GENERAL BANKING:Analysis & Description

3.1.1. GENERAL BANKING

General banking department usually performs a lot of important banking activities. General banking department is the department which is mostly exposed to the maximum number of bank customers. It is the introductory department of the bank to its customers. All business concerns earn a profit through selling either product or a service.

A bank does not produce any tangible product to sell but does offer a variety of financial services to its customers. The Eastern Plazabranch of UBL has all the required sections of general banking and this section are run by manpower with high quality banking knowledge. Hence a touch of rich customer service is prevailing in the branch.

In UBL the following departments are under general banking section.

- Account opening department.

- Local remittance department.

- Cash department.

- Clearing department.

- Collection department.

3.1.2. Account opening department.

The relationship between a banker in Uttara bank Ltd. and his customer begins with the opening of an account by the former in the name of the latter. Initially all the accounts are opened with a deposit of money by the customer and hence these accounts are called deposit accounts.

Bankers solicit deposit from the members of the public belonging to the different walks of life, engaged in numerous economic activities and having different financial status. There is one officer performing various functions in this department.

The following are the main functions performed by the department.

- Acceptance of deposit.

- Opening of account.

- Check book issue.

- Transfer of an account.

- Closing of account.

3.1.3. Acceptance of deposit:

Deposit is life-blood of an Uttara Bank Ltd. Without deposits there are no businesses for the commercial banks of any nature (NCBs, PCBs, and FCBs).in Uttara Bank Ltd. Eastern Plazabranch the various types of accounts are offered to various customers, which are grouped into:

- Demand deposit account.

- Time deposit account.

- Fixed deposit account.

3.1.4. Demand deposit account:-

The amount in accounts are payable on demand so it is called demand deposit account. The following accounts are under demand deposit accounts:

- Current account.

- Savings account.

- Short notice term deposit. (STD).

3.1.5. Current account:-

This type of account is opened by both individuals and business concerns. Frequent transaction (deposits as well as withdrawal) are allowed in this type of account. A current account a/c holder can drew checks on his account for any amount for any numbers of times in a day as the balance in his accounts permits. This account provides no interest. The minimum balance to be maintained is taka 2000.no new account can be opened with a check.

3.1.6. Savings account:-

Individuals for savings purposes open this type of account. Current interest rate of these accounts is 5.50% per annum. a minimum balance of tk.1000 is required to be maintained in a SB account interest on SB account is calculated and accrued monthly and credited to the account half yearly. Interest calculation is made for each month on the basis of the lowest balance at credit of an account in that month. A depositor can withdraw from his SB account not more than twice a week up to an amount not exceeding 25% of the balance in the account.

3.1.7. Special notice term deposit:-

The deposits in this account are withdrawal on prior notice varying from 7 to 29 days and 30 days or more. The interest is paid on the balance of the accounts. Current interest rate is 6.50% per annum.

3.1.8. Time deposit accounts:-

The amount in this a/c is payable only after stipulated time. The following a/c’s are under time deposit accounts.

- Fixed deposit.

- Bearer certificate of deposits.

3.1.9. Fixed deposit account:-

These are deposit, which are made with the Uttara bank ltd. for fixed period specified in advance. Uttara bank ltd. need not maintain each reserve against these deposits and therefore, Uttara Bank Ltd. gives high rate of interest on such deposit. A FDR is issued to the depositor acknowledging receipt of the sum of money mentioned therein. It also contains the rate of interest and the date on which the deposit will fall due for payment.

Interest Rates on Deposits

| Particulars | Rate of interest |

| Interest rate on deposit:1) Savings deposits.2) Special notice deposit. | 5.50%6.50% |

| Fixed deposit(Time deposit):1) 3 months.2) 6 months. 3) 1 year. 4) 2 year and above. 5) 3 years. | 7.00%7.50% 8.00% 8.25% 8.25% |

3.1.10. NATURE OF ACCOUNTS AND TYPES OF ACCOUNTS

Uttara Bank ltd. provides various types of account opening facilities for its clients. The nature of accounts and types of accounts are as follow:

NATURE OF ACCOUNTS

Individual.

Joint.

Proprietorship.

Partnership.

Club, society, trust, association.

School, college, university etc.

Limited company.

Government.

NGO.

Others.

TYPES OF ACCOUNTS

Current account.

