Executive summary

A government budget is a legal document that is often passed by the legislature, & approved by the chief executive-or president. For example, only certain types of revenue may be imposed & collected. Property tax is frequently the basis for municipal & county revenues, while sales tax or income tax are the basis for state revenues, & income tax & corporate tax are the basis for national revenues.

The two basic elements of any budget are the revenues & expenses. In the case of the government, revenues are derived primarily from taxes. Government expenses include spending on current goods & services, which economists call government consumption; government investment expenditures such as infrastructure investment or research expenditure; & transfer payments like unemployment or retirement benefits.

Introduction

THE announcement of the budget is an important event in a country’s political and economic calendar. In Bangladesh, public focus on the budget is still confined to a few weeks in June. The incumbent politicians and allied pundits hail the document as visionary and pro-people, the opposition denounces it as anti-poor and anti-people, and then, after a few weeks, nothing more is heard of it.

This is not conducive to democratic policymaking. With little review of the previous year’s budget, there is little accountability for the government if it fails to implement what was announced, or change course if announced policies produce undesirable outcomes. By requiring the finance minister to regularly update the parliament on budget implementation, the Public Moneys and Budget Management Act, 2009 should improve both the economic policy and our democratic culture

Objective of the report

There are various objectives of report, so some important objectives are as follows:

1.To gather practical experience on the national budget used in our country.

2.To get involved in real projects related with our economy.

3.To obtain more knowledge about the budget influencing factors.

4.To findout the ways of making the budget more efficient.

Methodology

Data are collected from two sources.

- Primary data

- Secondary data

For doing the job, we took the help of the Financil ministry official website. Then we took the help of our text and analyzed the national budget for last three years. We also went to Bangladesh Bank and collected information from the library

National Budget

A government budget is a legal document that is often passed by the legislature, & approved by the chief executive-or president. For example, only certain types of revenue may be imposed & collected. Property tax is frequently the basis for municipal & county revenues, while sales tax &/or income tax are the basis for state revenues, & income tax & corporate tax are the basis for national revenues.

The two basic elements of any budget are the revenues & expenses. In the case of the government, revenues are derived primarily from taxes. Government expenses include spending on current goods & services, which economists call government consumption; government investment expenditures such as infrastructure investment or research expenditure; & transfer payments like unemployment or retirement benefits.

GOVERNMENT REVENUE

Government revenue includes all amounts of money received from sources outside the government entity. Large governments usually have an agency or department responsible for collecting government revenue from companies & individuals.

Government revenue may also include Reserve Bank currency which is printed. This is recorded as an advance to the retail bank together with a corresponding currency in circulation expense entry. The income derives from the Official Cash rate payable by the retail banks for instruments such as 90 day bills. There is a question as to whether using generic business based accounting standards can give a fair & accurate picture of government accounts in that with a monetary policy statement to the reserve bank directing a positive inflation rate the expense provision for the return of currency to the reserve bank is largely symbolic in that to totally cancel the currency in circulation provision all currency would have to be returned to the reserve bank & cancelled.

GOVERNMENT EXPENDITURE

Government spending or government expenditure is classified by economists into three main types. Government acquisition of goods & services for current use to directly satisfy individual or collective needs of the members of the community is classed as government final consumption expenditure. Government acquisition of goods & services intended to create future benefits, such as infrastructure investment or research spending, is classed as government investment (gross fixed capital formation), which usually is the largest part of the government gross capital formation. Acquisition of goods & services is made through own production by the government (using the government’s labor force, fixed assets & purchased goods & services for intermediate consumption) or through purchases of goods & services from market producers. Government expenditures that are not acquisition of goods & services, & instead just represent transfers of money, such as social security payments, are called transfer payments.

To ensure consistency between a national accounts logic expressed in the sequence of accounts (production, generation, distribution, redistribution & use of income, accumulation & financing) & a government budget perspective (government spending & receipts), two additional concepts are defined to national accounts categories:

| Government revenue as a sum of: | Government expenditure as a sum of: |

|

|

AN OVERVIEW OF NATIONAL BUDGET IN BANGLADESH

Government forecast of a government’s expenditures & revenues for a specific period of time. The period covered by a budget of the government of Bangladesh is a financial year that starts on 1 July of a calendar year & ends on 30 June of the next calendar year. Government budget contains the strategies for mobilization, allocation & disbursement of public money by means of fiscal & monetary operations with due consideration of political, economic, & bureaucratic decision making process. It developed in Bangladesh on the basis of legal requirements, economy’s management needs, conventions, functional conveniences as well as accounting & auditing requirements, including transparency & accountability.

