Executive Summary

Banks are the pillars of the financial system of a country. Specially, in Bangladesh, proper banking system is very important, because the capital market is little developed here. AB Bank Limited has now emerged as a renowned and a reliable financial institution.

A B Bank Limited, the first private commercial Bank under joint venture with Dubai Bank Limited, UAE incorporated in Bangladesh on 31st December 1981. It started its journey as a private commercial Bank from April 12, 1982. But now A B Bank is fully owned by the Bangladeshis. AB Bank Ltd is one of the prominent thirds generation banks in the banking sector. Initially the authorized capital of the bank was Tk 200 million divided into 2 million share of Tk 100 each. The issued and paid up capital was Tk 80 million. As of December 31, 2006; the Authorized Capital and the Equity (Paid up Capital and Reserve) of the Bank are BDT 2000 million and BDT 2582.76 million respectively. The Sponsor-Shareholders hold 50% of the Share Capital; the General Public Shareholders hold 49.43% and the rest 0.57% Shares are held by the Government of the People’s Republic of Bangladesh. However, no individual sponsor shareholder of AB Bank holds more than 10% of its total shares.

I have done my internship on an important branch of A B Bank Limited. My internship report is based on the Deposit Mobilization activities of A B Bank Limited. For this reason, I have worked in the several departments such as, the account opening department, the remittance department, and the clearing department of that branch.

In A B Bank Limited, I found what are the sources they have used to collect their Deposit and what Loan they provide to mobilize they’re found. This is the two basic work that every organization done for earn some profit. A B Bank is first generation bank to mobilize their deposit.

1.0 INTRODUCTION

1.1 Background of the Report:

A Bank is a financial institution whose main objective is the mobilization of fund from surplus unit to deficit unit. In the process of acceptance of deposits and provision of loan, Bank creates money. This characteristic feature sets Bank apart from other financial institution. A Bank can influence the money supply through lending and investment. A Bank is also an economic institution whose main objective is to earn profit through exchange of money and credit instruments.

Commercial Bank is one, which is concern with accepting deposit of money from the public,Repaying on demand or otherwise and withdrawal on demand or otherwise and employing the deposits in the form of loan and investment to meet the financial needs of business and other Classes of society.

Bank is very old institution that is contributing toward the development of economy and an important service provider in the modern world. In the globalization and free market economy, banks provide their service worldwide and compete with other all over the world.

The banking sector is one of the major sectors in Bangladesh economy and can be divided mainly in to four categories-Nationalized bank, Local private bank, specialized financial institution and foreign banks. In Bangladesh, the journey of private commercial banks is not older. The banking in Bangladesh has passed three decades through different policy environment and comprises central bank at the apex.

The country’s central bank, Bangladesh bank, controls and monitors the banking industry.

At present, there are 4 nationalized, 5 are specialized, 30 are local private commercial and 10 are foreign commercial banks. AB Bank Ltd is one of the prominent thirds generation banks in the banking sector.

1.2 Objectives of the report:

The primary objective of this report is to achieve knowledge about how bank mobilize their surplus fund to the deficient units of AB Bank Ltd. Some others important objective of this report are as follows:

– Acquiring experience for future working life.

– To know the operation of commercial banks in Bangladesh.

– To describe the customer service process of AB Bank Ltd.

– To analysis the bank position of Deposit Mobilization.

– To get knowledge about the products and services offered by AB Bank Ltd.

– To analysis how well manage a customer.

1.3 Scope of the study:

The internship program is a partial requirement of the BBA program of the Northern University, Bangladesh. Which construct a relation and build a bridge between the real life state of affairs and theoretical concepts, which were taught in the classroom. After completing my forty threes- (43) courses, it was my great opportunity to get the practical knowledge of the corporate world. That’s why I had to join in the AB Bank Ltd., Islampur Branch and my internship report is based on the practical workings that I have performed.

In Bangladesh today financial sector is one of the most established areas. In the process of forming a good economic system, banks are playing an important role in the country. For this reason I chose to complete my internship with AB Bank Ltd. There I worked for three months as an internee and this report cover the above aspect of the work.

1.4 Sources of information:

The required data and information to prepare the report have been collected from the following sources:

1.4.1 Primary Sources:

- Personal interview with branch officials or executives

- Personal observation.

- Practical desk work

- Getting information from face to face dealing with the client.

- Interviewing the persons who are treated experts in respective to the assignment.

- Customers file study in the Account opening& Loan division.

- Collect financial information from ABBL accounts division.

1.4.2 Secondary Sources:

- Annual report of AB Bank Ltd-2007.

- Web page of A B Bank Ltd.

- Bangladesh bank report.

- Published or unpublished or personally collected data from officers.

- Files and documents of the branch.

- Some articles on banking sectors.

- Different textbooks.

1.5 Limitation of the study:

A B Bank Ltd is a large financial institution, therefore it is not possible to fund out the true picture within a short period. To prepare the report I have to face some problems & limitations. Those limitations are unavoidable for me. That may causes reduction the quality of my report. Those are:

- Time is very limited because in internship responsibility to attain the organization regularly.

- Bank has no formal guidelines for internship.

- Employees are so busy with their work; they have not enough time to cooperate me.

- Bankers don’t want to disclose all necessary information to me, as I am an external.

- Bank does not have sufficient collection of banking related books, journals, assignment and term paper.

2.0 Overview of the organization:

2.1 Historical Background of AB Bank Limited:

AB Bank Limited, the first private sector bank under Joint Venture with Dubai Bank Limited, UAE incorporated in Bangladesh on 31st December 1981 and started its operation with effect from April 12, 1982.

Dubai Bank Limited (name subsequently changed to Union Bank of the Middleast Limited) decided to off-load their investment in AB Bank Limited with a view to concentrate their activities in the UAE in early part of 1987 and in terms of Articles 23A and 23B of the Articles of Association of the Company and with the necessary approval of the relevant authorities, the shares held by them in the Bank were sold and transferred to Group “A” Shareholders, i.e. Bangladeshi Sponsor Shareholders. As of December 31, 2006; the Authorized Capital and the Equity (Paid up Capital and Reserve) of the Bank are BDT 2000 million and BDT 2582.76 million respectively. The Sponsor-Shareholders hold 50% of the Share Capital; the General Public Shareholders hold 49.43% and the rest 0.57% Shares are held by the Government of the People’s Republic of Bangladesh. However, no individual sponsor shareholder of AB Bank holds more than 10% of its total shares. Since beginning, the bank acquired confidence and trust of the public and business houses by rendering high quality services in different areas of banking operations, professional competence and employment of the state of art technology. During the last 25 years, AB Bank Limited has opened 70 Branches in different Business Centers of the country, one foreign Branch in Mumbai, India, two Representative Offices in London and Yangon, Myanmar respectively and also established a wholly owned Subsidiary Finance Company in Hong Kong in the name of AB International Finance Limited. To facilitate cross border trade and payment related services, the Bank has correspondent relationship with over 220 international banks of repute across 58 countries of the World.

AB Bank Limited, the premier sector bank of the country is making headway with a mark of sustainable growth. The overall performance indicates mark of improvement with Deposit reaching BDT 42076.99 million, which is precisely 53.78% higher than the preceding year. On the Advance side, the Bank has been able to achieve 46.32% increase, thereby raising a total portfolio to BDT 31289.25 million, which places the Bank in the top tier of private sector commercial banks of the country. On account of Foreign Trade, the Bank made a significant headway in respect of import, export and inflow of foreign exchange remittances from abroad.

2.2 Vision & Mission:

2.2.1 Vision Statement “To be the trendsetter for innovative banking with excellence & perfection”

2.2.2 Mission Statement “To be the best performing bank in the country”

2.3 CORPORATE STRUCTURE:

- BOARD OF DIRECTORS:

Chairman | Faisal M. Khan |

| Vice-Chairman | Sajedur Seraj |

| Director | D. S. Faisal Hyder Golam Sarwar Mohammad Tipu Sultan, FCA S. M. Salahuddin |

| President & Managing Director | Kaiser A. Chowdhury |

| Company Secretary | Badrul Haque Khan, FCA |

- Executive Committee:

| Chairman | Sajedur Seraj |

Members | D. S. Faisal Hyder Mohammad Tipu Sultan, FCA S. M. Salahuddin Kaiser A. Chowdhury |

| Member Secretary | Badrul Haque Khan, FCA |

- Audit Committee:

| Chairman | D. S. Faisal Hyder |

Members | Sajedur Seraj Golam Sarwar |

Member Secretary | Badrul Haque Khan, FCA |

- Management Committee:

President & Managing Director | Kaiser A. Chowdhury |

| Deputy Managing Director | Niaz Habib Faruq M Ahmed |

Head of Change Management & HRM | M. A. Abdullah |

| Senior Executive Vice President CFO & CS | Badrul H. Khan |

| Senior Executive Vice President & Head of Investment Banking | Fazlur Rahman |

| Executive Vice President & Head of RAM | Akhtar Hamid Khan |

| Executive Vice President & COO | Md. Azad Hossain |

| Executive Vice President & Head of FI & TSY | Abu H M Kamal |

| Senior Vice President & Head of IT | Reazul Islam |

| Vice President & Head of ICCD | Amzad Hossain |

| Vice President & Head | A.B.M. Abdus Sattar |

(Source: ABBL annual Report-2006)

2.4 Corporate Information of AB Bank Limited:

- Name of the Company: AB Bank Ltd

Legal Form: A public limited company incorporated on 31st December 1981 under the Companies Act, 1913 and listed in the Dhaka Stock Exchange Ltd and Chittagong Stock Exchange

Table#01: Corporate event of A B Bank Ltd.

| Commencement of Business: | February27 1982 |

| First meeting of the Board of Directors: | February 5, 1982 |

| Opening of the first Branch (Karwan Bazar Branch): | April 12, 1982 |

| Listing with Dhaka stock Exchange (DSE): | December 28,1983 |

| Publication of prospectus for IPO: | May 5.1984 |

| Subscription for shares starts: | June 25,1984 |

| Opening of principal Branch | January 16,1986 |

| Opening of ABIFL-Subsidiary of Hong Kong | November 1995 |

| Listing with the chittagong stock Exchange | January, 1996 |

| First Foreign Branch at Mumbai, India | April 1996 |

| Launching of ATM | April 12,2002 |

| Operating of Merchant Banking Wing (MBW | November 2 2002 |

| Incorporate of AB Bank Foundation | November 3 2003 |

| Launching of VISA Card | December 23,2004 |

| Operating of Islamic Banking Branch | December 23,2004 |

| Online Share Transaction in CDS | May 7 2006 |

(Source: ABBL annual Report-2006)

Registered Office:

BCIC Bhaban, 30-31, Dilkusha C/A Dhaka 1000, Bangladesh. Tel: +88-02-9560312 Fax: +88-02-9564122, 23 E-mail: info@abbank.com.bd Web: www.abbank.com.bd

Auditors: S.F. Ahmed & Co. Chartered Accountants

Tax Consultant: K.M. Hassan & Co. Chartered Accountants

Legal Retainer: A. Rouf & Associates

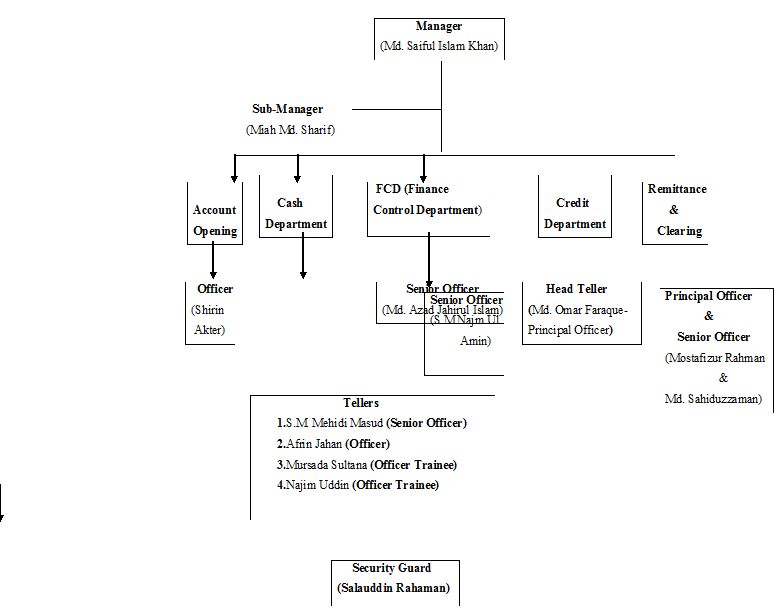

2.5 Organizational Structure at Islampur Branch

2.6 ABBL at a Glance: Year 2006

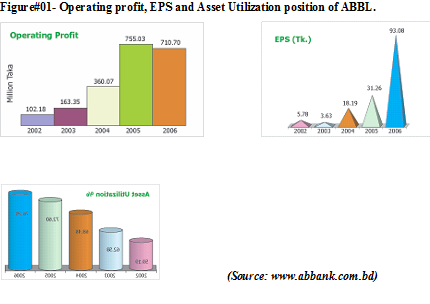

Million Taka | |||||

| December 31 | 2006 | 2005 | % Change | ||

| Gross Interest Income | 3,378.34 | 2,262.95 | 49.29 | ||

| Net Interest Income | 615.50 | 691.41 | (10.98) | ||

| Operating Profit (PBP & T) | 710.69 | 755.03 | (5.87) | ||

| Net Operating Profit (PBT) | 532.19 | 407.45 | 30.61 | ||

| Profit after Tax (PAT) | 532.19 | 162.45 | 227.60 | ||

| Deposit | 42,077.00 | 27,361.44 | 53.78 | ||

| Loans & Advances | 31,289.25 | 21,384.63 | 46.32 | ||

| Total Assets | 47,989.34 | 33,065.40 | 45.13 | ||

| Shareholders’ Equity | 2,582.76 | 1,526.88 | 69.15 | ||

| NIM % | 18.22 | 30.55 | |||

| Non-Interest Income to Operating Income (%) | 76.78 | 56.17 | |||

| Cost Income Ratio | 73.18 | 76.02 | |||

| Return on Equity (%) | 20.61 | 10.64 | |||

| Return on Assets (%) | 1.11 | 0.50 | |||

| Advance Deposit Ratio | 74.36 | 78.16 | |||

| CAR (%) | 9.23 | 9.17 | |||

| NPL (%) | 4.02 | 8.21 | |||

| EPS (Tk.) | 93.08 | 31.26 | |||

(Source: ABBL annual Report-2006)

2.7 Products:

2.7.1 Personal Banking:

2.7.1.1 Current & Short term deposit Account (CD):

Current Account is opened for both individuals and business concerns including non-profit making organization. For opening a personal current account, the account holder must provide his true names, parents names, present and permanent address, date of birth, place of birth, account holder’s two recent passport size color photograph, nominee’s one passport size color photograph, TIN number (if any), Passport or Voter ID or any others employer ID card and certificate from the ward commissioner or union council chairman, Details of occupation or employment and source of wealth or income and an introducer, who has a existing account with ABBL.

The requirement of sole proprietorship account is same as of personal account plus proprietor valid trade license photocopy.

The requirement of partnership account is same as of sole proprietorship account plus partnership deed and mentioned those will provide authority to operate the account.

The requirement of sole limited company account is same as of personal account plus:

- Certificate of incorporation

- Resolution of the board of directors

- Memorandum and articles of association

- Proper information as of personal account of directors and accounts operators

- Certificate of the returns submitted to the register of joint stock companies

- Attestation by embassies or high commissions in the respective countries if the company is incorporated outside of Bangladesh

Also Different club, Co-operative society, private school, college& Madrasa, Trustee board can open current account as per provide their board resolution, Deed of those organization and others document as per types of organization.

2.7.1.2 Saving Account (SB):

Saving account always opened by individual for saving purpose of deposited amount over a period of time. For opening a saving account, a person must provide his true names, parents names, present and permanent address, date of birth, place of birth, account holder’s two recent passport size color photograph, nominee’s one passport size color photograph, Passport or Voter ID or any others employer ID card and certificate from the ward commissioner or union council chairman, Details of occupation or employment and source of wealth or income and an introducer, who already has a account with ABBL.

Interest of a saving account is 6.00%.

2.7.1.3 Fixed Deposit Account (FDR):

Fixed deposit is open by the banker to know the source of income and form of receipt. A FDR account holder must fill a printed from with mention a nominee of account. Account holders also take loan against the FDR deposited amount. Longer period provide higher interest rate in a FDR account.

2.7.1.4 Monthly Saving Deposit (MSDS):

Monthly saving deposit account open for the businessman of Islampur branch for their family member and monthly deposited amount must deposit within 10th banking days of every month and if any one fail to deposit then deposit next with current month installment by provide some fine.

2.7.1.5 Double Deposit Scheme (DDS):

Deposited amount multiple within 6 years and minimum deposited amount is 1 Lac to above.

2.7.1.6 Special Term Deposit (STD):

These types of account also known as special notice deposit and STD account provide interest for minimum balance Tk.5.00 Lac to above and interest rate is 5.00%

2.7.2 Loan Products:

ABBL have categorize their loan product on the basis of the loan security into two types and those loan products that have different terms and conditions that are describe below:

2.7.2.1 Unsecured Loan:

A) Personal Loan:

- Target Customer: Employees of reputed Local Corporate, MNCs, NGOs, Airlines, Private Universities, Schools and Colleges, International Aid Agencies and UN bodies, Government Employees, Self-employed Professionals (Doctors, Engineers, Chartered Accountants, Architects, Consultants), Businessmen

- Purpose: Marriages in the family, Purchase of office equipment / accessories, Purchase of miscellaneous household appliances, Purchase of Personal Computers, Purchase of audio-video equipment, Purchase of furniture

- Loan Amount: Minimum Tk. 25,000.00 & Maximum Tk. 5,00,000.00

- Charges Loan: Application fee: Tk. 500.00,Processing fee: 1% on the approved loan amount or Tk. 2000.00 whichever is higher

- Tenor: Min 12 months and Max 36 months

- Rate of Interest: 14.50% p.a. – 17.50% p.a.

- Security: Hypothecation of the product to be purchased. Two personal guarantees (as per our list of eligible guarantors)

B) Auto Loan:

- Target Customer: Same as Personal Loan.

- Purpose: To purchase Brand new vehicle, non-registered reconditioned vehicle

- Loan Amount: 70% for the brand new car and 60% for the reconditioned car but must not exceed BDT 10,00,000.00

- Charges: Application fee: Tk. 500.00 and Processing fee: 1% on the approved loan amount or Tk. 5000.00 whichever is higher

- Tenor: For Reconditioned Car: Max 36 months and Brand new Car: Max 60 months

- Rate of Interest: 14.50% p.a. – 17.50% p.a.

- Security: Same as personal Loan.

C) Gold Grace (Jewellery Loan):

- Target Customer: The loan is specially designed for salaried women who are employed in different reputed companies

- Purpose: To purchase ornaments/Jewellery for personal use

- Loan Amount: Minimum Tk. 50,000.00 & Maximum Tk. 3,00,000.00

- Charges: Application fee: Tk. 500.00 and Processing fee: 1% on the approved loan amount or Tk. 1000.00 whichever is higher

- Tenor: Min 12 months and Max 36 months

- Rate of Interest: 16.00% p.a.

- Security: Letter of confirmation from the employer. Personal guarantee from the parents and spouse (if married)

D) Easy Loan (For Executives):

- Target Customer: The loan is specially designed for salaried people who are employed in different reputed companies

- Purpose: Marriages in the family, Purchase of office equipment / accessories, Purchase of miscellaneous household appliances, Purchase of Personal Computers, Purchase of audio-video equipment, Purchase of furniture, Advance rental payment, Trips abroad, Admission/Education fee of Children etc

- Loan Amount: Minimum Tk. 50,000.00 & Maximum Tk. 3,00,000.00

- Charges: Application fee: Tk. 500.00 and Processing fee: 1% on the approved loan amount or Tk. 1000.00 whichever is higher

- Tenor: Min 12 months & Max 36 months

- Rate of Interest: 16.00% p.a.

- Security: Letter of confirmation from the employer. One personal guarantee (as per our list of eligible guarantors)

E) Staff Loan:

- Target Customer: All permanent employees of ABBL

- Purpose: Marriages in the family, Purchase of office equipment / accessories, Purchase of miscellaneous household appliances, Purchase of Personal Computers, Purchase of audio-video equipment, Purchase of furniture

- Loan Amount: According to the debt burden ration and other criteria

- Charges: Processing fee: 1% on the approved loan amount

- Tenor: Min 12 months & Max 36 months

- Rate of Interest: 15.50% p.a.

- Security: Hypothecation of the product to be purchased

F) Education Loan:

- Target Customer:

Students Criteria: • Students of reputed Educational Institutes, such as Public & Private Universities, Medical Colleges & Engineering Institute. • Undergraduate & Post graduate Level • Professionals degrees (Chartered Accountants (CA), Cost & management Accountants (CMA), Marine, MBM, MBA) • Doctorate degree (PhD), FCPS etc. • Occupation: Student • Minimum Age: 17 years • Maximum Age: 40 years • Educational Qualification: Minimum HSC/A-Level Pass. Parents Criteria: Service Holder: • Individuals with ranks equivalent to Senior Assistant Secretary or higher would qualify guarantor • Bank officials (Equivalent to Senior Principal Officer of NCBs, AVP / Branch Manager of Local and Foreign banks) and Department Head of Multinational Company or established Local Corporate. Guarantors must be accepted by the Branch Manager / Head Office. Businessman: • well reputed and widely respected Self-employed professionals

- Purpose: To Financially Assist The Parents: Admission/Education Fees, Semester Fees, Study abroad

- Loan Amount: Minimum Tk. 50,000.00 and Maximum Tk. 3,00,000.00

- Charges: Application fee: Tk. 500.00 Processing fee: 1% on the approved loan amount or Tk. 1000.00 whichever is higher

- Tenor: Min 12 months & Max 36 months

- Rate of Interest: 14.50% p.a. – 16.00% p.a.

- Security: One personal guarantees (as per our list of eligible guarantors)

G) House/Office Furnishing/Renovation Loan:

- Target Customer: Expatriate Bangladeshi nationals who are in business or service holders. Employees of reputed Banks & Leasing companies reputed Local Corporate, MNCs, NGOs, Airlines, Private Universities, Schools and Colleges, International Aid Agencies and UN bodies. Government Employees. Self-employed Professionals (Doctors, Engineers, Chartered Accountants, Architects, Consultants). Reputed and highly respectable Businessmen with a reliable source of income

- Purpose: House/Office Furnishing/ Renovation, For interior decoration / Titles Stones, Electrical fittings, wooden cabinets / Overall furnishing and all types of House/Office Renovation, purchase/furnishing of apartments etc

- Loan Amount: Minimum Tk. 1,00,000.00 & Maximum Tk. 10,00,000.00

- Charges: Application fee: Tk. 500.00 Processing fee: 1% on the approved loan amount or Tk. 2000.00 whichever is higher

- Tenor: Min 12 months & Max 48 months

- Rate of Interest: 16.50% p.a.

- Security: Title deed of the House/Office to be furnished/renovated along with memorandum of deposit of title deed duly supported by a notarized power of attorney to be kept by the bank as a matter of comfort. Two personal guarantees (as per our list of eligible guarantors). Registered mortgaged of the property if the loan amount is more than Tk. 5.00 lac

2.7.2.2 Secured Loans:

A) Personal Loan:

- Target Customer: To meet personal requirement of fund

- Loan Amount: Maximum 95% of the present value of the security

- Charges: Processing fee: TK. 1000.00

- Tenor: Min 12 months & Max 36 months

- Rate of Interest: 13.50% p.a. – 16.50% p.a. (subject to type of the security). 2% spread must be maintained in case of own bank FDR

- Security: Lien over FDR, BSP, ICB Unit Certificate, RFCD, NFCD, CD account(s) etc. One personal guarantee in case of third party cash collateral (as per our list of eligible guarantors)

B) Personal Overdraft:

- Ø Target Customer: All Clients of ABBL

- Ø Purpose: To meet personal requirement of fund

- Ø Loan Amount: Maximum 95% of the present value of the security

- Ø Charges: Processing fee: TK. 1000.00

- Ø Tenor: Revolving with annual review

- Rate of Interest: 13.50% p.a. – 16.50% p.a. (subject to type of the security). 2% spread must be maintained in case of own bank FDR

- Security: Lien over FDR, BSP, ICB Unit Certificate, RFCD, NFCD, CD account(s) etc. One personal guarantee in case of third party cash collateral (as per our list of eligible guarantors)

2.8 Services:

2.8.1 Non-Resident Bangladeshi (NRB) Banking:

Facilities offered to NRBs:

- Opening of Foreign Currency A/C: ABBL open Foreign Currency Account for NRBs and Foreign Currency can be remitted by the Nationals of Bangladesh living abroad earned as wage earners or from other sources. The deposit amount can also be used for remittance to other countries as per their requirement. Nominee of Account holder can also able to operate this Account.

- NFCD: ABBL issued Foreign Currency Fixed Term Deposit with different tenure. Interest is paid in respective Foreign Currency. Rates of Interest are published in our daily Exchange Rate.

- Wage Earners Development Bond: These Bonds can be issued from the balance of the FC account with tenure for five years. Rate of interest is 12% p.a. in BDT.

- USD Premium Bond: These Bonds can be issued from the balance of the FC account with tenure for Three years. Rate of interest is 7.5% p.a. in BDT

- USD Investment Bond: These Bonds can be issued from the balance of the FC account with tenure for Three years. Rate of interest is 6.5% p.a. in USD. In addition to the above, ABBL also have Drawing Arrangements with 14 (Fourteen) Exchange/Money Transfer Remittance Houses all over the globe to facilitate fast, reliable and hassle-free inward remittance to the expatriate Bangladeshis around the world. ABBL also have special arrangements to credit Beneficiary’s account maintained with their valuable customer on the same day through our extensive real time on-line network.

2.8.2 Islamic Banking:

To provide the Islamic banking services in accordance with the principles of Islamic Shariah, AB Bank has established Islamic Banking Wing and started it’s functioning by opening full-fledged Islamic banking branch on 23.12.2004. The branch is known as AB Bank Islami Banking Branch, Kakrail, and is situated at 82, Kakrail, Ramna, Dhaka. Prominent Islami Banker Mr. M. Azizul Huq has joined the Bank as its Islamic Banking Consultant. A dedicated team of experienced Islamic bankers is working under his active guidance both at head office and branch level. A competent Shariah Council consisting of Islamic scholars, Ulema, Fukaha and Islamic bankers headed by Mr. Shah Abdul Hannan, a prominent Islamic scholar and former Secretary, Government of Bangladesh has also been formed to guide the Islamic banking affairs. Board of directors as well as management of the bank are very much interested to promote Islamic banking system in the bank aiming at opening more Islamic branches in the near future. AB Bank has already obtained membership of Islamic Banks Consultative Forum (IBCF) and Central Shariah Board for Islamic Banks of Bangladesh. The goals and objectives of Islamic banking Wing are as under:

- To facilitate the Islamic banking system in the country

- To create new entrepreneurs and to arrange required finance for them

- To play effective role for socio economic development of the country

- To give assistance in launching welfare oriented economic system under Islamic values

Under this wing AB Bank extends the following Islamic banking services:

- Deposit services

- Investment services

Under Deposit services the following services are being rendered:

- Mudaraba Savings Account

- Mudaraba Short Noticed Account

- Mudaraba Term Deposit Account (with different terms)

- Mudaraba Monthly Profit Account

- Al-Wadiah Current Deposit Account

- Mudaraba Deposit Pension Scheme

Besides Mudaraba Hajj Deposit Scheme and some other schemes are under process.

Investment Services: AB Bank Islamic Banking Wing provides investment facilities for project finance, working capital finance, SME finance, consumer / retail baking finance etc. under following modes:

Foreign Trade: Islamic Banking Wing provides the following services at its foreign trade desks:

- Opening of LCs

- Post -Import Finance

- Export bill purchase and negotiation

- Pre-shipment financing etc.

AB Bank Islamic Banking Wing has been continuously trying to expand its service horizon keeping the necessity of valued clients in view and upholding the principle of Islamic Shariah.

2.8.3 Investment Banking:

Merchant Banking Wing (MBW)

AB Bank Limited is the first Private Sector Joint Venture Bank in Bangladesh, which is now fully owned by the Bangladeshis. Since our inception in 1982, we have been participating in different industrial and national development activities in addition to normal Trade Finance and SME development. In addition to the 70 Branches within the country ABBL has a branch in Mumbai, India. Beside that ABBL have a wholly owned Finance Company in Hong Kong in the name and style of “AB International Finance Limited” and representative offices at London and Yangoon. To expand its horizon, ABBL launched its Merchant Banking operations in the year 2003. As a full-fledged merchant banker, we provide the following services:

- Portfolio Management

- Issue Management

- Underwriting

- Corporate Advisory

- Bankers to the Issue

- Private Placement

The Merchant Banking Wing (MBW) of ABBL has made notable progress and is presently equipped to serve customers’ needs by offering a comprehensive range of financial solutions. ABBL have also launched Custodial Services with a view to provide one-stop Capital Market services to our valued clients. ABBL understand an entrepreneur’s need for stability, trust, innovation and creativity required for the consolidation and growth of investments and endeavor to prosper. The professionals in ABBL MBW with its state of the art integrated computerized system, are always there to provide their vision, knowledge and service for customer success.

ABBL measure their success by the number of satisfied customer within a time frame.

2.8.4 Custodial Service

Target Customers: Investors who are interested to invest in the Bangladesh Capital Market

• Non Resident Bangladeshi (NRBs) • Foreign Institutional and individual clients • Local Institutions • Sponsors’ group and High net worth client Services: • Safe custody of client securities • Foreign Trade Execution and Settlement • Share transfer in the name of client • Complete the Dematerialization process as per client request • IPO, Private Placement & Right share subscription as per client instruction with deposit • All types of corporate action that includes cash dividend, bonus share and right share collection • Open BO account • Instant information regarding client securities position as per their request

• Quarterly reporting to the client by Custodial Department

2.8.5 Corporate Banking:

ABBL provide completes range of solutions to meet Corporate Customers’ requirement. Their Corporate Banking solutions include a broad spectrum of products and services backed by proven, modern technologies. Corporate Lending ABBL specialist teams offer a comprehensive service providing finance to large and medium-sized businesses based in Bangladesh. For more information as to how they might best meet customer corporate debt needs, please contact at Corporate Head Office of ABBL. Structured Finance ABBL have a specialist Structured Finance Team they arrange and underwrite finance solutions including Debt and Equity Syndication for financial sponsors, management teams and corporate. Also ABBL provide corporate advisory services. ABBL aim to provide tailored financing solutions with a dedicated team that can rapidly respond to client needs. Following are some of the products and financial tools of Corporate Banking:

- Project Finance

- Working Capital Finance

- Trade Finance

- Cash Management

- Syndicated Finance, both onshore & off-shore

- Equity Finance, both onshore & off-shore

- Corporate Advisory Services

2.8.6 Large Loan & Project Finance:

- In order to cater the demand of client ABBL has segmented its portfolio in terms of loan size. As per this segmentation any loan over Tk. 10.00 Crore falls under the purview of Large Loan Unit.

- In ABBL, there is also a separate Project Finance unit who evaluate the business. The unit is entrusted to handle the portfolio in a focused manner. AB Bank is always in fore front to support establishment of new projects of diverse nature, which will help to broaden the manufacturing arena vis-à-vis to generate to employment.

- At the moment ABBL ‘s exposure in Large Loan & Project Finance portfolio is distributed in the following sectors:

Table#02 Different sectors for Loan and Project Finance:

| SL | Sector | ABBL Exposure (Limit) (Fig. In Lac Tk.) |

| 1 | Agro- Business | 12,717.56 |

| 2 | Cement Power, Glass | 38,691.92 |

| 3 | Consumer Products | 21,855.00 |

| 4 | Edible Oil | 36,057.53 |

| 5 | Engineering & Construction | 18,106.42 |

| 6 | Financial Institution | 1,414.70 |

| 7 | Food & Beverage | 27,044.24 |

| 8 | Hotel | 2,505.26 |

| 9 | Health Care | 3,928.62 |

| 10 | Printing & Packaging | 11,867.61 |

| 11 | Real Estate | 10,451.49 |

| 12 | Micro-finance | 5,763.15 |

| 13 | Export | 9,441.63 |

| 14 | RMG & Backward Linkage | 94,826.13 |

| 15 | Ship Breaking | 18,029.20 |

| 16 | Steel | 42,824.97 |

| 17 | Telecom & Computer Accessories | 11,479.89 |

| 18 | Trading | 77,579.89 |

| Total (including syndicated exposure) | 444,585.21 | |

| Less Syndicated Exposure | 51,560.29 | |

| Total Large Loan & Project Finance portfolio without syndicated exposure | 3930,24.92 |

(Source: www.abbank.com.bd)

2.8.7 Loan Syndication:

- Syndication or club financing is a growing concept in Banking Arena of Bangladesh. Syndicated finance diversifies the risk of one bank on a single borrower and increases the quality of loan through consensus or cumulative judgment and monitoring of different banks / financial institutions.

- ABBL, the first bank in the private sector also took initiative to adapt to this growing concept.

- In 1997, ABBL for the first time arranged a club financing with Dhaka Bank Ltd to raise Tk. 6700 lac – out of which ABBL financed Tk. 5700 Lac and Dhaka bank financed Tk. 1000 Lac.

- In 1999, ABBL arranged its second syndicated credit facility with IPDC to raise Tk 3563 Lac.

- Since then ABBL did not look back.

- Since 1997 to 2008, ABBL has raised total Tk. 25989.56 Lac as Lead Arranger. The following banks from time to time have been our partners in these syndications: Dhaka Bank, IPDC, EXIM Bank, Bank Asia, Oriental Bank (Now ICB Islamic Bank), NCC Bank, The City Bank, Trust Bank, Bank Asia.

- ABBL has also participated in different syndications arranged by other Banks, out of which till date 6 (six) syndication has successfully been completed. ABBL exposure in these completed syndications was Tk. 4700 Lac.

- At the moment ABBL has participation in 19 (nineteen) syndicated facilities that exposure in the ongoing syndication of 2008 is Tk. 51560.29 Lac which is diversified in the following ten sectors:

Table#03 Sector for providing syndicate Loan:

| SL | Sector | ABBL Participation (Fig. In Lac Tk.) |

| 1 | Textile | 9,533.57 |

| 2 | Micro-finance | 3,000.00 |

| 3 | Cement | 7,990.00 |

| 4 | Energy & Power | 11,997.00 |

| 5 | Telephone (PSTN) | 5,500.00 |

| 6 | Glass | 900.00 |

| 7 | Sugar | 900.00 |

| 8 | Steel Mills | 9081.72 |

| 9 | Paper | 1158.00 |

| 10 | Chemical | 1,500.00 |

| Total | 51,560.29 |

(Source: www.abbank.com.bd)

2.8.8 Money Transfer:

Western Union- A fast, reliable and convenient way to send a money transfer Western Union Financial Services Inc. U.S.A. is the number one and reliable money transfer company in the world. This modern Electronic Technology based money transfer company has earned worldwide reputation in transferring money from one country to another country within the shortest possible time. AB Bank Limited has set up a Representation Agreement with Western Union Financial Services Inc. U.S.A. Millions of people have confidence on Western Union for sending money to their friends and family. Through Western Union Money Transfer Service, Bangladeshi Wage Earners can send and receive money quickly from over 280,000 Western Union Agent Locations in over 200 countries and territories world wide- the world’s largest network of its kind, only by visiting any branches of AB Bank Limited in Bangladesh.

For Inward Remittance, AB Bank established extensive drawing arrangement network with Banks and Exchange Companies for provide foreign remittance through exchange house those are located in the important countries of the world.

2.8.9 Cards:

In the present context of banking business in the world, Card is the future of any bank. Electronic payment system is now ruling the world and some days from now cash transactions system will turn into a history found only in the textbook. AB Bank Limited is one of the leading first generation private sector commercial banks with Branch Network all over the country. The Bank started issuing VISA Credit Cards from the end of year 2004 as a principal member of VISA International. Brief description of different features:

- Card Conversion & Balance Transfer Plan: ‘Card Conversion & Balance Transfer Plan’ to AB Bank Ltd. VISA Credit Card will be extended towards all local Credit Cardholders of the market, provided that their ‘other banks’ credit card is in ‘regular’ state, not in ‘overdue’ state. Cardholders will repay the approved transferred amounts to AB Bank Ltd. Credit Card Account in monthly installments stated in their monthly statements. Other bank credit cardholders having regular payment history will also be allowed to apply for this facility along with their new AB Bank Ltd. Credit Card application form. You can convert your other bank card to AB Bank Ltd. Card and get interest facility @ 19.95% on your outstanding.

- Easy Buy ‘Easy Buy‘ Installment Plan to AB Bank Ltd. VISA Credit Card will be extended towards all AB Bank Ltd. Visa Credit Cardholders. Cardholders can convert any retail purchase done using AB Bank Ltd. credit card into an installment scheme where they can pay back the amount at rate of interest of 19.95% per annum over a tenor ranging from 6 months to 48 months

- Easy, convenient and affordable Under the Easy buy program, cardholder can choose own installment plan, ranging from 6 to 48 months.

- Simple procedure, no documentation, no down payment

- Available in comfortable payment options of 6 months to 48 months

- Process just a call away

- No cash advance fee No cash advance fee for cash withdrawal from AB Bank Ltd. ATM Booths & Tk.10 only per cash withdrawal will be charged from other Q Cash ATM booths. Market rate is Tk. 125 per cash withdrawal.

- Auto bills pay facility Hassle free monthly payment from AB Bank Ltd. Account holders.

- Higher transaction limit AB Bank Ltd. VISA card gives you the facility to withdraw up to Tk. 60,000 or 50% of your credit limit (whichever is lower) of the credit limit from any ATM with Visa logo. Lot more features are in the pipeline to add more value to satisfy AB Bank Ltd. customers.

2.8.10 SME Banking:

SME Loan Considering the volume, role and contribution of the SMEs, in the last two decades ABBL has been patronizing this sector by extending credit facilities of different types and tenor. As of now 54% of the bank’s total loan portfolio is segmented to the SMEs which deserve all out attention in our plans, projections and forecasting.

As such the bank has emphasized on the following issues:

- To provide the best services to the SME sector

- To increase the SME portfolio of ABBL significantly

- To improve the quality of ABBL’s portfolio

SME Sectors in which ABBL has participated :

- Agro machinery

- Poultry

- Animal Feed

- Dairy Product

- Fruit Preservation

- Hotel & Restaurants

- Garments Accessories

- Leather products

- Plastic product

- Furniture: Wooden & Metal

- Ink

- Paint

2.8.11 Cordial Interaction Maintenance with customer:

As a bank is a service oriented organization, which closely deals with customer and bank employees have maintained cordial interaction with customer. There are some active step to maintained good relationships that is followed by ABBL, that are given below:

- Proactively greet each customer and to be friendly with them

- Listen carefully and with full attention.

- Handle their queries fast-efficiently and professionally.

- Make sure that confidentially and privacy is maintained always.

- Have a real smile on face and keep a natural eye contract.

- Handle clients without interruptions.

- Not talk over phone keeping customer in front.

- Maintain a perfect sitting position in front of customer.

- Make a fast body movement; not a lazy, sleepy.

- Conclude with the talking statements.

- Encourage the customers to use bank’s automated facilities.

- Try to use customer’s name whenever possible.

- Give priority attention and care to any old or physically disabled customer

- Apologize for any delay or omission.

- Be soft spoken even if the customer gets angry and agitated.

- Offer a solution and clearly tell the steps which will be taken to solve his or her problems.

2.9 Performances:

2.9.1 Online Banking:

Being the first private sector Bank of the country, ABBL has prided itself in the quality of the banking services it provides by taking conscious decision to employ the best available banking technology to serve the customers, which now stands over 200,000 in all. Core Banking System Kapiti was employed along side the manual banking operations ever since 1984. Later on in the year 2004, Misys core banking solution was selected for implementation to take ABBL in to super highway of real time online banking of today. Beginning, 2005 Misys implementation was taken-up and in the 1st Phase seven (7) Branches were upgraded to the new core banking system. For the year 2006, in line with the growth strategy, service quality improvement and availability were put into focus where upon coverage of remaining Branches under Misys became all the more important. Bank took up a massive Project of migration, connectivity and standardization of processes and hardware throughout. A CORE TEAM was formed. The theme was YES WE CAN. We made it possible.

Core Banking Software: Equation Banking System (EBS) Misys Equation is a fully integrated, real-time, multi-currency retail banking solution that helps organizations deliver competitive products and excellent service to customers. It supports consumer and corporate banking as well as treasury operations on a single platform.

Front End Software: Equation Branch Automation (EBA) Equation Branch Automation is designed to support customer-facing staff within a retail branch-banking environment. The Equation Branch Automation system is already tightly integrated with the Equation core-banking server, and provides ready-to-run functionality to support cashiers, personal bankers and relationship managers. Equation Branch Automation allows online, real-time transaction processing for the Equation Banking Server, with immediate access to account and transaction information and verification of availability of funds.

Reporting software: Web Form Web form applies the latest web-based technology to the Equation banking system. Reports are automatically captured and delivered to users as web pages over the bank’s internal network, removing the need to print and distribute paper versions of reports. Report data is available as web pages, as Excel spreadsheets, and for analysis using multi-dimensional PivotTables. Reports can also be distributed automatically as emails, enabling people who do not have direct access to the system to be kept informed with the latest data.

2.9.2 Operating Performance:

Board of Directors of AB Bank Limited (ABBL) takes immense pleasure in presenting the 25th Annual Report of the Bank to their valuable shareholders. ABBL is also the privilege of the Board to present the audited accounts of the Bank for the year ended 31st December 2006 and the Auditors’ Report thereon.

ABBL reached a milestone on 12th of April 2007 when ABBL reached 25 years of its journey, which started with a single Branch operation at Karwan Bazar, Dhaka way back in 1982. ABBL being the pioneer in private sector banking in Bangladesh will be the first to achieve this milestone. Over the years, ABBL has contributed in many ways towards development of the private sector banking in the country. Many of the big industries in different fields of the economy have ABBL name attached and remains a proud development partner of these industrial houses over the years. ABBL thrived on customer service and relationship banking which brought new a dimension to this particular service sector and many more new entrants to banking sector followed ABBL. ABBL Sponsors set a vision for the Bank, which reads: “To be the Trendsetter for innovative banking with excellence and perfection”. Throughout these 25 years, ABBL raised the bar for itself through services, initiatives, products, customer support and performance towards that visionary path.

3.0 DEPOSIT:

People can ensure safety of their money and easy to collect their deposited money from any where of the country by uses on-line banking.

3.1 TYPES OF DEPOSIT:

There are many type of deposit at AB Bank Ltd. Islampur Branch. Those are given below:

- Current & Short term deposit Account (CD)

- Saving Account (SB)

- Fixed Deposit Account (FDR)

- Monthly Saving Deposit (MSDS)

- Double Deposit (DDS)

- Special Term Deposit (STD)

3.1.1 Current & Short term deposit Account (CD):

Current Account & short team mostly prefer by businessmen for their frequently transaction with in day. This account balance most change frequently than other types of account because customer can withdraw and deposit as many times they wish in the daily banking hours. There are some steps that customers follow to open a Current & Short term deposit Account (CD) with AB Bank Ltd. that are givens bellows:

- ABBL Current & Short term deposit Account (CD) meets the needs of individual and commercial customers with their attractive benefits

Minimum balance: TK-10000/-

- ABBL Current & Short term deposit Account (CD) account maintenance charge for every six month is TK.300/-

- Account closing charge is TK.300+ VAT 15%

- Withdrawal of money is permitted through the leaves of the chequebook issued by the bank in any branch.

Customer Benefits:

- Chequebook facility.

- Collect foreign remittance through Western Union money transfers.

- Online facility to transfer of any amount of fund to any branch with some charge.

- Deposit other bank cheques through clearing house.

- Opportunity to apply for safe deposit locker services.

In my three-month internship I was able to collect ABBL last 03 months Current account (CD) deposit information. Those are as follows:

Table# 04 Three-month of 2008, current account position of ABBL (ISLP):

Month | Number of Current Account | Deposited amount (In TK) |

| March- | 432 | 71812624.48 |

| April- | 438 | 74517175.31 |

| May- | 455 | 77515520.45 |

(Source: The official document in ABBL, Islampur Branch)

This graph shows increase number of current account holders in A B Bank Ltd, Islampur Branch for their good service for the cloth & Textile, Medicine, Chemical Business man and ABBL Islampur Branch declare the month of May is the deposit mobilization month of the branch. So they have taken some step to increase their account holders.

3.1.2.Saving Account (SB):

Retail customers always prefer saving account those who transaction amount less than current account. In Islampur branch most businessman open saving account for their family members. There are some rules and regulations to open a saving account is as follows:

- Any person or persons of more than 18 years having sound mind can open and operate this account singly and jointly.

- Minimum initial deposit is TK.5000/-

- Provide interest at the rate @7% per month.

- Maintenance charge for every six month is TK.250/-

- Withdrawal cannot be twice TK.20000/- in a month.

The ABBL Saving A/C has the following position in three months during my Internship period that are follows:

Table# 05 In three-month of 2008, Saving Account position of ABBL (ISLP):

Month | Number of Saving Account | Deposited amount (In TK) |

March- | 321 | 16413637.64 |

April- | 326 | 13313380.90 |

May- | 335 | 17515520.45 |

(Source: The official document in ABBL, Islampur Branch)

Saving account graph show in March to April, there are some amounts of deposit for saving account has decrease but increase in the next month that is some more than the month March.

Saving account most preferable those who have small amount of income and their business transaction are small amount.

3.1.3 Fixed Deposit Account (FDR):

Fixed Deposit Account provide higher rate of return and that types of prefer businessman to save money for future investment in their business. ABBL provide Loan against such types of FDR.

Table#06 In three-month of 2008, FDR account position of ABBL (ISLP):

Month | Number of FDR Account | Deposited amount (In TK |

| March | 152 | 24303708.90 |

| April | 159 | 24507326.84 |

| May | 165 | 24665230.50 |

(Source: The official document in ABBL, Islampur Branch)

The FDR account in three-month consciously change one month to another for the better customer service of ABBL Islampur Branch.

AB Bank offers fixed term deposit account on different interest rate of different period of times.

Table#07 FDR Rate of ABBL:

| Time Period | Range of Amount | Interest Rate |

| 15 Days | 1,00,00,000 & Above | 10.00% |

| 1 Months | 50,00,000 & Above | 12.00% |

| 3 Months | 50,00,001 to 10,00,000 10,00,001 to Above | 11.75% 12.25% |

| 6 Months | 50,00,001 to 10,00,000 10,00,001 to Above | 12.00% 12.50% |

| 1 Years | 50,00,001 to 10,00,000 10,00,001 to Above | 12.50% 13.00% |

| 2 Years | 12.75% |

(Source: the official document in ABBL, Islampur Branch)

3.1.4 Monthly Saving Deposit (MSDS):

AB Bank introduces a new Monthly Saving Deposit scheme “AMAR SHOPNO” for the segment of the population who seek an assured monthly earning. This is help to build your fortune and found your future, one step at a time. This time saving deposit scheme that provides individuals to create a saving pool, which allows them, access to a substantial amount at the end of a tenure to materialize their dreams.

Under this plan one can maintain accounts with deposits ranging from TK.500.00 and it multiple to a maximum of TK.5000.00 per month per account or in multiple accounts. The tenure can be of either 5 or 10 years.

Table#08 In three-month of 2008, MSDS account position of ABBL (ISLP):

| Month | Number of MSDS A/C | Amount of Deposit (In Tk) |

| March | 200 | 5612032.62 |

| April | 217 | 5779157.32 |

| May | 235 | 6253212.25 |

(Source: the official document in ABBL, Islampur Branch)

In ABBL Islampur Branch, Some businessman opens MSDS for there family members and those who have small income of employee are open MSDS. In those three-month consciously increase MSDS A/C deposit.

Term and condition of a MSDS Account:

- Account shall come into effect from the 1st week of the month. Account may be opened any day of the month in which case the effect will be from subsequent month.

- Monthly deposit has to be within first 10 days of the month

- A person can maintain multiple accounts for different amount of deposits at any branch

- Depositor can pay installments through any branch of the bank by paying a normal service charge.

- Loan may be allowed up to 75% of the deposit amount against lien/ pledge of the same account. (Minimum loan amount shall not be less than tk.15,000/-)

- Standing including can be given by the depositors to the branch concerned to pay regular installment from his/ her CD/SB account maintained with the branch through payment of Tk. 10.00 service charge per transaction. Clause 6 shall also apply.

- A Fee of Tk.5.00 will be charged along with the installment for late deposit on every Tk.500/-.

Table#09 After Maturity payable value table of MSDS:

Monthly Deposit | After 5 Years | After 10 Years |

| Tk. 500.00 | Tk. 38,388.00 | Tk. 94,786.00 |

Tk. 1000.00 | Tk. 76,776.00 | Tk.189, 572.00 |

| Tk. 1,500.00 | Tk. 115,164.00 | Tk. 284,358.00 |

| Tk. 2,000.00 | Tk. 153,552.00 | Tk. 379,144.00 |

| Tk. 2,500.00 | Tk. 191,940.00 | Tk. 473,930.00 |

| Tk. 3,000.00 | Tk. 230,328.00 | Tk. 568,716.00 |

| Tk. 3,500.00 | Tk. 268,716.00 | Tk. 663,502.00 |

| Tk. 4,000.00 | Tk. 307,102.00 | Tk. 758,288.00 |

| Tk. 4,500.00 | Tk. 345,452.00 | Tk. 853,074.00 |

| Tk. 5,000.00 | Tk. 383,880.00 | Tk. 947,860.00 |

(Source: the official document in ABBL, Islampur Branch)

3.1.5 Double Deposit Scheme (DDS):

Double Deposit can only open in the personal name. ABBL offer only 6 (six) years duration double deposit scheme for their customer. The limit of deposit is 100000 to above.

Table#10 In three-month of 2008, DDS account position of ABBL (ISLP):

| Month | Number of DDS A/C | Amount of Deposit (In Tk) |

| March | 8 | 3114660.42 |

| April | 10 | 3212550.45 |

| May | 14 | 3522230.35 |

Figure # 07 DDS Account Flow Chart:

(Source: the official document in ABBL, Islampur Branch)

The ABBL Islampur Branch Have small number of DDS account but that change continuously from one month to another months for their better performance for the valuable customers.

3.1.6 Special Term Deposit (STD):

This is the special term deposit for ABBL customers. These types of account require more balance than any types of account to get interest at the rate of 6%.

Table#11 In three-month of 2008, STD account position of ABBL (ISLP):

| Month | Number of STD A/C | Deposit Amount (In Tk) |

| March | 33 | 15490042.53 |

| April | 36 | 18294562.63 |

| May | 41 | 19223525.25 |

(Source: the official document in ABBL, Islampur Branch)

The ABBL Islampur Branch has some STD account and those types of account increase day by day. Many businessman those have transaction value is higher. March to May, STD account are increasing in the same portion.

3.2 Prerequisite of opening an account:

Account Opening Document Checklist:

A) Individual and Joint Account

- Bank’s prescribed Account opening application form to be signed by the applicant.

- Two Passport Size Photograph of the Account holder(s) attested by the introducer.

- Specimen Signature Card also to be signed by the applicant.

- Estimated Transaction Profile and

- Any of the following Identification Documents

Table#12 Account opening document list:

| Name of Identification Document | Issuing Authority |

| Current valid passport | Passport Office |

| Valid driving license | Bangladesh Road Transport Authority |

| Voter ID Card | Election Commissioner |

| Armed Forces ID card | Employer or their delegate |

| A Bangladeshi employer ID card bearing the photograph and signature of the applicant | Employer or their delegate |

| A certificate from any local government organs such as Union Council chairman, ward commissioner etc. | UP Chairman / Ward Commissioner |

| Trade license with photograph can be accepted for individual’s identification | Local Govt Authority / UP Chairman Pourashava Chairman / Ward Commissioner |

The idea is any document showing photograph, signature and address of the customer issued from a dependable authority (Managers and Supervisors have to apply judgment) are acceptable.

All photocopies should be verified with the original and attested by an authorized officer of the Bank.

Particular care should be taken in accepting documents, which are easily forged, or which can be easily obtained using false identities.

B) Sole Proprietorship Account

- Bank’s prescribed Account Opening application form to be signed by the applicant.

- Two Passport Size Photograph of the Proprietor attested by the introducer

- Specimen Signature Card to be signed by the applicant.

- Copy of valid Trade License issued by Local Government authority (City Corporation, Pourashava, Union Parishad etc.)

- Permission from Bangladesh Bank (For Buying House, Indenting or other specific businesses)

- TIN issued by Income Tax Authority.

- The personal identity of the proprietor of the Firm has to be established by any of the documents as mentioned in Individual or Joint Customer category. If the Trade License carries the photo and signature of the Proprietor this is not required.

C) Limited Company Account

- Bank’s prescribed Account Opening application form.

- Certified copy of the Memorandum & Articles of Association of the Company

- Certificate of incorporation

- Certificate of commencement of Business (For Public Limited Companies only)

- Extract of the Board resolution sanctioning the account opening and signing authority

- List of the Director with address in form.

- Photograph of the signatories

- Copy of valid Trade License

- Introducer’s signature in the A/C opening form and at the back of the photograph(s) of Account holder(s).

- List of names with Appointment letter and Specimen Signature of the Persons authorized to operate the Account.

- The personal identity of all the directors or beneficial owner(s) proprietor of the Firm has to be established by any of the documents as mentioned in Individual or Joint Customer category

D) Partnership Account

- Bank’s prescribed Account Opening application form signed by the partners of any kinds of business.

- Certified copy of Partnership Deed/ Agreement

- List of the Partners with Address

- Extract of resolution of the partners Meeting

- Copy of valid Trade License

- Photograph of the signatories/ Partners

- Specimen signature card to be signed by the signatories.

- Introducer’s signature in the A/C opening form and at the back of the photograph(s) of Account holder(s).

- Identity of all Partners/ Directors must be verified in line with the requirements for personal customers. Where a formal partnership agreement exists, a mandate from the partnership authorizing the opening of an account and conferring authority on those who will operate it should be obtained.

- Evidence of the trading address of the business or partnership should be obtained.

- An explanation of the nature of the business or partnership to ensure that it has a legitimate purpose.

4.0 Loan:

Bank is a financial institution of service oriented. It provides financial services to the economy by mobilizing fund from surplus unit to deficit unit. Bank mobilizes funds by introducing various financial products. ABBL is extending their credit facilities in all sector covering commercial credit lines to business community

Interest on various lending categories will depend on the level of risk and type of security offered. It should be keep in mind that rate of interest is the reflection of risk in the transaction. The higher is the risk, me higher is the interest rate.

Interest may be reviewed at least once in 6 month and more often when appropriate. Fixed interest rate should be discouraged. Preferably all rates should vary with cost of funds fluctuation based on a spread for profit.

Effective yield can be enhanced to the extent the borrowers are required to maintain deposits to support borrowing activities. Commitment fee and service charges should further improve yield where possible. All pricing of loans should however have relevance with the market condition and be approved by the Executive Committee/Managing Director from time to time.

4.1 Types of loan & Advances offered by ABBL

4.1.1 Unsecured Loan:

- Personal Loan

- Auto Loan

- Gold Grace (Jewellery Loan)

- House/ Office furnishing/Renovation

- Staff Loan

- Education Loan

4.1.2 Secured Loan:

- Personal Loan.

- Personal Overdraft

4.2 Credit appraisal procedure of ABBL:

ABBL has well structured and managed written credit procedure that is followed the bank credit department. This well structured procedure covers the following steps that require to finalized a complete credit proposal.

4.2.1 Request for credit limit (RFCL):

Request for credit limit include the following step that furnished by the bank

- Name & Details:

A) About the firm

B) About the individual / proprietor

- Assets & Financial position:

A) Held in the name of the proprietor

B) Held in the name of the firm

C) Financial performance, capital & Net worth for three years

- Experience & Background of the proprietor / individual

- Name of the sister concern / subsidiaries / Affiliates.

- Details of business / Products.

A) Major customers / Competitors.

- Credit facilities sought.

- Details of the Non-funded facility

- Details of the securities offered

- Details of the guarantors

A) Personal information

B) Net worth

- Bank information related to loan.

A) With ABBL

B) With other banks

- Any others relevant information.

- Proposed debt equity ratios

- Declaration.

4.2.2 Loan Proposal:

- Customer’s details

- Credit facilities

- Consumer Loan

- Purpose of proposed facilities & bank’s income from proposed facilities

- Details of Non-funded facility

- Security Arrangement

- Transaction history: ABBL, Islampur Branch

- Transaction history: With others bank

- Account checking

- Account Performance

- Business performance & Bank income’s from the client

- Nature & Details of the business / Products:

A) Product & Market

B) Major customers / Competitors

- Financial performance:

A) Key financial indicators

B) Cash flow statement & working capital requirements

C) Requirement calculations / Justifications.

- Risk & Mitigations

- Recommended debt structure

A) Recommended following credit facilities

B) Comments & Recommendation of the branch

I. For the Head office only:

A) Name of the branch

B) Name of the client

C) Nature of business

D) A/C Relationship since

E) Borrowing relationship since

F) Credit facility:

- Existing:

– Funded

-Non-funded

- Proposed

– Funded

-Non-funded

- II. Remark by the credit officer

- III. Recommendation by the initiating Executive

- IV. Approved / Declined (with reasons if any) by the credit committee

G) Security

H) Conditions if any

4.2.3 Statement of stock under hypothetical:

- Particulars of commodity

- Quantity

- Rate

- Market value

4.2.4 Credit risk grading score sheet:

Financial risk:

i. Leverage.

ii. Liquidity.

iii. Profitably.

iv. Coverage.

v. Stock turnover days.

vi. Receivable turnover.

Business / Industry risk:

i. Size of business.

ii. Age of business.

iii. Business outlook.

iv. Industry growth.

v. Market competition.

vi. Entry / Exist barriers.

Management risk:

i. Experience.

ii. Second Line / Succession.

iii. Teamwork.

Security Risk:

i. Security coverage (Primary).

ii. Ownership of collateral security.

iii. Location of collateral security.

iv. Collateral coverage.

v. Support (Guarantee).

Relationship Risk:

i. Account conduct.

ii. Utilization of Limit.

iii. Compliance of covenants / Conditions.

iv. Personal Deposit.

4.2.5 Head Office Approval:

After analyzing and judging the credit risk branch credit committee send the loan proposal to the head office credit committee because branch offices does not posses the authority to disburse a single amount of loan.

4.2.6 Loan repayment procedure and loan position ABBL (ISLP):

ABBL offer easy procedure to repayment any types of loan and amount of installment depends on duration and amount of total loan. Loan interest is 17.50%. The different types of loans for the last 3 months has been given below:

Table#13 In three Month of 2008, All types of Loan products position of ABBL (ISLP):

Number of Month | Total loan amount of those month (In Tk) |

| March | 392818713.05 |

| April | 409258268.49 |

| May | 437526250.64 |

The ABBL Loan facilities are increasing for their regular and valuable customers. By providing loan they earn some sort of profit. The month March to May their loan product furnish by different offers for their valuable customers. In future they may introduce some sort of new loan products.

5.1 Findings:

After complete three-month internship on Deposit Mobilization on ABBL Islampur Branch

, I found that ABBL Islampur Branch Mobilize their deposit more but account figure change more frequently because there are lot of transaction occurs in a day. ABBL provide loan only for ABBL regular and profitable customer after analyzing all sort of risk that related with a Loan.

5.2 SWOT Analysis:

SWOT stands for Strengths, Weaknesses, Opportunities, and Threats. It is useful tools for evaluation, decision-making and planning for any kinds of organization

Strengths:

- Strong brand image of A B Bank Ltd.

- High level of On-line Banking technology.

- Friendly working environment

- Strong financial position

- Good management system

- Fast and strong distribution network

Weaknesses:

- Less number of manpower

- Low pay structure than other commercial Banks

- A single counting machine

Opportunities:

- Potential and large market.

- Expand product line to meet broader range of customer needs

- Available potential source of fund

- Faster market growth

- Diversity in to related product

Threats:

- Number of competitors are increasing by offering attractive offers

- Changing customer needs and tastes

- Growing bargaining power of customer

5.2 LEARNING POINTS:

I learning many things during my internship period at Islampur Branch of A B Bank Ltd. Those learning points are as follows:

- Open an account by On-line system

- Issuance of cheque books with serial posting to the customers

- Providing Bank statement and Solvency certificate as per client request

- Stop payment as per client request

- Preparing Debit and Credit Voucher

- Preparing Debit and Credit Advice

- Able to do inward clearing

- Make a good relationship with the customers by offering a cup of tea and keep myself within a smiling face

- Learn how to fulfill customer requirement by On-line Banking

- Issue pay orders with a proper register entry.

- Learn how to provide interest against FDR.

- Improve my communication skills to deal with customers

6.1 CONCLUSION:

AB Bank Limited is the first generation bank. After gathering practical experience from Islampur Branch of A B Bank Limited, it is stated that Islampur Branch have a nice chin of command and function level of strategy to achieve their expected target. Several function departments available at this branch such as Account opening, Credit Department, Remittance & Financial Control Department and Cash department. Islampur Branch is performing better to satisfy their valuable customers by using On-line Banking and Expert staff. Islampur Branch is always trying to satisfy their customers by providing hassle free services at fast & reliable ways.

6.2 RECOMMENDATION:

Banks internal charge may want to decrease to achieve high level of customer satisfaction and ensure provide equal opportunity to every level of customer. There are some shortest of manpower than any others commercial Bank. ABBL should introduce account for student like some other banks. Bank staff remunerations should increase to inspire them to do more for the organization. ATM card services should start in every Branch to provide customer hassle free service than others. Training facility available for every level of employees by establish a training institution. On-Line Banking facility time may increase to provide actual facility of this technology. Require a marketing department in every Branch for more Deposit Mobilization.