Deposit account.

Saving account.

Short term deposit

3.1.11. DOCUMENTS NEED TO OPEN AN ACCOUNT

Uttara Bank Ltd. keep some documents from a client when comes to open an account. These documents are varying according to the character of account and client.

Uttara Bank Ltd. encloses the following documents for the purpose of current deposit account opening in case of individual or sole proprietor firm:

Photography of the signatories 2 copies.

Photography of the nominee 1 copy each (attested by account holder).

Photocopy of passport (first 5 pages).

Copy of trade license.

Certificate of TIN.

Declaration regarding source of fund.

Rubber stamp of the firm. (if it is a sole proprietor firm)

Uttara Bank Ltd. encloses the following documents for the purpose of current deposit account opening in case of Club:

Photography of the signatories 2 copies (each).

Photography of passport (first 5 pages) of signatories.

Copy of constitution/byelaws.

Copy of resolution.

Rubber stamp of the signatories.

List of members of the executive committee.

Uttara Bank Ltd. encloses the following documents for the purpose of current deposit account opening in case of partnership business:

Photography of the signatories 2 copies.

Photocopy of passport (first 5 pages).

Copy of the trade license.

Declaration regarding source of fund.

Rubber stamp of the firm

Partnership deed registered with “RJSC”.

Uttara Bank Ltd. encloses the following documents for the purpose of current deposit account opening in case of limited company:

Certified true copy of the memorandum and article of association o the company.

Certificate of incorporation of the company of inspection and return (along with a duly certified photocopy for bank’s records).

Certificate from the registrar of joint company that the company is entitled to commencement business (in case of public Ltd.co.).

Extract of the resolution of the board/general meeting of the company for opening the account and authorization for its operation duly certified by the Chairman/Managing Director of the company.

List of Director/Authorized officer along with designation and specimen signature who will operate the account.

Latest certified copy of Form-x (to be certified by registrar of joint stock companies).

Latest certified copy of Form-xii (to be certified by registrar of joint stock companies).

Photography of the signatories and all Directors.

Photocopy of passport (first 5 pages).

Copy of the trade license.

Director’s particulars.

Declaration regarding source of fund.

Certification of TIN.

3.1.12. Clearing department:-

According to the article 37(2) Bangladesh Bank order 1972 the bank, which are the member of clearinghouse, are called as schedule banks. The schedule bank (Uttara bank Ltd.)Clear the checks drown upon one another through clearing house. All the representatives of all the banks meeting at a specified time, for exchanging the instruments and arriving at the net position regarding receipt or payment. The place where the banks meet and settle their dues is called the clearinghouse. Functions of clearing department are as follows:

- Pass outward instruments to the clearing house.

- Pass inward instrument to respective department

3.1.13. Collection department:-

Checks, drafts etc. are drown on Uttara Bank Ltd. located outside clearing house are sent for collection. Principal branch collects its clients above mentioned instruments from other branches of UBL and branches other than UBL .in case of out ward bills for collection customers account is credited after finishing the collection processor. And in case of in ward bills customers account is debited for the purpose.

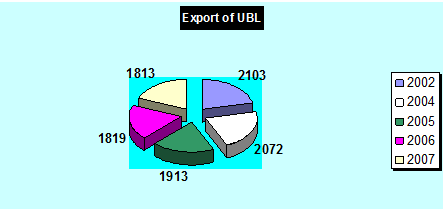

3.2.FIVE YEARS EXPORT CONDITION OF UBL

3.3. PERFORMANCE EVALUATION OF UTTARA BANK

3.3.1. CAPITAL ADEQUACY:

The Bank achieved the Tk 1.0 billion capital requirement ahead of the deadline set by Bangladesh Bank. The authorized and paid up capital of the Bank are Tk 1,200 million and Tk 744 million respectively. The total shareholders’ equity as of Dec 31, 2007 stood at Tk 1,188 million. The Bank maintained a capital adequacy ratio of 11.60% at the end of 2004 against the regulatory requirement of 9.0%.

| Capital Composition | 2007 | 2006 |

| Paid -Up Capital | 100 | 20 |

| Capital – Core | 19.97 | 9.98 |

| Capital – Supplementary | 188.58 | 176.52 |

| Total Capital | 308.55 | 206.5 |

3.3.2. INTERNATIONAL TRADE, REMITTANCES:

The import business of the Bank decreased to Tk 2263.07 crore in 2006 from Tk 2309.24 crore in 2003 and export bills decreased to Tk 1813.39 in 2006 from Tk 1819 in 2005. The Bank has remittance arrangement with “MONEYGRAM” of USA to facilitate foreign remittance inflows to the country. It also has agency arrangements with May Bank of Malaysia, Myanmar Investment Bank and Bhutan National Bank. As of end 2004 uttara bank Ltd. established correspondence relationship with 293 banks in 90 countries. The Bank is using SWIFT communication system for fast and accurate handling of foreign trade.

