Performance Evaluation of Credit Operation of

Trust Bank Limited

Today necessity of a Bank as a financial institution is undeniable. A country is financially rich when it has modern financial institutions of its own. These institutions play a vital role in the field of financial stability of a country. Banking sector is one of the stable financial institutions of a country. Due to Globalization and Technological changes, the banking business has become very competitive now a day. All banks are competing to give effective real time service to their customers. For giving friendly service to the customers they need experienced and well-educated working force.

The overall approach of the report is a Descriptive one as it goes into the depth of “Performance Evaluation of Credit Operation Systems of Trust Bank Ltd”. Here both primary and secondary information were used. Interview was the basic techniques comply to collect primary data from any people within the organization. Information about the varieties of activities within the Correspondent Banking Department was collected through interviewed. Among the secondary sources to collect data regarding the company’s performance over the Annual reports of Trust Bank Ltd. Different circulars and papers of Trust Bank Ltd, General Banking Operation manual, Banking Lecture sheet within the organization helped me to gather data about the organization.

The principal reason banks are chartered by the government and the central bank is to make loans to their customers. Banks are expected to support their communities with an adequate supply of credit for all legitimate business and consumes financial needs and to price that credit reasonably in the line with competitively determined interest rates. Indeed, making loans is the principal economic function of banks to fund consumption and investment spending by businesses, individuals and units of government. How well a bank performs its lending function has a great deal to do with the economic health of fits region, because bank loans support the growth of new businesses and jobs within the banks trade territory and promote economic vitality, Moreover, bank loans often seem to convey positive information to the marketplace about a borrower’s credit quality, enabling a borrower to obtain more and perhaps somewhat cheaper funds from other sources. The report contains seven chapters. The first chapter of the report describes the introductory words of the internship report in which Introduction of Topic, Origin of the report, Objective of the Report, Scope of the Report, Methodology, and Data Analysis and Organize & Limitations. The second chapter contains the Background of “Trust Bank Ltd.”, Organization Structure of “Trust Bank Ltd.”, Vision of “Trust Bank Ltd.”, and Mission Statement of “Trust Bank Ltd.” In third chapter, it contains the Theoretical framework. In chapter four, it contains Analysis of Credit Operation of Trust Bank Ltd and chapter five contains Ratio Analysis and Frequency Analysis & Findings. Different Problems, suggestions, recommendations have come at the end of the report.

TheProblems findings during the three-month internship period & suggestions are given from observation, comparative analysis, strategic point of view etc. In fine, this paper contains some findings and recommendations, which may be helpful for the Bank.

TBL has gained success from the very beginning of their operation and was capable enough to hold the success year after year. It gained success very early because it has a very strong backup to provide it financial support and they are the army welfare trust. The credit portfolio of the bank is a mix of scheme loans, micro credit, marriage loan, car loan, and commercial loans. Commercial loans comprise trade financing in the form of working capital and other funded and non-funded credit facilities. The bank has a classified loans and advances much lower (3%) than the national average (30%).The bank as a matter of priority it wants to ensure the quality of its loans portfolio by strengthening post disbursement recovery measures as well as by prioritizing on Early Warning System (EWS) to check the growth of non-performing assets.

Introduction

Now a day, education is not just limited to books and classrooms. In today‟s world, education is the tool to understand the real world and apply knowledge for the betterment of the society as well as business. From education the theoretical knowledge is obtained from courses of study, which is only the half way of the subject matter. Practical knowledge has no alternative. The perfect coordination between theory and practice is of paramount importance in the context of the modern business world in order to resolve the dichotomy between these two areas.

Banking system plays a very important role in the economic life of the nation. The health of the economy is closely related to the soundness of its banking system. In a developing country like Bangladesh the banking system as a whole play a vital role in the progress of economic development. A bank as a matter of fact is just like a heart in the economic structure and the capital provided by it is like blood in it. As long as blood is in circulation the organs will remain sound and healthy. If the blood is not supplied to any organ then that part would become useless.

So if the finance is not provided to agriculture sector or industrial sector, it will be destroyed Loan facility provided by banks works as an incentive to the producer to increase the production. Banking is now an essential part of our economic system. Modern trade and commerce would almost be impossible without the availability of suitable banking services.

First of all, banking promotes savings. All manner of people, from the ordinary laborers and workers to the rich land owners and businessmen, can keep their money safely in banks and saving centers.

Secondly, banking promotes investments. Banks easily invest the money they get in industry, agriculture and trade. They either invest it directly or advance loans to other investors.

Thirdly, it is most through banks that foreign trade is carried on. Whether we export or import, it is through banks that money is transferred from one country to another. For example, bills of exchange and letters of credit are the regular ways banks use to transfer money. A number of recent studies, however, indicate that the banking sector plays a more important role than it was believed earlier.

Trust Bank Limited is scheduled bank incorporated on 17 June 1999 under the Companies Act 1994 as a public limited company by shares for carrying out all kinds of banking activities. They received their Certificate if Commencement of Business on the same date. Trust Bank Limited listed with Dhaka Stock Exchange on 25th September, 2007 and Chittagong Stock Exchange on 24th September, 2007

The bank sponsored by Army Welfare Trust (AWT), is first of its kind in the country. With the wide range of modern corporate and consumer financial products Trust Bank has been operating in Bangladesh since 1999 and has achieved public confidence as a sound and stable bank.

Objectives of the Study

The main objectives of this study are to familiarize with overall activities of the Performance Evaluation of Credit Operation Systems maintained by TBL.

- To present an over view of Trust Bank Ltd (TBL).

- To analysis the Lending procedures maintained by the TBL

- To observe principal Lending activities of Trust Bank Ltd.

- To evaluate Lending performance of Trust Bank Ltd.

- To measure the actual position in classified Loan and provisions maintained by TBL

- To understand the project evaluation technique of TBL.

- To appraise the actual Recovery position of TBL

- To identify problems in credit operations of Trust Bank Ltd.

- To recommend suggestions for the successful Lending Operations of Trust Bank Ltd.

- To have a practical orientation of the job market;

- To gather knowledge about the practical application of the financial systems;

- To present an over view of TBL;

An Overview of the Trust Bank Limited

Trust Bank Limited is scheduled bank incorporated on 17 June 1999 under the Companies Act 1994 as a public limited company by shares for carrying out all kinds of banking activities. They received their Certificate if Commencement of Business on the same date. Trust Bank Limited listed with Dhaka Stock Exchange on 25th September, 2007 and Chittagong Stock Exchange on 24th September, 2007

The bank sponsored by Army Welfare Trust (AWT), is first of its kind in the country. With the wide range of modern corporate and consumer financial products Trust Bank has been operating in Bangladesh since 1999 and has achieved public confidence as a sound and stable bank. In 2001, Trust Bank introduced automated branch banking system to increase efficiency and improve customer service. In the year 2005, the bank moved further and introduces ATM services for its customers. Since bank‟s business volume increased over the years and the demands of the customers enlarged in manifold, their technology has been upgraded to manage the growth of the bank and meet the demands of their customer. They also provide online banking service which facilitates any branch banking, ATM banking, internet banking, mobile banking. All these facilities help customers to deposit or withdraw money from any branch within the country.

