Capital Market Analysis in Bangladesh

A capital market is a market for securities (debt or equity), where business enterprises (companies) and governments can raise long-term funds. It is defined as a market in which money is provided for periods longer than a year, as the raising of short-term funds takes place on other markets (e.g., the money market). The capital market includes the stock market (equity securities) and the bond market (debt). Financial regulators, such as the UK’s Financial Services Authority (FSA) or the U.S. Securities and Exchange Commission (SEC), oversee the capital markets in their designated jurisdictions to ensure that investors are protected against fraud, among other duties.

Capital markets may be classified as primary markets and secondary markets. In primary markets, new stock or bond issues are sold to investors via a mechanism known as underwriting. In the secondary markets, existing securities are sold and bought among investors or traders, usually on a securities exchange, over-the-counter, or elsewhere.

Macro-financial developments:

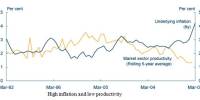

Overall, GDP growth in FY09 is likely to be around 6.0 percent and if no drastic shock affects the economy and business confidence and investment climate improve further, the economy could grow faster. The 12-month average inflation rose to 10.06 percent in September 2008 which fell afterwards reaching 8.46 percent in January 2009. If the current trends are maintained, it is likely that the average inflation would fall to around 7.8 percent in FY09. During the first half of FY09, total revenue and total expenditure as shares of GDP stood at 5.9 percent and 8.1 percent respectively. Overall fiscal deficit as share of GDP reached 2.2 percent at the end of the first half of FY09 as against the yearly target of 4.99 percent. Public sector credit grew at 9.6 percent during H1 FY09 while the growth rate of private sector credit was 10.8 percent. Bangladesh’s financial sector has shown remarkable resilience to the upholding global financial turmoil and slowing growth in high income countries, largely due to the country’s insulation from international capital markets and the negligible role of foreign portfolio investors. This resilience also derives partly from strengthened policy frameworks and macroeconomic fundamentals.

World growth outlook and economic environment:

World growth is projected to fall to 0.5 percent in 2009, its lowest rate since World War II. This substantially decelerated growth is attributed to recent financial turmoil initially affecting the developed countries but gradually hurting all other major sources of global growth. The growth projections foresee an average annual real GDP growth of 3.3 percent in 2009 compared with 6.3 percent in 2008 and in developing and emerging economies, five percentage points lower than in 2007. The expectation is that world output growth would gain buoyancy by late 2009. International commodity prices have started to ease and reached comfortable levels in the backdrop of sharp fall in aggregate demand in the developed economies. Global commodity prices are projected to fall further in 2009. In the backdrop of lax demand, global inflation is projected to moderate further in 2009.

Interest rate structure:

Commercial lending rate started to decline in nominal as well as in real terms since May 2003 and continued up to the end of January 2006. Simultaneously, commercial deposit rates also declined in both nominal and real terms. The real lending and deposit rates started to increase since January 2006. The large spread between lending and deposit rates of scheduled banks, however, still remains a matter of concern. It is also evident that various short-term rates (e.g., repo, reverse repo) have allowed BB to exert a greater control over the country’s overnight money market. Moreover, as the inflationary and exchange rate pressures are persisting, BB’s involvement in the overnight money market will remain crucial.

Balance of payments and foreign exchange market:

The overall balance of payments situation remained reasonably stable during July-November FY09; export earnings increased by 27.4 percent, workers’ remittances by 33.6 percent, and import payments by 28.2 percent. During July-December FY09, import of consumer goods as measured by settlement of import LCs declined by 23.5 percent in which food grains import declined by 35.8 percent while the import of other consumer goods declined by 10.8 percent. Over the period between January 2008 and January 2009, the foreign exchange market remained relatively stable except for minor uptrend in Taka/USD during some months. The gross foreign exchange reserves reached USD 5,787.8 million at the end of December 2008 higher than USD 5,514.6 million recorded in December 2007

Supply of and Demand for Financial Products

Payment and transaction products:

Bangladesh Bank has taken several initiatives such as formation of the National Payment System Council (NPSC) and establishment of the Bangladesh Automated Cheque Processing System (BACPS) and Bangladesh Electronic Fund Transfer Network (BEFTN), along with creating necessary legal and regulatory frameworks to enhance the efficiency of the payment and transaction system. Moreover, increasing adoption of modern and technology driven payment system will cater to meeting the payment requirements of the increasingly complex financial transactions of the Bangladesh economy.

