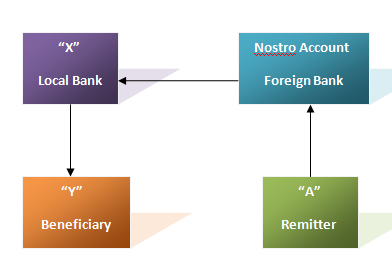

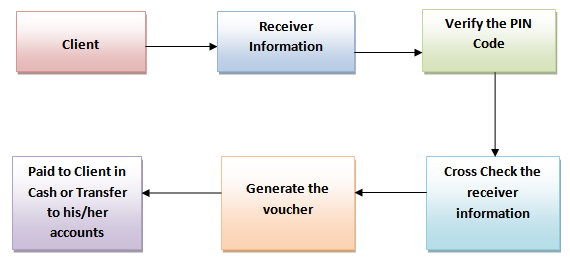

Fund transfer from one country to another country goes through a process which is known as remitting process.

Suppose a local bank has 200 domestic branches and has the corresponding relationship with a foreign bank say-“X”, maintaining “Nostro Account” in US$ with the bank. Bangladeshi expatriates are sending foreign remittance to their local beneficiary, through that account. Now, when the Bangladeshi expatriates through other banks of different countries remit the fund to their “Nostro Account” with “X”, then the local bank’s Head office international division will receive telex message and the remittance section will record the advice and generate the advice letter to the respective branch of the bank. The branch will first decode the test, verify signature and check the account number and name of the beneficiary. After full satisfaction, the branch transfers the amount to the account of the beneficiary and intimates the beneficiary accordingly. But sometimes complexity arises, if the respective local bank has no branch where the beneficiary maintains his account. Then the local bank has to take help of a third bank who has branch there.

Illustration: Flowchart of Remitting Process

Foreign Remittance of CBL:

By your side – all the way:

The City Bank Ltd. is the Authorized Dealer (AD) to deal in foreign exchange business, as an authorized dealer, bank must provide some services to the clients regarding foreign exchange and this department provides the service of remitting foreign currencies from one country to another country. In the process of providing this remittance service it sells and buys foreign currency, the conversation of one currency into another takes place at an agreed rate of exchange , which than Banker quote one for buying and another for selling.

The City Bank’s Foreign Remittance unit meets growing customer needs for fast, secure & easy money transfers to an extensive range of destinations. Being a committed bank to its customers, they go all the lengths to remit customer’s hard earned money safely to their loved ones. With us, apart from a range of high-class modem remittance solutions, customer’s will get peace of mind which they believe counts to most.

Facility:

City Bank Limited has 83 online branches across the country; besides, the Bank has a strong remittance network with other major banks of the country. Therefore, wherever your account is, we are able to send your money instantly.

If you are a City Bank account holder, then please visit any of our branches. Our Foreign remittance service personnel will be there to help you out. If you are not an account holder, then please open an account of your choice with us to receive your remittance at earliest convenience.

CBL understands the value of your precious time. That’s why have made the payment procedure simple & easy. You have the privilege of enchasing the remitted money instantly from your branch counter without going through any hassle. That is to say, if you are an account holder of City Bank, we can instantly credit the money to your account or pay cash to the receiver.

So, place your trust with City Foreign Remittance Service. Send your money to your loved ones & experience peace of mind.

Illustration: Remittance comes through CBL

Foreign Currency Remitting Procedures:

There are two types of remittance:

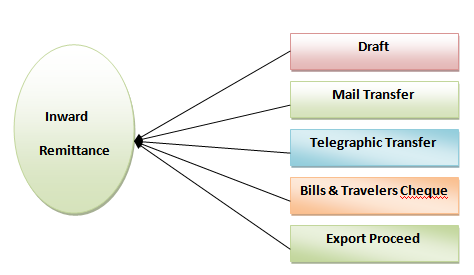

Inward Remittance:

Inward remittance covers purchase of foreign currency in the form of foreign Telegraphic Transfer (T.T), Demand Draft (DD) and Bills & Travelers Cheque, Export Bill etc. sent from abroad favoring a beneficiary in Bangladesh, purchase of foreign exchange is to be reported to Exchange Control Department of Bangladesh Bank on from – letter of Credit (L/C). Basically, these are the formal channels of receiving inward remittance. A local bank also receives indenting commission of local firm also comes under purview of inward remittance.