(Amount in Crore BDT)

| Foreign Exchange Business | |||||

| YEAR | 2003 | 2004 | 2005 | 2006 | 2007 |

| Imports | 2709.44 | 2620.49 | 2408.00 | 2309.24 | 2263.07 |

| Exports | 2103.65 | 2072.89 | 1913.31 | 1819.18 | 1813.39 |

3.3.3. LAST FIVE YEARS PERFORMANCE AT A GLANCE

| No | Particulars | 2004 | 2004 | 2005 | 2006 | 2007 |

| 01 | Authorized Capital | 20 | 20 | 20 | 20 | 100 |

| 02 | Paid-up Capital | 9.98 | 9.98 | 9.98 | 9.98 | 19.97 |

| 03 | Reserve Fund | 145.19 | 159.70 | 164.26 | 176.52 | 188.58 |

| 04 | Deposits | 2915.39 | 3147.76 | 3461.52 | 3689.19 | 3936.02 |

| 05 | Advances | 2293.83 | 1878.63 | 1860.10 | 2185.15 | 2516.39 |

| 06 | Investments | 673.94 | 988.39 | 1279.40 | 1006.21 | 956.45 |

| 07 | Gross Income | 391.83 | 382.14 | 382.09 | 426.50 | 443.51 |

| 08 | Gross Expenditure | 260.65 | 270.74 | 261.12 | 265.04 | 315.32 |

| 09 | Net Profit(pre-tax) | 50.20 | 62.47 | 68.31 | 78.26 | 86.68 |

| 10 | Import Business | 2709.44 | 2620.49 | 2408.00 | 2309.24 | 2263.07 |

| 11 | Export Business | 2103.65 | 2072.89 | 1913.31 | 1819.18 | 1813.39 |

| 12 | Foreign Correspondents | 193 | 256 | 295 | 322 | 329 |

| 13 | Number of Employees | 3200 | 3209 | 3382 | 3265 | 3505 |

| 14 | Number of Branches | 198 | 198 | 198 | 198 | 201 |

| 15 | Number of Shareholders | 5684 | 6120 | 5631 | 5351 | 5390 |

Credit Risk Measures By UTTARA BANK LTD.

4.0 Credit Risk

Management of risk is fundamental to the business of banking and is an essential element of corporate strategy. Banks face a number of risks in its operations and increasingly the success of the institution depends heavily upon its positive outlook rather than negative to affirm an efficient management of risk. UTTARA BANK LTD.

Liquidity risk is undoubtedly the most important concern for any financial organization as it is associated not with growth and profitability, but with survival. The liquidity ratio for a financial organization is measured by dividing the company’s investments in short-term securities by the total customers’ deposits.

Interest rate risk is major consideration for any financial organization because it relates to the company’s forecasts of interest rates. This ratio is easily calculated by dividing the interest-sensitive assets of the company by the interest-sensitive liabilities.

The capital risk of a bank indicates how much asset values may decline before the position of its depositors and other creditors are jeopardized. Thus a bank with a 10 percent capital-to-assets ratio could withstand greater declines in asset values than a bank with a 5 percent capital-to-assets ratio. From this perspective, UTTARA BANK LTD.

4.1 Principal of Credit Of The Bank

Basic principle governs the extension of Investment. These principles are strictly maintained to shape and define the acceptable risk profile of UTTARA BANK LTD. Bank and guides to respond business opportunities as they arise. Basic lending principles are;

- Know your customer

- Liquidity of the customer

- Safety

- Security

- Profitability from both bank’s and customer’s purpose of the loan’s perspective

4.2 Types Of Investment Offered By UTTARA BANK LTD. Bank

Basically UTTARA BANK LTD. Bank offers both funded and non-funded Investment facilities.