Savings products:

The banks currently offer 14 different types of savings products for their clients

Interest rates on fixed deposits for 2-3 years were increased by all types of banks in different magnitudes during the quarter under review. The share of urban deposits increased from around 80 percent at the end of December 2001 to nearly 87 percent at the end of March 2007. The deposit-GDP ratio was 29.6 percent in 1990, which grew to 44 percent at the end of December 2006 and declined to 39.5 percent at the end of March 2007.

Loan products:

The rise in credit disbursement of scheduled banks is mainly driven by growth in advances. During the period under review, quarterly growth rate of advances for agricultural purposes depicted a declining trend. However, working capital financing followed a fluctuating trend. Advances (in real terms) disbursed for other economic purposes also followed a stable pattern with growing importance of working capital for the industrial sector.

Specialized loan products—term lending:

In view of the relatively low but rising share of the industrial sector in GDP, ensuring adequate flow of term lending is important for Bangladesh. Total disbursement of industrial term lending in FY08 was dominated by PCBs and stood at Tk. 201.5 billion as against Tk. 123.8 billion in FY07 showing a robust growth of 62.8 percent. Infrastructure financing, on the other hand, covers a wide range of activities including financing of different industrial establishments, construction, and transport and communication related activities. Total outstanding credit to the above broad spectrum of infrastructure activities increased significantly during the last three years indicating rising demand for investment in such activities.

Access to finance by small and medium enterprises:

In the FY09 budget, the SME sector has been treated as a thrust sector with focus on deepening the activities of this sector along with ensuring their sustainability. BB has arranged refinancing facilities for banks and NBFIs. Since the beginning of the refinancing schemes, Tk.10.19 billion were refinanced to 18 banks and 21 NBFIs till the end of December 2008. For boosting the development of the SME sector, new generation of financial institutions are needed along with financing mechanisms to provide access to appropriate finance and meet up the diversified needs of financial services of this potential sector.

Micro Credit Operations:

Micro credit operations of large microfinance institutions (MFIs) show an overall satisfactory trend in terms of disbursement and recovery of loans. During the first half of FY09, total loan disbursement increased by 34.4 percent over the same period of FY08, much higher than the growth during the comparable period of FY08 and the average growth over the last few years.

The Banking Sector

Interest rate spread:

The interest rate spread showed declining trend since June 2001 except for few deviations in some periods. The spread between lending and deposits rate declined by 1.6 percentage points while deposit rates increased by 0.1 percentage points and lending rates decreased by 1.4 percentage points respectively between June 2001 to September 2008.

Earnings and profitability:

A comparison of total interest income and total assets by bank groups shows that PCBs have highest interest income-asset ratio followed by FCBs. Total interest income and total assets of SBs and SCBs fluctuated between periods. A straightforward measure of bank profitability is the net after-tax profit per unit of assets, or return on assets (ROA). This measure shows that ROA for FCBs is much higher than those of PCBs, SCBs, and SBs during all periods. During December 2008, the return on equity (ROE) for SCBs was highest followed by FCBs and PCBs, while it was negative for SBs.

Non-performing loans:

Bangladesh’s banking sector historically accumulated huge amount of nonperforming loans (NPLs). Trend analysis shows that the higher the total asset, the lower the NPL to total loan of a bank implying that an increase in bank’s total asset tend to lower non performing loans. The BB’s recent directives to the banks to take precaution while extending loans to high risk sectors and prioritize loans to productive sectors in conjunction with the government’s enactment of laws prohibiting loan defaulters to take part in elections at local and national levels and similar other measures would help to further improve the NPL situation in the country.

Default risks: loan-loss provisions:

The data on surplus/shortfall of actual provision by broad category of banks show that actual provision fell short of required provision for all but FCBs during December 2007- March 2008 indicating lack of efficiency in fund management especially in disbursing and recovering loans, sustained pressure of NPLs in all commercial banks (except FCBs). After March 2008, actual provisioning scenario for SCBs has reversed. The actual provision remained higher than required provision for SCBs during June-December 2008 mainly because of intensified recovery drive and rescheduling of overdue loans under the new management of the state-owned banks.

