The purpose of this report is to analysis Performance Analysis & Portfolio Management of ICB AMCL Mutual Fund. Other objectives of the report are to review the working process of the Investment Corporation of Bangladesh and to analyze the different functions managed by different departments of ICB. Finally, identify some problems of ICB’s mutual fund operation evaluate the mutual funds for taking the investment decision.

Objectives of the report:

The objectives of the report are:

- To relate theoretical learning with the practical situation.

- To review the practical aspect of the Investment Corporation of Bangladesh.

- To go through all departments of the corporation and observe how the works are going on.

- To investigate the different functions performed by different departments of ICB.

- To know how ICB floats and manage the mutual funds.

- To explore the problems of ICB’s mutual fund operation.

- To evaluate the mutual funds for taking the investment decision.

The scope of the report:

The main focus of the study is “Performance Analysis and Portfolio Management of the ICB AMCL Mutual Fund”. But the report has tried to cover an overview of ICB AMCL’s objectives, functions, management, business policy and other things. This report has also mentioned some problems of ICB AMCL‟s mutual fund and its solutions. The empirical part includes only the published information and current practices of the ICB Asset Management Company Ltd.

Methodology:

Nature of data:

- Ending price of the concerned companies in the portfolio

- Share price of the shares on the last trading day of June month

- Only DSE listed companies would be taken

- Data range from 2010-2012

- Dividend, P/E ratio, etc of all Mutual Funds of ICB AMCL

Data collection method:

The information and data for this report were collected from primary and secondary sources.

- Primary Sources: Primary data were collected through interviews and discussions with the officials of various departments.

- Secondary Sources: The secondary data were collected with several relevant articles of the ICB. These are given below:

- ICB AMCL annual report (2012)

- Annual report of Mutual Funds (2012)

- Other materials of the corporation

- The report would be prepared by the previous student

- DSE library

Data processing:

Data collected from secondary sources have been processed quantitative and qualitative approaches have been used in the report.

Data analysis and interpretation

The report relies on an analytical judgment, critical reasoning and table and graph analysis, ratio analysis, Efficiency measurement of ICB portfolio Management through Treynor model, Sharpe measure and efficient allocation of the resource with the solver.

Background of ICB AMCL:

ICB Asset Management Company Ltd. was established as part of the restructuring program of ICB under Capital Market Development Program (CMDP) initiated by the Government of Bangladesh and the Asian Development Bank. The Company was incorporated as a public limited company with an authorized capital of Tk. 100 crore and a nominal paid up capital of Tk. 2.00 lac, which was subsequently increased to Tk. 12.00 crore, under the Companies Act, 1994 with the Registrar of Joint Stock Companies and Firms on December 05, 2000. The Company obtained the license on October 14, 2001, from the Securities and Exchange Commission (SEC) under to carry out the mutual fund activities. The company started its operation from July 01, 2002 upon issuance of Govt. gazette notification.

The company is engaged in investment management; more specifically floating and managing both open-end and closed-end mutual funds. The company is dedicated towards development of mutual fund industry as well as the capital market of Bangladesh.

WHAT IS ASSET MANAGEMENT COMPANY LIMITED?

The company which undertakes the task of floating and managing the schemes delegated by the trustee. The Company is usually considered professionally sound and experts who are known for smart stock picks. AMC charges a fee for the services it renders to the fund. The company acts as the investment manager of the fund under broad supervision and direction of the trustees. The AMC must have a considerable net worth at all times and it cannot act as a trustee of any other mutual fund.

BASIC FUNCTIONS

| Underwriting of initial public offering of shares and debentures | |

| Underwriting of right issue of shares | |

| Direct purchase of shares and debentures including Pre-IPO placement and equity participation | |

| Providing lease finance to industrial machinery and other equipment singly or by forming syndicate | |

| Managing investors’ Accounts | |

| Managing Open-End and Closed-End Mutual Funds | |

| Operating on the Stock Exchanges | |

| Providing investment counsel to issuers and investors | |

| Participating in Government divestment Program | |

| Participating in and financing of, joint-venture projects | |

| Dealing with other matters related to capital market operations | |

| Trusty, Custodian, Bank Guarantee | |

| Consumer Credit |

INTRODUCTIONS OF ICB AMCL MUTUAL FUNDS

MUTUAL FUNDS

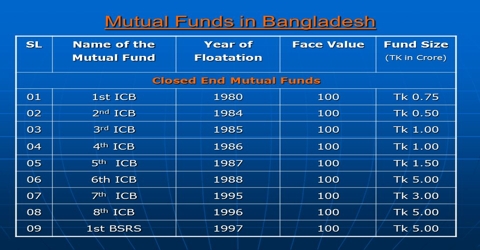

ICB Asset Management Company Ltd. has so far floated eleven closed-end mutual funds and two open-end. Mutual Funds through which the small and medium savers get opportunities to invest their savings in a balanced and relatively low-risk portfolio. The aggregate size of these funds is around Tk. 815.00 core.

A Mutual Fund is a Trust Fund established with the intention of investing a pool of savings in various types of securities for the benefit of investors. A small investor is unable to diversify his portfolio simply because of the inadequate amount available for investment. A mutual fund provides a means of diversification of investment to small investors. Initially, a mutual fund collects the funds from small investors and then they are invested in the securities of different types, thus diversifying the portfolio. The Mutual Fund serves as a link between the public and the capital market. The income earned through these investments is shared by its holders in proportion to the number of units owned by them. Due to the diversification of investment and professional management, investing through mutual fund carries lesser risk than investing individually.

