It is great privilege to express our gratitude to our creator Allah for such great opportunity to be in touch with Al-Arafah Islami Bank Limited (AIBL) for the following days. We also have to put our heartened feelings and gratitude for the kindness and assistance that was provided to me to complete our assigned report as on the topic “General Idea About Investment.” In preparing the proposed report we have taken great assistance support and guidance from the employee of Al-Arafah Islami Bank Limited, Gulshan Branch.

Objective Of The Study

The program of the internship program is to familiarize students with real business situation, to compare them with the business theories and at last stage make a report on assign task. Objectives regarding this study are as follows:

General Objectives:

- The general objective of this report is to fulfill the requirement of internship report.

- To earn practical experience and knowledge about the banking operation and corporate functions performed by Al- Arafah Islami Bank Limited

Specific Objectives:

- To submit a brief description about the performance of Al- Arafah Islami Bank Limited.

- To make general evaluation of AIBL activities among different professionals.

- To understand the various products and services the bank offers and to understand the mechanism of the services.

- To analyze the Investment of the bank to evaluate the performance.

- To know about the various products and services of AIBL

Methodology

To prepare this report I preferred different types of method that is suitable. Mainly, report is based on theoretical explanations. To collect information I used different type of primary and secondary sources. To present report I use different method. They are:

- Theoretical explanations

- Table

- Different type of chart

Background Of The Company

Al-Arafah Islami Bank started its journey on 18 June 1995 with the said in mind and to introduce a modern banking system based on Al-Quran and Sunnah. The opening ceremony took place on 27 September 1995. A group of established, dedicated and pious personalities of Bangladesh are the architects and directors of the bank. Among them a noted Islamic scholar, writer, economist and ex-bureaucrat of Bangladesh Government MR. A. Z. M Shamsul Alam is the founder and chairman of the bank. His continuous inspiration and progressive leadership provided a boost for the bank in getting a foothold in the financial market of Bangladesh. A group of 20 noted and dedicated Islamic personalities of Bangladesh are the member of Board of Director of the bank.

Wisdom of the directors, Islamic bankers and the wish of Almighty Allah make Al-Arafah Islami Bank Limited. It is most modern and leading bank in Bangladesh. New products are the tool of the bank to achieve success. The bank has diverse array of product and services to satisfy customer needs. The bank has achieved a continuous profit and declared a good technology. Now AIBL is one of the Best-Rated banks in Bangladesh. It is in 6th AIBL Profile

position in CAMELS rating. The bank is committed to contribute significantly to the national economy. It has made a positive contribution towards the socio-economic development of the country with 100 branches.

Form Of AIBL

Investment

Overall idea of Investment

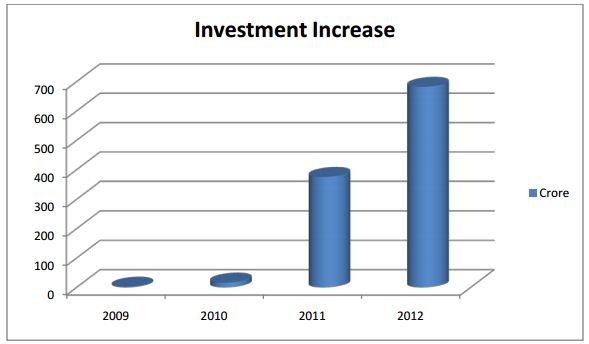

As known to all Al-Arafah Islami Bank Limited follows Islamic Shariah. The bank emphasizes on halal business. Al-Arafah Islami Bank Limited does not invest in loans and fixed interest securities. It can invest ordinary share only while interest based bank can invest in loans and different kinds of securities. The customer and the bank share become the joint owner of the property in proportion to their share in purchasing the property. For the time being customer manage to purchase the entire share of bank. Ultimately, customer becomes the sole owner. Now a day Al-Arafah Islami Bank Limited is one of the leading in our country. Gulshan branch of AIBL was opened in September, 2009. The total investment of Gulshan branch in 2009 is about 2 crore, in 2010 is about 16 crore, in 2011 is about 375 crore and in 2012 is about 682 crore only. Within 3 and half years this branch improves a lot.

Investment division of AIBL

Investment division divided into two parts. They are: investment monitoring unit and investment recovery unit.

