ORIGIN OF THE REPORT:

This is an internship report prepared as a requirement for the completion of the BBA Program of Department of Finance, Stamford University Bangladesh. The primary goal of internship is to provide an on-the-job exposure to the student and an opportunity to know how to implement theoretical concepts in real life situations. Students are placed in enterprises, organizations, research institutions and as well as in development projects.

As a requirement of the four-year academic program, after appearing in final exam, department placed me in Dhaka Bank Limited for the purpose of internship attachment under the guidance of respected faculty advisor Sohani Islam, Department of Business Administration. The duration of my organizational attachment was Two months, from May 11, 2009 to July 12, 2009.

Dhaka Bank Limited placed me to their Credit Division under the MD. Jahir Uddin Ferdous, Senior Assistant Vice President, of Credit Operation Unit. Another one months placed me their Operational Division Under the MD. Mahbubur Rahoman, Senior Principal Officer of Operation Division.

Through out my internship period I have got the privilege to gather knowledge about CIB inquiry procedure and credit appraisals of the Bank from the concerned officials of the Dhaka Bank Limited. My supervisor at Dhaka Bank and also of the department encouraged me thus work on the topic entitled “Credit Rating & Capital Preservation of Dhaka Bank Ltd”.

BACKGROUND OF THE STUDY:

Bank is a trader of deposit and credit, Basically it earns profit by increasing or maintaining the spread. As credit allocation is a present phenomenon and its repayment is futuristic, uncertainty prevails all the time.

Credit policy of any bank is the prime guide line towards the logic behind its overall credit appraisal process. A credit policy is not a one day invention rather it is the summary of year long innovations and conceptions generated form the vast experience of the bankers.

The credit appraisal process for any bank must be a sequence of logical and interlinked activities. The credit appraisal process is also a generation of year long routine and unavoidable experiences perceived by the bankers. Credit risk grading is perhaps the most significant part of the process because default risk management by means of proper credit approval policy depends significantly on CRG.

Although financial risk management primly credit risk management, now-a-days is getting good response in Bangladesh a compact, fully inclusive, efficient credit policy and credit appraisal process are yet to be introduced.

In this gloomy scenario and dismay a study on efficient credit policy, credit appraisal process, CRG will be a handful to lull the situation to a great extent.

OBJECTIVES OF THE STUDY:

My objectives of the study are as follows:

- To assess the credit policy of Dhaka Bank Limited.

- To assess the credit Rating of Dhaka Bank Limited.

- To evaluate the Performance of Dhaka Bank Limited.

- To know about the existing CRG practice of Dhaka Bank Limited.

- To know about the existing offering to the creditors of Dhaka Bank Limited.

- To know about the existing asset quality of Dhaka Bank Limited. And evaluate it.

- To provide an all inclusive list of recommendations for the credit division of Dhaka Bank Limited.

Now I am going to discuss about the data collection, data analysis, and questionnaire design of my report.

Data collection:

Both primary and the secondary data were used to prepare the report. The details of these sources are as below:

Primary Sources:

Primary data for this report had been collected through the conversation & discussion of different officers. On the job observation of the officers has helped a lot to know information of banking.

Secondary Sources:

The secondary sources of data are:

- Annual Report of Dhaka Bank Limited

- Internal Publications of Dhaka Bank Limited

- The website of Dhaka Bank Limited (www.dhakabankltd.com)

- The website of Bangladesh Bank (www.bangladesh-bank.org)

Data processing:

Hypothesis testing was the main tool of processing. Two tailed t-test were used. Concepts of central tendency, dispersion were used. Statistical diagrams are embedded.

LIMITATIONS OF THE STUDY:

Although I received co-operation from the concerned officials, they were not always able to give me much time, as they were busy with their works. Time is an important issue in Report writing. As I have been given a specific deadline for submission, observation and learning all the Banking Operations within 2 months was really tough. Another limitation of this Report is non-availability of the most Recent Data and Information of different activities of Dhaka Bank Limited (DBL) and Bank’s Policy of not disclosing some Data and Information for some reasons, which could be very much useful. Lack of secondary information was another major problem that was faced during the study. The branch office had very little of this information that’s why bulk of it had to be gathered from the head office. Due to lack of experience, there may have been faults in the report though maximum efforts have been given to avoid any kind of mistake. In spite of all these limitations, I have tried to put the best effort as far as was possible.

Other Limitations are as follows:

- Sampling error can be prevalent because of very small observation.

- Decorative responses and vague answers from the respondent of the questionnaire may affect my recommendations.

BANKING HISTORY OF BANGLADESH :

Bangladesh is a developing country. Banking sector plays a pivotal role in the economic development of the country. Banking system of a country can well be said as a barometer of its economic prosperity. Well-developed banking system is indispensable for modern trade and commerce. Now-a-days, banks not only act as custodian of public money but also are indispensable as vital agent for maintenance of sound financial position of a country.

Nationalized Commercial Banks (NCBs) were established in Bangladesh in 1972 through amalgamation of twelve commercial banks that were operating in pre-independent Bangladesh allowing the poor access to fund, reducing capital flight to foreign countries, and increasing domestic investment were some of the basic objective of this nationalization. That means a society with wealth distributed as equitably as possible. But with time difference those banks has changed their policies and strategies, which were not fulfilling the class banking policies of the government. On an evaluation of the activities of commercial banks, it has been observed that the progresses made by the banking industry since nationalization was not impressive. The nationalized banks could not play the due role in the implementation of government programs and policies. Hence, a trend of de-nationalization of banks started from mid 80’s.

In the meantime, the policy of the government towards banking industry regarding economic management has changed since 1976. That year private sector had been entrusted to play a bigger role in the economy than before. Accordingly, in order to provide more credit to local investors the private sector banking had been introduced. Government decided to allow setting up of local Private Commercial Banks (PCB) in addition to Nationalized Commercial Banks (NCB) operating in the country.

Bangladesh Bank acts as a central bank for our country and it controls, supervises, and looks after the scheduled banks in the private commercial banks as well as the nationalized commercial banks formed by amalgamating the business of the twelve banks doing business in Bangladesh before liberation as per schedule given below:

Table 1: Banking History

| Existing Bank | New Bank | Authorized Capital(Lac Tk.) | Paid up Capital (Lac Tk.) |

| The National Bank of Pakistan, The Bank of Behawalpur Ltd. | Sonali Bank | 500 | 200 |

| The Premier Bank Ltd., The Habib Bank Ltd., The Commerce Bank Ltd. | Agrani Bank | 500 | 100 |

| The United Bank Ltd., The Union Bank Ltd. | Janata Bank | 500 | 100 |

| The Muslim Commercial Bank Ltd., The Standard Bank Ltd. | Rupali Bank | 500 | 100 |

| The Austrasia Bank Ltd., The Eastern Mercantile Bank Ltd. | Pubali Bank | 500 | 100 |

| The Eastern Banking Corporation Ltd. | Uttara Bank | 500 | 100 |

After the liberation of Bangladesh the twelve Banking companies who were doing business in Bangladesh, were nationalized by the Government of the People’s Republic of Bangladesh under president’s order No.26 of 1972 entitled The Bangladesh Bank (Nationalizations) Order, 1972” on March 26, 1972.

During 1983 Bangladesh Government allowed the private sector to operate banking business. Now Banks are formed and are operated under The Bank Company Act, 1991. At present there are about 50 banks operating their business in Bangladesh.