HISTORY OF MUTUAL FUND

The concept of Mutual Fund was developed in the early nineteenth century. However, the first modern-day mutual fund was opened in America in 1924. The growth of the mutual fund industry stalled due to the great depression of the 1930s like many other economic activities. Mutual Funds became mainstream investments in the USA and the world in the 1990s. The number of mutual fund in the world stood at over 53500 at the end of June 2003 of which maximum of 59% was in America followed by 32% in Europe and 9% in Africa and the Asia Pacific. By type of fund, 42% were equity funds, 31% were debt fund and 21% were balanced/mixed fund, the rest 6% were unclassified fund.

OBJECTIVES OF THE MUTUAL FUND

- Providing regular, steady & Attractive dividend

- Investing the funds both in capital & money market instruments

- Stable the Capital Market

- To encourage and broaden the base of investment

- To develop the capital market.

- To provide for matters ancillary thereto.

- To mobilize savings.

- To promote and establish subsidiaries for business development.

INVESTMENT STRATEGY & POLICIES

Performance rigorous and in-depth analysis and evaluation have coned The Company Mostly Follow an investment strategy, which focuses on income, value, and growth. ‘Funds investment decisions were based on fundamental judgment and entry and exit strategy according to market opportunities. Investments are generally made in securities with strong fundamentals, future prospects in terms of return risk corporate management and other acted to pick securities for investment. The investment portfolios have been designed in such a manner as to provide sufficient liquidity to pay obligations as they become due. No concentration of investment in a particular company or sector has been made, rather investment has been diversified in accordance with the guidelines as laid down in the Securities & Exchange Commission (Mutual Fund) Ordinance, 2001.

RISK MANAGEMENT

Market Risk: The Funds primarily invest in shares of listed securities. Investment in shares carries the risk that is considered higher than that of investment in debt securities. Capital Invested in the stock market could, in extreme circumstances, lose its entire value. The company manages market risk by monitoring exposure to marketable securities by following the internal risk management policies and investment guidelines approved by the Securities & Exchange Commission and the Board of Directors of the Company.

Credit Risk: The credit risk arising from the possibility of default by participants or failure of the financial markets/stock exchange, the depositors, the settlements or clearing system, etc. is covered by the internal risk management policies and investment guidelines.

Liquidity Risk: The Company manages the liquidity risk by investing a maximum portion of the Fund’s assets in highly liquid shares and money market instruments.

Market Rate of Return Risk (MROR): MROR risk is the risk that the value of a financial instrument will fluctuate due to changes in the market interest rates. The Fund has minimal MROR exposure as it primarily invests in highly rated listed securities and money market instruments.

TYPES OF MUTUAL FUNDS

1) Open-ended mutual fund

Open-ended mutual funds are those Funds where subscription and redemption of units are allowed on a continuous basis. These schemes do not have a fixed maturity period. Investors can buy or repurchase the units at any time at NAV /NAV based prices declared by the fund manager on the daily or weekly basis.

2) closed-end mutual fund

Closed-end mutual funds are those Funds where the shares are initially offered to the public and are then traded on the secondary market.

3) Mutual fund by investment style

Over a period of time, the fund managers have developed a variety of products to cater to the needs of the investors. They are:

- Growth funds

This fund offers the potential for appreciation in share value, rather than the dividend. Such funds invest in stocks and have the tendency to outperform other funds and other modes of savings over a period of time.

- Income funds

This fund offers the lucrative dividend but the very little potential for growth. This fund mainly invests in government paper, bonds issued by municipal or local bodies, corporate debts and in stocks which offer the regular dividend.

- Balanced funds

The balanced funds offer prospects of both moderate appreciations in share value as well as current income. The fluctuation in share price may be low. Such funds invest in stocks, corporate debts, and Government paper.

4) Money market mutual funds

Such funds have an objective of taking advantage of the volatility in interest rates in the money market instruments. The funds are invested in the certificate of deposits, inter-bank call money market, commercial papers, T-bills and Short-term securities with a maturity period of less than one year.

5) Index funds

The objectives of these Funds are to increase the value of the portfolio in line with the benchmark index. The funds are invested in the shares of companies as included in the benchmark index in the same proportion.

6) Leveraged funds

These funds have an objective of increasing the value of the portfolio and benefit the shareholders by gains exceeding the cost of funds. The funds are invested in speculative and risky investments like short sales to take advantage of declining market.

ADVANTAGES OF MUTUAL FUNDS

- Diversification of risk: Mutual Funds substantially lower the investment risk of small investors through diversification of investments in different sectors. The objectives of the funds are to maximize the return for a given level of risk.

- Liquidity: Mutual Funds mobilize the saving of small investors and channel them into lucrative investment opportunities. As a result, mutual funds add liquidity to the market. Moreover, as the funds are long-term investment vehicles, they reduce market volatility by offering support to scrip prices.

- Accessible: Mutual Funds provide the small investor access to the whole market which would be difficult to achieve individually.

- Reduction of transaction cost: The investors can save the transaction cost by purchasing a single share of the mutual fund.

- Flexibility: The investors can pick and choose a mutual fund to match his particular needs. They have the option of transacting their holdings from one scheme to another, get updated information and so on.

DISADVANTAGES OF MUTUAL FUNDS

- Economic scenario

As the business and economic conditions do not remain constant, the mutual fund may face some difficulties in future. Especially if the manager does not shuffle the investment portfolio with the passage of time, or some other major unforeseen disaster/event changes the investment scenario.

- Management

As the portfolio of a mutual fund is managed by the fund managers, the investors have no say in the affairs of a mutual fund although they are the owner of the fund.

- Over-diversification

There exists the danger of over-diversification which would inevitably lead to a reduced return on the portfolio.

