre-Tax Profit | 3445.86 | 3839.47 | 5485.05 |

| 13 | Net Profit | 1515.23 | 2092.23 | 3233.09 |

| 14 | Total Assets | 89,884.70 | 107,579.60 | 128,462.65 |

| 15 | Fixed Assets | 1383.36 | 1443.50 | 3330.32 |

| Other Information | ||||

| 16 | Number of Employees | 5321 | 5375 | 5534 |

| 17 | Number of Shareholder | 24,153 | 30,899 | 86,200 |

| 18 | Number of Branches | 371 | 386 | 399 |

| 19 | Earning Per Share(absolute EPS for tk. 10 face value) | 5.15 | 5.47 | 6.51 |

Chapter o3

Literature Review

Ordinary people consider foreign exchange the same as foreign money or currency notes of foreign countries like American Dollar or British Pound Sterling. This is true only in a narrow sense. In practice, foreign exchange is not conceived the same as generally understood. Bank notes or what we commonly call foreign currency notes, do not play any significant role in settlement of international transactions. In a broader sense, foreign exchange can be defined as a process of conversion of one currency into other. According to Paul Einzig, “The foreign exchange market is the system in which the conversion of one national currency in to another takes place with transferring money from one country to another.”According to Kindleberger, “It is place where foreign moneys are bought and sold.”

In short, foreign exchange is the means and methods by which rights to wealth in one country’s currency are converted into those of another country. And foreign trade means the cross border of goods and services with release its payment.

Since the early days of civilization, nations have engaged in trading. At the same time each nation has developed its own currency. Internationalism of trade and nationalization of currencies are two divergent phenomena, as mentioned by the French economist. As the world, by the grace of modern technology, is getting smaller day by day, the need for foreign exchange has become a part of everyday life. Globalization of the world economy for goods and services makes foreign exchange necessary for almost every citizen across the country.

Foreign exchange has a price in relation to local currency in the same way as rice, jute or any other tradable goods has a price in terms of taka and the price will vary. Foreign currencies from our point of view can very well be equated to commodities.

Foreign Exchange transactions as well as business are controlled by the both local and international rules and regulations.

Our foreign exchange transactions are being controlled by the following local regulations:

Foreign Exchange Regulations Act: Foreign Exchange Regulations

(FER) Act 1947 enacted on 11th March 1947 in the British India,

Provides the local basis for regulating the foreign exchange . This act

was adapted in Pakistan and lastly in Bangladesh.

Guideline for Foreign Exchange Transaction: This publication issued By Bangladesh Bank in the year 1996 in two volumes. This is compilation Of the instructions to be followed by the authorized Dea/Crs in transaction Relating to foreign exchange .

F.E. Circular: Bangladesh Bank issues F.E circular from time to time control the export business and remittance to control the foreign exchange. It has one kind of supplementary and complementary action to the guideline for foreign exchange transaction.

Import-Export policy: Ministry of commerce issues Export policy and Import policy giving basis formalities and instructions for Import and Export business.

Public Notice: Sometimes Chief Controller of Import and Export issue public notice for any kind of change in foreign exchange transactions.

Instructions from Different Ministry: Different ministry of government sometimes instruct the authorized dealer directly or through Bangladesh Bank to follow something required for the government.

There are some international organizations influencing the foreign exchange transactions. Few of them are discussed below:

International Chamber of Commerce: ICC is a worldwide non-governmental organization of thousands of companies. It was founded in 1919. Its headquarters is in Paris. For managing and controlling the international trade ICC issues some publications which are being followed by the all member countries. It has also a International Court of Arbitration to solve the international business dispute. The major publications of ICC are:

- Uniform Customs and Practice for Documentary Credit (UCPDC).

- Uniform Rules for Collection.

- Uniform Rules for Reimbursement.

- International Standard for Banking Practice.

World Trade Organization (WTO): WTO is another international trade organization established in 1995. This organization has vital role in international trade through its 124 member countries.

The rate of exchange is the price of one currency, in terms of another currency or in the other words, the number of units of one currency which exchange for a given number of units of another currency.

There are mainly 4 theories explaining the determination of exchange rate. Such as:

- a. Mint Parity Theory

- b. IMF Par Value Theory

- c. Purchasing Power Party Theory

- d. Demand and Supply Theory.

Chapter 04

Analysis and Findings

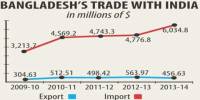

During the year the bank handled import business worth tk. 85683.53million. During the previous year the amount was tk. 60493.85million. The amount of import business handled by the bank increased by tk. 25189.68million during the year which was 41.64% higher than that of the previous year

Key Performance of Import

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| BDT in Million | 37316.50 | 48345.41 | 58009.10 | 60493.85 | 85683.53 |

Table 4.1: Key Performance of Import

Import of PBL

Letter of Credit is the most important instrument used for payment of imports. It is a legal instrument, which binds all relevant parties according to terms and conditions incorporated therein. Generally, there are 4 (four) parties involved in an L.C. They are:

- The importer/ Buyer Opening

- Bank/Issuing Bank

- Seller / Exporter Advising

- Bank/ Negotiating Bank.