HISTORY OF DHAKA BANK LIMITED:

Dhaka Bank Limited was incorporated as a public limited company under the Companies Act 1994. The Bank started its commercial operation on July 05, 1995 with an Authorized Capital of Tk.1,000.00 million and Paid Up Capital of Tk.100.00 million. The present Paid Up Capital of the Bank is Tk.1,934,252,875.00 as on June 30, 2008. The total equity (capital and reserves) of the Bank as on June 30, 2008 stood at Tk.3,424,609,016.00. The Bank has 45 branches and 2 Offshore Banking Units across the country and a wide network of correspondents all over the world. The Bank has a plan to open more branches in the current fiscal year to expand the network. Dhaka Bank Limited offers the full range of banking and investment services for personal and corporate customers, backed by the latest technology and a team of highly motivated officers and staffs. In the effort to provide excellence in banking services, the Bank has launched online banking service, joined a countrywide-shared ATM network and has introduced a co-branded credit card. A process is also underway to provide e-business facility to the bank’s clientele through online and home banking solutions. Dhaka Bank Limited is the preferred choice in banking for friendly and personalized services, cutting edge technology, tailored solutions for business needs, global reach in trade and commerce and high yield on investments.

MISSION:

To be the premier financial institution in the country providing high quality products and services backed by latest technology and a team of highly motivated personnel to deliver Excellence in Banking.

VISION:

At Dhaka Bank, we draw our inspiration from the distant stars. Our team is committed to assure a standard that makes every banking transaction a pleasurable experience. Our endeavor is to offer you razor sharp sparkle through accuracy, reliability, timely delivery, cutting edge technology, and tailored solution for business needs, global reach in trade and commerce and high yield on your investments.

Our people, products and processes are aligned to meet the demand of our discerning customers. Our goal is to achieve a distinct foresight. Our prime objective is to deliver a true reflection of our vision- Excellence in Banking.

VALUES:

Customer Focus

Integrity

Teamwork

Respect to the Individual

Quality

Responsible Citizenship

Dhaka Bank Limited was rated by Credit Rating Agency of Bangladesh (CRAB) Limited on the basis of audited Financial Statements as on December 31, 2007. The summary of the rating is as follows:

CRAB has awarded A1 (Pronounced as Single A One) rating in the long term and ST-2 rating in the short term to Dhaka Bank Limited. In 2006, CRAB awarded the same rating to Dhaka Bank Limited in the long term and short term.

Commercial Banks rated in this long-term category are adjudged to be strong banks, characterized by good financials, healthy and sustainable franchises, and a first rate operating environment. This level of rating indicates strong capacity for timely payment of financial commitments, with low likeliness to be adversely affected by foreseeable events.

Commercial Banks rated in this short-term category are characterized with commendable position in terms of internal fund generation, access to alternative sources of funds and moderate level of liquidity. The rating is valid for one year.

BRIEF PROFILE OF DHAKA BANK LIMITED:

| Name of company | : | Dhaka Bank Limited |

| Legal form | : | A public limited company incorporated in Bangladesh on 6th April 1995 under companies Act 1994 and listed with Dhaka Stock Exchange Limited and Chittagong Stock Exchange Limited. |

| Date of commencement | : | July 5, 1995 |

| Registered office | : | Biman Bhaban (1st floor), 100 Motijheel C/A, Dhaka 1000, Bangladesh |

| Telephone | : | +880 2 9554514, 9571006-10 |

| Telefax | : | +880 2 9556584, 9571013 |

| Swift code | : | DHBLBDDH |

| : | info@dhakabank.com.bd | |

| Auditors | : | ACNABINChartered Accountants |

| Tax Consultant | : | Howladar, Yunus & co.Chartered Accountants |

| Managing Director (CC) | : | Khondker Fazle Rashid |

| Company Secretary | : | Arham Masudul Huq |

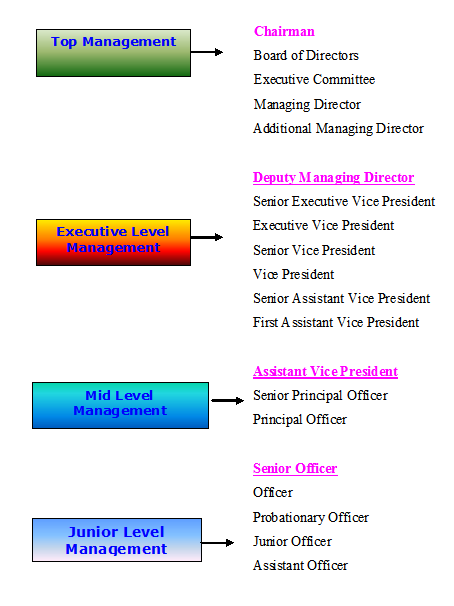

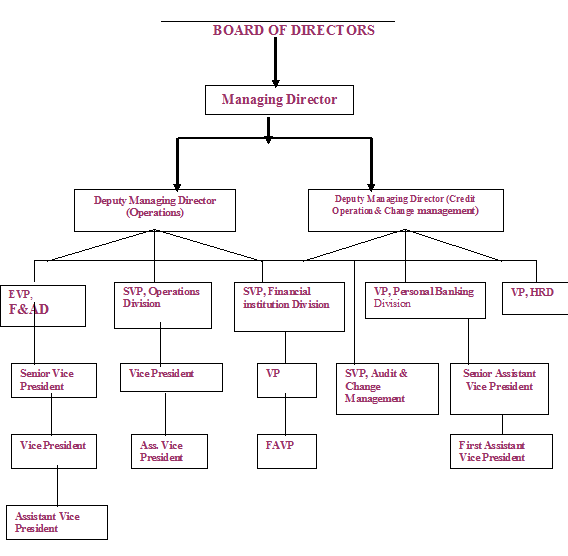

ORGANIZATIONAL HIERARCHY:

Management Hierarchy of the Dhaka Bank Ltd:

Since its journey as Commercial Bank in 1995 Dhaka Bank Limited (DBL) has been laying great emphasis on the use of improved Technology. It has gone to Online Operation System since 2003. And the new Banking Software FLEXCUBE was installed. As a result the Bank will able to give the services of international standards. As per Bangladesh Bank’s instruction “BASEL II Implementation Team has been formed which will be responsible for proper implementation of Basel II capital adequacy guidelines in the Bank. The guidelines have been issued by Bangladesh Bank recently but the target date for implementation is 31st December 2009.

1. Free enterprise and 1.Organizing process 1. DBL is leaded by 1.The regulatory

a competitive market under the supervision its management team authorities of the

System of CEO. Namely MANCOM bank is designed

& Operated. 2. Long-term 2.Management 2. The Management

Profitability Plans. Activities of the top team are unique.

Management is

3. Follow business- organized by the CEO.

Plans, development

Programs, Marketing 3. Account rules and

Plans for their day-to procedure, business

Day activities. Process & safeguarding

Assets are secured and

Observed.

OBJECTIVES OF DHAKA BANK LIMITED:

The main objectives of the Dhaka Bank Limited are as follows:

a) To establish, maintain, carry on, transact, undertake and conduct all types of banking, financial, investment and trust business of in Bangladesh and abroad.

b) To form, establish and organize any bank, company, institutions or organization either singly and/or in joint collaboration of partnership with any individual company, financial institution, bank, organization or any government and or government agency for the purpose of carrying on banking, financial investment and trust business and/or any other business as provided hereafter.

c) To carry on any business relating to Wage Earner Scheme as may be allowed by Bangladesh Bank from time to time including maintaining of foreign currency accounts and any other matter related there to.

d) To contract or negotiate all kinds of loan and/or assistance, private or public from any source, local or foreign, and to take all such steps as may be required to be complete such deals.

e) To form, organize assets, participate or aid in forming, promoting or organizing any company, bank, syndicate, consortium institute or any holding and subsidiary company in Bangladesh or abroad for the purpose of undertaking any banking financial investment and trust business.

f) To take part in the formation, management, supervision or control of business or operations of any company or undertaking and for that purpose to render technical managerial and administrative services and act as administrator, manager and secretary.

g) To purpose, or otherwise acquire, undertake, the whole or any part of or any interest in the business, goodwill, property, contract, agreement, right, private assets and liabilities of any other company bank corporation, partnership, body person or persons carrying on, or having ceased to carry on, any business which the company is authorized to carry on such terms and may be deemed expedient.

h) To encourage sponsor and facilitate participation of private capital in financial industrial or commercial investment, share and securities and in particular by providing finance in the form of long, medium or short term loans or share participation by way of subscription to the promoter shares, or underwriting supports or bridge finance loans and/or by any manner.

i) To amalgamate or reconstruct or recognize with any commercial bank, or body corporate or association in cooperation with any person, commercial bank or association.

j) To establish and open offices and branches to carry on all or any of the above business abroad and within the country provided prior permission is obtained from the Bangladesh Bank.

k) To establish provident fund, gratuity, pension, and other fund for the welfare and benefit of the employees and staffs, former or present and any matter related thereon.

l) To act as official liquidator and receiver.

m) To receive, borrow or raise money on deposit, loan or otherwise upon such terms as the Dhaka Bank may approve and to give guarantee and indemnity in respect of any debt or contract.

n) To appoint officials, staff, experts, advisers, consultants, auditors, Legal advisers and provide for their suitable remunerations.