Illustration : Model of Inward Remittance

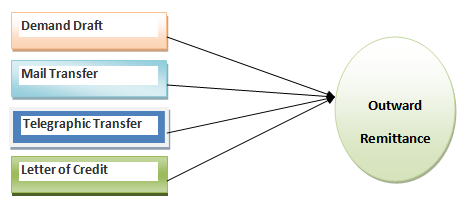

Outward Remittance:

Outward remittance covers sales of foreign Currency by Authorized Dealer (AD) or Formal Channel through issuing foreign Telegraphic Transfer (T.T), Demand Drafts (D.D), Traveler’s Cheque etc. as well as sell of foreign exchange under L/C and against Import Bills retired. The Authorized Dealers have to demonstrate utmost caution to ensure that foreign currencies remitted or released by them are used only for the purposes for which they are released. Most outward remittance is approved by the authorized dealer on behalf of Bangladesh Bank.

Illustration : Model of Outward Remittance

Modes of Foreign Remittance:

CBL Remittance facilities to its customer is to enable them to avoid risk rising out of profit or loss in cash carrying cash money to one place to another or making payment to someone in another places. Banks take this risk remit the fund on behalf of the customers to save them from any awkward happening through the network of their branches and ensure payment to the beneficiary in exchange of a little bit benefit known as commission. There are modes of remitting money from one place to another.

Pay Order Issue (PO):

Following procedure is maintained for the issuance of pay order (PO):

Customer is given a PO form.

After filling the form carefully, the customer is pays the money in casher cheque.

The concerned teller then issue PO on its specific block. This block has three parts, one for bank and another two for customer. “A/C payee” crossing its sealed on all PO issued by the bank. The teller then writes down the name and address of the beneficiary on the main part of the PO block. In other two part name and address of the customer is written.

The teller gives an entry to the registry book and maintains the same number of PO block.

Two authorized officer signed the PO block.

At the end customer is provided with the two parts of the PO block after signing of the backs of bank’s part.

Demand Draft Issue (DD):

Customer is supplied with DD form.

Customer fill up the form, which includes the name of the drawer, name of the payee, amount of money to be sent, commission, name of the drawer branch, signature and address of the drawer.

The customer may pay in cash or by cheque from his accounts (if any).

After the money is paid and the form is sealed and signed accordingly it is given to the DD issuing desk.

Upon block have two parts one for bank and another for customer.

Bank part contains issuing date, drawer’s name, payee’s name and some of the money and name of the drawer branch.

After finishing all the required information entry of the DD is given in the DD issuing register and at the same time bank issues a DD confirmation slip is entered into the DD advice issue register and a number is put on the confirmation slip form the same register. Later the bank mails this advice to the drawer branch.

Telegraphic Transfer (TT):

In this process the sender’s bank send a SWIFT message to the receiver’s bank. The SWIFT message received by the head office international division then the head office transfers the message to the respective branches. After getting message by the respective branches, the bank credited the beneficiary’s account. A beneficiary must have an account to receive the money.

Since the SWIFT message can be transfer from bank to bank, no exchange house can participate in this process. Exchange can take the advantage of the process with the help of a correspondent bank.

Some features of (TT) are given below:

Since SWIFT has been used in the transaction process it is very much a secured.

Sending and receiving time is very much minimum.

The process is also hassle free. The remittance directly deposited to the beneficiary’s account.

The process is frequently used.

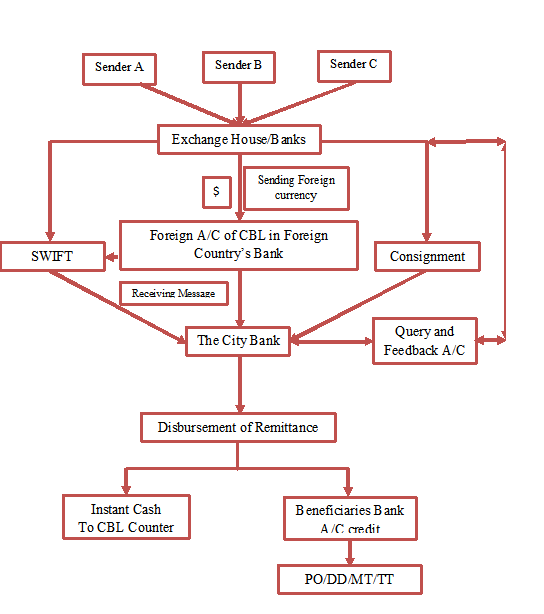

Foreign Remittance Process Diagram:

Illustration : Process of Inward Remittance Transfer

Mail Transfer (MT):

Mail Transfer means instructions of payment issued by one Bank to other bank. In other words, M.T. is an instrument issued by a remitting bank to the paying bank advising in writing to make payment of a certain amount to the specific beneficiary.