Present day Trust Bank Limited is one of the leading commercial bank having a spread network of 82 branches, 7 SME centers, 132 ATM Booths, and 55 Branch POS (Point of Sale) across Bangladesh and plans to open more branches to cover the commercial area of Dhaka, Chittagong, Sylhet and other areas. Trust bank is a customer oriented financial institution which meets up ever growing expectations of the customers.

In January 2007, Trust Bank successfully launched Online Banking Services which facilitate Any Branch Banking, ATM Banking, Phone Banking, SMS Banking, & Internet Banking to all customers. Customers can now deposit or withdraw money from any branch of Trust Bank nationwide without needing to open multiple accounts in multiple branches.

Via Online Services and Visa Electron (Debit Card), ATMs now allow customers to retrieve 24×7 hours Account information such as account balance checkup through mini-statements and cash withdrawals.

Trust Bank introduced Visa Credit Cards to serve its existing and potential valued customers. Credits cards can now be used at shops & restaurants all around Bangladesh and even internationally. Trust Bank is a customer oriented financial institution. It remains dedicated to meet up with the ever-growing expectations of the customer because at Trust Bank, customer is always at the center.

The bank has plans to invest extensively in the country‟s industrial and agricultural sectors in the coming days. The bank has participated in syndicated loan agreement with other banks. Such participation would continue in the further for greater interest of the overall economy. The bank is keen to constantly improve its services to the clients and launching new &innovative products to provide better services towards fulfillment of growing demands of its customers.

The authorized capital of the bank is Tk. 2000 million. The Army Welfare Trust (AWT) is the major shareholder bearing 51% share. Total shareholders‟ equity at the end of December 2007 stood at Tk. 7200.20 million, where Paid-up capital is Tk. 3405.41 million, statutory reserve is Tk 2169.22 million and Retained Earnings is Tk. 656.32 million. The Paid- up capital is indicative of the face value of 5, 00,000 ordinary shares of Tk. 1,000/-each fully subscribed by the shareholders.

General Banking

Trust Bank Ltd has been a strong structured general banking system since 1999. This Bank sponsored by the Bangladesh Army Welfare Trust (AWT). They have lots of product and schemes and strong policy to control over whole general banking system. Bay by day, they are increasing their growth.

- Cash Department

- Remittance Department

Cash Department

All sorts of transaction considering the cash are taken into the care in the cash department. Cash is deposit in the name of concern bank and disbursed to the client by his/her department.

- Opening of Cash: Beginning balance is used to start daily transaction.

- Maintenance of Receipt and Payment Registers while receiving & paying different amount of cash.

- Previously issued cheque will be paid if issued 6 months before.

- Advance issued cheque cannot be made payment even one day before.

- Evening Banking: can only receive cash. No payment can be made except some special cases.

- TBL Dhanmondi Branch provides “Sheba Service” in this branch

- Issue Note: Notes issued by the bank & accepted by the people, fresh notes.

- Non-issue Note: Notes cannot be issued for public like torn, mutilated notes Soiled Notes etc.

Remittance Department

Remittance mean “Remittance other than local” .Remittance is another significant part of the general banking. The bank provides services and various types of bills through the remittance within the country. Obviously, the bank charges commission on the basics of bills account. Anyone can now transfer money conveniently and in real-time to Bangladesh within minutes via the third party available at all in Bangladesh. Money may be remitted via any of the third party providers located in over 200 countries worldwide. This service is available to all.

Trust Bank Limited has some of the third party. Those are given below:

- Western Union

- Placid Express

- Orchid Money Transfer

- National Exchange Company, Italy (NEC)

- NEC Money Transfer, Spain (NMT)

You do not need to have a Trust Bank Account to avail this service. Western Union is a world leader in the money transfer business with global presence and international recognition. In 2013, Bangladesh faces decline in remittance earnings for the first time since 42 years of our independence. Compared to year 2012, our inward remittance reduced Taka 7,607 crore in 2013. In FY 2013, foreign remittance was 9.50% of our GDP against 11.11% & 10.55% in FY 2012 & FY 2011 respectively. The drop is keeping with the trend since last August, when it turned negative after slow down since the final half of FY 2013. Only 450,000 migrants managed overseas jobs in 2013, down by more than 33% from 2012 according to Refugee and Migratory Movements Research Unit (RMMRU). In the first seven months of FY 2014, remittance came down to USD 8.00 billion from USD 8.69 billion for the same period of last fiscal. In spite of that, our external sector stability eased due to foreign exchange reserves that reached USD 18.00 billion at the end of December 2013, sufficient to cover about 5.5 months of projected imports.

Trust Islamic Banking

Trust Islamic Banking (TIB) started its operation from later part of 2008 through 5 (five) Islamic banking windows at the TBL-Principal Br., Gulshan Br., Dilkusha Br. in Dhaka, CDA Avenue Br. in Chittagong & Sylhet Corporate branch in Sylhet. In addition to the above mentioned 5 (five) branches, all TBL branches are now providing Islamic banking services to their clients under centralized on-line operation system. In addition to the Sharia guidelines, Trust Islamic banking operations are strictly complied with the Bangladesh Bank instructions regarding Islamic banking operations and adhere to the followings:

- Completely Separate Fund management – no mingling of fund with the conventional banking deposits of the Bank.

- Separate book-keeping, Profit & Loss Account by Islamic banking software.

- Investment from the Islamic banking deposits only.

- Profit sharing with the depositors at 70:30 ratios.

Business Banking

Trust Business Banking includes with corporate financing, SME financing Syndicated loans, Women Entrepreneur Loan, Trust Falan Agri-Business Loan etc. These types of activity help Trust Bank Ltd to improve Customer relationship and also to improve his business rapidly. Entrepreneurship development is also a goal of this banking system.

Technology (IT) & Automation Information

All the branches of the TBL are fully computerized. New software named Flora is now in use to provide faster, accurate and efficient service to the clients. The bank is continuously striving for better services through extensive automation of its branches. Trust bank has launched “Any Branch Banking” through on-line connectivity. The bank has set up a full-fledged IT division to keep abreast of the latest development of IT for better service in the days to come.

