1.0 Introduction

1.1Objectives

Some basic objective has encourages us to study the topics and to prepare this term paper. They are:

- To learn the basic concept about the international liquidity and monetary system.

- To Study the Sources of International Liquidity and Role of IMF

- To Know the Criticism of Liquidity

- To Identify the Concept and Uses of SDR, and Valuation and Allocation of

SDRs.

- To know the meaning and scope of Euro dollar market.

- To learn the important features of the market.

- To explain the weather Euro dollar market is tonic or poison

1.2Scope

Bangladesh is developing country. Its economic condition is not good. So in that case by making this project we can learn the overall world liquidity and monetary system which help us to compare between Bangladesh and other countries monetary system. We also can know determination of exchange rate.

1.3Methodology

To prepare this term paper, standard methods of term paper writing have been used. For making this term paper different types of data were needed to complete. The required data were collected by using both primary sources & secondary sources.

For collecting data from secondary sources, go through various web sites. After completion of the data, these were sorted into different categories. Another secondary sources is that , we have collected some data from our text book.

Chapter 2

2.0 International liquidity:

2.1Preamble

International liquidity refers to the resources that are available to monetary authorities of countries for the purpose of meeting balance of payments deficits. Countries, like companies and individuals, need a sufficient supply of liquidity if they are to conduct their affairs in an orderly and planned way. The topic of international liquidity assumed greater significance because of the fact that during the past three decades the growth in the international reserves did not keep pace with the increase in the volume of international trade. Too little liquidity will impede the global growth of trade and a. surfeit of it will fuel inflation. Hence the need for along term strategy for estimating the liquidity needs of the world economy and arranging for its provisions at just adequate levels. Here it would be pertinent to differentiate between international reserves and international liquidity. International reserves have been defined as those assets of monetary

authorities that can be used, directly or through assured convertibility into other assets, when a country’s external payments are in deficit. from IMF and commercial credit..

2.2Adequacy of Liquidity

a) IMF Quotas:

The IMF quota increase has lagged behind with the increase in world trade. As a consequence, over the years, the IMF quotas have declined relative to world trade. From about 16% of world Imports in 1945, the IMF quotas fen about 10% in 1970and further to 4% in 1983. This is partly due to inhibitions nurtured in increasing the quotas at a faster rate. The Eighth Review of Quotas yielded an increase of47.5% as against an increase of 100 to 125% considered necessary by Technical Studies conducted on the eve of the Review. The other disturbing factor is that the distribution of quotas between developed and developing countries are not satisfactory. The basis of allocation of quotas largely reflects the situation immediately after the Second World War. Even after the lapse of a period of more than four decades, the basis of allocation has not changed to any substantial extent. Adding to its already learning towards developed countries, the adjustments made during the Eighth Review of Quotas have hit hard the developing countries.

b) Special Drawing Rights

Contrary to expectations, the share of the SDRs In the official reserves has-been showing a declining trend. The decline is from little over 4.1% at the end of1973 to less than 3% by 1983.Pleadings by developing countries for a large-scale increase in SDR allocation have been turned down largely due to opposition by developed countries. The contention of the developed countries opposing the increase is that it would lead to International l Business inflation. The developing countries point out that the argument is ill-founded.

(c) General Arrangements to Borrow

The condition that IMF can make use of the funds under GAB to finance a nonparticipant only in case the situation threatens the stability of the international monetary system puts a serve restraint on the use of funds making it discriminatory in the sense that it is available to a few members and not to others.GAB is at the most a poor substitute for quota increase. If they have to serve useful purpose, like other resources borrowed by IMF from its members, they should be available to all members on equal terms as normal supplement to IMF resources.

(d) Lending facilities

As compared with the conditional landings, the unconditional landings are limited. While there is a general agreement on the need for certain conditionality’s to go with the facilities, the dispute is over the nature of the conditions attached to IMF loans. Since there is no single solution to problems faced by deficit countries,

the conditions cannot be rigid and same for every case. Therefore, the IMF’s guidelines on conditionality are sufficiently general to leave room for substantial discretion in individual lending circumstances. The criticism leveled against the conditionality’s attached to IMF loans is that they are based on short-term consideration and are too rigid on monetary and fiscal International Business targets to be achieved by the borrowing country. The developing countries, lacking infrastructure, cannot bring about the changes in a short period.