The Constitution of Bangladesh, however, does not use the term budget. Instead, it uses an equivalent term ‘Annual Financial Statement’, which is to show the estimated receipts & expenditures of the government for a particular financial year. Government budget in the country has two parts: Revenue & Development. The former is concerned with current revenues & expenditures ie, maintenance of normal priority & essential services, while the latter is prepared for development activities. Formulation of the two budgets follows different procedures. Their financing pattern & the delegated authorities of incurring expenditure in different tiers in them are also different. Receipts in revenue budget are: domestic receipts (tax & non-tax); foreign grants; capital receipts (foreign loans); domestic capital (net of current receipts & expenditures in public accounts); extra-budgetary resources (debenture of autonomous bodies, their self-financing & accumulated balance, & materials at stock); & domestic loans & advances (net).

Receipts in development budget are grouped as public & private receipts. Public receipts are the revenue surplus (revenue receipts minus revenue expenditures), incomes through new measures (such as new taxes), net domestic capital, & extra budgetary resources. A special form of public receipts is the foreign aid (project aid, counterpart fund from commodity aid & net food aid). Receipts under the private head for development budget are generated through direct private investment, borrowing from banking system & foreign private investment. Revenue budget is prepared by the Finance Division & the agency to prepare the development budget is the Planning Commission.

Preparation of the revenue budget is a multi-stage process implemented under a time schedule. The first stage is the printing of departmental estimates, which is followed by printing & distribution of Budget Forms (Estimating Officer’s forms) for supply to the accounts officers concerned, who fill them up with estimates from all controlling offices & send consolidated estimates to the ministry of finance. The ministry of finance then examines the estimates, receives schedule of new expenditures & information on actual expenditures of agencies & organizations in last six months, reviews new estimates on the basis of these information, & prepares a rough edition of the budget & the schedule of new expenditures. The ministry also collects forecasts of foreign development assistance & development programs from ministry of planning & after making necessary adjustments, prepares the budget documents for presentation in the JATIYA SHANGSHAD (Parliament) for discussion & approval.

Two constituent parts of the government budget are the consolidated funds (Fund) & the public accounts (Account). These are not separate entities but are distinguished by differences in receipts & disbursements. Consolidated Fund includes all receipts of the government, all loans & grants received from domestic & foreign sources & the recoveries of loans & interest thereon. Receipts in Public Accounts of the Republic represent the part of the exchequer, which do not constitute the Consolidated Fund. These relate mostly to transactions, in respect of which the government acts as custodian or banker in trust. These receipts include provident funds of government employees, post office savings deposits, various deposit accounts (local funds, judicial deposits, foreign aid deposits etc.), & adjusting heads like suspense & remittances.

Stages of budget procedure in Bangladesh are preparation, approval, implementation, & follow-up. Policy components of the budget are:

(a) Fiscal measures or revenue policy;

(b) Expenditure proposed for basic functions of the government,

(c) Development or public investment, ie, ADP;

(d) Money budget, commonly called credit & liquidity program; &

(e) Authorization for implementation of these policies.

The finance minister places the budget before parliament in June. It accompanies an introductory speech known as budget speech consisting of two parts. Part one deals with the overall financial & economic conditions prevailing in the country & government economic performance during the last one year & government economic plans & programs & the budgetary allocation. Part two deals with taxation measures. After budget discussions, money bills, supplementary bill, & appropriation bill are placed before the parliament. If, for any reason, it is not possible to pass the appropriation bill within 30 June, a vote on account bill has to be placed before the parliament. Usually, through this bill an amount equivalent to two months expenditure is sanctioned

Implementation of the approved budget is carried out through various rules & orders embodied in General Financial Rules, Treasury Rules & the Delegation of Financial Orders issued by the finance division of ministry of finance. Authorizations embodied in the Appropriation Act constitute the outer framework of a control, while expenditure sanction & disbursement by executive authority at various levels follows a given pattern of delegated financial powers. Budget implementation also involves balancing of government incomes & expenditures. Measures for realization of income & its quantum & the direction of expenditure affect the economic life of corporate bodies, individuals & households of different income groups differently during the budget year.