- o) To advance, deposit or lend money to or with such persons or bodies, corporate, unincorporated, statutory, govt. and/or its agencies on such terms as the Dhaka Bank may approve.

CAPITAL AND RESERVES:

Dhaka Bank Limited has been consistently maintaining the ‘Capital Adequacy Ratio’, as prescribed by Bangladesh Bank. This has been made possible by a policy of building up both capital and reserves. It started with an Authorized and Paid-up Capital of Tk.1, 000.00 million and Tk.276.00 million respectively in 1995. Authorized and Paid up Capital increased to Tk.6, 000.00 million and Tk.1, 934.25 million respectively in 2008. In addition to Paid up Capital, the Bank has built up a strong reserve base over the years.

STRENGTH AND PERFORMANCE:

With the active support and guidance from Bangladesh Bank, clients and patrons, the Bank has been maintaining sound financial strength and showing a steady and impressive business performance. Dhaka Bank Limited is one of the few mentionable banks, which maintains Capital Adequacy ratio and has more than required provision as per Bangladesh Bank criteria.

Starting with a modest deposit of only Tk.10,749.00 million in 1996, the Bank had closed its business with a deposit of Tk.48,731 million as of December 31, 2007. The total deposits stood at Tk.56,986 million as of December 31, 2008. Total credit stood at Tk.49,698 million as on December 31, 2008 against Tk.39,972 million last year. Bank has posted a profit before tax and provision of Tk.2,533 million during the year ended December 31, 2008 against 2,010 million last year with a growth of 26%. Earning per share (EPS) is Tk.43.00 as on December 31, 2008 against Tk.36.00 as on December 31, 2007. Dhaka Bank has received ICAB National Award 2007 in the financial sector for their published Accounts and Reports.

FUNCTIONS OF THE DHAKA BANK LIMITED:

Dhaka Bank Limited performs all types of functions of a modern commercial bank, which generally includes:

1) Mobilization of savings of the people and safe keeping of all types of deposit account.

2) Making advances especially for productive activities and for the other commercial and socio-economic needs.

3) Providing banking services to common people through the branches.

4) Handling of export and import trade and foreign remittances and with special support to export activities.

5) Introduce modern Banking services in the country.

6) Discounting and purchasing bills.

7) Providing various information, guidance and suggestions for promotion of trade and industry keeping in view of the overall economic development of the country.

8) Industrial finance for both capital machinery and working capital.

9) Finance relating to constructions of both commercial and residential.

10) Finance under small business of self employed clients.

11) Finance of farming and non-farming activities to rural people including purchase of agricultural equipments.

12) Ensuing proper utilization of credit disbursed.

13) Developing new products.

14) Market surveys before making any finance.

15) Finance for small transport.

16) Monitoring and forecasting.

17) Developing marketing campaigns.

18) Finance for household durables.

19) Work simplification studies.

20) Monitoring diversification of portfolio among different sectors.

21) Pricing and minimum size of transaction ship.

CUSTOMER SERVICES IN DHAKA BANK LIMITED:

Like some other Banks Dhaka Bank Limited (DBL) has also some Services that it provides its Potential Customers. The Services of the Bank for its Customers are:

- Ø Corporate Banking Services:

- Floating of Public Issues

- Loan Syndication

- Ø Personal Banking Services:

- Deposit Accounts

– Current Account

– Savings Account

– Short Term Deposit Account

– Fixed Deposit Account

– Excel Account

- Foreign Exchange Transactions

- Consumer Credit Scheme

- E-Cash 24 Hour Banking

- Phone Banking

- Branch Banking

- Dhaka Bank Credit Card

- Secured Overdraft

- Personal Loan

- Car Loan

- Safe Deposit Lockers

- Private Foreign Currency Accounts

- Utility Bill Payments

- Ø International Trade & Foreign Exchange

- Ø Lease Financing

- Ø Capital Market Services

FINANCIAL PERFORMANCE:

Position of the Dhaka bank at a glance for the last 5 years:

(Tk in million)

| Particulars | 2004 | 2005 | 2006 | 2007 | 2008 |

| Income Statement | |||||

| Interest Income | 2,011 | 2,897 | 4,342 | 5,636 | 7,171 |

| Interest Expense | 1,389 | 2,149 | 3,380 | 4,049 | 5,214 |

| Net Interest Income | 622 | 748 | 962 | 1,587 | 1,958 |

| Non Interest Income | 648 | 739 | 1,110 | 1,582 | 1,929 |

| Non Interest Expense | 523 | 594 | 889 | 1,159 | 1,353 |

| Net Non Interest Income | 125 | 145 | 221 | 423 | 576 |

| Profit before Tax & Provision | 747 | 893 | 1,183 | 2,010 | 2,533 |

| Provision for Loans & Assets | 114 | 125 | 233 | 479 | 669 |

| Provision for Tax (including Deferred Tax) | 275 | 305 | 370 | 827 | 1,025 |

| Profit after Tax | 358 | 463 | 580 | 704 | 839 |

| Balance Sheet | |||||

| Authorize Capital | 1,000 | 2,650 | 2,650 | 6,000 | 6,000 |

| Paid up Capital | 664 | 1,228 | 1,289 | 1,547 | 1,934 |

| Reserve Funds & Other Reserve | 824 | 988 | 1,262 | 1,578 | 2,065 |

| Shareholders’ Equity (Capital & Reserve) | 1,488 | 2,216 | 2,551 | 3,125 | 4,000 |

| Deposits (Base & Bank excluding Call) | 22,270 | 28,439 | 41,554 | 48,731 | 56,986 |

| Loans & Advances | 16,539 | 23,372 | 34,049 | 39,972 | 49,698 |

| Investments | 3,078 | 3,926 | 5,378 | 5,972 | 7,239 |

| Fixed Assets | 125 | 122 | 217 | 291 | 387 |

| Total Assets ( excluding off-balance sheet items) | 28,178 | 33,072 | 47,594 | 57,443 | 71,137 |