2.4Objectives of IMF

The four main objectives of the fund are as follows:

To help member nations tide over their balance of payment difficulties of short term and long-term character.

To promote exchange rate stability and avoid competitive exchange rate depreciation.

To reestablished multilateral trade among the member countries, and

To move in the direction of dismantling trade and tariff barrier which separate the member countries through tariff, quotas etc.

2.5Other sources of Liquidity

World Bank and its affiliates along with other development banks provide the rest of the official international liquidity. These institutions are studied in separate chapter. By far the most important source of liquidity for the developing countries, exceeding the official sources, has been the International capital markets.

SDR:

The Special Drawing Right (SDR) is an international reserve asset created by the Fund, taking into account of the global need to supplement existing reserves and it represents a major innovation of the IMF to help alleviate the problem of international liquidity. It is the declared intention of member countries that the SDR should eventually become the principal reserve asset in the international monetary system. The IMF has two accounts of operation. First, there is General Account of the Fund through which all its business in national currencies is conducted. This reflects the currency holdings coming from its members. Since, the Fund’s International Business Inception, the Quota Contributions and the Purchase and Sale of these Currencies are under the Arrangements in Force. Second, there is the Special Drawing Account through which all operations and transactions in SDRs are conducted. The SDR is essentially only an entry in this account at the Fund. Moreover, it is an entry which. may be held only by (a) national monetary authorities (who must be

members of the Fund) and (b) by the General Account of the Fund to which participant countries are permitted to transfer SDRs for certain spec1ftedpurposes,for example, to pay charges levied by the Fund or to repay drawings from the General Account. It is apparent, then, that the SDR is really created in the sense that it is defined equivalent in foreign exchange from other members, and that it discharges specified obligations of members towards the Fund’s General Account. Every member of the IMF has the right to become a participant of the SDR facility, but every member is not obliged to join the facility. Obviously, only Members of the IMF can participate in SDR facility. The Special Drawing Right, as mentioned above, is only a book entry in the “Special Drawing Account” of the IMF. The allocation of SDR takes the form of a credit entry in the name of the participating countries in the Special Drawing Account.

2.6Problem of Inadequacy

The sum total of international reserves of all nations, Participating in the world monetary system , is called international liquidity. The international reserves of a single country, are also referred to as its international liquidity . For reasons of clarity, it may be useful to call the latter as ‘foreign reserves’ and the former as international liquidity.

If all the countries of world had balance of payments equilibrium at all time, then there would be no problem of international liquidity. Similarly, there would be no world liquidity problem or shortage if all the national currencies were freely convertible and international acceptable on a universal scale.

Why is there a world liquidity shortage in today’s world? Basically, there are two reasons. First, a vast majority of the less developed countries of the third world have been running persistently high and growing deficits in their balance of payments. Their problem of payment deficits, has been aggravated by international price escalations in recent years. The overall payment deficits of the non-oil exporting countries of the third world has risen from US $12 billion in1973 to $45 billion in 1975 and since then as well. Secondly, the surplus nations particularly of the advantage industrial world consisting of countries like Germany, Japan and so forth , have shown little or no interest in taking policy measures to get rid of their surpluses in balance payment .

The rich counties might argue that the poor countries have created their own problem of international liquidity shortage .They can attribute this to the general mismanagement in the poor countries , the government in these countries living beyond their means , unproductive and wasteful expenditure, over ambitious social and economic goals , trying to do too many things too fast too meet the challenges of the revelation of rising expectation of this people and dozens of things of this kind .

From the less developed countries point of view however the international liquidity problem takes on a different color. They belief that if their payment deficit are not bridged in a mutually acceptable way then everybody will suffer-the poor and the rich countries.

