Performance Evaluation of First Security Bank Limited from Different point of View

Trend of Assets Growth

Growth rate of Liquid Assets & Fixed Assets

Comparison of Operational Profit & Liquid

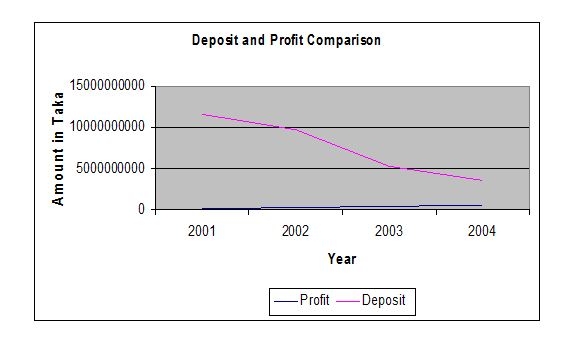

Deposit & Profit Comparison

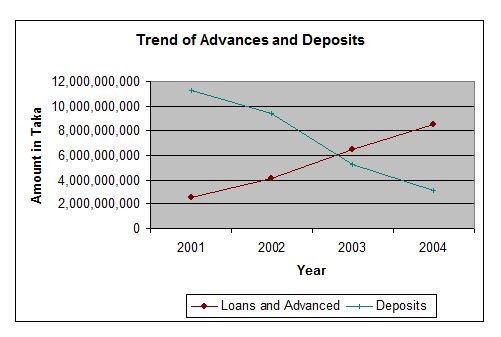

Trend of Advance & Deposit

4Total Assets

Asset Portfolio

Deposits and other Account

Loans and Advances

Foreign Exchange and Foreign Trade

Import

Export

Inward Remittance

Total Income

Net Interest Income

Operating Profit

Retained Earnings

Earnings per share

Capital funds

Reserve Funds

Investments

Branch Network and Expansion

Human Resources

From owners viewpoint

- Profitability of the Bank:

- Operating Profit margin

- Net Profit margin

- Growth of the Bank:

- Return on assets (RAO)

- Return on Equity (ROE)

- Provision for loan ratio

- Interest Income Ratio

- Non-interest Income Ratio

- Equity Multiplier

Asset utilization:

- Risk of the Bank:

- Interest expense ratio

- Non-interest expense ratio

Tax ratio

From the view point of Depositors

1. Internal Liquidity

- Current ratio

- Quick Ratio

2. Operating Performance

- Capital to deposit ratio

- Deposit to employee ratio

Loan to deposit ratio

CAMEL Rating

- Capital adequacy

- Asset quality

- Earnings

- Management efficiency

- Liquidity

Composite Rating

Chart 1

Chart 1 shows a significant improvement of the FSBL in treasury management. In successive years it has a remarkable improvement to increase its current assets while keeping investment in fixed. Even in year 2004 the fixed assets remain approximately close to previous year while there is double-digit growth in liquid asset this helped FSBL to gain from money market fluctuation in interest rate. Though in year 2003 fixed assets has increased more than 100%. But this is due to the set up cost and expansion in business. But following year it was able to maintain the fixed assets close to previous year.

Chart 2 shows rate of growth of the liquid assets and fixed assets. In this chart we see that in year 2002 fixed assets increased more than 150% due to the expansion of business, major investment in this year was in primary cost of opening of new branches including proclamation of land and installment of computer and furniture. But in the following its investment in fixed assets increase more not over 4%. Though keeping fixed assets may help FSBL to get a good score in CAMEL rating but being a third generation newly established not more than 5 years it should invest more in land proclamation and expansion of business to be remain competitive. But an sustainable growth may be ensured keeping fixed cost same level while increasing liquid assets at the same time this can ensure profitability because of short term investment in money market to take the advantage in the fluctuation of interest rate.

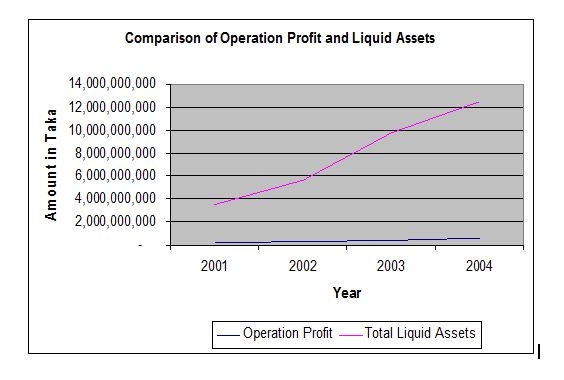

Chart 3 shows FSBL performance in Treasury Management. FSBL’s liquid assets ensured only liquidity. Where its volume of liquid assets increased sharply but it failed to ensure to profitability. It has invested more money in non interest bearing asset (cash and currencies) over the year profit has increased slightly but investment in liquid assets or non interest bearing assets increased straight upward. It is expected that over the year with more experience and strength and being acknowledge about the client transaction behavior it will shift more of it investment from non interest bearing assets to interest bearing assets like T-bills.