Capital adequacy:

The overall capital situation of the banks improved in December 2008. The year-end capital position in 2008 witnessed an increase of 66.8 percent as compared with 62.0 percent in the preceding year. Out of total capital for all banks, 73.4 percent was maintained as core capital in December 2008 which was 71.8 percent in December 2007. As a group, the PCBs registered a rapid growth in capital position in 2008. During end 2008, capital share of PCBs in total capital of all banks stood at 68.7 percent compared with 82.4 percent in end 2007. Nonetheless, most of the capital increase is attributed to increase in Tier I capital.

The Capital Market and Non-bank Financial Sector

The capital market:

The country’s capital market showed a mixed performance in 2008. Stock prices showed significant upturn during the first half while the second half witnessed downward movement. Different monthly average price indexes at Dhaka Stock Exchange (DSE) lost grounds although the daily average turnover improved showing some fluctuations in 2008. During the year, 15 companies were listed in DSE of which five were listed through the direct listing route.

Mutual funds:

In Bangladesh, there are only 19 mutual funds. Among these, two are open-ended of which one is managed by ICB and the other by ICB Asset Management Co. Ltd. Of these, 17 are listed in the Dhaka Stock Exchange (DSE). During 2008 two mutual funds (ICB AMCL 2nd NRB MF Grameen One: Scheme Two) listed in the DSE with issued capital of Tk. 1.2 billion.

Bond market developments:

The size of government debt instruments displayed a mixed trend during June 2006-December 2008 with the NSD certificates capturing the lion’s share. Total outstanding size of various t-bills stood at Tk. 116.2 billion at the end of December 2008 from Tk. 101.5 billion during end June 2008. Given the nature and duration of maturities, interest rates are relatively high for long-term bills/bonds indicating upward sloping nature of the yield curve in Bangladesh. Having the same level of risk, yields of treasury bills and bonds at different maturities are relatively low compared with yields of other instruments especially savings certificates.

Non-bank financial institutions:

The non-bank financial institutions (NBFIs) constitute a rapidly growing segment of the financial system in Bangladesh. Total assets of this sector showed a growth of 28.2 percent and stood at Tk.90.2 billion in June 2008 compared with Tk.70.4 billion in June 2007. A composition of asset and liability components of the NBFIs as a whole shows the overall consistent nature.

Macro-financial developments:

Overall, GDP growth in FY09 is likely to be around 6.0 percent and if no drastic shock affects the economy and business confidence and investment climate improve further, the economy could grow faster. The 12-month average inflation rose to 10.06 percent in September 2008 which fell afterwards reaching 8.46 percent in January 2009. If the current trends are maintained, it is likely that the average inflation would fall to around 7.8 percent in FY09. During the first half of FY09, total revenue and total expenditure as shares of GDP stood at 5.9 percent and 8.1 percent respectively. Overall fiscal deficit as share of GDP reached 2.2 percent at the end of the first half of FY09 as against the yearly target of 4.99 percent. Public sector credit grew at 9.6 percent during H1 FY09 while the growth rate of private sector credit was 10.8 percent. Bangladesh’s financial sector has shown remarkable resilience to the upholding global financial turmoil and slowing growth in high income countries, largely due to the country’s insulation from international capital markets and the negligible role of foreign portfolio investors. This resilience also derives partly from strengthened policy frameworks and macroeconomic fundamentals.

World growth outlook and economic environment:

World growth is projected to fall to 0.5 percent in 2009, its lowest rate since World War II. This substantially decelerated growth is attributed to recent financial turmoil initially affecting the developed countries but gradually hurting all other major sources of global growth. The growth projections foresee an average annual real GDP growth of 3.3 percent in 2009 compared with 6.3 percent in 2008 and in developing and emerging economies, five percentage points lower than in 2007. The expectation is that world output growth would gain buoyancy by late 2009. International commodity prices have started to ease and reached comfortable levels in the backdrop of sharp fall in aggregate demand in the developed economies. Global commodity prices are projected to fall further in 2009. In the backdrop of lax demand, global inflation is projected to moderate further in 2009.

Interest rate structure:

Commercial lending rate started to decline in nominal as well as in real terms since May 2003 and continued up to the end of January 2006. Simultaneously, commercial deposit rates also declined in both nominal and real terms. The real lending and deposit rates started to increase since January 2006. The large spread between lending and deposit rates of scheduled banks, however, still remains a matter of concern. It is also evident that various short-term rates (e.g., repo, reverse repo) have allowed BB to exert a greater control over the country’s overnight money market. Moreover, as the inflationary and exchange rate pressures are persisting, BB’s involvement in the overnight money market will remain crucial.

