Department wise Pre-tax profit:

The group comprises five major customer groups. Personal Financial Services provides financial services to individuals, including self employed individuals (but excluding individuals managed by Private Banking). Commercial Banking manages middle and smaller corporate relationships. Corporate, Investment Banking and Markets includes the relationships with large corporate and institutional customers together with the group’s treasury and investment banking operations. Private Banking provides financial services to high net worth individuals, who have complex financial affairs.

| 2003 | 2002 | 2001 | 2000 | |

| Personal Financial Services | 13,976 | 13,582 | 12,773 | 13,658 |

| Commercial Banking | 7,269 | 7,483 | 6,296 | 7,862 |

| Corporate Investment Banking & Markets | 14,022 | 13,414 | 13,874 | 10,965 |

| Private Banking | 24 | 14 | 171 | 553 |

| Other | (494) | (832) | 1,521 | 1,598 |

| Total | 34,797 | 33,661 | 34,635 | 34,636 |

Assets Position:

Total assets increased by HK$280.0 billion, or 15.0 per cent, since 31 December 2002.

Cash and short-term funds increased by HK$36.8 billion, or 11.4 per cent, reflecting the increase in customer deposits in the Bank in Hong Kong.

Long-term investments increased by HK$49.5 billion, or 14.1 per cent, with increases in Hang Seng Bank reflecting the redeployment of funds from interbank placings and as a result of increased customer deposits, and in the Bank in Hong Kong due to deployment of funds in higher yielding debt securities in the low interest rate environment.

Advances to customers increased by HK$93.2 billion, or 12.9 per cent, since December 2002. At constant exchange rates, advances to customers grew by HK$70.0 billion or 9.7 per cent.

Advances in Hong Kong grew by HK$25.6 billion, or 4.8 per cent, since the end of 2002 against a background of continued subdued loan demand and fierce market competition. In the Bank in Hong Kong, advances to customers grew by HK$20.5 billion, or 6.7 per cent during 2003, with increases in lending relating to stock borrowing, other property-related lending and trade finance.

Figure in HK$ million

| 2003 | 2002 | 2001 | 2000 | |

| Cash & Short term Funds | 359,137 | 322,305 | 455,193 | 344,637 |

| Placings with banks maturingafter one month and certificates of deposits | 170,215 | 144,176 | 174,427 | 150,170 |

| Long-term investments | 399,642 | 350,166 | 193,314 | 266,946 |

| Advances to customers | 815,004 | 721,775 | 652,503 | 674,557 |

| Other | 319,449 | 256,624 | 222,629 | 239,087 |

| Total | 2,063,447 | 1,795,046 | 1,698,066 | 1,675,397 |

Current, Savings and Other Deposit Accounts

HSBC is leading the Banking Industry by its excellence. The information given below from the annual report tells that from commencing of their business in Bangladesh (from 1996- till now) there is an appreciable growth in the deposit of HSBC.

| 2003 | 2002 | 2001 | 2000 | |

| Current accounts | 211,749 | 150,749 | 122,638 | 96,965 |

| Savings accounts | 682,412 | 528,231 | 469,554 | 397,910 |

| Total Deposits accounts(Call + Time + Debt Securities) | 775,543 | 794,559 | 785,927 | 900,827 |

Return On Assets (ROA):

Return on assets (ROA) is measured by the ratio of net income and total assets. By the returning assets, if the company’s net income increases the profitable ratios of the company increases. The higher the ROA, the better the company is attaining. But in the years 1999 through 2004, they have maintained a positive ROA, which indicates of good yielding of results. Although the ROA decreased in 2002 and was stable in 2003 , we can say that the managerial efficiency is pretty much satisfactory compared to the banking industry. HSBC is giving continued emphasis on quality assets, which resulted in providing a sound asset base for the bank.

Return On Equity (ROE):

The ROE (net income divided by equity capital) is the most important measurement of banking returns as well as a company’s returns because it is influenced by how well the bank has performed on all other categories and indicates whether a bank can compete for private sources of capital in the economy. The higher the ROE, the better for the company, as they are getting higher amount of net income over the equity. HSBC. has maintained significantly high ROE throughout the years of its operations.

2.10 Comparison with the other Bank regarding Level of Satisfaction

of service

(Customers’ View Point)

Ranking of The Banks

Name of the Banks | Frequency | Percent |

HSBC | 9 | 18% |

SCB | 11 | 22% |

Amex | 6 | 12% |

CA Igricole | 8 | 16% |

Bank Asia | 3 | 6% |

CItibank NA | 4 | 8% |

Nationalized Commercial Banks | 4 | 8% |

Other Private Commercial Banks | 5 | 10% |

Total | 50 | 100 |

Introduction of Credit Administration Department of HSBC:

Bank is committed to provide high quality financial services/products to contribute to the growth of the country through stimulating trade and commerce, accelerating the pace of industrialization, boosting up export, creating employment opportunity for the youth, poverty alleviation, raising standard of living of limited income group and overall sustainable socio-economic development of the country. In achieving the aforesaid objectives of the Bank, Credit Operation of the Bank is of paramount importance as the greatest share of total revenue of the Bank is generated from it, maximum risk is centered in it and even the very existence of Bank depends on prudent management of its credit portfolio. The failure of a commercial Bank is usually associated with the problem in credit portfolio and its less often the result of shrinkage in the value of other assets. As such, credit portfolio not only features dominant in the assets structure of the Bank, it is crucially importance to the success of the Bank also.

