Introduction:

Generally by the word “Bank” we can easily understand that the financial institution deals with money. But there are different types of bank like; Central Banks, Commercial Banks, Savings Banks, Investment Banks, Industrial Banks, Co-operative Banks, etc. But when use the name term “Bank” without any prefix, or qualification it refers to the Commercial banks. Commercial Banks are the primary contributor to the economy of a country. So we can say Commercial Banks are a profit making institution that holds the deposit of the individuals & business in checking & saving account and than uses these funds to make loans. For these, people and government are very much dependent on these banks as the financial intermediary. As banks are profit earning concern; they collect deposit at the lowest possible cost and provide loans and advanced a higher cost. The differences between two are the profit for the bank.

Banking sector is expanding its hand in different events every day. At the same time the banking process is becoming faster, easier, and the banking area becoming wider. As the demand for better service increases day by day, they are coming with different innovative ideas and products. In order to survive in the competitive field of the banking sector, all banking organization are looking for better service opportunity to provide their fellow clients. As a result, it has become essential for every person to have some idea on the bank and banking procedure.

Mercantile Bank Ltd is involved in both form of transactions of inflow and outflow of remittances through official channel. Mercantile Bank Ltd started its remittance business in Bangladesh since December, 1996, from the very beginning of its operation. These transactions are held through the maintenance of ‘Nostro Account’ with group banks and other foreign banks. These transactions are usually processed through the issuance of TT (Telegraphic Transfer), DD (Demand Draft), and CO (Cashier’s Order). Mercantile Bank Ltd Bangladesh is making significant remittance business with inward remittance service. In the recent financial year 2006-07, remittance collected by Mercantile Bank Ltd was worth of US Dollars 96,930,340.02, which was about 2.51% of the total remittance inflow in Bangladesh.

Background of the Study :

The internship program which is necessary to complete the BBA program exercise a significant importance as it enables a student to familiar with the practical business activities. The student work closing with the people of an organization and learn about the function of that organization. This program enables a student to develop his analytical skills and scholastics attitude.

Rationale of the Study:

With the growing competition among nationalized, foreign and private commercial banks as to how the banks operates it banking operation and how customer service can be made attractive. Commercial or private banks are trying to evaluate their traditional banking service to a better standard, to meet the challenging needs. So they pay attention on better performance and existence. Under the above circumstances, it has become necessary for Mercantile Bank Limited, one of the private commercial banks, to focus its attention towards the improvement, who are actually executing the policies undertaken by the top management will have a chance to communicate their feelings and will have the feedback about their dealings from the customer.

The present study will help Mercantile Bank Ltd to better understand their level of performance in generating inflow of remittances.

This proposed study will also help Mercantile Bank Ltd to compare their current remittance status with the aggregate remittance inflow in Bangladesh. Comparing with the proportion the bank can take necessary actions to perform the remittance business more efficiently and effectively.

From the perspective point of view, the importance and role of remittances as a major proportion of GDP, export, import and utilization of remittances as savings, investment and consumption can be better understood from this proposed study.

This study will encourage further study in the area of identifying effect of foreign remittance inflow on Bangladesh economy and will provide useful guidelines for similar types of researches.

Objective of the Report:

This reposting study will aim at focusing on General Banking services and their performance analysis in Bangladesh. In addition to this a comparative observations would be made with other commercial banking operation. The objectives are:

- To draw a clear scenario of General Banking activities.

- To analyze the performance of Mercantile Bank Ltd regarding customer care.

- To know about the modes of attracting more customers of Mercantile Bank Ltd.

- To focus on products, services and financial condition of Mercantile Bank Ltd.

- To expose strengths and weakness of Mercantile Bank Ltd in comparison with competitors.

METHODOLOGY OF THE STUDY:

In order to make the report more meaningful and presentable, two sources of data and information will be used widely.

Sources of Data /Information :

Primary sources:

- Practical work exposures regarding the customers/ users of different services of Mercantile Bank Limited.

- Responses from the sample through questionnaire.

- Observing procedures of different banking services.

Secondary sources:

- Annual Reports of Mercantile Bank Limited.

- Periodicals published by Bangladesh Bank.

- Various books, articles, compilations etc.

- Different brushier of the bank.

Scope of the Study/Report:

As I was sent to the Mercantile Bank, Main Branch, the scope of the study is only limited to this Branch. The report covers the topic on “General Banking Practices of Mercantile Bank Limited”, To conduct a study on what is Banking concept I have gathered valuable information from Dhaka International University & Mercantile Bank Limited. I have also got some information from web site.

Origin of the Report:

To complete a BBA degree it is necessary to perform an internship program under any reputed organization. This program actually makes a relationship between theoretical and practical knowledge. As a part of the requirement of the BBA Program of the Faculty of Business Administration of Dhaka International University “General Banking Practices of Mercantile Bank Limited”.

Limitations:

I had to face different problems while preparing this internship report. At the same time I tried to make an adjustment with those problems.

Those problems are as follows;

It was very difficult to collect the information from various personnel for the job constrain.

Bank policy was not disclosing some data and information for various reasons.

The department people always remain busy due to lack of supporting employees so they could not dedicate their full efforts

Because of the limitation of information some assumption was made. So there may be some personal mistake in this report.

The time 3 months are not sufficient to know all activities of the branch to prepare the report.

I had no opportunity to verify the satisfaction level of clients and receive their suggestions in banking activities.

Unavailability of statistical data on inward and outward remittance through informal channels can be considered as a major limitation.

The study has drawn from the perspective of Bangladesh. The global issues are not considered in this study.

Comparatively few researches have been conducted in Bangladesh in the field of foreign remittance. Therefore, some previous studies that were carried out in a different environment are reviewed in the study. As a result, the findings from those studies may not fit all the time with Bangladesh scenario.

Remittance is associated with other international, political, foreign policy and other related factors which are not considered because of the simplicity of the proposed study.

AN Overview of the Mercantile Bank Limited:

AN OVERVIEW OF BANKING SYSTEM:

Whoever, being an individual firm, company or corporation generally deals in the business of money and credit is called bank. In our country, any institution, which accepts, for the purpose of lending or investment deposits of money from public, repayable on demand or otherwise, and with transferable by checks draft order and otherwise can be termed as a bank.

The purpose of banking is to ensure transfer of money from surplus unit to deficit units. Banks in all countries work as the repository of money. The owners look for safety and amount of interest for their deposits with Banks. Entrepreneurs try to obtain money from the banks as working capital and for long-term investment. These entrepreneurs welcome effective and forward-looking advice for investment. Banking sector thus owe a great to the deposit holders on the hand and the entrepreneurs on the other. They are expected to play the role of friend, philosopher, and guide for the deposit holders and the entrepreneurs.

Since liberation, Bangladesh passed through fragile phases of development in the banking sector. The nationalization of banks in the post liberation period was intended to safe the institutions and the interest of the depositors. Those handling the banking sector have borne the burden of putting banks on reliable footings. Despite all that was done, some elements of irregularities appeared. With the assertion of the role of the Central bank, The Bangladesh bank started adopting measures for putting banking institutions on right track.

The opening of PRIVATE and FOREIGN participants to the banking sector was intended to obtain desirable results from banking. The authorization of private banks was designed to create competition among the banks and competition in the form of efficiency with and the productivity in enterprises funded by banks. Unfortunately, for the people, at large banking sector is yet to obtain the credit for efficiency, credibility, and growth.

The clever, among the user of banking services, have influenced the management of banks, for obtaining short-term and long-term loans. They sometimes showed inflated to get money for investment in business and industry. Few diverted their loan money to purposes different from the loan proposals, and invested in non-profitable units have failed to repay their loans to the banks. For this reason new entrepreneurs are not getting capital while defaulting entrepreneurs have started obtaining either relief in the form of rescheduling of the repayment program or additional inevitable money for diversified units.

Domestic banks can be divided into four main groups: Nationalized Commercial Banks (NCBs); Private banks established in the early 1980s; and private banks established in 1999:

Nationalized Commercial Banks (NCBs) In general terms; NCBs are large, operationally inefficient and technically insolvent. They are used as vehicles of government directed lending. These banks enjoy an enormous and stable customer deposit base, which provides a cheap source of funding. In addition, most large government related business is routed through these banks;

Private Banks, 1980s- set up to service the sectors not being addressed by the larger NCBs. Not subject to state directed lending but have generally suffered from related lending to directors and their extended families;

Private banks, 1995 – six new licenses were granted. These are the better managed banks with strong capital base and good asset quality and under a much improved regulatory regime. All the banks clustered in this group have successfully raised capital from secondary market and all the shares are now traded in the stock exchange at premium.

