INTRODUCTION OF THE STUDY

2.1 Introduction

It is necessary for all BBA (Bachelors of Business Students) to prepare an internship report at the end of this program. On the other hand internship is a course which is related to our course curriculum. As a student of BBA in American International University-Bangladesh (AIUB) my intention is to capture some theoretical concept and to know how implement this theoretical concept in our real life solution. Students are applying this concept in different organizations.

AB bank limited has started its business with all the features of a corporate Bank and the products of both corporate and retail banking system; to facilitate the daily clientele requirements. ABBL is always try to improve their service in every sectors but in today’s comprehensive business world AB banks need to offer additional concentration to the clients requirement in order to stay in the top.

In addition of all short of traditional banking activities, AB bank provides on-line banking service and a comprehensive range of financial service national and multinational companies in the country. It also undertakes the share and debentures, works as issue manager, and participates in other operations in MONAY MARKET and CAPITAL MARKAT. As a member of Dhaka stock exchange and Chittagong stock exchange.

Today is the time of competition. As a business student I am very interested to know the business world. On the other hand foreign trade is one of the parts of business. Foreign trade is divided in three categories like Import, Export and Remittance. Import and export both are related to letter of credit (L/C).

Letter of Credit is one kind of commitment or assurance or bank guarantee. The commitment is behalf of importer to exporter. If exporter will present his performance as far terms and condition and provide the asked documents, accordingly bank will make payment against the performance. There are different reason importers and exporters are involved in Letter of credit (L/C) like: Lack of trust between importers and exporters

contracts.Safe mode of transaction; Lack of confident to provide the payment in due date; Effective payment of shipping goods and services.

2.2 Rationale of the study

Foreign exchange transaction plays a vital role in the economic development of a nation. Foreign exchange transaction comprises both international trade & remittance. There are various rules and restrictions in international trade that means import and export transactions. To export or import any items the exporters or importers need financial support. The commercial banks of Bangladesh play an important role by providing them financial support through loan, various incentives and advising letter of credit. This paper empirically discuss with the rules, restrictions and procedures of foreign exchange transactions comprising LC advise, negotiation of documentary bills, repatriation of proceeds and its impact on profits. An easy and simple procedure of such transactions may help the exporters and importers to increase their business in future.

2.3 Scope of the report

The scope of the organizational part covers the organizational structure, background, vision, mission, objective, functions and rules, restrictions, procedures of foreign exchange transactions of the organization.

2.4 Objective of the study

To prepare the report I have acquainted with day-to-day foreign exchange functions of ABBL, know the progress of foreign exchange and foreign trade of ABBL, to gain in-depth knowledge of export, import and remittance of ABBL highlighting the foreign exchange activities of this bank. The primary & secondary objectives of this report are-

Primary Objective

The main objective is to know the significant relation that exists between import-export and branch performance in this sector. On the other hand the significant relation that exists between import-export and business world.

Secondary objective

To know and focus the whole import-export mechanisms.

To know and focus the remittances activates.

To know and focus the rules and regulation of import-export mechanisms.

Identify some problems and also make some recommendations.

To observe the working environment in commercial banks.

To apply theoretical knowledge in the practical field.

2.5 Methodology of the Report

Methodology includes-

Direct observation

Face-to-face discussion with employees of different departments

Study of files, circulars and practical work.

Annual Report of 2009 etc.

This study includes both quantitative and qualitative data. However, this report is basically qualitative in nature. In all the cases depending on the requirements data have been collected from different sources.

Source of Data

This report is based on both primary & secondary sources of information that has been collected from the various sources like different publications, library sources, books, articles, etc. For collecting primary data, I ask the respective officer(s). Others are like –

Exposure on different desk of the bank;

File study.

Getting information from face to face dealing with the client

Personal interview with branch officials or executives

The secondary sources are –

Annual Report of AB Bank Bangladesh Ltd,

Web site of ABBL

Periodicals published by the Bangladesh Bank;

Different publications regarding banking functions, foreign exchange operation, and export-import policies.

Time preference

The time preference of the study relates to the period covering the years 2005 to 2009. And also shown some analysis from 2008 to 2010 as a per month analysis & evaluation. All these years has been taken for different analysis purposes.

Data processing and analysis

Data processing has been done manually after checking and editing. For analyzing excel is used.