Products and Services of Credit Administration Department of HSBC:

When you choose a bank to help support your business you want to be sure that it can tailor solutions to meet your specific finance needs. At HSBC, we have a full range of products and services, which include:

Overdraft :

A convenient and flexible form of short-term financing for routine operating expenses and overheads of your company.

Import and Export Loans :

Loans against import are available to you when you purchase under Documentary Credit or Documentary Collections terms.

Pre-shipment Finance:

Pre-shipment finance is available to you to meet your working capital requirements. Advances are granted upon production of a buyer’s contract or export DC.

DP/DA Purchase :

A cash advance made to you when you have exported goods to a buyer through Documentary Collections, either on a Documents against Acceptance (DA) or Documents against Payments (DP) basis.

Long term Loans :

We can customise a Term Loan to finance the fixed assets that your business needs (such as land, new premises, equipment and machinery). It may be a greenfield project or an expansion of an existing plant, that may be financed at competitive floating rate of interest.

Guarantees and Bonds :

HSBC in Bangladesh issues a full range of Performance Guarantees, Advance Payment Guarantees, Financial Guarantees and Bid bonds for supporting the underlying business of our customers.

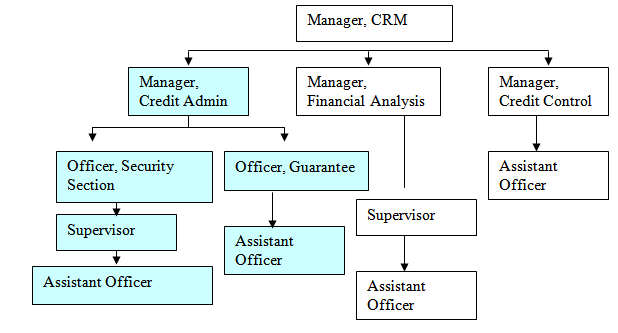

Organ gram of Credit and Risk Management:

Major Job Responsibility of the Department :

Security & Facility Offer Letter (FOL):

- Preparations of Facility Offer Letters

- Processing security documents.

- Preparation and dispatch of security documents.

- Charge creation with Registrar of Joint Stock Companies (RJSC).

- Creation of Legal and Equitable mortgage of Land.

- Coordinate legal matters with lawyers.

- Attending customer queries regarding FOL, securities, Limits and interest related queries.

- Issuance of Bank Certificate.

- Coordinate Search and Inspection Report.

- Responding to auditors of Customers.

- Renewal of Hold covers.

- Cancellation of facilities.

- Circulating Security tracking List to Senior Management on a monthly basis after having RMs comments.

- Update and monitor one off facilities of Trade Services.

Limit & HUB (HSBC Universal Banking):

- Monitoring exception reports and taking necessary action.

- Loan disbursement.

- Loan Rollover.

- Loan Repayment.

- Interest Adjustment.

- Limit / security loading.

- Canceling securities & limits from HUB.

- Updating & Circulating Preferential Pricing.

- Update open insurance policies in HUB.

Workflow of Fulfillment the Responsibilities:

Preparation and Dispatch of Facility Offer Letter:

- Receive approval for CARM (Credit And Risk Management) application through Lotus Notes.

- Review the approval terms of CRM.

- Check whether the facilities are in line with Bangladesh Bank and Banking Companies Act directives.

- Check the CIB (Credit Information Bureau) Report from Bangladesh Bank, Memorandum of Articles & Association and Search report.

- Prepare FOL in standard format as per set up Service Level Agreement (SLA).

- Hand over the draft FOL to the respective RM (Relationship Manager) for checking, amendment and conformation.

- Discuss with RM regarding different issues (Terms & Conditions) of the FOL.

- Finalize the FOL; take two copies of FOL printed on Bank’s Letterhead, take signature form the concerned RM/SRM and the MGR CDT ADM (Manager Credit Administration).

- Mail the FOL long with security papers to the client for their signing.

- Receive the duplicate FOL duly signed by the customer as an indication of the acceptance of the offer.

- Update SLA tracking, security tracking list.

- Review fees will be finalized according to the FOL terms.

Preparation and dispatch of Security Documents :

- Receive approval for CARM application through Lotus Notes.

- Prepare security documents as per CARM and FOL as per SLA.

- Mail the security papers to the client for signing.

- Receive the signed security documents from their customer.

- Update SLA tracking, security tracking list.

Issuance of Bank Certificate:

- Receive request from the customer or from the auditor of the customer for issuance of Bank’s certificate.

- Verify the signature.

- Take HUB printout.

- Prepare the certificate as the standard format.

- Realize charges and VAT.

- Take signature from authorized signatories of the Bank.

- Keep a copy of the certificate in credit file.

Cancellation of Facilities:

- Check the CARM approval for cancellation of facility.

- Send Lotus Notes (L/N) to related departments and RM for “no claim” confirmation.

- Upon recipient confirmation from concern departments, delete securities, limits & pre facility from HUB.

- Prepare Memorandum of Satisfaction for vacation of Charges.

- Advise lawyer for preparing the Deed of Redemption for mortgage.

- Cancel the securities and transfer them to central store.

Loan Disbursement:

- Receive customer’s request letter and verify the signature.

- Check FOL for terms and conditions.

- Check the invoices

- Process the Loan.

- Disburse the loan through A5 Debit /Credit vouchers.

- Send the customer’s advice through courier.

- File the documents after final checking.