Electronic Fund Transfer (EFT):

Electronic fund transfer refers to the computer-based systems used to perform financial transactions electronically.Electronic fund transfer getting more popular in these days due to quickness of its operation.

Some features of EFT:

Electronic fund transfer is a very fast service.

It requires some formalities, as beneficiary does not need to maintain an account with the bank.

The use of EFT is increasing very fast.

Sometimes it may not be secured.

Private FC Account:

(i) Without prior approved of the Bangladesh Bank open foreign currency accounts may be opened with CBL in the names of:

(a) Bangladesh Nationals residing abroad.

(b) Foreign nationals residing abroad or in Bangladesh or in Bangladesh and also foreign firms registered abroad and operating in Bangladesh or aboard.

(c) Foreign missions and their expatriate employees.

Foreign exchange earned through business done or services rendered in Bangladesh cannot be put into these accounts.

(ii) On the above foreign currency accounts maintained with CBL under this authority they can pay interest or such accounts provided the accounts are maintained in the form of term deposits for a minimum period of 90 days. Rates of interest payable on such accounts should normally be comparable with the rates available on similar accounts maintained abroad.

Bangladesh nationals working and earning abroad intending self-employed Bangladeshi migrants proceeding abroad on employment may open foreign currency accounts even without initial deposits. They may open foreign currency accounts with CBL even without initial deposits. They may operate the accounts themselves or nominate other persons in Bangladesh for this purpose. The account can be opened either in Pound Starling US Dollar, Deutsche Mark or Japanese Yen or the option of the prospective account holder and maintained as long as the account holder desires.

Foreign currency accounts in the names of the Diplomatic Bonded Warehouse (duty free shops) licensed by the Custom Authorities may be opened by us without prior approval of the Bangladesh Bank or following conditions:

(a) Convertible foreign currency (traveler’s Cheques, Drafts, Cheques or credit card settlements) received only on account of sale of merchandise may be credited to these accounts.

(b) Foreign exchange may be remitted abroad only for the purpose of import of merchandise by bonded warehouses

(c) Monthly statement of purchase, sale and foreign exchange transaction related thereto along with Bank certificate concerning encashment in Taka shall be submitted to the Bangladesh Bank in prescribed form

Foreign currency accounts in the name of local and joint venture contracting firms employed to execute projects by foreign donor/international donor agencies may also be opened by us as per terms of the approved contract without prior permission of the Bangladesh Bank. Only foreign exchange received from the donors/donor agencies to meet expenses in foreign of the project can be credited to these accounts. All expenses in foreign exchange as per relevant contract may be met from these accounts. These accounts should be closed as soon as the transactions relating to the project are concluded.

Foreign nationals residing in Bangladesh are allowed to maintain and operate their foreign currency accounts abroad.

Foreign currency accounts may be opened in the names of resident Bangladesh nationals working with the foreign/international organizations operating in Bangladesh provided salary is paid in foreign currency.

Resident Forcing Currency Deposit (RFCD):

Persons ordinarily resident in Bangladesh may open and maintain with CBL Resident Forcing Currency Deposit (RFCD) accounts with forcing exchange brought in at the time of their return from travel abroad. Any amount brought in with declaration to Custom authorities in up to us $ 5000 brought in without any declaration, can be credited to such accounts. However, proceeds of export of goods or services in Bangladesh or commission arising from business deals in Bangladesh shall not be credited to such accounts.

Balances in these accounts shall be freely transferable abroad. Fund from these accounts may also be issued to account holders for the purpose of their foreign travels in the usual manner (i.e. with endorsement in Passport and Ticket up to USD 300/- in the form of Cash currency notes and the remained in the form of TC). These accounts may be opener in us Dollar, Pound, Staling, DM or Japanese Yen and may be maintained as long as the account holder’s desire.

Interest in foreign exchange shall be payable on balances in such accounts. if the deposits are for a term of not less than one month and the balance is not less than USD 1000/- or $ 500/- or its equivalent. The rate of interest shall be 0.25 present less than the rate at which interest is paid on balance of back in their foreign currency clearing accounts maintained with the Bangladesh.