Chart 4 shows that in successive years deposit have fallen sharply. It is because in these successive years Government had taken loan from money market to meet its deficit budgets by increasing at the same time limit of investment in a single name had weaved so it fund flowed from depository financial sector to less risky Government Securities sectors. In this squeeze financial scenario it is very difficult to make any profit. But we see that in this period profit did not decrease even in year 2004 we that profit have increased slightly. Though in these periods core deposit has decreased sharply but FSBL was able to collect deposit from other financial institutions. That is a reason of FSBL to maintain high liquidity. Because it is more like that the deposit from other banks and financial institutions will be call back any time or have to repay on demand. Though this can help to keep cost of fund lower because it reduces dependent on high cost fixed deposit but at the same time it also hamper the growth rate. Over the year savings deposit even fixed deposit has decreased so it very much necessary for this moment to expand business, getting more strength by collecting money from offering saving deposit account or even fixed deposit account. Other wise growth will be stopped.

Chart 5 is showing the deposit and advance position of FSBL over the period. It depicts that though advance over the year has increase rapidly but deposit has decreased gradually. This is due to heavy dependency on borrowing from the other financial institutions. But heavy dependency on the deposit of other financial institute may not be seen a good sing. FSBL should improve it core deposit that is from small severs by offering various types of saving product other wise in case of deposit crunch a deposit run may create a heavy problem in future especially in case of contraction monitory policy.

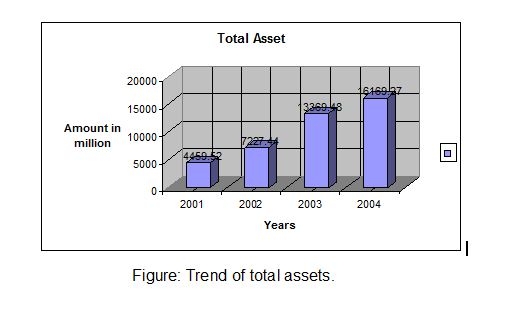

Total Assets: Trend of total asset is shown in the table from year 2001-2004.

Year | 2001 | 2002 | 2003 | 2004 |

Total Assets | Tk. 4459.52 million | Tk.7227.44 million | Tk. 13369.48 million | Tk.16169.27 million |

Asset Portfolio:

The bank total assets outstanding as of December 31, 2004 amounted to Tk. 16169.27 million as compared to 2003 amounted to Tk. 13369.49. Loans & advances contributed 52.57% cash 2.48% balances with others bank 14.47%, money at call and short notice 2.15%, investments 7.87% and the total other assets 20.46% as against 48.44%, 3.00%, 14.83%, 4.52%, 5.63% and 23.58% respectively in 2003.

Components | Amount in million | % Of Total |

| Loans and Advances | 8500.27 | 52.57 |

| Cash | 402.33 | 2.48 |

| Balance with other Banks | 2338.98 | 14.47 |

| Money at Call and short Notice | 347.50 | 2.15 |

| Investments | 1271.72 | 7.87 |

| Total Other Assets | 3308.47 | 20.46 |

| Total | 16169.27 | 100.00 |

Figure of Assets Portfolio

Deposits and other Accounts:

Deposits are the major sources of a Banks fund. They serve surplus units y offering a wide variety of deposit accounts. During the preliminary stages of operation the volume of deposit was comparatively low. But it started increasing as its operations gets going.

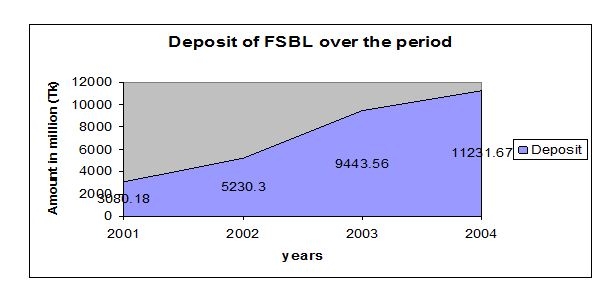

The total deposit of the Bank increased sharply from Tk. 5230.30 million at the end of 2002 to Tk. 9443.57 million at the end of 2003 and at the end of the year 2004 it increased to 11231.67 million. Deposits of the bank stood at tk. 11231.67 million at the end of December 2004 as compare to tk 9773.56 million at the end of December 2003. Deposits of the bank include Savings bank deposits, Term deposits, Current and other account deposits and bills payable.