| Foreign Exchange Business | |||||

| Import Business | 28,048 | 30,213 | 46,277 | 49,496 | 65,737 |

| Export Business | 8,881 | 13,505 | 23,268 | 31,081 | 39,038 |

| Guarantee Business | 3,663 | 6,099 | 6,473 | 6,523 | 7,887 |

| Inward Foreign Remittance | 1,110 | 3,377 | 16,764 | 10,609 | 11,834 |

| Capital Measures | |||||

| Core Capital ( Tier I ) | 1488 | 2216 | 2551 | 3126 | 3964 |

| Supplementary Capital (Tier II ) | 163 | 237 | 373 | 554 | 844 |

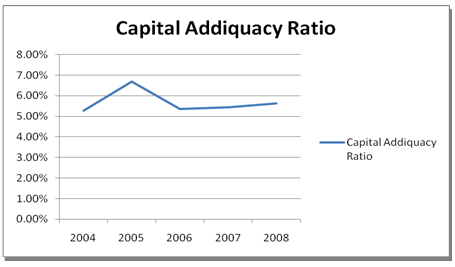

| Tier I Capital Ratio | 9.47 | 9.94 | 8.23 | 8.80 | 9.77 |

| Tier II Capital Ratio | 1.04 | 1.06 | 1.2 | 1.56 | 2.08 |

| Total Capital | 1651 | 2,453 | 2,924 | 3,680 | 4,808 |

| Total Capital Ratio | 10.51 | 11.00 | 9.43 | 10.36 | 11.84 |

| Credit Quality | |||||

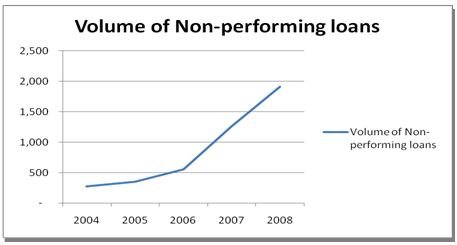

| Volume of Non-performing loans | 271 | 351 | 554 | 1,258 | 1,908 |

| % of NPLs to Total Loans & Advances | 1.65 | 1.51 | 1.64 | 3.15 | 3.84 |

| Provision for unclassified Loans | 162 | 236 | 372 | 465 | 620 |

| Provision for Classified Loans | 76 | 103 | 172 | 439 | 825 |

| Share Information | |||||

| Number of Shares Outstanding | 6.64 | 12.28 | 12.89 | 15.47 | 19.34 |

| Earning per Share (Taka) | 61 | 44 | 45 | 36 | 43 |

| Book Value per share (Taka) | 224 | 180 | 198 | 202 | 207 |

| Market Price per share (Taka) | 850 | 469 | 466 | 706 | 361 |

| Price Earning Ratio (Times) | 14.03 | 10.66 | 10.32 | 15.33 | 8.31 |

| Price Equity Ratio (Times) | 3.79 | 2.60 | 2.35 | 3.49 | 1.74 |

| Dividend per Share: | |||||

| Cash Dividend (%) | 10 | 20 | 10 | – | 15 |

| Bonus Share | 7:20 | 1:20 | 1:5 | 1:4 | 1:10 |

| Operating Performance Ratio | |||||

| Net Interest Margin | 3.57 | 3.43 | 3.77 | 4.54 | 4.60 |

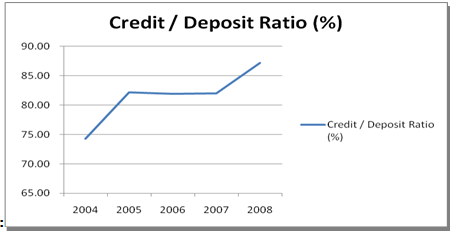

| Credit / Deposit Ratio (%) | 74.26 | 82.18 | 81.94 | 82.03 | 87.21 |

| Current Ratio (Times) | 1.60 | 1.33 | 1.24 | 1.38 | 1.28 |

| Return on Equity (ROE) % | 24.06 | 20.89 | 22.74 | 22.53 | 20.97 |

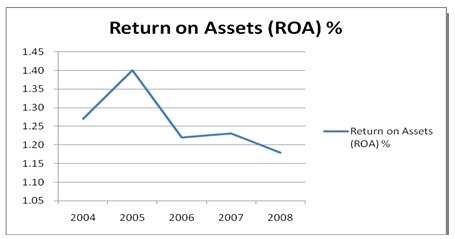

| Return on Assets (ROA) % | 1.27 | 1.40 | 1.22 | 1.23 | 1.18 |

| Cost of Deposit (%) | 6.75 | 8.13 | 9.15 | 8.97 | 9.40 |

| Cost / Income ratio in operating business (%) | 71.91 | 75.44 | 78.14 | 72.15 | 72.16 |

Table 2: Financial Performance

FINANCIAL PERFORMANCE ANALYSIS:

First I will present key financial variables by graphs and relevant interpretations are embedded later.

Return on Equity (ROE):

Graph 1: Return on Equity (2004-2008)

Return on Assets (ROA):

Graph 2: Return on Assets (2004-2008)

Credit Deposit Ratio:

Graph 3: Credit- Deposit Ratio (2004-2008)

Nonperforming Loan:

Graph 4: Volume of Non Performing Loans (2004-2008)

Capital Addiquacy Ratio:

Graph 5: Capital Adequacy Ratio (2004-2008):

- Asset quality situation of DBL is deteriorating as the portion of NPL in the credit portfolio is on a firstly increasing tone.

- Profitability of DBL in terms of ROE was superb in absolute terms. But comparison with the industry norm is necessary to make any justifiable comments regarding ROA and ROE. Net Income’s growth was pretty satisfactory.

- Total capital ratio (which integrates both tier I capital and tier II capital) during the all 5 years was within a satisfactory range if compared with the international standard.

- The bank is using its deposits in a comparatively moderate level. If we consider the regulatory demand of cash reserves.

PRODUCTS & SERVICES OF DBL:

Different banking products and services are being offered exclusively to the Non Government Organizations and international projects in Bangladesh and its staff, both local and expatriate, based in Bangladesh. With the assistance of the Marketing Team, who have prior experience of serving diplomatic missions with other multinational banks, the Bank has tailored-made a list of products to address the NGO / International Organization’s unique banking requirements in Bangladesh. Dhaka Bank Limited is committed to developing and delivering to the corporate relationships total banking solutions while ensuring a level of service that exceeds customer expectations.

Products of DBL:

Retail Banking:

In 2001 DBL. introduced its personal banking program responding to the market demand for a complete range of modern banking products & services. On 14th July 2002, DBL launched a new product-Excel Account which is first of its kind in Bangladesh. Designed exclusively for the salaried executives, Excel Account offers a packaged solution to companies and organizations in processing their employees’ salaries and funding employees’ loans.

Deposit Double:

Deposit Double is a time specified deposit scheme for individual clients where the deposited money will be doubled in 6 years. The key differentiators of the product will be:

Amount of deposit – The minimum deposit will be BDT 50,000.00 (either singly or jointly). The

- client will have the option of depositing any amount in multiples of BDT 10,000 subject to a maximum of Tk 20, 00,000 in a single name and Tk 35, 00,000 in joint name.

- Tenure of the scheme – The tenure of the scheme will be 6 years.

- Premature encashment – If any client chooses to withdraw the deposit before the tenure, then she/he will only be entitled to prevailing interest rate on savings account in addition to the initial deposit. However, withdrawal of the deposited amount before one year will not earn any interest to the depositor(s).

- OD Facility against Deposit – Clients will have the option of taking advance upto 90% of the initial deposited amount. The lending rate will be tied up with the interest rate offered on the deposit.

Product Features | |

| Deposited Amount | Min Tk 50,000 (singly or jointly) with multiples of Tk 10,000 Max Tk 20,00,000 (in single name) Tk 35,00,000 (in joint name) |

| Initial Deposit date | Any day of the month |

| Tenure | 6 years |

Govt. Charges – The matured value is subject to taxes and other Govt. levies during the tenure of the deposit.

Deposit Pension Scheme:

Dhaka Bank is well poised to be the leading Personal Banking business amongst the local private banks. Bank’s conscious efforts in brand building, introducing and supporting new packaged products, developing PB organization along with non-traditional delivery channels have resulted in good brand awareness amongst its chosen target markets. Installment based savings schemes are a major category of saving instruments amongst mid to upper middle-income urban population.