The Net Asset Value (NAV) of the different Mutual Funds as on 30, October 2012 is enumerated below:

| Sl. No | Particulars | Face Value | At Market Price (Tk.) |

| 1. | ICB AMCL Unit Fund | 100 | 263.34 |

| 2. | ICB AMCL First Mutual Fund | 10 | 34.71 |

| 3. | ICB AMCL Pension Holders’ Unit Fund | 100 | 238.45 |

| 4. | ICB AMCL Islamic Mutual Fund | 10 | 18.30 |

| 5. | ICB AMCL First NRB Mutual Fund | 10 | 27.37 |

| 6. | ICB AMCL Second NRB Mutual Fund | 10 | 11.35 |

| 7. | Prime Finance First Mutual Fund | 10 | 12.42 |

| 8. | ICB AMCL Second Mutual Fund | 10 | 7.92 |

| 9. | ICB Employees Provident Mutual Fund One: Scheme One | 10 | 7.17 |

| 10. | Prime Bank 1st ICB AMCL Mutual Fund | 10 | 7.14 |

| 11. | Phoenix Finance 1st Mutual Fund | 10 |

MUTUAL FUNDS

ICB Asset Management Company Ltd. has so far floated eleven closed-end mutual funds and two open-end Mutual Funds through which the small and medium savers get opportunities to invest their savings in a balanced and relatively low-risk portfolio. The aggregate size of these funds is around Tk. 815.00 crore.

Conventional Mutual Funds:

| Sl.No. | Name of the Funds | Date of Launching | Nature of the Fund | Size of the Fund (TK. in crore) |

| 1. | ICB AMCL First Mutual Fund | 16/06/2003 | Close-end | 10.00 |

| 2. | Prime Finance First Mutual Fund | 04/01/2009 | Close-end | 20.00 |

| 3. | ICB AMCL Second Mutual Fund | 09/08/2009 | Close-end | 50.00 |

| 4. | ICB Employees Provident Mutual Fund One: Scheme One | 22/11/2009 | Close-end | 75.00 |

| 5. | Prime Bank 1st Mutual Fund | 06/12/2009 | Close-end | 100.00 |

| 6. | Phoenix Finance 1st Mutual Fund | 07/03/2010 | Close-end | 60.00 |

| 7. | ICB AMCl Unit Fund | 21/06/2003 | Open-end | 150.00 |

Non-Conventional Mutual Funds:

| Sl.No. | Name of the Funds | Date of Launching | Nature of the Fund | Size of the Fund (TK. in crore) |

| 1. | ICB AMCl Islamic Mutual Fund | 12/10/2004 | Close-end | 10.00 |

| 2. | ICB AMCL First NRB Mutual Fund | 28/01/2007 | Close-end | 10.00 |

| 3. | ICB AMCL Second NRB Mutual Fund | 15/05/2008 | Close-end | 100.00 |

| 4. | ICB AMCL Third NRB Mutual Fund | 28/03/2010 | Close-end | 100.00 |

| 5. | ICB AMCL Pension Holders’ Unit Fund | 18/10/2004 | Open-end | 30.00 |

| 6. | IFIL Islamic Mutual Fund-1 | 26/09/2010 | Close-end | 100.00 |

Table Conventional and Non-Conventional Mutual Funds

These funds received the spectacular response from the investors. The business of the Islamic mutual funds should be the inconsistency with the Sharia Law. With a view to tapping the savings of Non-Resident Bangladeshis (NRBs) for investment in the country’s capital market, ICB Asset Management Company Ltd. launched ICB AMCL First NRB Mutual Fund, ICB AMCL Second NRB Mutual Fund, and ICB AMCL Second NRB Mutual Fund. Investors have shown the overwhelming interest in all the mutual funds. ICB AMCL Unit Certificates and ICB AMCL Pension Holders’ Unit Certificates are sold and repurchased on the counters of ICB AMCL Head Office and the branch offices of ICB. ICB AMCL Pension Holders’ Unit Certificates are sold exclusively to the retired pension holders. ICB along with some other banks and financial institutions extend loan facility against the lien of units. The company plans to launch some other conventional mutual funds named First Agrani Bank Mutual Fund, Sonali Bank Limited 1st Mutual Fund and specialized open-end mutual fund for NRBs named ICB AMCL NRB Unit Fund.

Financial Results

- Total assets under management grew by 7.77% to BDT 25.37 billion.

- Net operating profit decreased by 23.99% to BDT 255.57 billion

- Net profit after tax BDT 233.27 billion

| Key Figures | |||||||||

| 2011-12 | 2010-11 | 2009-10 | |||||||

| BDT mn | BDT mn | BDT mn | |||||||

| total revenue income | 309.79 | 388.02 | 371.14 | ||||||

| operating revenue income | 309.24 | 387.84 | 371.13 | ||||||

| net operating profit | 255.57 | 336.22 | 325.61 | ||||||

| operating cost -income ratio(%) | 17.36 | 13.31 | 12.26 | ||||||

| Total asset Under manament | 25370.56 | 23541.59 | 13894.9 | ||||||

Table Financial Result 2011-12

Earning Summary

In spite of a long lasting downtrend in the capital market, ICB AMCL delivered a moderate financial result in FY 2011-12: Total revenue income declined by 20.16% to BDT 309.79 million. Our operating revenue income declined by 20.27% to BDT 309.24 million due to significant decrease in management and other fees and our operating profit decreased by 23.99% to BDT 255.57 million.

At 17.36% our cost income ratio was higher than 13.31% from that of the previous year, which is quite a challenging performance in the adverse capital market scenario.