New private sector banks. Ten new banks have been granted licenses over the year 1999. While some bankers complain that the country is over-banked, the more commonly held view, including that of the World Bank, is that there is adequate scope for these banks to survive given currently untapped gaps in the market, fat in existing interest margins (currently circa 5%), and efficiency/ service level disparities. It is estimated that up to 70% of the Bangladeshi economy remains un-banked. While this appears to imply that the newer banks may move downstream in terms of asset quality but in reality the last two sets of new banks are successfully competing with NCBs and Foreign banks on the top end market segment.

Long-term interest rates have traditionally been lower than short-term rates. This inverted yield curve is a fall out from the source of long term lending. Long term lending was traditionally extended by the NCB’s, usually for non-commercial loans, thus setting a low benchmark for longer-term funds.

Clearly the banking industry is in a very poor state and it will take years to clean up. The Government and BB have been working with the World Bank to introduce reforms, including related party lending, restricting lending concentrations to 15% of the capital base, capital adequacy and bankruptcy laws. The World Bank has indicated that there are funds available to assist individual banks improve their capital bases, but this depends on them first making full provision for NPLs. Some banks have also successfully raised capital through IPOs. BB has reaffirmed its intention to continue extension of support to banks through rediscounting. However care should be exercised when taking comfort from BB’s assertion that it will not allow any bank to fail. While this pledge has held true to date, in effect it means that BB will allow a technically insolvent bank to continue in operation with BB guidance and “technical” support but BB will not provide a capital injection or write-off government related bad loans.

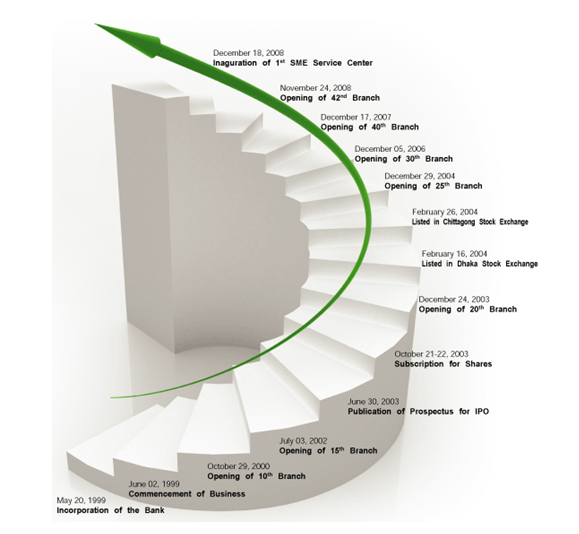

Mercantile Bank Limited emerged as a new commercial bank to provide efficient banking services and to contribute socio-economic development of the country. The Bank commenced its operation on June 2, 1999.

The Authorized Capital of the Bank is Tk. 3000 million and the Paid -up Capital is Tk. 1199.12 million.

The Bank provides a broad range of financial services to its customers and corporate clients. The Board of Directors consists of eminent personalities from the realm of commerce and industries of the country.

The Bank is manned and managed by qualified and efficient professionals. The name of the honorable chairman is Md. Abdul jalil, Mr. Shah Md. Nurul Alam is the Managing Director and CEO of the bank. He brings with him a wealth of experience of managing private sector banks in the country.

The Bank is not depending only on interest earnings; rather it strives hard to go for fee-based income from non‑fund activities of the bank. This type of business include capital market operations like underwriting, portfolio management, mutual fund management, investors’ account as well as commission‑based business like Letter Of Guarantee, Inland remittance, Foreign remittance etc. These businesses usually do not involve Bank’s fund, but on the contrary, offer immense opportunity and scope to expand bank services to the members of public at large. The head office of the Bank is situated at 61, Dilkusha Commercial Area, Dhaka‑1000.

- Vision:

- Would make finest corporate citizen.

- Mission:

Will become most caring, focused for equitable growth based on diversified development of resources, and nevertheless would remain healthy and gainfully profitable Bank.

- Slogan: Efficiency is our Strength.

- Objectives:

Strategic objectives:

- To achieve positive Economic Value Added (EVA) each year.

- To be market leader in product innovation.

- To be one of the top three Financial Institutions in Bangladesh in terms of cost efficiency.

- To be one of the top five Financial Institutions in Bangladesh in terms of market share in all significant market segments we serve.

- Financial objectives

- To achieve a return on shareholders’ equity of 20% or more, on average.

- Core values:

For the customers: Providing with caring services by being innovative in the development of new banking products and services.

For the shareholders: Maximizing wealth of the Bank.

For the employees: Respecting worth and dignity of individual employees devoting their energies for the progress of the Bank.

For the community: Strengthening the corporate values and taking environment and social risks and reward into account.

New technology: Adopting the state-of-art technology in banking operations.

THE BANKER-CUSTOMER RELATIONSHIP:

The Banker-Customer relationship is essentially a debtor-creditor contractual relationship. This relationship may be divided into two categories

- Legal relationship

- Behavioral relationship

After the contractual relationship is established between the banker and customer, they have to avoid by some implied conditions of the contract as well as practices of the bank.

Some of the conditions and practices are as follows:

- Customer is to use cheque books while demanding payment from his account.

- Customer should keep cheque books in his safe custody.

- Customer must inform the bank on time for any loss of cheque leaf or cheque books.

- Customer while depositing money or presenting cheque, they must do that during business hour of the bank.

- Banker also should give necessary banking advice and help the customer in various banking activities.

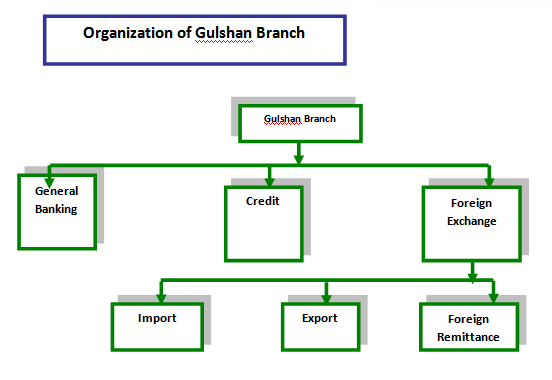

General Banking Practices of Mercantile Bank Ltd

Foreign Exchange- its meaning and definition:

Foreign exchange refers to the process or mechanism by which the currency of one country is converted into the currency of another country. Foreign exchange is the means and methods by which rights to wealth in a country’s currency are converted into rights to wealth in another country’s currency. In banks when we talk of foreign exchange, we refer to the general mechanism by which a bank converts currency of one country into that of another. Foreign Trade gives rise to foreign exchange. Modern banks facilitate trade and commerce by rendering valuable services to the business community. Apart from providing appropriate mechanism for making payments arising out of trade transactions, the banks gear the machinery of commerce, specially in case of international commerce, by acting as a useful link between the buyer and the seller, who are often too far away from and too unfamiliar with each other.

According to Foreign Exchange Regulation Act (FERA) 1947, “Any thing that conveys the right to wealth in another country is foreign exchange. Foreign exchange means and includes all deposits, credits and balances payable in foreign currency as well as foreign currency instruments such as drafts, TCs. Bill of Exchange, promissory Notes and Letters of Credit payable in any foreign currency. “.

This definition implies that all business activities relating to Import, Export, Outward & Inward Remittances, buying & selling of foreign commissions, etc. come under the purview of foreign exchange business.

Foreign exchange department of banks plays significant roles through providing different services for the customers.

- Deposit Section

- Cheque Clearing Section

- Local remittance Section

- Data Entry Section

- Cash Section

- Accounts Section

- Dispatch

General Banking Department:

The General Banking Department does the most important and basic works of the Bank. All other departments are linked with this department. It also plays a vital role in deposit mobilization of the branch. MBL provides different types of accounts, locker facilities and special types of saving scheme under General Banking Department.

General Banking of this branch consists of different sections, namely Account Opening section, Checkbook Issue, Remittance section, Clearing and Bills Section, Accounts section, Cash section.