2.7Problem solution

Then what are the ways of solving the problem of world , could liquidity shortage ?If we have correctly identify the problem in hand ,we can suggest appropriate measure. The world liquidity problem, can be solved by adopting the following measures:

a) The non –essential imports, however they are define ,could and should be cut down. Import-substitution could be carried to a point beyond which it turns out to be in efficient causing miss-allocation of economic resource of the country.

b) The surplus countries should try to reduce their balance payment surpluses. This can be done in one of the two ways or a combination of both. 1) accepting payment in terms of the national currencies of the deficit countries with which the country have balance of trade surplus.2) surplus countries should fascinated the export goods and service.

Chapter 3

3.0The World Monetary System:

3.1 Preamble

The monetary system of the country cannot function in isolation. in the someway that no man can live in isolation able there is a need for an international monetary system which brings together the national monetary system and facilitates their harmonious functioning. Such a system should:

a) facilitate international trade and capital movement by ensuring that international payments can, be made easily;

b) provide for mechanism for adjustments of balance of payments fluctuations;

c) ensure stability of exchange rates among the currencies;

d) respect the individual national policies and not interfere with the domestic

affairs of the nations. Different systems of monetary management have been tried over the years to achieve the above objectives. Each system was evolved out of and was compatible with the economic and political conditions that prevailed at that time. In the beginning of the present century we had the gold standard was replaced by the fixed parity system under International Monetary Fund. Which functioned well for about 25 years. The early 1970s saw the collapse of the fixed rate regime giving way to the present era of floating rates.

3.2The Eurodollar Market

The growth of the Eurodollar market is one of the significant developments in the international economic sphere after the Second World War. But its phenomenal development, though poses problems for national monetary authorities and international trade, transitional corporations and the economies of certain countries. Recent1y, it has been proposed that India should evil itself of Eurocurrency credit to accelerate her economic growth. International Business

3.3Meaning and Scope

In a narrow sense, Eurodollars are financial assets and liabilities denominated in US dollars but traded in Europe. True the US dollars still dominates the market and most of the transactions are still conducted in the money markets of Europe especially London. But, today, the scope of the market stretches far beyond European the sense that Eurodollars transactions are held also in money markets refers than European and currencies other than the US dollar. Interpreted in a wider sense, the Eurodollar market refers to transactions in a currency deposited outside the country of its issue. “Thus, any currency internationally supplied and demanded and in which a foreign bank is willing to accept liabilities and loan assets is eligible to become a Eurocurrency”, Interpreted this way, dollar deposits with banks in Montreal. Toronto. Singapore. Beirut. etc., are Eurodollars; so are the deposits denominated in European currencies in the money markets of the USA and the above centers. It is evident, therefore, that the term Eurodollar is misnomer. “Foreign currency market” would be the appropriate term to describe this expanding market. The term Eurodollar came to be used because the market had its origin and earlier development with dollar transactions in the European money markets. But despite the emergence of other

currencies and the expansion of the market to other areas, Europe and the dollar still hold the key to the market. Today, the term Eurocurrency market is in popular use.

3.4Important features of the market

The important characteristics of the Eurocurrency market are:

i) By its very nature, the’ Eurodollar market is outside the direct control of any national monetary policy. “It is aptly said that the dollar deposits in London are outside United States’ control because they are’ in London and outside British control because they are in dollar.” The growth of the market owes a great deal to the fact that it is outside the control of any national authority.

II) “It is a short-term money market

The deposits in the market range in maturity from one day to several months, and interest is paid on all of them. Although some Eurodollar deposits have a maturity of over one year. Eurodollar deposits are predominantly a short-term instrument.”The Eurodollar market is viewed in most discussions more as a credit market in dollar bank loans-and as an important accessory to the Euro pond market” Eurodollar loans are employed for longer term loans. Eurobonds developed out of the Eurodollar market to provide longer-term loans that was usual with Eurodollars. These bonds are usually Issued by a consortium of bank and issuing houses.

iii) It is a wholesale market

The Eurodollar market is a wholesale market in the sense that the Eurodollars’ a currency dealt only in large units. The size of an individual transaction is usually $ 1 million.

iv) It is a resilient market

Its efficiency and competitiveness are reflected in its growth and expansion. The resilience of the Eurodollar market is reflected in the responsiveness of the supply of, and demand for, funds to changes in the interest rates and vice versa. Otherwise would have been. Without these controls, much of the market’s activity would instead be carried on In the New York money market.”