At present, following online banking services are with the system:

- Cash deposits i.e. accountholders of one branch can deposit cash in account at another branch.

- Cash withdrawals, i.e. accountholder of one branch can withdraw cash from another branch.

- TBL cheque deposits i.e. accountholder of one branch can deposit TBL cheque in his/her account at another branch.

- Online Clearing i.e. account holder of one branch can deposit clearing instruments in his/her account at another branch.

Mobile Banking Services

Trust Bank Limited launched “Trust Bank Mobile Money” on 31 August 2010 especially for the unbanked rural people to materialize the motto “A Bank for financial Inclusion”. In Bangladesh most of the rural people are not educated and thus cannot write cheque or sign. Also they need to maintain a minimum balance in their accounts to pay various charges which tends to be difficult for the rural people. Through Trust Bank Mobile money service the customer can use their mobile phone to authenticate a transaction by typing their secret PIN (instead of having to write a cheque and signing it); if the combination of the PIN and the customer‟s mobile phone number is correct, the transaction will be done successfully and a confirmation SMS will be sent to the user end. Trust Bank Mobile Money is a Bank-Led model complying all the rules and regulation of Bangladesh Bank. It enables subscribers to quickly, easily, and securely transfer balances to other subscribers via their mobile phones (SMS & USSD) or Internet. Any mobile subscriber can avail Trust Bank Mobile Money services using any mobile handset from low end to high end. Customer of Trust Bank Mobile Money can avail the service at all Trust Bank Branches SME Centers, T-Lobby and accredited Pay points. Trust Bank is deploying its Pay point Network through different distributor such as Teletalk, Robi, Citycel, Arena, Quantum, A2i (UISC,PISC) and Third Eye NC Limited.

Social Commitment and Future Prospect

It has been all most nine years since the stepped in to the banking arena. They are not yet past of their formative stage. It would be only a matter of time for them to testify that they are equally committed to the social up liftmen of the country. They would stand by the people through philanthropic activities whenever any crisis and disaster confront them. They will not keep their social welfare activities restricted to one area only. It will be diversified in the days ahead of us as they are planning to award students of exceptional academic performance with scholarship in different educational institutions. They expect to launch soon school banking by extending their services, which would encourage parsimony in the students. It would also help in the creation of savings, which could be utilized for pursuing higher studies in future. Keeping in mind their social commitment would soon launch “Educational” and “Hajj” loans. Agriculture, being the only means of subsistence for innumerable people in rural areas of the country, needs more attention. They have plans to manufacturing agricultural equipments in the Bangladesh Machine Tools Factory Ltd., which would be distributed among their farmers at an affordable price.

Products and Schemes

As a private limited bank, Trust bank is also committed to its owner to return profit by providing a good service to the customer. To providing efficient and innovative banking services to the people of all sections of our society, Trust Bank Ltd has been offered different products and schemes to its customer. They are given below-

- Current Account

- Savings account

- Short Term Deposit

- Trust Smart Savers Scheme (TSSS)

- Trust Money Double Scheme (TMDS)

- Monthly Benefit Deposit Scheme (MBDS)

- Lakhopoti Savings Scheme (LSS)

- Trust Money Making Scheme (TMMS)

- Trust Education Scheme (TES)

- Fixed Deposit Receipt (FDR)

- Interest First Fixed Deposit Scheme (IFFDS)

Deposit Products

A Banks main activity is to collect deposit, because this deposit will use as loan money. So deposit is very much important for the bank. Generally a bank‟s principal activity is to serve the customer or give service. There are different types of deposits which not only help the bank to attract the customer but also help the customer by fulfilling their demand. Different types of deposit provide different opportunities, different terms & condition. They are:

- Current Deposits Account (CDA)

- Savings Deposit Account (SBA)

- Special Notice Account.

- Fixed Deposit Account (FDR)

- Trust Education Scheme (TES)

- Trust Smart Savers Scheme (TSSS)

- Trust Money Double Scheme (TMDS)

- Trust Mobile Money (TMM)

Current Deposit Account & STD Account:

The characteristics of the current account are different from the savings account but same as STD account. In current account there is no interest on the current deposit account, but in STD account there is interest on deposit amount and there is no restriction on withdrawal. The depositor can withdraw the money from any time when he needs money, but withdrawal must be in transaction hour. The minimum limit of opening a current account & STD account in The Trust Bank is Tk.1000. There are different types of current & STD account. They are and their requirements are:

- Individual Current Account/STD A/C

- Proprietorship Current A/C /STD A/C

- Partnership Current A/C /STD A/C

- Private LTD Co. / Current A/C/STD/A/C

- Public LTD Co. / A/C STD/ A/C

- Club/Societies Current A/C/STD A/C

Savings Deposit Account:

Savings account is specially designed for the middle and low-income groups who are generating limited income and have the tendency to save. A minimum initial deposit of Tk. 500 shall be required for opening savings account. There are different types of savings account and their opening requirements are also change. They are:

- Club/ Societies/Asso. Savings A/C

- Individual Savings Account

Fixed Deposit Account (FDR):

There are various fixed deposit schemes in The Trust Bank. The interest rate of the deposited amount depends on duration and volume of the amount. If duration is long the interest rate is high, and at the same time if the volume of amount is large the interest rate is also high and viceversa. Depositors have to withdraw the interest after the maturity date. If the depositors intend to withdraw the interest earning before expiring the maturity date then the bank is not bound to pay the interest. But some times it depends on the party like if the party is big then the bank will consider to that party for getting the interest amount. The requirements for the FDR are:

- Signature Card

- Application for Fixed Deposit.

Retail Products or Loans

Bank is an institution which creates money by money. Only collecting deposits are not the task of a bank. They have to provide different loans to customer. And by this way Bank earn profit. As a private commercial bank, Trust Bank Ltd has different types of retail products. These Products create a center of attention of loan among the general customer. The Trust Bank provide Special offer for Bangladesh Army from their retail products. Retail product given by Trust Bank Ltd is given below.

- Car Loan

- House Hold Durable Loan

- Doctor‟s Loan

- Education Loan

- Advance against salary

- Travel Loan

- Any purpose Loan

- CNG conversion Loan

- Marriage Loan

- Loan against TMDS

Loan Products

Unsecured Loan:

Personal Loan, Loan against Salary, Education Loan, Doctor‟s Loan, Trust Digital Loan. Any Purpose Loan for Defence Officers, Motor Cycle Loan for Defence Personnel, Marriage Loan for Defence Personnel, House Hold Durable Loan for Defence Officers, CNG Conversion Loan Defence Officers, OD against Salary for Defence Officers, RRDH for JCO‟s and Others.