DPS is an installment based savings scheme (Deposit Pension Scheme) of Dhaka Bank for individual clients. The key differentiators of the product will be –

- Amount of monthly deposit – The scheme offers the clients the flexibility of tailoring the amount of monthly deposit based on his monthly cash flow position. The minimum monthly deposit will be BDT 500.00 The client will have the option of depositing any amount in multiples of BDT 500.00 subject to a maximum of Tk 20,000.

- Flexible tenor of the scheme– The client has flexibility of deciding on the tenor of the scheme in-terms of number of months. However, the minimum tenor would be 48 months and the maximum would be 144 months.

- Flexibility to open any number of DPS Account– A client can open maximum five DPS accounts in client’s name, in his/her spouse’s name or in the name of his/her children or in joint names with any of his/her family members.

- Bonus point – if the client continues the scheme up-to maturity then at maturity, the client will be awarded a bonus 1% on the total deposit amount. However, to qualify for the bonus point, client may default in paying maximum 2 installments within the tenure of the DPS.

- Premature encashment – if any client closes the deposit account before one year, s/he will not be entitled to any interest. Account running more than a year will be eligible for the prevailing interest offered in the savings account.

- Late payment fee – Clients failing to deposit any installment will pay 5% late payment fee on the deposit installment amount as late payment fee, which will be realized at the time of depositing the next deposit Installment.

- Payment through Account – Clients will have to open an Account with Dhaka Bank Limited and a standing instruction will be executed for auto-debit to effect the monthly installment.

- OD Facility against DPS – Clients will have the option of taking advance upto 90% of the deposited amount at the time of application. However, to be eligible for the OD facility, the account must be at least 2 years old or the minimum ticket size of the advance will be Tk 20,000.00.

RESTRICTIONS AND CLIENT ELIGIBILITY:

- Any Bangladeshi Citizen attaining 18 years of age will be eligible to avail this product by opening an account in any of the branches of DBL. Branch will ensure compliance with account opening formalities.

- A minor operated by the legal guardian may also open the account.

- The tenor and the deposit amount agreed by the applicant and accepted by the Bank at the time of opening the account cannot be changed afterwards.

CLOSURE OF ACCOUNT:

The account will immediately cease to operate in case of the following:

- Death of the account holder and Failure to pay 5 consecutive installment

SETTLEMENT OF THE ACCOUNT:

DOCUMENTATION – In order to open the account, the account holder will execute the following documentation:

- Fulfilling Account opening formalities

- Filling up the DPS Application form

- 2 copy Pass port size Photograph of the applicant

- 1 copy passport size photograph of the nominee attested by the applicant

Income Unlimited:

The management of Dhaka Bank Limited is pleased to launch Special Deposit Scheme, a new liability product on May 04, 2005.

- § Product Name– Special Deposit Scheme

- Products Feature

| Deposit Amount | In multiples of Tk 50,000 However the minimum deposit will be Tk 1,00,000 (singly or jointly) and the maximum Tk 50,00,000 (singly/Jointly). |

| Initial Deposit Date | Any day of the month |

| Interest Due | One month after the initial deposit date the interest will be credited to the savings/current account. |

| Tenure | 3 Years |

| Monthly income on Tk 100,000 | Tk 1,000 subject to 10% Income Tax |

| Rate of Interest | 12% (simple) |

- § Opening an Account – Clients must have or open a savings account through which initial deposit will be collected. The monthly interest accrued on the deposit will be disbursed to the client through this savings/current account.

- § Deposit Mode – The depositor(s) will have the option of making the initial deposit to the new / existing savings account in cash or through an account payee cheque.

- § Interest Payout Mode – Interest payout mode should be transfer to savings account.

- § Interest Payout Frequency – Interest Payout Frequency should be monthly.

- § Renewal / Redemption Instruction – Maturity / Renewal Instruction should only be “Renew principal and redeem interest” or Redeem interest & principal

- § Closure Of Account – The account will immediately cease to operate in case of death of the depositor

- § Settlement Of Account – The account will be settled in line with the instructions laid down in the account opening forms in case of death of the accountholder.

- § Premature Encashment – If any client chooses to withdraw the deposit before the tenure, then s/he will only be entitled to prevailing interest rate on savings account in addition to the initial deposit. However, withdrawal of the deposited amount before one year will not earn any interest to the depositor(s). Amount already paid to the clients monthly along with the tax should be adjusted accordingly.

- § Settlement of pre-mature encashment

| Premature encashment before Maturity, but after one year | The client will be entitled to prevailing interest rate on the savings account | The interest already credited to the clients account on a monthly basis to be adjusted against principal deposit at the time of premature encashment |

| Premature encashment before Maturity and before one year | The client will be entitled no interest | The interest already credited to the clients account on a monthly basis to be adjusted against principal deposit at the time of premature encashment |

- § OD Facility against Deposit – Clients will have the option of taking advance upto 90% of the deposited amount at the time of application. The prevailing lending rate will be effected against the advance.

- § Documentation – In order to open the account, the account holder will execute the following documentation:

Fulfilling Account opening formalities

Filling up the SDS Application form

1 copy Passport size Photograph of the applicant

1 copy passport size photograph of the nominee attested by the applicant

- § Restrictions and Client Eligibility

Any Bangladeshi Citizen attaining 18 years of age will be eligible to avail this product by opening an account in any of the branches of DBL. Branch will ensure compliance with account opening formalities.

A minor operated by the legal guardian may also open the account.

The deposited amount and the tenure agreed by the applicant and accepted by the Bank at the time of opening the account cannot be changed afterwards.

Smart Plant:

Smart Plant offers you to multiply your initial cash to 10 times in 6 years. You are required to deposit at least Taka 10,000 or multiple of it to avail the opportunity. In single name you can deposit maximum Taka 50, 00,000. Dhaka Bank shall contribute 4 times of your deposited amount to build up a fund for issuance of Smart Plant.

Maturity period of the Smart Plant is 6 years.

The total Smart Plant amount (your deposit + Bank Contribution) will double in 6 years. For example; if you deposit Taka 10,000, bank shall contribute Taka 40,000, altogether the Smart Plant amount will be Taka 50,000. On maturity (after 6 years) the Smart Plant amount will be Taka 1,00,000.

You will repay the bank contribution amount in 72 equal installments. After repayment of all installments the matured value will be credited in your savings account. If you fail to pay the installment within the due date, a late payment fee of 2% per month of the installment amount will be charged. If you are a Bangladeshi with an age more than 18 years and not exceeding 54 years, you can avail Smart Plant. to minimum Taka. You are required to open a Savings account or Smart Account to maintain the Smart Plant.

What will happen if I die before Smart Plant maturity?

Your nominee shall get matured value of Smart Plant if you demise prematurely before completing Smart Plant period. However, death from Self-inflicted injury, Suicide during the first year of insurance coverage, AIDS and HIV related disease, Abuse of alcohol or drugs, War, or riot, or civil commotion, Illegal act/criminal activity, Death due to any reason within the first 3 months of coverage except for accidental death, Natural Disaster viz. Earth Quake, Tsunami etc

Personal Loan:

As part of establishing a personal banking franchise of Dhaka Bank Limited, the bank has successfully launched Personal Loan. The product is a term financing facility to individuals to aid them in their purchases of consumer durables or services. The facility becomes affordable to the clients as the repayment is done through fixed installment s commonly known as EMI (equal monthly installment) across the facility period.

| Loan amount limits under the program | Type of Loan | Minim loan amount | Maximum loan amount |

| Personal | BDT 25,000 | BDT 500,000 |

Car Loan:

- As part of establishing a personal banking franchise of Dhaka Bank Limited, the bank has successfully launched Car Loan. The product is a term financing facility to individuals to aid them in their pursuit of has a car of their dream. The facility becomes affordable to the clients as the repayment is done through fixed installment s commonly known as EMI (equal monthly installment) across the facility period. Depending on the size and purpose of the loan, the number of installments varies from 12 to60 months.