Balance of payments and foreign exchange market:

The overall balance of payments situation remained reasonably stable during July-November FY09; export earnings increased by 27.4 percent, workers’ remittances by 33.6 percent, and import payments by 28.2 percent. During July-December FY09, import of consumer goods as measured by settlement of import LCs declined by 23.5 percent in which food grains import declined by 35.8 percent while the import of other consumer goods declined by 10.8 percent. Over the period between January 2008 and January 2009, the foreign exchange market remained relatively stable except for minor uptrend in Taka/USD during some months. The gross foreign exchange reserves reached USD 5,787.8 million at the end of December 2008 higher than USD 5,514.6 million recorded in December 2007

Supply of and Demand for Financial Products

Payment and transaction products:

Bangladesh Bank has taken several initiatives such as formation of the National Payment System Council (NPSC) and establishment of the Bangladesh Automated Cheque Processing System (BACPS) and Bangladesh Electronic Fund Transfer Network (BEFTN), along with creating necessary legal and regulatory frameworks to enhance the efficiency of the payment and transaction system. Moreover, increasing adoption of modern and technology driven payment system will cater to meeting the payment requirements of the increasingly complex financial transactions of the Bangladesh economy.

Savings products:

The banks currently offer 14 different types of savings products for their clients.

Interest rates on fixed deposits for 2-3 years were increased by all types of banks in different magnitudes during the quarter under review. The share of urban deposits increased from around 80 percent at the end of December 2001 to nearly 87 percent at the end of March 2007. The deposit-GDP ratio was 29.6 percent in 1990, which grew to 44 percent at the end of December 2006 and declined to 39.5 percent at the end of March 2007.

Loan products:

The rise in credit disbursement of scheduled banks is mainly driven by growth in advances. During the period under review, quarterly growth rate of advances for agricultural purposes depicted a declining trend. However, working capital financing followed a fluctuating trend. Advances (in real terms) disbursed for other economic purposes also followed a stable pattern with growing importance of working capital for the industrial sector.

Specialized loan products—term lending:

In view of the relatively low but rising share of the industrial sector in GDP, ensuring adequate flow of term lending is important for Bangladesh. Total disbursement of industrial term lending in FY08 was dominated by PCBs and stood at Tk. 201.5 billion as against Tk. 123.8 billion in FY07 showing a robust growth of 62.8 percent. Infrastructure financing, on the other hand, covers a wide range of activities including financing of different industrial establishments, construction, and transport and communication related activities. Total outstanding credit to the above broad spectrum of infrastructure activities increased significantly during the last three years indicating rising demand for investment in such activities.

Access to finance by small and medium enterprises:

In the FY09 budget, the SME sector has been treated as a thrust sector with focus on deepening the activities of this sector along with ensuring their sustainability. BB has arranged refinancing facilities for banks and NBFIs. Since the beginning of the refinancing schemes, Tk.10.19 billion were refinanced to 18 banks and 21 NBFIs till the end of December 2008. For boosting the development of the SME sector, new generation of financial institutions are needed along with financing mechanisms to provide access to appropriate finance and meet up the diversified needs of financial services of this potential sector.

Micro Credit Operations:

Micro credit operations of large microfinance institutions (MFIs) show an overall satisfactory trend in terms of disbursement and recovery of loans. During the first half of FY09, total loan disbursement increased by 34.4 percent over the same period of FY08, much higher than the growth during the comparable period of FY08 and the average growth over the last few years.

The Banking Sector

Interest rate spread:

The interest rate spread showed declining trend since June 2001 except for few deviations in some periods. The spread between lending and deposits rate declined by 1.6 percentage points while deposit rates increased by 0.1 percentage points and lending rates decreased by 1.4 percentage points respectively between June 2001 to September 2008.

Earnings and profitability:

A comparison of total interest income and total assets by bank groups shows that PCBs have highest interest income-asset ratio followed by FCBs. Total interest income and total assets of SBs and SCBs fluctuated between periods. A straightforward measure of bank profitability is the net after-tax profit per unit of assets, or return on assets (ROA). This measure shows that ROA for FCBs is much higher than those of PCBs, SCBs, and SBs during all periods. During December 2008, the return on equity (ROE) for SCBs was highest followed by FCBs and PCBs, while it was negative for SBs.