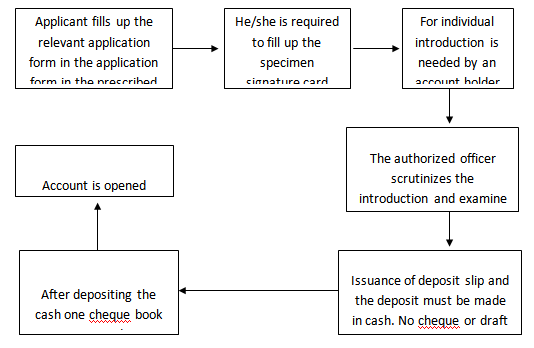

Account Opening Section:

According to the Law and Practice, the Banker-Customer relation arises only from contract between the two. And opening of Account is the contract that establishes the relationship between a banker and a customer. So this section pays a very important role in attracting customer and therefore should be handled with extra care.

According to the International code of conduct, banks should maintain following steps regarding their customers:

- Banks will act fairly and reasonably in all their dealings with their customers,

- Banks will help customers understand how their accounts operate and seek to give them a good understanding of banking service,

- Banks should maintain confidence in the security and integrity of banking and payment system.

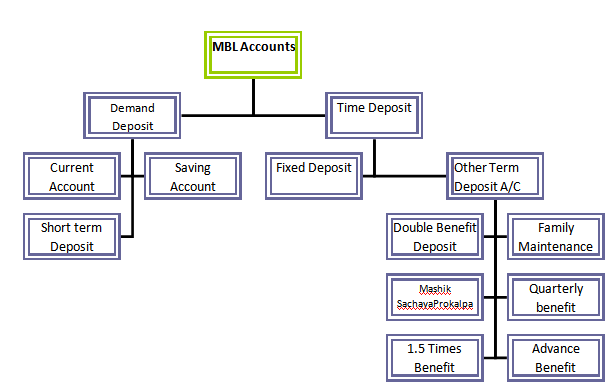

Mercantile Bank Ltd. (MBL) opens the following accounts for its customers –

Current Deposit (CD) Account:

It is purely a demand deposit account. There is not restriction on withdrawing money from this account. As many withdrawals are allowed to the customers, it is suitable when funds are to be collected and money is to be paid away at frequent interval.

Current Account is most suitable for private individuals, traders, merchants, importers and exporters, mill and factory owners, limited company etc.

For opening of a Current Account, minimum deposit of Tk. 1,000/- is required along with introductory reference. No interest is given on the Current Account deposited money.

Journal Entry:

a) When money is deposited in CD account:

Cash A/C or Party A/C———————————Dr.

Current Deposit-Sundry Parties A/C——–Cr.

b) When money is withdrawn from the account:

Current Deposit-Sundry Parties A/C ——————Dr.

Cash A/C or Party A/C————————-Cr.

The Following Points are Important to This Extent:

- A current account is a running and active account, which may be operated upon any number of times during a working day. There is no restriction on the number and the amount of withdrawals from a current account.

- The Banker is under an obligation to repay these deposits on demand, so they are called demand liabilities of a banker.

- The primary objective of current account is to save big customers as businessmen, joint stock companies, public authorities etc. from risk of handling a lot of cash themselves.

- The cost of providing current account facilities is considerable to the Bank since they undertake to make payments and collect the bills, drafts, cheques, for any number of times daily. The Bank therefore do not pay interest on current deposits while on the other hand, some banks charge for incidental charges on such accounts.

- The Bank provides overdraft facilities also in certain cases.

Savings Bank (SB) Account:

This deposit is primarily for small-scale savers. The main objective of this account is to save small savers money. Hence there is restriction on withdrawals in a month. Heavy withdrawals are permitted only against prior notice.

- Minimum amount to Tk. 5,000.00 is required as initial deposit.

- Frequent withdrawal is not encouraged.

- Formally withdrawal not allowed more than ¼ th of the balance.

- 7 days notice is required for withdrawal of large amount.

- The rate of interest is 8% against S.B. Account.

Journal Entry:

a) On receiving money:

Cash A/C ————————————————-Dr.

Savings Deposit-Sundry Parties A/C——–Cr.

b) On withdrawal of money:

Savings Deposit-Sundry Parties A/C——————Dr.

Cash A/C or Party A/C ————————-Cr.

Short Term Deposit (STD) :

Short Term Deposit (STD) Account opening procedure is similar to that to the Savings Account. The rate of interest on this type of account is 6% per annum.

Journal Entry:

a) On receiving money:

Cash A/C—————————————————–Dr.

Short Term Deposit-Sundry Parties A/C ——-Cr.

b) On withdrawal of money:

Short Term Deposit-Sundry Parties A/C—————–Dr.

Cash A/C or Party A/C —————————-Cr.

Fixed Deposit Receipt (FDR) :

Many expert bankers think that Fixed Deposit Receipt (FDR) is not an account. It is merely a deposit receipt. It is popularly known as “Time Deposit”. Because these deposits are not repayable on demand but they are withdrawal subject to a period of notice. The prospective fixed deposit holder is expected to fill up an application form prescribed for the purpose, stating the amount and the period of deposit. The application itself contains rules and regulations of the deposit including the space for specimen signature.

- Payment made on expiry of agreed period.

- Payment demanded before expiry of agreed date then Penalty might be charged.

- Introducer is not needed.

- 2 Copies of Party and 2 copies of Nominees photographs are needed.

- Loan is sanctioned against FDR.

Interest Rate

Rate of Interest varies depending on the period of maturity date.

Duration | Rate of Interest |

1 month | 8.25% |

3 months | 9.00% |

6 months | 9.25% |

12 months | 9.50% |

24 months | 10.00% |

36 months | 10.50% |

Journal Entry:

c) On opening of FDR:

Cash A/C —————————————–Dr.

Fixed Deposit-FDR ——————–Cr.

d) On encashment of FDR:

Fixed Deposit-FDR——————————Dr.

Interest Expense A/C-FDR ———————Dr.

Cash A/C ———————————Cr.

Income tax on interest ——————Cr

Other Term Deposit Accounts :

- Double Benefit Deposit Scheme (DBDS)

- Family Maintenance Deposit (FMD)

- Mashik Sanchaya Prokalpa (MSK) Or Monthly Savings Scheme (MSS)

- Quarterly Benefit Deposit Scheme

- 1.5 Times Benefit Deposit Scheme

- Advance Benefit Deposit Scheme (ABDS) Or Agrim Munafa Amanat Prokolpo (AMAP)

Monthly Savings Scheme (MSS):

Objectives:

- Build up habit of savings.

- Attract small savers.

- Saving for rainy days.

Mode:

- Monthly installments of various sizes.

Benefits:

(Amount in TK.)

| Period | Monthly Installment | |||||

250 | 500 | 1,000 | 1500 | 2500 | 5,000 | |

Benefits | ||||||

5 Years | 20,625 | 41,250 | 82,500 | 1,23,750 | 2,06,250 | 4,12,500 |

8 Years | 40,375 | 80,750 | 1,61,500 | 2,42,250 | 4,03,750 | 8,07,500 |

10 Years | 57,500 | 1,15,000 | 2,30,000 | 3,45,000 | 5,75,000 | 11,50,000 |

Other Features:

- All taxes/duty/levy and /or any other surcharges presently in force or that may be imposed by the Government of Bangladesh (GOB) from time to time will be deducted/ recovered from the deposit account under this scheme.

- In case of premature encashment interest will be paid on Saving A/C Rate.

- Upon deposit of installment for at least 01 year (minimum deposit amount must be BDT 12,000.00) under this scheme, loan may be granted up to maximum 82% of the deposited amount.

- Loan processing fee be realized BDT 50.00 only and stamp costs also be realized.

Documents Needed for Opening Each Account Separately

Current/Saving Deposit Account:

Introduction of the applicant by a current account holder of this branch.

Proprietorship Firm:

- Name of authorized persons, designation, specimen signature card,

- Trade license,

- Passport (if there is no introducer)

Partnership Firm:

- Account must be opened in the name of the firm,

- Three form should describe the names and addresses of all partners,

- Partnership deed is required,

- Trade license from City Corporation is needed,

- Letter of authority is achieved.

Limited Company:

- Certificate of incorporation

- Certificate of Commencement of Business (in case of Public Limited Company only)

- Form XII, (List of all Directors, Designation, Address, Specimen signature)

- Memorandum of Association

- Articles of Association

- Power of attorney

- Resolution of the Board of Directors authorizing opening of an account.

Societies/Clubs/Associations:

Other than above mentioned common documents resolution of who will operate the account must be noted.