Year | 2001 | 2002 | 2003 | 2004 |

| Deposit (million tk) | 3080.18 | 5230.30 | 9773.56 | 11231.67 |

Break-up of Deposits:

(Tk. in Million)

Type | 2001 | 2002 | 2003 | 2004 |

Savings Bank Deposits | 92.37 | 180.45 | 218.78 | 311.43 |

| Term Deposits | 2176.67 | 3688.00 | 6939.10 | 7806.26 |

| Current & Other account deposit | 602.71 | 1006.21 | 2066.68 | 2767.50 |

| Bills Payable | 97.15 | 152.97 | 208.07 | 340.32 |

| Bearer certificates of deposit | 111.28 | 203.58 | 10.93 | 6.15 |

| Total | 2968.9 | 5027.63 | 9432.63 | 11225.5 |

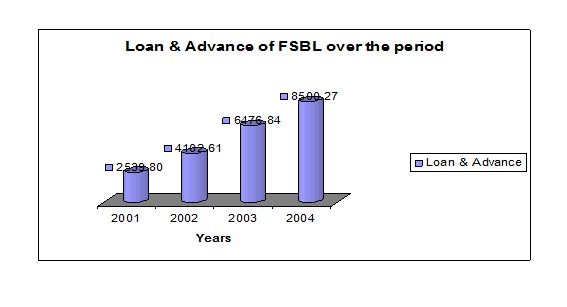

Loans and Advances:

First Security Bank Limited has been extending credit facilities to productive and priority sectors under the guidelines of Bangladesh Bank. Outstanding advances of the bank moved up from tk. 6476.84 million on the 31st December 2003 to tk. 8500.27 million on the 31st December 2004. That means the loans and advances of First Security Bank Limited has increased over time. In extending credit facilities, the bank attached due importance to sectoral needs and requirements of both public and private sectors.

Year | 2001 | 2002 | 2003 | 2004 |

| Loans &Advances (million tk) | 2539.80 | 4102.61 | 6476.84 | 8500.27 |

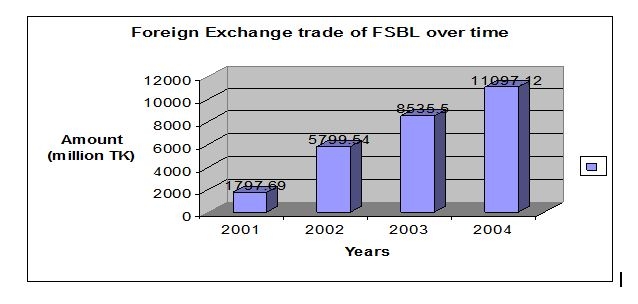

Foreign Exchange:

The bank has earned excellent business reputation in handling & funding international trade, particularly in boosting-up of export & import of the country. The foreign exchange and foreign trade business during the year 2004 stood at tk. 11079.12.

The comparative position of foreign exchange & trade business during the year 2001-2004 as follows –

| Year | 2001 | 2002 | 2003 | 2004 |

| Foreign Exchange (Tk. in Million) | 1797.69 | 5799.54 | 8535.50 | 11079.12 |

Import: The bank foreign exchange business relating to import into Bangladesh expanded markedly by 31.32% to Tk. 7413.90 million at the end of December 2004 from Tk. 5645.60 million a year ago. A year wise graphical presentation of the same is provided below.

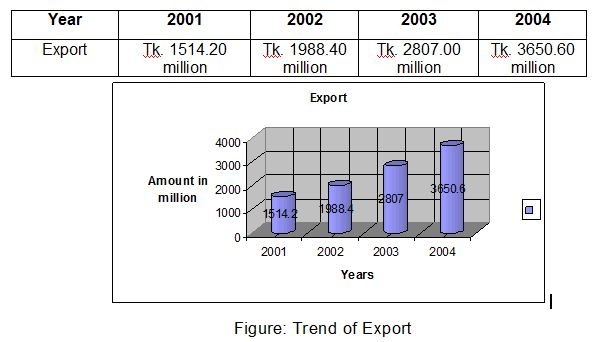

Export: Export business handled by the bank during 2004 stood at tk. 3650.60 million, showing a growth of 30.05% from Tk. 2807.00 million during 2003. A year wise graphical presentation of the same is provided below.

Branch Network and Expansion:

During the year 2002 the total number of branches of First Security Bank Limited stood at 10, in 2003 it was 11 and in year 2004 it stood at 12 branches. The Bank has proposed a long-term program to Bangladesh Bank to open more branches in phases in important locations in Bangladesh.

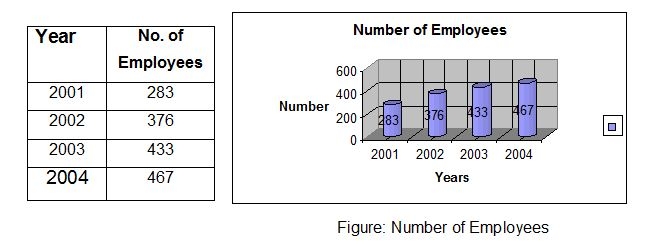

Human Resources:

Total number of employees stood at 467 as on 31st December 2004. The bank continued to encourage its employees to receive training and participate in various seminars and workshop to enrich their professional skills.

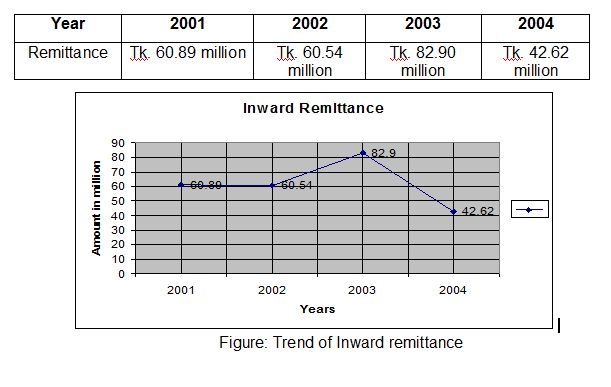

Inward Remittance:

During 2004 the bank handled inward remittance from Bangladeshi workers abroad to the tune of Tk. 32.62 million against 82.90 million of 2003. A year wise graphical presentation of the same is provided below.

Results of Operation:

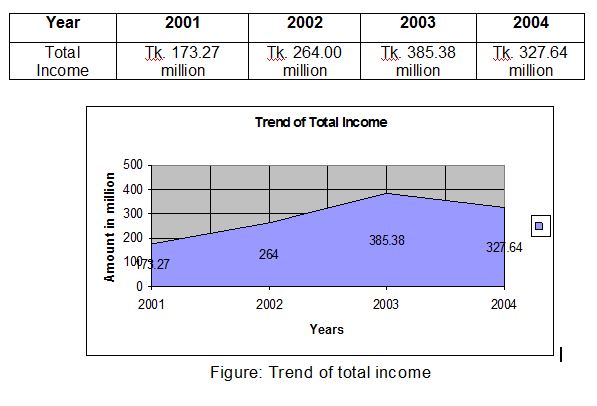

Total Income: During the year total operating income of the bank stood at Tk. 327.64 million compare to previous year total income of Tk. 385.38 million. A year wise graphical presentation of the same is provided on next page:

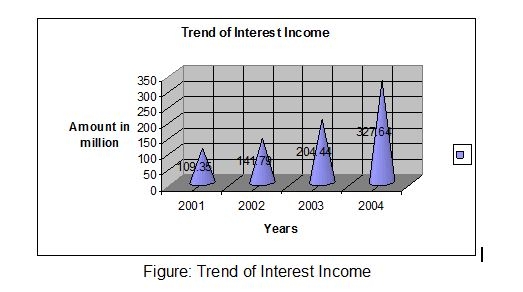

Net Interest Income:

The interest income of the year 2001 was 109.35 million; in year 2002 amounted to Tk. 141.79 million. In year 2003 it was Tk. 204.44 million. In year 2004 the interest income stood for Tk. 327.64 million showing a gradual increase.

Year | 2001 | 2002 | 2003 | 2004 |

Net Interest Income | Tk. 109.35 million | Tk. 141.79 million | Tk. 204.44 million | Tk. 327.64 million |

Operating Income:

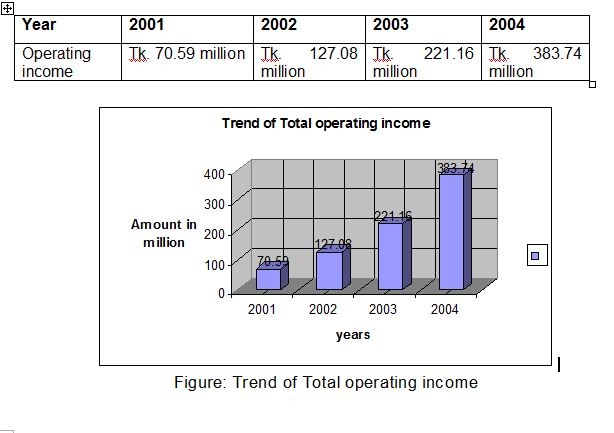

The profit of the year 2002 before provision amounted to Tk. 127.08 million as against Tk. 70.59 million of preceding year showing and increased by 80.03%. But in year 2003 before provision amount is 221.16 million. In year 2004 operating profit stood for Tk. 383.74 million.