Investment monitoring unit: According to the name Investment monitoring unit observe investment recovery unit’s work. Either recovery unit did right thing or not. After doing recovery unit work investment monitoring unit just monitor recovery unit work.

Investment recovery unit: Investment recovery unit recover the loan money to the client. This unit head talk with the client and decide either they disburse loan to the client or not.

According to Gulshan branch, though they called them two units. But according to my observation I don’t see two unit’s works are different. Investment monitoring unit and investment recovery unit do their work jointly.

Investment Principles &Investment Products

Islamic banks do not directly deal with money. They run business with money. The funds of Islamic banks are mainly invested in following modes:

Mudaraba: Mudaraba is a shared venture between labor and capital. Here bank provides with entire capital and the investment client conducts the business. The bank, provider of capital, is called Sahib-Al-Maal and the client is called Mudarib. The profit is distributed between the bank and the investment client at a predetermined ratio. If any loss cause in that business the bank has to bear the entire loss.

Musharaka: Musharaka means partnership business. Every partner has to provide more or less equity funds in this partnership business. Both the bank and the investment client reserve the right to share in the management of the business. But the bank may opt to permit the investment client normally conducts the business. The profit is divided

between the bank and the investment client at a predetermined ratio. If any loss cause in that business both the bank and the investment client have to bear the loss according to capital ratio.

Bai-Murabaha: Contractual buying and selling at a mark-up profit is called Murabaha. In this case, the client requests the bank to purchase certain goods for him. The bank purchases the goods as per specification and requirement of the client. The client receives the goods on payment of the price which include mark-up profit as per contract. Under this mode of investment the purchase/ cost price and profit are to be disclosed separately. The following conditions are essential in the contracts of Murabaha. The respective contracts must include the following aspects regarding the goods:

- Number/Quantity

- Quality

- Sample

- Price and amount of prifit

- Date of supply/ time limit

- Place of supply

- Who will bear the cost of supply?

Bai-Muajjal: Bai-Muajjal means sale for which payment is made at a future fixed date or within a fixed period. In short, it is sale on credit. It is a contract between a buyer and seller under which the seller sells certain specific goods which is under Shariah and Law of the country, to the buyer at an agreed fixed price payable at a certain fixed date in

lump sum or within a fixed period by fixed installments. The seller may also sell the goods purchased by him as per order and specification of the buyer.

In bank’s perspective, Bai-Muajjal is treated as a contract between the bank and the client under which the buyer pays the price of the goods in advance on the client specific goods, purchase as per order and specification of the client at an agreed price payable within a fixed future date in lump sum or by fixed installments.

The following conditions are essential in the contracts of Bai-Muajjal. The respective contracts must include the following aspects regarding the goods:

- Number/Quantity

- Quality

- Sample

- Price and amount of profit

- Date of supply/ time limit

- Place of supply

- Who will bear the cost of supply?

- Timeframe for payment

Salam and Parallel Salam: Salam means advance purchase. It is a mode of business under which the buyer pays the price of the goods in advance on the condition that the goods would be delivered at a particular future time. The seller supplies the goods within the fixed time.

Parallel Salam is a Salam contract where by the seller depends, for executing his obligation, on receiving what is due to him- in his capacity as purchase from a sale in a previous Salam contract, without making the execution of the second Salam contract dependent on the execution of the first one.

The following conditions are essential in the contracts of Salam. The respective contracts must include the following aspects regarding the goods:

- Number/Quantity

- Quality

- Sample

- Price and amount of profit

- Date of supply/ time limit

- Place of supply

- Who will bear the cost of supply?

- Timeframe for payment

Istisna and Parallel Istisna:

Istisna: Istisna is contact executed between a buyer and a seller. The seller pledges to manufacture and supply certain goods according to specification of the buyer. An Istisna agreement is executed when a manufacturer or a factory owner accepts a proposal placed to him by a person or an Institution to produce certain goods for a latter at a certain negotiated price.

Here, the person giving the order is called Mustasni, the receiver of the order is called Sani and the goods manufactured as per order is called Masnu. An order placed for manufacturing or producing those goods which under prevailing customs and practice are produced will be treated as Istisna Contract. Condition & characteristics if Istisna are enumerated below:

- The concerned agreement must contain the detail, such as the type, class, quantity and features of the goods to be produced, so that no misunderstanding is created later on.