BUDGET 2010-11

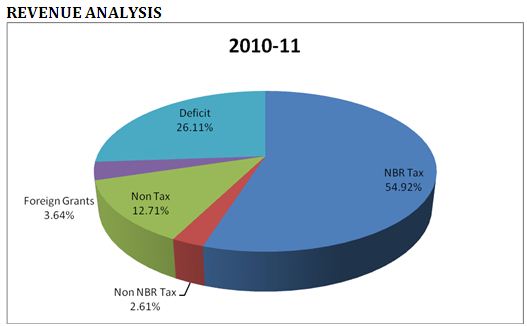

Tax revenue in 2010-11 was 54.9%, non NBR tax revenue is 2.6%, non tax revenueis 12.7% foreign grants is 3.6% of the total revenue. The ambitious revenue target for FY10, which was set at 16.6 per cent higher than the realized figure of FY09, marginally fell short of target by 1.9 per cent. The realisation in FY10 was 14.4 per cent higher than the corresponding figure of previous fiscal year. Tax component grew by 13.2 per cent during this period, while NBR and Non-NBR components grew by 13.0 per cent and 18.6 per cent respectively. The incremental contribution of VAT in total revenue growth was about 31.6 per cent, while tax on income contributed only 19.6 per cent to the added revenue intake. To match the high reaching expenditure target in a pre-election year, the government has set a new height in its revenue target. According to the new target of revenue earnings, the government will have to collect 17.1 per cent more revenue in FY10 whereas NBR will have to record a 19.15 per cent growth. Given the past record of revenue collection, this is just an unachievable target! Its seems that the government (average 11.5 per cent) first decided on a high spending outlay and then tried to make adjustment for the financing sources leading to improbable resource projection.

The targeted amount of revenue expenditure for FY10 was Tk 132170 crores which has been revised at Tk 34805 crores. Though the revised revenue expenditure for FY10 is only 2.0 percent lower than its target, it is however 10.2 per cent higher than the revised figure of FY09. Economic analysis of the composition of revenue expenditure indicates that the three heads which account for more than 80 per cent of the total revenue expenditure, accounted a 12.6 per cent growth in FY10, over the corresponding figures of the previous year. The share of these three heads increased marginally from 79.1 per cent in FY09 to 82.6 per cent in FY10. Within these three heads, “Salary and Allowances” registered a 15.5 per cent annual growth in FY10, of which “Pay of officers” increased by 22.1 per cent. According to the target for FY11, salary and allowances and other would increase by 15.8 per cent over the augmented figures of FY10. The “pay of officer” is projected to be increased by 5.8 per cent in FY11. “Subsidies and transfers” registered a 6.1 per cent growth in FY10, while “interest payments” accounted a 16.0 per cent growth during this period. Interest payment (domestic) during FY10 accounted a significant growth of 17.6 per cent, while Interest Payment (foreign) recorded an 8.3 per cent growth. Among others, “Goods and Services” registered a moderate growth of 7.1 per cent in FY10.

EXPENDITURE ANALYSIS

Non-development expenditure is 65.66%, net outlay for food account operation is 0.18%, loans and advances 2.44%, structural adjustment expenditure is 0.11% and development expenditure is 31.98% of the total expenditure. Total revenue earnings registered 14.5 per cent growth in FY10 as against a 9.8 per cent growth in total public expenditure. Revenue expenditure registered a whooping 17.3 per cent growth against a 4.9 per cent ADP growth. Given the poor utilisation of ADP, a moderate budget deficit (3.89 per cent of GDP) was also observed. For FY11, the government has set the growth of public expenditure at 14.2 per cent, which is lower than the projected growth of revenue earnings (17.1 per cent). Target of ADP growth has been set at 20.9 per cent in FY11 as against a 14.1 per cent growth in revenue expenditure.

| Particulars | Amount (2010-11) (Tk in Crore) |

| Education and Technology | 18372 |

| Interests | 14671 |

| Transport and Communication | 8855 |

| LGRD | 10838 |

| Fuel & Energy | 6080 |

| Health | 8195 |

| Agriculture | 11367 |

| Defense Service | 9120 |

| Public Service | 18768 |

| Social Security & Welfare | 9648 |

| Public Order & Safety | 6873 |

| Housing | 1322 |

| Recreation, Culture, Religion | 1586 |

| Industrial & Economic Services | 1190 |

| Others | 5155 |

| Total= 132170 |

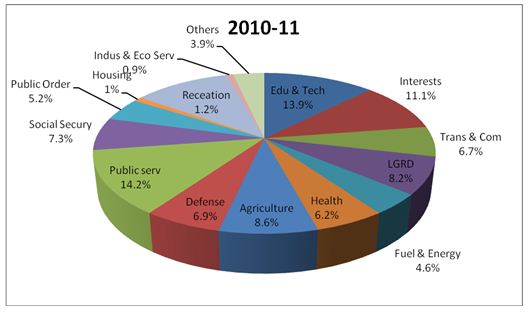

The total expenditure of 2010-11 was BDT 132170 crore. The expenditure was distributed among fifteen sectors. The percentage of the distributed sectors are given below:

Budget2008-09

EXPLANATORY NOTES:

1. Grants have been grouped together with government revenues as they are unrequited receipts from development partners;

2. Expenditure for acquisition of assets, acquisition of land, construction and works, and investment in shares and equities has been included in Non-Development Capital Expenditure;

3. Loans and Advances to state-owned enterprises/autonomous bodies and government employees minus repayment of loans and advances have been shown as Loans and Advances (Net);

4. This group includes allocation to some small development programmes under Non-Development Budget and but included in the ADP;

5. As per agreements with development partners these are transfers of food sale-proceeds and parts of FFW that are not included in the ADP but forms part of the Development Budget;

EXPLANATORY NOTES:

1. Grants have been grouped together with government revenues as they are unrequited receipts from development partners;

2. Expenditure for acquisition of assets, acquisition of land, construction and works, and investment in shares and equities etc. has been included in Non-Development Capital Expenditure;

3. Loans and Advances to state-owned enterprises/autonomous bodies and government employees minus repayment of loans and advances have been shown as Loans and Advances (Net);

4. This group includes some development programmes that are financed from Revenue Budget but not included in the ADP;

5. Transfer of sale proceeds from food grains received under the agreement with development partners & receipts from food for works which are not included in the ADP have been shown;

6. Net Increase/Decrease in the Public Accounts of the Republic (excluding National Savings Schemes) has been included in this group.

Budget2010-11

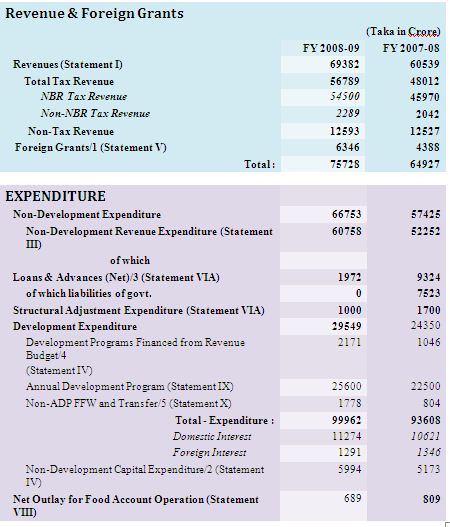

| Revenue & Foreign Grants | ||

(Taka in Crore) | ||

FY 2010-11 | FY 2009-10 | |

| Revenues (Statement I) | 92847 | 79461 |

| Total Tax Revenue | 76042 | 63955 |

| NBR Tax Revenue | 72590 | 61000 |

| Non-NBR Tax Revenue | 3452 | 2955 |

| Non-Tax Revenue | 16805 | 15506 |

| Foreign Grants/1 (Statement V) | 4809 | 5130 |

Total : | 97656 | 84591 |

| EXPENDITURE |

|

|

| Non-Development Expenditure | 85786 | 77243 |

| Non-Development Revenue Expenditure (Statement III) | 75230 | 69504 |

| of which | ||

| Domestic Interest | 13271 | 14471 |

| Foreign Interest | 1438 | 1337 |

| Non-Development Capital Expenditure/2 (Statement IV) | 10556 | 7739 |

| Net Outlay for Food Account Operation (Statement VIII) | 241 | 326 |

| Loans & Advances (Net)/3 (Statement VIA) | 3223 | 1631 |

| Structural Adjustment Expenditure (Statement VIA) | 150 | 332 |

| Development Expenditure | 42770 | 34287 |

| Development Programs Financed from Revenue Budget/4 |

| FINANCING | ||

| Foreign Borrowing-Net | 10834 | 8673 |

| Foreign Borrowing (Statement V) | 15968 | 13215 |

| Amortization (Statement IX) | -5134 | -4542 |

| Domestic Borrowing (Statement VIB) | 23680 | 20555 |

| Borrowing from Banking System (Net) | 15680 | 16755 |

Long-Term Debt (Net) | 12570 | 12577 |

Short-Term Debt (Net) | 3110 | 4178 |

| Non-Bank Borrowing (Net) | 8000 | 3800 |

| National Savings Schemes (Net) | 7477 | 3277 |

| Others/6 (Statement VII) | 523 | 523 |

Total – Financing | 34514 | 19228 |

| GDP Memorandum Item | 780290 | 686730 |

EXPLANATORY NOTES:

1. Grants have been grouped together with government revenues as they are unrequited receipts from development partners;

2. Expenditure for acquisition of assets, acquisition of land, construction and works, and investment in shares and equities etc. has been included in Non-Development Capital Expenditure;

3. Loans and Advances to state-owned enterprises/autonomous bodies and government employees minus repayment of loans and advances have been shown as Loans and Advances (Net);

4. This group includes some development programmes that are financed from Revenue Budget but not included in the ADP;

5. Transfer of sale proceeds from food grains received under the agreement with development partners & receipts from food for works which are not included in the ADP have been shown.

PUBLIC-PRIVATE PARTNERSHIP (PPP)

BACKGROUND

In order to achieve the Vision 2021 goal of Bangladesh becoming a middle income country by 2021, we will need to ensure a more rapid, inclusive growth trajectory. To reflect the aspirations of the people the target of the government is to raise the GDP growth rate to 8 percent by 2013. To achieve this GDP growth rate, the share of investment to GDP needs to be raised to 35-40 percent. At present average investment GDP ratio is 24-25 percent, which is lower than the national savings ratio. One estimate suggests that to sustain GDP growth rate of 8 percent in 2013 and beyond requires additional USD 28 billion or BDT 1.96 trillion for 2010-2015. To reduce the investment deficit, participation of the private sector through public-private partnership (PPP) is an important route. In order to create an enabling environment for attracting private investments on a sustained basis, GOB has taken a series of measures. Previously, the GOB had issued the Bangladesh Private Sector Infrastructure Guidelines (PSIG) for implementing the PPP Projects. There has been some success in attracting private investment through PPP route in the power, gas and telecom sectors. The Government seeks more investment in these and other sectors such as ports, roads, railway, water supply, waste management, tourism, e-service delivery etc.

For the first time in the country, the Government through its national budget FY 2009-10 introduced the concept of PPP budget. This is a very strong statement and commitment for the development of PPP in the country. In addition, the Government issued a position paper on PPP, titled, æ Invigorating Investment Initiative Through Public-Private Partnership” dated June 2009. The PPP Budget aims to provide support for upfront development of PPP projects, create a mechanism for targeted subsidies and set long term financing of PPP projects.

The government has taken a two-pronged strategy for building public-private partnership: one is to attract investment for projects, where building new infrastructure and expanding existing infrastructure is the major component; the second is to attract innovation and sustainability of public service delivery to the citizens. While the government is committed to launch public-private partnership in a big scale, the essential ingredient to that Endeavour is to set up a forwardlooking strategy and a framework for operationalisation of public-private partnership as well as clear-cut procedural guidelines for the sake of ensuringtransparency and building confidence among the private sector players.

A wide spectrum of PPP arrangements exists, differing in purpose, service scope, legal structure and risk sharing. The choice of the PPP arrangement for a particular project will depend on social and economic importance and potential value for money to be generated under such arrangement.

PPP fosters economic growth by developing new commercial opportunities and increasing competition in the provision of public services, thus encouraging crowding-in of private investment. Successful application of PPP concept through this æPolicy and Strategy” document is likely to open up the doors for

increased flow of investment from both local and foreign investors.

OBJECTIVES

Presently, initiation and approval process of PPP projects in Bangladesh are unclear. Procurement processes for PPP projects are less well known and understood compared to similar projects included in the Annual Development Programme (ADP). A major cause for the lack of private sector participation in

PPP projects is the absence of consistent procedures to identify, formulate, appraise and approve PPP Projects.

In this context, the objectives of this Policy and Strategy are to :

a. spell out The principles of partnership with private sector for undertaking various projects related to infrastructure as well as public service delivery;

b. define an institutional framework, which is conductive and efficient in handling the PPP projects as well as effective to protect public interest; and

c. ensure balance between risk and reward for both the government and private partners while aiming to keep the undertaking attractive for the private sector.