2.6 Limitation of the study

AB Bank Ltd. is a large financial institution; therefore it is not possible to find out the true pictures within a short period. To prepare the report I faced some problems & limitations. Those limitations are unavoidable for me. That may causes reduction in the quality of my report. Some of the major problems are pointed below-

Difficulties to communication and collect data.

Difficulties to gather data in a specific way.

In many cases, up to date information is not published.

Organization confidentiality.

Time constraints are one of the major problems/limitations to know the information.

3.1 Foreign Exchange

Foreign Exchange means foreign currency and it includes any instrument

drawn, accepted, made or issued under clause (13), Article 16 of the Bangladesh Bank Order, 1972. All deposits, credits and balances payable in any foreign currency and draft, travelers cheque, letter of credit and bill of exchange expressed or drawn in Bangladeshi currency but payable in any foreign currencies.

Foreign Exchange Act. 1947 defines foreign exchange as “Foreign currency and includes deposits, credits, and balances payable in foreign currency as well as drafts, travelers cheques, letter of credit, bills of exchange drawn in local currency but , payable in foreign currency”.

According to Dr. Paul Einzig, “Foreign exchange is the system or process of converting one national currency into another and transferring money from thecountry to another.” Foreign exchange deals with foreign trade and foreign currency.

3.2 Foreign Trade

No country is self-sufficient in all the goods. Some countries have special advantage to produce some items. Bangladesh can manufacture readymade garments easily due to lower cost of labor. So Bangladesh is exporting readymade garments to USA where as USA is exporting machinery to Bangladesh due to their favorable transaction to that item. These kinds of cross border transaction or exchange of goods are called foreign trade.

3.3 Foreign Exchange and Foreign Trade

ABBL undertakes spot purchase and sales foreign currencies by deploying its own fund.

Foreign exchange and foreign trades of a country are conducted according to the law of that country. AB Bank Ltd. performs all its banking operations including foreign exchange activities according to that law.AB banks conduct their foreign exchange businesses mainly into two ways:

a) Bank provides service as an agent for the transaction and earns service charge, commission etc.

b) Bank invests its fund for the purchase of foreign currencies and sale of such currencies on the basis of present transaction and may earn profit thereof.

3.4 Foreign Exchange Transactions

Conversion of currencies or exchanges is known as foreign exchange transactions. The conversion may arise for a transaction between a bank and its customers or between a bank and another bank at home or abroad. The transaction involves at least two currencies. For a bank in Bangladesh, the process of conversion frequently involves conversion of Bangladeshi taka into foreign currencies or vice- versa.

For instance, one of the customers of your bank wishes to send an amount of $1000 to his son in USA. Assuming that this remittance is permissible or that permission from the exchange control authority has been obtained, you will issue a draft in favour of the beneficiary for $1000 drawn on your USA correspondent or a branch of yours, if any, in favour of your customer’s son and ask your customer to pay the equivalent amount in Taka. The transaction involves two things: payment of $ 1000 from your dollar account – your Nostro account maintained with your USA branch or correspondent and recovery of its taka equivalent at the ruling ready (spot) rate of exchange between taka and dollar. In another instance, your customer may ask you to buy a draft for Tk.10000 drawn on a bank in Iran towards the value of jute bags supplied to the Iranian buyer against a letter of credit open by a bank of Iran. If you are satisfied that the documents accompanying the drafts are in order, you will pay the taka amount and ask that bank of Iran to pay you equivalent amount in dollar or Iranian Real.

In the illustration given above, remittance of $1000 to USA would involve conversion of local currency into a foreign currency and in the later case the transaction would involve conversion of a foreign currency- dollar or Iranian Rial into local currency.

3.5 Wings of Foreign Exchange

A Bank’s Foreign exchange department has three definite wings through which foreign exchange transactions are conducted.

Foreign Exchange

Import Section Export Section Remittance Section

The achievement of AB Bank in the above three areas of foreign exchange business has been quite phenomenal. The Bank has been providing services to import and export trade and for repatriation of hard-earned foreign exchange of Bangladeshis living and working abroad and has, by now, consolidated its position in these areas. The following chapters will discuss about these areas in details.

4.1 Introduction

Import trade of Bangladesh is controlled under the Import & Export control Act (IEC) 1950. Authorized Dealer Banks will import the goods into Bangladesh following import policy, public notice, F, E circular & other instructions from competent authorities from time to time.