- The price has to be settled, payment time and modes thereof is to be predetermined.

- When, where and on whose cost the goods to be supplied has clearly mentioned.

- If agreed by both parties, payment may be made in advance to the seller in part or in full or may be deferred to be paid in due agreed time.

- Generally timeframe is not mandatory for supplying the goods under Istisna agreement. It may be executed without determining timeframe. But in case of bank, timeframe for supplying goods must be determined to avoid any dispute in future.

- Condition for imposing stipulated compensation may be included in the Istisna agreement against the party who breaches the terms of the agreement causing the other suffer. But no compensation would be imposed on any party if it happens for any valid reason or unavoidable circumstances.

- As per opinion of the contemporary jurists, the compensation in case of Istisna may be treated as legal income.

Parallel Istisna: If it is not stipulated in the contract that the seller himself would produce the goods and services, then the seller enter into another contract with third party for getting the goods and services produced by the third party. This type of contract is called Parallel Istisna. This may be treated as a sub-contract. The main features of this

contract are:

- The original Istisna contract remains valid even if the Parallel Istisna contract fails and the seller will be legally liable to produce the goods and services mentioned in the Istisna contract.

- Istisna and Parallel Istisna contracts are treated as two separate contracts.

- The seller under the Istisna contract will remain liable for failure of the sub-contracts. Al-Arafal Islami Bank Limited

Ijara: The mode under which any asset owned by the bank, by creation, acquirement or building-up is rented out is called Ijara. Another name of Ijara is leasing. In this mode, the lease pays to the bank rents at a determined rate for using the asset and returns the same to the bank at the expiry of the agreement. The bank retains absolute ownership of the assets in such a case. However, at the end of the leased period, the asset may be sold to the client at an agreed price.

Ijarah Muntahia Bittamleak: Under this mode, the bank purchases vehicles, machineries and instrument, building, apartment etc. This mode allowed clients to use those on payment of fixed rents in installments with the ultimate objective to sell the asset to the client at the end of the rental period. The client acquires the ownership of the asset subject to full payment of all the installments.

Hire Purchase Musharaka Mutanaqisa (HPMM): Hire-purchase Musharaka Mutanaqasa means purchasing and acquiring ownership by one party by sharing in equity and paying rents for the rest of the equity held by the bank. Under this mode, the bank and client on contract basis jointly purchase vehicles, machineries, building, apartment etc. the client uses the portion of the assets of the assets owned by the bank on rental basis and acquires the ownership of the same assets by way of paying banks portion of the equity on the assets in installments together with its rents as agreed upon.

The features of this mode are given below:

- The client applies to the bank expressing his/her wishes to purchase the assets and the bank accords its approval after proper evaluation.

- The client deposits his/her share of equity with the bank after obtaining approval and the bank pays total price of the assets together with its equity.

- Before purchasing of the assets an agreement is executed stipulating the actual prices, monthly rents, price of the bank’s portion of the assets, payment schedule and installment amount and the nature of the security.

- The bank shall rent out its own portion of the assets to the client as per terms & conditions of the agreement.

Direct Investment: Under this mode, the bank can under its full proprietorship conduct business by directly investing in the industries, trading and transport. In these cases, the profit fully goes to the bank.

Investment Auctioning: Selling by auction of those assets acquired by the bank through direct investment is called investment auctioning. Generally the bank establishes industrial units by direct investment, makes the same operationally profitable and then sells out on auction. This mode of investment is very helpful for industrialization of the country.

Mode Of Investment

Murabaha

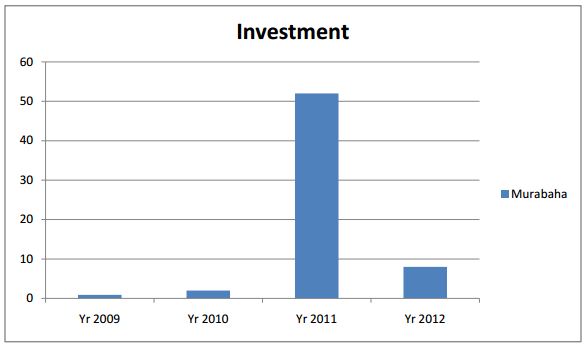

In Murabaha mode investment there was 90 lack in 2009. In 2010 it was in 2 crore and in 2011 it was in 52 crore. But investment decrease in 2012 it is only 8 crore. Under Murabaha there is only one mode. It is:

Murabaha (Post Import)

Bai-Muajjal

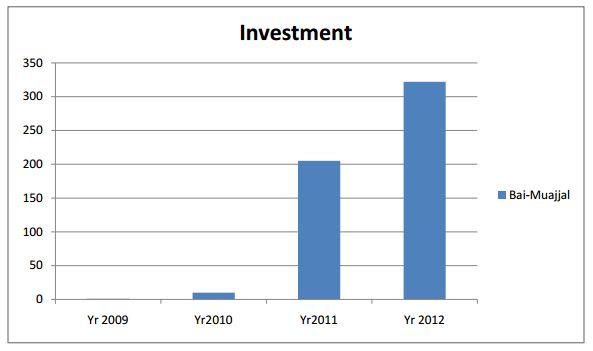

In Bai-Muajjal mode investment in 2009 was about 1 crore, in 2010 about 10 crore, in 2011 about 205 crore and in 2012 about 322 crore. In 2011 and 2012 Bai-Muajjal mode’s investment increases a lot.

Under Bai-Muajjal there are several investment modes. They are:

- Bai-Muajjal (CIS)

- Bai-Muajjal (General)

- Bai-Muajjal (Against Work Order)

- Bai-Muajjal Real Easte

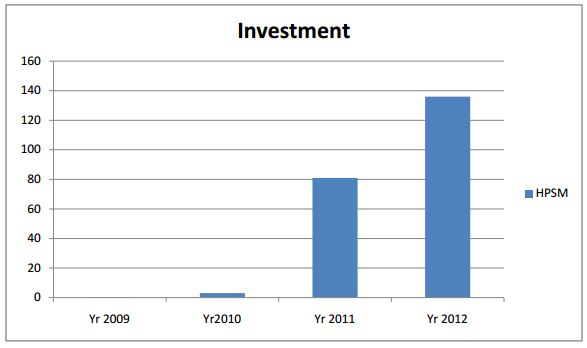

Hire Purchase Under Shirkatul Meelk or H.P.S.M.

In Hire Purchase Under Shirkatul Meelk or H.P.S.M. mode investment in 2009 was about 20 lack, in 2010 about 3 crore, in 2011 about 81 crore and in 2012 about 136 crore. In 2011 and 2012 Hire Purchase under Shirkatul Meelk or H.P.S.M. mode’s investment increases a lot.

Under HirePurchase under Shirkatul Meelk or H.P.S.M. there are several investment modes. They are:

- H.P.S.M. (General) short term

- H.P.S.M. (Real Easte)

- H.P.S.M. (Transport)

- H.P.S.M. (Machinery)

Bills Purchased

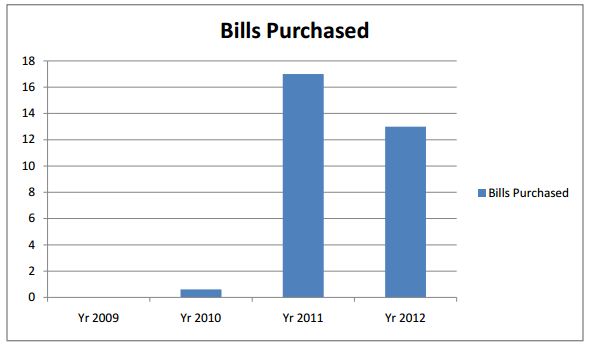

In 2009 there was no investment in Bills Purchase mode. In 2010 it was in 61 lack. In 2011 it was 17 crore but in 2012 it was in 13 crore. In 2009 Bills Purchase mode was nil. In 2010 and 2011 it was increasing but 2012 it decreased. Under Bills Purchased there are few modes. They are:

- Quard Against Inland Bills (QIB)

- Foreign Bills Purchased (FBP)

- Bai-Muajjal Wes Bill

- Bai Istisna

- Trust Receip

Other Investment

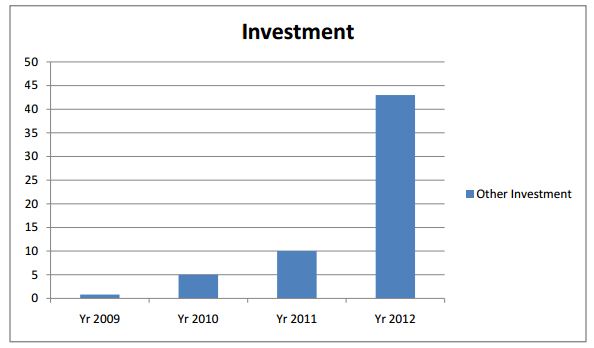

In 2009 there was only 80 lack. In 2010 Other Investment was 5 crore. In 2011 it was 12 crore. In 2012 it was 43 crore. From 2009 to 2012 it was increasing but in 2012 Other Investment was increased a lot.