| Loan amount limits under the program | Type of Loan | Minimum loan amount | Maximum loan amount |

| Car | TK.2,00000 | Tk.20,00,000 |

Vacation Loan:

As part of establishing a personal banking franchise of Dhaka Bank Limited, the bank has successfully launched Vacation Loan. The product is a term financing facility to individuals to aid them in their pursuit of spending a vacation in the country or abroad. The facility becomes affordable to the clients as the repayment is done through fixed installment s commonly known as EMI (equal monthly installment) across the facility period. Depending on the size and purpose of the loan, the number of installment varies from 12 to 48 months.

| Loan amount limits under the program | Type of Loan | Minimum loan amount | Maximum loan amount |

| Vacation | BDT 25,000 | BDT 500,000 |

Home Loan:

The product is a term financing facility to individuals to aid them in their purchases of apartment or house or construction of house. The facility will become affordable to the clients as the repayment is done through fixed installment as commonly known as EMI (equal monthly installment) across the facility period. Depending on the size of the loan, the maximum period of the loan would be (20 years). The amount of loan TK.1, 00000 to 75, 00000

Any Purpose Loan:

Its time to do a few things you really wanted to.

Introducing “Any Purpose Loan” from Dhaka Bank Limited. Now you can get loan up to Tk. 500,000* to spend it any way you choose to. Just walk into any of our branches and walk out loaded

Services of DBL:

Personal Banking:

Amongst Private Sector bank’s, Dhaka Bank has already made its mark in the personal banking segment. The promotions like “Baishakhi Offer”, a strategic tie up with Electra International Limited, distributor of Samsung brand products, and “Freeze the Summer Campaign” a strategic tie-up with Esquire Electronics Limited, distributor of Sharp/General Brand electrical appliances saw Dhaka Bank to experience more than a reasonable growth on the personal banking business in 2008.

Corporate Banking:

Providing a tailored solution is the essence of our Corporate Banking services. Dhaka Bank recognizes that corporate customers’ needs vary from one to another and a customized solution is critical for the success of their business.

Dhaka Bank offers a full range of tailored advisory, financing and operational services to its corporate client groups combining trade, treasury, investment and transactional banking activities in one package.

Whether it is project finance, term loan, import or export deal, a working capital requirement or a forward cover for a foreign currency transaction, our Corporate Banking Managers will offer you the right solution. You will find top-class skills and in-depth knowledge of market trends in our corporate Banking specialists, speedy approvals and efficient processing fully satisfying your requirements – altogether a rewarding experience.

Their experience in handling Corporate Banking business covers a wide span of businesses and industries. You can leverage on our expertise in the following sectors particularly:

-Telecom, Media and Technology

– Textile, Ready Made Garments

– Edible Oil, Consumer and Diversified Industries

– Shipping, Ship Breaking, Steel and Engineering

– Energy, Chemicals and Pharmaceuticals

– Cement and Construction

– Financial Institutions

Floating of Public Issues:

The Bank assists companies to underwrite public issues. Dhaka Bank has successfully participated in a number of issues.

Loan Syndication:

DBL participates in a number of loan syndication arrangements involving foreign investment has been highly acclaimed. The projects we have handled as the lead arranger or co-arranger with other banks and financial institutions include production and export oriented ventures in power generation, cement production, food processing and a large undertaking in leisure and amusement.

Islamic Banking:

Dhaka Bank Limited offers Shariah based Islamic Banking Services to its clients. The bank opened its First Islamic Banking Branch on July 02, 2003 at Motijheel Commercial Area, Dhaka. The second Islamic Banking branch of the bank commenced its operation at Agrabad Commercial Area, Chittagong on May 22, 2004.Dhaka Bank Limited is a provider of on line banking services and any of its clients may avail Islamic Banking services through any of the branches of the bank across the country.

Capital Market Services:

Capital Market Operation besides investment in Treasury Bills, Prize Bonds and other Government Securities constitute the investment basket of Dhaka Bank Limited. Interest rate cut on bank deposits and government savings instruments has contributed to significant surge on the stock markets in the second half of 2004, which creates opportunities for the Bank in terms of capital market operations. The Bank is a member of Dhaka Stock Exchange Limited and Chittagong Stock Exchange Limited.

Capital Market Division conducted a total trade of tk.2,045 million against tk.1,164 million in 2005. Gross Operating profit from Capital Market Services Division is tk.39.80 million against tk.5 million in 2005.

ATM Card services:

| Card Features |

- Cash Withdrawals – up to Tk.1 Lac per day

- Utility payments – T&T, Mobile phones, DESA, etc.

- Multi-account access

- Fund Transfers

- Mini Statements

- PIN change

To apply, please contact your Dhaka Bank Branch or Card Centre (+8802 9553104, ext 212)

Features:

- Cash Withdrawals – up to Tk.1 Lac per day

- Utility payments – T&T, Mobile phones, DESA, etc.

- Multi-account access

- Fund Transfers

- Mini Statements

- PIN change

Credit Card Services:

Get it in just 7 days, or free!

Dhaka Bank Limited brings you Your Everyday Credit Card in the shortest possible time. We recognize that you need your card every day. That is why we have developed processes to guarantee delivery of your card in just 7 days when you apply for a fully secured card; for an unsecured card it will be ready in just 10 days. Otherwise we will give you the card free – the subscription fee completely waived!

What you can do with your Dhaka Bank Credit Card

Everything you would expect from a credit card. You can use it at all the merchant locations that display the Vanik Card sticker. That’s not all. You can also use it at all the locations that display the Card sticker. And that’s a whopping 1,700 merchants and more than 50 products and services. What’s more, we are always increasing our merchant locations. An updated list is available from our Card Centre.

Free Spouse Card:

Your spouse needs a card too for everyday use. That is why we offer a card to your spouse absolutely FREE. Your spouse can enjoy the same facilities as you do. So, you won’t have to worry about whether either of you are carrying enough cash.

Convenience:

Unlike other cards, all branches of Dhaka Bank Ltd. can accept your bill payments and handle your card service requests. You may open an account as well with any of these branches to conduct all your banking and card service requirements under one roof.

Flexible Repayment Options:

Dhaka Bank Credit Card offers you credit facility absolutely FREE up to a maximum of 45 days. You get 15 days time from the date of statement to repay your dues. You can pay in full within 15 days (and save money; no interest accrued, no payout) or in part. The minimum amount required to pay is 1/12th of the total amount or Tk. 200 (whichever is higher). The revolving credit line of your card allows you to select payment terms to suit your other financial commitments.

Quick Replacement:

If card has been lost or stolen, a replacement will be sent to the client within a couple of days. But remember to report the loss as soon as you have detected it. Once reported, there will be no liability on fraudulent.

Locker Services:

A client could use the locker facility of Dhaka Bank Limited and thus have the option of covering your valuables against any unfortunate incident.

DBL offer security to our locker service as afforded to the Bank’s own property at a very competitive price.

DBL would be at your service from Saturday through Thursday from 9:00 am to 4:00 pm.

Lockers are available at Gulshan, Banani, Dhanmondi, Uttara, CDA Avenue & Cox’s Bazar Branch.

Online Banking Services:

Dhaka Bank Limited introduces Net Banking and intends to maintain the lead with enhanced facilities through this media. Client can get access to real time account information through the Internet. Transfer money from his/her account, utility bill payment and more. Through on–Line Banking Services, clients can deposit to and withdraw from his/her account held with a particular branch up to a limit of Tk: 10,000.00 through any branch of Dhaka Bank Limited

Internet Banking Services:

Through Internet banking the client can access the account to view and print the balance account statement for last 20 (twenty) transactions.