Loan Rollover:

- Receive customer’s request letter and verify the signature

- Check FOL for terms and conditions

- Process the Rollover.

- File the documents after final checking in credit file.

Loan Repayment:

- Receive customer’s request letter and verify the signature

- Check FOL for terms and conditions

- Cross the letter with red ink and write “entry passed on ———-(dated)’.

- Process the repayment through A5 debit/credit.

- File the documents after final checking in repayment file.

Limit / Security Loading:

- Check and confirm that all securities are in place.

- In case of pending security, check dispensation in CARM and/or file note.

- Release limits and pre facility.

- Maintenance to be raised and approval to be obtained.

- File the maintenance in limit/security maintenance file.

Clearing Exception:

- Receive telephone call from NSC.

- Respective RM/RO (Relationship Officer) are informed for decision for corporate customers and inform PCM for non-facility customers.

- Obtain decisions from RM /RO/PCM and checked by Senior Manager of Credit Administration (CDT ADM).

- File the exception in clearing exception file.

Preferential Pricing:

- Receive approval copy of the preferential pricing from RM.

- Update HUB.

- Send a copy to HTV (Trade Services) with acknowledgement.

- Update credit and preferential pricing files.

Open Insurance Policies:

- Obtain original open insurance policy from HTV.

- Update HUB.

- Send a copy of the policy to HTV (Trade Services) with acknowledgement.

- As and when exception generates for renewals send a L/N to HTV for renewal.

- Keep the original policy in fireproof cabinet.

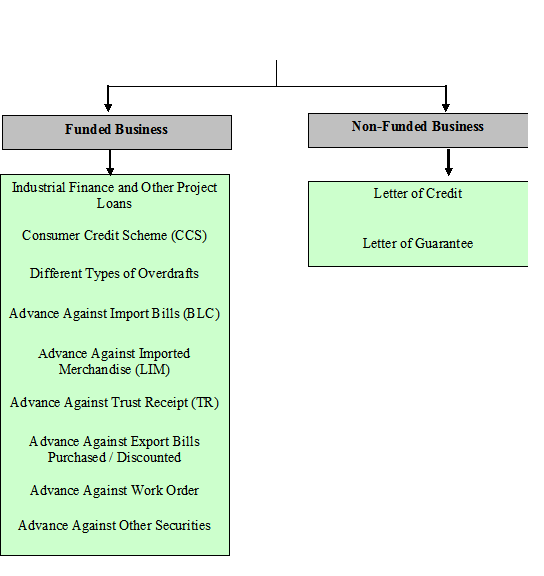

Different Types of Credit Facilities and Policies Practiced in Credit Administration Department of HSBC

DIFFERENT TYPES OF CREDIT FACILITY

|

|

Funded Business :

A funded credit facility that a bank offers to a customer result in actual disbursement of cash to the customer or to any designated supplier of the customer.

A) INDUSTRIAL FINANCE AND OTHER PROJECT LOANS

Project loan normally has fixed maturity and it relates to term investment. As such it requires appraisals of those proposals to have a rational decision. Appraisal may be termed as assessment of viability over a period of time.

These loans are usually made for:

- Setting up of industries and to meet working capital

- Balancing, Modernization, Replacement and Expansion (BMRE) of existing industries.

- Construction of commercial / Residential Building / Warehousing etc.

B) CONSUMER CREDIT SCHEME (CCS)

Objectives

The objective of this loan is to provide essential Household durables to the fixed income group (Service holders) and other eligible borrowers under the scheme. The abbreviated name of the scheme will be “consave”.

Items of Investment:

- Refrigerator / Deep Freeze

- Television / VCR / VCP / Dish Antenna

- MusicCenter

- Motor Car / Motor Cycle

- Air –Cooler / Air – Conditioner

- Personal computer

- Washing Machine

- Household Furniture & Fixtures

- Sewing Machine

- Kitchen appliances like Oven, Toaster, Pressure Cooker, Blender etc.

- Any other item not specified above but considered essential.

Eligibility:

The criteria to become eligible for availing the facility under the scheme are given below. The borrower must be confirmed official of any of the following organizations:

a) Government Organization.

b) Semi-Government Organization / Autonomous body.

c) Multinational Organizations.

d) Banks & Insurance Companies.

e) Reputed Commercial Organizations.

f) Professions.

Entitlement:

i. Eligibility borrower can avail the facility to purchase more than one article but the amount of total loan shall not exceed the maximum limit fixed by Head office from time to time.

Further loan may be allowed to the same borrower if 50% of the previous loan is

recovered from him but the same shall not exceed the maximum limit.

Amount of bank’s investment will be fixed in such a manner that the monthly

deduction from borrower salary / income against payment of bank’s dues shall not normally exceed 50% of his net income. Exceptional cases may be considered if the bank is satisfied about the repayment capacity if the client.

Period of Investment: Maximum three years.

Client’s Equity:

Prescribed margin as fixed by Head Office from time to time on the total value of the articles shall have to be deposited with the bank by the client as equity before disbursement of loan.

Mode of Disbursement:

Client will procure the specified articles from dealer / agent / shops acceptable to bank.

All papers / Cash memos etc. related to the procurement of the goods will be in the name of bank ensuring ownership of the goods. Wherever applicable, the ownership shall be transferred in the of the client after full adjustment of Bank’s dues.

- The client shall have to bear all the expenses of license, Registration, Insurance etc. of the articles wherever necessary. The insurance will be with the Bank mortgage clause. The premiums shall be paid by the borrower by debt to his account.