Under Other Investment there are few modes. They are:

- Quard Against MTDR

- Quard Against Car

Personal Investment Scheme

Personal investment shall be allowed for miscellaneous personal financial requirement of salaried or self-employed people living in the cities where the bank has its operation. It is a clean or unsecure investment in the sense that only security in the type of investment products is:

- Letter of introduction from employer.

- Transfer of monthly salary and assignment of terminal benefits.

- Personal guarantee taken from specific section of people.

Purpose: The customer has to declare the purpose of the investment. Purposes may be as follows:

- Marriage expenses and purchase of gold ornaments

- Hospitalization or other emergency medical needs

- Educational expenses

- House renovation

- Setting up tube-well

- Mobile /telephone set

- Bicycle and purchase of miscellaneous household appliances.

Maximum amount of investment

- Without collateral security, upto Tk.300,000/=

Tenure:

- Minimum 12 months

- Maximum 48 months

- Repayment will be equal monthly installment

Idea About Loan

Loan Classification

Loan classification is a process by which the risk or loss potential associated with the loan account of a bank on a particular date is identified and quantified to measure accurately the level of reserve to be maintained by the bank to provide for the probable loss on account those risky loan.

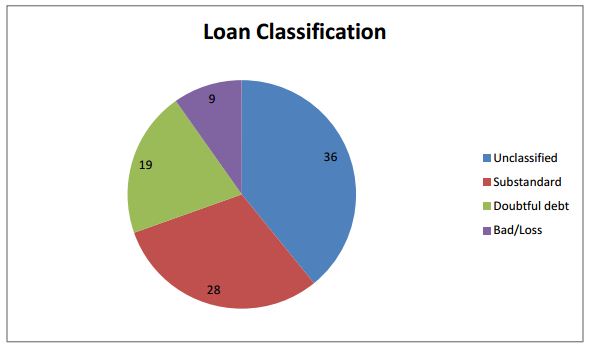

Unclassified: Repayment is irregular. The unclassified amount is about 36 crore according to year 2012. The companies are Bashundhara Chemical, Otobi Ltd and so on. Unclassified has two parts. They are:

1) Stand over: 0 to 2 months

2) Special mentioned account: 2 to 3 months.

Classified: Classified has two parts. They are:

1) Substandard: Repayment is stopped or irregular but there has reasonable prospect of improvement. The substandard amount is about 24 crore in year 2012. The companies are Ramisha Import & Export Ltd. And so on. Time limit of substandard is 4 to 6 months.

2) Doubtful debt: Unlikely to be repaid but there is special collection efforts that may result in partial recovery. The doubtful amount of AIBL is about 19 crore in year 2012. The companies are Spread Printing And Packaging, T&A Technology, Delta Printing And Packaging and Chemitan Trading House. Time limit of doubtful debt is

6 to 9 months.

3) Bad/Loss: There is very little chance of recovery. That is also known as classified. Classified amount of AIBL is about 9 crore according to year 2012. The companies that are under classified are Bestec Construction, Bestec Corporation, Ramisha Enterprise and Momo Enterprise. Time limit of bad/ loss is over 10 months.

Categories of Loan

All types of loan will be grouped into four categories. They are: Continuous Loan: AIBL provide this loan for one year. Any time of the investor can take his/ her loan amount. Under continuous loan there are: Bai-Muajjal (general), Bai-Muajjal (against work order), Bai-Muajjal Real Easte (short term) and Quard Against TDR.