According to payment terms, there are mainly three types of L/Cs such as:

- Sight Credit

- Acceptance Credit

- Deferred Payment Credit

In addition to the above, the following special types of credits are also used for settlement of payments:

- Revolving LC

- Back to Back LC

- Red Clause LC

- Stand by LC

- Performance LC

To have an import L/C limit, an importer submits an application to the department of (PBL) furnishing the following importers:

Full particular of bank account.

Nature of business

Required amount of limit.

Payment terms and conditions.

Goods to be imported.

Offered security.

Repayment schedule.

A credit officer scrutinizes this application and accordingly prepares a proposal (CLP) and forwards it to the head office credit committee (HOCC). The committee, if satisfied, sanctions the limit and returns back to the branch. Thus the importer is entitled for the limit.

The letter of credit (L/C) registration function shall allow the user to register a new L/C upon receipt of an application for issuance / opening of L/C.

It shall provide the followings:

- Able to automatically generate and assign a unique reference number for each new L/C according to the bank pre- defined format. The system assigned number will be the L/C reference number and shall be used for all future transactions on the L/C.

- Able support and indicate the following types of L/C:

Normal L/C

Revolving L/C

Transferable L/C

Restricted L/C

Back to back L/C

Red clause L/C

- Capture brief information on L/C, such as type of L/C, customer, application date, date of receipt of application, currency and amount of L/C.

- Book/earmark on the customer’s L/C credit line, using L/C amount in local equivalent / currency of facility, computed using prevailing counter mid rate exchange rate.

- To log the name of user who perform the registration and the date of registration in the registration record.

- Allow user to “cancel/delete” the registration record 9marked unused) with reason, should the bank decide not to proceed with the issuance transaction. Reference numbers that are’ deleted, cannot be re used.

Before Opening a L/C, the issuing bank must check the following:

- L/C application properly stamped, signature verified and margin approved and properly retained.

- Indent/ proforma/ sales contract invoice signed by the importer and indenter / supplier.

- Ensure that the relevant particulars of L/C application correspond with those stipulated in indenter / Proforma invoice.

- Validity of LCA entitlement of goods, amount etc. conforms to the L/C application.

- Conversion and rate of exchange correctly applied.

- Charges like commission, FCC, Postage, telex, SWIFT charge, if any recovered.

- Insurance cover note- in the name of issuing bank- A/C importer covering required risk and voyage route.

- Incorporation of instruction for negotiating Bank as per banks existing arrangement.

- Reimbursement instructions for reimbursing bank.

- If foreign bank confirmation is required, necessary permission should be obtained and accordingly advising bank is advised as per banks existing arrangement.

- If add confirmation is required on account of the applicant charges should be

- Recovered from the applicant

In foreign exchange banking Letter of credit (L/C) opening is an important part. L/C opening is a set of procedure which every importer needs to follow to import their products. At first importer need to contact with Exporter and with their understanding exporter prepare pro forma invoice and sent it to the importer.

After received the pro forma invoice importer present it to their bank that is known as issuing bank that prepare L/C on behalf of importer. After preparing L/C proposal need to send Head office of issuing bank for approval. After approval, issuing bank open L/C on behalf of importer, signed it by proper authority of bank officer, and send it their authorized export country bank for authentication. The process is done through SWIFT/ Telex. The bank that provides authentication then it called advising bank. After given the authentication seal- advising bank send it to the exporter bank as per requirement of invoice.

Charges of L/C opening : To open local L/C:

- Commission-

- SWIFT charge

- Stamp-

- Service charge-

- VAT

To open foreign L/C:

- Commission-

- SWIFT charge

- Stamp-

- Service charge-

- VAT

Documentation check list for L/C: To open L/C the following documents are required-

- Application of the client

- Acceptance of the terms and conditions of sanctions advice on duplicate copy.

- Copy to municipal trade license.

- IRC TIN of importer and valid registration certificate of indenter.

- Copy of registered partnership deed duly certified as true copy (in case of partnership firm)

- Copy of resolution of the partners for taking financial facilities and authorizing partner(S) for execution of documents and operation of the account (in case of partnership firm).

- Copy of memorandum and article of association of the company including certificate of incorporation duly certified by RJSC and attested by the managing director accompanied by an up- to –date list of director ( in case of limited company) in case of public limited certificate of commitment of business is to be obtained.

- Copy of board resolution of the company for taking financial facilities and authorizing directors for execution of documents and operation of the account (in case of limited company)

- An undertaking not to change the management of the company and the memorandum and the articles of

- Association of the company without prior written permission of the bank (in case of the limited company).

- Copy of the audited balance sheet for last three years(In case of limited company).

- L/C application (Stamped).

- D.P note single / joint stamped.

- Letter of arrangement.

- Letter of continuity (Stamped)

- Letter of disbursement.

- Letter of authority.

- Agreement of pledge.

- Undertaking from the client that import documents will be retired by them on the first presentation (In case no post import facility is extended)

- Marine insurance policy.

- Declaration from the importer to barer the exchange rate fluctuation.

- Letter of guarantee (stamped) of all the partners in their individual capacity (In case of a partnership firm)

- Letter of guarantee (stamped) of all the directors in their individual capacity (In case of a limited company)

- Comparative guarantee from legal entity on TK- 150 non judicial stamp if required in Head office sanction advice.