4.2.1 Non-funded facilities:

Non-funded facilities also known, as contingent facilities are those where banks fund is not required directly. A non-funded facility can turned to a funded facility as per situation creates. Bank receives commission rather than interest income by providing non-funded facilities. Following non-funded facilities are provided by UTTARA BANK LTD. Bank –

4.2.2.Letter of Investment (L/C):

A letter of Investment is an Investment line given by a bank to an importer to facilitate both foreign and inland transactions. This is a contingent liability which can be converted to a funded facility in case bank makes the payment on behalf of the importer. A letter of Investment can be revocable or irrevocable, restricted or negotiable so on.

4.2.3.Guarantee:

UTTARA BANK LTD. Bank offers guarantee for its reliable and valuable customer as per requirements. This is also an Investment facility in contingent liabilities from extended for participation in development work like supply of goods and services.

4.4.1. FINANCIAL POSITION OF UBL

ASSETS

The economic activities on the country as a whole wee positive and satisfactory during the year under report and the bank closed the year recording steady growth. At the end of the year 2006, total assets o the bank stood at 4521.70 crore as against taka 4206.22 crore registering an increase of 7.5 percent.

The assets for last five (2002 to 2007) year are as below (taka in crore):

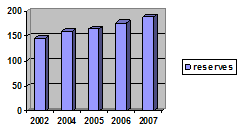

CAPITAL AND RESERVES

During the year under report authorized capital of the bank remained unchanged at TK 100crore and the paid-up capital stood at TK 19.97 crore. The reserve fund of the bank increased by 6.8 percent to TK 188.58 crore against TK 176.52 crore in the previous year. The reserves for the last five years (2002 to 2006) are as below (taka in crore):

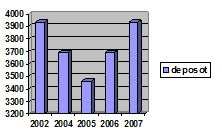

DEPOSIT

The deposit of the bank registered an increase of 6.69 percent in the year under review. At the close of 2006, Total deposit stood at TK 3936.02 crore as against TK 3689.19 in the previous year.. Deposits of last five years (2002to2006) are shown below:

CREDIT

The bank continued its participation in different credit programs for financing new industrial projects, working capital, trade finance, international etc. consequently net credit rose to TK 2185.15 crorefrom Tk 2516.39 of 2005.. Sector wise net advances during the year were as follows:-

- CONTINUOUS LOAN 11707.88

- DEMAND LOAN 3076.14

- TERM LOAN (UP O 5 YEARS) 3222.64

- TERM LOAN (OVER 5 YEAR) 1954.23

- STAFF LOAN 250.11

Loans and advance of last five years (2002 to 2006) are given below:

4.4.2. INCREASED FINANCIAL STRENGTH

The Bank had to operate in a declining interest rate environment, but was able to maintain a reasonable spread. It achieved an Operating Profit of Tk 128.19crore in 2006 compared to Tk 161.46 crore in the previous year. After necessary provision net profit stood at BDT 24.88 crore as of December 31, 2006.

(Amount in crore BDT)

| YEAR | 2003 | 2004 | 2005 | 2006 | 2007 |

| Operating Profit | 131.18 | 111.40 | 120.97 | 161.46 | 128.19 |

| Profit Before Tax | 50.20 | 62.47 | 68.31 | 78.26 | 86.68 |

| Profit After Tax | 24.95 | 19.71 | 10.06 | 14.26 | 24.88 |

4.4.3. INCREASING EARNING

The increased earnings were driven by enlarged loans and advances portfolio, increase in export and import business and efficient fund management. Non-interest income continued to contribute higher share in the total income of the Bank. Total income increased from BDT 426.50 crore in 2005 to BDT 443.51 in 2006. Interest income accounted for 69.12%, Income from Investments 10.86%, commission 18.12% and other income 1.90% of total income in 2004 as against 72.77%, 8.65%, 15.47% and 3.11% respectively in 2007.