Account Opening Procedure in Flow Chart:

Issuing Cheque Book to the Customers :

Issuance of Cheque Book (For New Account):

- When a new account is opened and the customer deposits the minimum required money in the account, the account opening form is sent for issuance of a cheque book.

- Respected officer first draws a cheque book kept under his own disposal. He then sealed it with branch name, MBL’s round seal.

- He enters the number of the cheque book in Cheque Book Issue Register. He also writes down the name of the customer and the account number in the same Register.

- Account number is then write down on the face of the Cheque Book and on every leaf of the cheque book including Requisition Slip.

- The name of the customer is also written down on the face of the Cheque Book and on the Requisition Slip.

- The word “Issued on” along with the date of issuance is written down on the Requisition Slip.

- Number of cheque book and date of issuance is also written on the application form.

- Next, the customer is asked to sign in the Cheque Book Issue Register.

- Then the respected officer signs on the face of the Requisition Slip, put his initial in the register and hand over the cheque to the customer.

Issuance of Cheque Book (For Existing Account):

- All the procedure for issuing a new cheque book for existing account is same as the procedure of new account. Only difference is that customer have to submit the requisition slip of the old cheque book with date, signature and party’s address. Computer posting is then given to the requisition slip to know the position of account and to know how many leaf/leaves still not used. The number of new cheque book is entered on the back of the old requisition slip and is signed by the officer.

- If the cheque book is handed over to any other person then the account holder, an acknowledgement slip is issued by the bank addressing the account holder with details of the cheque book. This acknowledgement slip must be signed by the account holder and returned to the bank. Otherwise the bank will not honor any cheque from this Cheque Book.

- At the end of the day, all the Requisition Slips and application forms are sent to the computer section to give entry to these new cheques.

Transfer of an Account:

- When an account is transferred from one branch to another, the account opening form etc. signed at the time of opening account and any forms or documents signed subsequently which are necessary for its proper conduct at the time of transfer, must be forwarded under cover of form, to the branch to which the account is transferred. Specimen signature card(s) and standing instruction if any must also be transferred. No charge is taken on such transfer.

- The necessary information regarding the character, means and standing of the account holder and must be given to the receiving branch.

Closing of an Account :

A banker can close the account of his/her customer. The stoppage of the operation of the Account can be under following circumstances –

- Notice given by the customer himself

- Death of customer

- Customer’s insanity and insolvency

- Order of the court/Injunction of the court

- Garnishee Order

An application to close the account from customer is received. Signature must be verified by the respective officer. The following activities are the part and parcel of account closing –

- Draw amount from the A/C keeping Tk. 50 for Savings and Tk. 100 for Current A/C as closing charge.

- Cheque book or outstanding cheque leaf (if any) is destroyed.

Remittance Section:

Cash handling from one place to another is risky. So, bank remits funds on behalf of the customers to save them from any mishaps through the network of their branches. MBL has a wide network of branches all over the country and offers various types of remittance facilities to the public. They serve as best media for remittance of funds from one place to another. This service is available to both customers as well as non-customers of the bank. The followings are some of the important modes of transferring funds from one place to another through banks. These are –

i) Payment Order (PO)

ii) Demand Draft (DD)

iii) Telegraphic transfer (TT)

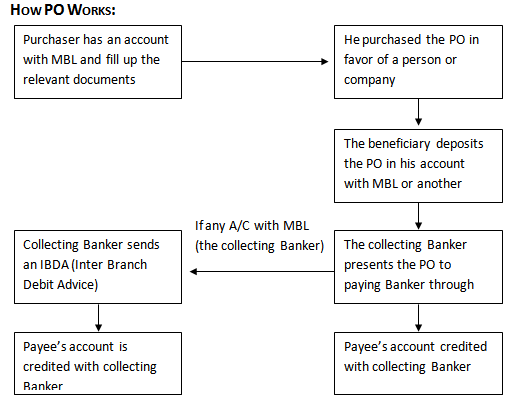

Payment Order/Pay Order (PO):

This is an instrument issued by the branch of a bank for enabling the customer/purchaser to pay certain amount of money to the order of a certain person/firm/organization/ department office within the same clearing house area of the pay order issuing branch. Unlike cheque, there is no possibility of dishonoring pay order because before issuing P.O., bank takes out money of the pay order in advance. P.O. is issued regionally or in the same city. This instrument is generally used in tender, bids, earnest money etc.

Reasons for Issuing PO:

a) Remittance purpose

b) Payment against bill submitted to the Bank.

Procedure for Issuing PO:

a) Customer is supplied with PO form

b) After filling the form, the customer pays the money in cash or by cheque

c) The concerned officer then issues PO on its specific block. This block has three parts; one for bank and other two for the customer. ‘A/C Payee’ crossing is sealed on all Pay Orders issued by the bank

d) The officer then writes down the number of the PO block on the PO form

e) Two authorized officers sign the block.

f) At the end, customer is provided with the two parts of the block after signing on the back of the Bank’s part.

Journal Entry:

a) On Issuing of PO:

- Cash A/C or Party A/C ——————————-Dr.

MBL General A/C—————————–Cr.

Income A/C-Commission on PO ————Cr.

- MBL General A/C————————————-Dr.

Bills Payable A/C-PO ————————-Cr.

b) On Encashment of PO:

Bills Payable A/C————————————-Dr.

Party A/C ————————————-Cr.

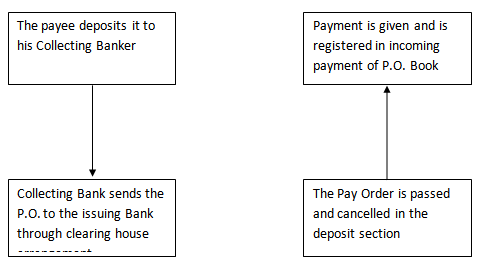

Procedure of Payment of PO:

a) Examine genuinely the pay order

b) Enter into PO register and give contra entry

c) Debit if fund OK for payment.

As the PO issued by the bank is crossed one, it is not paid over the counter. On the contrary, the amount is transferred to the payee’s account. To transfer the amount, payee must duly stamp the PO.

Commission and VAT on PO:

Amount | Commission | VAT | |

| Up to Tk. 10,000 | @ 20% | Tk. 25 | 4 |

| From 10,001 to 100,000 | @ 20% | Tk. 50 | 8 |

| From 100,001 to 500,000 | @ 20% | Tk. 100 | 15 |

| Above Tk. 500,000 | @ 20% | Tk. 150 | 23 |

| Cancellation or Duplicate Issue of Pay Order | Tk. 100 | ||

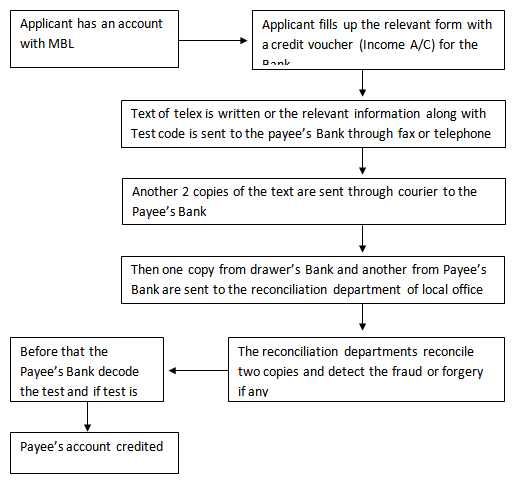

Telegraphic Transfer (TT):

Telegraphic transfer is effected by mobile phone, telegram, telephone, telex or Fax as desired by the remitter. Transfer of funds by telegraph is the most rapid and convenient but expensive method. The drawer and the payee should have account with MBL.

TT is issued against cash, cheque and letter of instruction. All TTs in MBL is sent through mobile phone and Tk. 30 is charged per remittance.

Commission on TT:

Tk. 1.00 is charged in every thousand Taka. (Tk. 1,000)

Procedure of Issuing TT:

- Customer fill up the TT form and pays the amount along with commission in cash or by cheque

- The respective officer issues a cost memo after receiving the TT form with payment seal, then sign it and at last give it to the customer

- Next a TT confirmation slip is issued and its entry is given in the TT issue register

- A test number is also put on the face of the slip. Two authorized officer signs this slip

- The respective officer transfers the message to the drawee branch mentioning the amount, name of the Payee, name of the issuing branch, date test umber and his/her power of attorney (P.A.) number

- The confirmation slip is sent by post

How TT Works (Outward):

Journal Entry:

a) On Issuing of TT:

- Cash / Respective A/C (issuer)———————-Dr.