Secured Loan:

Car Loan, Apon Nibash Loan (House Finance), HBL against Registered Mortgage for Defence Officers, Army Officers Housing Loan Scheme, Trust Thikana- Home Loan, Loan against Commutation Benefits for Defence Personnel.

Credit Card

In January 2007, Trust Bank successfully launched Online Banking Services which facilitate Any Branch Banking, ATM Banking, Phone Banking, SMS Banking, & Internet Banking to all customers. Customers can now deposit or withdraw money from any Branch of Trust Bank nationwide without needing to open multiple accounts in multiple Branches. Via Online Services and Visa Electron (Debit Card), ATMs now allow customers to retrieve 24×7 hours Account information such as account balance checkup through mini-statements and cash withdrawals. Trust Bank has successfully introduced Visa Credit Cards to serve its existing and potential valued customers. Credits cards can now be used at shops & restaurants all around Bangladesh and even internationally.

Trust Bank has put emphasis on its Credit Card services. Already a Credit Card Policy has been designed and in near future the bank will come up with attractive features to provide multi level benefits to Card Holders. Already we have 2075 Credit Card users with an outstanding amount of Tk. 71 million.Now a day, Bangladesh Army members including officer and soldier can collect their money by using debit card. Trust Bank Ltd Provides 4 types of Card to collect their money from their account. They are given below:

- Visa Gold Local

- Visa Classic Local

- Visa Gold International

- Visa Classic International

- Visa Dual Card

SME Finance

SME finance is the funding of small and medium sized enterprises, and represents a major function of the general business finance market – in which capital for different types of firms are supplied, acquired, and coasted or priced. SME finance is the most effective weapons to reduce poverty & unemployment and increase productivity, industry and the growth of GDP. As a private limited bank, Trust Bank is concern to take part on improvement of our nation. SME finance is of their activity to improve the income level of poor people and newly initiated entrepreneur. Now a day, Trust Bank Ltd is more interested to invest on SME financing tricks.

As a result they are willing to endow among this type of investment.

- Trust Falan Agri-Business Loan

- Entrepreneurship Development Loan

- Loan for Light Engineering

- Loan for Poultry Farm

Risk management

Risk management refers to the practice of identifying potential risks in advance, analyzing them and taking precautionary steps to reduce/curb the risk.

In the world of finance, risk management refers to the practice of identifying potential risks in advance, analyzing them and taking precautionary steps to reduce/curb the risk.

When an entity makes an investment decision, it exposes itself to a number of financial risks. The quantum of such risks depends on the type of financial instrument. These financial risks might be in the form of high inflation, volatility in capital markets, recession,bankruptcy,etc.

For example, a fixed deposit is considered a less risky investment. On the other hand, investment in equity is considered a risky venture. While practicing risk management, equity investors and fund managers tend to diversify their portfolio so as to minimize the exposure to risk.

Risk management process

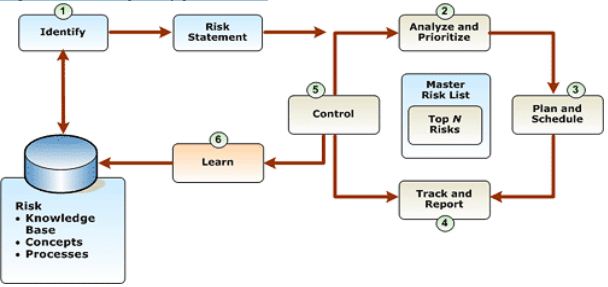

The following diagram illustrates the six steps of the risk management process: identify, analyze and prioritize, plan and schedule, track and report, control, and learn. It is important to understand that the process of managing each risk goes through all of these steps at least once and often cycles through numerous times. Also, each risk has its own timeline, so multiple risks might be in each step at any point in time.

Risk Management Process Steps

The following is a brief introduction to the six steps of the risk management process.

Identify – Risk identification allows individuals to identify risks so that the operations staff becomes aware of potential problems. Not only should risk identification be undertaken as early as possible, but it also should be repeated frequently.

Analyze and prioritize – Risk analysis transforms the estimates or data about specific risks that developed during risk identification into a consistent form that can be used to make decisions around prioritization. Risk prioritization enables operations to commit resources to manage the most important risks.

Plan and schedule – Risk planning takes the information obtained from risk analysis and uses it to formulate strategies, plans, change requests, and actions. Risk scheduling ensures that these plans are approved and then incorporated into the standardday-to-day processes and infrastructure.

Track and report – Risk tracking monitors the status of specific risks and the progress in their respective action plans. Risk tracking also includes monitoring the probability, impact, exposure, and other measures of risk for changes that could alter priority or risk plans and ultimately the availability of the service. Risk reporting ensures that the operations staff, service manager, and other stakeholders are aware of the status of top risks and the plans to manage them.

Control – Risk control is the process of executing risk action plans and their associated status reporting. Risk control also includes initiating change control requests when changes in risk status or risk plans could affect the availability of the service or service level agreement (SLA).

Learn – Risk learning formalizes the lessons learned and uses tools to capture, categorize, and index that knowledge in a reusable form that can be shared with others.

Credit risk

Credit risk refers to the risk that a borrower will default on any type of debt by failing to make payments which it is obligated to do. The risks are primarily that of the lender and include lost principal and interest, disruption to cash flows, and increased collection costs. The loss may be complete or partial and can arise in a number of circumstances. Credit risk covers the inability of a borrower or counter-party to honor commitments under an agreement and any such failures, which have an adverse impact on the financial performance of the Bank. The Bank is exposed to credit risk through lending and capital market activities.

For example:

- A consumer may fail to make a payment due on a mortgage loan, credit card, line of credit, or other loan

- A Company is unable to repay amounts secured by a fixed or floating charge over the assets of the company

- A business or consumer does not pay a trade invoice when due

- A business does not pay an employee’s earned wages when due

- A business or government bond issuer does not make a payment on a coupon or principal payment when due

- An insolvent insurance company does not pay a policy obligation

- An insolvent bank won’t return funds to a depositor

- A government grants bankruptcy protection to an insolvent consumer or business

To reduce the lender’s credit risk, the lender may perform a credit check on the prospective borrower, may require the borrower to take out appropriate insurance, such as mortgage insurance or seek security or guarantees of third parties, besides other possible strategies. In general, the higher the risk, the higher will be the interest rate that the debtor will be asked to pay on the debt.