- The client shall have to bear the cost of Repair & maintenance of the acquired articles.

Mode of Recovery :

Dues shall be recoverable in the following manners:

- In equal monthly installments.

- The monthly installment shall be payable by the 7th of every month, but the first installment shall be payable by the 7th of the subsequent month of disbursement.

Through deduction from the monthly salary of the client wherever applicable, by his employer. In this regard the concerned employee shall authorize irrevocably his employer to deduct the said amount from his monthly salary. The client can only revoke this authority with the concurrence of the bank.

(C) DIFFERENT TYPES OF OVERDRAFTS:

Arranged Overdraft:

In this case the customer is allowed on the basis of prior arrangements overdraw his current account by drawing checks for amounts exceeding the balance upto an agreed limit within certain period of time not exceeding one year. These facilities are granting after the credit standing, financial ability and status of the customer as well as the purpose have been established.

Overdraft against Pledge of Goods / stocks:

Under this arrangement, the credit facility is granted to the borrower against the security of pledge of goods or produce in the form of raw materials or finished products subject to credit /margin restrictions. The borrower signs a letter of pledge and surrenders the physical possession of the goods / produce under banks effective control but retains the ownership with himself. In case of default the bank can sell the goods on serving proper notice to the borrower and adjust the outstanding out of sell proceeds.

Sometimes collateral securities by way of legal or equitable mortgage of immovable properties are also obtained. Overdraft against Hypothecation of goods / stocks /plant & machinery.

Under this method facilities are extended to borrower on his signing a letter of hypothecation, creating a charge against the goods / produce, plant & machinery’s etc. hypothecated for the amount of agreed limit of the debt subject to credit / margin restrictions. The control / possession as well as the ownership of the hypothecated goods/produce etc. is retained by the borrower but binding himself to surrender possession of the goods to the bank as and when called upon to do so. The bank only acquires a right or interest over the goods hypothecated. The bank may ask for collateral securities by way of legal or equitable mortgage of immovable properties and or guarantees where deemed fit.

D) ADVANCE AGAINST IMPORT BILLS (BLC):

Advance against Bills under Letter of Credit are originated from the lodgment of shipping documents received from foreign banks against letter of credit established by the bank.

(E) ADVANCE AGAINST IMPORTED MERCHANDISE (LIM):

Under loan against imported merchandise bank release the imported goods through the nominated clearing agent of the bank. In this case bank holds the possession of the goods. Importer takes delivery of the goods from the bank’s godown against payment. It is one type of forced loan.

(F) ADVANCE AGAINST TRUST RECEIPT (TR):

Advance against Trust Receipt to the client are to release shipping documents for taking delivery of merchandise which is hypothecated to the bank.

(G) ADVANCE AGAINST EXPORT BILLS PURCHASED / DISCOUNTED

Discount:

Banks allow advances to the clients by discounting bill of Exchange / pro. note which matures after a fixed tenor. In this method , the bank calculates and realize the interest at a prefixed rate and credit the amount after deducting the interest from the amount of instrument.

Purchase of bill:

Banks also make advances by purchasing bills, instead of discounting, which are accompanied by documents of title of goods such as bill of lading or railway receipts etc. In this case the bank becomes the purchaser / owner of such bill which are treated as security for the advance. This is allowed primarily relying on the credit worthiness of the client.

H) ADVANCE AGAINST WORK ORDER

Advance can be made to a client perform work order. The following points are to be taken into consideration:

- The client’s management capability, equity strength, nature of the scheduled. Work and feasibility study should be judiciously made to arrive at a logical decision.

- If there is a provision for running bills for the work, appropriate amount to be deducted from each bill to ensure complete adjustment of the liability within the payment period of the final bill.

- Besides assignment bills receivables, addditional collateral security may be insisted upon.

- Disbursement should be made only after completion of documentation formalities and fulfillment of arrangements by the client to undertake the contract.

- The progress of work under contract be reviewed periodically.

Non–Funded Business:

Non funded credit facility to a customer refers to a bank’s commitment to a third party on behalf of the customer. The commitment itself constitutes facility but does not involve cash outflow from the bank. The bank’s commitment essentially states that in the event of occurrence / non occurrence of a particular event , within a particular date , due to a particular reason or reasons , a specific sum of money shall be paid by the bank to the third party upon claim in a particular manner. Though this types of facilities are primarily non funded in nature but at times it may turn into funded facility . As such liabilities against this types of credit facilities are termed as ‘contingent liability’ and do not affect the balance sheet of the bank at the time of commitment but contains the possibility. The non funded facilities are :

1. Letter of Credit:

A banker’s documentary credit is an instrument or letter issued by a bank on behalf of and for the account of the buyer of the merchandise. By this instrument the bank undertakes that the bill(s) of exchange of the beneficiary (the seller of the merchandise) drawn on the buyer , or on the issuing bank , or on another bank designated in the instrument, strictly according to the conditions stipulated in the instrument , will be duly honored by acceptance and /or payment depending upon the issuance of the bill(s) of exchange in question.

A banker’s letter of credit gives the seller or the exporter:

(a) credit security- by eliminating the credit risk in the sale and the shipments of goods

(b) credit facilities- by financing the sale when the goods are in transit ; and

(c) exchange security- by assuring him that the required amount is available to him under credit from the time he receives the buyer’s order and the time of shipment and presentation of shipping documents.