Definition on Import:

Buying of goods & services form foreign countries for sales is considered as import. The person or organization who import the goods & services form foreign countries is known Importer and from which goods & services are imported is known as Exporter. In case of Import, the importers are asked by their Exporters to open a Letter of Credit (L/C). So that there payment against goods & services is ensured.

4.2 General Provision for Import

Regulation of Import – Import of goods under this order shall be regulated as under:

Banned list: Banned goods are not allowed to import through the foreign exchange transaction. Such as Live Swine, Eggs of shrimps and prawns etc.

Restricted list: Any item, which is restricted by the “Import Policy Order 1997-2002” in Annexure –1(b) shall be importable only on fulfilment of the conditions (b) specified therein against the item.

Free Importable Items: The items which are not included either in the Banned list or Restricted list shall be freely importable:

In addition to the conditions mentioned in the Restricted and Banned Lists the conditions restrictions and procedures for import of various items mentioned in the test portion of this Order, shall as usual apply in case of import of those items.

4.3General conditions of Import Goods

1) Import Trade Control Schedule Numbers- For import purpose use of new ITC Numbers with at least six digits corresponding to the classification of goods as given in the Import Trade Control Schedule 1998, based on the Harmonized Commodity Description and Coding System shall be mandatory.

2) NOC on the basis of ROR (Right of Refusal): No objection Certificate on the basis of right of Refusal form any authority shall not be required for import of any freely importable item by any Public Sector Agency. However, in cases where a public sector agency is required to import banned or restricted items included in the control list prior permission of the Ministry of Commerce shall have to be obtained on the basis of ROR issued by the ministry of Industries or by the Sponsoring Ministry/Division or by both as the case may be.

3) Restriction regarding source of procurement of goods:

(a) Goods from Israel or goods originating form that country shall not be importable. Goods shall also not be importable in the flag vessels of that country.

(b) All kinds of import from and export to Serbia and Montenegro, fragments of former Socialist Republic of Yugoslavia shall be banned.

4) Pre- Shipment Inspection: Unless otherwise specified pre-shipment inspection of imported goods shall not be obligatory in case of import be the private sector importers.

5) Shipment of Bangladesh Flag Vessels: Subject to waiver specified below shipment of goods shall normally be made on Bangladesh flag vessels.

4.4 Types of Importer

Goods are imported for personal use, commercial or industrial purpose. So there are three kinds of importer such as:

- Personal Importer.

- Commercial Importer.

- Industrial Importer.

4.5 Authorized Dealers

Authorised Dealer means a Bank, Authorised by Bangladesh Bank to deal in Foreign Exchange under the Foreign Exchange Regulation (FER) Act 1947. But there are some persons or firms, authorized by Bangladesh Bank to deal in Foreign Exchange with limited scope are called Authorized Money Changers. To get a license for authorization a bank will apply the General Manager, Foreign Exchange Policy Department, Bangladesh Bank, Head Office, Dhaka complying the subsequent conditions:

i. The Bank must have adequate manpower trained in Foreign Exchange.

ii. Prospect to attract reasonable volume of Foreign Exchange business in the desired location.

iii. The bank meticulously complies with the instruction of Bangladesh Bank.

iv. The bank will commit to deal in Foreign Exchange within the limit & will submit periodical returns as instructed by Bangladesh Bank.

4.5.1 Functions of Authorized Dealer

Authorized Dealer can handle all kinds of Foreign Exchange transaction as per Foreign Exchange Regulation (FER) Act 1947 under the instruction of Bangladesh Bank. Following are the main function of an Authorized Dealer:

i. Exchange of Foreign Currencies.

ii. To make arrangement with Foreign Correspondent.

iii. Buying & Selling Foreign currencies.

iv. Handling of Inward & Outward Remittance

v. Opening of L/C & Settlement of Payment.

vi. Investment in Foreign Trade.

vii. Opening & Maintenance of Accounts with Foreign Banks under intimation to Bangladesh Bank.

viii. Export Documents handling.