Types of credit risk

Credit risk can be classified in the following way:

- Credit default risk – The risk of loss arising from a debtor being unlikely to pay its loan obligations in full or the debtor is more than 90 days past due on any material credit obligation. Default risk may impact all credit-sensitive transactions, including loans, securities and derivatives.

- Concentration risk – The risk associated with any single exposure or group of exposures with the potential to produce large enough losses to threaten a bank’s core operations. It may arise in the form of single name concentration or industry concentration.

- Country risk – The risk of loss arising from sovereign state freezing foreign currency payments (transfer/conversion risk) or when it defaults on its obligations (sovereign risk).

Credit Risk Management

While financial institution have faced difficulties over the years for a multitude of reasons, the major cause of serious banking problems continues to be directly related to lax credit standards for borrowers and counterparties, poor portfolio risk management or a lack of attention to changes in economic or other circumstances that can lead to a deterioration in the credit standing of a bank‟s counterparties. Credit risk is most simply defined as the potential that a bank borrower or counterparty will fail to meet its obligations in accordance with agreed terms. The goal of credit risk management is to maximize a bank‟s risk-adjusted rate of return by maintaining credit risk exposure within acceptable parameters. Banks need to manage the credit risk inherent in the entire portfolio as well as the risk in individual credits or transaction. Banks should also consider the relationship between credit risk and other risks. The effective management of credit risk is a critical component of a comprehensive approach to risk management and essential to the long term success of any banking organization. The sound practices set out in the document specially address the following areas:

- Establishing an appropriate credit risk environment.

- Operating under a sound credit granting process.

- Maintaining an appropriate credit administration, measurement and monitoring process.Ensuring adequate controls over credit risk.

Borrower Selection Process on TBL

In bank, a borrower is the party in a loan agreement which receives money or other instrument from a lender (bank) and promises to repay the lender (bank) in accordance with agreed terms. So, selection of borrower is an important component of the credit granting process. Professional loan officers analyze financial and non-financial information of proposed borrowers and set preferred levels of collateral and covenants. Borrower selection is associated with the amount of information examined, lenders’ risk preferences and years of lending experience. Effective system that ensures repayment loans by borrower is critical.

Lending means deployment of credit and all loans contain some degree of risk involved in the whole process. So, borrower selection is very much important to minimize the risks of lending as wrong borrower selection may lead to unexpected situations among the Bank, the depositors and the borrower that based upon trust.

Applications for loans and their processing

(a)Loan Application

As part of the banking business, the bank has various segments to which credit facilities are provided for their business requirements. These include a wide range of customers and range from small & medium enterprises to large corporate borrowers. The bank has a process for identification of target customers to whom facilities can be provided based on customer selection and risk assessment for that segment.

Thus, the focus is on contacting prospective customers and encouraging them to avail of banking services from Trust Bank based on the incremental value we can add to a customer’s business, rather than customers making applications to the Bank for facilities / services.

In the process of lending, loan application is vital in the sense that the borrowers express their requirement in light of their present situation. We can come to know about the clients fund requirement and purpose through loan application.

The client completes the Loan Application with the assistance of the Branch Manager or his / her delegated officer as per the suggested format. The form will help insure that adequate information about the borrower is obtained. The application should be filled out as completely as possible to provide sufficient information with which to begin the analytical process, form the basis for an initial site visit and understand proposed collateral.

One of the objectives of thorough initial visits with the client is to determine the client‟s character, business condition, prospects and to gather supplemental financial information.

Identification and appraisal of collateral is also essential during initial visits.

The way a potential borrower handles its obligations with other creditors, such as lenders and suppliers, is a strong indication of how it will handle its obligations with the bank. Therefore, we should ask questions to other creditors concerning their experience with our potential borrower.

Answer to these questions will increase understanding of the credit and make loan officers more confident about processing sound loan recommendation. The core questions may be as follows:

Does the potential borrower honor its obligations on a timely basis?

- When did you first extend loans / deliver goods to this client?

- When did you first establish credit terms (or lend money) to this client?

- What is the highest amount of credit approved for this client?

- What is the current outstanding balance?

- Will you continue to grant credit terms to this client?

- How often is payment received? When was the last payment received?

- Are payments received on a timely basis?

- Has the client ever defaulted on a payment? Was legal action ever threatened / initiated?

- Do you consider the client as safe credit risk? Why?

When checking with another bank, try to obtain information on collateral, interest rate, tenor, maturity date, payment amount, outstanding balance, status of payments (current, past due etc.) and past repayment history. The goal here is to obtain as much pertinent information as is possible.

Written confirmation of credit references, if possible, is important because it indicates that the information is most reliable. In many instances, refusal to provide written confirmation means that the information is not reliable. The bank would give an acknowledgement for receipt of all loan applications. Time-frame within which loan applications will be processed would be indicated in the acknowledgement of such applications.

The bank would verify the loan applications within a reasonable period of time. If additional documents are required, it would intimate the borrowers immediately.

(b) Credit Assessment

The bank would ensure that there is proper assessment of credit application made by borrowers. The assessment would be in line with the bank’s credit policies & procedures and relevant regulatory guidelines.

Credit risk analysis begins with the clear and careful identification of risk factors such as:

- Through Borrower / Industry Analysis

- Background of the borrower

- Loan Purpose / Tenor Justification

- Historical Financial Analysis

- Owner‟s background, character and management capability

- Ability to penetrate market sectors and competitive factors

- Projections / Repayment Ability

- Account Conduct

- Value of collateral and guarantee(s)

- Adherence to Lending Guidelines

- Mitigating Factors

- Risk Grade Scorecard

- Environment issues.

Credit Approval Process

Process relating to approval/sanctioning of credit following steps are followed in TBL:

Pre-Approval stage at branch

The credit proposals are generally routed through the Branches. The Loan Processing Department at the branch level prepares the Credit Proposals through necessary evaluation / analysis by fulfilling TBL‟s lending criteria, ensuring perfection of the security for the loans and to provide all information required on the creditworthiness of the clients. Proposals, which do not meet TBL‟s lending criteria, are not entertained generally without particular merit and justification of the case. The credit proposals are signed by the Chief Manager and the departmental head / credit officer. Then, the Credit Proposals with specific recommendation by the Branch are sent to the Head Office addressing Credit Risk Management (CRM) Division for the pre-sanction evaluation and subsequent approval or regret as the case may be.

