EXECUTIVE SUMMARY:

This internship report ‘Business Activities of Corporate Sales Department of Grameen Phone Limited’ is prepared on the basis of three months practical working experience from the department of Corporate Sales of Grameen Phone Ltd.This is a learning report divided into four parts- organizational part, learning part, findings & recommendations, and conclusion.

Organizational part focuses on Historical Background of GrameenPhone Ltd., Founding Partners of GrameenPhone Ltd., About GrameenPhone Ltd., Share Holding Structure, Company Organogram, Services Offered, Products.Learning part contains objective, data source, methodology, and limitations of the report. According to the objective sort out the body of the report as The Sales and Distribution Division, The Corporate Sales Department, Organogram Of The Department, Units under Corporate Sales Department, Business Activities of Corporate, Strategic and Communication & MIS units, and the importance of those Business Activities.

Then findings & recommendations part pulls out several findings from the learning part. And some recommendations are given for the findings.

And then conclusion part provides an overview of the Corporate Sales Department of Grameen Phone Ltd.

Historical Background of GrameenPhone Limited:

GrameenPhone was offered a cellular license in Bangladesh by the Ministry of Posts and Telecommunications on November 28, 1996. The Company launched its service on March 26, 1997, the Independence Day of Bangladesh.

In 1996, Bangladesh was preparing to auction off private cell phone licenses to four companies. So at the behest of Dr. Muhammad Yunus (Grameen Bank’s founder) but completely independent of Grameen Bank, a not-for-profit private company called Grameen Telecom was created. Grameen Telecom, in turn, created a for-profit company called Grameen Phone, found a foreign partner, and put in a bid; Grameen Phone received one of the four licenses. Grameen Phone’s total capitalization was US$120,000,000, including around US$50 million from IFC/CDC, and the Asian Development Bank (ADB). It also received US$60 million in equity from the four Grameen Phone private partners. These were the Norwegian Telenor with a 51% share, Marubeni of Japan with a 9.5% share, and the American Gonophone at 4.5%. Grameen Phone’s fourth partner is Grameen Telecom (with 35%), and Grameen Telecom borrowed US$10.6 million from the Open Society Institute to set up Village Phone.

Grameen Phone launched service in urban Dhaka on March 26, 1997. It makes its profits by serving wealthier urban customers. But from the point of view of the Grameen family and its strong anti-poverty mission, the for-profit, urban-only Grameen Phone exists for only one reason: To fund, with its profits, the extension of cell phones into rural Bangladesh in order to provide entrepreneurial opportunity to Grameen Bank members through Village Phone. As Dr. Yunus puts it, “Grameen Phone is merely what we need to do Grameen Telecom’s Village Phone.

Founding Partners of GrameenPhone:

GrameenPhone is a joint venture company comprising of:

Telenor – A state-owned telecommunication company from Norway. It has a long history of successful cooperation with other operators in Russia, Hungary, Montenegro, Ireland, Bangladesh, Greece, Germany, Australia, Malaysia etc.

Grameen Telecom – A sister concern of Grameen Bank. It was established by Grameen Bank to organize and assist those Grameen bank borrowers who wish to retail telephone services in the rural areas.

Marubeni Corporation – A leading investment and trading company from Japan.

Gonofone Development Corporation – A New York-based telecommunication development company having investments in many companies in USA, Russia and other parts of Europe.

These four companies owned shares of GrameenPhone in the following manner:

Company | Percentage of share (%) |

Telenor | 51.0 |

Grameen Telecom | 35.0 |

Marubeni Corporation | 9.5 |

Gonofone | 4.5 |

Table: Share holders of GrameenPhone

About GrameenPhone Ltd.

The Vision:

“To be the leading provider of telecom services all over Bangladesh with satisfied customers, shareholders and enthusiastic employees”.

The Mission:

GrameenPhone Ltd. aims at providing reliable, widespread, convenient mobile and cost effective telephone services to the people in Bangladesh irrespective of where they live. Such services will also help Bangladesh keep pace with other countries including those in South Africa region and reduce her existing disparity in telecom services between urban and rural areas.

The Purpose:

GrameenPhone has a dual purpose:

- To receive an economic return on its investments and

- To contribute to the economic development of Bangladesh where telecommunications can play a critical role.

This is why GrameenPhone, in collaboration with Grameen Bank, is aiming to place one phone in each village to contribute significantly to the economic uplift of those villages.

The Strategy:

GrameenPhone’s basic strategy is coverage of both urban and rural areas. In contrast to the “island” strategy followed by some companies, which involves connecting isolated islands of urban coverage through transmission links, GrameenPhone builds continuous coverage, cell after cell. While the intensity of coverage may vary from area to area depending on market conditions, the basic strategy of cell-to-cell coverage is applied throughout GrameenPhone’s network.

The People:

The people who are making it happen – the employees – are young, dedicated and energetic. All of them are well educated at home or abroad, with both sexes (genders) and minority groups in Bangladesh being well represented. They know in their hearts that GrameenPhone is more than just about phones. This sense of purpose gives them the dedication and the drive, producing – in about three years – the biggest coverage and subscriber-base in the country. GrameenPhone knows that the talents and energy of its employees are critical to its operation and treats them accordingly.

The Technology:

GrameenPhone’s Global System for Mobile or GSM technology is the most widely accepted digital system in the world, currently used by over 300 million people in 150 countries. GSM brings the most advanced developments in cellular technology at a reasonable cost by spurring severe competition among manufacturers and driving down the cost of equipment. Thus consumers get the best for the least.

The Service:

GrameenPhone believes in service, a service that leads to good business and good development. Telephony helps people work together, raising their productivity. This gain in productivity is development, which in turn enables them to afford a telephone service, generating a good business. Thus development and business go together.

The Result:

By bringing electronic connectivity to rural Bangladesh, GrameenPhone is delivering the digital revolution to the doorsteps of the poor and unconnected. By being able to connect to urban areas or even to foreign countries, a whole new world of opportunity is opening up for the villagers in Bangladesh. Grameen Bank borrowers who provide the services are uplifting themselves economically through a new means of income generation while at the same time providing valuable phone service to their fellow villagers. The telephone is a weapon against poverty.

Share Holding Structure:

The shareholders of GrameenPhone contribute their unique, in-depth experience in both telecommunications and development. The international shareholder brings technological and business management expertise while the local shareholder provides a presence throughout Bangladesh and a deep understanding of its economy. Both are dedicated to Bangladesh and its struggle for economic progress and have a deep commitment to GrameenPhone and its mission to provide affordable telephony to the entire population of Bangladesh.

Telenor Mobile Communications:

Telenor is the leading Telecommunications Company of Norway listed in the Oslo and NASDAQ Stock Exchanges. It owns 62% shares of GrameenPhone Ltd. Telenor has played a pioneering role in development of cellular communications. It has substantial international operations in mobile telephony, satellite operations and pay Television services. In addition to Norway and Bangladesh, Telenor owns GSM companies in Denmark, Austria, Hungary, Russia, Ukraine, Montenegro, Thailand and Malaysia. It has recently started a mobile phone operation in Pakistan.

Telenor uses the expertise it has gained in its home and international markets for the development of emerging markets like Bangladesh.

Grameen Telecom:

Grameen Telecom, which owns 38% of the shares of GrameenPhone, is a not-for-profit company and works in close collaboration with Grameen Bank. The internationally reputed bank for the poor, has the most extensive rural banking network and expertise in microfinance. It understands the economic needs of the rural population, in particular the women from the poorest households. Grameen Telecom, with the help of Grameen Bank, administers the Village Phone Program, through which GrameenPhone provides its services to the fast growing rural customers. Grameen Telecom trains the operators,

supplies them with handsets and handles all service-related issues. Grameen Bank currently covers more than 51,000 villages which are serviced by 1326 bank branches (December’ ‘04) all over the countryside. At the end of the year, the bank had 3.78 million borrowers, 95 percent of whom were women.

Grameen Telecom’s objectives are to provide easy access to GSM cellular services in rural Bangladesh, creating new opportunities for income generation through self- employment by providing villagers with access to modern information and communication based technologies.

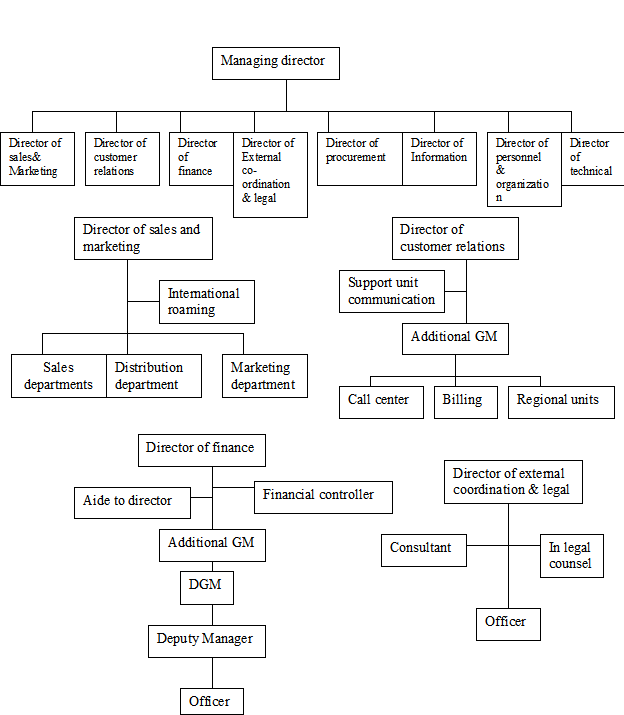

Company Organogram:

Services Offered

Company Service:

GrameenPhone believes in service, a service that leads to good business and good development. Telephony helps people work together, raising their productivity. This gain in productivity is development, which in turn enables them to afford a telephone service, generating a good business. Thus development and business go together.

Service for the Rural Poor:

Establishing a nation wide network gives fair access to all geographical areas. From a business point of view, this strategy serves both the long distances as well as the rural markets. This emphasis on rural coverage brings a much-needed infrastructure in the underdeveloped rural areas. In collaboration with Grameen Bank, which provides micro-credit only to the rural poor, GP utilizes the bank borrowers to retail telecom services in the rural areas. Leveraging on Grameen Bank borrowers reduces the distribution costs of Grameen Phone’s rural services, contributing to the profitability of this segment.

By bringing electronic connectivity to rural Bangladesh, GrameenPhone is bringing the digital revolution to the doorsteps of the rural poor and unconnected.

Village Phone Program:

The Village Phone program is Grameen Phone’s unique method of bringing connectivity to the rural areas of Bangladesh. This program enables Grameen Bank’s borrowers to retail telephone service in their respective villages, and has the potential to penetrate the rural areas rapidly and effectively.

A typical Grameen Bank borrower takes a loan of Tk 6000 without collateral from the Bank to purchase, say, a cow. The cow would then produce milk that the borrower could sell to her neighbors enabling her to make a living and pay off the loan. The process allows the poorest of the poor to stand up on their feet. In the case of Village Phone, a telephone also acts as an income generating mechanism for a borrower; a telephone serves as another “cow.” A woman borrows about Tk20,000 from the Bank and purchases a handset and sell telephone services to the villagers, making a living and thus paying off her loan. It creates a self-employment opportunity in each village and provides access to telephones to all.

Grameen Telecom, Grameen Bank’s arm for administering the Village Phone operators, typically selects women by considering past borrowing records with the Bank. There are 2144 Village Phones in operation today and soon thousands of Village Phones around the country are expected across rural Bangladesh.

Products:

The products of Grameen Phone can be classified as:

Post Paid

Pre-Paid

djuice

Business Solutions

Post Paid:

Under Post Paid Service there are 3 products:

GP-Regular:

GP Regular connects to BTTB local, BTTB-NWD (Nationwide Dialing), ISD (International Standard Dialing), all Grameen Phone mobiles, other mobiles and receives calls from the same. Recently all GP Regular phones have been given the mobility facility that enables a GP Regular mobile holder to receive and send calls from anywhere in the country (under GP coverage).

GP- National:

GP National is a post-paid product with mobile-to-mobile connectivity and BTTB incoming facility. Anyone can make and receive calls to and from all mobiles (within GP coverage area). It has network mobility feature, with which anyone can move around the country with GP mobile phone (within GP coverage area).

Anytime 500:

‘Anytime 500’ is a post-paid product with BTTB (Local/NWD/ISD) connectivity. Anytime 500 offers a monthly 500 minutes (billed duration) of talk-time free of charge. It has the network mobility feature, with which one can move around the country with GP mobile phone (within GP coverage).

Pre-Paid:

EASY Gold:

Easy Gold is a pre-paid product with BTTB (Local, NWD and ISD) connectivity. One can connect to all mobiles and BTTB lines. It has the network mobility feature, with which one can move around the country with GP mobile phone (within the GP coverage area).

EASY Pre-Paid:

Easy Pre-paid is a pre-paid product with mobile-to-mobile connectivity. One can make and receive calls to and from all mobiles (within GP coverage) using EASY Pre-paid. It has network mobility feature, with which one can move around the country with GP mobile phone (within GP coverage).

This service helps the subscriber to control costs. It frees the subscriber from the hassles of paying bills, security deposits and line rents. But it contains nearly all services available in other GP products. Subscribers can subscribe the service from all Grameen Phone authorized points of sale.

The GP Regular, GP-GP Regular and National subscribers enjoy a number of GSM Features and Value Added Services (VAS).

djuice:

djuice is a mobile subscription for young people who use the mobile phone for communication and entertainment. It is a registered trademark owned by Telenor. The product is a balanced combination of several tailor-made elements and benefits. It is a pre-paid connection with differentiated feature options (group message, STK, My time, Free trials (SMS), etc.).

djuice provides lifestyle based basic and compelling contents plus privilege card with extras with contents related to Music, sports, etc. Most promotions are Value Added Service based usage.

Business Solutions:

Business Solutions is a high quality and fully integrated telecommunications service from GrameenPhone, especially designed for the business entities of Bangladesh.

As the largest and most customer centric telecommunication service provider in the country, we provide customer oriented and customized telecommunications solutions through a highly consultative approach.

What we offer is a suite of specialized products and services covering all communication needs for professionals, small, medium-sized enterprises to large companies.

Comprising of modern mobile telecommunications services for any business needs, we provide voice services, messaging services and mobile data and internet services. We also provide a complete Mobile Office solution, including mobile e-mail, mobile high speed data access, internet access, mobile fax and more, giving you the freedom to work from anywhere anyone want to.

Learning Part:

GrameenPhone is heading towards a brighter future by targeting the corporate clients along their glorious path of meeting the telecommunication need of the corporate business segment of Bangladesh. This endeavor will open up a new prospect for the company as this segment represents a huge number of premium business customers of the country. Corporate Sales Department handling this responsibility of Grameen Phone.

To find out the ‘Business Activities of Corporate Sales Department of Grameen Phone Limited’ is the topic of the report.

Objectives:

- I. To identify the formal and informal structure of Corporate Sales Dept.

- II. To identify different units of Corporate Sales Department.

- III. To identify business activities of different units of the department.

- IV. To identify the importance of those business activities.

Methodology & Data Source:

Secondary data have collected by searching the Grameen Phone web site – www.grameenphone.com. Primary data have collected through discussion with the colleagues by using a questionnaire. Questions are designed to find the answers to all the specific objectives.

Limitations:

This report is a Learning report not project report.

It does not focus on all activities of Corporate Sales Department.

For maintaining secrecy no information has represents from internal documents.

The Sales and Distribution Division:

The sales and Distribution Division includes the following departments:

- Corporate Sales

- SME Sales

- Tele Sales

- Distribution

- Trade Marketing

The Corporate Sales Department:

Corporate Sales Department offers a suite of specialized products and services covering all communication needs for large companies. Comprising of modern mobile telecommunications services for any business needs, the product Business Solutions provide voice services, messaging services and mobile data and internet services. Business Solutions also provides a complete Mobile Office solution, including mobile e-mail, mobile high speed data access, internet access, mobile fax and more, giving business people the freedom to work from anywhere they want to.

The Corporate Sales Department is a well formed team of X members, each person well selected and groomed to perform the critical sales process of selling to the valued corporate clients of GrameenPhone. Out of the panel of X, Y are engaged in direct sales, a vital task of the department.

Direct sales to the esteemed large offices in Dhaka city is a task the department handles with care and caution. Thus the process of sales make sure that the consumers in no way are disturbed but feels honored to be looked after or served with a product as soon as the need is sensed.

Organogram Of The Department:

This formal structure of Corporate Sales shows that all instructions downs from GM to DGM and then managers. Unit wise instructions downs to deputy managers and then officers. In the same way reports go to upward directions.

Beside the formal structure of the department an informal structure also found where instructions passes directly from top level to bottom level without any interruptions and reports also passes directly vice-versa. This is happened for quick decision making and for time saving that is called time management.

Units under Corporate Sales Department:

There are three different units namely Strategic, Corporate, and Communication & MIS under the department of Corporate Sales. Unit definitions are as follows.

STRATEGIC:

Strategically important organizations that held socially influential positions are considered strategic clients, e.g. Government Organization, Embassies, UN Organizations, Ministries, Educational Institutions, Media Sectors etc.

CORPORATE:

Organizations with 200+ employees and investment of more than Tk. 300 million are considered to be corporate client. They have an average purchasing power of approximately 200 subscriptions, e.g. MNC’s, Public Limited Companies etc.

COMMUNICATION & MIS:

This unit maintains database of corporate & strategic clients to communicate with them after sales by arranging different types of event. It works to give back up to Corporate unit and Strategic unit.

Business Activities of Corporate unit & Strategic unit:

Both the unit Corporate and Strategic do the vital activity that is selling.

The Sales Process:

The sales process of the Corporate Sales Department is quite different and specified. Instead of all the sales representatives having their individual ways and styles of selling, since the product is a standard product, that is Business Solutions, The sales process is also standard and defined. Following is the steps of sales process:

- Established contact by the sales personnel through existing customers, relatives, friends.

- Preparations taken for doing the presentations about the product features.

- Meeting to the contacted person(s) and presenting the prepared presentation.

- Action for negotiating to get benefits both the party regarding price, services, number of subscribers, number of periods.

- Offer to sale the product after negotiation, if all or most of all requirements is fulfilled of both the parties.

- Implementation that is agreement signing ceremony.

- Follow up the sale with value added services provided according to the clients’ requirement.

Business Activities of Communication & MIS unit:

Communication & MIS unit of Corporate Sales Department maintains the database of clients and arranges different types of event for the clients. These are two business activities done by Communication & MIS unit. Details of them are discussed as follows:

Database:

The database contains name, designation, mobile number, phone number, e-mail, fax and address of the clients. For the database data collected by Agreements signing papers, business cards, and by phone calls.

A sample figure of the database maintained by Corporate Sales Department is shown below:

SALUTATION PHONE ZONE

FULL NAME E-MAIL COMPANY

DESIGNATION FAX CATEGORY

MOBILE NO ADDRESS KAM

In this database it is shown that there are three parts. First part is for entering the data into the fields. Second part is for saving, deleting, editing, and searching the data. And the last part shows all saved records.

Some criteria of this database are:

- This database is made by SQL where huge amount of data can stored and many users can use it at a time.

- Salutation, full name, designation, and mobile number field must be filled up to save a record.

- Each and every record must save before going to enter another record.

- Zone, company, category, key account manager (KAM) fields have a combo box (previously enter several data) to select required one from that.

- To search any record select zone, company, category, or KAM fields.

- To delete or edit a record select that record from the table then click delete or edit.

Events:

Different types of event arranged to communicate to the clients by Communication & MIS unit of Corporate Sales Department. To promote the product other than the regular promotional activities that applies for the mass market products of GrameenPhone, Corporate Sales Department arranged events as the promotional activities.

Besides the huge Billboards that carry the Business Solutions advertisements, most of promotional activities are customized to attract and impress the people of the corporate world. A few examples of the promotional activities are-

- Corporate Fair

- Corporate Mezban

- Corporate Movie Show

- Corporate Open Day

- Corporate Night

- Corporate Iftar

Some promotional activities are also associated with using the Business Solutions Brand name on items such as-

- Clocks

- Slip Pad Boxes

- Key Rings

- Diaries

- Pens etc.

This is all for maintaining long-term relationship with the clients. During the whole year all the events are arranged one after another. And clients are invited getting the attractive invitation card which is made by Communication & MIS unit of Corporate Sales Department.

Importance of Business Activities

Importance of Sales:

It is a vital activity for the Corporate Sales Department. It has a unique process to do the total work. Without this activity maintaining the database and arranging the events is quite useless. Because database maintenance is actually back up activity and events arrangement is promotional activity.

Importance of Database:

Database is a large source of information. Some essentials reasons of maintaining the database by Corporate Sales Department are highlighted here:

Easy to contact with customers:

For any kind of queries or for any invitation, if Corporate Sales Department wants, it can easily contact with their clients by mobile, e-mail, telephone or by sending letter to their addresses. These information exist in the database.

Easy to update:

Beside data storage in the database, updating of data is very important as well. Because it is very natural that address, phone number, fax number or even personnel of a company can be changed in future. So these information are adjusted easily in the database, if it is maintained.

Easy to promote value added service:

Database also helps to promote value added service (VAS) to the clients. Because it becomes very easy to inform clients about the VAS of past package by mobile, e-mail, or telephone using the database.

Importance of Events:

Long term customer relationship:

Corporate events are designed to maintain long term relationship with the clients. These types of events can make corporate clients to understand that Grameen Phone honored and cared them. Then clients also try to maintain a long term relationship with GP.

2. Easy way of communication:

It is definitely a best way of communication which is not actually possible otherwise. Corporate clients get the opportunity to meet with the top and mid level of employees of Grameen Phone and to express their opinion for getting VAS in a friendly environment.

3. Public Awareness:

Whenever any kind of special events are arranged for corporate clients, this news comes in the newspaper. So this published news works as a tool of public awareness. This news builds awareness about the new approach of corporate customer care of Grameen Phone among other corporations who are not the clients of GP. And this awareness turns them into the corporate clients of Grameen Phone.

Findings & Recommendations

Findings: I. Beside the formal structure of the department an informal structure also found where instructions passes directly from top level to bottom level without any interruptions and reports also passes directly vice-versa. This is happened for quick decision making and for time saving that is called time management.

II. There are three different units namely Strategic, Corporate, and Communication & MIS under the department of Corporate Sales. Both the unit Corporate and Strategic have done the vital activity that is selling. And Communication & MIS unit maintains database and arranges events.

III. For the database when data is collected by phone call, spelling mistakes may be happened. It creates a bad image when invitation card is delivered to the corporate clients with those mistakes.

IV. Different types of event arranged to communicate to maintain long-term relationship with the clients.

V. The sales process is followed a unique way in the Corporate Sales Department including contact, preparations, meeting, Action, offer, implementation, and follow up.

Recommendations: I. For the informal structure of the department, it must be maintained that bottom level employees directly pass the report of any work to the top level after getting instructions from top level. Otherwise they should not cross the mid level.

II. To get the authentic data for the database agreement signing papers and business cards of the clients i.e. written document are the right sources. There is no chance to happen spelling mistakes.

III. Event is arranged for maintaining long-term relationship with the clients. So, decision must be made carefully to invite the clients based on their age, gender, zone for specific event.

IV. Selling is the vital activity and the sales process is unique. So, the sales personnel should be get training before entering the sales process about how to prepare them for each step of sales process.

Conclusion:

The Corporate Sales Department under Sales & Distribution Division of Grameen Phone Ltd. sells the customized product Business Solutions to the big corporate bodies.This department has three different units namely Strategic, Corporate, and Communication & MIS. Where Strategic and Corporate both the units do the vital activity i.e. selling and Communication & MIS unit maintains database and arranges different types of event like Corporate Fair, Corporate Mezban, Corporate Movie Show, Corporate Open Day, Corporate Night, and Corporate Iftar.

Strategic and Corporate both the units followed a unique sales process including contact, preparations, meeting, Action, offer, implementation, and follow up.

Maintaining the database is important to easily contact to the clients, to easily update the database in future, and to easily promote the value added services (VAS).

Arranging different types of event by Corporate Sales Department is important to maintain long term relationship with clients and to build up public awareness.