MBL General A/C —————————-Cr.

Income A/C-Postage ————————–Cr.

Income A/C-Commission on TT————Cr.

- MBL General A/C————————————-Dr.

Bills Payable A/C-TT Payable —————Cr.

b) On Payment of TT:

Bills Payable A/C-TT Payable ——————————–Dr.

Party A/C ———————————————–Cr.

TT Payment:

- When a TT arrives through telex, it is sent to the respected officer for the verification of the test number. If the test number is OK, the officer write down “Test Agreed” on it and sign it. Otherwise a message is sent back to the issuing branch for the correction of the test number.

- After agreeing the test, the branch issues a debit voucher and a credit voucher debiting the issuing branch and crediting the payee’s account. Branch also issues a credit advice slip addressing the payee informing him/her about the arrival of the money.

- Later on, when the confirmation slip arrives the contra date, on which the payment was made, is put on it and the officer signs it.

- The test number on TT is a security measure for the bankers. The computer section of MBL supplies some arbitrary numbers to each branch of the bank. At the time of issuing the TT, the issuing branch codes the numbers and puts the total figure on the TT voucher. This number is known as test number. The test is said to be agreed. MBL uses the numbers as –

One number for issuing branch say———101

One number for responding branch say—-150

One number for the month of issue say —-100

One number for the day of issue say ———50

One number for the amount say ————-600

So the test number of the TT is————-1001

Online Banking:

Online Banking have so far been activated with 37 Branches of the Bank from January 01, 2006. Online service is now available for all customers- both cash deposit and withdrawals, cheque deposits and transfer in CD, SB, STD, Loan accounts. Monthly Saving account will not fall under online transaction service.

Online Banking Hours:

Sunday to Thursday :9.00 am – 3.00 pm

Saturday : 9.00 am – 12.00 pm. (only in open branches on Saturday)

Account wise Online Banking Limit (cash withdrawal, deposit and transfer)

Maximum Deposit Limit: Tk. 500,000 per transaction

Cumulative deposit shall not be more than Tk. 1,000,000 per day.

Maximum Withdrawal Limit : Tk. 300,000 per transaction

Cumulative Withdrawal shall not be more than Tk. 6,000,000 per day.

Charges for Online Banking:

| Intra City* | Inter City** | Mode of realization | |

|

Free | Up to BDT 100000 Up to BDT 200000 Up to BDT 300000 Up to BDT 400000 Up to BDT 500000 | Tk.50 Tk.100 Tk.150 Tk.200 Tk.250 |

Up front Cash |

* Intra City Transaction: Branches under Same City Corporation Areas

** Inter City Transaction: Branches outside City Corporation Areas

***Service charge applicable

Clearing and Bills Section:

In clearing section, cheque, dividend warrant and other forms of financial instruments, which are easy for encashment, are received. The clearing departments send these instruments to the clearing House of the Bangladesh Bank for collection. As soon as cash is received the amount is deposited in the clients account. Collection of cheque, drafts etc. on behalf of its customers is one of the basic functions of commercial bank. Clearing sends for mutual settlement of claims made in between members banks at an agreed time and placed in respect of instruments drawn on each other. Negotiable instrument law provides protection to a banker who collects a cheque or a draft if the banker fulfills the following conditions –

- He collects the instrument for customer.

- The instrument be crossed.

- The acts in good faith and without any negligence.

Dispatch Section:

This section is responsible for receiving the entire letter from outside of the bank and to send the entire letter from the bank. For this purpose, this section keeps two register books. It also receives the entire document and anything addressing the bank.

However, two types of letters are continuously received in his branch, these are –

- Inward (Registered/Unregistered) letters

- Outward (Registered/Unregistered) letters.

At first, recording is required whether it is Inward or Outward Registered/ Unregistered letters. Then letters are disbursed to their respective destination. Inward letters are firstly segmented according to their different sections and after that, an entry is given to the Inward Register book. The chronological number of the register (both Inward & Outward) is known as inward & outward number respectively.

The main objective of this section is –

- Maintaining all records of the documents send to other branches or banks

- Makes best effort to send these documents safely and correctly

- Letters are disbursed to their respective destination

- Receives documents come through different medium, such as postal service, courier service, via messenger etc.

Books Maintained:

- Local Dispatch Khata/Kaccha Register (including Peon Book)

- Register Dispatch Khata (for Registered Letters)

- Ordinary Register Khata/Kaccha Register (for Unregistered letters)

Cash Section:

Mercantile Bank Ltd., Nayabazar Branch has a heavy equipped cash section. This branch uses several moving cameras in cash section to identify the movement of unauthorized person or miscreants. I was not authorized to deal in this section because of its sensitivity. Time factor is also vital for not to deal in this section. But I was fortunate enough to know the procedures of this section. Operation of this section begins at the start of the banking hour. Cash officer begins his/her transaction with taking money from the vault, known as the opening cash balance. Vault is kept in a very secured room. Keys to the room are kept under control of cash officer and branch incumbent. The amount of opening cash balance is entered into a register. After whole days’ transaction, the surplus money remain the cash counter is put back in the vault and known as the closing balance. Money is received and paid in this section.

Cash Receipt:

- At first, the depositor fill up the Deposit in Slip. There are three types of deposit in slip in this branch. One for Savings Account, one for Current Account and another for Term deposit Account.

- After filling the required deposit in slip, depositor deposits the money.

- Officers at the cash counter receives the money, count it, enter the amount of money in the scroll register kept at the counter, seal the deposit in slip and sign on it with date.

- Then this slip is passed to another officer who enter the scroll number given by the cash counter in his/her register along with the amount of the money. Sign the slip and keep the bank’s part of the slip. Other part is given to the depositor.

- All deposits of Savings and Current account are maintained by one officer and other accounts by another officers.

- At the end of the day, entries of both of these registers are cross checked with the register kept at the cash counter to see whether the transactions are correct or not.

Cash Payment:

- When a person comes to the bank to cash a cheque, he/she first gives it to the computer desk to know the position of the cheque and posting of the cheque. If the account has sufficient fund, the computer in charge will post it into the computer, will sign it and seal it.

- This cheque is then sent to the concerned officer. There are two officers who verify the cheques – one for Savings and similar types of account and another for Current and similar types of account.

- After receiving the cheque, respective officer first checks it very carefully for any kind of fraudulent activity. He also checks the date of the cheque, amount in word, amount in figure and signature of the drawer.

- If the instrument is free of all kinds of errors, the respective officer will request the bearer to sign on the back of it.

- He will then put his/her initial beside the bearer’s signature. He will also sign it on its face, will write down the amount by red pen and will put on a scroll register. It is known as passing of cheques.

- Then the cheque will be sent to the cash counter. At the cash counter bearer will be asked again to sign on the back of the instrument.

- The cash officer will then enter the scroll number in his/her register and will pay the money to the bearer.

- At the end of the day, these scroll numbers of the registers will be compared to ensure the correctness of the entries.

MBL, Nayabazar Branch is very much cautious about the payment of instruments. This branch has issued office orders mentioning that if the instruments are not paid as ‘Payment In Due Course’ under section – 10 of the “Negotiable Instrument Act – 1981”, the respective officers will not get legal protection under section – 181 of the said Act.

Data Entry Section:

A strong Computer network system exists here. Total 11 PC are available here and all are connected with LAN. One PC of Foreign Exchange Department is connected with internet for foreign transaction of L/C and others. One is connected with all branches of MBL for online transactions. But a separate section exists in general banking section. Two officer and two computers are available in this section. They perform all type of posting of the day of this branch, make statement for the customer about their financial status and produce various types of statement and supplementary documents for future reservation and verifying purpose.

Accounts Section:

Accounts Section performs the following tasks:-

- Collection of clearing cheques from Clients and send to the main branch to present clearing house for collection without any charge.

- Computer entry of clearing cheque and credit posting.

- Voucher sorting and reconciliation with supplementary summary.

- Voucher arrangement and preparation of voucher cover.

- Preserve daily cash position and trial balance.

- To prepare salary sheet and record all the stationary cost.

- To provide solvency certificates.

- If the supplementary summary and voucher are not same his/her duty to find out the discrepancies. And other works demanded by the authority.

