Origin of the Report

Any academic course of study has a great value when it has practical application in real life. Only a lot of theoretical knowledge will be little important unless it is applicable in practical life. So we need proper application of our knowledge to get some benefit from our theoretical knowledge to make it more fruitful. This is why, Internship program is a pre-requisite for acquiring BBA Degree my University. The entire BBA program is divided into twelve semesters. The internship program is executed in the last semester and it has got the same weight as other semesters in the evaluation process. As the classroom discussion alone cannot make a student perfect in handling the real business situation, therefore, it is an opportunity for the students to know about real life situation through this internship program. This program consists of three phases:

Orientation to Organization: To accustom the internee with the structure, functions, and performance of the organization.

The Project Work: Pertaining to a particular problem matching with the internee’s capacity and organization’s requirement. In the proceeding one phase.

The Report Writing:

To epitomize the internee’s analysis, findings and achievements, In this connection, I was assigned to BASIC Bank Limited Shantinagar branch, all departments for my practical orientation. The topic “Marketing Strategyof Basic Bank Ltd” was selected by the Human Resource Division of BASIC Bank Limited and was approved by Rokeya Binte Shahid, lecturer, Department of Business Administration, Green University of Bangladesh.

Objective of the Report:

Marketing Objective:

The Marketing objective of the report is to know about the International Trading system of BASIC Bank Limited as a private commercial bank as well as its formation, and its functional, operational, and financial aspects.

- Broad Objective:

- To know about the functions of the all Departments especially the opening of Varies scheme & Sanchyapatra, L/C & the procedure of lodgment & retirement of import bills.

- To be familiar with day to day functioning and service offered by a commercial bank.

- To determine the satisfaction level of clients with the present procedure.

Finally to identify problems and to provide some suggestions for the improvement of all transactions & other services of BASIC Bank Ltd.

1.4 Scope of the Study:

This report covers the details of BASIC Bank’s practices about all activities emphasiz A N Marketing Strategy of Banking Practice”. This report consists of the writer’s observations and on the job experiences during the internship period in the all Departments of Shantinagar Branch. This report emphasizes on the sequential activities involved and used by BASIC Bank Ltd. for all transactions. The report also focuses on the impact of the foreign exchange activities upon the clients. Finally it incorporates an evaluation of the different aspects of the export-import process in comparison to other competitor banks and recommends some measures to further strengthen its all departments.

1.5 Methodology:

To make the Report more meaningful and presentable, two sources of data and information have been used widely

Both primary and secondary data sources were used to generate the report.

Data Collection: Both the primary and secondary form of information is used to make the report more meaningful and presentable. The details of these sources are given below:

Primary Sources:

Major sources of information were discussions with the officers of all Departments especially Rumana Ahad (In-charge of Foreign Exchange Department), Fatema Khairunnesa (Assistant Manager) and Wahida Sultana (Assistant Officer) of BASIC Bank Limited, Shantinagar Branch.

Informal conversation with the clients.

Practical work exposure from the different desk of the Branch. Tools and Techniques for Analysis:

SWOT Analysis for analyzing the gathered information.

Many statistical tools like “Likert Scaling”,“Dichotomous Scaling” etc are used to analyze the data collected from various sources.

Secondary Sources:

“Annual Report 2008” of Prime Bank Limited.

Foreign Exchange Manual.

Periodicals published by Bangladesh Bank.

Various book, articles, compilations etc regarding Foreign Exchange Operations.

Various books of Business Communication.

Language: Abstract terminology and technical terms have been avoided as much as possible so that any person can realize the theme of the report.

Layout: All necessary parts of conventional formal report have been followed. The readers are expected to get a different taste from this report.

Limitation:

There were certain limitations regarding the study that is summarized below:

The main hindrance behind preparing this report was time. The tenure of the Internship program is only three months. So it is not possible to go through in depth within this short span of time.

Deficiencies in data required for the study.

Inaccurate or contradictory information.

Field practice varies with the standard practice that also created problem

Background of BASIC Bank Limited

Bangladesh Small Industries and Commerce Bank Limited, popularly known as BASIC Bank, is a state-owned scheduled bank. However, it is not a nationalized Bank. It is a bank-company and operates on the lines of a private bank. The very name Bangladesh Small Industries and Commerce Bank Limited is indicative of the nature of the bank. It is a blend of development and commercial banks.

BASIC Bank is a banking company registered under the Companies Act 1913. It was incorporated under this Act on the 2nd of August 1988. The bank started its operation from the 21st of January 1989. It is governed by the banking Companies Act 1991. The bank was established as the policy makers of the country felt the urgency for a bank in the private sector for financing Small Scale Industries (SSIs). At the outset, the bank started as a joint venture enterprise of the BCC Foundation with 70 percent shares and the government of Bangladesh (GOB) with the remaining 30 percent shares. The BCC Foundation being nonfunctional following the closure of the BCCI, the government of Bangladesh took over 100 percent ownership of BASIC on 4th June 1992. Thus the Bank is state owned. However, the Bank is not nationalized; it operates like a private bank as before.

The Memorandum and Articles of Association of the bank stipulate that 50 percent of loanable funds shall be invested in small and cottage industries sector. Thus the bank’s priority remains with promoting and financing development of small-scale industries in the country.

Adjudged as one of the soundest banks in Bangladesh, BASIC Bank Ltd is unique in its objective, it is a blend of development and commercial banking functions. 50% of its loanable funds require to be invested in small and cottage industries sector.

Steady growth in client base and in their high retention rate since bank’s inception testifies to the immense confidence they repose to its services. Diversified products, both liability and assets side, particularly a wide range of lending products related to development of small scale industries and micro enterprises, and commercial and trading activities attract entrepreneurs from varied economic fields. Along with promotions of products special importance is given to individual clients through providing personalized services. In fact, individuals matter in this Bank. This motto has been followed for development of clientele as well as human resources of the Bank.

Business Philosophy of BASIC Bank Limited

The statement of a company’s philosophy, often called the company creed, reflects or specifies the basic beliefs, values, aspirations, and philosophical priorities to which strategic decision makers are committed in managing the company.[1] The philosophy of BASIC Bank is to develop an ideal, excellent and unique financial institution in the banking industry. The sponsors’ perceptions were since inception and till now that BASIC Bank should be distinguished from other private owned and commercial banks operating in Bangladesh. Another philosophy is to provide best customer service so that BASIC Bank Ltd. can be grown as a leader in the banking industry rather than a follower. BASIC Bank Ltd. is tirelessly striving to achieve this philosophy. It is therefore evident that BASIC Bank Ltd. would seek fair return on owner’s equity as of its one prime goal. The profit earning goal is sought to be achieved by rendering maximum possible satisfaction to clients through quick and efficient services. Therefore, quality service to the clients is another important goal of BASIC Bank Ltd.

Mission of BASIC Bank Limited

The mission of any company is the unique purpose that sets it apart from other companies of its type and identifies the scope of its operations. In short, the mission describes the company’s product, market, and technological areas of emphasis in a way that reflects the values and priorities of the strategic decision makers.[2] The mission of BASIC Bank is to become one of the leading Banks in Bangladesh by its prudence. BASIC Bank’s business mission lies with the slogan “A Bank with international connection is to assist the business development of private sector institutions, industries and household”. It also emphasizes on a reasonable return from its investments to satisfy the shareholders. The mission of BASIC Bank can be summarized in the following points:

- BASIC Bank intends to provide better benefits and good returns to its customers and shareholders.

- It intends to meet the needs of its clients and enhance its profitability by creating corporate culture.

- BASIC Bank aims to ensure its competitive advantage by upgrading banking technology and information system.

- It provides high financial services to strengthen the well-being and success of individual, industries and business communities.

- BASIC Bank believes in strong capitalization.

- It maintains congenial atmosphere for which people are proud and eager to work with BASIC Bank Ltd.

- It believes in disciplined growth strategy.

- BASIC Bank encourages investors to boost up share market.

It intends to play more important role in the economic development of Bangladesh and its financial relations with the rest of the world by interlining both domestic and international operations.

Vision of the BASIC Bank Limited:

The gist of their vision is “Working Together For a Caring Society”. BASIC Bank Limited, as the name implies, is not a type of Bank in some countries on the globe, but is the first of its kind in Bangladesh. It believes in togetherness with its customers, in its march on the road to growth and progress with services.

- Provides the greatest return to the stakeholders by the stakeholders by achieving sound profitable growth.

- Be perceived by the customers and employees as the best whenever it operates.

Corporate Culture

- This bank is one of the most disciplined Banks with a distinctive corporate culture. Here we believe in shared meaning, shared understanding and shared sense making. Our people can see and understand events, objects and situation in a distinctive way. They mould their manners and etiquette, character individually to suit the purpose of the Bank and the needs of the customers who are of paramount importance to us. The people in the Bank see themselves as a tight knit team that believes in working together for growth. The corporate culture they belong has not been imposed; it has rather been achieved through their corporate conduct. The Bank achievement has been possible because of the able leadership; dedicated and committed services provided by all levels of management and staff which all possible because of a good and quality full corporate .

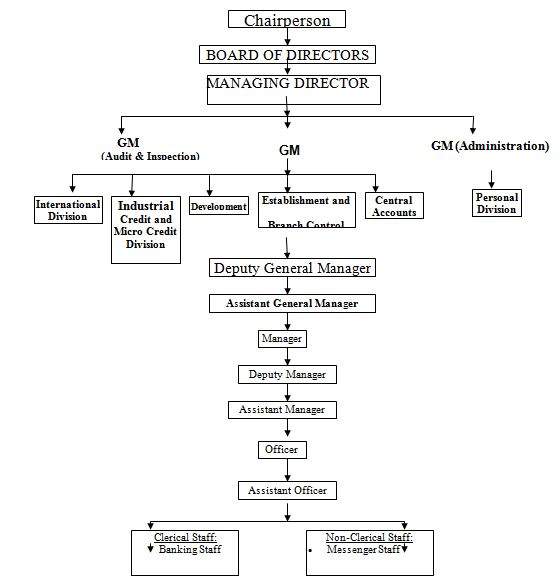

Hierarchy of position in Basic Bank

As stated earlier the government holds 100 percent ownership of the Bank. The Government of Bangladesh appoints all the Directors of the Board. The secretary of the Ministry of Industries is the Chairman of the Bank. Other Directors of the Bank are high Government and central Bank executives.

The Managing Director is an ex-officio member of the Board of Directors. There are at present seven Directors including the Managing Director.

Board of Directors

As on March 31, 2008

Md nurul amin Chairman

Secretary

Ministry of industries

Govt. of the peoples republic of Bangladesh

Shilpa Bhaban, Motijheel commercial area,Dhaka

Mr. Mohammad Mahbubur Rahman Director

Chairman

Bangladesh small & cottage industries corporation (BSCIC )

137-138, Motijheel commercial area,Dhaka

Mr. Mahbub Ahmed Director

Additional secretary, finance division

Ministry of finance, Govt. of the peoples republic of Bangladesh

Bangladesh secretariat, Dhaka

Mr. Md. Ehsanul Hoque Director

Director Marketing

Chief advisor’s office

Old sangsad Bhaban, tejgaon, Dhaka

Mr. Mustafa Mohiuddin Director

Joint secretary

Ministry of commerce, Govt. of the peoples republic of Bangladesh

Bangladesh secretariat, Dhaka

Mr. Md. Asaduzzaman khan Director

Executive director

Bangladesh bank, head office, Dhaka

Mr. A. H. Ekbal Hossain Managing Director

BASIC Bank Limited

Head office

Dhaka

Mr. Mesbahul Haque Company Secretary

ACNABIN Company Auditor

Chartered Accountants

Bsrs Bhaban (13th Floor )

12 karwan bazaar, Dhaka-1215

Management

The Managing Director heads the management. The two Marketing Managers and Departmental Heads in the Head office assist him. BASIC is different in respect hierarchical structure from other banks in that much more vertically integrated as far as reporting to the Chief executive is concerned. The Branch Managers of the Bank report direct to the Managing Director and, for functional purpose, to the Heads of Departments. Consequently, quick decision making in disposal of assess is ensured2.

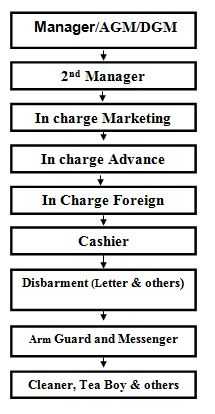

ORGANOGRAM OF BASIC BANK:

Branch Office Organogram

Human resource division

BASIC has a well- diversified pool of human resource, which is composed of personnel with high academic background. Also, there is a demographic characteristic. Most employees are comparatively young in age yet mature in experience. As at the end of 2007 the total employee strength was 721.

The bank follows strict recruitment policy in order to ensure that only the best people are recruited. The bank , so far, has recruited five batches of entry level management stuff.

Intensive training program, on a regular basis, is being imparted to employees of both management and non-management levels to meet the challenges in the banking industry and to adapt the changes and new working conditions. Human resource is the main driving force and quality human resource are the key sources for the success of todays banking business. Keeping view in mind and recognizing the importance of training for professional excellence BASIC Bank Ltd. Has established its own training cell in 2005with all modern facilities. In 2007 the cell arranged 22 btraining courses and provided training to as many as 360 employees of the bank. The bank also sends its employees to BIBM and other local and foreign institutions with a view to sharpening their knowledge base.

In 2007 total 122 employees of various stages were given promotion, which is almost 17.00 percent of total employees of the bank.

Branches of Basic Bank Ltd:

At present, there are thirty conveniently located branches in all over Bangladesh. These Branches are given below –

- Dhaka [Ten Branches in the capital city]

- Chittagong, [Eight Branches in the commercial city]

- Narayanganj, [Two Branches in]

- Norshinngdi, [One each in]

- Rajshahi,

- Saidpur,

- Bogra,

- Khulna,

- Jessore,

- Sylhet,

- Barisal,

- Chawmuhoni,

- Comilla,

- Moulvibazar, and

- Uttara

- Gazipur

T&T Bills Collection Booths :

- Sher-E-Bangla Nagar (Telephone Exchange Bhaban)

- Gulshan (Telephone Exchange Bhaban)

- Ramna (Telephone Exchange Bhaban)

18 out of 30 branches are authorized dealers of foreign exchange. This facilities speedy disposal of transaction of export and import trades.

A Foreign Exchange booth was opened at OsmaniInt’lAirport, Sylhet in April ’05 for mobilizing foreign exchange. This is one of the areas, where BASIC Bank is relatively lagging behind. The Bank has already signed an agreement with Placid NK Corporation, USA and Money Gram International, Minneapolis, USA, for obtaining foreign currency remittances. The bank is expected to sign agreement with Tele Money transfer, London, UK and some similar agreement with companies located in Saudi Arabia and UAE are going to be finalized shortly.

Financial report of Basic Bank ltd. For year ended 2006 & 20

| Particulars | 2,007 | 2,006 | |||

| Taka | Taka | ||||

| Property & Assets | |||||

| Cash | 2,125,018,037 | 1,522,871,378 | |||

| In Hand (Including Foreign Currency) | 237,050,824 | 228,750,752 | |||

| Balance with Bangladesh Bank & Sonali Bank | 1,887,967,213 | 1,294,120,626 | |||

| Balance With other Banks & Financial Institions | 6,937,531,606 | 4,191,369,656 | |||

| In Bangladesh | 6,510,675,772 | 3,927,113,757 | |||

| Outside Bangladesh | 426,855,834 | 264,255,899 | |||

| Money at call & Short Notice | 1,320,000,000 | 750,000,000 | |||

| Investments | 5,303,391,104 | 3,270,874,460 | |||

| Government | 5,271,306,344 | 3,241,864,700 | |||

| Others | 32,084,760 | 29,009,760 | |||

| Loans & Advances | 22,263,349,608 | 19,000,004,688 | |||

| Loans, Cash Credit, Overdraft etc. | 20,047,920,837 | 17,075,598,785 | |||

| Bills Purchased & Discounted | 2,215,428,771 | 1,924,405,903 | |||

| Fixed assets including Premises, Furniture & Fixture | 196,107,160 | 154,524,607 | |||

| Other Assets | 579,144,820 | 498,748,464 | |||

| Deffered Tax Asets | 49,363,500 | 28,701,686 | |||

| Non-Banking Assets |

| 0 | 0 | ||

| Total Assets | 38,773,905,836 | 29,417,094,939 | |||

| Liabilities & Capital | |||||

| Liabilities | |||||

| Borrowings From other Banks, Financial institutions & Agents | 1,385,810,725 | 830,065,983 | |||

| Depsits & Othter accounts | 31,947,979,101 | 24,084,659,391 | |||

| Current Deposit & Other Accounts etc | 2,867,190,249 | 2,370,449,860 | |||

| Bills Payable | 290,755,265 | 239,250,562 | |||

| Savings Bank Deposits | 886,304,853 | 1,007,791,880 | |||

| Fixed Deopsite | 27,903,728,734 | 20,467,167,089 | |||

| Bearer Certificate of Deposit | 0 | 0 | |||

| Other Liabilities | 2,843,532,719 | 2,263,371,938 | |||

| Total Liabilities | 36,177,322,545 | 27,178,097,312 | |||

| Capital/ Shareholders Equity | 2,596,583,291 | 2,238,997,627 | |||

| Paid up capital | 1,247,400,000 | 945,000,000 | |||

| Statutory Reserve | 1,045,085,405 | 883,456,765 | |||

| Others Reserve | 40,000,000 | 40,000,000 | |||

| Surplus in Profit & loss Account | 129,477,308 | 370,540,862 | |||

| Revaluation Reserve of HTM Securities |

| 134,620,578 | 0 | ||

| Total Liabilities & Shareholders’ eqity | 38,773,905,836 | 29,417,094,939 | |||

Profit and Loss Account (Income Statement)

| 2,007 | 2,006 | |||||

| Taka | Taka | |||||

| Interest Income | 2,866,572,741 | 2,278,549,727 | ||||

| Interest Paid on Deposits and Borrowings | (1,928,472,617) | (1,315,864,251) | ||||

| Net Interest Income | 938,100,124 | 962,685,476 | ||||

| Income on Investment | 206,480,219 | 225,733,106 | ||||

| Commission, Exchange and Brokerage | 414,018,179 | 307,290,200 | ||||

| Other Operating Income | 62,389,876 | 58,749,929 | ||||

| Total Operating Income (a) |

| 1,554,458,711 | ||||

| Salaries and Allowance | 331,184,032 | 292,206,732 | ||||

| Rent, Tax, Insurance, Electricity etc. | 54,082,864 | 44,155,004 | ||||

| Legal Expenses | 1,912,794 | 1,375,225 | ||||

| Postage, Stamp, Telecommunication etc. | 26,863,912 | 21,637,470 | ||||

| Auditors Fee | 150,000 | 120,000 | ||||

| Stationary, Printing, Advertisements Etc. | 12,871,200 | 18,180,340 | ||||

| Managing Directors Salaries | 2,150,000 | 1,910,000 | ||||

| Directors’ Fee | 517,000 | 422,500 | ||||

| Depreciation And Repaires Of Fixed Assets | 55,414,430 | 43,170,735 | ||||

| other expenditure | 447,796,387 | 39,230,311 | ||||

| total operating expenses (b) | 529,942,619 | 462,444,317 | ||||

| prfit before provision (c)=(a-b) | 1,091,108,779 | 1,092,014,394 | ||||

| provision for loan & advances | 276,575,540 | 80,393,610 | ||||

| provision diminution in value of invstmnts | 0 | 0 | ||||

| provision for posted bill | 6,390,039 | 0 | ||||

| interest subsidy adjustment | 0 | 0 | ||||

| total provision (d) | 282,965,579 | 80,393,610 | ||||

| Profit Before Taxation(c-d) | 808,143,200 | 1,011,620,784 | ||||

| Provision for Income Tax | 545,839,928 | 467,463,971 | ||||

| Deffered Tax Income/ Expenses | (20,661,814) | (9,981,681) | ||||

| 457,482,290 | |||||

| Profits After Taxation | 282,965,086 | 554,138,494 | ||||

| Appropriation: | ||||||

| Statutory Reserve | 161,628,640 | 202,324,157 | ||||

| Retained Earning for Year Carried Forward | 121,336,446 | 351,814,337 | ||||

| 282,965,086 | 554,138,494 | |||||

| Earning per Ordinary Share (eps) | 23 | 59 | ||||

Cash Flow Statement

| 2,007 | 2,006 | ||||||

| Taka | Taka | ||||||

| Cash inflow from operating activities | |||||||

| Interest received in cash | 3,054,156,410 | 2,322,359,212 | |||||

| Interest paid by cash | (1,618,246,317) | (1,166,162,508) | |||||

| Dividend received in cash | 5,560,480 | 4,920,340 | |||||

| Fees & commission received in cash | 414,081,179 | 307,290,200 | |||||

| Recovery of loans previously written off | 5,626,068 | 4,439,712 | |||||

| Cash paid to employees | (295,781,826) | (257,876,464) | |||||

| Cash paid to employees | to suppliers | (12,871,200) | (18,180,340) | ||||

| Income tax paid | (641,874,003) | (296,255,115) | |||||

| Received from other operating activities | 54,687,145 | 53,013,833 | |||||

| Paid for other operating activities | (138,902,279) | (119,118,468) | |||||

| Operating profit before changes in operating assets liabilities | 826,435,657 | 834,430,402 | |||||

| Changes in operating assets &liabilities Statutory Deposit | 1,359,986,000 | 876,121,000 | |||||

| Purchase/sales of Trading Securities | (1,425,400,000) | 1,243,192,500 | |||||

| Loans & advances to other Banks | 0 | 0 | |||||

| Loans & advances to other Banks | (3,263,344,921) | (3,660,653,841) | |||||

| Other assets (item-wise) | 154,247,833 | (173,599,945) | |||||

| Deposits From other Banks | (23,671,000) | 28,949,000 | |||||

| DepositsFrom | customers | 6,527,004,710 | 854,008,051 | ||||

| Trading Liabilities | 0 | 0 | |||||

| Other Liabilities | (40,875,739) | (179,538,859) | |||||

| A. Net Cash providd by operating activities | 4,114,382,539 | (177,091,692) | |||||

| Cash inflows from investing activities | |||||||

| Proceeds From sale of Securities | 2,500,000 | 27,500,000 | |||||

| Purchased of fixed assets | (609,616,644) | (1,016,200) | |||||

| Sales of fixed assets | (87,062,414) | (50,398,179) | |||||

| 2,360,386 | 1,922,847 | ||||||

| B. Net Cash Provided by investing activities | (691,818,672) | (21,991,532) | |||||

| Cash inflows from financing activities | |||||||

| Increase /(decrease) of long term borrowings | 555,744,742 | (107,449,587) | |||||

| Payment of Dividend | (60,000,000) | (60,000,000) | |||||

| C. Net cash Provided by financing activities | 495,744,742 | (167,449,587) | |||||

| Net increase of cash & cash equivalent (A+B+C) |

| 3,918,308,609 | (366,532,811) | ||||

| Effects of exchange rate changes on cash & equivalent | |||||||

| Opening Cash & Cash equipment |

| 6,464,241,034 | 6,830,773,845 | ||||

| Closing Cash & Cash Equivalent | 10,382,549,643 | 6,464,241,034 | |||||

| Analysis of Closing Cash & Cash Equivalent | |||||||

| Cash in hand & balance with BB& Sonali Bank | 2,125,018,037 | 1,522,871,379 | |||||

| Cash with other banks | 6,937,531,606 | 4,191,369,655 | |||||

| Money at call & short notice | 1,320,000,000 | 750,000,000 | |||||

| Total | 10,382,549,643 | 6,464,241,034 | |||||

Credit Rating Report

CAMEL Rating of Banks:(Weekly “Investment”, July 2, 2006)

Central bank the regulatory authority of country’s banking sector has rated the positions of different banks based on the performances of December 2005. The serial has been prepared on the basis of credit and asset management performance as well as local banks first then foreign banks. It is mentionable that Prime Bank Ltd. and Mutual Trust Bank Ltd. got the top position in “A” class banks. The performance of both of the banks are same but volume of business, net worth and customer base of Prime Bank is almost double than Mutual Trust. The criteria for measuring the performance of all the commercial banks include Capital adequacy, Asset’s Quality, Management efficiency, Earnings and Liquidity maintenance (CAMEL).

The list of the banks according to CAMEL rating is given in the following;

A- Class Banks:

- Prime Bank Ltd. & Mutual Trust Bank Ltd.

- Dutch Bangla Bank Ltd.

- Bank Asia Ltd.

- EXIM Bank Ltd.

- Mercantile Bank Ltd.

- Jamuna Bank Ltd.

- Dhaka Bank Ltd.

- 8. BASIC Bank Ltd.

- Standard Bank Ltd.

- Commercial Bank of Ceylon.

- Citibank N.A.

- State Bank of India

- HSBC

B – Class Banks:

1. Eastern Bank Ltd.

2. Premier Bank Ltd.

3. The Trust Bank Ltd.

4. BRAC Bank Ltd.

5. Southeast Bank Ltd.

6. NCC Bank Ltd.

7. One Bank Ltd.

8. Standard Chartered

9. Woori Bank

10. Bank Alfalah Ltd.

11. National Bank of Pakistan.

C- Class Banks:

1. Islami Bank Bangladesh Ltd.

2. Pubali Bank Ltd.

3. Uttara Bank Ltd.

4. National Bank Ltd.

5. The City Bank Ltd.

6. UCBL

7. Shahjalal Islami Bank Ltd.

8. Al – Arafah Islami Bank Ltd.

9. IFIC Bank Ltd.

10. AB Bank Ltd.

11. First Security Bank Ltd.

12. Habib Bank Ltd.

D- Class Banks:

1. Social Investment Bank Ltd.

2. Bangladesh Commerce Bank Ltd.

3. Agrani Bank

4. Janata Bank

5. Rupali Bank Ltd.

6. Sonali Bank

7. Bangladesh Shilpa Rin Sangstha

8. RAKUB

E – Class Banks:

1. Bangladesh Krishi Bank

2. Bangladesh Shilpa Bank

3. The Oriental Bank Ltd.

Marketing Strategy of Banking:

Marketing department performs the majority functions of a bank. It is the core department of any bank. The activities of GB of BASIC Bank Ltd are mainly divided into the following categories:

- Account opening section

- Local remittance section

- Online branch banking section

- Deposit scheme section

- Clearing section

- Collection section

- Cash section

- Accounts section

All of the above activities of GB are discussed elaborately in the next chapter which is the core chapter of this report.

Account Opening Section:

To establish a Banker and customer relationship Account opening is the first step. Opening of an account binds the Banker and customer into contractual relationship. But selection of customer for opening an account is very crucial for a Bank. Indeed, fraud and forgery of all kinds start by opening account. So, the Bank takes extremely cautious measure in its selection of customers.

Types of Account:

- Current Account.

- Savings Account.

Fixed Deposit Account.

A Corporative table of the product & their restrictive profit RATE:

Name of Deposit | Profit Rate(%) |

| Mudaraba Term Deposit Receipts | |

| 8.00 |

| 12.50 |

| 12.75 |

| 13.00 |

| Mudaraba Savings Deposit | 6.00 |

| Mudaraba Notice Deposit A/C | 5.50 |

| Mudaraba Scheme Deposit | |

| 12.00 |

| 12.00 |

| 12.00 |

| 12.00 |

| 12.00 |

| 12.00 |

| 12.00 |

| 12.00 |

| 12.00 |

| 12.00 |

| 12.25 |

| 12.00 |

| 12.00 |

| 12.00 |

Procedure to open an Account:

or opening an account, at first the prospective account holder will apply for opening an account by filling up account opening form. Account opening form consists of the name of the branch, type of account, name of the applicant(s), present address, permanent address, passport number (if any), date of birth, nationality, occupation, nominee(s), special instruction (if any), initial deposit, specimen signature(s) of the applicant(s), introducer’s information etc.

- The prospective customer should be properly introduced by the followings:

- An existing customer of the bank.

- Officials of the bank not below the rank of Assistant Officer.

- A respectable person of the locality who is well known to the

Manager or authorized officer.

- Two copies of passport size photograph duly attested by the introducer.

- Signature of the prospective account holder in the account opening form and on the specimen signature card duly attested by the introducer.

- Then the concerned authority will allocate a number for the new account.

- The customer then deposit the “initial deposit” by filling up a deposit slips. Initial

deposit to open a current account in bank is Tk. 1000.00 and saving account is Tk. 100.00.

After depositing the initial deposit, the account is considered to be opened. The Bank maintains all of its accounts in computer. After depositing the initial deposit, Bank records it in the computer by giving new account number. Then it issues cheque book requisition slip by the customer. Then it distributes all relevant papers to respective department.

Requirment of Opening an Account:

(A) Joint Account:

If the account is a joint account, then the joint account holder should submit a declaration and operational instructions of the account along with their signature. The declaration is

“Any balance to the credit of the account is and shall be owned by us as joint depositors. Any liability whatsoever incurred in respect of this account shall be joint and several.”

(B) Partnership firm:

The following documents have to be submitted for preparing an account of a partnership firm:

- Partnership deed.

- (a) If the partnership firm is a registered one, then one copy of registration forms.

(b) If not, then a copy of certificate from the notary public.

(C) Limited Company:

For the opening of an account of a limited company, following documents have to be submitted:

- A copy of resolution of the company that the company decided to open an account in the BASIC Bank.

- Certified true copy of the Memorandum & Articles of Association of the Company.

- Certificate of Incorporation of the company for inspection and return along with a duly certified Photocopy for Bank’s records.

- Certificate from the Registrar of Joint Stock Companies that the company is entitled to commence business (in case of Public Ltd. Co. for inspection and return) along with a duly certified Photocopy for Bank’s records.

- Latest copy of balance sheet.

- Extract of Resolution of the Board/Marketing Meeting of the company for opening the account and authorization for its operation duly certified by the Chairman/Managing Director of the company.

- List of Directors with address (a latest certified copy of Form-XII)

(D) Club/Society:

Following documents have to be obtained in case of the account of the club or society:

- Up to date list of office bearers.

- Certified copy of Resolution for opening and operation of account.

- Certified copy of Byelaw and Regulations/Constitution.

- Copy of Government Approval (if registered).

(E) Cooperative Society

Following documents have to be obtained in case of the account of Cooperative Society:

- Copy of Bye-Law duly certified by the Co-operative Officer.

- Up to date list of office bearers.

- Resolution of the Executive Committee as regard of the account.

- Certified copy of Certificate of Registration issued by the registrar, Co-operative societies.

(F) Non-Govt. College / School / Madrasha / Muktab:

Following documents have to be obtained in case of the account of non-govt. College / school / madrasha / muktab:

- Up-to-date list of Governing Body/Managing Committee.

- Copy of Resolution of the Governing Body/Managing Committee authorizing opening and operation of the account duly certified by Gazetted Officer.

(G) Trustee Board:

Following documents have to be obtained in case of the account of trustee board:

- Prior approval of the Head Office of BASIC Bank.

- Certified copy of Deed of Trust, up to date list of members of the Trustee Board and certified copy of the Resolution of Trustee Board to open and operate the account.

(H) Minor’s Account:

Following documents have to be obtained in case of the account of minor:

- Putting the word “MINOR” after the title of the account.

- Recording of the special instruction of operation of the account.

- The AOF is to be filled in and signed by either the parents or the legal guardian appointed by the court of law and not by the minor.

Issuing a cheque book:If the cheque has no defect and it is payable,the in charge will sing in the cheque affixing signature verification seed along with his or her initial and will cancel the cheque by string it by pen.The officers will handover the payment to the appropriate payee.

Local Remittance Scetion:

Local remittance is one of the main components of Marketing Strategy of Banking. The activities of local remittance are :

- Telegraphic Transfer,

- Demand Draft issue,

- Pay order

Telegraphic Transfer (TT):

It is an order from the issuing branch to the drawer bank / branch for payment of a certain sum of money to the beneficiary. The payment instruction is sent by telex and funds are paid to the beneficiary through his account maintained with the drawee branch or through a pay order if no account is maintained with the drawee branch.

Procedure of issuing TT:

Following procedures are followed while issuing of TT:

- The applicant fills up the relevant parts of the prescribed application form in triplicate, duly signed the same and gives it to the GB.

- GB will fill up the commission part for bank’s use and request the applicant to deposit necessary cash or cheque at the cash booth.

- GB will prepare telex in appropriate form, sign it and send it to the telex operator for transmission of the message.

- GB will prepare necessary advice. Debit advice is sent to the client if client’s account is debited for the amount of T.T.

- T.T. Confirmation Advice is sent to the drawer branch.

- Credit Ticket (second copy of the application form) is used to credit the PBL Marketing Account.

- The first copy of the application form will be treated as Debit Ticket while the second copy will be treated as Credit Ticket. The third copy will be handed over to the applicant as customer’s copy.

Accounting Treatment:

For telegraphic transfer, BASIC Bank gives the following entries—

Client’s Account .Dr.

Prime Marketing Account…….. .Cr.

Telex Account………………. Cr.

Commission Account……….. Cr.

Payment of T.T.

On receipt of T.T. payment instructions the following entries are passed by the drawee branch if the T.T. is found to be correct on verification of the Test number—

a) Prime Marketing Account Dr.

DAD Account – TT Payable……… Cr.

b) DAD Account – TT Payable Dr.

Client’s Account/Pay Order……….. Cr.

In case the beneficiary does not maintain any account with the drawee branch a pay order will be issued in favor of the payee and sent to his banker / local address as the case may be.

Every branch maintains a prescribed T.T. Payable Register. All the particulars of T.T. are to be properly recorded in this register duly authenticated. A separate Type of T.T. confirmation advice is sent to the drawee branch on the same day. On receipt of T.T. confirmation advice, the particulars of T.T. are verified with reference to particulars already recorded in the T.T. payable register.

Demamd Draff (DD):

Sometimes customers use demand draft for the transfer of money from one place to another. For getting a demand draft, customer has to fill up an application form. The form contains date, name and address of the applicant, signature of the applicant, cheque number (if cheque is given for issuing the DD), draft number, name of the payee, name of the branch on which the DD will be drawn and the amount of the DD. The form will be duly signed by the applicant and by the authorized officer. The bank charges .15% commission on the face value of DD as service charge.

Process of issuing Local Draft:

Following procedures are followed while issuing local draft—

- Get the application form properly filled up and signed by the applicant.

- Complete the lower portion of the form for the bank’s use.

- Calculate the total amount including the bank’s commission.

- If the cheque is presented for the local draft, the officer should get the cheque duly passed for payment by the authorized person and record the particulars of local draft on the back of the cheque.

- If the client wants to debit his account for the payment of the draft amount, the officer should get the account holder’s signature verified properly, from signature card on record of the branch and debit clients account for the total amount including commission.

- The first copy of the application form will be treated as Debit Ticket while the second copy will be treated as Credit Ticket and kept by the GB. The third copy is handed over to the applicant as customer’s copy.

- The GB Department maintains a prescribed L.D. Issue Register. All the required particulars of LDs issued by the bank should be entered in that register duly authenticated.

Duplicate Draf:

Duplicate Draft is not normally issued unless getting of satisfactory evidence is produced regarding loss of the draft. If the L.D. is reported to be lost or stolen, the issuing branch on receipt of a written request from the purchaser may issue a duplicate draft.

Before issuing duplicate L.D. the branch should observe the followings—

- Verify the purchaser’s signature on the request letter from the signature appearing on the original application form.

- Immediately issue a stop payment instruction to the drawee branch under advice of head office and obtain confirmation of non-payment the L.D. in acquisition.

- After the drawee branch has acknowledged the stop payment order and confirmed that the local draft in acquisition remains unpaid at their end, the issuing branch should obtain an Indemnity Bond on stamp paper as per prescribed format from the purchaser duly signed by him. The branch will thereafter write to head office for their approval to issue a duplicate draft.

- The head office on receipt of the request from the issuing branch will immediately issue a caution circular to all the branches regarding the lost of the local draft asking them to record stop payment.

- The head office will thereafter issue clearance to the issuing branch for issuing for issuing a duplicate draft in lieu of original reported lost.

- On receipt of the clearance from head office, the issuing branch will issue a completely fresh draft marking clearly the words duplicate issued in lieu of original draft no………………. dated …………….in bold letters on the top of the front page of the draft. The printed serial number on the draft should not however be struck off. Intimation should be given to the drawee branch furnishing full particulars of the duplicate draft.

- The particulars of the duplicate draft must resemble those of the original draft in all respects, i.e., all the particulars to the duplicate draft must be identical with those in the original draft. No further IBCA is to be issued for the duplicate draft.

- Prescribed duplicate issuance charge is to be recovered for issuing the duplicate draft and credited to “Income Account”.

Cancellation of Local Draft:

The followings are followed while canceling a L.D.—

- The purchaser should submit a written request for cancellation of the L.D. attaching therewith the original L.D.

- The signature of the purchaser will have to be verified from the original application form.

- Manager’s prior permission is to be obtained before refunding the amount of draft.

- Cancellation charge is to be recovered from the applicant and only the amount of the draft less cancellation charge should be refunded. Commission charge, posted charge etc. recovered for issuing the L.D. should not be refunded.

- The original entries are to be reversed giving proper narration. An IBDA for the cancelled L.D. should be issued on the drawee branch.

- Cancellation of L.D. should also be recorded in the L.D. Issue Register.

Payment of L.D.:

While payment of L.D. BASIC Bank Ltd. performs the following functions—

- On receipt of Credit Advice (IBCA) from the issuing branch the following entries are to be passed –

BASIC Marketing Account Dr.

DAD Account………. Cr.

- When L.D. is presented for payment at the paying branch, its details are to be carefully examined with reference to the following points—

- Whether the draft is drawn on the Local office.

- Whether the draft is crossed or not. Amount of crossed draft is not paid in cash to the payee but to be paid to his account with a bank.

- Draft must have to be signed by two authorized officers of the issuing branch. Their signatures are to be verified from the specimen signature book for being sure that draft that the draft is genuine. The verifier should put his initial.

- Endorsement on the back of the draft must be regular in case the draft is presented through clearing.

- The amount of the draft should not exceed the amount written in red ink at the top of the draft.

- The payee is to be properly identified in case of cash payment.

- The particulars of the draft i.e. the draft number, date, amount and the name of the payee should be verified from the L.D. Payable Register.

- In case of payment, the draft should be cancelled with red ink. The date of payment should be recorded in the L.D. Payable Register.

Accounting Treatment:

While payment:

DAD –L.D. Payable Account…………….. Dr.

Client’s Account………………………….. Cr.

An IBCA should be sent with this.

Stop payment of Local Draft:

The payee or purchaser of the draft cannot give stop payment instruction to the drawee branch. If the paying branch receives a request from the purchaser of the draft for stopping payment of the draft, it will ask the purchaser to approach the issuing branch about the purpose. The paying branch should however exercise necessary precaution in this regard. Only the issuing branch can issue instruction for stop payment of the draft under special circumstances.

Pay Order (PO):

For issuing a pay order, the client is to submit an application to GB in the prescribed form. This form should be properly filled up and signed. For issuing pay order BASIC charges commission on the following rate—

- For Tk. 1 to 10,000, the commission is Tk.10.

- For Tk. 10,001 to 1,00,000, the commission s Tk. 15.

- For Tk 1,00,001 to 5,00,000, the commission is Tk. 50.

- For Tk 5,00,001 to 10,00,000, the commission is Tk. 75.

- For Tk 5,00,000 above, the commission is Tk. 100.

Payment of Pay Order:

The pay order is presented to the bank either through clearance or for credit to the client’s account. While payment, relative entry is given in the pay order register with the date of payment.

Cancellation of Pay Order:

- The following procedures should be followed for the cancellation of the pay order:

- The client should submit a written request for canceling the pay order attaching therewith the original pay order.

- The signature of the purchaser will have to be verified from the original application form.

- Manager’s prior permission is to be obtained before refunding the amount of the pay order.

- Cancellation charge is to be recovered from the applicant and only the amount of the pay order less cancellation charge should be refunded. Commission recorded for issuing of the original pay order should not be refunded.

- Then the officer should write “cancelled” on the pay order

- The original entries should be reversed with narration.

- Cancellation of the pay order should also be recorded in the register.

Clearing Section

According to the Article 37(2) of Bangladesh Bank Order, 1972, the banks, which are the member of the clearinghouse, are called as Scheduled Banks. The scheduled banks clear the cheque drawn upon one another through the clearinghouse. This is an arrangement by the central bank where everyday the representative of the member banks gathers to clear the cheque. Banks for credit of the proceeds to the customers’ accounts accept Cheque and other similar instruments. The bank receives many such instruments during the day from account holders. Many of these instruments are drawn payable at other banks. If they were to be presented at the drawee banks to collect the proceeds, it would be necessary to employ many messengers for the purpose. Similarly, there would be many cheque drawn on this the messengers of other banks would present bank and them at the counter. The whole process of collection and payment would involve considerable labor, delay, risk and expenditure.

All the labor, Risk, delay and expenditure are substantially reduced, by the representatives of all the banks meeting at a specified time, for exchanging the instruments and arriving at the net position regarding receipt or payment. The place where the banks meet and settle their dues is called the Clearinghouse.

Activities of the Section:

(a) Preparation of Clearing Outward and Inward Lodgment and record maintenance of the same.

(b) Batch posting as and when required.

On receipt of instruments, the same is endorsed here. Then clearing section will sent IBDA to head Office for clearing purpose and on receipt of IBCA from Head Office amount is credited to customers account and vice versa. If the instrument is return then the same is given back to the customer.

Collection Section:

Checks, drafts etc. are drown on bank located outside clearing house are sent for collection. Shantinagar Branch collects its client’s above-mentioned instruments from other branches of BASIC Bank and branches other than BASIC Bank. In case of out ward bills for collection customers account is credited after finishing the collection processor. And in case of in ward bills customers account is debited for this purpose. So it places dual role as follows:

i) Collecting Banker

ii) Paying Banker.

Activities of the Section:

- Preparing of Outward and Inward Collection Item.

- Inter-Branch Transfer.

- Batch posting and checking as and when required.

- Other works as and when require.

Collection is done when

- Paying Bank is located out side DhakaCity.

- Paying Bank is other branches of BASIC Bank situated inside DhakaCity.

Paying Bank is outside Dhaka City:

Collection department of Shantinagar Branch, BASIC Bank sends outward bills for collection (OBC) to the concerned paying bank to get inter Bank Credit Advice (IBCA) from paying Bank. If the paying bank dishonors the instrument, the same is returned to principal Branch.

The Paying Bank of their own branches inside Dhaka City:

Collection Department sends transfer delivery item to other branches of same bank situated inside DhakaCity. Upon receiving IBCA customer’s a/c is credited.

Commission for Collection:

Up to 1 lac ——————————————— 0.15%

Above 1 lac——————————————— 0.10%

Above 5lac ———————————————-0.05%

Maximum charge is Tk. 3000 and minimum charge is Tk.20.

Accounts Section:

In banking business transactions are done every day and these transactions are to be recorded properly and systematically as the banks deal with the depositors’ money. Any deviation in proper recording may hamper public confidence and the bank has to suffer a lot. Improper recording of transactions will lead to the mismatch in the debit side and credit side. To avoid these mishaps, the bank provides a separate department whose function is to check the mistakes in passing vouchers or wrong entries or fraud or forgery. This department is called Accounts Department.Besides these, the branch has to prepare some internal statements as well as some statutory statements, which are to be submitted to the Central Bank and the Head Office. This department prepares all these statements.

Functions of Accounting Department:

We can divide the functions of accounting department into two categories. One is day-to-day task and another is periodical task.

- a. Day to day functions: Here day-to-day function refers to the every day tasks. Accounting department of PBL performs the following day to day functions:

- Recording of transaction in the cashbook, Marketing and subsidiary ledger.

- Preparing the daily position of deposit and cash.

- Making the payment of the expense of the branch.

- Recordings of inter branch fund transfer.

- Checking whether all the vouchers are correctly passed.

- Recording the voucher in the voucher register.

- Packing and maintains the total debit and total credit vouchers.

b. Periodical functions: Periodical functions of accounts department include the preparation of different weekly, fortnightly, monthly, quarterly and annual statement. The accounts department prepares the following statements:

- Monthly statement of deposits, loans and advances, profit and loss etc.

- Quarterly statement of deposits, loans and advances, profit and loss etc.

- Yearly statement of deposits, loans and advances, profit and loss etc.

- Yearly statement of classified Loans and Advances.

- Statement of Affairs.

- Yearly Budget of the Branch, etc.

Cash Section:

Cash section is a very sensitive organ of the branch and handle with extra care. Operation of this section begins at the start of the banking hour. Cash officer begins his/her transaction with taking money from the vault, known as the opening cash balance. Vault is kept in a much secured room. Keys to the room are kept under control of cash officer and branch in charge. The amount of opening cash balance is entered into a register. After whole days’ transaction, the surplus money remain in the cash counter is put back in the vault and known as the closing balance. Money is received and paid in this section

Cash Receipt:

- At first the depositor fills up the Deposit in Slip. For saving account and current account same Deposit in Slip is used in this Branch.

- After filling the required deposit in slip, depositor deposits the money.

- Officers at the cash counter receives the money, count it, enter the amount of money in the register kept at the counter, seal the deposit in slip and sign on it with date and keep the banks’ part of the slip. Other part is given to the depositor.

- In this branch, i.e., Motijheel Branch, two different officers maintain two different books for entering such entries. All deposits of saving account are maintained by one officer and other accounts by another officer.

- At the end of the day entries of both of these registers are cross checked with the register kept at the cash counter to see whether the transactions are correct or not.

Cash Payment:

- When a person comes to the bank to cash a cheque, (s)he first gives it to the computer desk to know the position of the check and posting of the cheque. If the account has sufficient fund the computer in charge will post it into the computer, will sign it and seal it.

- This cheque is then sent to the concerned officer. There are two officers who verify the cheques – one for savings and similar types of account and another for current and similar types of account.

- After receiving the cheque respective officer first checks it very carefully for any kind of fraudulent activity. (S) He also checks the date of the cheque, amount in word, amount in figure and signature of the drawer.

- If the instrument is free of all kind of error the officer will ask the bearer to sign on the back of it.

- He will then put his/her initial beside the bearers’ signature. (S)he will also sign it on its face, will write down the amount by red pen.

- Then the cheque will be sent to the cash counter. At the cash counter bearer will be asked again to sign on the back of the instrument.

- The cash officer will then enter the details of the cheque in his/her register and will pay the money to the bearer.

- At the end of the day these registers will be compared to ensure the correctness of the entries.

Providing Loans & Advances

Actual fund of BASIC Bank is 35506 million taka as on 31-03-2008 and the loanable fund is 25915 million taka. The sources of these funds are;

a) Deposit

b) Capital & reserve

c) Borrowing

(Fig. in million Taka)

| SL. No | Year | Total Advance |

| 01 | 2007 | 19069.87 |

| 02 | 2006 | 17026.67 |

| 03 | 2005 | 15339.35 |

| 04 | 2004 | 12000.15 |

| 05 | 2003 | 9282.20 |

| 06 | 2002 | 7957.04 |

| 07 | 2001 | 6260.78 |

| 08 | 2000 | 4618.90 |

| 09 | 1999 | 3960.11 |

| 10 | 1998 | 3218.90 |

| 11 | 1997 | 2630.90 |

| 12 | 1996 | 1724.81 |

| 13 | 1995 | 1561.29 |

| 14 | 1994 | 1112.24 |

| 15 | 1993 | 986.61 |

| 16 | 1992 | 715.75 |

Industrial Credit

BASIC Bank’s services are directed towards the entrepreneurs in the small industries sector. A small industry, as per Industrial policy 1999 approved by the Cabinet, has been defined as an industrial undertaking whose total fixed investment is less than Tk.100 million.

The industrial loan reflected a significant growth of 22.59 percent over the previous year. Total outstanding industrial loans including term and working capital stood at Taka 12,243.56 million at the end of 2006 compared to Taka 9,987.50 million of 2005. Total outstanding term loan stood at Taka 3,897.12 million as on December 31, 2006 compared to Taka 3,517.85 million in 2005 reflecting a growth of 10.78 percent. The outstanding working capital finance extended to industrial units stood at Taka 8,346.44 million at the end of the reporting period compared to Taka 6,479.71 million in 2005. Growth rate here was 29.00 percent. BASIC Bank’s services are specially directed towards promotion and development of small industries. Its exposure to small and medium industries sector accounted for 53.43 percent of the total loans and advances. During the year total of 159 projects were sanctioned term loan. Out of which 89 were new and the rest were under BMRE of the existing projects. As on 31 December, 647 projects were in the portfolio of the bank. The textile sector including garments being one of the major contributors to national economy dominated the loan portfolio of the Bank. Other sectors financed include engineering; food and allied industries; chemicals, pharmaceuticals and allied industries; paper, board, printing and packaging; glass; ceramic; and other non-metallic goods and jute products. Recovery rate of project loan was 89 percent. Recovery rate of this sector is above 85% which is remarkable.

(Fig in million Taka)

| SL. No | Year | Industrial Credit. |

| 1 | 2007 | 13590.35 |

| 02 | 2006 | 12243.56 |

| 03 | 2005 | 9987.50 |

| 04 | 2004 | 7691.20 |

| 05 | 2003 | 6252.00 |

| 06 | 2002 | 4654.00 |

| 07 | 2001 | 3769.00 |

| 08 | 2000 | 2737.50 |

| 09 | 1999 | 2062.19 |

| 10 | 1998 | 2028.50 |

| 11 | 1997 | 1408.25 |

| 12 | 1996 | 914.40 |

| 13 | 1995 | 915.20 |

| 14 | 1994 | 724.70 |

| 15 | 1993 | —- |

| 16 | 1992 | —- |

Commercial Credit

The Bank also supports development of trade, business and other commercial activities in the country. It covers the full range of services to the exporters and importers extending various facilities such as cash credit, export cash credit, packing credit, short term loans, local and foreign bills purchase facilities. As on December31, 2006 total outstanding commercial loans stood at Taka 6,397.21 million compared to Taka 5,013.55 million in 2005.

Micro Credit

BASIC Bank launched a Micro Credit Scheme in 1994. Micro Credit Scheme provides for the poor for generation of employment and income on a sustainable basis particularly in urban and suburban areas. Recovery rate in micro credit sector is almost 100%. The Bank follows three systems of credit delivery. These are:

- Lending to the NGOs who on-lend to their members. At present there are 15 such NGOs.

- Lending direct to the targets groups or ultimate borrowers under the Bank’s own management.

- Lending direct to the member-borrowers and NGOs providing nonfinancial services like group formation and monitoring and supervision on exchange for a supervision fee.

- At the end of 2006, total amount of Taka 359.24 million remained outstanding as against Taka 338.30 million in 2005. Recovery rate during this period remained at a satisfactory level of 100.00 percent.

(Fig in million Taka)

SL. No. | Year | Micro Credit |

01 | 2007 | 398.75 |

02 | 2006 | 359.24 |

03 | 2005 | 338.30 |

04 | 2004 | 284.10 |

05 | 2003 | 186.20 |

06 | 2002 | 104.00 |

07 | 2001 | 183.50 |

08 | 2000 | 120.40 |

09 | 1999 | 103.90 |

10 | 1998 | 68.70 |

11 | 1997 | 45.10 |

12 | 1996 | 12.31 |

13 | 1995 | 4.59 |

14 | 1994 | —- |

15 | 1993 | —- |

16 | 1992 | —- |

Foreign Trade

The bank achieved substantial growth in export in 2006 and the performance of the bank in import business was also satisfactory. The Bank handled total export business of Taka 15,463.74 million and import business of Taka 17,804.27 million in 2005. The export and import business grew by 39.34 percent and 26.32 percent respectively. Major items of exports were garments, jute products, textile, leather etc. Items of import included mainly industrial raw materials, garments accessories, capital machinery, food items and other essential commodities.

The Bank became a proud member of SWIFT (Society for Worldwide Inter bank Financial Telecommunication) that would pave the way to achieving uninterrupted communication related to banking for international trade business and fund transfer.

Other Activities

The Bank provides services for remittance, underwriting, guarantee, public offering of shares etc. The bank also provides funds to investment and leasing companies. The Bank has recently created a venture capital fund for equity support to innovative but risky projects.

Sources of Fund

BASIC collects fund from deposits from the members of the public, borrowing and shareholders’ equity. It also borrowed funds from the following sources:

- Bangladesh Bank

- Asian Development Bank (ADB) and

- KfW German Development Bank.

Funding from all of these sources is relatively for long period. Receiving the credit lines form ADB and KfW is in recognition of the Bank’s highly satisfactory performance in terms of operational capability and financial health.

Foreing exchange operation

Foreign exchange means and covers all business activities relating to export, import, inward and outward remittance and buying and selling of currency. One of the largest businesses carried out by the commercial bank is foreign trading. The trade among various countries falls for close link between the parties dealing in trade. The situation calls for expertise in the field of foreign operations. The bank, which provides such operation, is referred to as rending international banking operation. Mainly transactions with overseas countries are respects of import; export and foreign remittance come under the preview of foreign exchange transactions. International trade demands a flow of goods from seller to beyond of payment from buyer to seller. In this case the bank plays a vital role to bridge between the buyer and seller.

Foreign Trade Department

Mainly foreign trade deals with import and export business that is two parties in foreign trade department in Basic Bank Ltd. (BBL)

- Import department

- Export department

Import department deals with the import oriented foreign trade while export department deals with export oriented foreign trade.

Foreign Correspondents

Foreign correspondent relationship facilitates foreign trade operation of the bank, mainly in respect of export, import and foreign remittance. The number of foreign correspondents and agents of the bank in the year 2007 stood at 322, which covers important business and trade centers of the world. The bank maintains excellent relationship with the leading international banks, for handling all foreign

Correspondent and maintaining all foreign business there is an International Division, which is called ID.

Import / Export

Import and export means flow of goods/services purchased by a party of one location from a party of another location. Normally import/export is done through letter of credit (L/C).

Wide-ranging changes and expansion in the world trade owing to the process of evolution in globalization and free market economy have facilitated free flow of goods, which resulted in worldwide trade competition.

Import Procedures

For engaging in international trade every trader must maintain the following steps:

1. Understanding

Import trade in Bangladesh is controlled under the import and export control Act 1950. Authorized Dealer Banks will import the goods into Bangladesh following the import policy, public notice, F, E, circular and other instructions from competent authorities from time to time.

2. Registration of importer

In terms of the importers, exporters and indenters (Registration) order 1981, no person can import goods into Bangladesh unless he is registered with the chief controller of import and export or exempted from the provisions of the said order. So the following documents are required to be submitted to the licensing authority for registration as importers.

- Questionnaire from duly filled in and signed.

- Income tax registration certificate.

- Trade License from the municipal or local authority.

- Bank certificate.

- Nationality certificate.

- Partnership Deed where applicable.

- Certificate of registration with the Registrar of joint stock companies and Memorandum and Articles of Association in case of private and public Ltd. Company.

- Certificate from the chamber of Commerce/Registered Trade Association.

- Ownership documents or rent receipts of the place of business.

- Any other documents required under the relevant import policy

After submission of the above documents and payment of requisite fees, if the documents are found in order and the C, C, E & I are satisfied, the import Registration Certificate (IRC) is issued to the applicant- importer.

Purchased contract between importers and exporters:

Now the importer has to contact with the seller outside the country to obtain the pro-forma invoice/indent, which describes goods.

Indent is got through indentures a local agent of the sellers.

After the importer accept the preformed invoices, he makes a purchase contract with the exporter declaring the terms and conditions of the import.

Import procedure differs with different means of payment. In most cases import payment is made by the documentary letter of credit (L/C) in our country.

Then the importer collects a letter of credit Authorization (LCA) from BBL principal branch.

Banks gives export guarantee that it will pay for the goods on behalf of the buyer. This guarantee is called letter of credit. The buyer and seller conclude a sales contract providing for payment by a documentary credit.

Restricted items of imported goods

1. Maps, charts and geographical globes, which indicate the territory of Bangladesh but do not do so in accordance with the maps published by the

Department of survey, Government of the People’s Republic of Bangladesh. Horror comics, obscene and subversive literature including such pamphlets, posers, newspapers, periodicals, photographs, films, gramophone records and audio and videocassette tapes etc.

2. Books, newspaper, periodicals, documents and other papers, posters, photographs, films, gramophone records, audio and video cassette tapes etc. containing matters likely to outrage the religious feelings and beliefs of any class of the citizens of Bangladesh.

3. Unless otherwise specified in this order, old, second-hand and recondition goods, factory rejects and goods of job-lot/stock-lot of secondary/sub-standard quality.

4. Reconditioned office equipment, photocopier, typewriter, telex, phone, computer, and fax.

5. Unless or otherwise specified in this order, all kinds of waste.

6. Goods (including their contains) hearing any words or inscriptions of a religious connotation the use or disposal of which may injure the religious feelings and beliefs of any class of the citizens of Bangladesh; and

7. Goods (including their containers) bearing any obscene picture, writing inscription or visible representation.

Source of finance

Import may be allowed under the following sources of finance:

(a) Cash

- Cash foreign exchange (balance of the foreign exchange reserve of Bangladesh Bank);

- Foreign currency accounts maintained by Bangladeshi Nationals working/living abroad.

(b) External economic aid.

(c) Commodity exchange.

4.4 Terms related to Import / Export

The following terms are related to the import/export business

(A) Letter of credit (L/C)

A-1 Definition of letter of credit

A-2 Consideration of letter of credit

A-3 Types of letter of credit

A-4 Parties of letter of credit

(B) Commercial Invoice

(C) Bill of lading

(D) Certificate of origin

(E) Inspection certificate

(F) Certificate of manufacture

(G) Insurance certificate

(H) Pro-forma invoice

(I) Bills of exchange

(J) Packing list

(K) Shipment advice

(L) Bill of entry

(A) Letter of Credit (L/C)

A-1. Definition of letter of credit (L/C):

It goes without saying that you, the exporter, what to be paid as quickly as possible, whereas your overseas customer may well want to defer payment for as long as possible. The answer of course is credit.

A letter of credit is a financing instrument opened by a foreign buyer with a bank in her/his locality. The letter of credit stipulates the purchase price agreed upon by the buyer and seller, the quantity of merchandise to be shipped and the type of insurance coverage to protect the merchandise during shipment. The letter of credit names the seller as beneficiary (that is, you are the party who gets paid)

and identifies the definite time period, the terms remain in force. The letter of credit authorized the buyers to pay when all the stipulated conditions have been met. A letter of credit gives some assurance to the seller that the buyer is solvent. Most letter of credit (L/C) is irrevocable and often confirmed when requested by the seller’s bank before the seller accepts them. This confirmation obligates the confirming bank to pay you once have meet all the stated condition in the particular letter of credit (L/C).

A-2. Consideration of letter of credits (L/C)

There are two simple considerations when using letter of credit (L/C):

(I) specify as fully as possible to your buyer the amount of credit (payment) needed, the length of time for which this letter of credit (L/C) should be valid, whether partial shipments are acceptable and all necessary documents.

(II) When the letter of credit (L/C) is delivered to you through the advising bank, check to see that you can meet all provisions specified. If not, request an amendment by the foreign buyer before proceeding.

Letter are most often used when initiating business with a new account, when a check of the importer’s credit reveals it would be unwise to make shipment on a less secure basis or when large purchases are requested by an unknown buyer.

A-3. Types of Letter of Credit (L/C)

Letter of credit may be-

- Revolving letter of credit (L/C).

- Assigned (L/C).

- Banker’s acceptances

Revolving letter of credit (L/C)

This is useful when shipping a variety of goods to an established customer. It normally runs far a period less than one year and it provides for prompt reinstatement when drawn against.

Assigned letter of credit (L/C)

This type is the same as the normal letter of credit (L/C) except that is includes the phrase and/or assignees following the names of the beneficiary. This allows the exporter to make his or her domestic purchase by using the overseas buyer’s credit. That is you are agreeing that payment for the letter of credit (L/C) may be made to your supplier. This is a way for an exporter to conduct business with limited capital.

Banker’s acceptances

As your business grows you will want to extend credit to your importer. One of the most efficient methods of doing this is through a banker’s acceptance, after agreeing to the terms (e.g. 90 days at sight) the importer opens a draft (check) under a L/C in favor of the exporter (beneficiary). The exporter presents the draft and the requested shipping documents to the paying bank. The bank review the documentation for correctness, the “accept” the draft to become payable (mature) in 90 days, or if the exporter requires “accepts” the draft and discounts the amount because of the need for immediate funds.

Revocable credit

A revocable credit is a credit, which can be amended or cancelled by the issuing bank at any time without prior notice to the seller.

2. Irrevocable credit:

An irrevocable credit constitutes a definite undertaking of the issuing bank (Since it can not be amended or cancelled without the agreement of all parties thereto), provided that the stipulated documents are resented and the terms and conditions are satisfied by the seller. This sort of credit always referred to revocable letter of credit.

A-4 Parties of letter of credit

Various parties are related to the letter of credit, such as-

- The issuing bank.

- The confirming bank, if any

- The beneficiary other parties, which facilitate the documentary credit, are

- The applicant.

- The advising bank.

- The negotiating bank/applicant bank

- The transferring bank, if any

Importer- seller who applies for opening a L/C

Confirming Bank: It is the bank, which adds its confirmation to the credit and it is done at the request of issuing bank. Confirming bank may or may not be advising bank.

Issuing Bank: It is the bank which opens/issues a L/C on behalf of the importer.

Advising/Notifying Bank: It is the bank through which the L/C is advised to the exporters. This band is actually situated in exporter’s country. It may also assume the role of confirming and/or negotiating bank depending upon the condition of the credit.

Negotiating Bank: It is the bank, which negotiates the bill and pays the amount of the beneficiary. The advising bank and the negotiating bank may or may not be the same. Sometimes it can also be confirming bank.

Paying/Accepting Bank: It is the bank on which the bill will be drawn (as per condition of the credit). Usually it is the issuing bank.

Reimbursing Bank: It is the bank, which would reimburse the negotiating bank after getting payment-instructions from issuing bank.

B. Commercial Invoice

As in a domestic shipment, good business practice dictates that a commercial invoice includes:

1. Full address of the shipper, seller and consignee, if different;

2. The respective reference number

3. Date of the order

4. Shipping date

5. Mode of shipment

6. Delivery and payment terms

7. A complete description of the merchandise and prices

8. Discounts and quantities.

In addition, if payment is to be against a letter of credit (L/C) reference to the bank and the corresponding credit or advice numbers must be given.

In some instances, it is necessary for the seller to sign his or her invoices and even have them notarized or countersigned by the local chamber of commerce or both.

C. Bills Lading

These may be overland (truck or rail) air, or ocean bills of lading, depending on destination or terms of sales. As in domestic shipment, there are two basic types of bills of lading:

- Straight (or nonnegotiable)

- Shipper’s order (negotiable)

The shipper’s order (negotiable) is used for sight draft or letter of credit shipments. This shipment must endorse the original copy of the “order” bill of lading before it is presented to the bank for collection. The endorsement may either be “in bank” or “to the order of” a third party, such as the negotiating bank. The letter of credit will stipulate which endorsement to use with the exception of ocean shipments; the carrier issues only one original bill of lading. Any number of original ocean bills of lading may be issued depending on the requirements of the buyer. Normally, all original copies are endorsed and submitted to the bank.

D. Certificate of Origin:

Even though a commercial invoice may contain a statement of origin of the merchandise a few countries require a separate certificate sometimes countersigned by a chamber of commerce and possibly even visage by the country’s resident consul at the port of export. These may be on a special from of the foreign government, or in other cases, a certificate on the shippers own letterhead will suffice. Statements of origin are required to establish possible preferential rates of import duties under a most favored nation arrangement.

E. Inspection Certificate:

In order to protect themselves, many foreign firms request a certificate of inspection. This may be either an affidavit by the shipper or by an independent inspection from, as dictated by the buyer, certifying to the quality, quantity and conformity of goods in relation to the other. This is usually done before the goods are shipped.

F. Certificate of Manufacture:

This document is used when a buyer intends to pay for the goods prior to shipment but the lead time for the manufacture of the products is lengthy and the buyer dose not desire to allocate the money so far in advance. If the seller feels that the buyer is a good credit risk, the seller will produced with the manufacture of the products with perhaps only a down payment. After the merchandise is ready, the seller prepare a certificate stating that the ordered goods have been produced in accordance with the contract and have been set a side for the account of the buyer. Commercial invoice and packing list are sent as supporting documents.

G. Insurance Certificates:

Where the seller provides ocean marine insurance it is necessary to furnish insurance certificates, usually in duplicate indicating the type and amount of coverage involved. Here again these are negotiable documents and must be endorsed before submitting them to the bank.

H. Proforma Invoice:

When a commercial invoice is required but it is not available at the time of foreign shipment arrives at importer’s customs, the importer (not the foreign exporter) may prepare a pro-forma invoice. This invoice contains Marketing ly the same information required on the proper commercial invoice, which is prepared by the exporter.

I. Bill of exchange

An unconditional order in writing, addressed by one person (the drawer) to another (the drawee) and signed by the person giving it, requiring the drawee to pay on demand or at a fixed or determinable future time a specified sum of money to or to the order of a specified person (the payee) or to the bearer. If the bill is payable at a future time the drawee signifies acceptance, which makes the drawee the party primarily liable upon the bill; the drawer and endorsers may also be liable upon a bill. The use of bills of exchange enables one person to transfer

to another an enforceable right to a sum of money. A Bill of Exchange is not only transferable but also negotiable, since if a person without an enforceable right to the money transfers a bill to a holder in due course, the latter obtains a good title to it.

J. Packing list

Packing list is the letter describing the number of packets, packet’s weight and their size. If there are several copies, then two copies should be given to the client and the remaining should be kept in the bank but if there is only one copy, then the photocopy should be kept in the bank and the original copy should be given to the client.

K. Shipment Advice

The copy mentioning the name of the insurance company should be given to the client and the remaining copies should be kept in the bank but if only one copy is given then the photocopy should be kept in the bank and the original copy should be given to the bank.

L. Bill of entry