CREDIT RATING & CAPITAL PRESERVATION OF DBL

Banks are among the most important financial institutions in the economy. They are the principle source of credit (loan able fund) for millions of households (individuals and families) and for most local units of government. Moreover, for small businesses ranging from grocery stores to automobile dealers, banks are often the major source of credit to stock the shelves with merchandise or to fill a dealer’s showroom with new goods. When the business and consumers need financial information and financial planning, it is the bankers to whom they turn most frequently for advice and council.

Worldwide, banks grant more installments loans to consumers than any other financial institution. Banks are among the most important source of short-term working capital for businesses and have become increasingly active in recent years in making long-term business loans for new plant and equipment.

Dhaka Bank Limited is a financial intermediary that offers the widest range of financial services- especially credit, savings, and payment services-and performs the widest range of financial functions of any business firm in the economy. This multiplicity of bank services and functions has led to banks being labeled “financial department stores”.

CREDIT RISK:

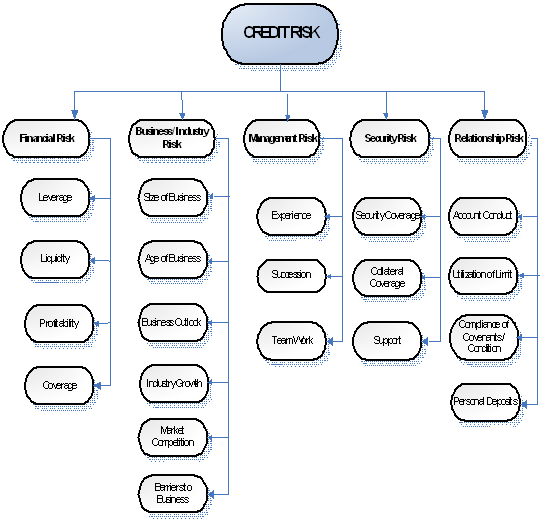

George E. Peterson (1998) defines credit risk, as “Credit risk is the risk that a borrower will not make full and timely payment of debt service. Once a borrower falls behind in debt servicing, credit risk also involves the relative size and probable duration of default.” It is one of the significant risks a bank is exposed to. Each of the risk areas requires to be evaluated and aggregated to arrive at an overall risk grading measure.

a) Evaluation of financial risk: Financial analysis of leverage, liquidity, profitability and interest coverage ratios will help to analyze the risk that borrower might fail to meet obligation due to financial distress.

b) Evaluation of Business/Industry Risk: Analyzing the business outlook, size of business, industry growth, market completion and barriers to entry or exit to understand the industry situation or unfavorable business condition that might have an impact on borrower’s capacity to meet obligation. This capitalizes on the risk of failure due to low market share and poor industry growth.

c) Evaluation of Management Risk: Due to poor management skill, experience of the management, its succession plan and teamwork might cause the borrower to default.

d) Evaluation of Security Risk: Risk that the bank might be exposed due to poor quality or strength of the security in case of default. This may involve the strength of security and collateral, location of collateral and support.

e) Evaluation of Relationship Risk: These risk areas cover evaluation of limits utilization, account performance, conditions / covenants compliance by the borrower and deposit relationship.

CREDIT RISK ANALYSIS:

The term credit analysis is used to describe any process for assessing the credit quality of a company or individual. Credit analysis include credit scoring, it is more commonly used to refer to process that entail human judgment. Credit professionals in banks review the client’s balance sheet, income statement, recent trends in its industry, the current economic environment, etc. from this they can also assess the exact nature of an obligation. Based on this analysis, the credit manager assigns the client a credit rating, which can be used for making credit decision.

Many banks, investment managers and insurance companies hire their own credit analysts who prepare credit ratings for internal use. In Bangladesh there are two rating agencies one is CRAB (Credit Rating Agency of Bangladesh) and another is CRISAL. These two does the rating of all organizations.

Figure 1: Credit Risk Components.

Principal Risk Components: | Weight: |

Financial Risk | 50% |

Business/Industry Risk | 18% |

Management Risk | 12% |

Security Risk | 10% |

Relationship Risk | 10% |

Assign weight ages to each of the key parameters:

| Principal Risk Components | Key Parameters | Weight |

| Financial Risk |

| 50% |

Leverage | 15% | |

Liquidity | 15% | |

Profitability | 15% | |

Coverage | 5% | |

| Business/Industry Risk |

| 18% |

Size of Business | 5% | |

Age of Business | 3% | |

Business Outlook | 3% | |

Industry growth | 3% | |

Market Competition | 2% | |

Entry/Exit Barriers | 2% | |

| Management Risk |

| 12% |

Experience | 5% | |

Succession | 4% | |

Team Work | 3% | |

| Security Risk |

| 10% |

Security coverage | 4% | |

Collateral coverage | 4% | |

Support | 2% | |

| Relationship Risk | 10% | |

Account conduct | 5% | |

Utilization of limit | 2% | |

| Compliance covenants/condition | 2% | |

| Personal deposit | 1% |

How is Credit Risk MEASURED?

Credit risk is usually measured on a comparative scale. As per BRPD (Banking Regulation and Policy Department), CRG (credit Risk Grading) score sheet, a scale, is used to summarize risk assessments. Since there is no accurate way to combine the different risk factors, credit professionals either examine and weigh the underlying risks directly, or confirm the track record over time of a credit rating system to discriminate effectively between high and low-risk lending in a particular bank.

GUIDELINES ON CREDIT RISK MANAGEMENT:

Credit risk is the primary financial risk in the banking system. Identifying and assessing credit risk is essentially a first step in managing it effectively. In 1993, Bangladesh Bank as suggested by Financial Sector Reform Project (FSRP) first introduced and directed to use Credit Risk Grading system in the Banking Sector of Bangladesh under the caption “Lending Risk Analysis (LRA)”. The Banking sector since then has changed a lot as credit culture has been shifting towards a more professional and standardized Credit Risk Management approach.

Credit Risk Grading system is a dynamic process and various models are followed in different countries & different organizations for measuring credit risk. The risk grading system changes in line with business complexities. A more effective credit risk grading process needs to be introduced in the Banking Sector of Bangladesh to make the credit risk grading mechanism easier to implement.

Keeping the above objective in mind, the Lending Risk Analysis Manual (under FSRP) of Bangladesh Bank has been amended, developed and re-produced in the name of “Credit Risk Grading Manual”The Credit Risk Grading Manual has taken into consideration the necessary changes required in order to correctly assess the credit risk environment in the Banking industry. This manual has also been able to address the limitations prevailed in the Lending Risk Analysis Manual.

Credit Risk Grading (CRG):

Credit risk grading is an important tool for credit risk management as it helps the Banks & financial institutions to understand various dimensions of risk involved in different credit transactions. The aggregation of such grading across the borrowers, activities and the lines of business can provide better assessment of the quality of credit portfolio of a bank or a branch. The credit risk grading system is vital to take decisions both at the pre-sanction stage as well as post-sanction stage.

At the pre-sanction stage, credit grading helps the sanctioning authority to decide whether to lend or not to lend, what should be the loan price, what should be the extent of exposure, what should be the appropriate credit facility, what are the various facilities, what are the various risk mitigation tools to put a cap on the risk level.

At the post-sanction stage, the bank can decide about the depth of the review or renewal, frequency of review, periodicity of the grading, and other precautions to be taken.

Having considered the significance of credit risk grading, it becomes imperative for the banking system to carefully develop a credit risk-grading model that meets the objective outlined above

Definition of Credit Risk Grading:

- The Credit Risk Grading (CRG) is a collective definition based on the pre-specified scale and reflects the underlying credit-risk for a given exposure.

- A Credit Risk Grading deploys a number/ alphabet/ symbol as a primary summary indicator of risks associated with a credit exposure.

Credit Risk Grading is the basic module for developing a Credit Risk Management system.