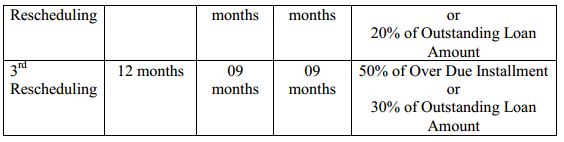

Next Maximum Months From Rescheduling Date:

Demand Loan: According to the demand of the client AIBL provide this loan. Under demand loan there are: Marabaha (post import), Trust receipt, Quard Against Inland Bills (QIB), Foreign Bills Purchased (FBP) and Bai Istisna. Next Maximum Months From Rescheduling Date:

Fixed Term Loan: Under fixed loan there are: Bai-Muajjal CIS (staff), BaiMuajjal (general), Hire Purchase (SHBS), Hire Purchase Real Easte (short term), H.P.S.M short term (general), H.P.S.M short term(transport), H.P.S.M Machinery (short term), H.P.S.M Machinery (long term), H.P.S.M Real Easte (long term).

Next Maximum Months from Rescheduling Date:

Non-performing Loan

In short non-performing loan is called NPL. A sum of borrowed money debtor has missed his/her schedule payment for at least 90 days or 3 months is called non-performing loan. Many loans become non-performing after being in default for 90 days, but this can depend on the contract terms and condition between client and bank. A non-performing loan is either default or close to being in default. If debtor start to pay his/her loan then it is not under nonperforming loan.

A loan is non-performing when payments of interest and principal are past due by 90 days or more, or at least 90 days or 3 months of interest payments have been capitalized, refinanced or delayed by agreement, or payments are less than 90 days or 3 months overdue. In other words, a loan is usually considered to be non-performing after it has been in default for three consecutive months

Non-performing loan is no longer producing income for the bank. Bank holds nonperforming loans in their portfolio. They choose right buyer to sell them to other investors in order to get rid of risky assets and clean up their balance sheet. Bank must be careful to sale of non-performing loan because they can have numerous financial implications, including affecting the company’s profit and loss and tax situation.Al-Arafal Islami Bank Limited Consider NPL ratio, a smaller NPL ratio indicate smaller loss for the bank. If it is larger NPL ratio mean larger losses for the bank as it writes off bad loan. Some banks are interested to invest money in higher risk sector. They want to get more profit by disbursing high-quantity of loan and charging borrower higher interest rate. Higher risks takers earn more profit. However, the large numbers of NPL have large number of side effects.

Reasons for Non-Performing Loan

Intentionally: One who intentionally do not repay the loan. As it is known to all they take this money for business purpose or buying-selling. But they do not do that. Instead he/she has intention to lout a big amount of money from the bank. Mutual understanding with higher management: One takes loan from bank with the help of higher level officer. They divide loan money between them. Instead they have intention to lout a big amount of money from the bank. For example, Hallmark case with Sonali Bank.

Economy Fall of the Country:

Exchange rate fall: If dollar rate is increasing and taka rate is decreasing. That may cause economy fall of the country. Political unrest: Because of political restrain economy fall of our country for example, Hortal hamper production, that’s why company are not able to shipment their product in time. As a result they don’t earn as much as they assume.

Lack of raw material: It is related with the political restrain. Political restrain cause obstacles in communication. That’s why raw material doesn’t reach timely according to the need of manufacturer. From the above reasons, economy falls of the country.

Market down: One who take loan for any specific goods. But that goods market is down. Customers are not interested to buy those goods. Client is not able to earn that much money as they assume. Client who takes from the bank he is not able to repay his loan timely.

Natural Calamities: Sometimes natural calamities also cause loan to default. One takes loan from bank. Because of natural calamities he/she is not able to supply his/her goods to the client in time. Same product in market: Now there is more than one company who produce same product. As a result debtor who takes loan from bank, he/she is not able to get success by that product.

Effect of NPL

There are some effects of NPL that are given below:

There is a negative relationship between non-performing loan and performing loan. If there is increase of non-performing loan that hamper the performing loan. Non-performing loan cause efficient problem on banking sector. If non-performing loan increase that discourage bank’s management to invest money. They lend less money than

demand. Non-performing loan stopped money cycling. After one party return money, bank management can lend money to the other party. If that party is failure to return money bank is not able to lend it another. Slow flowing of cash always has negative impact on any business.

Non-performing loan cause earning reduction for the bank. If lender is not able to repay money that hamper bank’s earnings. Interest earning gets stopped. But cost of fund and cost of management are not stopped. The existing lending price has to be increased to run the management cost along with cost of fund. Suddenly increased rate of interest makes hard the return bank money for a performing borrower.