- Supplier satisfactory credit report in all cases where the amount of letter of credit exceeds TK 200000 against the proforma invoice issued directly by foreign supplier and TK 500000 against indent issued by local agent of the suppliers.

- Partnership inspection certificate if required in H.O sanction advice.

- Lien and physical possession of valid irrevocable Export L/C of the foreign buyers in favor of the client advice through our bank or any other scheduled bank of the

- Undertaking of the client that in case of failure to export the goods as per terms of export L/C they will make payment of relative import bills at maturity date from WES fund from their own sources (In case of back to back L/C

Effect payment if document in order

- Exporter and Importer sing a sales contract.

- Importer applies to a bank open an L/C in favor of the exporter.

- Issuing bank request a second bank to advice the credit.

- When satisfied with the terms of the L/C exporter is ready to ship goods.

Amendment of irrevocable L/C is not permissible without the joint consent of all the parties involved in document credit operation.

Each and every clause of the L/C can be amended provided the parties involved in the L/C consents to it. Each and every amendment of L/C must be noted in the L/C file and copies of each amendment be kept in the L/C file chronologically (date wise). The amendment may relate to-

- The amount

- The date of shipment/ negotiation

- Any other requirement of the credit.

Charges against Amendment of L/C:

- Any change except value TK 1000

- Value as well as other changes –TK 1000 + Commission (not specified)

- Only change in value- Commission (not specified)

The following types of discrepancies may be noted while the negotiating bank examines the documents:

01. L/C expired.

02. Late shipment.

03. Amount drawn in excess of the L/C

04. Bill of exchange not properly drawn.

05. Descriptions of goods differ.

06. Bill of lending or Airway Bill State.

07. Bill of landing closed.

08. Insurance cover not as per terms L/C.

09. Insurance cover obtained after the bill of landing or airway bill date.

10. Enough number of copies not submitted as required by L/C.

11. Negotiation under L/C restricted.

12. Packing list and certificate of analysis not as per the L/C.

13. Documents not properly endorsed in favor of the bank.

14. Full shipment not effective and part per shipment prohibited.

15. Gross weight and net weight shown in different documents differ.

16. Some of the documents required by L/C not submitted.

Documents with major discrepancies, which could not be negotiated, should be sent on collection basis with the permission of the exporter.

a) Advising means forwarding of a Documentary letter of credit received from the issuing bank to the beneficiary (Exporter).

b) Before advising a L/C the advising Bank must see the following:

- Signature of issuing bank officials on the L/C verified with the specimen signatures book of the said bank when L/C received.

- If the export L/C is intended to be an operative cable L/C test code on the L/C invariable be agreed and authenticated by two authorized officers.

- L/C scrutinized thoroughly complying with the requisites of concerned UCPDC provisions.

- Entry made in the L/C advising register.

- L/C advised to the beneficiary (Exporter) promptly and advising charges recovered.

Settlement means fulfillment of issuing bank in regard to affecting payment subject to satisfying the credit terms. Settlement to may be done under three separate arrangements as stipulated in the credit.

Settlement by Payment: Here the seller presents the documents to the nominated bank and the bank scrutinizes the documents. If satisfied, the nominated bank makes payment to the beneficiary.

Settlement by Acceptance: Under this arrangement, the seller submits the documents evidencing the shipment to the accepting bank (nominated by the issuing bank for acceptance) accompanied by draft down on the bank at the specified tenor. After being satisfied with the documents, the bank accepts the documents and the draft and at maturity the reimbursement will be obtained in the pre-agreed manner.

Settlement by Negotiation: This settlement procedure starts with the submission of documents by the seller to the negotiating bank. After scrutinizing the documents the negotiating bank sends the documents to the issuing bank as usual; reimbursement will be obtained in the pre-agreed manner.

The latter of credit (L/C) cancellation function shall allow user to cancel or close a latter of credit / documentary Credit.

It shall provide the following:

a) Able to allow cancellation of L/C on line for bellow conditions:

Cancel L/C based upon instruction from applicant and agreement from beneficiary. Bank charges are collected.

Cancel L/C with remaining small outstanding balance from L/C negotiation(S).

Cancel before L/C expiry date.

Cancel L/C due to error correction. The error correction cancellation can only be performed if the L/C is recently issued L/C (L/C on the same day), and has no negotiations / drawings yet.

b) Able to refund cash margin deposit and credit customer’s current account at time of on- line cancellation. System shall prompt a massage to inform the users, if there is any outstanding L/C margin deposit pending refund to the customer.

c) To update credit line utilization and reinstate unutilized credit balance after approval of L/C cancellation.

d) To automatically default / calculate charges as stated in the ‘ charges’ section , at selling exchange rate (if applicable).

e) To debit customer’s current account for the charges (if any).

f) To automatically generate GL entries for reversals of liabilities, charges, refund margin deposit and payments, as stated in the ‘GL Entries’ section.

Charges against cancellation of L/C: PBL limited charges TK 500/- for cancellation of L/C.