vi) Innovative Banking

The advent of innovating banking, spearheaded by the American banks In Europe and the willingness of the banks in the market to operate on a narrow spread also encouraged the growth of the Euro market.

vii) Supply of Petro-Dollars

The flow of petro-dollars, facilitated by the tremendous Increase in OPEC’s oil revenue following the frequent hikes in oil prices since 1973, has been a significant factor in the growth of the Eurodollar market In the last one decade. ‘There is a wide array of reasons pointing to a continued high demand for Euro credit. In order to cover these extensive credit needs, Euro-banks will however, require an increasing flow of deposits. One source that may well quash forth in the coming years would be the ‘surplus oil Income of OPEC oil members.”

Chapter 4

4.o Bangladesh Perspective:

4.1Foreign Exchange Market

Foreign exchange Market is a place in which foreign exchange transactions take place. In other word, foreign exchange transaction is a market where foreign money were brought and sold. It is a part of money market in financial centre.

4.2Function of foreign exchange market in Bangladesh

The basic and primary function of a foreign exchange market is to transfer purchasing power between countries. The transfer function is performed through T.T, M.T, Draft, Bill of exchange, Letters of credit, etc. the bill of exchange is the most important and effective method of transferring purchasing power between two parties.

Another important function of foreign exchange market is to provide credit to the importer debtor. The exporters draw the bill of exchange on importers on their bankers. On acceptance of the bills by the importer or their bankers, the exporter will get the money realized on the maturity of the bills. In case the exporters are anxious to receive the payment earlier, the bills can be discounted from their bankers, or foreign exchange banks or discount houses.

The Foreign Exchange market performs the hedging function covering the risks on foreign exchange transactions. There are frequent fluctuations in exchange rates. If the rate is favorable, the exporter will gain and vice verse. In order to avoid the risk involved, the foreign exchange market provides hedges or actual claims through forward contracts in exchange against such fluctuations. The agencies of foreign currencies guarantee payment of foreign exchange at a fixed rate. The exchange agencies bear the risks of fluctuation of exchange rates.

4.3Limits of Foreign Exchange Trading

The foreign exchange market of the country is confined to the city of Dhaka. The 32 scheduled banks operating as authorized dealers in the inter-bank foreign exchange market are not permitted to run a position beyond certain limits. In the event of speculation on an appreciation of the value, an authorized dealer may buy more foreign currencies than it needs, but at the end of the day it must maintain its limit by selling excess currencies either in the inter-bank market or to customers. Authorized dealers maintain clearing accounts with the Bangladesh Bank in dollar, pound sterling, mark and yen to settle their mutual claims. If there any excess foreign exchange holdings exist after these transactions, it is obligatory for them to sell it to the Bangladesh Bank. In case of shortfall of the limit, authorized dealers have to cover it either through purchase from the market or from the Bangladesh Bank.

4.4Role of Bangladesh Bank

At present, the system of exchange rate management in Bangladesh is to monitor the movement of the exchange rate of taka against a basket of currencies through a mechanism of real effective exchange rate (RFER) intended to be kept close to the equilibrium rate. The players in the foreign exchange market of Bangladesh are the Bangladesh Bank, authorized dealers, and customers. The Bangladesh Bank is empowered by the Foreign Exchange Regulation Act of 1947 to regulate the foreign exchange regime. It, however, does not operate directly and instead, regularly watches activities in the market and intervenes, if necessary, through commercial banks. From time to time it issues guidelines for market participants in the light of the country’s monetary policy stance, foreign exchange reserve position, balance of payments, and overall macro-economic situation. Guidelines are issued through a regularly updated Exchange Control Manual published by the Bangladesh Bank.

According to Bangladesh Bank “banks and authorized dealers are free to set their own rates of foreign exchange against Bangladesh Taka for their inter-bank and customer transactions. The exchange rate is being determined in the market on the basis of market demand and supply forces of the respective currencies. However, to avoid any unusual volatility in the exchange rate, BB occasionally engages itself to intervene in the market through purchase and sale US Dollar as and when it deems necessary to maintain stability in the foreign exchange market.