Types of Foreign Trades:

There are mainly three types of transactions which lead to foreign exchange. These are:

a) Import

b) Export

c) Foreign Remittance

Credit Division:

Mercantile Bank Limited is a new generation Bank. It is committed to provide high quality financial service/products to contribute to the growth of GDP of the country through stimulating trade and commerce, accelerating the place of industrialization, boosting up export, creating employment opportunity for the educated youth, poverty alleviation, raising standard of living of limited income group and overall sustainable socio-economic development of the country.

In achieving the aforesaid objectives of the Bank, credit operation of the Bank is of paramount importance as the greatest share of total revenue of the Bank is generated form it, maximum risk is centered in it and even the very existence of Bank depends on prudent management of its credit portfolio. The failure of a commercial Bank is usually associated with the problem in credit portfolio and it’s less often the result of shrinkage in the value of other assets. As such, credit portfolio not only features dominant in the assets structure of the Bank, it is critically importance to the success of the Bank also.

Nature wise loan:

Fundamentals of Credit:

The word is “credit” is derived from the Latin word “credo” meaning “I believe”. The term credit may be defined broadly or narrowly. Speaking broadly, credit is finance made available by on party (lender, seller, or shareholder/owner) to another (borrower, buyer, corporate or non-corporate firm). More generally the term credit is used narrowly for debt finance. Credit is simply opposite of debt. Debt is obligation to make future payment. Credit is the claim to receive the payments. Both are created in the same act of borrowing and lending.

Principal of Advances:

The granting of advances is one of the most important functions of a Bank and the test of Bank strength depends considerably on the quality of its advances and proportion they bear to the total deposit. Although receipt from exchange, commission and Banks charges contribute a fair amount of the profits or commercial Banks, its earning are chiefly derived from interest charged on loans and discount. A wise and prudent policy with regard to advances is therefore considered an important factor inspiring confidence in the depositors and customers of a Bank. Traditionally Banks have been following three cardinal principal of lending they are: Safety, Liquidity and Profitability. Loans and advances may be made either of the borrowers and the latter is called secured advances. Confidence in the borrower is the basis of unsecured advances.

Different Type of Loans and Advances:

As initiated by Bangladesh Bank vide BCD circular no: 33 dated 16/11/89 different kinds of lending were subdivided into 11 categories w.e.f. 01/01/90 which was subsequent reduced to 9 vide BCD circular no: 23 dated 09/10/93 and again to 7 prime sectors vide BCD circular no: 8 dated 25/04/94 for fixation of rates of interest by the individual Banks on competitive basis depending on the cost of funds, prevailing marketing condition and monetary policy of the country. Loans and advances have primarily been divided into two major groups:

Fixed term loan:

There are the advances made by the bank with fixed repayment schedules. The term of loan are defined as follows:

Short term : Up to 12 months

Medium term : more than 12 and up to 36 months

Loan term : More than 36 months

- Continuous Credits:

These are the advances having no fixed repayment schedule, but have an expiry date of which it is renewable on satisfactory performances. Depending on the various nature of financing, all the lending activities have been brought under the following major heads.

- Cash Credit Hypothecation:

A cash credit is an arrangement by which the customer is allowed to borrow money up to a certain limit. This is a permanent arrangement and the customer need not draw the sanctioned amount at once, but draw the amount as and when required. He can back surplus amount, which he may find with him. Thus cash credit is an active and running A/C which deposits and withdrawals may be affected frequently. Interest is charged only for the amount withdrawn and not for the whole amount charged. Cash credit arrangements are usually made adjust pledge or hypothecation of good.

- Overdraft (OD):

Overdraft is an arrangement between a bank and his customer, which the latter is allowed to withdraw over and above his credit balance in the current up to an agree limit. This is only temporary accommodation usually granted against securities. The borrower is permitted to draw and repay any number of times, provided the total amount overdrawn doesn’t exceed limit. The interest is charge for the amount drawn and for the amount sanctioned. A cash credit is used for long term for the businessmen are doing regular business whereas overdraft is made occasionally and for short duration.

- SOD (Other):

Advances allowed against assignment of work order for execution of contractual works falls under this head. The advance is generally allowed for a specific purpose. It is not a continuous loan.

- SOD (General)

Advances allowed to the individuals/firms against the financial obligations i.e. line of F.D.R. or Defense Savings Certificate, ICB unit certificate etc.

- Secured Overdraft (SOD):

It is a continuous advance facility. By this agreement the bankers allowed his customer to overdraft his current A/C up to his credit limits sanctioned by the bank. The interest is charged on the amount, which he withdraws, not on the sectioned amount. MBL sections SOD against different security. Based on different types of security, we can divide the following category of the facility.

- SOD (Export)

- IBP (Inland Bill Purchase):

Payment made through purchase of inland bills/cheques to meet urgent requirement of the customer falls under this type of credit facilities. This temporary advance is adjustable from the proceeds of bills/cheques purchased for collection. It falls under the category ‘commercial lending’.

- Packing Credit (P.C.):

Advance allowed to a customer against specific L/C firm contract for processing/ packing of goods to be exported falls under this head and is categorized as ‘Packing Credit’. The advances must be adjusted form proceeds of the relevant exports within 180 days. It falls under the ‘Export Credit’.

- F.D.B.P. (Foreign Documentary Bill Purchase):

Payment made to a customer through purchase/negotiation of a foreign documentary bill falls under this category. This temporary advance is adjustable from the proceeds of the shipping/export documents. It falls under the category ‘Export Credit’.

- F.D.B.P. (Local):

Payment is made against documents representing sell of goods to local export oriented industries, which are deemed as exports as which are denominated in Local Currency / Foreign Currency falls under this category. This liability is adjustable form proceeds of the bill.

- F.B.P. (Foreign Bill Purchase):

Payment made to a customer through purchase or foreign currency Cheques / Draft falls under this head. This temporary advance is adjustable form the proceeds of the cheque / draft.

- L.D.B.P. (Inland Documentary Bill Purchase):

Payment made to a customer through purchase of inland documentary bills. This temporary liability is adjustable from proceeds of the bill.

Leasing System of the Bank:

- Export Cash Credit:

Financial accommodation allowed to a customer for exports of goods falls under this head and is categorized as “Export Credit”. The advances must be liquidated out of export proceeds within 180 days.

- L.T.R. (Loan Against Trust Receipts):

Advance allowed for retirement of shipping documents and release of goods imported through L / C falls under this head. The goods are handed over to the importer under trust with the arrangement that sale proceeds should be deposited to liquidate the advances within a given period. This is post import finance by MBL

- P.A.D. (Payment Against Documents):

Payment made by the bank against lodgment of shipping documents of goods imported through L / C falls under this head. It is an interim advance connected with import and is generally liquidated against payments usually made by the party for retirement of the documents for release of imported goods from the customs authority. It falls under the category of `Commercial Lending`.

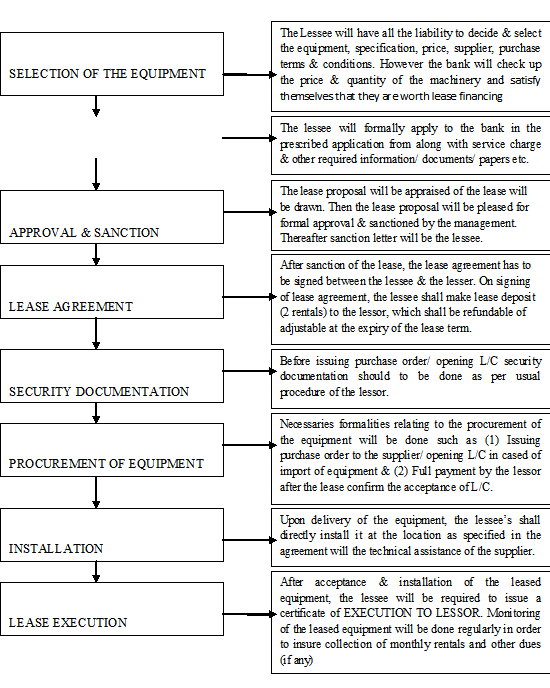

- Credit approval procedure:

After receiving the application from the client, MBL official prepares a credit line proposal (CLP) (Annexure-1, 2, 3) and forwards the same to the Head Office to place before Head Office Credit.

Committee (HOCC) or approval. It includes: –

- Request for credit limit for customer.

- Project profile / profile of business.

- Copy of trade license dully attested.

- Copy of TIN certificate.