Approval Process at Head Office

Credit Risk Management (CRM) Division consists of Corporate Credit Unit, Small & Medium Enterprise Department & Retail Banking Unit for processing & approval of credit facilities matching with the requirement:

Upon receiving credit proposals from the branches, respectivedepartment processes the proposals and makes in-depth analysis taking different risk factors into consideration for approval or regret. It takes all necessary measures to ensure quality assets. The respective department finds out all the positive and negative sides of each credit proposal recommended by the branch credit officers or relationship managers. This department ensures that the proposal has been analyzed as well as prepared complying all the necessary rules, regulations, circular, guidelines and recommendation has been made in conformity with the Credit Policy, Guidelines and Credit

Norm of our Bank, Bangladesh Bank and any other agency. It also ensures that that the recommendation falls under the purview of bank‟s lending cap, industry preference, liquidity preference, tenure preference, and other considerable factors. If the result of the analysis is found to be very satisfactory, then memo on the proposals is prepared for approval from the delegated body with opinion of the department.

Upon the recommendation of the respective department, the proposal is placed to the competent delegated authority as per discretionary power viz. Head of CRM, Deputy Managing Director, Managing Director, the Executive Committee of the Board of Directors or the Board of Directors for final approval.

Upon approval as per delegation, Sanction Advice is prepared stipulating all the standard terms and conditions to the respective branches and the copy is forwarded to the Monitoring & Control Department.

Conveying credit rejection

In the case of all borrowers seeking loans, the bank would convey in writing, the main reason/reasons which, in the opinion of the bank after due consideration, have led to rejection of the loan applications. In case the proposal does not meet the internal risk parameters of the bank, the borrower would be intimated accordingly.

Loan applications and appraisal under consortium

In the case of lending under syndication arrangement, the bank would endeavor to evolve procedures to complete appraisal of proposals in a time bound manner to the extent feasible, and communicate its decisions on financing or otherwise within a reasonable time, in co-ordination with other members of the consortium/syndication.

Disbursement of loans including changes in terms and conditions

The bank would ensure timely disbursement of loans sanctioned in conformity with the terms and conditions governing such sanction. It would give notice of any change in the terms and conditions including interest rates, service charges etc. Terms and conditions are revised as per prior agreement with the customer, the process for which is covered in the sanction letter duly accepted by the customer on the loan agreement.

Conveying credit limit and terms & conditions

Loan closings represent the end of an approval process and the beginning of a relationship process, which involves many different activities on the part of borrower and lender, which include, among other processes, repayment, monitoring and possibly collection activity.

All new loans and facilities must be evidenced by a signed agreement which is a contract between the lender and the borrower. A borrower should know precisely what he is receiving; how the loan is structured; how the bank intends to monitor and how it will enforce any special terms and conditions of the contract. Also under the terms of loan agreement, the borrower acknowledges its responsibility to promptly advise the bank about any inability to repay contractually and also of any material changes in circumstances which could give rise to an event of default in an agreement.

Creation of Charges on Securities and its Implication

For sound lending inter-alia the following points should be kept in view:

- a) Judicious selection of Customers

- b) Purpose

- c) Safety

- d) Security

- e) Liquidity

- f) Adequate return (Profitability)

- g) Supervision

- h) National/Social interest

- i) Credit Control Policy of Bangladesh Bank

It is to be always remembered that the Bank is the custodian of public money and as such we must be judicious, careful and selective while lending out the depositors‟ money to ensure timely recovery. The deciding factors for recovery of loans are selection of right type of borrowers, endues of credits and effective follow-up and proper supervision.

Securities

Securities may primarily be divided in two categories as under

- Primary security.

- Collateral security.

The assets created by the borrower from the credit facilities granted by the bank form the primary security for the bank advance as a matter of rule. The bank invariably obtains a charge over those assets. Similarly, other assets on which the advance is primarily based even if it is not created from the credit facilities granted by the bank will also be taken as primary security.

In some cases where primary security is not considered adequate or the charge on the security is open the bank may insist on an additional security to collaterally secure advances granted by it. Such securities are termed as collateral securities. Collateral security may either be tangible or third party guarantees may also be accepted.

Note: Floating assets are not permanent and these are ever changing assets that change depending on the business e.g. cash, accounts receivable, notes receivable, finished products, goods in the process of manufacturing, raw material, supplies etc. Fixed assets are those which are fixed in nature like plant/factory, machinery, building, land, etc.

Charging of securities

While talking about charging securities, we basically mean charging tangible securities. Tangible security is something that can be realized from the sale or transfer. Shares, inventory, land, machinery, furniture, vehicles, life policies, bills, savings instruments etc. are examples of tangible securities.

Security is obtained by the bank as an additional cover against default by the borrower in repayment of bank’s dues. Charging of security means making such security available to the bank and involves certain formalities. Charging should be legal and perfect so that it is possible to realise the security if such a need arises. In order to perfect a claim on a tangible asset offered as security, we need to establish Bank‟s charge by obtaining proper charge document duly executed. For example, if a borrower offers pledge of his inventory as security against a loan, we need to obtain a letter of pledge executed by the borrower. So, pledge is a kind of bcharge applied to certain kind of assets offered as security. Similarly, there are other modes of charging securities, applicable for different kinds of securities.

There are 7 different modes of charging a security as under:

- Pledge

Pledge is bailment of goods as security for payment of debt or performance of a promise. In another definition it says that bailment is the delivery of goods by one person to another for some purpose, under a contract that goods shall, when the purpose is according, be returned or otherwise disposed of according to the directions of the person delivering them.

The definitions above suggests that-

– Pledge means delivery of goods

– The bailment must be by or on behalf of the debtor or intending debtor

– It must be intention of the parties that the goods will serve as security for a debt or performance of a promise.

So, a pledge may be in respect of goods, stocks & shares, documents of title to goods or any other moveable assets. Possession of goods is important in a contract of pledge. A pledge is said to be created, when the goods are handed over by the borrower to the lender with the intention of their being treated as a security for the repayment of the loan. The delivery of the goods can be actual or constructive. Physical handing over of goods in the warehouse by the borrower to the lender is handing over actual possession. Where documents of title to goods are delivered duly endorsed it is termed „constructive possession‟. Both are legal delivery.

The pledge has special interest in the goods pledged and has a right to retain the goods, till his claims are fully satisfied. If the borrower is in default in payment of the debt against which goods are pledged, the lender may sell the goods held under pledge as security on giving the borrower reasonable notice of sale. The document executed to establish a contract of pledge is called a Letter of Pledge.

- Hypothecation

Hypothecation is a charge against property for an amount of debt where neither ownership nor possession is passed to the creditor.

In hypothecation, the goods remain in the possession of the borrower and are equitably charged to the lender under a document signed by the borrower. The borrower binds himself under hypothecation agreement to give possession of the goods to the lender when called upon to do so. After possession is handed over to the lender, the charge converted from hypothecation to pledge. Hypothecation being only an equitable charge on moveable assets without possession, the facility is granted only to parties of undoubted means with high estintegrity.