If non-performing loan is increasing that also cause capital erosion. Capital erosion also hampers economic growth. As a result of poor economic condition. Non-performing loan affects opening of LC. International importers always healthy condition of the exporter’s bank. If bank’s health condition is worse that affects the opening of new LCs. Low rate of LCs makes low bank earning.

NPL creates the credit crunch situation. Credit crunch is a phenomenon that banks ration loan disbursement and new credit commitment that add more risk. Credit crunch also increase the rate of NPL. As we know bank’s work is to take money from one and give it to another. That person who take loan from bank he is not able to repay it. After a certain period bank have to pay money that keep in bank. Because of NPL it affects bank’s re-balancing action.

Management of Non-performing Loan

Early Alert System

An early alert account is one that has risks or potential weakness of a material nature requiring monitoring supervision or close attention by management. If the weaknesses are left uncorrected, they may result deterioration if the repayment prospects for the investment accounts at some future with prospect of being downgraded to IRG-file. Investment monitoring department will identify the weaknesses of the investment accounts, report promptly to the IRM, and take proactive corrective measures immediately on a continuous basis. Monitoring department will prepare an early alert statement within 7 days of identification of investment account and issue to concern branches and to the IRM.

IRG cell will update the IRG grade as soon as possible and no delay should be taken to refer the problem accounts to IRM. The relationship management will contact regularly to the customers for developing account status.

Monitoring department will identify the investment accounts which are going to be classified within next 30 days report to the IRM and managing direction for the prompt action. Monitoring department shall closely monitor early alert identified accounts and contact regularly and the investment clients so that the accounts can be regularized.

Non-Performing Account Management

Management of non-performing accounts will be assigned to recovery unit who will be responsible for coordinating and administering action plan for recovery of NPL account. Recovery management to serve as the primary customer contact after the investment account is downgraded. The IRM will assist recovery management to implement the appropriate strategies.

Transfer of Non-Performing Account to recovery department

An investment account downgraded as sub-standard will be transferred to the Recovery Management/ Recovery Management from the Monitoring Department along with a request for action (RFA) in format and a handover/downgrade checklist. The recovery department / recovery unit will review all documents, meet the customer and prepare a review report within 15 days of transfer.

The initial review report should include documentation issues; investment structuring weakness, proposed workout strategy, security issues as per Instruction Circular no.INV/130 dated 08022005 regarding Eligible Securities and should seek approval for provisioning that is necessary. The recovery unit should ensure that the following is carried out when an account as sub standard or worse.

a) Facilities are withdrawn or repayment is demanded as appropriate. Any drawings or advances should be restricted and only approved after careful scrutiny and approval from appropriate executives within IRM.

b) CIB reporting is updated according to Bangladesh Bank guideline and the Investment Client’s Risk Grade is changed as appropriate.

c) Loan loss provisions are taken based on Force Sale Value (FSV).

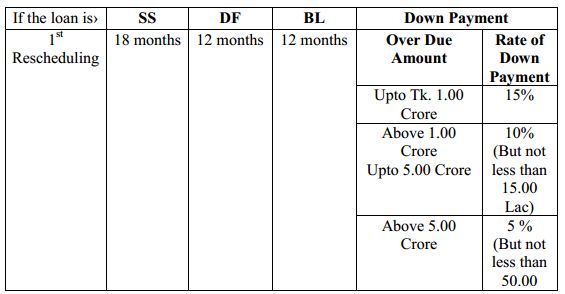

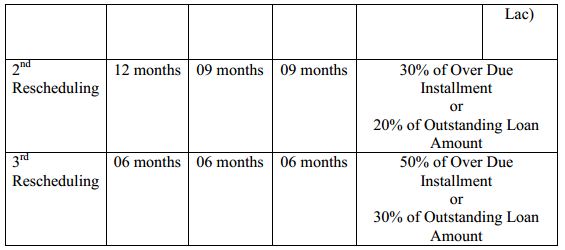

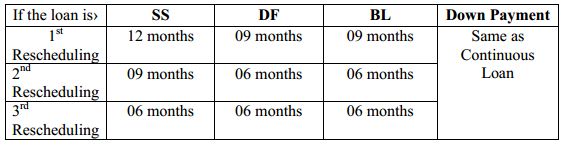

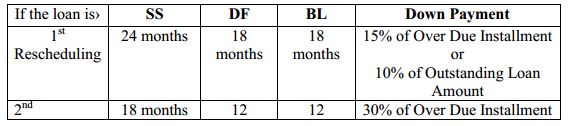

d) Loans are rescheduled in conjunction with the Large Loan Rescheduling guideline of Bangladesh Bank. Any rescheduling should be based on projected future cash flows and should be strictly monitored.