2. Guarantee:

In banking, it is an irrevocable obligation of a bank to pay a certain sum of money in the event of non-performance of a contract by a third party. The basis of guarantee is always a contractual relationship between principal debtor (account holder) and creditor (beneficiary), which is either a contract that has been definitely concluded or a relationship in its pre-contracted as is the case with the tender guarantee. This relationship is referred to as the principal or underlying relationship or contract. The contract of guarantee is independent of this underlying relationship.

PROCESSING OF CREDIT:

8.3 SECURITY FOR LOANS AND ADVANCES:

Security is a Cover against loans and advances. It ensures recovery of loans and advances. Though now-a-days greater emphases are put on the purpose of the loan rather than securities, nevertheless the securities play an extremely important role to take a decision. Security is an insurance or cushion to fall back upon in emergency if borrower fails to repay the loan amount. Importance of charging security is :

- Protection of Interest

- Ensuring the recovery of the money lent

- Provision against unexpected change

- Commitment of the borrower.

Types of Security:

The types of securities offered vary from place to place. In metropolitan cities, it may be Govt. bonds / share / assignment of Book debt / Bills receivable etc. whereas, in the industrial area raw materials & finished goods etc. may be offered as securities. Again agricultural produce is the principal securities in the agricultural centers. Further, a bank also accepts moveable & immovable properties, life insurance policy etc. as securities.

Securities are classified into three broad categories:

COLLATERAL SECURITIES:

The tangible securities pledged / assigned by the borrower to the bank and additionally held by the bank to secure a loan are called Collateral Securities. In case of advances against pledge / hypothecation of goods, bank may insist on immovable properties as collateral.

Good collateral security must have the following characteristics:

- Tangible

- Transferable / negotiable

- Easily marketable

- Price stability

- Durability (not perishable)

- Ascertainability of market value

- Genuineness of title (free from encumbrance)

GUARANTEE:

At times when the personal security of the borrower is not considered sufficient or when the risk involved is a border line case and the borrower is not in a position to offer sufficient collateral to the loan, the bank may ask for a guarantee of a third party whose financial ability and credit standing is acceptable to the bank. A guarantee is an undertaking given to the bank by a third party, called the guarantor to be answerable to the bank for the debt of the borrower upon his default in repayment of the loan. It should be remembered that such security for the loan depends on the continued solvency of the guarantor. To safeguard the bank’s interest a continuing guarantee in the bank’s standard form should be obtained.

MARGIN:

The difference between the market value / asset valued of the goods, merchandise and produces pledged / hypothecated to secure a loan / advances and the amount of the loan / advance (normally the drawing power) is known as MARGIN. The margin to be retained for each type of loan / advances will be in accordance with instructions issued from time to time by Bangladesh bank / Head office of the bank. In case where minimum margin is specified, the percentage may be increased according to market conditions, salability / durability / storage capacity and inspection facility of the goods.

DOCUMENTATION AGAINST ADVANCES :

Document is the written statement of facts or evidence in regard to a particular transaction, which on placement may bind the parties answerable and liable to the court of law.

Importance of Documentation:

Documentation formalities against loans and advances should be properly completed prior to extension of the facility to safeguard the Bank’s interest. Complete and correct documentation enables the Banker to take legal recourse against the borrower in case of non-realization of dues.

Purpose of Documentation:

Documentation is necessary for acknowledgement of debt by the borrower and for charging of securities to the Bank against loans and advances.

Types of Documentation:

Documents related to securing loans and advances are classified into the following 2 (Two) categories:

Charge documents are preformatted and printed required to create charge on securities against loans and advances and the documents are provided by the Bank to the client for execution.

Legal documents are legal papers provided by the client certifying the legal status of the borrower, borrowing power, title to goods and property; legal deeds and power of attorney related to creation of charge on securities.

Charge Documents:

a) Demand Promissory Note:

It is an unconditional written promise of the borrower made to the Bank to repay debt(s) on demand or at a fixed or determinable future date along with interest at a stated rate. The demand promissory note must be obtained while extending any type of credit facilities. It is taken for almost all the facility customers.

b) Letter of hypothecation over stocks, Book Debts, Plant & Machinery:

A ‘hypothecation Agreement’ must be obtained when the collateral is in the name of a person other than the borrower, Bank should ensure the person executing the agreement owns that hypothecated commodities/ goods etc. are solely. If the securities are owned by more than one person all of them must sign the Hypothecation Agreement, even though it may be jointly owned and payable to either or survivor.

The borrowers agree to Hypothecate to the bank goods and merchandise or any other securities in consideration of credit facilities granted to them. They give the Bank the right to sell the securities without notice to them and adjust their outstanding and other expenses from the sale proceeds.

c) Loan Subordination Agreement:

“Letter of Subordination” is an agreement on the part of one party not to collect or enforce an indebtedness of a second party until certain obligations of such second party to a third party (bank) are fully met. In other words, the claim of the third party (Bank) is considered as a primary lien.

d) Power of Attorney:

This document authorities the bank to sign or endorse documents on behalf of the party executing the power. If it is given by a corporate body it must be accompanied by a corresponding copy of a resolution of the board of Directors authorizing the execution.

e)Letter of Continuity& Revival :

In consideration of the bank allowing credit facilities, the borrower agrees to execute all relevant documents and to remain liable for repayment of all outstanding as principal debtor, or as guarantor. The borrower undertakes to remain liable on the promissory note and other loan documentation notwithstanding that his liabilities may have been

fully or partly adjusted during the period of the credit facilities and even though his overdrawn account may show credit balance from time to time.