However, in case of hypothecation advance to a limited company, the charge has to be compulsorily filed for registration with the Registrar of Joint Stock Companies under relevant section of the Companies Act, 1994.

However, due to the underlying risks of making advances purely on hypothecation basis, lenders usually prefer to obtain adequate collateral security in addition to the hypothecated goods/assets

- Mortgages

A mortgage is the transfer of an interest in specific immovable property for the purpose of securing the payments of money advanced by way of loan, an existing or future debt, or performance of an engagement which may give rise of a pecuniary liability. The transferor is called a mortgagor, the transferee a mortgagee and the principal money and interest of which payment is secured for the time being arc called the mortgage money and the instrument by which the transfer is effected is called a mortgage deed.

A mortgage is entirely different from a sale. A sale is the transfer of property (all the rights the seller may have in the property) to the purchaser in exchange for a price. Mortgage is the creation of right of the Bank on a landed property against loans and advances.

A mortgage is the transfer of legal or equitable interest in property by the borrower (mortgagor) to the lender (mortgagee) as security for the repayment of a debt etc. Mortgages have different forms, such as Simple mortgage, English mortgage, mortgage by conditional sale,equitable mortgage etc. However, with the recent amendment of the Registration Act, only Registered Mortgage is applicable for creation of charge on landed property in Bangladesh.

- Registered mortgage

When a mortgagor executes a deed of mortgage in favour of a lender and the deed is registered with Sub-Registrar’s office, the mortgage thus created is called a registered mortgage. Banks usually prefer a registered mortgage as the encumbrance on the property is registered and it will come in the notice if a search is made before anyone considers accepting a transfer of right/interest in the property. Notwithstanding, any subsequent mortgage/sale transaction registered will be effective subject to redemption of the charge by the first mortgagee.

The mortgagor has a right of redemption on payment of the debt after it has become due. However, mortgage does not automatically give the right to sell the property to the Bank in case of borrower‟s default. It is given through the Irrevocable General Power of Attorney executed by the owner

- Assignment

Assignment means transfer of a right, property or debt by one person to another person. The person transferring the right is known as assignor and the person to whom the right is transferred is known as assignee. The assignment may be legal in which case the assignor must give a written notice of the assignment stating the name and address of the assignee to the debtor or may he equitable where no such notice is sent. This form of charge is generally adopted for charging of book debts, monies due from Government (supply bills) and life insurance policies etc. Banks generally go in for legal assignment and insist for obtaining an acknowledgement of assignment from the debtor.

- Set-Off

Set off is the right of combining of accounts between a debtor and a creditor so as to arrive at a net balance payable to one or the other. Set off in relation to bank means his right to apply the credit balance in customer’s account towards liquidation of debit balance in another account of the customer provided both the accounts are maintained by him in the same capacity. The right may not be considered as absolute and the bank may be required to give a notice for exercising his right of set off. The right of set off can be applied by the bank only if the following conditions are met:

(a) The liability of the borrower is for a sum which is certain,

(b) The repayment of debt is due, and

(c) Both the accounts are held by the customer in the same capacity.

The right of set off should, however, not be exercised arbitrarily and a notice for combining the accounts must invariably be served by the bank on the customer.

- Lien

Lien means the right of the creditor to retain the goods or securities of the debtor, which are in his possession until the debt due from the debtor is paid. It does not require any specific agreement to support this right. The lien may be general which confers the right to retain any goods for a general balance of account or it may be particular lien where goods can be retained by the creditor for a particular debt only. The person exercising general lien has only a right to retain the goods till the dues are paid and may not be able to sell those goods.

The right of the banks to general lien is however, considered on a different footing and banks have a general lien on all securities deposited with them as bankers by a customer, unless there be an express contract or circumstances that show an implied contract, inconsistent with lien. A banker‟s lien is thus more than a general lien, it is an implied pledge. The bank, therefore, has a right to sell the goods in its possession after giving a reasonable notice. The lien can be exercised on bills and cheque deposited for collection, dividend warrants received by the banker as a mandate from the customer, securities left with the banker after a particular loan has been paid.

The banker‟s lien however, does not extend to:

(i) Securities or valuables lying in the locker rented to the customer.

(ii) Securities deposited upon a particular trust.

(iii) Securities deposited to secure a specific loan.

(iv) Securities left with the banks after an advance against them have been adjusted.

(v) Securities left inadvertently with the bank.

No specific letter of lien agreement is necessary as the banks enjoy the right of lien under the Contract Act. However, in some cases the bank may obtain a specific letter of lien so that the borrower is not able to contend later that the securities were deposited by him for a specific purpose inconsistent with the lien.

Loan Monitoring, Control of Security and Compliance

Loan Monitoring

- The monitoring starts when copy of sanction letter/approval is received in this connection.

- This extensive measure is taken to strictly comply the terms and conditions stipulated in the sanction advice.

- Besides the monitoring and follow up of the existing loan accounts need to be expedited with a view to finding out timely measures if required any.

Steps -1

- Monitoring starts at the time of receiving application from our valued client.

- After receive application branch should check whether the purpose is clearly mentioned or not on the application.

- Then obtain all the relevant documents of the loan that would be serve client‟s purpose as per process guide line.

Steps -2

- Examine all docs whether these are true or fake.

- If more info needed contact with the initiator / branches immediately.

- After getting all the information & charge documents are in order then go for approval process from the competent authority.

- If there is any major discrepancy is identified return application to the respective branch or initiator.

- Check genuinely of the CVP.

- Fulfill KYC of applicant.

Steps -3

- Prepare sanction advice & send it to the branch.

- Branch will meticulously go through the contents of the sanction advice, prepare agreement letter as per terms & condition of sanction advice done by the Head office & will take written consent as acceptance on the agreement letter.

- After completion all the formalities by the respective branch the loan would be disbursed to the mentioned saving or current acct as per disbursement schedule.

Steps -4

- If any company (CPV) submits false verification report then bank will go for necessary action against them as per bank‟s policy or deed of agreement on timely basis.

- Branch & head office will maintain a strong MIS to monitor assets portfolio health & review them as well.

Steps -5

- Separate expiry schedule will have to be maintained so that the status of the outstanding well ahead of the stipulated expiry dates.

- Remain in touch with the clients so that they will come to know whether they are facing any difficulty in complying the terms and conditions of the sanction letter.

- Periodically contact with the clients to ascertain the end use of the credit facility extended.

Steps -6

- In this connection weekly, fortnightly or monthly statement as and when required, may be prepared and meticulous review thereof may be instantly intimated to the respective branches for immediate rectification.

