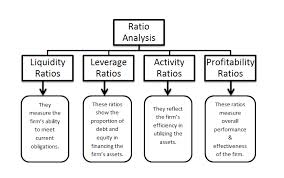

Basic objective of this article is to Discuss and Analysis on Ratio Analysis. Here analysis Ratio Analysis in accounting perception. Ratio analysis is used to estimate relationships among financial statement items. The ratios are used to classify trends over time for one company or to compare two or more companies at one point in time. Here discuss all types of analysis with example and calculation. Financial statement ratio analysis focuses on three key aspects of a business: liquidity, profitability and solvency.

Discuss and Analysis on Ratio Analysis