Asset under management

As of June 30, 2012, total assets under management amounted to BDT 25.37 billion. Of this open-end fund accounted for BDT 6.66 billion while the remaining BDT 0.92 billion related to ICB AMCLs own assets. In 2011-12, net inflows were the largest component of BDT 5.99 billion growth in total assets under management through net inflows decreased by 36.715% i.e.BDT 3.47 billion. Market-related application accounted for BDT 5.30 billion grew by 37.71%. Due to consolidation effects, total assets under management increased by BDT 1.82 billion, which was mainly driven by the Bangladesh Funds contribution to net inflow.

Total Income

Total income from our operation decreased by 20.27% to BDT 78.60 million. The bulk of our income generates mainly from our profit on the sale of investment and management and other fees which contributed 40.94% and 52.42% respectively. Due to negative trend in capital market, our profit on sale on investment decreased by 43.31% and Management and other fees decreased by 9.35%

Operating Revenue Income

Operating Revenue Income decreased to BDT 309.24 million, driven mainly by a negative growth in profit on a sale of investment and management and other fees. Operating income decreased by 20.27%

Net Operating Profit

We recorded net operating profit of BDT 255.57 million from profit on sale on investment of the company’s own portfolio and from management and other fees for managing increased numbers of mutual funds. Overall declination of operating profit in FY 2011-12 is 23.99% by BDT 80.65 million. Staff expenses increased by 16.45% to BDT 35.42 million. The growth in operating revenues, supported by strong management fees, exceeded the growth in operating expenses, reflecting in an excellent cost-income ratio of 17.36% which was 13.31% in 2010-11.

| Particulars | 2011-12 | 2010-11 | 2009-10 |

| Operating income | 309,243,243 | 387,839,908 | 371,126,854 |

| Non operating income | 544,699 | 178,300 | 8,500 |

| Total income | 309,787,942 | 388,018,208 | 371,135,354 |

| Operating expenses | 53,676,977 | 51,620,315 | 45,513,229 |

| Non operating expenses | 9,124,257 | 15,254,587 | 16,769,731 |

| Total Expenses | 62,801,243 | 66,874,902 | 62,282,960 |

| Total operating profit | 255,566,266 | 336,219,593 | 325,613,625 |

| Net income/(Loss)Before Tax | 246,986,708 | 321,143,306 | 308,852,394 |

| Net income after Tax | 233,265,575 | 255,643,306 | 281,938,347 |

| Cost-income ratio | 17.36% | 13.31% | 12.26% |

Table Net Operating Profit

Shareholder’s Equity

On June 30, 2012, shareholder’s equity amounted to BDT 928.08 million, a decrease of BDT as of June 30, 2011. Net income attributable to shareholders increased our equity by BDT 233.27 million.

Recommendation for Appropriation of profit

The Board of Director of ICB AMCL proposed that the available Net profit Tax of BDT 233.27 million for the FY 2011-12 be appropriated as follows: Distribution of dividend 25% Stock i.e. 78.75 million, BDT 10.00 million to general reserves, BDT 143.50 million to other reserves and retained to business 1.02 million

PERFORMANCE OF OVERVIEW

- ICB AMCL First Mutual Fund

- ICB AMCL Unit Fund

- ICB AMCL Islamic Mutual Fund

- ICB AMCL Pension Holder’s Unit Fund

- ICB AMCL First NRB Mutual Fund

- ICB AMCL Second NRB Mutual Fund

- Prime Finance First Mutual Fund

- ICB AMCL Second Mutual Fund

- ICB Employees Provident Mutual Fund (One: Scheme One)

- Prime Bank 1st ICB AMCL Mutual Fund

- Phoenix Finance 1st Mutual Fund

- ICB AMCL Third NRB Mutual Fund

- IFIL Islamic Mutual Fund-1

ICB AMCL Unit Fund

Introduction

ICB AMCL Unit Fund is the first managed open-end Mutual Fund of ICB Asset Management Company Limited. With the approval of the Securities & Exchange Commission prospectus of ICB AMCL Unit Fund was published on June 16, 2003, under the SEC Rules, 2001. ICB Asset Management Company Limited is acting as the asset manager of the Fund.

What is Unit Fund?

Unit Fund is an open-end Mutual Fund through which the small & medium savers get the opportunity to invest their savings at any time to a balanced & relatively lower risk portfolio.

Investment in Unit Fund does not only contribute to the economic & Industrial development of the country but also broaden the base of ownership in the securities.

Fund Management

ICB AMCL is responsible for the managing of the fund for which the company charges the management fee on the net asset value of the fund as per the securities & exchange commission ordinance 2001. The company makes the investment of the fund for the benefit and interest of the unitholders. As per Securities & Exchange Commission (Public Issue) Rules, 2006, 10% of any Public offer is reserved for Mutual Fund.

Who Can Invest in this Fund?

Any Bangladeshi adult citizen of sound mind can invest in this fund. No organizations other than Charitable Institutions and Provident Fund trust can invest in this fund.

Investment of Non-Resident Bangladesh

The Bangladeshi citizens living abroad may invest in unit certificates in fulfilling the following conditions:

- The value of units to be paid by remittance through banking channel;

- The money invested in Unit Fund and the dividend/profits thereon are not allowed to be repatriated.

- The investors must mention their local/bank address in Bangladesh for the convenience of registration of units.

Purchase of Units

Units can be purchased by properly completed prescribed Application form collected from designated sales centers. Application form can also be collected by downloading from the website of ICB Asset Management Company Limited. Payment for the purchase of units can be made in cash or by cheque/ pay order. The cheque for the purchase of units should be drawn on banks located nearby the respective sales center.

Limit of Unit purchase

An eligible person can buy minimum 20 units and maximum 50000 in a single or joint name. The charitable organizations and the recognized provident fund may buy 500000 units certificates.

Re-Purchase of Units

Units are re-purchased by surrendering the certificates along with duly filled in prescribed Surrender Form at the prevailing re-purchase price. Prior notice is not required. Surrender value is paid through account payee cheque.