- Certificate copy of Memorandum and Article of Association, certificate of incorporation, certificate of commencement of business, Resolution of the Board, Partnership deed. (Where Applicable).

- 03 (Three) years Balance Sheet and Profit and Loss account.

- Personal net worth statement of the owner / directors / partners etc.

- Valuation certificate of the collateral security in banks from with photographs of the security.

- CIB inquiry from dully filled in (for proposal of above ten lac).

- Credit report from another banks.

- Stock report dully verified (Where Applicable).

- Indent / Performa invoice / Quotation.

- Price verification report.

- Statement of accounts.

- Declaration of the name of the sister concern and their liability

- In case of L / C detailed performance of L / C during last year.

- Schedule of mortgage able properties and relevant papers.

- Market reputation.

- Lending risk analysis, LRA (Applicable only for Loan more than Tk. 50 lac).

- Financial spreadsheet analysis.

- Credit scoring.

- Credit report.

Therefore, the steps in lending can be sum up as follows: –

- Entertainment of application for loan proposal.

- Preliminary screening of credit proposal.

- Feasibility study and Appraisal of loan proposal or credit investigation.

- Sanction of loans or advances.

- Documentation.

- Disbursement of loans or advances.

- Supervision and follow up of loans and advances.

Sanction:

When a branch manager writes a letter to the customer accepting all terms and conditions of loan, it is called loan sanction. The conditions, which include in the loan sanction, are given below: –

- Limit of the loan amount.

- Primary securities.

- Collateral securities.

- Rate of interest of the loan.

- Expire date.

- Documentation and,

- Other conditions.

Securities:

To make the loan secured, charging, sufficient security on the credit facilities are very important. The banker cannot afford to make the risk of non-recovery of the money let. MBL charges the following two types of security.

- Primary security: These are the security taken by the ownership of the items for which the bank provides the facility.

- Collateral security: Collateral securities refer to the securities deposited by the third party to secure the advance for the borrower in narrow sense. In wider sense, it denotes any types of security on which the bank has a personal right of action on the respect of the advance.

- Pledge: Pledge is the bailment of the goods as security for payment of a debt or performance of promise. A pledge by in respect of goods including stocks and shares as well as documents of title to goods such as railway receipt, bill of landing, dock warrants etc, duly endorsed in bank’s favor.

- Hypothecation:

In case of hypothecation the possession and the ownership of the goods both rest the borrower. The borrower to the bankers creates an equitable charge on the security. The borrower does this by executing a document known as Agreement of Hypothecation in favor of the lending bank

- Lien:

Lien is the right of the banker to retain, the goods of the borrower until the loan id repaid. The banker’s lien is general lien. A banker can retain all the securities in his possession till and claims against the concern are satisfied.

- Mortgage:

According to section (58) of the transfer of property Act, 1882 mortgage is the “Transfer of an interest in specific immovable property way of loan, existing or future debt or the performance of an engagement which may give rise to a pecuniary liability”. In this case the

Mortgage doesn’t transfer ownership of the specific immovable property to the mortgage, only transfers some of his rights as an owner. The banker exercises the equitable mortgage.

Documentation:

Documentation can be described as the process or technique of obtaining the relevant documents. In spite of the fact that banker lends credit to a borrower after inquiring about the

Character capacity and capital of the borrower, he must obtain proper documents executed from borrower to protect his against willful defaults. Moreover, when money is lent against some security of some assets, the document must be executed in order to give the banker a legal and binding charge against those assets. Documents contain the precise terms of granting loans and they serve as important evidence in the law courts if the circumstances so desire. That’s why all approval procedure and proper documentation shall be completed prior to the disbursement of the facilities. Charge documents as required by the different types of advances are mentioned bellow: –

Loan:

- D.P. notes signed by revenue stamp.

- Letter of agreement

- Letter of disbursement

- Letter of partnership (partnership farm) or Board of resolution (limited companies)

- Letter of lien and ownership / share transfer from (in case of advance against share)

- Letter of hypothecation

- Letter of lien for packing credit

- Letter of lien (in case of advance against FDR)

- Letter of lien and transfer authority (in case of advance against PSP, BSP)

- Legal documents for mortgage of property (as draft by legal adviser)

- Copy of sanction letter mentioning details of terms and conditions duty acknowledges by the borrower

- Trust receipt

- DP Note

- Letter of partnership

- Letter of arrangement

- Letter of continuity

- Letter of lien

- Letter of lien and ownership / share transfer from (in case of advance against share)

- Letter of lien and transfer authority

- Legal documents for mortgage of property

- Letter of hypothecation of bill

- DP Note

- Letter of partnership (partnership farm) or Board of resolution (limited companies)

- Letter of continuity

- Letter of arrangement

- Letter of hypothecation [in case of cash credit (Hypothecation)]

- DP Note

- Letter of partnership (partnership farm) or Board of resolution (limited companies)

- Letter of arrangement

- Letter of acceptance, where it calls for acceptance by the drawee

- Letter of hypothecation of bill

- DP Note

- Letter of arrangement

- Letter of authority

- Letter of installment

- Letter of disbursement

- Letter of guarantee

- Letter of hypothecation

- Legal documents for mortgage of property

Overdrafts

Cash Credit

Bill purchased

Lease Finance

- C.C.S:

- DP Note

- Letter of arrangement

- Letter of authority

- Letter of installment

- Letter of disbursement

- Letter of guarantee

- Letter of hypothecation

- Legal documents for mortgage of property

- DP Note

- Letter of arrangement

- Letter of authority

- Letter of installment

- Letter of disbursement

- Letter of guarantee

- Letter of hypothecation

- Legal documents for mortgage of property

- DP Note

- Letter of continuity

- Letter of authority

- S.S.S

Letter of Guarantee:

Disbursement:

Loan disbursement has to be made after completion documentation and observation of the sanctioning terms against raising equity by sponsor as lay down. Each phase of loan disbursement to be supervised by bank official that the project and the phase of implementation of the project to be effectively supervised and borrower persuaded for completion of project in time. There are main three important factors in the loan disbursement, such as: –

- Completion of documentation

- Verification of stocks

- All-important documentation

Credit Monitoring, Follow-Up and Supervision:

Credit monitoring implies that the checking of the pattern of use of the disbursed fund to ensure whether it is use for the right purpose or not. It includes a reporting system and communication arrangement between the borrower and the lending institution and within departments, appraisal, disbursement, recoveries, follow-up etc.

Recovery:

The commercial bankers of the experience are mounting problem of recovery of advances in our country. Consequently, they should think of listing to what polonaise advised to his son Lacerates in Shakespeare’s Hamlet,” Neither a borrower nor a lender be, loan often losses both itself and friend”. However most of them, presumable, would reject the advice to be utterly in application in a world of trade and commerce where borrowing and lending are the wheels of business, be it a national or international level. While considering the capital of banks in connection with their total assets, banks are usually highly leveraged companies. Advances, i.e. overdrafts, loan cash credits and bill discounting comprise a major part of such assets. And the adequacy or inadequacy of capital depends significantly on the quality of the bank management exemplified by prudent lending decision; systematic control and ultimate recover of advances.

Loan Classification:

Loan classification is a process by which the risk or loss potential associated with the loan a /c’s of a bank on a particular date is identified and quantified to measure accurately the level of reserves to be maintained by the bank to provide for the probable loss a/c those risk loan

1. Unclassified : Repayment is regular

2. Substandard : Repayment is topped or irregular but has reasonable prospect of improvement.

3. Doubtful debt : Unlikely to be repaid but special collection efforts may

result in partial recovery

4. Bad / Loss : Very little chance of recovery

FINDINGS:

Findings:

Mercantile Bank is an authorized dealer branch. Though customer are satisfy there not highly satisfy with there services. All kinds of transaction are occurred here. But they have to face different kinds of problems in this Branch, Like in General Division, Advance Division, Foreign Exchange Division all of three division finding some problems are as below :

- Delay in transaction and over the counter for this reason the customer very finds that there is long queue in the counter. The reason of such queues due to the lack of initiative of the concern officers.

- Absence of modern technology so works delay and it does not compete with other Bank.

- In Foreign remittance previously customer need only nationality certificate. But now change of the rules they need passport and ICDC Number. So sometime people face problem for this new rules.

- Discourteous Behavior by staff and officers very often it is found that customer and a member including branch manager on some occasion are found in heated discussion.