Non-performing loans:

Bangladesh’s banking sector historically accumulated huge amount of nonperforming loans (NPLs). Trend analysis shows that the higher the total asset, the lower the NPL to total loan of a bank implying that an increase in bank’s total asset tend to lower non performing loans. The BB’s recent directives to the banks to take precaution while extending loans to high risk sectors and prioritize loans to productive sectors in conjunction with the government’s enactment of laws prohibiting loan defaulters to take part in elections at local and national levels and similar other measures would help to further improve the NPL situation in the country.

Default risks: loan-loss provisions:

The data on surplus/shortfall of actual provision by broad category of banks show that actual provision fell short of required provision for all but FCBs during December 2007- March 2008 indicating lack of efficiency in fund management especially in disbursing and recovering loans, sustained pressure of NPLs in all commercial banks (except FCBs). After March 2008, actual provisioning scenario for SCBs has reversed. The actual provision remained higher than required provision for SCBs during June-December 2008 mainly because of intensified recovery drive and rescheduling of overdue loans under the new management of the state-owned banks.

Capital adequacy:

The overall capital situation of the banks improved in December 2008. The year-end capital position in 2008 witnessed an increase of 66.8 percent as compared with 62.0 percent in the preceding year. Out of total capital for all banks, 73.4 percent was maintained as core capital in December 2008 which was 71.8 percent in December 2007. As a group, the PCBs registered a rapid growth in capital position in 2008. During end 2008, capital share of PCBs in total capital of all banks stood at 68.7 percent compared with 82.4 percent in end 2007. Nonetheless, most of the capital increase is attributed to increase in Tier I capital.

The Capital Market and Non-bank Financial Sector

The capital market:

The country’s capital market showed a mixed performance in 2008. Stock prices showed significant upturn during the first half while the second half witnessed downward movement. Different monthly average price indexes at Dhaka Stock Exchange (DSE) lost grounds although the daily average turnover improved showing some fluctuations in 2008. During the year, 15 companies were listed in DSE of which five were listed through the direct listing route.

Mutual funds:

In Bangladesh, there are only 19 mutual funds. Among these, two are open-ended of which one is managed by ICB and the other by ICB Asset Management Co. Ltd. Of these, 17 are listed in the Dhaka Stock Exchange (DSE). During 2008 two mutual funds (ICB AMCL 2nd NRB MF Grameen One: Scheme Two) listed in the DSE with issued capital of Tk. 1.2 billion.

Bond market developments: The size of government debt instruments displayed a mixed trend during June 2006-December 2008 with the NSD certificates capturing the lion’s share. Total outstanding size of various t-bills stood at Tk. 116.2 billion at the end of December 2008 from Tk. 101.5 billion during end June 2008. Given the nature and duration of maturities, interest rates are relatively high for long-term bills/bonds indicating upward sloping nature of the yield curve in Bangladesh. Having the same level of risk, yields of treasury bills and bonds at different maturities are relatively low compared with yields of other instruments especially savings tes. Certificate

Non-bank financial institutions: The non-bank financial institutions (NBFIs) constitute a rapidly growing segment of the financial system in Bangladesh. Total assets of this sector showed a growth of 28.2 percent and stood at Tk.90.2 billion in June 2008 compared with Tk.70.4 billion in June 2007. A composition of asset and liability components of the NBFIs as a whole shows the overall consistent nature

Monetary policy and Capital Markets in Bangladesh

Introduction

The Securities and Exchange Commission exercises powers under the Securities and Exchange Commission Act 1993. It regulates institutions engaged in capital market activities. Bangladesh Bank exercises powers under the Financial Institutions Act 1993 and regulates institutions engaged in financing activities including leasing companies and venture capital markets.

Bangladesh capital market is one of the smallest in Asia but the third largest in the south Asia region. It has two full-fledged automated stock exchanges namely Dhaka Stock Exchange (DSE) and Chittagong Stock Exchange (CSE) and an over-the counter exchange operated by CSE.