Transfer of Units

Unit certificates are transferable subject to presentation of duly filled in transfer form by the transferor and transferee. No fee is charged for transfer.

Registration Number

The registration number is issued to the unitholders. The existing unitholder is required to mention the previous registration number on the specified column of the application form when he intends to buy more units. More than one registration number is not issued to the same unitholder.

Issue of units

The certificate is issued within a maximum of 90 days from the date of sale at the cost of the fund. Money receipt given at the time of purchase is treated as allotment letter which is returnable at the time of receiving the certificates.

Price Fixation

ICB AMCL fixes the sale and re-purchases prices on the basis of the Net Asset Value of the fund following the Securities & Exchange Commission ordinance, 2001. Changes of sale and re-purchase prices of units are disclosed through the notice board, newspaper and website of the company. The difference of Tk. 5.00 between sale and re-purchase prices of units is considered as the premium of the fund.

Publication of NAV

Net Asset Value (NAV) of the Fund is calculated on the weekly basis at cost price and the market price of the portfolio as per guideline and formula approved by the Securities and Exchange Commission. NAV is published in the daily newspaper and website of the company. The Securities and Exchange Commission and Trustee of the Fund are also being kept informed of the NAV.

Transaction Period

Units are transacted on all working days from 10.00 A.M. to 2.00 P.M except Thursday. Transaction of units remains suspended during the month of July in every year.

Declaration of Dividend

The net income earned on investments of the fund on account of dividend, interest, capital gain etc. are distributed among the certificate holders as per provision of the Securities and Exchange Commission’s relevant rules. The dividend is usually declared at the end of July each year and is distributed within shortest possible time but not later than 45 days of the declaration of dividend.

Cumulative Investment plan (CIP)

Under this Scheme, a unitholder may reinvest dividend income accrued thereon for purchasing unit at a concessional rate instead of receiving the cash dividend. In this case, new units are issued at Tk. 1.00 less than the opening price of the financial year.

Income Tax benefit

- Investment in the fund provides the same tax exemptions as investment qualifying under Section 44 (2) of the Income Tax Ordinance,1984

- Dividend received on investment in the fund is treated as dividend income under Income Tax Ordinance and is exempted from tax at the hand of the investors with limits specified in the Ordinance.

- The income of the fund is also exempted from tax.

BANGLADESH FUND

Introduction:

Bangladesh Fund, a special purpose open-end growth Mutual Fund with unlimited size is floated and managed by the ICB Asset Management Company Limited (ICB AMCL) with the initial target size of the TK.5000.00 crore.The Trust Deed of the Fund was registered on April 28, 2011, under the Trust Act, 1882 and Registration Act, 1908.The Fund was registered with the Securities and Exchange Commission (SEC) on May 04, 2011 under the Securities and Exchange Commission (Mutual Fund) Rules-2011.

Sponsors of the Fund

- Investment Corporation Of Bangladesh

- Sonali Bank Limited

- Janata Bank Limited

- Agrani Bank Limited

- Rupali Bank Limited

- Bangladesh Development Bank Limited

- Sadharan Bima Corporation

- Jiban Bima Corporation

Trustee & Custodian of the Fund

ICB Capital Management Limited

Asset manager of the Fund

ICB Asset Management Company Limited

Bangladesh Fund:

Bangladesh Fund is an open-end Mutual Fund through which the large, small and medium holders get the opportunity to invest their fund at any time to a balanced and relatively lower risk portfolio. Investment in this Fund does not only contribute to the economic and industrial development of the country but also broaden the base of ownership in the securities. This mega fund is expected to play an important role in the stabilization and development of capital market particularly the securities of the country.

Objective of the Fund

The main objective of the fund is to help stabilize the capital market, long-term development of capital market, provide liquidity and depth in the market and provide the attractive dividend to the fund holders by investing the proceeds in the capital market and money market.

Risk factors

The performance of the Fund is directly related to the micro and macroeconomic situation particularly the capital market of Bangladesh. Investment in Mutual Fund involves investment risks. Government policy and tax laws may change, affecting the return on investment in the fund.

Initial size, face value & market lot

The initial target size of the fund is Tk.5000.00 core divided into 50.00 core units at par value of Tk.100.00 each. Market lot is 100 units

Fund Management

ICB AMCL, the largest Asset Management Company in the country, is responsible for managing the fund for which the company charges the management fee on the Net Asset Value (NAV) of the fund as per the Securities and Exchange Commission (Mutual Fund) Rules-2011. The Company makes the investment of the Fund for the benefit and interest of the unitholders. The Company has a very good track record of managing eleven (closed-end) and two open-end Mutual Funds. Two more mega Funds (closed-end) are in the process of floatation.

As per the Securities and Exchange Commission (Public Issue) Rules-2006, 10% of any Public offer is reserved for Mutual Fund.

Who Can Invest in this Fund?

Institutional Investors: Any government organization including state-owned Banks and Financial Institutions, autonomous bodies, private commercial Banks, insurance Companies, Non-Banking Financial Institutions, Merchant Banks, Asset Management Companies and other institutional investors; Individual Investors: Non-Residential Bangladeshis (NRB) & General Public and other individuals can invest in this Fund.

Investment by NRBs

The Bangladesh Citizens living abroad may invest in Bangladesh Fund unit certificates on fulfilling the following conditions:

- The value of units to be paid by remittance through banking channel;

- The money invested in the Fund and the dividend/profits thereon are not allowed to be repatriated;

- The investors are investors are encouraged to mention their local/bank address in Bangladesh for convenience of registration of units;

- For convenience, NRBs can invest under cumulative investment plan to reinvest their dividend earned on unit every year.