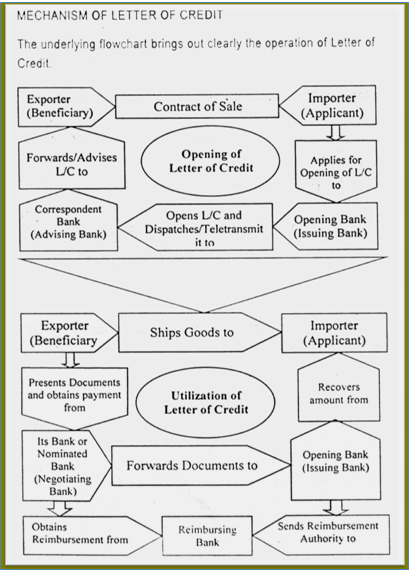

4.6 Letter of Credit (L/C)

Letter of Credit (L/C) is a payment guarantee to the seller by the issuing bank on behalf of the importer. In other words, it is a letter of the Issuing Bank to the beneficiary undertaking to effect payment under some agreed conditions. L/C is called documentary Letter of Credit, because the undertaking of the Issuing Bank is subject to presentation of some specified documents. Through the L/C Buyers & Sellers enter into a contract for buying and selling goods/ services and the buyer instructs his bank to issue L/C in favour of the seller. Here bank assumes fiduciary function between the buyer and seller.

4.6.1 Flowchart of L/C

Accounting treatment for opening L/C:

For opening L/C, importer will apply to the issuing bank. In that case, importer is called applicant or opener. After opening it bank will create a contingent liability. In that case, the accounting posting will be the following-

Customer liability …….. Dr.

Contingent liability………..Cr.

- While paying money but the issuing bank, issuing bank will reverse the above entry & the entry will be-

Contingent liability…….. Dr.

Customers liability…………..Cr.

- Then the issuing bank will give another entry-

Payment Against Document(PAD)……….. Dr.

AB General Account…………………………….. Cr.

Exchange gain…………………………………….Cr.

PAD will debit because the bank will pay the money against some documents. AB General Account is a miscellaneous account. It will be credited because by this entry ABBL creates a liability. He has to pay the money to the advising bank. & the gain made by the transaction is shown at Exchange Gain Account. All this entries are made after receiving some documents from the exporters. The above procedure is called Lodging. After giving the above entry, ABBL will inform the clients for collecting the documents from the bank.

After opening L/C, ABBL (Issuing Bank) must receive the documents for any other proceedings. These documents are-

I. Bill of Lading

II. Invoice

III. Packing List

IV. Country of Origin

4.7 Different Parties to a Documentary Credit

Normally the subsequent parties are related to a documentary credit. Such as

1) The Issuing Bank: This is the bank who issues Documentary credit on account of it’s client.

2) The advising Bank: This is a Bank acting as Agent of the Issuing Bank, to advise the L/C to the beneficiary.

3) The confirming Bank: This Bank gives the beneficiary a double assurance of payment. This is a third Bank undertake to make payment, to the beneficiary, if the Issuing Bank fail to make Payment.

4) Negotiating Bank: This Bank provides value to the beneficiary against presentation of documents complying credit terms. Usually this is exporter’s Bank who purchases the export documents.

5) Reimbursing Bank: This is a Bank acting as Agent of the Issuing Bank Authorised to make payment or to honour reimbursing claim of the Negotiating Bank.

6) The Transferring Bank: If the L/C is transferable then the 1st beneficiary through a bank nominated by the Issuing Bank this bank is called the Transferring Bank.

7) The Applicant: Importer or buyer is the applicant of a Letter of Credit. Applicant must be the client of the Issuing Bank.

8) The beneficiary: Exporter or Seller of the goods is the Beneficiary of a Letter of Credit.

9) Notify Party: The Party / Bank to whom the arrival of shipment has to be notified or to be informed is called notify party.

4.8 Import Procedure

To import a person should be an importer. In accordance with Import & Export Control Act, 1950 the office of chief Controller of Import & Export provides the registration (TRC) to the importer. After getting this person has to secure a letter of credit authorization from Bangladesh Bank. Then he becomes a qualified importer; He is the person who requests or instructs the opening bank to open an L/C. He is also called opener or applicant of the Letter of Credit.

4.8.1 Import Registration Certificate

Import Registration Certificates are issued by the office of chief controller of imports and exports. Intending importers are to submit applications to CCI & for registration along with required documents are as follows:

I. Application

II. Trade License

III. Nationality Certificate

IV. Income tax certificate along with TIN

V. Bank Certificate

VI. Membership certificate from Trade Association Certificate of incorporation, Article and Memorandum of Association. Partnership Deed for partnership firm.

4.8.2 Procedure for Registration

To obtain import registration certificate (IRC) the applicant will submit the following paper to the CCI & E through this nominated Bank.

a) Questionnaire duly filled in & signed by the applicant

b) Trade License

c) Membership certificate from chamber of commerce or any other trade Association

d) Nationality Certificate

e) Income tax registration certificate.

f) Partnership deed/certificate of registration with the register of join stock companies where applicable.

On being satisfied, the CCI & E issues IRC obtain original copy of treasury challan for payment of registration fee.

4.9 Preliminary Steps for Opening L/C

Before opening the L/C Bank will takes the subsequent steps:

1) Applicant to be Bank’s A/C Holder: Bank will open the L/C on behalf of an entity who has an account with the Bank. Unknown person will not be allowed to open L/C.

2) Registered importer: Before opening the L/C bank must confirm that the L/C applicant is a registered importer or personal user, and the IRC of the importer has been renewed for the current year.

3) Permissible item: The item to be imported must be permissible and not banned item. If the item is from conditional list, the condition must fulfill to import the same.

4) Market Report: Bank will verify the marketability of the item & market price of the goods. Some times the importer may misappropriate the Bank’s money through over invoicing.

5) Sufficient Security or margin: Price of some items fluctuates frequently. In case of those items Bank will be more careful to take sufficient cash margin or other security.

6) Business Establishment: Bank should not open an L/C on be half of a floating businessman. The importer must have business establishment, particularly he must have business network for marketing the item to be imported.

7) Restricted Country: Goods not to be imported from Israil.

8) Credit report of the beneficiary: It the amount of L/C in one item exceeds TK. 5.00 lac, suppliers credit report is mandatory. Bank will collect credit report of the beneficiary through its correspondent in abroad.

9) Application of the client to open the L/C: The client will approach to open the L/C in Bank’s prescribed form, duly stamped & signed, along with the following paper & documents: Such as

I. Indent / Performa invoice.

II. Insurance cover note with money receipt.

III. LCAF duly filled in & signed.

IV. Membership certificate form chamber of commerce / Trade Association.

V. Tax payment certificate / declaration.

VI. IMP & TM form signed by the importer

VII. Charge document.

VIII. IRC, Pass book, Trade license Membership certificate & VAT, registration certificate in case of new client. IX. Export L/C in case of back-to-back L/C.

10) Permission From Ministry of Commerce: If the goods to be imported under CIF (cost insurance & freight), then permission form ministry of commerce to be obtained.

11) Creditability of the Client: In consideration of all the above points, if Bank become satisfied regarding the client then L/C may be ope3ned on behalf of the client. Before opening the L/C bank will issue & authenticate a set of LCAF in the name of the importer.

4.10 Presentation of the Documents

The seller being satisfied with the terms and the conditions of the credit proceeds to dispatch the required goods to the buyer. Them he has to present the documents evidencing dispatching of goods to the negotiating bank on or before the stipulated expiry date of the credit. After receiving all the documents, the negotiating bank them checks the document against the credit. If the documents are found in order the bank will pay accept or negotiate to Bank. Then bank checks the documents. The usual documents are:

- Invoice

- Bill of lading

- Certificate of origin

- Packing List

- Shipping Advice

- Nor negotiable copy of bill of lading

- Bill of exchange

- Pre-shipment inspection report

- Shipment Certificate

4.11 Steps Involved in Import procedures:

Procurement of IRC from the concerned authority

Signing purchase contract with the seller

Requesting the concerned bank (importer’s bank) to open an L/C on behalf of the importer favouring the exporter/seller/beneficiary.

The issuing bank opens/issues the L/C in accordance with the instructions/request of the importer & request another bank(advising bank) located in sellers /exporter’s country to advice the L/C to the beneficiary. The issuing may also request the advising bank to confirm the credit, if necessary.

The advising bank advises the seller that the L/C has been issued.

As soon as the exporter /seller receives the L/C & is satisfied that he can meet L/C terms & conditions, he is in a position to make shipment of the goods.

After making shipment of the goods in favour of the importer the exporter’s submit the documents to the negotiating bank for negotiation.

5.1 Introduction

The export policy 1997-2002 has been formulated by the government to operate within imperative and opportunities of the market economy with a view to maximizing export growth and narrowing down the gap between import payment and export earning. As per existing Export Policy an Exporter can export any goods or services except the items listed as band and restricted in the said policy.Duration of present EPO-5 years effected from 1st July 1998, but valid till announcement of new policy.

Foreign Exchange Regulation Act, 1947 Clearly states that nobody can export by post and otherwise than by post any goods either directly or indirectly to any place outside Bangladesh, unless a declaration is furnished by the exporter to the collector of customs or to such other person as the Bangladesh Bank (BB) may specify in this behalf that foreign exchange representing the full export value of the goods has been or will be disposed of in a manner and within a period specified by BB. So a clear lawful procedure must be followed in case of export of goods & services.

5.2 Meaning of export

– Selling goods to foreign countries against of foreign currency.

– Export means lawfully carrying get of anything from one country to another country for sale. The import and export trade of the country is regulated by the IEC Act. 1950.

5.3 Export Policy

As per export policy order, 1997-2002 now in force an exporter can export any goods or services except the items listed as banned and restricted in the said policy.

5.3.1 Objectives of Export / Export Policy

Growth of national wealth, increase of production in export sectors, generation of employment & flow of capital and to achieve the growth of GDP target @7%.

5.3.2 Exporter Registration

An exporter must obtain Export Registration Certificate from the office of the Chief Controller of Import & Export (CCI & E). The procedure for obtaining Export Registration Certificate (ERC). Procedures for obtaining export registration certificate (ERC) from the CCI & E, the following documents are required:

1) Application as per format prescribed by CCI & E.

2) Bank Solvency Certificate.

3) Membership Certificate from a Chamber of Commerce.

4) Nationality certificate.

5) Partnership deed (Registered / Un-Registered) for partnership business concern.

6) Memorandum & Articles of Association & its incorporation certificate for public limited company.

7) Income Tax payment certificate (TIN)

8) Recent passport size photographs of the applicant.

9) Treasury challan showing payment of fees for ERC.

5.3.3 Securing the order:

After getting ERC Certificate the exporter may proceed to secure the export order. He can do this by contacting the buyers directly or through agent. In this purpose the exporter may get help from:

- Licence officer

- Buyers local agent

- Export promotion organization

- BangladeshMission Abroad

- Chamber of Commerce(local & foreign)

- Trade fair etc

5.4 Classification of Export

i. Export under L/C: Exporters are allowed to export the commodity under irrevocable L/C, under this type of export, exporter will ship the goods as per terms of the credit and will get payment as per arrangement of the credit.

ii. A firm Contract/Consignment Basis Export: Exports are allowed against firm contract. As per contract, exporter will ship the goods and the buyer will make payment after selling the consignment.

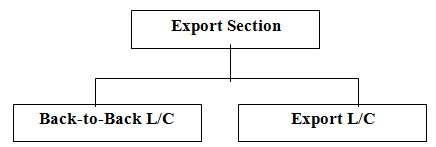

iii. Export against Advance Payment: Sometimes exporter receives payment in advance. In that case AD should obtain a declaration from the exporter on the “Advance Receipt Voucher certifying the purpose of the remittance. Then the exporter will export the goods against the advance payment. Export section ABBL, New market Branch deals with two types of L/C that are as follows-

5.5 Back-to-back letter of credit

Back-to-back L/C is a secondary L/C (New Import L/C) opened by the seller’s bank based on the original L/C (Master L/C) to purchase the raw materials and accessories for manufacturing of the export product (s) required by the seller.

Under the ‘Back to Back’ concept, the seller as the Beneficiary of the master L/C offer it as a ‘security’ to the advising Bank for the issuance of the second L/C. The beneficiary of the Back-to-Back L/C may be located inside or outside the original beneficiary’s country. In case of a Bark-to-Back L/C, the bank takes no cash security (margin). Bank liens the Master L/C and the drawn bill is an Usance/ Time bill.

5.6 Export letter of credit

The other type of L/C facility offered by the bank is Export L/C. Bangladesh exports a large quantity of goods and services to foreign households. Readymade textile garments (both knitted and wove), jute, jute-made products, frozen shrimps, tea are the main goods that Bangladeshi exporters exports to foreign countries. Garments Sector Is the largest sector that exports the lion share of the country’s export. Bangladesh exports most of its ready-made garments products to USA and European Community (EC) countries. Bangladesh exports about 40% of its readymade garments products to USA.