This letter of Revival refers to and constitutes as an integral part of the loan documentation executed by the borrowers including the promissory notes. The letter is obtained in order to preclude any question of law of limitation.

(f) Letter of Pledge :

When securities are pledge to the bank in consideration of credit facilities extended to the borrowers, these remain in possession of the Bank and can be sold in case of default and the sale proceeds be adjusted towards borrowers liabilities. Other terms and conditions are similar to those under the letter of Hypothecation.

(g) Trust Receipt :

Two different types of trust receipts will be in use to cover the following area of credit lines:

i) Letter of trust receipt (For Release of shipping Documents):

This is executed by the borrowers to release shipping documents for taking delivery

of merchandise which is hypothecated to the bank. The Borrowers agree to take

delivery of merchandise as the Bank’s agents and acknowledges that the ban remains owner of the goods and they will be holding the goods on behalf of the bank, as Trustees until complete repayment of the debts to the bank.

ii) Letter of Trust Receipt (For Pre-shipment Financing):

This is executed by the borrowers for availing pre-shipment finance by creating lien on the original letter of credit. The borrower also undertakes that the credit facilities will be utilized to purchase / process the merchandise for shipment as per terms of the credit.

(h) Supplemental Hypothecation :

This is an integral part of the letter of pledge / Hypothecation / Letter of Trust Receipt /Packaging Credit Trust Receipt / General Letter of Trust Receipt. It describes the securities referred to in the above mentioned documents.

(i) Blanket Counter Indemnity:

In consideration of the bank issuing guarantees / indemnities from time to time, the borrower agrees to keep the bank indemnified from all liabilities, costs and legal actions that may arise from the guarantee.

(j) Pari-passu Security Sharing Agreement:

If the borrower is taking the facilities on a specific business area from the different Banks and other financial institutions, then the question of this agreement arise. Here who will take the first charge or second charge i.e. priority on the property of the borrowers if he fail to repay the loan amount. This agreement is the situational.

Procedures for giving Loans and advances:

The Hongkong and Shanghai Banking Corporation Limited (HSBC), corporate branch (head office) usually follows the below-mentioned procedures and steps for sanctioning any kind of loans and advances as available in line with the Bank’s guidelines:

Personal Analysis :

At the beginning of the process, the bank officials analyze the applicants using their discretions and experiences. Generally, an applicant is analyze on the following grounds:

- Character

- Capital

- Capacity

- Collateral

- Economic Condition

After the satisfaction of the Bank officials, the applicant is asked to submit a formal application for loan.

Application :

In this step the applicant formally applies for credit facility to the Bank. Business Houses apply on the printed company letterhead.

Obtaining Required Documents :

After getting the application, the bank collects following documents from the business houses for preparing a credit proposal. They are:

- Project profile or the profile of business;

- Copy of Trade License duly attested;

- Copy of TIN (Tax Identification number) certificate;

- Copy of Memorandum of Association duly attested by the authorized signatory.

- Copy of Articles of Association duly attested by the authorized signatory;

- Certificate of Incorporation

- Resolutions of Board of Directors;

- Personal Net Worth Statement of the owners in Bank’s format

- Bank Statement for prior 12 months from previous Banks; and so on.

Apart from the above mentioned documents, a export oriented company required to submit the following additional documents :

- Export License

- Bonded warehouse License

- Tax holiday approval from NBR

- EPB Registration

Collection of Credit Information Bureau (CIB) Report :

HSBC’s Credit Administration Department collects information on borrower’s liabilities to different banks from the CIB of Bangladesh Bank. The information is sought by filling up the specific CIB Inquiry Form.

The importance of CIB Report to the Loan provider is :

b) to ensure whether the Borrower’s have a sound economic condition;

c) to ensure that the Borrower’s are not a loan defaulter;

d) to ensure about the repayment condition of the Borrower’s.

Search and Inspection Report :

Bank officials or their representatives makes a visit to the project/factory/godown sight to investigate the existing facilities and relevant securities offered by the Bank. These reports are prepared by the visiting officers and attached with the Credit Proposal which is named in HSBC is CARM.

Lending Risk Analysis :

Lending risk analysis is a systematic procedures for analyzing and quantifying the potential risk of failure to repay the credit facilities. Various risks such as: industry risk, market risk, security risk, company risk have to be evaluated.

Classification of Loans and Provisioning :

Loan classification is a process by which the risk or loss potential associated with the loan accounts of the Bank on a particular date is identified and quantified. It is done to determine the level of reserves to be maintained by the Bank for the probable loss on that risky loan account.

1. Unclassified Loans :

An unclassified loan or commitment is one which is set by Bangladesh Bank or the Head Office of the Bank. Unclassified loans are those loans in which repayment is regular.

2.CLASSIFIED LOANS :

A classified loan or commitment is one which is classified as substandard, Doubtful or Loss as per policy of loan classification set by Bangladesh Bank or Head Office of the bank.

Loan Classification means to categorize the debt information in a systematic manner. But in true sense it is defined in terms of degree of risk associated with these loans. The objectives/importance of loan classification are:

- To find out Net Worth of a bank;

- To assess financial soundness of a bank;

- To calculate the required provision and the amount of interest suspense;

- Strengthen credit discipline;

- To improve loan recovery position and

- To put the bank on sound footing in order to develop sound banking practice in Bangladesh.