It also consists of a dedicated regulator, the Securities and Exchange Commission (SEC), since, it implements rules and regulations, monitors their implications to operate and develop the capital market. It consists of Central Depository Bangladesh Limited (CDBL), the only Central Depository in Bangladesh that provides facilities for the settlement of transactions of dematerialized securities in CSE and DSE.

Capital market analyst Salahuddin Ahmed Khan said, “2009 was really a good year for Bangladesh’s capital market. This year will be a milestone in the history of Bangladesh’s capital market.”Khan, also a former Chief Executive Officer of Bangladesh’s main bourse Dhaka Stock Exchange (DSE), said the number of investors in 2009 increased by 500,000 and stood at nearly 2 million while the number of branches of broker houses throughout the country has reached 387 in the outgoing year from 272 in 2008.

The DSE market capitalization surged to 27.54 billion U.S. dollars. The market capitalization increased to 30.95 percent of GDP in 2009 from 19.26 percent in 2008. The total amount of turnover in 2009 stood at over 1,475 billion taka with 120 percent rise from that in 2008. Bangladesh Bank (BB) adjusted its monetary policy stance during 2005 in order to contain inflationary pressures and facilitate stability in the foreign exchange market. At the end of 2005, interest rates on NSD certificates (government borrowing instruments from the non-bank public) were also adjusted upward. The latter development, however, raised some concern among different economic agents regarding its possible impact on the country’s capital market. One recent study by Ahmed et. al. (2006) for Bangladesh found that contractionary monetary policy shock, measured by increases in short term policy interest rates have small, negative and short lived effect on the stock price index. In this paper we attempt to closely inspect the evolvement of monetary policy and capital market indicators in recent years and their possible interrelationship to shed some light on the issue.We focus our analysis on the period, January ’02 to December ’06. Data on capital market indicators are collected from monthly reviews of Dhaka Stock Exchange (DSE), while interest rates and Treasury bills data are taken from various Bangladesh Bank’s sources.

In a modern monetary system central banks have control over very short term (overnight) or short term (covering several months) interest rates; long term (1-year or more) interest rates, however, are determined by inflation expectations and real activities.1 Relationship between monetary policy and stock prices can be understood within the stock price valuation model. When central bank raises the interest rates on monetary policy instruments, expected return on alternative assets (other than equity) rise, reducing the present discounted value of future cash flow or price of stocks.

The rest of this paper is organized as follows. Section 2 provides a brief discussion on recent changes in monetary policy stance while Section 3 discusses the changes in yields and stock of Government T-bills and NSD certificates. Section 4 provides a review of recent development in the capital market. A parallel analysis is conducted in Section 5 and finally, Section 6 concludes the paper

Recent Development in the Capital Market

The role of capital market in financing private investment remained at a nascent stage in the context of Bangladesh. Banks and financial institutions disbursed BDT 96.5 billion as industrial term loans during FY06, whereas only BDT 1.7 billion was raised in the capital market through private placements and public offerings (BB Annual Report FY06). As of December, 2006 a total of 310 securities were listed at DSE comprising 255 companies, 13 mutual funds, 8 debentures and 34 treasury bonds as opposed to a total of 249 securities comprising 230 companies, 10 mutual funds and 9 debentures as of December 2001. Thus during the last five years only 54 new companies got listed in the DSE of which only three were listed by direct listing route, and the rest were listed by public offering. Total market capitalization of all listed securities in DSE, however, increased substantially (by around 130 percent) in 2004 to BDT 224.9 billion. At the end of December ’06 it stood at BDT 323.4 billion. DSE market capitalization as share of GDP fell to 5.41 in June ’06 from 6.06 in June ’05.

In order to attract companies into the capital market, a few more steps were also taken. For example corporate tax rate for nonlisted companies was fixed at 37.5 percent and for listed companies it remain unchanged at 30percent (and 45 percent on banks, insurance and financial institutions). However, 10% tax rebate was allowed for companies declaring a 20 percent or more in dividend.

ANALYSIS OF THE LITERATURE REVIEW

There has been an increase in the demand for infrastructure services and opening up of the infrastructure sector for private investment. As a result, a large number of financial intermediaries and private sector participants have invested in the financial market to raise long term funds in Bangladesh. It is important, therefore, to set up the required debt market infrastructure that can create a vibrant secondary debt market in Bangladesh. This paper analyzes recent developments in the country’s capital market and suggests measures to ensure a liquid capital market in Bangladesh to support the country’s rapid development needs.