5.6.1 Formalities Required for Export L/C

The export trade of the country is regulated by the Imports & Exports (Control) Act, 1950. There are a number of formalities that an exporter has to fulfill before and after shipment of goods. These formalities or procedures are enumerated as follows –

A. EXPORT REGISTRATION CERTIFICATE (ERC): The exports from Bangladesh are subject to export trade control exercised by the Ministry of Commerce through Chief Controller of Imports & Exports (CCI&E). No exporter is allowed to export any commodity permissible for export from Bangladesh unless he is registered with CCI&E and holds valid ERC. The ERC is required to be renewed every year. The ERC number is to be incorporated on EXP (Export) Forms and other documents connected with exports.

B. THE EXP FORM: Foreign Exchange Regulation (FER) Act- 1947 prohibit export of any goods directly or indirectly to any place outside Bangladesh unless the exporter furnish a declaration to the effect that the export value of goods has been or will be repatriated into the country within a period time specified by the Bangladesh Bank. So, repatriation of export proceed is mandatory for all exported goods or services. Accordingly, before shipment of goods an exporter must declare on Export Form (Exp) prescribed by Bangladesh Bank and issued by the Authorized Dealer (Exporters Bank). The EXP Forms are numbered serially and issued in quadruplicate. For delay in repatriation of export proceeds or non-realization of export proceeds, the exporters render themselves for action under Foreign Exchange Regulation Act 1947. Authorized Dealers (AD) and their officials who certify the export forms also render themselves of such action by the Central bank. An EXP Form usually contains the following particulars –

i. Name and address of the Authorized Dealer;

ii. Particulars of the commodity to be exported with particulars and code no;

iii. Country of destination;

iv. Port of destination;

v. Quantity;

vi. L/C value in foreign currency;

vii. Terms of sale;

viii. Name and address of Importer/ Consignee;

ix. Bill of Lading/Railway Receipt/Airway Bill/Truck Receipt/Post Parcel Receipt no. and date;

x. Port of Shipment/Post Office of Dispatch;

xi Land custom post

xii. Shipment Date;

xiii. Name of the Exporter with address;

xiv. Registration number and date;

xv. Sector (public or private) under which the exporter fails.

C. SECURING THE ORDER: Upon registration, the exporter may proceed to secure the export order. Contracting the buyers directly through correspondence can do this.

D. SIGNING of THE CONTRACT: While making a contract, the following points are to be mentioned: a) Description of the goods;

b) Quantity of the commodity;

c) Price of the commodity;

d) Shipment; e) Insurance and marks;

f) Inspection, and

g) Arbitration.

E. PROCURING THE MATERIALS: After making the deal and on having the L/C opened in his favour, the next step for the exporter is set about the task of procuring or manufacturing the contracted merchandise.

F. REGISTRATION of SALE: This is needed when the proposed items to be exported are raw jute and jute-made goods.

G. SHIPMENT OF GOODS: The following documents are normally involved at the stage of shipment: (a) EXP From, (b) photocopy of registration certificate, (c) photocopy of contract, (d) photocopy of the L/C, (e) customs copy of ERF Form for shipment of jute-made goods and EPC Form for raw jute, (f) freight certificate from the bank in case of payment of the freight if the port of lading is involved, (g) railway receipt, berg receipt or truck receipt, (h) shipping instructions, and (i) insurance policy.

5.7 Export Documents:

After due passing of EXP, the exporter then execute shipment. As evidence of export and as per terms of the export L/C, Contract, exporter must prepare document in order to get his payment and to facilitate release of goods by the buyer abroad. Document are of (2 (two) types.

i) Financial document: The Financial document, prepared by exporter is known as Bill of Exchange or Draft. It is prepare by the exporter directing the L/C issuing Bank to pay sum of money at a certain date or determinable future time to negotiating Bank or order. The parties to a Drafts are Drawer, Drawee, Payee, Endorser & Endorsee..

ii)Commercial Document : The documents evidencing description and other details of goods shipped and supporting other terms and condition of L/C Contract are commercial documents.

Some Vital commercial documents are:

Invoice/ Commercial Invoice

Bill of Lading/Airway bill/Truck Receipt

Packing/ weighment/ Measurement List

Certificate of origin

Pre-shipment Certificate

GSP Certificate issued by EPB.