Position of classified loans and advances and other assets should be placed before the Board of directors of the bank.

The following are the broad definitions of the classified categories: however instruction issued by Bangladesh bank / Head Office of the bank regarding basis of loan classification and provisioning should be followed:

- Substandard :

A well defined weakness is present in loans f this category, which could affect the ability of the borrower to repay. This is clearly a troubled situation, for one reason or another, that requires immediate and intensive effort to correct and reduce the possibility of loss.

- Doubtful:

A serious doubt must exist that full repayment will not be forthcoming but the exact amount of the loss cannot be ascertained at the time of classification.

- Loss:

Advances, or portions of advances, which are determined to be uncollectible, based on presently known factors.

LEGAL ACTION

Legal proceedings are lengthy and consuming and as such every effort must be made to settle a defaulter’s outstanding out of court. However, if situation compels the bank to

take legal action for recovery of stuck up loans and advances, the same should be done with prior approval of Head office. All legal process should be conducted by the bank’s legal retainer, if necessary in consultation with Bank’s legal adviser.

Provision for Classified Loan :

Bank should preserve following provisions for classified loans:

| Types of Classification | Rate of Provision |

| Unclassified / Regular | 1% |

| Substandard | 20% |

| Doubtful | 50% |

| Bad & Loss | 100% |

Calculation of Interest and Provision on Advances :

e) Interest is calculated on a daily product basis but charged and accounted for quarterly on accrual basis. Interest on classified loans and advances is kept in suspense account as Bangladesh Account Instructions and such interest is not accounted for as income until realized from borrowers.

f) Provision for loans and advances is made on the basis of period and review by the management and instructions contained in Bangladesh Bank Ordinance.

Portfolio of Loans and Advances as on December 2003

Sl. No. | Sector | % of Total Loans |

| 01 | Agriculture | 0.46% |

| 02 | Large and Medium Scale Industry | 22.33% |

| 03 | Working Capital | 12.64% |

| 04 | Export Finance | 13.22% |

| 05 | Commercial Lending | 33.45% |

| 06 | HouseBuilding Loan | 3.09% |

| 07 | Small and Medium Enterpise | 0.90% |

| 08 | Consumer Credit Scheme | 3.73% |

| 09 | Others | 10.18% |

Performance of Credit Operations:

ADVANCES SCENARIO :

The HSBC Group Head Office is responsible for formulating high-level credit policies; the independent review of the Group’s larger credit exposures; the control of the Group’s cross-border exposures, as well as those to banks and financial institutions; and the portfolio management of risk concentrations. It also reviews the efficiency of credit approval processes, a key element of which is the Group’s universal facility grading system. Both the HSBC Group and the Bank Executive Committees receive regular reports on credit exposures. These include information on large credit exposures, concentrations, industry exposures, levels of bad debt provisioning and country exposures.

In HK$ million

| 2003 | 2002 | 2001 | 2000 | |

| Gross Advances to Customers | 829,415 | 738,988 | 698,712 | 645,556 |

| Net Advances Customers | 816,004 | 721,775 | 679,897 | 633,781 |

| Overdue Advances to Customers | 11,004 | 14,828 | 15,654 | 14,525 |

(Source : HSBC Annual Report 2003)

Credit Facilities Position:

2003 2002 2001 2000 1999

Credit facilities 1,295 1,403 1,534 1,580 1,189

Chapter 10 : Conclusion Part

Major Findings of the Project and Recommendation for Credit Administration Department:

Findings of the Study :

- With a view to improving the quality and soundness of loan portfolio, credit risk management methods were updated in 2003. The Bank is now applying a new system of credit assessment and lending procedures by stricter separation of responsibilities between risk assessment and lending decisions.

- From the analysis of Loans and Advances from the annual report 2003, it shows that the net advances to customers to HKD$816,004 million up by 14% compared to the year 2002.

- The Bank provide incentive bonus to its employees on the basis of profit earned during the year. This year the Bank provides several time’s basic salary as the incentive bonus to its employees and two festival bonuses which motivates employees to perform effectively and efficiently.

- The employees of the Bank are young, energetic, cooperative and friendly. Their dealings with the client are cooperative and friendly which creates attractive perception about the client and interest to do business with the Bank.

- HSBC also gives preferences to local customer through its marketing efforts.

Identification some problems regarding Credit Management:

- Proper Credit Management is the most important function of any Bank. But the credit management activities suffer from some kinds of problems which are learnt from discussion with officers, clients and also problems identified from the job observations. The problems are as follows :

- Undue Pressure from Relationship Managers and the Top Management :

- 2. Lack of Deposit for Credit Extensions:

- Discussion with officers of the Head Office revealed that if the Bank collect more deposit, it would be able to advance credit to more viable projects.

Mentally of not to repay the loan:

A culture has been developed among the common people that Bank loans need not to be repaid.

4. Defective Legal System:

Existing bad legal system is another greatest blow and curse to the credit management system and alarming factor recovering loan from defaulter. In reality it is very difficult, lengthy and expensive to have a verdict in favor of the Bank.

- Delay in Loan Sanction:

Lengthy process of loan sanction or delay is a common problem of credit management.

- Higher Rate of Interest for Credit :

Clients generally complain that rate of interest for various type of credit are quite high. In many cases productivity from loaned investment is inadequate that borrower become incapable in repaying loan.

- Changes in Policies :

Due to changes in the export, import, foreign exchange policy as well as monetary and fiscal long term financing suffer a lot.