Wage Earner Bonds:

Non-resident Bangladesh nationals can remit their surplus earnings in foreign currency to their home country for investment in the 5 years term Wage Earners Development Bond in BD Taka. Such Bonds can be purchased in denomination of Tk.1, 000/=, Tk. 5,000/=,

Tk10, 000/=, Tk.25, 000/=, Tk.50, 000/=, and Tk.1, 00,000/=. These Bonds are renewable and attractive rate of interest is allowed on this investment in BD Taka, present rate of interest is 12% p.a. and rate of interest to be utilized in Bangladesh. For premature encashment of the Bonds reduced rate of interest is applied. Death risk insurance benefit is allowed on the Bonds of value Tk.25.000/= and above.

Principal amount of the investment under this scheme can be frilly repatriated in FC in foreign country. Interest earned on the Wage Earners Development Bond is Tax Free in Bangladesh. Remittance may be sent from abroad by way of TT/MT/DD which has already been explained above. A remitter abroad simply has to approach a bank branch there with certain amount to be deposited beneficiary in Bangladesh either in foreign currency or in equivalent Taka currency. The Branch so approached abroad usually should have agency arrangement with the paying banks in Bangladesh. However, in the absence of any such agency arrangement, remittance may also be made by transferring cover value of the remittance to the paying bank’s account abroad by the remitting bank.

Payment of Traveler’s cheques:

Traveler’s cheques may be paid at the counter of bank on presentation on obtaining signature on the T.C. after verifying the signature of the holder with the signature already on the T.C. The payment will be effected in local currency at the prevailing conversion rate fixed by the rate committee. The T.C. may also be deposited in foreign currency account T.C.’s are being issued by some reputed banks & Co.’s of the world such as:-

The American Express Bank.

The City Bank

The National West Minister Bank

The Barclays’ Bank

The Bank of Oman

The Saudi Travelers Cheque Co.

T.C. is bought & sold by banks with which arrangements have been made by the issuing banks. T.C.’s are being paid at the T.T. clean buying rate. The traveler’s cheques bought by the bank have to be sent to their foreign correspondents with the instruction to credit the proceeds on collection to their NOSTRO account with them.

Payment of Foreign Currency Notes:

Authorized branches of the bank are to make payment of F.C. notes in equivalent Taka currency at the prevailing rate (T.T. clean buying rate). Generally, two foreign currencies namely U.S. Dollar & Britain Pound Sterling is being bought and sold along with two other currencies like K.S.A. Riyal & Kuwaiti Diner.

These above currency notes are normally disposed of in the following ways:-

By selling them to travelers abroad. In this case, endorsement has to be made in the passport of the Travelers.

By sending them to foreign correspondent/agent for depositing to Bank’s NOSTRO account. But in this particular case, approval of Bangladesh Bank is required & customs clearance has to be obtained.

By selling them to another Authorized Dealers. (FET Schedule is not required while transacting in each foreign currency).

Authorized dealer’s power:

Authorized Dealers can issue foreign currency remittance in respect of the following:

Travel quota per year:

SAARC Countries: By Road=USD500/- & BY AIR=USD1000/-

Other than SAARC Countries: USD 3000/-

Minor will get half of the above mentioned amount.

AD can issue USD 200/- for SAARC Countries & USD2 50/- for other Countries per dime allowance to attend seminar, conference and workshop arranged by recognized bodies.

For medical treatment abroad, USD.10, 000/- can be issued as expenses.

Examination fees, foreign education fee & evaluation fee for immigration at actual amount.

A.D. can remit membership fees, annual fees, and registration fees of international Bodies.

A.D. can remit foreign currency required for current expenses of Foreign Offices of Bangladesh Biman, Bangladesh shipping Corp.

A.D. can remit consular fees of foreign Embassies, Pre-shipment Inspection fees & genuine export claims up to 10% of the proceeds realized.

A.D. can remit cost of ships bought in private sector.

Commercial remittance.

Payment of rent of hiring foreign ship/Aircraft by local branch/agent.

Appointment of agent by Bangladeshi firm.

Advertisement in foreign News paper by Bangladeshi Firm etc.

Prior approval of Bangladesh Bank is required on the following:-

Family Remittance facility

Other private remittance.

While applying for Bangladesh bank permission for outward remittances along with others, the following prescribed forms are used.

IMP form (Remittance for Import)

T/M Form (Traveling & Miscellaneous).