Purchase of units of the fund

Unit Certificates of the Fund can be purchased by properly completed prescribed Application From collected from designated Sales Centers and also by downloading from the website of ICB AMCL. Application for purchasing of units should be accompanied by account payee cheque/pay order/demand draft in favor “Bangladesh Fund” which should be drawn on banks located nearby the respective sales Center.

Limit of Unit Purchase

Minimum 100 unit certificates of the fund can be purchased in a single or joint name.

Repurchase of Units

The unit holders may surrender their unit certificates along with duly filled in prescribed surrender from at the prevailing re-purchase price during the business hour as specified by the ICB AMCL. The ICB AMCL shall be liable to repurchase the units on behalf of the fund. Prior notice is not required in this regard. Surrender value is paid at the prevailing surrender price through account payee cheque.

Transfer of units

The unit certificates of the fund are freely transferable by way of inheritance/gift/specific operation of the law subject to presentation of duly filled in transfer from by the transferor and transferee. Presently no fee is charged for transfer. The Unit certificates of the Fund could be purchased surrendered & transferred from the counter of the registered office of ICB AMCL, ICB branch offices and designated selling Agent’s Branches.

Registration Number

Registration Number will be issued to the Unitholders for purchasing units of the Fund. The existing unitholder is required to mention the previous registration number on the specified column of the Application from when he/she intends to buy more units. More than one registration number is not issued to the same unitholder.

Price Fixation

The ICB AMCL will fix the sale & re-purchase prices of the units on the basis of the NAV of the fund as per the Securities & Exchange Commission (Mutual Fund) Rules-2001. Changes of the sale and re-purchase prices of units are disclosed through the notice board, newspaper and website of the Company. The difference of Tk.3.00 between sale & re-purchase prices of units will be considered as the premium of the fund.

Publication of NAV

Net Asset Value of the Fund will be calculated on the weekly basis at cost price and at the market price of the portfolio as per the guidelines approved by the SEC. NAV will be published in the daily newspapers and website. The SEC & Trustee of the Fund is also being kept informed of the NAV.

Transaction Period

Unit certificates will always be available for sale and surrender/re-purchase from 10.00 a.m. to 2.00 p.m. except on the last working day and holidays of every week during book closure period of the fund. The ICB AMCL shall disclose selling price and surrender/re-purchase price of units at the beginning of business operation on the first working day of every week as per the Securities and Exchange Commission (Mutual Fund) Rules-2001.transactions of units remain suspended during the month of July every year for finalization of accounts and declaring dividends.

Declaration of dividend

The net income earned on investments of the fund on account of dividend, interest, capital gain etc. will be distributed among the certificate holders as per provision of the SEC’s relevant Rules. The dividend will usually be declared at the end of July each year and distributed among the eligible unit holders within the shortest possible time, But not later than 30 working days of the declaration of dividend.

Cumulative Investment Plan (CIP)

There will be a Cumulative Investment Plan (CIP) scheme in this fund. Under this Scheme, a unitholder instead of receiving cash dividend may re-invest such dividend income accrued for purchasing unit at a concessional rate. In such case, units will be issued at a discount of Tk.1.00 from the opening price of that financial year. This is one of the best options for NRBs who are unable to visit Bangladesh every year.

Income Tax Benefit

- Investment in the Bangladesh Fund will provide the same tax exemptions as investment qualifying under Section 44 (2) of the Income Tax Ordinance, 1984.

- Dividend received on investment in the fund will be treated as dividend income under Income Tax Ordinance and is exempted from tax at the hand of the investors with limits specified in the ordinance.

Annual Report and Accounts

Summary of annual report and accounts of the fund will be published in the daily newspaper. An investor can also collect the detailed report and accounts in exchange for nominal from ICB AMCL.

Performance Analysis of ICB Mutual Fund

Formula used for Analysis

- Average price= (Year high price+ year low price)/2

- Dividend Yield Ratio= {Dividend per certificate (DPC)/ Market price per certificate (MPC)} * 100

- Growth Rate (Based Year) = {Value of current year – value of previous year} *100

- Price- Earning (P/E) Ratio = (MPC/EPC)

- Dividend pay-out Ratio = (DPC/EPC)*100

Tables and Graph used for Analysis

Price Earnings Ratio

| Year | 1st | 2nd | 3rd | 4th | 5th | 6th | 7th | 8th |

| 2010 | 13.5 | 10.59 | 9 | 9.83 | 11.17 | 9.044 | 11.6 | 8.68 |

| 2009 | 15 | 16.56 | 10.37 | 10.82 | 15.66 | 13.59 | 17.85 | 14.77 |

| 2008 | 24.08 | 31.46 | 17.54 | 20.21 | 33.57 | 20.87 | 33.17 | 24.47 |

| 2007 | 14.26 | 11.83 | 9.47 | 9.95 | 11.06 | 10.73 | 10.3 | 12.3 |

The P/E ratio (price-to-earnings ratio) of a stock (also called its “P/E, “ERE”,” earnings multiple”, or simply “multiple”) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share.

In general, a high P/E suggests that investors are expecting higher earnings growth in the future compared to companies with a lower P/E. However, the P/E ratio doesn’t tell us the whole story by itself. It’s usually more useful to compare the P/E ratios of one company to other companies in the same industry, to the market in general or against them or against the company’s own historical P/E. It would not be used for the investor using the P/E ratio as a basis for their investment to compare the P/E of a technology company (high P/E) to a utility company (low P/E) as each industry has much different growth prospects.

It is important that investors note an important problem that arises with the P/E measure, and to avoid basing a decision on this measure alone. The denominator (earnings) is based on an accounting measure of earnings that is susceptible to forms of manipulation, making the quality of the P/E only as good as the quality of the underlying earnings number.