Importance of Credit Risk Grading:

1. Well-managed credit risk grading systems promote bank safety and soundness by facilitating informed decision-making.

2. Grading systems measure credit risk and differentiate individual credits and groups of credits by the risk they pose. This allows bank management and examiners to monitor changes and trends in risk levels.

3. The process also allows bank management to manage risk to optimize returns.

Use of Credit Risk Grading:

- The Credit Risk Grading matrix allows application of uniform standards to credits to ensure a common standardized approach to assess the quality of individual obligor, credit portfolio of a unit, line of business, the branch or the Bank as a whole.

- As evident, the CRG outputs would be relevant for individual credit selection, wherein either a borrower or a particular exposure/facility is rated. The other decisions would be related to pricing (credit-spread) and specific features of the credit facility. These would largely constitute obligor level analysis.

Risk grading would also be relevant for surveillance and monitoring, internal MIS and assessing the aggregate risk profile of a Bank. It is also relevant for portfolio level analysis.

Credit Risk Grading:

The following CRG is being set by the Bangladesh Bank, which helps to evaluate the borrower. Risk manager will input data available from their income statement, balance sheet and cash flow to the (FSS) known as Financial Spread Sheet, which will calculate the risk ratio and provide the score based on the total score of profitability, risk ratio etc. manager will grade the client. A borrower will be categorized ‘Superior’ when he will provide full-cash security, or guaranteed by the government or international bank. This type of guarantee is superior because there is zero possibility of loan being classified or zero exposure. Next, a borrower is classified as ‘Good’ when the score is 85 or more. ‘Acceptable’ when his credit risk grading score is between 75 and 84. Banker need not to be worry till the score is 75 because they are considered to be ‘Good-performing loan’. When the client is ranked ‘Marginal’ banker needs to be careful about sanctioning loan because this client has 50% probability that he might classify. Then as the score become less by 10 points the client will be categorized ‘Special Mention’, ‘Substandard’, ‘Doubtful’ and ‘Bad/Loss’ when score is below 35. These four are called Non-performing loan. This scoring system is a decision making tool.

Table: Credit Rate Grading (CRG)

Number | Grading | Abbreviate | Score |

1 | Superior | SUP | 100% Fully cash secured, secured by government guarantee/international bank guarantee |

2 | Good | GD | 85+ Strong repayment capacity of the borrower, excellent liquidity, low leverage, consistent strong earnings and cash flow. |

3 | Acceptable | ACCPT | 75-84 Not strong as GOOD grade borrower but has consistent earnings, cash flow and a good record of accomplishment. |

4 | Marginal/Watch list | MG/WL | 65-74 Borrower having an above average risk due to strained liquidity, higher than normal leverage, thin cash flow and /or inconsistent earnings. |

5 | Special Mention | SM | 55-64 Potential weaknesses that deserve management’s close attention. If left uncorrected, these weaknesses may result in a deterioration of the repayment prospects of the borrower. |

6 | Substandard | SS | 45-54 Weak financial condition, capacity to repay is in doubt. |

7 | Doubtful | DF | 35-44 Full repayment of principal and interest is unlikely and the possibility of loss is extremely high. Due to specifically identifiable pending factors such as litigation, liquidation procedures or capital injection, the asset is not yet classified as Bad & Loss. |

8 | Bad / Loss | BL | <35 Long outstanding with no progress in obtaining repayment or on the verge of wind up/liquidation. Prospects of recovery are poor and legal options have been pursued. |

Source: Bangladesh Institute of Bank Management, Mirpur, Dhaka, May 2006

Ultimately, if client wants to ensure a good credit score they should keep financially fit and deal responsibly with their financial commitments. It is confidence that a loan will be paid back on schedule that determines whether credit is granted.

Re-assessing clients regularly is always a good practice for ensuring proper risk management and financial growth in banks. DBL updates the records with the latest financial statement of the client every year and sometimes every six months for clients. It is a good practice from a credit-risk control standpoint.

Amendment of delegation of Credit authorities to the Management Credit Committee. As on 11 March,2008

| Credit Facilities | Individual/ Business Firm | Individual/ Public Ltd Company. | ||

| 1 | LC | Letter of Credit (Sight with minimum 05% cash margin) (Except for machinery) | TK.500.00 Lac | TK.900.00 Lac |

| 2 | ||||

LTRLoan against Trust Receipt (LTR): (With collateral): Up to 50% of collateral value (DV)

TK.450.00 Lac

TK.700.00 Lac

Loan Against Trust Receipt (LTR) : (With out collateral security)

TK.100.00 Lac

TK.200.00 Lac

3LIMLoan Against Improved Merchandise (LIM)

TK.400.00 Lac

TK.700.00 Lac

4CC(H)Cash credit (Hypo) : with collateral security: Up to 50% of Collateral Value (DV) only for existing clients

TK.100.00 Lac

TK.200.00 Lac

5CC (P)Cash Credit (Pledge): in Bank’s Godown ( only for existing clients)

TK.100.00 Lac

TK.200.00 Lac

6SODSecured Overdraft (SOD)Financial obligation): (Up to 90% of Present value of eligible instrument with minimum 02% spread)

TK.2500.00 Lac

TK.2500.00 Lac

7OD(W/O)Overdraft (Work Order- With collateral ): Up to 50% of collateral value (DV) Work orders from Govt, Semi Govt. Autonomous Bodies, Multinational companies & Scheduled Bank assignment of bill in favor of Bank.

TK.2000.00 Lac

TK.500.00 Lac

Overdraft (Work order) without collateral:

TK.100.0 Lac

TK.200.00Lac

8OD(O)Overdraft (Work Order- With collateral ): Up to 50% of collateral value (DV) Work orders from Govt, Semi Govt. Autonomous Bodies, Multinational companies & Scheduled Bank assignment of bill in favor of Bank.

TK.50.00 Lac

TK.50.00 Lac

9STLShort Term Loan (STL) : only for existing regular clients

TK.50.00 Lac

TK.50.00 Lac

10IBPInland bill Purchase ( Up to 90% of bill amount) subject to obtaining bills on due from respective scheduled Banks

TK.500.00 Lac

TK.500.00 Lac

11BGBank Guarantee (BG): At 100% margin/cash collateral

Any amount

Any amount

Bank Guarantee (BG): -Open EndedLAt 50% margin)

TK.200.00 Lac

TK.200.00 Lac

Bank Guarantee (BG)- Bid Bond : (At 10% cash margin)

TK.50.00 Lac

TK.250.00 Lac

Bank Guarantee (BG): – Performance Guarantee (PG) and Advance Payment Guarantee (APG): (At 10-25% margin)

TK.50.00 Lac

TK.250.00 Lac

12LFLease Finance (Other than machinery)

TK.100.00 Lac

TK.200.00 Lac

It was decided that all credit related memorandums bear the signature Of Head Office, Deputy Managing Director (Risk Management) and the Managing Director and delegation to be applied as per notes outline in the Memo.

CAPITAL & LARGE LOAN POSITION OF DHAKA BANK LIMITED

As on 31.12.2008

Total Capital | TK.480.82 Crore |

Maximum Loan to a Single Borrower/Group (other than export clients) | TK.168.29 Crore(35% of Capital) |

Maximum Funded Liability to a single Borrower/Group | TK.72.12 Crore (15% of Capital) |

Maximum Nom-Funded Liability to a Single Borrower/ Group | TK.168029 Crore (35%* of capital) (if funned is not availed, than up to 35%) |

Large Loan limit for a single Borrower/Group | TK.48.08 Crore (10% of capial) |

Maximum Loan to a Single /Group (for export clients) | TK.240.41 Crore (50% of Capial) |

Some are parts:

Report on Credit Rating and Capital Preservation of Dhaka Bank Ltd(Part 1)

Report on Credit Rating and Capital Preservation of Dhaka Bank Ltd(Part 2)