(Amount in crore BDT)

| Particulars | 2007 | 2006 | ||

| Amt. | % | Amt. | % | |

Interest Income | 274,20,42,728 | 37% | 200,08,79,507 | Base |

| Income from Investment | 55,78,86,628 | 36% | 88,23,18,102 | Base |

| Commission, Exchange and Brokerage | 82,36,76,310 | 23.70% | 107,94,80,693 | Base |

| Other Operating Income | 31,15,27,018 | 3.3% | 30,23,35,955 | Base |

| Total | 267,82,97,789 | 100.00% | 278,72,52,813 | Base |

4.4.4. EARNINGS PER SHARE:-

Earnings pr share and return on equity also experienced a steady shock from 2002 to 2004 although it rises in 2005 from that of the previous year.

| YEAR | 2003 | 2004 | 2005 | 2006 | 2007 |

| Earnings per Share (Taka) | 249.89 | 197.41 | 100.80 | 142.83 | 124.59 |

4.5.Investment Classifications And Provisioning By UTTARA BANK LTD. Bank

4.5.1 Investment Classifications:

Investment classification is required to have a real picture of the investment and advances provided by the Bank. It helps to monitor and take appropriate decision regarding each investment account like other banks, all types of investments of BA fall into following four scales:

Unclassified: Repayment is regular

Substandard: Repayment is stopped or irregular but has reasonable prospect of improvement.

Doubtful debt: Unlikely to be repaid but special collection efforts may result in partial recover.

Bad/Loss: Very little chance of recovery.

| Investment Type | Unclassified(Month | Substandard (Month) | Doubtful (Month) | Bad (Month) |

| Continuous InvestmentDemand Investment | Expiry up to 5 month | 6 to 8 month | 9 to 11 month | 12 month+ |

| Term investment up to 5 year | 0 to 5 month | 6 to 11 month | 12 to 17 month | 18 month+ |

| Term Investment more then 5 years | 0 to 11 month | 12 to 17 month | 18 to 23 month | 24 month+ |

| Micro Investment | 0 to 11 month | 12 to 13 month | 36 to 59 month | 60 month+ |

4.5.2 Investment Provisioning:

A Certain amount of money is kept for the purpose of provisioning. This percentage is set following Bangladesh Bank rules.

Type of Classification | Rate of Provision |

| Unclassified | 1% |

| Substandard | 20% |

| Doubtful | 50% |

| Bad debt | 100% |

5.1 Definition Of Credit Risk Grading (CRG)

- The Credit Risk Grading (CRG) is a collective definition based on the pre-specified scale and reflects the underlying credit-risk for a given exposure.

- A Credit Risk Grading deploys a number/ alphabet/ symbol as a primary summary indicator of risks associated with a credit exposure.

- Credit Risk Grading is the basic module for developing a Credit Risk Management system.

5.2 Functions Of Credit Risk Grading

Well-managed credit risk grading systems promote bank safety and soundness by facilitating informed decision-making. Grading systems measure credit risk and differentiate individual credits and groups of credits by the risk they pose. This allows bank management and examiners to monitor changes and trends in risk levels. The process also allows bank management to manage risk to optimize returns.

5.3 Use Of Credit Risk Grading

- The Credit Risk Grading matrix allows application of uniform standards to credits to ensure a common standardized approach to assess the quality of individual obligor, credit portfolio of a unit, line of business, the branch or the Bank as a whole.

- As evident, the CRG outputs would be relevant for individual credit selection, wherein either a borrower or a particular exposure/facility is rated. The other decisions would be related to pricing (credit-spread) and specific features of the credit facility. These would largely constitute obligor level analysis.

- Risk grading would also be relevant for surveillance and monitoring, internal MIS and assessing the aggregate risk profile of a Bank. It is also relevant for portfolio level analysis.

5.4. Credit Risk Grading Review

Credit Risk Grading for each borrower should be assigned at the inception of lending and should be periodically updated. Frequencies of the review of the credit risk grading are mentioned below;

Number | Risk Grading | Short | Review frequency (at least) |

1 | Superior | SUP | Annually |

2 | Good | GD | Annually |

3 | Acceptable | ACCPT | Annually |

4 | Marginal/Watchlist | MG/WL | Half yearly |

5 | Special Mention | SM | Quarterly |

6 | Sub-standard | SS | Quarterly |

7 | Doubtful | DF | Quarterly |

8 | Bad & Loss | BL | Quarterly |

5.5. MIS On Credit Risk Grading

Bank should have comprehensive MIS reports on credit risk grading to evaluate entire credit portfolio of the Bank. Format of such MIS reports on credit risk grading has been presented in .