The P/E gives an idea of what the market is willing to pay for the company’s earnings. The higher the P/E the more the market is willing to pay for the company’s earnings. Some investors read a high P/E as an overpriced stock and that may be the case, however, it can also indicate the market has high hopes for this stock’s future and has bid up the price.

Conversely, a low P/E may indicate a “vote of no confidence” by the market or it could mean this is a sleeper that the market has overlooked. Known as value stocks, many investors made their fortunes spotting these “diamonds in the rough” before the rest of the market discovered their true worth. Here, all the mutual fund has higher PE ration in the year of 2008 and after that, in 2009 and 2010 the PE ratio goes down. That means investors are less willing to pay the mutual funds.

Earnings per certificate

| Year | 1st | 2nd | 3rd | 4th | 5th | 6th | 7th | 8th |

| 2010 | 564.44 | 254.86 | 184.38 | 177.72 | 142.34 | 90.67 | 99.87 | 92.73 |

| 2009 | 385.24 | 135.55 | 121.4 | 114.28 | 78.56 | 50 | 50 | 42.85 |

| 2008 | 331.03 | 107.14 | 92.86 | 85.73 | 64.26 | 42.64 | 42.86 | 35.7 |

| 2007 | 240.82 | 76.15 | 69.11 | 63.1 | 41 | 26.05 | 27.52 | 22.13 |

Earning per certificate means that how much mutual fund is earning from a particular certificate within a year. When the performance of mutual funds is well then it automatically increases the earning per share.

Portfolio investment and management approach of ICB AMCL

Formation of portfolio

ICB AMCL forms portfolio by

- Own 13 mutual funds

- Unit fund

- Equity participation shares

- Investors account and

- Government holdings.

Guidelines on investment:

- No mutual shall invest more than 5% of its capital in any one company’s shares

- Investments by way of previously placed debentures, securitized debts, and other unquote debt instruments shall not respectively exceed ten percent of the total assets of the scheme in case of growth schemes and forty percent of the total assets of the relevant scheme in case of income schemes.

- No individual scheme of the mutual fund should invest more than five percent of any company’s shares.

- No mutual fund under all its scheme should own more than five percent of any company’s paid up capital carrying voting rights

- No mutual fund under all its schemes taken together should investment more than ten percent of the funds in the share, debentures or other securities of a single company.

- No mutual fund under its entire scheme taken together should invest more than fifteen percent of its funds in the shares and debentures of any one industry, provided that provision shall not apply to a scheme which has been floated for investments in one or more specified industries and declaration to that effect has been made in the offer letter.

Portfolio investment

The purchase of stocks, bonds and money market instruments by foreigners for the purpose of realizing a financial return, which does not result in foreign management, ownership, or legal control, is called the portfolio investment

Some examples of portfolio investment are:

- Purchase of shares in a foreign company.

- Purchase of bonds issued by a foreign government.

- Acquisition of assets in a foreign country.

- Purchase of stocks in a foreign company.

Factors affection international portfolio investment:

- Tax rates on interest or dividends (investors will normally prefer countries where the tax rates are relatively low)

- Interest rates (money tends to flow to countries with high-interest rates)

- Exchange rates (foreign investors may be attracted if the local currency is expected to strengthen)

Portfolio investment is part of the capital account on the balance of payments statistics. A portfolio investment is in contrast to a direct investment.

Portfolio Investment Criteria

Before investment investor follow some rules

- Price- Earning Ratio- P/E Ratio

- Dividend Yield

- Closing Market Price

Trend Analysis

An aspect of technical analysis that tries to predict the future movement of a stock based on past data. Trend analysis is based on the idea that what has happened in the past gives traders an idea of what will happen in the future.

There are three main types of trends: short-, intermediate- and long-term.

Trend analysis tries to predict a trend like a bull market run and ride that trend until data suggests a trend reversal (e.g. bull to bear market). Trend analysis is helpful because moving with trends, and not against them, will lead to profit for an investor.

Portfolio management

Portfolio management is used to select a portfolio of new product development projects to achieve the following goals:

- maximize the profitability or value of the portfolio

- provide balance

- support the strategy of the enterprise

Portfolio management is the responsibility of the senior management team of an organization or business unit. This team, which might be called the product committee, meets regularly to manage the product pipeline and make decisions about the product portfolio. Often, this is the same group that conducts the stage-gate reviews in the organization.

A logical starting point is to create a product strategy – markets, customers, products, strategy approach, competitive emphasis etc. the second step is to understand the budget or resources available to balance the portfolio against. Third, each project must be assessed for profitability (rewards), investment requirements (resources), risks, and other appropriate factors.

The weighting of the goals in making decisions about products varies from the company. But organizations must balance these goals: risk vs. profitability, new products vs. improvements, strategy fit vs. reward, market vs. product line, long-term vs. short-term. Several types of techniques have been used to support the portfolio management process:

- Heuristic models

- Scoring techniques

- Visual or mapping techniques

The earliest portfolio management techniques optimized projects’ profitability or financial returns using heuristic or mathematical models. However, this approach paid little attention to balance or aligning the portfolio to the organization’s strategy. Scoring techniques weight and score criteria to take into account investment requirements, profitability risk and strategic alignment.

SWOT Analysis of the Organization

SWOT analysis means the analysis of strength, weakness, opportunity & threats. For ICB, it is given below:

Strength

- The activities of ICB AMCL has invigorated the Mutual Fund industry and has already established itself as one of the fast expanding Asset Management Company in this country

- ICB AMCL gives high dividend payment TK.25.00 than Subsidiary Company ICB AMCL

- The company surpassed all the previous records in its key areas like asset growth, profitability growth and return to asset

- Always creative in activities the company designed two new mutual funds. And already one has launched in this year which is ICB AMCL Second NRB Mutual Fund

Weakness

- There are no branches of ICB AMCL where ICB CML has four branches.