- Physical Joint inspection with the Head Office people if required under the condition of the sanction advice will have to be done in time and report thereof will be submitted to the higher Authority for kind consideration.

Steps -7

- In this connection, a periodical preferably monthly statement pointing out all the important features may be submitted to the Management Committee for kind information.

Steps -8

- Reminder through letter/SMS/internet/telephone about installment payment before the due date.

- In case of limit enhancement or reduction, additional security must be obtained to cover the full exposure along with revised up to date charged documents.

- Surprised checking by the internal auditor or Special inspection team whether the documents are in order according to guideline.

Steps -9

- Business development Manager/Portfolio Manager should check volume on regular basis for setting new strategy of the business to increase its volume.

- Checking validity of the charge document.

- Do review according to the expiry.

- Remind customer to complete formalities to regularize the exposure so that they can do transaction without any hassle.

Steps -10

- Maintain MIS of security held with loan and monitor regularly. It will help customer to replace security on due date/time.

- Retirement of LC documents by taking proper consent of the client.

Steps -11

- Existing loan position of all the regular clients.

- All relevant statements will have to be prepared.

- All the statement will have to be meticulously reviewed with a view to identify the anomalies and necessary measures to be taken for rectification.

- Periodical and sometimes surprise examination of the account transactions of the selective clients.

- Surprise checking if felt necessary of daily outstanding position of the branches.

Steps -12

- Historical analysis be done as well as maintained in order to observe the repetition/frequency of irregular/ casual or excess drawing allowed to the same clients by the same person.

- Surprise visit to the branches may be carried out with a view to emphasizing the strict compliance of the terms and conditions of the sanction advice as well as all the circulars and credit norms.

Findings of the Study

The middle in of twenty first century here we are facing a heavy competition with each other. Here everyone is competing with each and every single point. So today‟s business institution are moving forward to remember this concept. If anyone has a week point than the rival party will take the opportunity and make a problem for the week intuition. After complete my internship in The Trust Bank I realized that there are many problems and this may be a cause of huge loss or create a barrier for the future prospect. So the bank should take care of it very seriously.

Bank faced with higher operating cost in recent year, because Trust Bank has increasingly turned toward automation and electric equipment‟s to replace labor based production systems. Specially for taking deposits, dispensing payments and taking credit available.

Bangladesh is a developing country. If bank service replaced by electronic communication and automated as a result further loss of jobs as capital equipments is substituted for labor. So bank employment will become declined.

- Trust Bank Ltd has a good reputation Among Bangladesh Army. From this three month internship, I have been observed that, there are soft corner among Bangladesh Army about the employee of Trust Bank. When a Military police (MP) saw an employee of trust bank, then he never stop him to search because of trust and respect. Other peoples may have to face lots of question to enter on cantonment. But the employee of trust bank ltd may not face those types of questions.

- Trust bank Ltd making Salary card or debit card for Bangladesh Army. By making this process, every army will get an account number on trust bank. As a result they will be interested for deposit money on TBL. On the other hand, when soldiers get any purpose loan from trust bank, then the loan‟s default risk will reduce by this system.

- Bangladesh Bank, the central bank, has instructed all banks to keep 1% as provision against of outstanding of total loans. This provision has been made to meet any kind of future losses. Although Trust Bank Ltd does not have any classified loans it is maintaining 1% provision for future. The bank is prepared to meet any unwanted situation in future.

- The credit analysts have a strong background in accounting financial statement analysis, business law and economics along with good negotiating skills.

- The controlling officers are effective in providing necessary guidance and support to the branch.

- Branch Manager Conscious efforts to achieve the targets and knows how to motivate employees and how to represent the Bank well in the local community.

- The monitoring system of the Credit department of TBL is very excellent. The chain of command is strictly maintained here.

Recommendation

- The credit policy of Trust Bank is very restrictive and defensive. As a result, its loan sanction procedure is somewhat complex. The loan policy and loan sanction procedure should be made flexible and easy.

- Trust Bank, usually, does not provide overdraft without full coverage of security. TBL only provide Secured Overdraft. As a result, its overdraft facility is not expanding.

- Trust Bank has little attention about publicity and advertisement. As a result, most of the consumers are unaware about the bank. So extensive publicity and advertisement is required. Trust bank can set up bill board and it can sponsor different social program to introduce TBL.

- Trust bank holds huge reserves and fund that are not utilized. As a result, huge opportunity cost is incurred by TBL. So TBL should provide more loans to the profitable credit line.

- Trust Bank is introducing retail banking in recent time. But the rules and loan sanction requirement is so strict and conservative that retail banking department is not in satisfactory position.

- Bank should use more automated and electronic modern equipments like ATM, debit card, credit card, smart card.

- Trust bank training programs can encourage their trainees to seek additional education including computer classes, accounting, MBA programs and foreign language instruction.

- The number of employees & Officers should increase for operating official activities smoothly.

- In the credit department, strict supervision is necessary to avoid loan defaulters.

The bank official should do regular visit to the project.

Conclusion

The Trust Bank Limited is a 3rd generation bank in Bangladesh and has a strong position in the today‟s competitive market. It has some features which makes the bank quite different in the private sector. The bank has a tremendous management side that is still trying to make the bank more successful.

The Trust Bank Ltd. has incorporated in 1999. But within this short period of time it becomes in a good position and is continuously upgrading itself with a view to be competitive and to remain the leader of the banking industry. The bank renders service accuracy, friendliness, new ways of meeting customer needs and good quality of services.

Success in the banking business largely depends on effective lending. Less the amount of loan losses, the more the income will be from lending operations. And the more will be the profit of the bank and there lies the success of lending risk. Trust Bank Ltd is one of the most potential banks in the banking sector. It has a large portfolio with huge assets to meet up its liabilities and the management of this bank is equipped with the expert bankers and managers in all level of management. So it is not an easy job to find out the drawbacks of this bank. I would rather feel like producing my personal opinion about the ongoing practices in Mirpur Branch. The service provided by the young energetic officials of the Trust Bank Limited is very satisfactory. As a commercial bank TBL has to follow the rules of Bangladesh bank despite the fact that these rules sometime restrict the foreign business to some extent. Though its main customer is Bangladesh army but it is committed to provide the best service to general customer. As a Disciplined and strong structured Bank, trust bank ltd provide the quick & well-organized service to the customer. As result, day by day Credit business is going to be a popular business among the customer of Trust bank Ltd. During my internship in this branch I have found its Credit to be very efficient; therefore this department plays a major role in the overall profitability of the branch and to the Bank as a whole.