Bangladesh Taka is fully convertible for current international transactions.” However, only authorized dealers are allowed to participate in trading with license from Bangladesh Bank, and license may be revoked due to irregularities or if the Bangladesh Bank regulations are not followed.

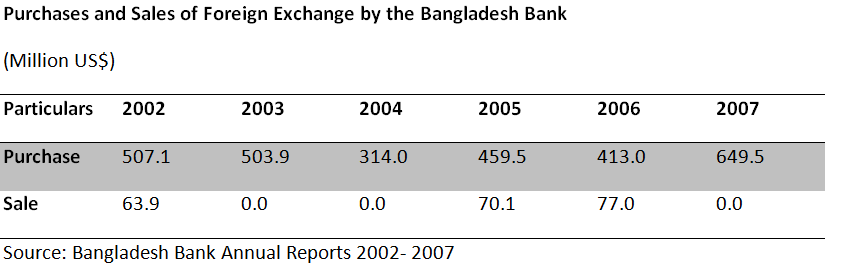

The exchange rates of Bangladesh Taka were left on the market forces after the floatation where any intervention in the foreign exchange market by the Bangladesh Bank is not enviable. The exchange rates of Bangladesh Taka against major international currencies witnessed somewhat stability since then, which did not warrant any intervention in the foreign exchange market by the Bangladesh Bank. In view of keeping foreign exchange reserve at a comfortable level, however, the Bangladesh Bank had to participate in the market. Data as shown at the table below indicate that the Bangladesh Bank did not sell any foreign currency during the last two fiscal years.

The Bangladesh Bank only purchased US $ 503.9 million and US $ 314.0 million during 2003 and 2004 respectively. Overall trends in both the sales and purchases of foreign currency by the Bangladesh Bank show declining trends during 2002-2004 indicating gradually less necessity for intervention by the Bangladesh Bank.

Because of relatively faster growth in import payments than export receipts, the demand for foreign exchange than that of supply was much stronger during the last half of 2005 generating some depreciating pressure on the Taka-Dollar exchange rate. With a view to mitigating the mismatch between the supply and demand for foreign exchange, the Bangladesh Bank intervened by selling a sizeable of amount of foreign currency in the foreign exchange market. The Bangladesh Bank sold USD 459.5 million as against the purchase of USD 70.1 million in 2005. Bangladesh Bank’s intervention helped stabilize the exchange rate to Taka 63.70 during fourth quarter of 2005, although pressure on force market continued, reflecting widening current account deficit.

Bangladesh Bank also allowed limited overdraft facility on foreign currency clearing account with the Bangladesh Bank to NCBs and some private sector banks facing temporary mismatch in liquidity and relaxed restrictions on swap and forward operations in order to give banks some flexibility to manage their liquidity.

4.5Major Factors that Affect the Foreign Exchange Market

Some of the major factors that affect the foreign exchange market in Bangladesh are:

i) Exchange rates

ii) Remittances

iii) Foreign Exchange Reserve

iv) Foreign Exchange Regulations

4.6Foreign exchange controls

Common foreign exchange controls include:

- Banning the use of foreign currency within the country

- Banning locals from possessing foreign currency

- Restricting currency exchange to government-approved exchangers

- Fixed exchange rates

- Restrictions on the amount of currency that may be imported or exported

Countries with foreign exchange controls are also known as “Article 14 countries,” after the provision in the International Monetary Fund agreement allowing exchange controls for transitional economies. Such controls used to be common in most countries, particularly poorer ones, until the 1990s when free trade and globalization started a trend towards economic liberalization.

Chapter 5

5.1Conclusion

Making term paper is a matter of great pleaser. Our term paper topic is very important for the financial market of Bangladesh. We are student of business administration, so this topic will help us to take overall financial decision in both individual life and corporate life. Bangladesh is developing country. Its economic condition is not good. So in that case by making this project we can learn the overall world liquidity and monetary system which help us to compare between Bangladesh and other countries monetary system. We also can know determination of exchange rate.