LOANS AND ADVANCES DEPARTMENT

Introduction:

Banking is essentially a business dealing organization with money and credit like all other business activates. Banks are profit-oriented organization. A bank invites its find many ways to earn more and more profit and most of its income is derived from loans and advances. Bank makes loans and advances to traders, Businesspersons, industrialists and many other persons against security of some cautions policy and sound lending principle in the matter of lending. EXIM Bank is a lending bank in loans and advances and it grant loans in various sectors especially in industry, trade and commerce.

Types of loans and advances:

There may be different types of loans and advance given from the commercial banks such as EXIM Bank Ltd. Of our country. Loans and advances may be in the following types:

1. Cash credit

2. Overdraft

3. HouseBuilding loan (General and Staff)

4. Transportation (Car) loan (only for senior staff)

5. Consumer credit Scheme

6. Loan against Imported Merchandise (LIM)

7. Loan Bills purchases Documentary (LBPD)

8. Loan against Other Securities (LAOS)

9. Term Loan

Brief Idea about the different types of loans and advance:

Cash Credit (CC):

Cash credit is an arrangement by which the customer is allowed to borrow May up to a creation limit. This permanent arrangement and the customers need not to draw the sanctioned amount of money at a time. The borrower can draw the money when required. The borrower can put back any surplus, amount, which he/she may he affect frequently. Intersect is charged only to the amount with drawn and not he whore amount sanctioned cash credit arrangement is usually divide into two ways such as:

1. Cash credit pledge

2. Cash credit hypothecation

Cash Credit Pledge:

In case of cash credit pledge possession of the goods dealings to bank and ownership of the of the goods belongs to borrower and bank the possessions of the goods as primary security. The goods storied in go down under lock and key by direct supervision of the bank. If the borrower wants to sell any potion of the pledged goods he/she permission of bank with returning the value of the loan amount. It is therefore regarded as the most secured type of advance.

Cash Credit hypothecation:

In case of cash Credit hypothecation possession of the goods not transferred to the bank and therefore such and advance is no better than a clean loan, such an advance can thus only be granted to a person in whose integrity the barked has full confidence cash credit in the form of Hypothecation is normally accompanied with mortgagee of immovable properties. The pray/ borrower possesses the lock and key of the down.

The Formalities of opening cash Credit:

There intending cash credit holder should submit the following documents and being fill up properly:

1. Stock repot, rend receipt

2. Trade license

3. Up to date income tax clearings certificate

4. Charge documents

5. Letter of Continuity

6. Letter of arrangement

7. DP (Demand Promissory) note

8. Letter of guarantee

9. Letter lien

10. Limit sanction advice

11. Non-Encumbrance Certificate

Observing the documents the bank authority prepares a cc proposal from that contains the following information:

1. Nature of business

2. Banking with EXIM

3. Transition with CD account by the client

4. Allied deposit with SB/STD account.

5. Number of adjustment (s) how many times the CC holder made his/her

Account nil that means debit balance equal to credit balance.

6. Recycling it is ration of total credit summation to the limit. If the ratio is

Higher it is better from banker’s points of view.

7. Turn over in the account

8. By the encasement authority the bank holds the power to encase the FDR the encasement authority at any time in case borrower’s failure to repay the loan amount with interest in due time.

Based in the above-mentioned information the dealing officer of the loans and advances department prepares recommendation about the prospect of granting the CC loan to the client.

Overdraft:

Overdraft is an arrangement between the banker and the customer by which the letter is allowed to withdraw over his/her credit balance in the current account up to an agreed limit. The borrower is permitted for draw and repays any number of times, provided he total amount overdrawn dose not exceeds the agreed limit. Here the interest is charged only for the amount withdrawn over the limit. Not for the whole amount. Overdraft is divided into tow categories:

■ Secured overdraft (SOD)

■ Temporary overdraft (TOD)

Secured overdraft: It is allowed against the full security (i.e. FDR, ICB unit

Certificates).

Temporary Overdraft: It is allowed to the customer for a very short period of time. But EXIM bank deals only secured overdraft.

Car Loans:

This is a special type of loan, which is only provided for the staff of EXIM

Bank. Usually AVP and above level officers get this kind facility. This loan is reimbursed on instrument basis and repayable after each month.

House Building loan (General and Staff):

General house building loan is providing into two sectors:

■ Generally

■ Staff

Naturally house building loan is paid for the construction of commercial building, and owners etc, procedures for sanctioning house- building loan as follows:-

■ Application for sectioning loan

■ Application properly filled up for credit facilities supplied by the bank.

■ Personal net worth statement each director

■ Enquiry form

Required papers for sanctioning HB loan:

■ Copy of general power of attorney

■ Copy of material certificate

■ Copy of engineer’s estimate

■ Copy of projected cash flow

Loan (General):

In case of loan the banks sanction some of money for a certain period of time. The enter amount is one time disbursement and paid in cash or credit loan A/C.

The interest is charged on full sanctioned amount @16%. The bank generally sanctions loan to establish industry. These types of loan are granted for capital expenditure such as purchase of land, constriction of factory building, purchase of new machinery and modernization of plant. The borrower cannot withdraw this type of loan once repaid in full or in part again.

Formalities for extending project loan:

Loan application form:

After receiving the loan application from the borrower the branch scrutinizes the application whether it is viable or not. Loan application from contains the following particulars amongst other detail below:

■ Particular description of the Project.

■ Nature of the Project

■ Detail information about the borrower

■ Statements of assets and liabilities of the borrower with declaration

■ Detail information about proposed products, machinates and manpower etc

■ Project cost and source of fund.

■ Market for the proposed project.

Feasibility report:

This report is provided by the borrower, which includes the following aspects of the project:

■ Marketing aspect

■ Technical aspect financial aspect

■ Managing aspect

■ Socio-economic aspect

1) Classification Procedure

- Categories of Loans- At first all loans and advances will be grouped into four categories for the purpose of classification, such as- (a) Continuous Loans (b) Demand Loans (c) Fixed Term Loans and (d) Short Term and Agriculture & Micro Credit.

(a) Continuous Loans : The loan A/C in which transaction may be made within a certain limit and have an expiry date for full adjustment will be treated as continuous loan. Exp CC, OD etc.

(b) Demand Loans: The loan that becomes repayable by the party on demand by his bank will be treated as demand loans. If any contingent or any other liabilities are turned into forced loan will also be treated as demand loan. Exp. LIM, PAD, FBP, IBP etc.

(c) Fixed Term Loans: The loan which is repayable with in the specific time period under a pacific repayment schedule will be treated as Fixed Term Loans.

(d) Short Term Agriculture & Micro Credit: Short Term Agricultural Credit will be as per list issued by Agricultural Credit and Specialized Programmers Department (ACSPD) of Bangladesh Bank under the Agricultural Credit Programmed. Credit in the Agricultural sector repayable within 1(one) year will also be included herein. Short Term Micro Credit includes any micro credit not exceeding TK. 25,000.00 and repayable within 12 months.

2) Basis for Loan Classification:

(A) Objective Criteria

(1) Past due/ over due:

In this point we saw four factors those are;

a) Any continuous loan if not repaid / renewed within the fixed expiry date for repayment be treated as past due/ overdue from the following day of the expiry date. any demands loan if not repaid/ rescheduled within the fixed expiry date will be treated as past due/ overdue from the following day of the expiry date.

b) In case any installment of a fixed term loan (repayable within fives) is not repaid within the fixed expiry date, the amount of unpaid installment will be treated as past due/ overdue (defaulted instilment) from the following day of the expiry date of the particular installment.

c) Incase of any installment or part installment of a Fixed Term Loan (repayable over five years) is not repaid within the fixed expiry date, the amount of unpaid installment will be treated as past due/ overdue after 6(six) months of the expiry date of that particular installment.

d) The Short Term Agriculture & Micro Credit if not repaid within the fixed expiry date for repayment will be considered as past due/ over due (defaulted instilment) after 6(six) month of the expiry date.

(B) Qualitative Judgment;

If any uncertainty or doubt arises in respect of recovery of any continuous,

Demand or Term Loans the same will have to be classified as Sub- Standard or Doubtful or Bad/ Loss. Considering the merit of the A/C on the basis of qualitative judgment be it classified or not on the basis of objective criteria.

The Bank will classify on the basis of qualitative judgment and can be- classify loans if qualitative improvement does occur. But if a loan classified by Bangladesh Bank inspection Team, the same can be de- classified with the approval of the Board of Directors of the Banks.

CIB Report:

Before making credit report to the head office the lending branch takes the credit information to the borrower from the CIB (credit Information Bureau) of Bangladesh Bank and other financial institutions. For obtaining this report the branch sends Inquiry form’ to CIB duly filled in particulars of the borrower. The report id divided into 5 segments.

Project appraisal:

It is the reinvestment analysis done by Banker before a project is approved. Project appraisal in the Banking sector is needed for following reasons:

■To ensue repayment of the Bank finance

■To achieve the organizational goals

■To establish industrialists in a country.

The main tasks of the project appraisal is to justify the soundness of an investment by the Banker by means of a capital and systematic of the different elements of the Project For this purpose Banks use two types of analysis:

■Lending Risk Analysis (LRA)

■Spread Sheet Analysis (SSA)

Lending risk analysis:

Lending risk analysis is modern methodologies, which describes how to access the risks that are inherent any credit extension and how to access the likelihood that the customer will repay a loan. The LRA form contains 16 pages to analysis different categories of Risks. The Financial Sector Reform project introduces the lending Risk analysis format in 1993. LRA is a standardize format for analyzing the credit worthiness of a borrower and the likelihood that the borrow will repay. Bangladesh bank issued a letter number BCD (p) 611/13/290 dated 17-07-1994, which now makes it mandatory for the commercial Banks to implement the LRA approach to credit analysis prior to extending credit facilities to a Borrower.

The modern concept of lending is purpose and production oriented and not security oriented. The emphasis should be given not any security rather on he likelihood of repayment, the credit worthiness of the customer soundness and viability of the business etc.

Lending Principles

The Principle of lending is a collection of certain accepted time tested standards, which ensure the proper use of Investment fund in a profitable way and its timely recovery. Different authors describe different principles for sound lending.

- Safety

- Security

- Liquidity

- Adequate yield

- Diversity

Process of Investment

| Heads | Characteristics |

| Application | Applicant applies for the Investment in the prescribed form of the bank describing the types and purpose of Investment. |

| Sanction |

|

| Documentation |

|

| Disbursement | An Investment Account is opened. Where customer A/C—————————————————————————————Dr.Respective Investment A/C —————————————-Cr. |

FOREIGN EXCHANGE DEPARTMENT

Introduction:

One of the largest businesses carried out by the commercial bank is foreign trading. The trade among various countries fills for close link between the parties dealing in trade. The situation calls for expertise in the field of foreign exchange operations. The bank, which provides such operations refereed to as rending international Banking operation. Mainly trisections with overseas countries are respects of import, export and foreign remittance come under the preview of foreign exchange transaction, and international trade demands a flow of goods from seller to buyer of payment from buyer to seller. In this case the Bank plays a vital role to bridge between the buyer and seller.

Foreign Exchange Mechanism in Flow Chart

Foreign Exchange department of EXIM Bank is department of all departments. This department handles various types of activates by three separate sections:

1. Import Section

2. Export section

3. Foreign Remittance.

Import Section:

The functions are of the section is mainly to deal with various components such as

■ Letter of Credit (L/C)

■ Payment against Document (PAD)

■ Payment against Trust Receipt (PTR)

■ Loan against Imported Merchandise (LIM)

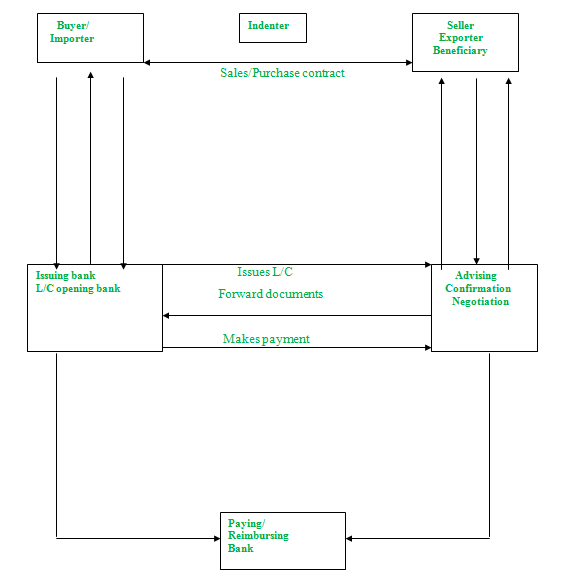

Letter of Credit (L/C):

Definition:

A letter of credit can be defined as an arrangement where in a Bank Guarantee on behalf of these customers to make payments to the beneficiary upon presentation of documents specified in the credit.

Parties involved in L/C:

Opener/ Buyer/Importer:

The person who opens the L/C is known as opener/ buyer/importer of the L/C. The buyer and the seller conclude a sales contract providing for payment by documentary credit.

0pening Bank:

The Bank issuing the L/C in favor of exporter is known as opening Bank. The opening bank opens L/C on request of importer according to application of the importer.

Advising Bank:

The Bank through L/C is advised their agent (correspondent Bank) abroad. The duty of the advising Bank is to authenticate the message so that is to the seller can act on it without any fear of forgery etc.

Beneficiary:

Seller and exporter in whose favor the L/C are opened. The beneficiary is normally the seller of good who receive payment under documentary credit. If has compiled with terms and conditions thereof.

Negotiating Bank:

The Bank that is authorized to handle (purchase) the documents under the L/C in the exporting country is known as negotiating Bank. L/C will stipulate either a notified bank to negotiate (restricted L/C) or any bank can negotiate in the seller’s country (unrestricted L/C).

Reimbursing Bank:

The Bank that is (by the L/C issuing Bank) to effect reimbursement is known as reimbursing bank. Reimbursing Bank authorized to honor the reimbursement claims in settlement of negotiation/ accepting/ payments lodged with its by the paying/ negotiating/ accepting Bank.

Confirming Bank:

A Confirming Bank is one which adds the guarantee to the credit opened by another bank. Therese undertaking the responsibility of payment/ negotiating/ acceptance under the credit in addition to that of the issuing Bank. A confirming Bank normally does so it requested by the issuing Bank.

Types of L/C:

– Revocable/ irrevocable L/C

– Confirmed/ unconfirmed L/C.

– Transferable L/C

– Back to back L/C

– Acceptance L/C

– Revolving L/C

– Red clause L/C

– Green close L/C

The EXIM Bank basically deals with irrevocable L/c. which can not be amended or cancelled by the issuing Bank at any moment and without prior to the beneficiary.

It also deals back to back L/C, which is the letter of credit, provided by the exporter to the import the raw materials from abroad in order to produce the exportable commodity for the importer.

Procedures for opening L/C:

Application for opening L/C:

An importer who is desirous to import goods from foreign country will apply

Issuing Bank for opening a L/C. The importer will provide an application mentioning the following aspects:

○ Full particulars of applications Bank account.

○ Types of business

○ Historical background

○ Amount of required L/C limit

○ Amount of L/C margin.

○ Term of payment

○ Name of imported goods

○ Repayment schedule and source of fund

Document schedule and source of fund.

An importer or L/C opener has to submit the following documents

○ Application from (provided by the Bank)

○ Import registration certificate

○ Pro-forma invoice

○ Four sets of IMP from

○ Insurance cover not

○ VAT registration number

○ Tex registration number

○ Letter of credit authorization form

Examination for opening L/C:

Application must be carefully checked by the concerned officer considering the facts mentioning below:

▪The terms and conditions of L/C applications are consistent with exchange control and import trade resolution UCPDC 500.

▪Illegibility of imported goods

▪The L/C must be opened in favor of importer

▪That is signed by the importer and agreed with the terms and conditions.

▪ Indenting registration number

▪Goods are not of Israel and vassals to be used are not of Israel

▪Insurance cover note with date of shipment.

▪Whether RC is up to date or not

▪Whether IMP form is duly filled up and singed

▪The imported goods are marketable

After scrutinizing all thee legal aspects necessary entry is given to the margin register and charge, commission and margin in realized.

Transmitting the L/C:

The L/C is transmitted to the advising Bank for advising the L/C to he beneficiary. L/C is generally transmitted through tested Telex of Fax. Before transmission of final examination of the L/C contents is necessary for the issuing Bank. It is customary to advice a credit to the beneficiary through advising Bank. Advising Bank after receiving L/C documents informs to the beneficiary for receiving L/C.

Add Confirmation:

Very often advising Banks received request from the issuing Bank to add their conformation while advising credit to the beneficiary. The advising can do it if there is prior arrangement between advising and issuing bank or if it feels that the issuing Bank is repute reliable and institution and good enough to discharge this obligation.

Amendment o f L/C:

In case of revocable L/C amendment is brought without prior notice of the beneficiary-issuing Bank. But in cage of irrevocable L/C prior notice of the beneficiary is essential.

Issuing Bank will accept amendment of the L/C after getting consent of both importer and exporter.

Payment against Document (PAD):

The issuing, Bank starts (PAD) procedure after getting all necessary documents from the exporter as evidence of export in goods. Documents required for PAD is mentioned below:

○Original (non-negotiable) bill of landing

○Commercial invoice

○Certificate of insurance

○Certificate of origin

○Bill of exchange

○Pre-shipment inspection certificate

○packing list

○clean report of Finding (CRF)

Examination of PAD documents:

Scrutinizing documents is very important for the issuing Bank. As after Examining all the documents the issuing Bank will make payment to the Negotiation Bank. So, any mistake in the examination process may cost issuing Bank.

Examining the bill of exchange:

■It is drawn a duly signed by the market indicating as the beneficiary

■It is drawn on the import indicating him draw.

■L/C number quoted on it.

■Tenors of the draft are strictly in conformity with the terms stipulated in the L/C.

■Amount is identical

■Amount in words and in figures is same

■Examining the commercial invoice

■It is addressed to the importer

■It is dated, signed and submitted in required number

■It must bear detailed description of goods that must tally with L/C and bill of landing

■Price, quality, quality etc is corresponded to L/C.

■It must be prepared in the language of L/C.

■Invoice must bear L/C authorization and other relevant number.

■Charge relevant to merchandise is included in the invoice and is permitted by the L/C.

Examination of transport document:

■It is presented in full set of negotiable and non-negotiable copies.

■Date of shipment on the bill of landing.

■Bill of landing must be made out in the name of Bank notify the importer.

■Description of goods in the bill of landing must agree with invoice and L/C.

■Port of shipment and destination is as per L/C.

■Bill of landing is singed by shipping company or their agent.

Examination of other document:

Weight lists, inspection certificate, quality certificate, certificate of origin, packing list etc. should agree with L/C terms and conditions and also signed by the appropriate authority. These certificates are usually dated before the date of shipment.

Common discrepancies of the import document:

Following are the common discrepancies found in the documents operation:

■Inadequate number of invoice

■Late shipment

■Late shipment of transshipment beyond L/C terms

■one broad endorsement unsigned or not dated on the bill of lading.

■Specifications of goods are not as per terms of L/C.

■Tenor of draft wrong.

■Inconsistent documents presented

■Absence of some documents

If any major discrepancies found in the documents it is informed to the buyer for his/her opinion. If discrepancies are minor then these are overlooked

Lodgment and retirement of import document:

Date of payments: Usually payment is given within 7 days of documents received. Otherwise incase of documents purchased by negotiating Bank it may claim for interest.

Intimation letter: Before payment intimation letter is given to the International department for arranging necessary fund before final payment.

Retirement Procedures:

■Receive all kinds of documents

■Checking of documents as per L/C terms

■Entry of PAD registers

■Vouching of PAD register

■Posting of voucher

■Sending credit advice to the head officer

■Informing importer about receiving documents.

Other parts of this post-

Report On Export Import Bank Limited (Part-1)