e) Prompt legal action is taken if the client is uncooperative. The recovery department / unit will prepare a quarterly review report to update the status of the action / recovery plan review and access the adequacy of provisions and modify the bank’s strategy as appropriate.

Non performing Investment Provisioning policy

Bangladesh Bank issued BRPD Circular No. 05 on June 2005 under the caption “Master Circular-Loan Classification and Provision” with detail guideline for provisioning against classification investment. The circular is enclosed in annexure-16.

AIBL follow the Bangladesh Bank’s master circular and its subsequent amendments in provisioning against classified investment. Investment recovery department will ensure the implementation of investment write off policy.

Non-performing write off policy Bangladesh Bank issued BRPD Circular No. 02 on January 13, 2003 under the caption “Loan Write off Policy” with detail guideline for classification. Bank will follow the Bangladesh Bank’s circular and its subsequent amendments in write off classified investment. Investment recovery department will ensure the implementation of investment write off policy.

Rescheduling Of Non-Performing Investment

Bangladesh Bank issued BRPD Circular No 01 on January 13, 2003 under the caption “Loan Rescheduling Policy” with detain guideline for rescheduling of classified investment. The circular is enclosed in annexure-18.

Bank will follow the Bangladesh Bank’s circular and its subsequent amendments in rescheduling of classified investment. Investment recovery department will ensure the implementation of investment write off policy.

Recommendation

Al-Arafah Islami Bank Limited has lacking of branches all over the Bangladesh. For this reasons, customers have to visit long distance to continue their bank activities. They can open more branches that can attract more customers. As we know ATM card is the modern innovation in banking industry. ATM helps to get money as soon as possible. Recently they opened only 8 ATM booths in Dkaha. That is not sufficient.

- AIBL should concentrate on ATM card.

- AIBL should concentrate in increasing its profit earning capacity.

- Bank should provide more foreign exchange and other sort of facilities to new customers, new entrepreneurs, new businessmen or new companies.

- Bank should increase their office space and take more care in interior decoration.

- Al-Arafah Islami Bank should promote introduce its Unique Selling Proposition, the Islamic Visa Card service in order to obtain better customer response.

- AIBL should give more emphasize on their marketing effort and try to their sales force.

- AIBL should try to attend different type of target customers.

- Bank should introduce training courses for their employee in order to develop human resource according to the Islami Bank Training & Research Academy.

- AIBL should carry out more promotional activities to make aware about their offers.

- AIBL is absent in TV, print media, bill boards and sponsorships. The bank should advertise about itself and its offers so that it can attract more customers that will increase the business volume of the bank.

Conclusion

The management of Al-Arafah Islami Bank Limited is quite confident that, with their competitive market strategy, high standard of customer service and loyal employees, they shall continue to successfully grow and increase their business and profit. Al-Arafah Islami Bank Limited continues to accelerate its business growth through existing and new relationships. Its business units will function within the confines of policies and procedures which are consistent with its underlying values and principals as a leading banking institution. Al-Arafah Islami Bank Limited is a premier banking institution of the country. It integrates the latest technology into every facet of its operations. But recently there have been a problem with their online banking functions. The online banking system of Al-Arafah Islami Bank Limited is being upgraded into a world class system. But the temporary loss of the online function is hampering its image. Even then the development of the bank is going on according to its goal.

One thing that I come to know from the employee in Gulshan Branch there was no nonperforming loan till 2012. That means its creditor is so smart they can repay their loan. As it has less the amount of loan losses, the more the income will be from credit operations. The more the income from credit operation the more will be the profit of the Al-Arafah Islami Bank Limited. The Bangladeshi banking market is a highly competitive market. In our country the banking sector is growing up very rapidly. So every bank faces this stiff competitive situation. In this competitive market, Al-Arafah Islami Bank Limited has done better to earn quite a good amount of profit in the banking sector.