- Lack of Team work is a major problem in general section. It is one of the most important criteria for development of customer service in this branch.

- In Advance Division they face the various problems to recovery the loan installment. The loan installment does not realize in the proper time for that reason this branch may be assign as a problem bank.

- IBP (Inland Bill Purchase) is a risky business it is one of the main business in this branch. There are many IBP party in this branch but there not big party. IBP limit is very small so many times then face some problem. For that reason advance is not increase. Big L/C amount and the bank Purchase the big amount.

- In Gulshan Branch marketing system is very poor to sell their products like-Loan. There are very few schemes are offered by MBL consumer loan is one of them but now it is close.

- Sometimes the valuation of properties are does not calculate properly for that reason customer is sufferer. It does not offer various loan projects than other Bank.

- In Foreign Exchange Division there main problems is lack of manpower for that reason the employee does not complete the job in time.

- In the Foreign Exchange document systems are not moderns so employee wastes their time for looking document for in time.

- Decisions are centralized.

- As an authorized dealer branch, they always need to correspondent with others.

- In credit and foreign exchange section has to proper different types of loans and L/C proposal. But they have only three computers in the whole branch.

- Broad Band line is suitable instead of on line care systems. Lack of on line banking the work is slow.

- In general banking system they follow the traditional banking system. The entire general banking procedure is not fully computerized.

- Lack of verity of services is also a drawback of the general banking area of the Mercantile Bank. The bank provided only some traditional limited services to its clients. As a result the bank is falling behind in competition.

- They are not using Data Base Networking in IT department. So they have to transfer data form branch to branch and branch to Head Office by using floppy disk and it is not a good system.

- In cash of online banking service Mercantile Bank charge is Tk.1000.00 yearly, which is high compare with the other bank.

- According to some clients, opinion introducer is one of the problems to open an account. If a person who is new of the city wants to open account, it is a problem) or him/her to arrange an introducer of SB or CD accounts holder.

- The loans and advance department takes a long time to process a loan because the process of sanctioning loan is done manually.

- Bankers face enormous problem to fill up loan related paper like parties loan application, stock report, Net worth valuation report etc.

- CIB inquiry form does not provide information about new client of the bank.

- CIB report is not readily available from Bangladesh Bank.

- Political influence is one of the major problems in Bangladesh. Due to political intervention, the bank becomes obliged to provide loans in most of the cases, which are rarely recovered. Bank has to face this in convenience situation almost every year.

- There is no central generator. So due to load shading every day employees can’ not work.

- Space shortage is another major problem in Foreign Exchange Department.

- Modem technical equipment such as computer is not sufficient in each department. As a result, the process makes delay and it is also complicated.

- In foreign exchange department it is required to communicate with foreign banks frequently and quickly. To make the process easy modem communication media for example e-mil, Fax and win fax, Internet etc. Should be used. But the bank doesn’t have mass use of this medium of communication.

- In some cases the number of employee engaged in rendering specific services is insufficient.

- Employees are exposed to customer excessively which is an obstacle in systematic and prompt service.

- The location of this branch is main constraint to give its customer proper and full service. There is no easy way to go to the branch. People who want service from this branch don’t feel interest because of location.

The findings of the study suggest that, the trend of the foreign remittance inflow shows a gradual increase in remitting amount through years, which is a major contribution of country’s GDP. In 2003, remittance inflow was 4.2% of GDP. Through exporting manpower from Bangladesh to other countries, the country earns a huge amount of foreign earnings. In the recent financial year (2004-05) the remittance amount stands for US$3,866.63 million. On the other hand, it is of no doubt that the remittance inflow generated by migrants helps to stabilize the foreign currency reserve of the country, which is important for import based country like Bangladesh. Remittances into Bangladesh were equivalent to 29% of merchandise exports and 144% of official reserves in FY-2003. The proportion of the remittances can be used for savings, investments and consumption. In Bangladesh, 4.8% of remittances are used for investment in business and 3.1% is used for savings (Afsar, 2003).

A huge amount of unrecorded remittance inflow transaction occurs through informal channel. In Bangladesh, in the period of 1981-86 the unrecorded remittance was 20% of total remittances (Mahmud, 1989). Remittance contribution of GDP, export and import will be much higher if this unrecorded amount will be added. To motivate migrants to use formal channel, the complexity of remitting process through formal channel need to reduce. On the other hand, government should take necessary steps to encourage remitters, foreign investors and beneficiaries to use formal channel which will generate more revenue, increase foreign currency reservation and even export, import and GDP contribution of the country.

RECOMMENDATIONS CONCLUSION BIBLIGRAPHY:

Recommendations:

Mercantile Bank Limited has been successful in all of its operation since its inception. It has outperformed all its peer and competitor and peer banks in virtually all area of its activities. Still there is scope for improvement for the bank and the any or all of the following could be which Mercantile Bank Limited can implement to better its performance:

- The Bank should as soon as possible install highly automated banking software like Flex cube to add value to its service. This will not only allow faster service but also reduce the wok load.

- The bank should employ an outside company for recovery of its dues because it takes a great amount of time for the bank’s employees to recover stuck up loans.

- The bank can increase its retail credit loan by allowing credit to more customers. This can be possible through relaxation of credit norms like waiver of guarantee from third parties.

- The bank can attract more lease finance customer through reduction of cost of borrowing on the part of the customer. This can be made possible through return of a fraction of the lease deposit taken by the bank at the time of sanction and disbursement. Similarly the bank can return the risk fund realized from retail credit customers in case of timely and smooth adjustment of the loan by the customers. This will provoke customers to repay the loan timely.

- The bank can enhance its asset quality through offering rebate on interest rate and hence provocation of timely repayment by the customers. This will be offered only to regular customers.

- In addition, with the present services they should include more services.

It is badly needed to provide more services to the customer in order to

compete in the market. - As the clients are not in favor of introducer system that currently

present, if possible the rule of introducing to open an account should

be changed. Because many people face in problem to arrange an

introducer in the time of opening accounts. - In advance section to recovery loan and the delay problems. Special monitoring cell should work in the field level.

- The loan sanction process should be easier that the clients can feel convenient to take loan from the bank.

- The valuation of the property should be calculated by the surveyors.

- The Software in General Banking as well as foreign exchange should be upgraded.

- Online Banking should be provided for fast services

- The number of computer is not sufficient, especially every desk need one computer.

- Manpower should be increase in foreign exchange section

- Foreign exchange department should be fully computerized that the

exchange process would be convenient for both the bankers and the

clients. - For selling their products this branch need strong marketing to sell their products.

- Regular Performance Appraisal and assuring promotion/reward depending upon that will resist the employees switching tendency.

- Internal conflict among the employees should be mitigate

- Space shortage is another major problem for decoration Mercantile Bank Limited, Gulshan branch is congested than other private banks. Management should consider this for external marketing.

- For uninterrupted electricity supply a central generator is required. Because due to load shading every day employees can’ not work one to two hours on an average.

- While the whole world is depending on information there is no clear information for customer in Gulshan Branch. So, management should take proper step for it.

- There is no library for improving the quality and efficiency of its employee in the bank.

- The operation manual of the bank is backdated. It should be replaced by a new and finally manual.

- Customer services must be dynamic and prompt. Without prompt service, Bank cannot keep its current account base and that’s why branch should increase quality service.

- To attract new customers and to retain it self in the banking market, the banking market, the bank should be innovative and diversified its product services.

- The Bank should develop credit card system because it has been observed that in near future all the payments will be consisted of only credit card plastic money.

- Ad is the key factor for a business organization to up hold it in the market and for making market share and goodwill in future. That’s why management should give priority on it.

- Bank should always adopt modern technology and facilities to keep itself in business with other banks and to improve the working efficiency of its employees use of ATM brings speed in banking services.

- General ledger posting and customer service should be together.

- At the same time For.Ex, Gen a/c Ledger should be computerized instead of manual posting.

- Online Banking should be provided for fast services.

- For selling their products this branch need strong marketing to sell their products.

- Consumer loan should be continuing.

- If the IBP (Inland Bill Purchase) party open the big L/C amount then bank also purchase the big amount in this situation advance will be increase and the bank does not face any problem.

- For.Ex documents should be modern instead of Manual.

- Decision should be decentralized. Manager should be considering the opinion of the subordinate.

- Manpower should be increase in foreign exchange section.

- All of work should be computerized instead of manual posting because of better services.

Conclusion & Bibliography:

Conclusion: