Introduction:

Now I would like to provide some recommendation which may be helpful to promote the export import business of United commercial Bank Limited as well as Bangladesh. Through conducting this study I have acquired some practical knowledge about export import business in Bangladesh and other relevant matters.

Origin of the Study:

In today’s competitive area the importance of practical learning is raising day by day besides academic education. In fact academic education becomes rich when acquired knowledge is applied to practical situation. Proper application of knowledge to theoretical field implies to get extra benefit while understanding the matter related to subject. So the procedure of gaining knowledge through practical application is known as internship.

In this regard I had got an opportunity to carry on my internship program in United Commercial Bank Limited at Mohammadpur Branch for a period of 3 months from June 8, 2006 to September 10, 2006. The Management of United Commercial Bank Limited assigned me to work on Foreign Exchange operation. After completion of my internship I submit my report on the project titled”Foreign Exchange operation in United

Commercial Bank.

Background of the Study:

Any academic course of the study has a great value when it has practical application in the real life. Only a lot of theoretical knowledge will be little important unless it is applicable in the practical life. So we need proper application of our knowledge to get some benefit from our theoretical knowledge to make it more fruitful when we engage ourselves in such field to make proper use of our theoretical knowledge in our practical life, only then we come to know about the benefit of the theoretical knowledge. Such an application is made possible through internship. When theoretical knowledge is obtained from a course of study it is only the half way of the subject matter. Internship implies the full application of the methods and procedures through rich acquired knowledge of subject matter can be fruitfully applied in our daily life. Such a procedure of practical application is known as internship. The case study is titled”Foreign Exchange operation of United Commercial Bank Limited”. As a student of MBA this study will be more significant in my practical life. I have worked for three months at Mohammadpur Branch of United Commercial Bank Limited to complete the internship program as an academic requirement.

Objectives of the study:

Objective of the study acts as a bridge between the starting point and the goals of the study. To illustrate the objectives properly, presented into two parts:

A. General:

To observe the Foreign Exchange Operation of United Commercial Bank Limited and their services.

B. Specific

- To observe the major outline of Foreign Exchange Business.

- To observe Credit line arrangement.

- To observe the Foreign correspondents of UCBL.

- To observe the post important financing operations.

- To analysis the expansion of foreign trade Business of the UCBL.

- To identify the problems of its financing.

- To recommended solutions of or solving the problems faced by UCBL in Foreign Exchange Branch.

Scope of the Study:

The main objective of the study is to obtain a clear idea about the foreign exchange Business of our banking operation i.e. how the L/C is opened and how the import& export is done. The other objectives are as follows:

- To fulfill the requirement of our MBA program

- To evaluate the performance of the uunited commercial Bank Limited import and export business.

- To recommend about Foreign Exchange Business Of the United Commercial Bank Limited.

Methodology of the Study:

In order to make the report more meaningful and presentable, to sources of data and information have been used widely.

The primary Source of data is:

- Face to face conversation with the respective Officer of the Branch.

- Face to face conversation with the clients.

- Relevant file study as provided by the officers concerned.

- Observation

The Secondary Sources of Data are:

- Annual Reports of the UCBL.

- Periodicals Published by Bangladesh Bank.

- Different books, articles etc. regarding Foreign Exchange Operations.

Limitation of the study:

The study has been conducted to be made an investigation of the Banks state of affairs of foreign trade. On the study in this field some problems were created, which may be termed as limitations of the study:

- Unavailability of sufficient written documents as required to make a comprehensive study.

- Very inadequate time to make an in depth inference about foreign exchange for the schedule of the department.

- In many cases, up to date information is not published.

- Because of the unwillingness of the busy key persons, necessary data collection became hard.

- Incomplete and obscure data are also limitation.

- Foreign Exchange some times is very confidential, so getting adequate relevant information was different.

- Audited data of 2002 were not available.

- Limited time of internship program.

Abbreviation Used:

The mostly used abbreviations in the report are as follows:

UCBL:- United Commercial Bank Limited

T.T:- Telegraphic Transfer.

DD:- Demand Draft.

PO:- Pay Order

LTR:- Loan against Trust Receipt.

LIM:-Loan against Imported Merchandise.

PAD:- Payment against Document.

PSP:- Pratirakhwa Sanchay Petra.

BSP:- Bangladesh stanched Petra.

CR:- Confidential Report.

IRC:- Import Registration Certificate.

ERC:- Export Registration Certificate.

TIN:- Tax Identification Number.

FBC:- Foreign Bill Collection.

LFBC:- Local Foreign Bill Collection.

C&F:- Cost And Freight.

FBPN:-Foreign Bill Purchase and Negotiation.

AD: – Authorized Dealer.

MSS: – Monthly Saving Scheme.

FD: – Fixed Deposit.

STD:-Short Term Deposit.

CA:-Current Account.

OVERVIEW OF BANGLADESH ECONOMY AND FINANCIAL INSTITUTES:

Bangladesh is a least development country, Whose economy country is agro-based. The agriculture system is primitive and frequently affected by natural disaster. Poverty is the main problems of this country about 47.6% of its population is living below the poverty line whoever as about18%of the population is living below the hard core poverty line(with less then 1800 calories per head per day).

After the devastating flood 1998-1999, the economic activities of the country resumed by taking various rehabilitation program and bumper production of the agriculture sector helps to recover that below. Bangladesh economy has faced severe set back again after the terrorist attack on world trade center of USA on september11,2001 and afghan war. This event has changed the world economic scenarios and caused global economic recession. This global recession has severely affected export system& Bangladesh economy like made garments industry, frozen food, Manpower export hotel and tourism sector etc. Due to global recession foreign financial assistance also severely affected.

To overcome this situation government has taken various sect oral reform plan (closer of Amaze jute Mill is an example of it). Govt. also prepares the current fiscal years budget to decrease the foreign aid dependency. Although global recession has caused the ever lowest foreign currency reserve of US$1057n million in October, 2001 which is increased to US$1478 million in April 2002 by various positive steps taken by the government anti money laundering law, emphasis on remittance through proper banking channel.

According to Bangladesh economic analysis 2002 of ministry of finance, income is increased by 1.73% and population is increased 1.71%. Per capital GDP, GNP and NNI are shown in the following table:

Fiscal Year | GDP | GNI | NNI | |||

US$ | Taka | US$ | Taka | US$ | Taka | |

2001 | 363 | 19595 | 377 | 20332 | 349 | 18809 |

2002 | 362 | 20673 | 375 | 21448 | 347 | 19805 |

Overview of Financial institutes of Bangladesh:

Financial institutes play an important role of the economic development of any country. The objective of these institutions is to accumulate the scattered deposit and invest it in a productive manner for economic emancipation.

There are 52 schedule banks(January 2001) operate in Bangladesh of them 4 nationalized commercial Banks, 5 Specialized Banks, 30 private Banks and 12 Foreign Banks. The number of Branches of those Banks is 6242. Of which 2511 (40.2% of total) are in urban areas and rest 3731(59.8% of total) are in rural areas.

Up to February 2002, of fiscal 2001-2002, total deposit and loan of all Banks is Taka 85259.8 and Taka 69392.6 Cr. Respectively.

For proper monitoring the operations of Banks, Bangladesh bank introduces ”Problem Bank Monitoring Division” in addition to Camel Rating. To increase the economic activities Bangladesh Bank reduces the Bank rate to 6% from 7%.

To increase Customer service Banks are using Various modern techniques like on line banking ATM, Money Gram, Credit Card etc.

List of Banks operating in Bangladesh:

Nationalized Commercial Banks (NCBS)

- Sonali Bank.

- Janata Bank.

- Agrani Bank.

- Rupali Bank.

- Basic Bank Limited.

Private Commercial Bank (PCBS)

1. Pubali Bank Limited.

2. Uttara Bank Limited.

3. Arab Bangladesh Bank Limited.

4. National Bank Limited.

5. The City Bank Limited.

6. International Finance investment and Commerce Bank Limited.

7. United Commercial Bank Limited.

8. Eastern Bank Limited.

9. National Credit and Commerce Bank Limited.

10. Prime Bank Limited.

11. South East Bank Limited.

12. Dhaka Bank Limited.

13. Dutch Bangla Bank Limited

14. Mercantile Bank Limited.

15. Standard Bank Limited.

16. One Bank Limited.

17. Mutual Trust Bank Limited.

18. First Security Bank Limited.

19. The Trust Bank Limited.

20. Premier Bank Limited.

21. Bank Asia Limited.

22. Bangladesh commerce Bank Limited.

23. Export and Import Bank Of Bangladesh Limited.

24. Shahjalal Bank Limited.

25. Jamuna Bank Limited.

26. BRAC Bank Limited.

27. Islami Bank Bangladesh Limited.

28. The Oriental Bank Limited.

29. Al-Arafah Islami Bank Bangladesh Limited.

30. Social Investment Bank Limited.

Foreign Commercial Banks: (FCBS):

1. American Express Bank.

2. Standard Chartered Bank.

3. Habib Bank Limited.

4. State Bank of India.

5. Credit Agricole Indosuez.

6. National Bank of Pakistan.

7. Muslim Commercial Bank.

8. Citibank NA.

9. Hanvit Bank.

10. The Hongkong and Shanghai Banking corporation (HSBC).

11. Shamil Bank of Bahrain E.c.

12. Bank Alfalah.

Specialized Bank:

1. Bangladesh Shilpa Bank.

2. Bangladesh Shilpa Rin Shonghstha.

3. Bank of Small Industries and Cottage.

4. Bangladesh Krishi Bank.

5. Rajshahi Krishi Unnayan Bank (RAKUB).

2.3. A Bank is usually defined as a financial institution which deals in money. Today however the function of a Bank have increased so much that it is considered a very vital agent of development in country like ours. Because of their positive involvement in trade industry, business finance and a host of other allied services, Banks today form a very important part of an economy.

A bank like private commercial bank helps to develop economy as follows:

The nationalized banks, countries margin operational banking units could not demonstrates and achieve optimistic results in terms of overall economic growth. The gloomy picture of nationalized banks is mainly due to:-

- Lack of quality of services.

- Minimum of commitment toward institutions.

- Management inefficiency.

- Excessive intervention of collective bargaining agent(CBA).

- Lack of security.

- Documentation of loans and advances debarring legal action in case of default.

- Slow rate of recovery of loan.

- Lack of supervision and monitoring of loans and advances.

- Directive loans.

- Political instability.

- Transitional inconsistency while formulating policy issue on banking.

Due to inefficient and continuous loosing concern of public sector, the main objective of privatization policy was-

- To reduce deficit of the Govt. to meet continuous loss of public

enterprises.

To improve operative efficiency of enterprise.

- To introduce competitiveness in all spheres of economic activities except few areas where Govt. control of economic activities was unavoidable.

In the country 80s it was increasingly felt that a number of PCBs might have improve their position putting nationalized banks into competition. The launching of PCBs has finally created a significant impact in quality of services in banking. Banking being a service industry, it is not easy to quantity to performance of this sector like manufacturing. The performance of the banking sector in terms of generating of profit expansion of bank branches, mobilization of deposits, deployment of advances, involvement in foreign trade and generating of employment.

It is revealed from the loan operations of banks. The PCBs provide operation mainly for trading(internal trading, export and import trade)and construction while the NCBs are providing finance for priority areas like agriculture, industry and export import tasks.

PCBs have shown some efficiency in terms of branch expansion employment generation, mobilization of deposits and deployment of advances but their activities remained concentrated in city areas. They could not provide finance for priority sector like agriculture.

The key to success of private sector banks is identified as a professional efficiency in choosing various risk assets, personalized quantity of services, result oriented business strategy and achievement against stipulated target. But by rapidly issuing fresh licenses to the promoters of private banks, the quality of entrepreneurs is not being ensured and developed. As a result too many banks are chasing same customers/entrepreneurs within limited deposit base.

Now a day, the banking business exclusively depends on quality of services in terms of new innovative strategies for boosting banking operations compatible to international standard. Modern technology, equipment and innovation like computerized money counting machine, automatic teller machine (ATM) etc. are being utilized to a great extent for survival and to face competitors.

PCBs have already explored new financial products by introducing master card, credit card to attract customer/entrepreneurs. Many PCBs have implemented various attractive schemes acceptable to the existing and prospective customers such as the customer credit scheme, marriage and educational scheme, micro credit scheme and small loan scheme etc. In this respect PCBs are keen for development of human resources to train and equip their manpower with new ideas and products to Enable them to contribute to the greater innovation.

The PCBs are talking part in stimulating foreign exchange reserve by financing 100% export oriented RMG industries. Neutrally 65% of export earnings of Bangladesh is generated by this sector.

The PCBs are participating and financing in various types of medium and long term industries either wholly or partly through consortium arrangement among the member Banks. The PCBS are also general investor and recently a package program has been derived to stabilize the countries capital market by launching merchants banks which will extend loan to the brokers and general investors.

The nationalized banks are talking advantages of restrictions imposed on non-nationalized banks while mobilizing deposits form government autonomous and semi-autonomous bodies. Our of total available funds of Govt. sector, the PCBs are restricted to the range of 25% to 40% of this funds only. Such dual practice is not desirable when we are hoping the theory of free market economy.

Above all, PCBs have been playing an indispensable role in the money market for the growth and development of our economy along with all nationalized specialized and foreign Banks. The better performance of PCBs will finally be recognized still when they offer better quality of service based on new ideas/products. We foresee a good future for the PCBs. They are expected to develop their lending role in the near future in financial market. The importance of variant economic refers to the due attention to a sound financial system. The base of financial services in Bangladesh is quite narrow. By improving only the financial structure and financial super structure, our financial system can be made sound.

United Commercial Bank Limited in a nutshell:

Historical Back Ground:

Sponsored by some dynamic and reputed entrepreneurs and eminent industrialists of the country and also participated by the government United Commercial Bank Limited started its operation in mid 1983 and has since been able to establish the largest network of 80 Branches as on 31.08.2001 among the first generation Banks in the private sector.

With its firm commitment to the economic development of the country, the Bank has already made a distinct mark in the realm of private sector banking through personalized services, innovative practices, dynamic approach and efficient management. The Bank aiming to play a leading role in the economic activities of the country, is firmly engaged in the development of trade, commerce, and industry through a creative credit pricy.

Structure and management:

The bank has an authorized capital of Tk. 1000.00 million and a paid up capital of Tk.230, 157, 608.00 contributed by sponsors. The head office of the bank is situated at 60, Motijheel Commercial Area, Dhaka-1000. The sponsor directors of the bank are well established businessman, industrialist, and professionals of the country having business in and out of Bangladesh. The chairman of the Board Hajee Younus Ahmed is a renowned businessman besides being an eminent personality of the country. The management team of the bank is successfully led by Mr. Hamidul Huq, Managing Director of the Bank. He is prominent and dynamic banker Mr Niaz Habib Deputy Managing Director of the bank. The management is ably supported and assisted by qualified executives and officers.

Strategies:

- Synchronized and steady growth of the bank.

- Utilize all available resources to develop various plans, policies and procedure in each of the objective and goal areas.

- Implement plans, policies and procedures.

- Utilize a team of professional employees.

- Search for a total customized solution of let for the purpose of full automation step.

Goals:

- Develop a realistic deposit mobilization plan.

- Develop appropriate lending risk assessment system.

- Develop capital plan.

- Develop a system to make good advances.

- Develop a recruitment, compensation, training and orientation plan.

- Develop a plan for offering better customer service.

- Develop appropriate management structure, system, procedures and approaches.

- Develop scientific MIS to monitor banks activities.

Business objectives:

- Build up a low cost fund base.

- Make sound loan and investment.

- Meet capital adequacy recruitment at all the time.

- Ensure 100% recovery of all advances.

- Ensure a satisfied work force.

- Focus on free based income.

- Adopt a appropriate management technology.

- Install a scientific MIS to monitor banks activities.

Current Position:

Capital:

During the year 2002 authorized capital of the Bank remained unchanged at tk.1000.00 million and the paid up capital stood at tk.230.16 million. On the other hand the reserve fund of the bank increased by tk.46.92 million to tk.440.42 million as against tk.393.50 million in the previous year.

Number of Branches:

UCBL always places utmost importance on the client services. With that end in view The Bank continued its personalized approach in rendering improved and modernized services. Presently the number of branches stand at 80 covering almost all the important places of the country. The number of authorized dealer branches are 18.

At the close of 2002, total investment of the bank stood at tk.3961.60 million as against tk.1961.58 million in2001. However, dividend amounting to Tk. …million has been received from different companies/institutions against investment in shares during the year.

Number of share holders:

During the year 2002, total number of share holders of the bank stood 3943 as against number of share holders 3539 in the year 2001.

Operations:

The importance of the mobilization of savings for the economic development ok our country can hardly be over emphasized. We consider savings and deposits life blood of the bank. More the deposits, greater is the strength of the bank. The bank intends to launch various new savings schemes with prospect of higher return duly supported by a well orchestrated system of customer services.

The bank is catering to the credit needs of individuals as well as corporate clients. It is emphasizing on trade finance which would be short-term and self-liquidating in nature, considering the importance of foreign trade in our national life, financing and handling of export & import business and also handling of foreign remittance business by giving top most priority.

Objective:

United commercial bank Limited aims at excellence and is committed to explore a new horizon of m banking and provide a wide range of quality products and services. It is a bank for the common people including businessmen and professionals. It intends to serve with quality at a price competitive to anyone in the financial market. It would constantly keep on exploring the needs of the clients. So the united commercial bank Limited shall also develop a youthful and exuberant management team-technologically sound and rich in experience. They would work hand in hand with zeal and enthusiasm to achieve the objectives of the bank in the new millennium.

Foreign trade can be easily defined as a business activity, which transcends national boundaries. These may be between parties or government ones. Trade among nations are a common occurrence and normally benefit both the exporter and importer. In many countries, international trade accounts for more than 20% of their national income.

Foreign trade can usually be justified on the principle of comparative advantage. According to this economic principle, it is economical profitable for a country to specialize in the production of that commodity in which the producer country has the greater comparative advantage and to allow the other country to produce that commodity in which it has the lesser comparative advantage. It includes the spectrum of goods, service, investment, technology transfer etc.

This trade among various countries causes for close linkage between the parties dealing in trade. The bank which provides such transactions is referred to as rendering international banking operations. International trade demands a flow of goods from seller to buyer and of payment from buyer to seller and this flow of 23 goods and payment are done through letter of credit (L/C).

As more than one currency is involved in foreign trade, it gives rise to exchange of currencies which is known as foreign exchange. The term”Foreign Exchange” has three principal meanings. Firstly, it is a term used referring to the currencies of other currencies in terms of any single one currency. To a Bangladesh, Dollar, pound sterling etc. are foreign currencies and as such foreign exchange. Secondly, the term also commonly refer to some instruments used in international trade, such as bill of exchange, drafts, Travel Cheques and other means of international remittance. Thirdly, the terms foreign exchange is also quite of ten referred to the balance in foreign currencies held by a country.

In terms of section 2(d) of the foreign exchange regulations 1947 as adopted in Bangladesh, Foreign exchange means Foreign currency and includes any instrument drawn, accepted made or issued under clause (13) of article 16 of the Bangladesh Bank order 1972 all the deposits, credits and balance payable in any foreign currency and draft Cheque, letter of credit and bill of exchange expressed or drawn in Bangladesh currency but payable in any Foreign country.

In exercise of the power conferred by section 3 of the foreign exchange regulation, 1947 Bangladesh bank issues license to schedule bank to deal with exchange. These Banks are known as Authorized dealers. Licensees are also issued by Bangladesh bank to persons or firms to exchange foreign currency instruments such as T.C currency notes and coins. They are known as authorized money changers.

Functions of Foreign Exchange Department:

Exports:

- Pre-shipment advance.

- Purchase of foreign bills.

- Negotiating of foreign bills.

- Export guarantees.

- Advising/confirming letters-letter of credit.

- Advance for deferred payments exports.

- Advance against bills for collection.

Imports:

- Opening of letter of credit (L/C)

- Advance bills.

- Bills for collection.

- Import loan and guarantees.

Remittances:

- Issue of DD, MT, TT etc.

- Payment of DD, MT, TT etc.

- Issue and enhancement of traveler’s cheques.

- Sale and enhancement of foreign currency notes.

- Non-resident accounts.

The Most commonly used documents in Foreign Exchange:

- Documentary Letter of Credit.

- Bill of exchange.

- Bill of Lading.

- Commercial Invoice.

- Certificate of origin of goods.

- Inspection certificate.

- Packing List.

- Insurance policy.

- Pro-forma Invoice/ Indent.

- Master receipt.

- GSP certificate.

Documentary Credit:

In simple terms a documentary credit is a conditional bank undertaking a payment. Expressed more fully, it is a written undertaking by a bank (issuing bank) given to seller (beneficiary) at the request, and in accordance with the instructions of the buyer (applicant) to effect payment (that is, by making a payment or accepting or negotiating bill of exchange) up to a started sum of money, with in a prescribed time limit and against stipulated documents. The customary clauses contain in a L/C are the followings:

- A clause authorizing the beneficiary to draw bills of exchange up to certain on the

- opener.

- List of shipping documents, which are to accompany the bills.

- Description of the goods to be shipped.

- An undertaking by the opening bank that bills drawn in accordance with the conditions will be dully honored.

- Instructions to the negotiating banks for obtaining reimbursement of payments under the credit.

Parties to a letter of credit (L/C): The parties to a letter of credit are:

- Importer/ Buyer

- Opening Bank/ Issuing Bank.

- Exporter/ Seller/ Beneficiary.

- Advising Bank/ Notifying Bank.

- Negotiating Bank.

- Confirming Bank.

- Paying/ Reimbursing Bank

Bill of Lading:

A bill of lading is a document that is usually stipulated in a credit when the goods are dispatched by sea. It is evidence of a contract of carriage, is a receipt for the goods, and is a document of title to the goods. It also constituted a document that is, or may be, needed to support an insurance claim.

The details on the bill of lading should in Claude-

- A description of the goods in general terms not in consistent with in the credit.

- Identify marks and numbers, if any.

- The name of the carrying vessel.

- Evidence that the goods have been paid loaded on board.

- The ports of shipment and discharge.

- The names of shipper, consignee, and name and address of the notifying party.

- Whether freight has been paid or is payable at destination.

- The number of original bills of lading issued.

- The date of issuance.

A bill of lading specifically states that goods are loaded for ultimate destination specifically mentioned in the credit.

Commercial Invoice:

A commercial invoice is the accounting document by which the seller changes the goods to the buyer. A commercial invoice normally includes the following information;

- Date

- Name and address of the buyer and seller

- Order of contract number, quantity and description of the goods, unit price and the total price.

- Weight of the goods, number of the package, shipping marks and numbers.

- Terms of delivery and payment.

- Shipment details.

Certificate of origin:

A certificate of origin is a signed statement providing evidence of the origin of the goods.

Inspection certificate:

This is usually issued by an independent inspection company located in the exporting country certifying or describing the quality, specification or other aspects of the goods, as called for in the contract on the L/C. The inspection is usually nominated by the buyer who also indicates the types of inspection he wishes the company to undertake.

Insurance certificate:

The insurance certificate documents must-

- Be that specified in the credit.

- Cover the risks specified in the credit.

- Be consistent with the other documents in its identification of the voyage and description of the goods.

- Unless otherwise specified in the credit

- Be a document issued and/or signed by an insurance company or its agent, or by underwriters.

- Be dated on or before the date of the date of shipment as evidenced by the shipping documents.

- Be for an amount at least equal to the C/F value of the goods and in the currency of credit.

Import operation:

Import is foreign goods and services purchased by customer, firm and Government in Bangladesh.

An importer must have import registration certificate (IRC) given by chief controller of import and exports (CCI&E) to import any thing form other country. To obtain import registration certificate (IRC) the following certificates are required:-

- Trade License

- Income Tax clearance certificate.

- Nationality certificate

- Banks solvency certificate

- Asset certificate.

- Registration partnership deed (if any)

- Memorandum and Article of Association.

- Certificate of incorporation (if any)

- Rent receipt of the business premises

Import procedure:

To import though United Commercial Bank Limited (UCBL) a customer/Client requires:-

- Bank Account

- Import registration certificate.

- Tax paying identification number

- Pro-forma Invoice/Indent

- Membership certificate

- L/C application form duly attested

- One set of Imp Form

- Insurance cover note with money receipt

- Others.

Import Mechanism:

To import, a person should be competent to be an importer. According to import and export control Act, 1950, the office of chief controller of import and Export provides the registration certificate (IRC) to the importer. After obtaining the person has to secure a letter of credit Authorization (LCA) from Bangladesh Bank and then a person becomes a qualified importer.

He is the person who requests or instructs the opening Bank to open an L/C. He is also called opener or applicant or the credit.

Importers application for L/C limit/ Margin:

To have an import L/C limit, an importer submits an application to the department of (UCBL) furnishing the following information:-

- Full particulars of Bank account.

- Nature of Business.

- Required amount of limit.

- Payment terms and conditions.

- Goods to be imported.

- Offered Security.

- Repayment Schedule.

A credit officer scrutinizes this application and accordingly prepares a proposal (CLP) and forwards it to the head office credit committee (HOCC). The committee, if satisfied, sanctions the limit and return back to the Branch. Thus the importer is entitled for the limit.

Opening of letter of credit (L/C) by bank:-

Opening of L/C means, at the request of the applicant (Importer) issuance of a L/C in favor of the beneficiary (Exporter) by a bank. The bank which open or issue L/C is called L/C opening bank or issuing bank. On receipt of the importers L/C application supported by the firm contract (Indent/Pro-Forma Invoice) and insurance cover note the bank scrutinize the same thoroughly and fix up a margin on the basis of banker-customer relationship.

Before opening a L/C, the issuing bank must check the following:-

- L/C application properly stamped, signature verified and margin approved and properly retained.

- Indent/ pro-forma Invoice signed by the importer and Indenter/supplier.

- Ensure that the relevant particulars of L/C application correspond with those stipulated in indenter/pro-forma invoice.

- Validity of LCA entitlement of goods, amount etc. Conforms to the L/C application.

- Conversion and rate of exchange correctly applied.

- Charges like commission, FCC, postage, Telex charge, swift charge, if any recovered.

- Insurance cover note-in the name of issuing bank-A/C importer covering required risks and voyage route.

- Incorporation of instruction for negotiating banks as per banks existing arrangement.

- Reimbursement instruction for reimbursing bank.

- If foreign bank confirmation is required, necessary permission should be obtained and accordingly advising bank is advised as per banks existing arrangement.

- If add confirmation is required on account of the applicant charges should be recovered from the applicant.

- In case of séance L/C, mention rate of interest clearly in the letter of credit.

Liability of issuing Bank:-

As per article 9(a) of UCPDC 500, An irrevocable credit constitutes a definite undertaking of the issuing bank, provided that the stipulated documents- comply with the terms and conditions of the credit.

Advising of letter of credit:

Advising means forwarding of a documentary letter of credit received from the Issuing bank to the beneficiary (exporter).

Before advising a L/C the advising bank must see the following:-

- Signature of issuing bank officials on the L/C verified with the specimen signatures book of the said bank when L/C received.

- If the export L/C is intended to be an operative cable L/C test code on the L/C invariably be agreed and authenticated by two authorized officers.

- L/C scrutinized thoroughly complying with the requisites of concerned UCPDC provisions.

- Entry made in the L/C Advising Register.

- L/C advised to the beneficiary (Exporter) promptly and advising charges recovered.

Advising Banks Liability:-

Advising banks liability is fixed up in uniform customs and practice for documentary credits, publication 500.

Article7(a):- Credit may be advised to a beneficiary through another bank (the “Advising Bank”) without engagement on the part of the advising bank, but the bank, if it elects to advice the credit shall take reasonable care to check the appeasement authenticity of the credit which it advises. If the bank elects not to advice the credit, it must inform the issuing bank without delay.

Article7(b):- If the advising bank cannot establish such apparent authenticity it must inform, without delay the bank form which the instructions appear to have been received that it has been unable to establish the authenticity of the credit and if its elects nonetheless to advice the credit it must inform the beneficiary that it has not been able to establish the authenticity of the credit.

Adding confirmation:-

Adding confirmation is done by the confirming bank. Confirming bank is a bank which adds its confirmation to the credit and it is done at the request of the issuing bank the advising usually does not do it if there is not a prior arrangement with the issuing bank. By being involved as a confirming agent the advising bank undertakes to negotiate beneficiary bill without recourse to him.

- Issue L/C and request to add confirmation.

- Review the L/C terms.

- Provide reimbursement.

- Drafts to be drawn on L/C opening bank.

- Availability of credit facilities.

- Line allocation from the business and ownership units in the importers country.

- Confirm and advice L/C.

Amendments to letter of credit:

After issuing and advising of a L/C, it may be felt necessary to delete, add or alter some of the clauses of the credit. All these modifications are communicated to the beneficiary through the same advising bank of the credit. Such modifications to a credit are termed as amendment to a letter of credit.

There may be some of the conditions in a credit are not acceptable by the beneficiary. In that cases beneficiary contract applicant and request for amendment of the clauses. On receipt of such request applicant approaches his bank that is issuing bank with a written request for amendment to the credit. The issuing bank scrutinizes the proposal for the amendment and if the same is not in contravention with the exchange control regulation and banks interest, the bank may then process for amendment. There can be more than one amendment to a credit. All the amendment forms an integral part of the original credit.

L/C amendments are to be communicated by SWIFT or mail. If there are more than one amendment to a credit, all the amendment must bear the consecutive serial number so that the missing the any amendment can be identified by the advising bank or by the beneficiary.

What is to be done by the issuing bank before advising amendment:-

The issuing bank has to-

A) Obtain written application from the applicant of the credit duly signed and verified by the bank.

B) In case of increase of value, applications for amendment are to be supported by revised indent/pro-forma invoice evidencing consent of the beneficiary.

C) In case of extension of shipment period, it should be ensured that relative LCA is valid/ revalidated/increased up to the period of proposed extension.

D) Amendment of an increase of credit amount and extension of shipment period both the cases amendment of insurance cover note also is submitted.

E) Proper recording and filling of amendment is to be maintained.

F) Amendment charges (if an account of applicant) will be recovered and necessary voucher is to be passed

The following clauses of L/C are generally amendment:-

- Increase/decrease value of L/C and increase/decrease of quantity of goods.

- Extension of shipment/negotiated period.

- Terms of delivery i.e. FOB, CFR, and CIF etc.

- Mode of shipment.

- Inspection clause.

- Name and address of the supplier.

- Name of the reimbursing bank.

- Name of the shipping line etc.

Settlement of letter of credit:

Settlement means fulfillment of issuing bank in regard to affecting payment subject to satisfying the credit terms. Settlement may be done under three separate arrangements as stipulated in the credit.

Settlement by payment:

Here the seller presents the documents to the nominated bank and the bank scrutinizes the documents. If satisfied the nominated bank makes payment to the beneficiary and in case this bank is other than the issuing bank, then sends the documents to the issuing bank and claim reimbursement as per arrangement.

Settlement by Acceptance:

Under this arrangement, the seller submits the documents evidencing the shipment to the accepting bank (nominated by the issuing bank for acceptance) accompanied by drafts down on the bank at the specified tenor. After being satisfied with the documents, the bank accepts the documents and the draft and if it is a bank other than issuing bank, then sends the documents to the issuing bank stating that it has accepted the drafts and the maturity the reimbursement will be obtained in the pre-agreed manner.

Settlement by Negotiation:

This settlement procedure starts with the submission of documents by the seller to the negotiating bank in a freely negotiate documents and if negotiation restricted by the issuing bank, only nominated bank can negotiate the documents. After scrutinizing that the documents meet the credit requirement, the bank may negotiate the documents and give value to the beneficiary. The negotiating bank then sends the documents to the issuing bank, as usual, reimbursement will be obtained in the pre-agreed manner.

Accounting Treatment:

Sundry Deposit L/C Margin A/C—————————————— Dr

PAD A/C————————————————————————-Cr

(Margin amount transferred to PAD A/C)

Customer A/C——————————————————————– Dr

PAD A/C————————————————————————– Cr

(Customer account debited for the remaining amount)

PAD A/C————————————————————————— Dr

Head Office A/C+ Exchange Trading A/C———————————- Cr

Income A/C interests on PAD————————————————- Cr

(Amount given to Head office ID and interest credit)

Reversal Entries:

Bankers Liability ————————————————————— Dr

Customers Liability ——————————————————— Cr

(When lodgment is given)

After realizing the telex charge, service charge, interest (if any) and the shipping documents is then stamped with PAD number & entered in the PAD register. Intimation is given to the customer calling on the banks counter requesting retirement of the shipping documents. After passing the necessary vouchers, endorsements is made on the back of the bill of exchange as “Receipt payments” and the bill of lading is endorsed to the effect “please deliver to the order of M/S–

Under two authorized signatures banks officers (P.A. holder). Then the documents are delivered to importer.

Payment procedure of the import documents:

This is the most sensitive task of the import department. The officials have to be very much careful while making payment.

- Date of payment: Usually payment is made within 7 days after the documents have been received. If the payment is become deferred, the negotiating bank may claim interest for making delay.

- Preparing sale Memo: A sale memo is made at BC rate to the customer. AS the TT & DD rate is paid to the ID the difference between these two rates is exchanging trading. Finally, an inter Branch exchange Trading credit advice is sent to ID.

- Requisition for the foreign Currency: For arranging necessary fund for payment, a requisition is sent to the International Department.

- Transmission of Telex: A telex is transmitted to the correspondent bank ensuring that payment is being made.

Export Operation:

Practically by the term Export we mean out carrying of anything from one country to another. As banker we define export as sending of visible things outside the country for sale. Export trade plays a vital note in the development process of an economy. With the earning we meet out import bills.

Although export trade is always encouraged, any body can not export anything to any place. Like importer the exporters are also required to get them registered before entering into export trade. Export registration certificate (ERC) given by CCI & E is required for this purpose. The required documents to obtain ERC are also same as IRC.

When a bank (Authorized Dealer) receives a L/C (Cable or original) it ascertains the correctness of the test number and the authorized signature. Then the bank sends the original copy of the L/C to the Beneficiary.

The exporter presents the relative documents to the negotiating bank after the shipment of the goods. The L/C issuing bank undertakes to honor is obligation only if the beneficiary fulfills the conditions stipulated in the L/C, may namely, the submission of stipulated documents with in the stipulated time. Even a slide deviation of the documents from these specified in the L/C may give an excuse to the negating bank. So the negotiating bank must be careful, promote, systematic and bias-free while scrutinizing the tender documents after careful and through examination of the documents, the banker has to list out the discrepancies which may be classified as major or minor, irremovable or removable. The removable discrepancies can be corrected by the tendered or future losses, which may arise due to non-repatriation of proceeds.

The following types of discrepancies may be noted while the negotiating bank examines the documents:

- L/C expired

- Late Shipment

- Amount drawn in excess of the L/C

- Bill of exchange not properly drawn

- Descriptions of goods differ.

- Bill of lading or Airway bill of state

- Bill of lading classed

- Insurance covered Note as per terms L/C

- Insurance cover obtained after the bill of lading or Airway bill date

- Enough number of copies not submitted as required by L/C

- Negotiation under L/C restricted

- Packing list and certificate of analysis not as per the L/C

- Documents not properly endorsed in favor of the bank

- Full shipment not effective and part shipment prohibited

- Gross weight and Net weight shown in different documents differ

- Same of the documents required by L/C not submitted and

- Documents inadequately stamped.

Documents with major discrepancies, which could not be negotiated, should be sent on collection basis with the permission of the exporter.

Exporter Procedure:

The export and importer trade in our country are regulated by imports and exports (control) Act, 1950. Under the Export policy of Bangladesh the exporter has to get the valid export Registration certificate (ERC) from chief controller of import & Export (CCI & E). The ERC is required to renew every year. The ERC number is to be incorporated on EXP forms and other papers connected with Exports.

Registration of exporter:

For obtaining ERC indenting Bangladesh exporters are required to apply to the controller/ Join controller/ Deputy controller/ Assistant controller of imports and Exports, Dhaka/ Chittagong/ Khulna/ Mymensingh/ sylhet/ comilla/ Barisal/ Bogra/ Rangpur/ Dinajpur in the prescribed from along with the documents:

- Nationality and assets certificate

- Memorandum and Articles of Association and certificate of Incorporation in case of limited company.

- Bank certificate

- Income Tax certificate

- Trade license etc.

Securing the order:

After getting the ERC (Export Registration certificate) the Exporter may proceed to secure the Export order. He/she can do this by containing the buyers directly or though agent. In this purpose exporter can get help from-

- Liaison office

- Buyer’s local agent.

- Export promotion organization

- Bangladesh mission abroad

- Chamber of commerce (Local & Foreign)

- Trade fair etc.

Signing the contract:

After communicating with buyer exporter has to get contracted (writing or oral) for exporting exportable items from Bangladesh detailing commodity, quantity, price shipment, insurance and marks, inspection, arbitration etc.

Receiving the letter of credit:

After getting contract for sale, exporter should ask the buyer for letter of credit clearly stating terms and conditions of export and payment.

The following are the main points to be looked into for receiving (collecting export proceeds by means of documentary credit) –

- The terms of the L/C are in conformity with those of the contract

- The L/C is an irrevocable one, preferable confirmed by the advising bank.

- The L/C allows sufficient time for shipment and negotiation

Terms and conditions should be stated in contract clearly in case of other modes of payment:

- Cash in advance

- Open A/C

- Collection basis (Documentary/ clean)

- (Here the regulatory frame work is URC-525, ICC publication).

Procuring the Materials:

After the making deal on the L/C opened in his favor, the next step for the Exporter is to set about the task of procuring or manufacturing the contracted materials/ merchandise.

Shipment of goods:

Then the Exporter should take the preparation for export arrange for delivery of goods as per L/C and INCO-terms, prepare and submit shipping documents for payment/Acceptance/Negotiation in due time. Documents for shipments-

- Exp form

- ERC (Valid)

- L/C Copy

- Customer Duty Certificate

- Shipping instruction

- Transport Documents

- Insurance Documents

- Invoice

- Other Documents

- Bill of Exchange (if required)

- Certificate of origin

- Inspection certificate

- Quality control certificate

- G.S.P. certificate

- Photo -sanitary certificate

Final step:

After those exporter submits all these documents along with a letter of indemnity to NCCBL for negotiation. An officer scrutinizes all the documents. If the document is a clear one, NCCBL purchases the documents of the banks of banker- customer relationship. This is known as Foreign Documentary bill purchases (FDBP).

Procedure for FDBP:

After purchasing the documents, NCCBL gives the following entries.

FDBP A/C DR

Customer A/C CR

(Before realization of proceeds)

Head Office A/C DR

FDBP A/C CR

(Adjustment after realization of proceeds)

A FDBP Registered is maintained for recording all the particulars:

Foreign Documentary Bills for collection:

United commercial Bank Limited forwards the documents for collection due to the following reason:-

- If the documents have discrepancies.

- If the exporter is a new client.

- The banker is in doubt.

Foreign documentary bills for collection signify that the exporter will receive payment only when the issuing bank gives payments. The exporter submits duplicate EXP form & commercial invoice, subsequently, the value of the bill is calculated and the following accounting entries are given:-

Head Office A/C DR @ TT clean

Clients A/C CR

@ OD sight)

Govt. Tax A/C CR

(@ of invoice value)

Postage A/C CR

Income A/C profit on Exchange CR

After passing the above vouchers, an inter Branch Exchange Trading Debit advice is sent for debiting the NOSTRO Account. United commercial bank limited has NOSTRO account with its reimbursing bank. An FDBP register is maintained, where first entry is given when the documents are forwarded to t5he issuing bank for collection and the second one is done after realization of the proceeds.

Export Bill Scrutiny sheet:

A) General

- Late shipment

- Late presentation

- L/C expired

- L/C overdrawn

- Partial shipment or transshipment beyond L/C terms

B) Bill of Exchange

- Amount of bill differs with invoice

- Not drawn on L/C issuing bank

- Not signed

- Tenor or B/E not identical with L/C

- Full set not submitted

- Invoice

- Not issued by the beneficiary

- Not signed by the beneficiary

- Not made out I name of the applicant

- Description, price, Quantity, sales terms of the goods not correspond to the credit.

- Not marked one fold as original

- Shipping marks differ will B/A & packing list

C) Packing List

- Gross weight, Net weight & measurement, Number of cartoons/ Packages differs with B/L

- Not marked one fold as original

- Not signed by the beneficiary

- Shipping marks differ with B/L

D) Bill of Lading/Airway Bill:

- Full set of bill not submitted

- B/L is not drawn or endorsed

- B/L shipping on board”Freight prepaid” or”Freight collect” etc. Notations are not marked on the B/L.

- B/L not indicate the name and capacity of the party i.e. carrier or master, on whose behalf the agent is signing the B/L.

- Shipped on board notation not showing name of pre-carriage vessel/intended vessel.

- Shipping on board notation not showing port of loading and vessel name (Incase B/L indicates a place of receipt or taking in charge different from the port of the loading).

- Short form B/L

- Charter party B/L

- Description of goods in B/L not agrees with that of invoice/E & P/L

- Alternations in B/L not authenticated

- Loaded on deck

- B/L bearing clauses or notations expressly declaring defective condition of the goods and/or the packages.

E) Others

- Non-negotiable documents not forwarded to buyers or forwarded beyond L/C terms.

- Inadequate number of invoice, packing List & others submitted.

- Short shipment certificate not submitted.

Settlement of Local bill:

The settlement of local bill is done is the following ways:-

- The customer submits the L/C to United Commercial Bank Limited along with the documents to negotiate.

- United Commercial Bank Limited official scrutinize the documents to ensure the conformity with the terms and conditions.

- The documents are then forwarded.

- The L/C issuing bank gives the acceptance and forwards an acceptance letter.

- Payment is given the customer on either by collection basis or by purchasing the documents.

Accounting treatment of or purchase of local bill:

Local bill purchase documentary DR

Party A/C CR

Commission A/C CR

Interest A/C CR

A LBPD (Local bill purchase documentary) register is maintained to record the acceptance of the issuing bank. Until the acceptance is obtained, the record is kept in a collection register.

Mode of payment of export bills under L/C:-

The most common methods of payment under a L/C are as follows:-

- Sight payment credit:-In a sign payment credit, the bank pays the stipulated sum immediately against the exporters presentation of the documents.

- Negotiation credit:-In negotiation credit, the exporter has to present bill of exchange payable to him in addition to other documents that the bank negotiation.

- Deferred payment credit:-In deferred payment, the bank agrees to pay on a specified future date or event, after presentation of the export document. No bill of exchange is involved in UCBL payment is given to the party at the rate of D.A 60-90-120-180 as the case may be. But the head office is paid at T.T clean rate. The different between the two rates is the exchange trading for the branch.

- Acceptance credit: In acceptance credit, the exporter presents a bill of exchange payable to himself and drawn at the agreed tenor (That is, on a specified future date event) on the bank that is to accept it. The bank signs its acceptance on the bill returns it to the exporter. The exporter can then represent it for payment on maturity. Alternatively he can discount it in order to obtain immediate payment.

Advising Letter of credit (L/C):-

When exporter L/C is transmitted to the bank for advising, the bank sends an advising letter to the beneficiary depicting that L/C has been issued.

Test key Arrangement:

Test key Arrangement is a secret code maintained by the banks for the authentication for their telex message. It is a systematic procedure by which a test number is given and the person to when this number is given can easily authenticate the same text number by maintaining that same procedure. United commercial bank limited has test key arrangements with so many banks for the authentication of L/C messages and for making payment.

Back to Back Letter of credit:

A back to back letter of credit is a new credit. It is different from the original credit based on which the bank under takes the risk under the back to back credit. In this case, the banks main security is the original credit (selling credit) are separate instruments independent of each other and in no way legally connected, although they both from part of the same business operation.

The supplier (beneficiary of the back to back credit) ships goods to the importer and presents documents to the bank as is specified in the credit. It is intended that the exporter would substitute his own documents for negotiation under the original credit his liability under the back to back letter of credit would be adjusted out of these proceeds. The exporter L/C is marked lien and no margin is taken.

In UCBL, papers/ documents required for submission for opening of back to back L/C:-

A) Master L/C

B) Valid Import registration certificate (IRC) & Export Registration certificate (ERC).

C) L/C application & LCA form duly filled in signed.

D) Pro-forma invoice or indent.

E) Insurance cover note with money receipt.

F) IMP form duly signed.

In addition to the above the following papers/documents are also required are export oriented garments industries while requesting for opening back to back letter of credit:-

1) Textile permission.

2) Valid bonded warehouse license.

3) Quota allocation letter issued by export promotion bureau (EPB) in favor of the applicant in case of quota items.

4) In case of the factory premises is a rented one, letter of disclaimer duly executed by the owner of the house/ premises to be submitted.

Detective points or clauses appear in the master L/C:-

- Issuing bank is not reputed.

- Advising credit by the advising bank without authentication.

- Port of destination absent.

- Inspection clause.

- Nomination of specific shipping/Airline or nomination of specified vessel by subsequent amendment.

- B/L to blank endorse, to third bank, to be endorsed to buyer or third party.

- No specific reimbursing clause.

- UCP clause not mentioned.

- Shipment/presentation period is not sufficient.

- Original document to be sent to buyer or nominated agent.

- FCR or HAWB consigned to applicant or buyer.

- Shippers Load and count is acceptable.

- L/C shall expire in the country of the issuing bank.

- Negotiation is restricted.

Payment of back to back letter of credit:-

In case of back to back as 60-90-120-180 days of maturity period, deferred payment is made. Payment is given after realizing export proceeds from the L/C issuing bank.

Accounting treatment for back to back L/C:-

When the document is arrived, the following vouchers are passed:-

Customers A/C DR

Commission on Acceptance CR

When payment, if the fund is at hand, the accounting entry is-

Sundry deposit margin on acceptance DR

Customers A/C CR

If the party is paid in foreign currency, B.C. rate is applied in this regard. International department takes the T.T. OD. rate. If the payment is made to ID in local currency in national rate, T.T. clean rate is followed by ID. When the party is paid O.D sight rate is followed.

If the fund is not available to make the payment, the following vouchers are to be passed:-

OAP Dr

Customers A/C CR

Under the back to back concept, the seller, as beneficiary of the credit, offer it as security to the advising bank for the issuing of the second credit. As applicant for this second credit the seller is responsible for reimbursing the bank for payment made under it regardless of whether or not be himself is paid under the first credit. There is, however, no compulsion for the bank to issue the second credit, and in fact, many banks will not do so.

Foreign Exchange Remittance:

Remittance means sending of fund. The word remittance we understand sending/ transferring of fund through a bank form one place to another place which may be within the country or between two countries, one is abroad is called foreign remittance.

“Foreign Remittance” means purchase and sale of freely convertible foreign currencies as admissible “Foreign Exchange Regulations Act-1947” and “Guidelines for foreign exchange transaction-VOL. 1&2 of the country. Purchase of foreign currencies constitutes inward foreign remittance and sale of foreign currencies out ward foreign remittance.

So we see that there are two types of foreign remittance:-

- Foreign inward remittance.

- Foreign outward remittance.

- Inward Remittance.

The remittances which are received from abroad are called inward remittance.

Purpose of inward remittance:-

- Family maintenance

- Indenting commission

- Donation

- Gift

- Foreign Investment

- Export proceeds

- Others.

Mode of inward remittance:

- Telegraphic Transfer (TT)

- Mail transfer (MT)

- Foreign demand Draft (FDD)

- Payment Order (PO)

- Travelers Cheque (TC)

- Foreign currency Notes.

Outward remittance:

Remittance which is made from our country to abroad is called outward remittance.

Mode of outward remittance:

- Foreign Telegraphic Transfer (FTT)

- Foreign Mail Transfer (FMT)

- Foreign Demand Draft (FDD)

- Travelers Cheque (TC)

- Foreign Currency Notes.

Present limit of outward remittance fixed by Bangladesh Bank:

- Travel

A) For private Travel: Private travel quota entitlement of Bangladesh Nations total US$3000 per calendar year for visit to countries other than SAARC (India, Pakistan, Nepal, Bhutan, Srilanka, Maldives) and Myanmar.

Quota for SAARC countries and Myanmar is US$1000 for travel by air and US$500 for travel by land. At a time Bank can issue full amount of above quota if required. Case dollar may be issued maximum US$600 per passport per travel. The amount of travel quota mentioned above is prescribed for adults only. The minors are eligible for 50% of the annual ceilings of adults.

B) Business Travel:

1) Subject to an annual upper limit of US$5000 importers are entitled to Business travel quota 1% of their imports settled during the previous financial year.

2) Subject to an annual upper limit of US$5000 non exporting producers are entitled to business travel quotas 1% of their turnover of the preceding financial year as declared in their tax return.

C) For Exporters: New exporters are entitled to a quota for US$ 6000 annually and old exporters can use FCAD expanse retention quota A/C as per their requirement.

D) For Foreign Nationals: The Authorized Dealers may issue foreign currency TCS to foreigners without any limit and foreign currency notes up to US$ 300 or equivalent amounts in foreign currencies.

Education:

Foreign exchange may be remitted for studies abroad by Bangladesh National in all regular courses (Subject to being consistent with the education policy of the Bangladesh Govt.) in recognized institutions. Authorized dealer has to open file for the individual student. Application and papers required for this purpose as follows:-

- Application duly filled in.

- Original and photocopy of admission letter issued by the educational institution in favor of the student.

- Original and photocopy of estimate relating to annual tuition free, board and loading incidental expenses etc. issued by concerned institution.

- Attested copies of educational certificates of all applicant.

- Valid passport.

Seminar/ workshop/ conferences:

Up to US$ 250 per dicer and US$ 200 per diem receptively may be issued by Authorized dealers to private sector participants for attending seminars, conferences and works hops arranged by recognized international bodies in SAARC member countries or Myanmar and in other countries without prior approval of the Bangladesh Bank. Foreign exchange may be released only for the actual period of the seminar, workshop and conference to be held.

Medical Treatment:

Foreign currency up to US$ 10000 our equivalent may be released by the ADS on the basis of the recommendation of the medical Board set up by the health directorate and the cost estimate of the foreign medical institution. Application for release of exchange exceeding US$ 10000 should be forwarded along with supporting documents to Bangladesh Bank for prior approval.

2. Fees

The ads may release foreign exchange towards remittance of membership fees of foreign professional and scientific institutions and fees for application, registration, admission, examination (TOFEL, SAT, etc). In connection with admission into foreign educational institutions on the basis of written application supported by demand notice/ letter from the concerned foreign institutions showing the amount to be-

- Family Maintenance:

- Bangladesh National: Outward remittance may be made to family members/ dependent parents, spouses and children living abroad with the permission from Bangladesh Bank. A certificate issued by relevant Bangladesh embassy regarding residency of the beneficiary extend of income abroad along with the embassies recommendation as required for this purpose.

- Foreign Nationals: Foreign Nationals who are resident in Bangladesh and who have an income in Bangladesh are permitted to make monthly remittances to the country of their domicile out of their current savings up to 50% of their income to cover their commitments abroad.

- Foreign shipping lines/Air Lines/ Courier Services Company:

These Companies may remit their income after adjustment of the amount of shipment for local disbursement and tax payable.

- Dividend/Gain of foreign Companies/Shareholders:

Dividend, Profit, Gains may be remitted abroad to the owner, shareholders without prior approval of Bangladesh Bank.

- The Govt. of Bangladesh announces each year the scale at which foreign exchange may be issued to intending pilgrims for performing Hajj. Release of foreign exchange for this package should be made as per instruction, to be issued for this purpose by Bangladesh bank each year.

- Remittances of salaries and savings by expatriates:

Expatriates working in Bangladesh with the approval of the Govt. may remit through an authorized Dealer 50% of salary and 100% of leave salary as also actual savings and admissible pension benefits. No prior Bangladesh Bank approval is necessary for such remittance.

- Expenses of office opened abroad:

Remittance of up to US$ 3000 or equivalent may be made annually meet current expenses of such offices opened abroad by a commercial or industrial concern. Such remittance may also be made in the names of concerned offices, subsidiary companies abroad.

- Remittance of Royalty and Technical Fees:

No prior permission of Bangladesh Bank or BOI is required by the enterprises for entering into agreement involving remittance of Royalty, technical know how or technical Assistance Fees. Operational services Fees, Marketing commission etc. If the total fees and other expenses connected with technology transfers do not exceed the following limit:-

- For new projects, not exceeding 6% of the cost of imported Machinery.

- For on going concerns not exceeding 6% of the previous years sales as declared in the income tax return.

Operating Expense of Bangladesh Shipping Corporation & Bangladesh Biman:

Bangladesh shipping corporation and Bangladesh Biman are allowed to make remittances to meet bona fide disbursements in foreign ports, foreign station without approval of Bangladesh Bank.

Remittance against Export claims:

The Authorized Dealers may remit export claims not exceeding 10% of the repatriated export proceeds on the following counts:-

- Short weight claims

- Quality claim

- Part shipment

- Subscriptions to Foreign Media Services:

On application from the local news papers, Ads may remit foreign exchange towards cost of subscriptions of news items features articles of foreign news agencies. Remittance should be made on the basis of contracts entered into between the applicant and the foreign agency and NOC of the ministry of information Ads may remit abroad costs, fees on account of their own subscription of foreign media services such as Router monitor service without prior Bangladesh Bank approval.

Advertisement of Bangladeshi products in Mass Media Abroad:

Ads may without prior Bangladesh Bank approval effect remittance towards cost of advertisement of Bangladeshi products on mass media abroad.

Bank charges and sundries:

The Authorized dealers may affect remittances toward settlement of dues to foreign Banks of Bank charges, Cost of cables and other incidental charges arising in their normal curse of the business without prior Bangladesh Bank approval. All such remittances should be reported to the Bangladesh on forms TM along with appropriate return.

Incoming, outgoing passengers may bring in/ take out up to taka 500 per person in Bangladesh currency.

In all above cases for outward remittance TM form to be obtained and this will have to be reported to Bangladesh Bank Monthly basis.

The Ads must maintain adequate and proper records of all foreign exchange transactions including transaction on non-resident Taka A/C in their book and furnish such particular in the prescribed statements/ returns for submission to the Bangladesh Bank.

The purpose of submission of return and statements to Bangladesh Bank for keeping systematic and proper records of all dealings in foreign exchange including transactions on non-resident Taka A/C. Submission of the returns/ statements to Bangladesh Bank is very much important. Total picture of foreign exchange transaction of the country such as reserve of FC, FCS earned through export, wage earners & other reference and FCS paid through import, treatment, education, traveling etc can be ascertained after compilation of these returns/ statements submitted to Bangladesh Bank by the Ads.

Procedures for reporting transactions:

A) Export:

1) Export bills drawn under confirmed and/or irrevocable L/Cs:

Transactions in respect of export bills negotiated by the Ads should be reported as purchase only at the time entries are made in the currency account duly supported by Exp form and schedule-A

- Exp original reported by custom Authority to Bangladesh Bank at the time of shipment/ export.

- Exp duplicate to be reported by the Ads to Bangladesh Bank within 14 days of shipment.

- Exp Triplicate: To be reported after repatriation of the export proceeds.

ii) Export bills drawn on collection basis:

Sometimes Ads also purchase export bills drawn on collection/CAD basis. Transactions relating to such export bills should be reported as outright purchases against ”Export” in the summary statement on receipt of advice of realization of the export proceeds.

iii) Export bills pertaining to head office or Branch maintaining independent currency account:

When export bills are re-discounted with the Bangladesh Bank the transactions should be reported as purchase in the summary statement supported by schedule A and Exp form and the contra entries should be reported on schedule D as sales to Bangladesh Bank.

iv) As and when the exports are re-discounted with the Bangladesh Bank the Branch concerned will report the transactions as purchase in the summary statement supported by schedule A-1/0-1 and Exp. Form.

B) Other Receipts:

Purchase of DD, TT and MT etc. Should be reported to Bangladesh Bank only when the transactions are put through the currency account

C) Imports:

- Foreign currency A/Cs of Ads is debited at the time of negotiation of import documents by their foreign correspondent drawn under the L/Cs established by the Ads. Sale of this F.C. should be reported on receipt of negotiated import documents and not on the basis of retirement of bills by the importer.

- All sales on account of imports are required to be supported by the original copy of the IMP form.

- Import bills received on collection/CAD basis, the transactions will be reported on schedule E-2 supported by original IMP form.

E) Other payment:

Transactions relating to DD, MT, TT etc issued by the Ads should be reported only at the time of entries are made in the currency Accounts.

Transactions in non-resident Taka accounts of foreign Banks should also be reported by the Ads.

Coding of Transactions:

AD will give code numbers for all receipts and payments transactions on the relevant forms and schedules as per code list provided by foreign Exchange policy Dept. Bangladesh Bank (2000 edition) and AD will use the HS code number form the HS code guide titled “The Harmonized commodity Description and coding system” exports and imports in the relevant schedules.

Reporting procedure for cash transaction:

Ads shall export to the Bangladesh Bank particulars of all their foreign exchange transactions i.e. all outward and inward remittances effected. Whether through their accounts in foreign currencies or through the taka accounts of non-resident Banks. The original copies of statement/ schedules to be sent directly to the statistics Dept. Bangladesh Bank Head Office, Dhaka the duplicate copies along with the relevant forms should be endorsed to the concerned area office of Bangladesh Bank. These monthly statement/ schedules to be sent to Bangladesh Bank by the 5th day of the following month.

Compilation of summary statement:

Each summary statement will be an abstract of the Ads ledger A/C and will consist of totals under specified heads. Opening and closing balances should be added making each summary a complete and balance statement.

Supporting Schedules and forms of the summary statement:

Every summary statement must be accompanied by schedules and the relative forms as indicated in the summary statements.

Preparation of schedules:

Schedule A-1:

When Exp form is certified against purchase of FCS the transaction must be listed in schedule A-1 in triplicate showing the number of Exp form and the amount.

Schedule A-2:

- Advance receipt for goods to be exported this is to be reported through “Advance Receipt Voucher” (Appendix-19 Vol-2)

- Where the duplicate EXP form has already been lodged with the Bangladesh Bank and the triplicate is not available at the time when proceeds are received. This is to be reported through “EXP form not attached voucher” (Appendix-20-Vol-2)

Schedule A-3:

Schedule A-3/0-3 is used to report purchase of F.C. against export to Mayan mar under Bangladesh – Mayan mar Border Trade Arrangement.

Schedule – C:

Currencies purchased from other Ads or branches in Bangladesh to be reported in schedule – C to be attached with relative S-1, S-2, and S-6 statement.

Schedule – G:

Currencies sold to other Ads or Branches in Bangladesh to be reported in Schedule –G to be attached with S-1, S-2, and S-6.

Schedule – D:

FCs Purchased from and sold to Bangladesh Bank to Be reported as Schedule—D.

Schedule-E-2/P-2, E-3/P-3 and EL 1/2/3:

All import transactions to be reported schedule E=2/P-2 and the charges (interest reimburse etc.) there against and other sales other than import traveling, Treatment, Service/ Technical charges etc in Schedule E-3/P-3. Transactions relating to Loans/ Grants will be reported through EL-1/2/3.

Reporting to Inland L/C settlements:

Payment against inland L/Cs in foreign exchange will be reported in summary statement S-1 or sales side as “payment against Inland L/C” and the recipient AD will report the receipt on the purchase side of S-1 as “Receipt in settlement of Inland L/c”.

Date of Submission of statement of Bangladesh Bank:

__________________________________________________________________

1. Operations on private non resident taka Accounts of non –Bank clients

2. Monthly statement of outstanding payment commitments abroad.

3. Commodity Wise statement of imports L/Cs outstanding as on each month end.

4. Monthly statement of outstanding exports bills as of each month end.

Currency wise daily position statements should be kept ready for immediate submission to Bangladesh Bank as and when called for.

Performance of United Commercial Bank Limited in Foreign Exchange Business:

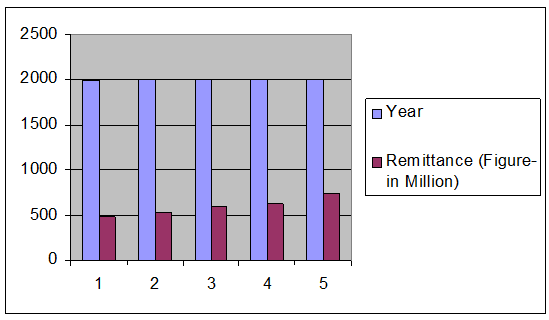

United Commercial Bank Limited has diversified activities in retail banking, corporate banking and international trade. From the very beginning it has obtained a solid foundation in respect of foreign trade. Its total import, export and remittance for the year of 2002 were 14,970.30, 5,620.90 & 735 million taka respectively. The United Commercial Bank limited has established a modern dealing room for foreign trade money management. It has 18 authorized branches out of total so branches for dealing foreign exchanges business. SWIFT has already been introduced and installed at 10 A.D Branches out of 18 to spread up international transactions and parsing of L/Cs and it will be installed at all the A.D branches of the Bank shortly.

The progress of UCBL at a glance:

Fig in million

2000 2001 2002 2003 2004

1. Authorized Capital 1000 1000 1000 1000 1000

2. Paid-up Capital 230 230 230 230 230

3. Reserve Fund 349 394 440 658 783

4. Deposits 12,387 14,246 16,417 17,413 20,970

5. Advances 9,444 10,942 11,826 14,396 15,385

6. Investment 2,163 1,962 3,962 3,022 3,020

7. Gross income 1,402 1,727 1,766 2,197 2,554

8. Gross Expenditure 1,096 1,224 1,311 1,493 1,697

9. Net Profit (pre-tax) 23 175 155 417 626

10. Import Business 12,534 13,133 14,975 18,488 24,386

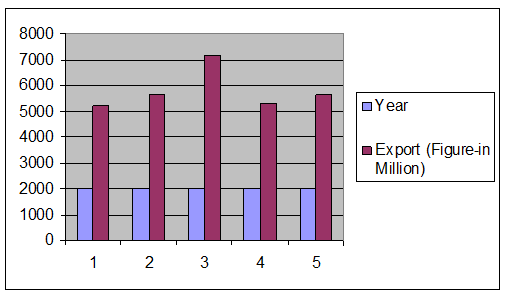

11. Export Business 7,179 5,309 5,621 7,492 10470

12. Foreign Exchange 156 193 256 295 322

13. Number of Employee 1,842 1,812 1,819 1,874 1,878

14. Number of Branch 79 79 80 80 80

15. Number of Shareholders 3,200 3,539 3,943 3,907 3,979

Import Business:

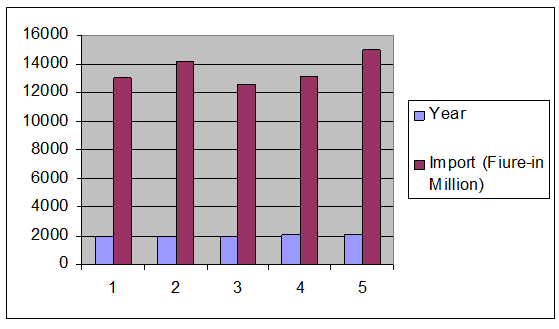

United Commercial Bank Limited has embarked on Extensive foreign exchange with a view to facilitating international trade transactions of the country. The bank has established 8761 Letter of credit for import worth Tk.13132.90 million-during the year 2001.

Table-1

Foreign Exchange Business-Import

_________________________________________________________________

Year Import

(Figure-in million)

1998 13,049.90

1999 14,150.90

2000 12,534.40

2001 13,132.90

2002 14,975.30

__________________________________________________________________