Auto –cancellation of a L/C: The system will automatically close / cancel L/C that has expired, allowed to be auto canceled by the system and after lapse of the bank specified grace period (30 days after expiry date) and only if the ‘Auto cancel’ indicator is turned on for L/C.

It shall provide the following:

- Set the outstanding balance of L/C to zero and status of L/C as ‘Closed’ in L/C Master Record.

- To update credit line utilization and reinstate unutilized credit balance upon L/C cancellation.

- To automatically generate GL entries for reversals of liabilities as stated in ‘GL Entries’ section.

- Create a history record for each L/C cancellation performed by system.

- Report the auto- canceled L/C in the Daily Transaction Activity list.

Documents : This is most sensitive task of the import department. The officials have to be very much careful while making payments.

Date of payments: Usually payment is made within 90,120 or 180 days (must be specified) after the documents have been received. If the payment is become deferred, the negotiating bank may claim interest for making delay.

Preparing sale Memo: A sale memo is made at BC rate to the customer. As the TT & DD rate is paid to the ID, The difference between these two rates is exchange trading. Finally, an inter Branch Exchange Trading credit advice is sent to ID.

Requisition for the foreign currency: For arranging necessary fund for payment, a requisition is sent to the international department.

In simple terms, a documentary credit is a conditional bank undertaking a payment. Expressed more fully, it is a written undertaking by a bank (issuing bank) given to seller (Beneficiary) at the request, and in accordance with the instruction of the buyer (applicant) to effect payment (that is, by making a payment, or accepting or negotiating bill of exchange) up to a stated sum of money

Within a prescribed time limit and against stipulated documents. The customary clauses contain in a L/C are the followings:

- A clause authorizing the beneficiary to draw bills of exchange up to certain on the opener.

- List of shipping documents, which are to accompany the bills.

- Description of the goods to be shipped.

- An undertaking by the opening bank that bills drawn in accordance with the conditions will the dully honored.

- Instructs to the negotiating banks for obtaining reimbursement of payments under the credit.

Liability of Issuing Bank : As per Article 9(A) of UCPDC 500, an irrevocable credit constitutes a definite undertaking of the issuing bank. Provided that the stipulated documents comply with the terms and conditions of the credit .

Adding Confirmation: The confirming bank does adding confirmation. Confirming bank is a bank that adds its confirmation to the credits and it is done at the request of the issuing bank. The advising bank usually does not do it if there is not a prior arrangement with the issuing bank. By being involved as a conforming agent the advising bank undertakes to negotiate beneficiary’s bill without recourse to him

- Issue L/C and request to add confirmation.

- Review the L/C terms.

- Provide reimbursement.

- Drafts to be drawn on L/C opening bank.

- Availability of credit facilities.

- Line allocation from the business and ownership units in the importer’s country.

- Confirm and advise L/C.

It is the responsibility of A/D branch to make proper scrutiny and examination of import documents to ensure that.

- Full set of document as stipulated in the credit had been received.

- The document has been drawn strictly as per L/C terms.

- The document is in order not discrepant.

Scrutiny and examination of import documents is very vital and important. FEB keeps a record of their checking on the negotiating bank’s bill forwarding schedule with a rubber stamp notation “Documents checked and found correct” duly authenticated by the respective officer.

Checking of import documents:

Import documents are checked thoroughly and some specific points receive crucial attention that delineated below:

- The Letter of Transmittal

- It must be addressed to L/C issuing bank

- It has ac current date.

- It relates to current Documentary number credit of the bank.

- The documents enumerated are attached.

- The value of documents and the value mentioned in the cover letter are same etc.

- The Documentary Credit

- It is the correct referenced Documentary Credit

- It is still valid that nit not expired or cancelled.

- Available balance in tit is sufficient to cover value of drawing etc.

- Bill of Exchange

a) The draft bears the correct L/C number.

b) The name of the drawer corresponds with the name of the beneficiary

c) It is drawn on the correct drawer indicated in the L/C

d) Amount in words agrees with the amount in figures.

e) The beneficiary as duly signed the draft.

f) The tenor is as required by the credit.

g) The value of draft and the value of invoice are identical.

- Commercial Invoice

a) Beneficiary as stated in documentary credit issues it.

b) The description of gods. Value and unit price matches that stated in

c) Credit as regards to the amount and currency.

d) Value of invoice does not exceed the available balance of the credit

e) The invoice is signed as required in the credit.

f) The correct number of original copies is presented.

g) The terms of delivery match with the terms of credit.

h) In case of partial shipment, the invoice amount corresponds

Proportionally to the dispatched quantity etc.

- Marine Bill of Lading

a) The shipping company must issue it.

b) Full sets of originals issued and presented.

c) The consignee’s name and address are correct as mentioned in the credit.

d) The bill of lading bears issuing date, duly signed by the issuer and the name of ship papers.

e) The port of departure and port of destination are correct.

f) The bill of lading bears the “on board shipped” notation.

g) It is correctly marked Freight prepaid of Freight to collect.

h) The goods are consigned as stipulated in the credit

- Airway Bill

The consignee’s name and address and the airport of departure and destination are stated in the Airway bill are consistent and in agreement with the terms of credit.

a) The documents indicated the name of the carrier.

b) The issuer is the carrier or a named agent of the named carrier.

c) The airway bill indicates the actual flight date and flight number

d) The documents are signed by the courier.

e) The consignee’s name and address and notify party’s name address are correct.

f) It is correctly marked “Freight prepaid” of “Freight collect” etc.

g) The consignor’s copy is being presented.