- The manpower is very short and few than other two subsidiaries. It has only 10 offices and 6 nonofficial employees.

- Customer service is not so enough. They don’t give enough time to deal with customers and clients.

Opportunities

- Low level of competition. Because they have competitors or rivals. So it’s a great opportunity to sustain leadership.

- the growth of mutual fund represents institutionalization of a developing country.

Threats

- There are no threats to the country. Because they have a competitors or rival.

FINDINGS, RECOMMENDATION, AND CONCLUSION

FINDINGS

- Among this mutual fund, the portfolios of 1st mutual fund show the best combination of risk and return that is high return and low risk. And it has the lowest Coefficient of Variation. Trey nor Portfolio performance measure of the Thirteen Mutual Funds of ICB AMCL shows that 1st Mutual Fund has the highest ‘T’ value. And last of all comes 13th because it has highest beta value .48.This means this fund largely affected by market forces.

- Sharpe Portfolio performance measure of the 13th Mutual Funds of ICB AMCL shows that the 3rd NRB mutual fund is having the highest ‘S’ value. It has the 2nd position in CV and Trey nor measures result. Worst is 13 mutual funds.

- Sharpe measure is more acceptable than neither they nor measure because it considers all the market and non-market neither risk that Trey nor do not consider. And it is also better than Jensen measure.

- Jensen Portfolio performance measure of the 13th Mutual Funds of ICB shows that the 3rd NRB mutual fund is having the highest ‘J’ value

- So lastly we see all four measures show that 3rd NRB Mutual Fund performs best than all. And 11th Mutual Fund performs worst.

- The most efficient combination of risk-return is return=50% and risk=15%. This is measured by a coefficient of variation.

- To achieve best risk-return combination ICB AMCL Prime Finance Mutual fund should invest 26% of its fund in Eastland Insurance and 74% in Meghna Pet Industries.

- ICB AMCL 3rd Mutual fund lies much below than the minimum variance portfolio risk-return point. ICB AMCL 3rd Mutual fund did not try for achieving this level of efficiency.

- Mutual fund regulations constrain ICB AMCL to go for the efficient frontier. It is almost impossible to achieve that level in reality.

RECOMMENDATIONS

Recommendations of this report have been made on the basis of my working view on ICB AMCL Mutual Fund; Head Office, Dhaka. ICB AMCL is a service-oriented organization. I involved in Mutual Fund activities i.e. Data entry, Finding documents & providing the clients. Service and other related services. I faced some problems providing my service and customers also faced getting service. That is why the authority always should be aware of their service quality and performance as service quality can lead to increased customer satisfaction. Despite these problems, there is something that the ICB AMCL should look at:

- The ICB AMCL should offer more facilities to the customers & Organizations such as providing dividend home delivery & Online Transfer.

- The internal environment of the ICB AMCL should make more attractive. And it should keep neat & clean.

- The ICB AMCL should provide one-stop service to its customers.

- The ICB AMCL should computerize all its function and should provide online Systems facility.

- The employees should always take time to hear the problems of the customers. It will help them to deliver the right service.

- When a customer will go to the ICB AMCL with an unusual problem the employees will have to act positively so that it creates confidence in the heart of the customer that his/her problem will be solved.

- Materials associated with the services should make more attractive.

- The customers should give chance to complain about their dejection. For this, the ICB AMCL should have an active complaint system. From this, the ICB AMCL can also get the customers feedback.

- The ICB AMCL should provide more service products to the customers.

- The ICB AMCL should continue their service at the time of lunch and prayer.

- The authority should recruit more employees to serve the customers. The can recruit experienced employee as well as fresh graduate.

- The ICB AMCL can allow the clients to pay their installments at any branches the customer finds convenient.

- The ICB AMCL should increase the promptness of services.

Though my report is on ICB AMCL Mutual Fund, I tried hard to cover all about the customer and their behavior with the Organization. By ensuring the above recommendations the management of ICB AMCL. Can improve their service quality and create a good image in the customers’ mind.

CONCLUSIONS

ICB is a unique name in our country as an investment bank, but ICB AMCL is a subsidiary of ICB. It is a playing pivotal role to develop the country’s capital Market, ICB as the National Investment house, is the organization to perform the activities by creating demand for securities and on the other hand to ensure the supply of securities in the Capital Market. ICB AMCL investor’s scheme helps to boost up the domestic economy through facilitating to invest in the capital market. At a stage, this made an important effect on the capital market and excellent response from the investor’s. The floatation of mutual funds and issuance of unit certificates by the ICB AMCL strengthens the supply of attractive securities in Bangladesh capital market. Mutual fund management can manage the activities of the mutual fund. Recently ICB has floated Bangladesh Fund to overcome the problem of the stock market in Bangladesh on 10th October 2011.

Mutual fund department should be innovative, explorative and dynamism. ICB AMCL should especially emphasize on the operations and management of mutual fund because most of the small investors are key clients of the mutual fund. So, ICB AMCL should concentrate to increase the performance of its mutual fund and way to find out the path for overcoming the problems of operations. So, lastly, we see all three measures show that 3rd NRB ICB AMCL Mutual Fund performs best than all. And ICB AMCL Employees Mutual Fund performs worst.

We are quite optimistic that recent improvement in transaction procedure, the new fund, computerized system and online service in transaction procedure, support of CDBL, efficient workforce shall reach the ICB AMCL in apex position and efficiently contribute in the rapid development of Bangladesh capital market.