- Irregularity in Providing Loan:

Usually Banks are responsible to provide loan to those who are eligible for the loan. But in reality, small investors do not get the loan easily. They have to fulfill more terms and conditions than those who have greater influence in the business community.

- Lower Remuneration Structure :

HSBC is the leading Bank in the banking sectors not only in Bangladesh but also all over the world. The Bank is earning huge amount of profit every year. But the Remuneration structure of the employees especially lower level employees are comparatively less than other multi-national Bank like Standard Chartered or Citi Bank NA.

Observation and Recommendation :

- Lending policies in Bangladesh should be geared to growth potential.

- HSBC should be enforced to expand its activities and loan programs in the rural areas to serve the national interest.

- Diversification of the loan portfolio is, of course, the key to lowering the overall credit risk.

- HSBC should introduce distinguished rate for the best customers which will

attract the good customers.

- For motivating the employees to perform their activities efficiently and effectively HSBC should restructure the remuneration package of the employees.

- Since the lending rate of HSBC is comparatively high, it can attract more customers by lowering the rate.

- HSBC should be increase Marketing activities to be competitive in the marketplace.

Personal Experience and Conclusion :

The Six months Internship program in The Hongkong and Shanghai Banking Corporation Limited (HSBC), in Head Office: AnchorTower, Sonargaon Road, Dhaka, gave me the opportunity to have practical knowledge on Banking system as well as the financial spheres of Bank. My successful completion of the Internship program is of the contribution of the concerned officers of the credit division. Because of their cooperative an friendly attitude I felt quite easy during my internship period. The credit officers helped me, supported me and guided me to understand the functions of the credit administration.

At first I would like to thank our Placement Teacher/Faculty for giving me the opportunity to complete my Internship Program in the world’s second largest Bank. It was a great achievement to be a part of HSBC for the time being.

My Internship program started from 17 July, 2004. At that day after submitting my joining report I was assigned to Credit Administration Department. On the first day I was only introduced with the officers of the department without doing any jobs. After few days I was assigned to do the preparation and processing of the security documents. My major job responsibility was to handle the security documentation, updating their loans and advances on the daily basis, drafting and sending the debit and credit advise for the related parties. During my Internship period I prepared a questionnaire on the “Employees Satisfaction Survey” for the Credit Department and I was highly appreciated for this job.

Since I am a student of Accounting and Information Systems, the concerned credit officer then assigned me some my subject related job. The credit officers have to prepare credit proposal before sanctioning loan by the credit committee. There they have to make financial analysis on the prescribed format of Head Office. The clients usually send their annual report and I had to prepare the financial statement of them according to the format of the Bank. Sometimes I had to analyze the financial statements through ratio analysis. Sometimes I had to assess the working capital of the clients. The concerned officers helped me in all respect. There one thing comes to my notice that Bank usually provide loan to different types of institutions like sole

proprietorship, partnership company, leasing institutions and so on. But since they have to follow the prescribed format of financial statements it creates problem. Because different institutes has different types of assets, liabilities, expense and income. So the Bank can prepare the format according to the nature of the organization.

HSBC issues different type of Bank Guarantee. Sometimes I helped the concerned officer in registering the bank guarantee related activities. Sometimes I prepared vouchers by charging commission, VAT and creating Banker’s and Customer’s liabilities. There I learnt that commission rate vary from institute to institute depending on the creditworthiness of the clients. The credit officers have to update Register by recording the different types of securities and charge documents offered and signed by the client. From there I learnt about different types of securities and charge documents.

Loan against different schemes are sanctioned for a specific time limit. When the limit is expired, concerned officers send letters to the clients. I wrote some letters by noticing the client the matter. Then in response to their application the loan’s time limit is extended or loan amount is adjusted. I helped the concerned officers in this respect.

When I was free I visited different desks. There I saw that everyone is doing their job properly. They are cooperative and friendly to the customers. When I face any problem they helped me cordially without showing any type of irritations although I was not the internee of their department.

Working atmosphere of HSBC is very cordial. All of the employees received me not as an intern but the member of the HSBC. I did not felt any fear or hesitation in my working because of appreciation and cordial, friendly and cooperative attitude.

During my study, I learnt the theories and in my internship period I saw the application of them to some extent. It was a great experience to learn the application of my knowledge and to be one of the members of HSBC.

CONCLUSION:

Most of the Banks in Bangladesh are offering a wide array of financial services including new types of loans and advances and some whole new services are being launched every year. HSBC, a bank of difference, also has a discover new avenues to reach its goals. HSBC is the world’s local Bank in the sense that the activities or services of this Bank is operating in all the six Continents ( the logo of HSBC represents that by the six sides). For the brand name HSBC, it is gone to peoples heart through updating various services. HSBC should diversify its credit portfolio so that in near future when competition among Banks will serve, it can stand with its own identity. Now HSBC is continuing business operation successfully in Bangladesh since 1996 through developing an image and goodwill among its clientele by offering its excellent services. The success has been resulted from the dedication, commitment and dynamic leadership of its management. During the short span of time of its operation, HSBC has successfully grabbed a position as a highly progressive and dynamic financial institution in the country. By proliferation of new advance services, expanding use of automated equipment and electronic transfer of financial information, HSBC will be the world’s first largest institution in the near future.

Some are parts:

Internship Report on Hongkong and Shanghai Banking Corporation Limited(Part 1)

Internship Report on Hongkong and Shanghai Banking Corporation Limited(Part 2)