Credit Risk Grading Report (Consolidated)

Credit Risk Grading Report (Branch Wise)

Credit Risk Grading Report (Branch & Risk Grade Wise)

Credit Risk Grading Report (Grade Wise Borrower List)

6.1. FINDINGS OF THE STUDY

The primary purpose of this study report is to get an idea about the “Credit Risk Management in Uttara Bank Ltd”. After working in this bank we find the some important points.

The bank has a well-organized credit management process in place. The study found that the bank has a well-developed lending policy. The bank follows certain general principle of lending such as safety, purpose, liquidity and diversification. All the loan applications go through each of the steps of the loan granting process. The bank uses its own credit risk evaluation process in addition to LRA Manual of Bangladesh Bank and project appraisal method for evaluating loan proposals. The bank also has a proper loan administration to ensure proper documentation, monitoring and follow up of each loan granted by it.

In this paper bank’s deposit mobilization and loan disbursement, the average growth rate of deposit and loans & advances from 2002 to 2006 was 45.38% respectively. For loans and advances sanctioning it is observable that in 2004 and 2005 bad loss of giving loans is near about 60% which is not good for the bank. Besides their loans and advances in 2004 is greater than deposit amount. Overall their growth rate is good from the date of establishment

Uttara bank is expanding, it must focus on attracting, and getting and retaining qualified personnel for filling up its positions. It is worth spending more on attracting qualified human resources rather than getting the wrong people in the wrong positions.

RECOMMENDATIONS

From our performance evaluation I saw that the Uttara Bank losing its business in comparison and other bank because of its lack of use modern age banking technology and human resources. To improve the business condition of Uttara Bank Ltd. and to gain the lost market share I suggest implementing the following suggestion:

Management of the Bank is to work for creation of conceptual framework covering core elements of developed “Model Marketing Plan – (MMP)” of UBL to face the competition a changes in the banking industry into the new millennium for sustained growth of business / profitability of the bank. To accomplish the tasks of formulation of “MMP” focus should be made on the following issues:

Business philosophy that identifies current and future opportunities, defines magnitude and quantum, determines target markets and cluster, and decides on products, services and programs to secure entry to markets for economic and financial gains were made. The aim of planned marketing efforts is to understand customers and to ensure that offered products and services adapt to targeted customers’ needs perfectly. The marketing plan to be designed to perform tasks of stimulating demands for Bank’s products and services to influence the level timing and composition of demand help customers’ consummate their business objectives.

Ideas of satisfying the customers’ needs by means of products and the entire cluster of action as associated with creation / delivering and finally consuming the products and services.

Process to be employed to interpret markets, customers’ needs and transformation: defining mission / objectives and goals, portfolio plans and new business plans. The plans were structured in 3 (three) operational levels: corporate level, business level and product level. The marketing mission was converted into specific objectives for each level targeted at: profitability, market-share, positioning, risk-diversification and innovation. The objectives to be made

Quantifiable, realistic and consistent towards useful implementation of the marketing action plan. The portfolio plan involved in reviewing of the current portfolio of businesses and deciding on new businesses and potential thrust sectors.

Identification of market opportunities through analysis of subjective issues, concepts, strategies and techniques of penetration to create market along with efforts to integrate actions based on collected data to fit into real banking solution having operational linkages with the marketing plan “ “Model Marketing Plan – (MMP)” of UBL.

Natural inducement of the target groups to UBL is that customers must perceive greater degree of satisfaction from the offered services. The qualitative improvement and development of cutting-edge products precipitate in higher degree of customers satisfaction and UBL to plan for improvement of services, adding flair to the products like introduction of ATM / On-line banking / Credit Card / Debit Card / introduction of relationship Manager and Customer-friendly deposit schemes.

CONCLUSION

As an organization the Uttara Bank Limited has earned the reputation of top listed banks operating in Bangladesh. The organization is much more structured compared to any other listed bank operating in Bangladesh. It is relentless in pursuit of business innovation and improvement. It has a reputation as a leader in financing manufacturing sector.

With a bulk of qualified and experienced human resource, Uttara Bank Limited can exploit any opportunity in the banking sector. It is pioneer in introducing many new products and services in the banking sector of the country. Moreover, in the retail-banking sector, it is unmatched with any other listed banks because of its wide spread branch networking thought the country.

Some More Parts-