Cancellation of M.T. / D.D.:-

The above instruments may be cancelled & payment may be made to the applicant by cancellation after observing all existing formalities. Bangladesh Bank should also be reported about the cancellation of the outward remittance as inward remittance.

Online Remittance:

Online Remittance is the process of sending money or transferring using the Internet, and is usually done by an expert back to his/her home country. According to the World Bank, remittances are an important source of income for the receiving country, usually developing and emerging market countries.

Money Gram:

It is mentionable that The City Bank Ltd. is one of the Bangladeshi Bank, which has a membership of Money Gram network. CBL is a member of Money Gram and SWIFT networks. Using the services of these global network, nonresident Bangladesh nationals can send money from abroad to their home country within a few minutes without any risk, Besides Money Gram, they have also arrangement with foreign money exchange companies like U.S.E. Exchange Co. Redha-al-Ansari Co. etc. through which Bangladeshi expatriates can remit these money to their relatives in home country very easily and safely using SWIFT network. Money Gram and SWIFT mechanism ensure 100% secured and quickest possible mode of money transfers from abroad tour country and Bangladeshi money receivers are enjoying these facilities through us. CBL is rendering exceptional services to its clients by arranging such private remittance of money from foreign countries to Bangladesh.

The City Bank Limited is very happy to announce to have joined hands with Money Gram Payment Systems to serve expatriates to send money back home quickly from anywhere in the world. Moreover, money can also be sent quickly through Money Gram from Bangladesh to other parts of the world as is done through the banking channel. At the moment we are concentrating on home remittances being sent by the expatriates.

Money Gram Payment system is a non-back provider of electronic money transfer service. Money Gram is providing its customers a service of an unsurpassed quality and superior value. Money Gram has over 80,000 Agent locations throughout the world. Persons anywhere require transferring cash quickly, reliably, conveniently and at attractive prices to more than 180 countries can depend Money Gram agents for the service.

CBL continuous commitment to serve the country’s economy in a better way we have made agreement with Money Gram Payment Services Company to facilitate transfer flow money from abroad. The best benefit of the service can be derived by our expatriates who are living in many countries of the world.

The major problem being faced by CBL expatriated in many countries in not having bank accounts. Many banks do not entertain customers for remitting money without having accounts. Moreover many of our expatriates cannot get acquainted with banking formalities immediately on reaching abroad. It is not necessary to have a bank account to use Money Gram Service. Our expatriates can visit any Money Gram agent when they want to send money, which gives very easy and convenient transfer.

Money Gram is represented in over 180 countries and is available at more than 80,000 locations worldwide. In the USA alone Money Gram is available at more than 15,000 locations. Besides in the UK Money Gram is available through 1700 Postal Branches and 500 Thomas Cook travel shops making it the UK’s largest money transfer network.

Sender completes a “Send” form and gets a Receipt. Money Gram Agent gives a Ref. No. which has to be passed to the Receiver. Recipient goes to CBL Branch in Bangladesh. Fills out a “Receive” form and show proper identification. CBL Bank makers and inquiry on the Money Gram computer network to obtain authorization to pay Recipient and Recipient receives the fund.

Money Gram is one of the fastest ways to transfer money. Customers using Money Gram can send or receive money usually within 10 minutes from anywhere in the world. At The City Bank provide the Recipients immediate attention and made it a point to pay the Recipient within minutes. The Recipients need not require having a bank account. The City bank does not levy any extra charge. We give a better exchange rate to the Recipient. The Recipient can approach any for the CBL branches at his convenience for payment.

For foreign dealings, any of these 10 ID’s is necessary:

Passport (not expired).

Driving License.

Ration Card.

Voter ID.

Pan Card.

Refugee Card.

Student ID (Nationalized University and College).

Bank Passport (CBL).

Army Card.

Post office loyalty card, Govt. employee ID card, local (W/C) ID Card.

All ID are valid only if they have a photograph and the ID verifies the person’s signature.

Reporting To Bangladesh Bank:

At the end each month, transactions on outward remittance have to be reported to Bangladesh Bank similar to foreign inward remittance through the statements S-1, S-2, S-4 & S-6 along with schedules. Finally, one has to remember that foreign inward remittance has no restriction to our in while foreign outward remittance should have to be made in accordance with the Bangladesh Bank’s Guidelines for foreign exchange transactions & latest circulars of Bangladesh Bank. Last but not the last, we must keep in mind that all types of transaction involving foreign remittance.