- Certificate of Origin

a) The country of origin of the goods as stated in the certificate agrees with the terms of the credit.

b) The certificate has been signed as required by the credit.

c) The certificate has been authenticated by the stipulated authorities.

- Packing List

a) It is unique a document and not combined with any other documents.

b) The list contains all necessary information especially concerning the packing units.

c) The data on it is consistent with that of the other documents

After scrutiny of import document if the above mentioned points are found in order ad drawn as per credit terms, A/D branch shall make lodgment of documents.

- Pre-shipment inspection:

To ensure the qualities of imported goods and to become sure that imported goods are not radioactive pre-shipment inspection are performed by some government approved PSI Company. For different block different PSI Company works.

Block A # ITS-Interlake Testing Service.

Country includes China and Europe.

Block B # Inspectorate Griffith.

Country includes India, Spelunker, Bhutan, Nepal, Myanmar, Malaysia, Singapore, Thailand and south East Asia.

Block C # Bureau Varieties International

Country includes, Indonesia Japan, Korea, Taiwan, Indonesia, Pakistan, Australia, and New Zealand, UAS, Meddle East.

PSI not required for items such items include Dyes, Capital machinery, Poultry feed, Drug and medicine (They require manufacture and expiry date) Fruits, Computer accessories, Surgical equipment, Food items (They require certificate that is provided by chamber of commerce and industry of exported.

During the year the bank handled export business worth tk. 33909.78 million. During the previous year the amount was tk. 24739.65 million. The amount of import business handled by the bank increased by tk. 9170.13 cores during the year which was 37.07% higher than the previous year.

Key Performance of Export

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| BDT in Million | 17701.80 | 19907.50 | 24795.65 | 24739.65 | 33909.78 |

Table 4.2: Key Performance of Export

Export of PBL

- Procedure for registration of Exporter.

- Book and resister ledger required for export;

- Export L/C checking and advising;

- Formalities of back to back L/C opening;

- Accounting of back to back L/C;

- B.B bill checking / Lodgment;

- Mechanism of acceptance;

- Pre-shipment financing;

- Export document checking and negotiation under reserve/ collection basis;

- Calculation of offering sheet for fund disbursement system;

- Proceeds realization correspondents;

- Formalities of back to back payments system;

- Substitute benefits realization / collection system;

- EXP from reporting to Bangladesh bank;

- Disposal of EXP form;

- Export incentives;

- Disputes and settlement of export claim.

For obtaining export registration certificate (ERC) from the CCI & E, the following documents are required:

- Application form

- Nationality certificate

- Partnership deed (registered)

- Memorandum & Articles of association and incorporation certificate.

- Bank corticated.

- Income tax certificate

- Valid trade license

On receipt of export L/C it is to be recorded in the banks inward resister and then the signature on the L/C or test number for telex L/C is to be verified by an authorized officer or a bank and finally it is to be forwarded to the beneficiary under forwarding schedule.

- Back – to –back L/C is a secondary L/C opened by the advising bank in favor of domestic / foreign supplier on the basis of an export L/C. Back – to – back L/C opened for procurement of raw materials / finished goods for execution of shipment order. The beneficiary of back – to –back L/C is generally paid on negotiation of the final documents submitted by the exporter.

- Although BB L/C is normally opened at nil margin but Brach may ask for margin and collateral security or new clients or special cases.

- The following points will be considered for allowing BB L/C-

- Only recognized units of readymade garments, specialized Textiles under bonded warehouse system will be extended BBLC facility. Therefore Branch must satisfy that the client has a valid bonded warehouse license.

- The genuineness of the export L/C must be valid with the advising bank.

- The validity of the export L/C will be for a reasonable time so that after receiving of goods under BB L/C may be processed / manufacture red comfortably keeping in view the validity of shipments period of muster L/C and production capacity of the factory.

- The value addition by the exporter will be at least 80% of the net FOB value of the export L/C (in some cases 75% are also allowed, subject to Bangladesh bank restrictions). FOB value is calculated by deducting freight charges, insurance, commission involved in shipment of the merchandise under the export L/C.

- The import L/C will be opened on usence basis covering usence of not more than 180 days or as prescribe by Bangladesh bank from time to time.

- Interest on essence period shall not exceed LIBOR or the prevailing rate of interest of supplier’s country or as may be prescribed by Bangladesh Bank from time to time.

- All amendments of the export L/C should be noted down carefully to rule out the change of excess L/C obligation under import L/C.

- Opening of import L/C against export L/C under Barter should not be allowed without prior permission of Head Office.

- In cases, where pre- shipment inspection certificate is required international recognized agencies should be nominated by name to carry out the pre- shipment inspection and the same should be stipulated in the L/C, as on clause of the L/C.

- Valid import registration certificate (IRC) & export registration certificate (ERC)

- L/C application & LCA form duly filled in signed.

- Performa invoice or indent.

- Insurance cover note with money receipt.

- IMP form duly signed.

- Full particulars of bank account.

- Balance sheet.

- Statement of assets and liabilities.

- Trade license.

- Valid bonded ware house license.

- Membership certificate.

- Income tax declaration.

- Memorandum of articles.

- Partnership deeds.

- Resolution.

- Photographs (all directors)

On receipt of above documents and papers the back to back L/C opening section will prepare a credit report. Branch must obtain sanction from head office for opening BB L/C.

Processing and Opening of Back- to – Back Letter Of Credit: Bank will supply the following papers / documents for opening back to back L/C

- L/C application form;

- LCA form;

- IMP form;

- Charge documents;

The above paper must be completed and signed by the party will verified the signature.

For opening L/C the client is to submit to the bank an application in the printed format of the designed bank which is also an agreement between the importer and the bank. The form is to be stamped under the stamp act. In force in Bangladesh. The importer must submit the LCAF, IMP insurance cover note and indent/ contract/ purchase order/ proforma invoice (duly accepted by the importer) or more whenever required.

The L/C application must be completed / filled in and signed by the authorized person of the importer giving the following particulars-

- Full name and address of the suppliers or beneficiary or importer;

- Brief description of the goods;

- L/C amount (CFR value) which must not exceed the LCAF value;

- The unit price, quantity, quality of the goods;

- Origin of the goods, port of loading, and port of destination must be mentioned.

- Mode of shipment;

- Last date of shipment and negotiation time;

- Insurance cover note number and name of the company;

- Tenor of draft;

- Mode of advising L/C;

- Whether shipment / transshipment is allowed;

- Instruction to add confirmation if required;

- LCAF number;

- Export L/C number and date;

- Any other relevant information and instructions if any must be mentioned in the L/C application form.

Procedure: An exporter desires to have an import L/C limit under back to back arrangement, must have apply to designed bank and in prescribed forms for sanction for opening back to back L/C. In that case the following information’s are to be furnished by the applicant:

- Full particulars of bank account.

- Type of business, in case of limited company, balance sheet of last three years and name of directors.

- Historical background.

- Amount of limit required.

- Terms of payments.

- Goods to be imported.

- Security to be offered.

- Repayment schedule and source of fund.

- Other liabilities of the customer with the bank.

- Statement of assets and liabilities.

- Trade license.

- Membership certificate.

- Income tax declaration with TIN.

- Memorandum of articles.

- Registered partnership deed (if partnership firm)

- Resolution.

- Photographs.

On receipt of above particulars and papers, the back to back L/C opening section of the bank will prepare a credit report of the concerned importer / exporter. The report should be collected from their previous bank if any.Banks prepared a credit report in prescribed forms. Bankers have to make inquiries from those if their customers and other peoples and inquired the report by the banker. Sometime information’s are gathered by deputing marketing officers or credit officers.On receipt of above information, the designated branch must obtain a sanction from Head Office for opening back to back L/C.n all cases the sanction must be informed to the importer for acceptance. On security conformation from the client that the terms and conditions of the sanctioned are acceptable, the subsequent documentation / charge documents are taken up.

When the document is arrived, the following vouchers are passed:

Customer’s A/C Dr.

Commission on Acceptance Cr.

While payment, if the fund is at hand, the accounting entry is-

Sundry deposit margin on acceptance Dr.

Customer’s A/C Cr.

Under the back to back concept, the seller, as beneficiary of the credit, offer it as security to the advising bank for the issuance of the second credit. As application for this second credit the seller is responsible for reimbursing the bank for payment made under it regardless of whether or not be paid under the first credit. There is, however for the bank to issue the second credit, and in fact, many banks will not do so.

- Clause (Unclean) bill of landing;

- Charter – party bill of landing (Unless stipulated in the L/C);

- ON BOARD notion of bill of landing undated / unauthenticated;

- Shipment effected from port other than that stipulated in the credit;

- Goods ship on desk (unless stipulated in L/C)

- Full set of bill of landing not presented;

- Certificate of country of origin not provided;

- Certificate notifying insurance company of shipment not presented

- Cutting alteration in documents not authenticated;

- Document consistent with each other;

- Documents of goods on invoice differ from that in the credit;

- Weights differ between documents;

- The amount shown in invoice and bill of exchange differ;

- Shipping marks and number differ between documents;

- Credit L/C amount exceeded;

- Document not presented in time / sale bill of lading;

- Late shipment;

- Short shipment;

- Bill of exchange drawn on a wrong party;

- Bill of exchange payable on an indenter minable date;

- Bill of landing , insurance documents or bill of exchange are not endorsed correctly;

- Absence of signature, where required on documents presented;

- Bill of landing does not evidence whether freight is paid or not;

- Packing list not submitted;

- Part shipment/ transshipment effected not being covered by the L/C terms;

- Notifying party differs/ not as per L/C stipulated;

- Third party bill of landing / short form bill of landing submitted;

- Inspection certificate not submitted;

- Unit price not mentioned in invoice;

- Description of documents on collection schedule differs with documents presented;

- Fumigation / Health certificate (Fit for human consumption) not submitted;

- Forwarder’s cargo receipt not acceptable (Unless provided the L/C);

- Shipment before L/C opening;

Discrepancy Charge:

For local L/C discrepancy charge is $ 30

And for foreign discrepancy charge is $ 50 + telex charge $30

Detective points or clauses appear in the master L/C:

- Issuing bank is not reputed.

- Advising credit by the advising bank without authentication.

- Port of destination absent.

- Inspection clause.

- Nomination of specific shipping/ Airline or nomination of specified vessel by subsequent amendment.

- B/L to blank endorse, to third bank, to be endorsed to buyer or third party.

- No specific reimbursing clause.

- UCP clause not mentioned.

- Shipment / presentation period is not sufficient.

- Original document to be to buyer or nominated agent.

- FCR or HAWB consigned to applicant or buyer.

- Shippers load and count is acceptable.

- L/C shall expire in the country of the issuing bank.

- Negotiation is restricted.

After realization of master L/C payment, BB L/C payment may be made. So, BB L/C amount for payment is kept on head named sundry account FCBP AR. After period, payment is given from sundry account FCBP AR. When payment is given reverse the contra voucher.

Debit: Banker liability on L/C BTB

Credit: Customer liability on L/C BTB

Bank will earn acceptance charge for BB L/C, such as-

Income account acceptance charge on BTB is-

= 0.60% on foreign BTB L/C amount.

= 0.50% on local BTB L/C amount

Local BTB L/C payment is given to the beneficiary bank by issuing demand draft/ pay order in favor of them.

In case of back to back as 60 – 90 – 120 – 180 days of maturity period, deferred payment is made. Payment is given after realizing export proceeds from the L/C issuing bank.

Negotiating of local back to back letter of credit : PBL negotiates local BTB L/C and make payment to the party after realization. After dispatching of goods to the buyer, seller comes to the bank with proper evidence of dispatching. If documents are in order then PBL. Kill, put LDBC (Local bill for collection) and number from LDBC resister and lit the same time given entry on the LDBC resister. Then these documents are sent to the opening bank of BTB L/C for making payment in favor of PBL. If the delay for paying, negotiating bank sends a reminder letter to them for realizing payment of BTB L/C. If party needs immediate payment, then PBL purchase these documents and gives LDBP seal and number form tile LDBP register and gives entry on the resister. In that time, full amount of the local BTB L/C is not paid to the party. It is taken some amount for margin. So, margin is BTB L/C amount paid to tile party. Margin is kept for adjusting interest on LDBP. Here, bank earns commission. After realizing the BTB L/C bills, interest is calculated on the basis of amount paid. Interest is calculated from the date of amount paid to tile date of one day before of realizing date. Interest is deducted from the margin amount and the rest of the margin amount is credit to the party account.

Advising of local back to back letter of credit: PBL advise document of local BTB L/C at the payment of charge TK-500/-the purpose of buying their accessories. The government organization then buys their accessories from local supplier by issuing a BB L/C again the foreign L/C. In this case, after supplying tile goods to the tile government organization, party come in PBL, with tile evidence of dispatching goods and request for realizing payment of this L/C then. Tile bank gives LFDBC seal and number from the register on the documents and marks entry on tile resister. These documents are sends to the foreign bank that is authorized for payment. After realizing payment, party is supposed to take their payment. Bank can purchase these documents as LDBP but, here it will be LFDBP (Local foreign documents bills purchase).

Convertibility of Taka in current account transactions symbolized a turning point in the country’s exchange management and exchange rate system. Now the operation of foreign currency accounts has been more liberalized. Funds from these accounts are freely remittable to any country according to the needs of A/c holders.

Authorized Dealer remittance means purchase and sale of freely convertible Foreign Currencies as permissible by the rules and regulations of Exchange Control Authority of Bangladesh Bank.

Remittance takes place in two types:

i) Inward remittance

ii) Outward remittance

The term “Inward Remittance” includes not only remittances by TT, MT, Draft etc. but also purchases of bills and traveler’s cheques.

Generally, Inward remittance comprises:

a) Remittance received by Drafts

b) Remittance received by mail transfer

c) Remittance received by telegraphic transfer

d) Purchase of bills & travelers cheques

Remittance equivalent to USD 2,000 and above should be reported on “Form – C” therefore, after receipt of Inward remittance of USD 2,000 or above or equivalent, the A/D Branches, before

disbursement of the same shall obtain declaration from the beneficiary in a prescribed form “Form C”.

But declaration in “Form-C” will not be required by the beneficiary against any remittance sent by Bangladesh national working abroad which meant for family maintenance. “Form-C” is required when remittance comes from abroad in the name of Firms, Companies, and NGO’s etc.

Remittance received against export should be certified and reported on EXP Forms, In case of remittance received in advance for exports, the A/D should obtain a signed declaration from the beneficiary on the back of the Advance Receipt Voucher certifying the purpose of remittance.

It may be mentioned here that Inward Remittance received through DD/MT/TT/TC should be reported on “Form-C”. Remittance received against exports should be certified and reported on EXP Form.

There are three types of such accounts:

a) FC accounts

b) Resident Foreign Currency Deposit Account

c) Non-resident Foreign Currency Deposit Account

The Bangladesh Nations working abroad may maintain F.C. Account & brought Foreign Currency at the time of their return to Bangladesh. These accounts are termed as Resident Foreign Currency Deposits A/c.

One person can bring into Bangladesh for USD 3,000/- or above has been duly declared by them to the custom on Form FMJ at the time of arrival can be credited to F.C A/c or be encased in Bangladesh Taka within 30 days of arrival ( F.E. circular No.05 dated 04.02

Remittance from our country to foreign countries is called outward foreign remittance. The Authorized Dealer on behalf of Bangladesh Bank approves outward remittance. Only a few remittances of special nature require Bangladesh Bank’s prior approval. Any person who wishes to purchase foreign exchange must lodge an application for the purpose on a prescribed Form with the authorized Dealer Branch. There are two types of application forms for outward remittances – “IMP Form” and “T/M Form”.

a) The IMP form is designed to cover remittances for payment of import obligation.

b) T/M form is designed to cover all other types of remittances other than Imports.

- Outward remittance may be made for following purposes:

a) Travel

b) Medical Treatment

c) Educational purpose

d) Attending seminar etc.

e) Balance amount of F,C. A/c

f) Profit of foreign companies

g) Technical assistance

h) New exporters up to USD 6,000/- for business promotion

I) F.C. remittance can be made for fare, exhibition from Export Retention Quota.

- Outward remittance in favor of beneficiaries outside Bangladesh may be made in any of the following manners:

a) By issuing Demand Draft

b) By issuing Mail Transfer

c) By issuing Telegraphic Transfer

- Excluding payment of import obligation some commercial remittances may take place in the form or DD/MT/TT for under noted cases:

I) Remittance or Dividend to non-resident shareholders

ii) Remittance of profit of foreign firms and companies.

iii) Remittance for import of Books and Journals

iv) Remittance of pre-shipment inspection fees etc.

1 | Purchase of Foreign Check/Drafts/TCS | a) Tk 0.30 per USD b) Tk. 0.40 per GBP c) In all other currency as per USD Minimum Tk.200/= + P&T Tk.100/= |

2 | Payment of any foreign Taka drafts which are drawn on our Bank (This shall include payment in cash account or by clearing) | –Free- |

3 | a) Disbursement of Inward remittances at our counter FTT-FDD | Handling charge Tk.100/= up t Tk.20,000/=, Tk.200/= above Tk.20,000/- |

| b) If payment of remittances to the beneficiary made by DD , MT or TT | Charge at actual as per rule plus P&T Tk.200/= above Tk.20,000/-+ P&T | |

4 | Collection of foreign currency draft/instrument from other Local bank | Tk.100/= per instrument |

5 | Collection of foreign currency draft from abroad | Foreign Bank charge + handling charge Tk.200/= Plus P & T |

6 | Encashment of any foreign currency at our counter | Tk.100/= per instrument/case |

7 | Encashment of any TT at our counter in F.C | Tk.100/= per TT |

8 | Transactions by Nominee/Account holder in F.C. A/cs | Tk.100/= per instrument/Trans |

9 | Issuance of Foreign Currency drafts on foreign correspondents or favoring Local Bank | a)Tk.200/=Non Commercial/individual b) Tk.500/= up to USD 5,000/- Tk.1,000/= above USD 5,000/- or eqvt. Commercial + SWIFT Charge + F.Bank Charges if any |

10 | Transfer of L/C authorization form to other Bank | Tk.500/=flat |

11 | Delivery order (D/O) charge (Bank’s and Party’s Go down) | Tk.100/= per delivery order |

12 | Opening of student file | Minimum Tk.3,000/- + actual charge for opening, subsequent charge Tk.2,000/= |

Chapter 05

Conclusion and Recommendation

It can be conclude that, since 1983, the Government of Peoples Republic of Bangladesh started taking ownership reform measures in financial sector. Two out of six NCBs were denationalized and a number of private commercial Banks (PCBs) were allowed to operate by the government. It results competition and improves the level of customer services operation efficiency of the Banking sector. As a result of this competition peoples are favoring a lot, Banking services are improved, employments are generated and public money earns more and more securities and benefits which ultimately developing economy as a whole.

It is also to be stated that this competition is not confined within the country. Due to high fuel cost and relatively lowers technological use made us competitive in the world economy. But we are in a state of consistent in economic sector maintaining on an average five (05%) percent of GDP growth. This constant growth results in high-tech introduction and positive competitive environment in financial sector especially within financial intermediaries (Banks). Introduction of high-tech services can ensure growth towards first generation Bank like Pubali Bank Ltd.

Bank always contributes towards the economic development of a country. PBL, compared with other banks are contributing more by investing most of their funds in fruitful projects leading to increase in production. It is obvious that right thinking of this bank including establishing a successful network over the country and increasing resources, will be able to play a considerable role in the portfolio of development financing in the developing country like ours.

PBL continues to play its’ leading role in socio-economic development of the country as a companion of Independent Bangladesh. Besides its’ traditional function such as deposit mobilization, deployment of fund in trade, commerce, industry, agriculture, import & export business, outward and inward remittance, as an agent of Bangladesh Bank, PBL has emerged as the pioneer of playing key role in the country.