Introduction

Banking Industry is one of the most promising industries of our country. The importance of the sector revealed through its contribution in the economic growth of the country. This sector accelerates economic growth through mobilizing funds from surplus unit to the deficit unit. Banking Industry is moving towards rapid changes due to technological innovation and diversified needs of its customers.

Banks deal with the most important factor of the economy i.e. Money. It flow funds from surplus unit to deficit unit and through this it facilitated the efficient allocation of the resources as well as accelerated economic growth. This sector is moving towards new dimension as it is changing fast due to competition, deregulation, financial, reforms.

Due to the globalization competition in banking sector is increasing very fast. Banks are becoming more customers oriented and offer High tech customized products to it’s target market to hold the market .Our central bank always keep monitoring banks performances. Individual banks also need to assess their own performance to satisfy the parties those are related to its growth:

- For Shareholders.

- For depositor.

- For Bangladesh Bank.

- For its own Assessment to view the future growth and profit.

ORIGIN OF THE REPORT:

The report has been prepared as an academic requirement for the accomplishment of BBA degree through three month internship program by Shahana Akter Ripa BBA student majoring in finance from the faculty of Business Administrations. I have joined National Credit & Commerce Bank(NCC Bank Ltd) Limited for the completion of my internship program and requested our honorable course teacher Mohammed Ruhul Amin to supervise me during my internship program. He kindly accepted my request and asked me to prepare a report on “Overall Banking System Special Focus on Foreign Trade” after my internship period thereon. The bank scheduled my place of posting at the Foreign Exchange Branch for three month. During this internship I worked different department especially in Foreign exchange division to come to know about the different functions of the bank. And at long last after getting practical knowledge I managed to prepare my report on “Overall Banking System Special Focus on Foreign Trade in Foreign Exchange Branch” and submitted my honorable supervisor.

OBJECTIVE OF THE STUDY:

Broad Objective:

The prime objective of this report is to achieve practical knowledge about the activities of NCC Bank Limited, Foreign Exchange Branch.

Specific Objectives

- To gain practical experience on different function on different departments like general banking, cash department especially foreign trade from the perspective of the NCC Bank Ltd.

- To know the Foreign Exchange activities in NCC Bank

- To know the studies and conditions of Foreign Trade

- To know how a L/C is opened.

- To know the documentation of an L/C

- To know the whole procedure of a L/C

- To know the Import procedure of foreign Exchange Br.

- To know the Export procedure of Foreign Exchange Br.

- To analyze the Procedure of Foreign Exchanges of NCC Bank

- To analyze the foreign trade position of NCC Bank ltd.

- To know the disbursement and recovery procedures of Foreign Exchanges

- To know the procedure of opening a bank account

- To know how a PO (pay order) is being processed

- To know cash receiving & disbursement process of cash department.

- To know how a customer can get their financial statement or related information of their account.

METHODOLOGY:

To make the report more meaningful and presentable, two sources of data and information have been used widely these are Primary Data and Secondary Data. Both primary and secondary data sources were used to generate the report. But Most of the information collected from secondary sources:

Secondary Sources: The secondary sources of information is:

- Annual report of NCCBL.

- Materials and files of NCCBL, Foreign Exchange Branch.

- Website of NCCBL.

- Unpublished data received from the branch.

- General information of banking activities.

Primary sources: The primary source of information is as follows:

- Face-to-face conversation with the bank officers and staffs.

- Practical desk work

- Personal diary (that contains every day experience in bank while under going practical orientation).

LIMITATIONS OF THE STUDY:

There were several constrains while preparing this report are:

- Difficulty in accessing data of its internal operations.

- Non Availability of some preceding year’s statistical data.

- Non-disclosure of some basic information.

- Like any other research, this reports limited to time and resource and only three months are not enough to cover such wide area of banking.

- The information of NCC Bank Ltd was not found in a structured way.

BACKGROUND OF NCC BANK LIMITED:

National Credit and Commerce Bank Ltd. bears a unique history of its own. The organization started its journey in the financial sector of the country as an investment company back in 1985, under the name of National Credit Limited. National Credit Ltd. (NCL) performed well for near about 7 years. The core objective of the company was to play a catalyst role in the capital market of the country by way of participating in security trading, underwriting, etc. . The Bank commenced its Banking business with sixteen Branches from 17 may, 1993. The Bank is listed with Dhaka Stock Exchange Limited and Chittagong Stock Exchange limited as a public quoted company for its shares. Subsequently NCL converted into a full fledge commercial Bank on 17 .May 1993 after obtaining license from Bangladesh Bank under the name & style “National Credit and Commerce Bank Ltd.” The authorized capital of the bank was fixed at Tk. 75.00 crore and paid up capital at Tk.39.00 crore of which 19.50 crore was subscribed by the sponsors at that time.

The principal place of business is the registered office at 7-8 Motijheel commercial area, Dhaka 1000. It has 81 branches as over Bangladesh as 31 July 2009. It carries out all banking activities through its branches in Bangladesh.

CORPORATE INFORMATION:

- Address: 7-8 Motijheel C/A,Dhaka-1000.

- Incorporation of the bank: 23march 1992.

- Licensed Issued by the Bangladesh Bank: 12 May, 1993

- Formal launching of the Bank: 17 May 1993

- Listed with Dhaka Stock Exchange: 20 November, 1994

- Listed with Chittagong Stock Exchange: 03 November1994

- Registration Certificate as Stock Broker:12 November 2007

- Number of Employees: 1458

Vision of the Organization :

To become the Bank of choice in serving the Nation as a progressive and Socially Responsible financial institution by bringing credit & commerce together for profit and sustainable growth.

Mission of the Organization:

To mobilize financial resources from within and abroad to contribute to Agriculture’s, Industry & Socio-economic development of the country and to play a catalytic role in the formation of capital market.

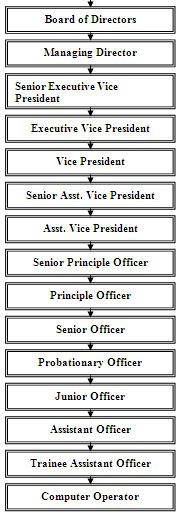

Organization Structure:

About Foreign Exchange Branch:

The history of Foreign Exchange branch is an integral part of the history of National Credit and Commerce Bank ltd. The Foreign Exchange branch started its operation on 12th June 2002. From the beginning of the branch it shows its potentiality to grow swiftly. Within very short time it established one of the commanding positions among all the branches in term of profit. Basic reasons of its sound growth are location, effective & efficient management team and most importantly providing the best service to their customers.

Branch Information:

- Branch Name: Foreign Exchange

- Date of establishment: 12 Jun 2002

- Address: 29/A Toyenbee Circular Road, Motijheel C/A Dhaka.

- Phone: 9556765

- Licensed Issued by Bangladesh Bank:

- Number of Employees: 38 (32 officers and 6 staff) till September 30,2010

- Number of foreign corresponding : 398

Workforce of the branch:

The branch has a total number of 38 employees including Branch manager & operations manager. All other employees work under several departments. The departments are

- General Banking

- Cash department

- Accounts Department

- Foreign Trade

- Credit department

Branch manager and operations manager looks after the activities of each division and take major decisions.

Internship position

For the accomplishment of my BBA program I have completed my three month internship program from the Foreign Exchange Branch of NCC Bank Ltd. I joined the on 1st September 2010 and successfully completed my internship program on 30th November 2010.

In the internship period, I tried to; learn various types of work related to banking sector. Ihave worked in three different departments in different times.

During my internship period I had not any specific organizational position. I worked there 5days in a week. My office hour was 10am to 6 pm. At the first day of internship Mr.Abdul Haque, Executive Vice President told me about my duties and responsibilities and then Mr. Maksumul Islam introduced me to whole staff.

Job Rotation

This report has been prepared on the basis of experience gathered during the period of my internship from 1st September to 30th November. Within this period I have visited all the section of foreign exchange department. I have worked in the following three Divisions for a certain period of time:

| Serial No. | Division | Period Of Time |

| 1 | General Banking Division | 30Days |

| 2 | Foreign Trade Division | 50 Days |

| 3 | Remittance Section | 10 Days |

| Total | 90 Days |

The officers of every department were very cooperative and I have really learned a lot from them. During my internship period I was assigned to do some work in every department and I was supposed to do following assigned job with sincerity and diligence.

Internship Duties

General Banking Division:

In general banking division I have performed following works:

Clearing section:

In clearing section the main responsibility was to receive several cheques from clients.I have endorse those cheques for clearing. I had to ensure account number, a/c holder name,which bank’s cheque ect is properly stated in the cheque or not. And than enter to the computer & complete other tasks.

Statement Providing:

I used to give statement to the customers. At first the customer should entry their name & a/c number in the register book, than I can give them their financial statement from the software.

Pay order writing and preparing to provide:

In my internship period I used to prepare pay order and provide it to the customer.

Current and saving Account opening

I worked in a/c opening section for several days and learn how to open current & saving a/c. I used to check the application forms to make sure that applicant has given all the information properly.

Cheque book requisition receiving:

To get a new cheque book the a/c holder should give a requisition for cheque book at least 5 days before they want to get it. I used to receive this requisition forms.

Cheque book providing:

I used to give customers the cheque as their required date. Before getting the cheque book an applicant have to sign in the cheque book receive register.

Cash receiving:

In the period of my internship period I worked in cash section for a few days, there I used to receive cash from the customers. I should check the voucher thoroughly before taking the cash and then endorse a cash receive seal in the voucher.

Foreign Trade Division:

Import section: As foreign activities import is one of the important functions of Ads. The major function is to import goods from abroad. In this section I observed the total process of import. Some major activities of import section are: checking IMP form, checking the documents of the LC etc.

To fill up the IMP form I had to fill the information of the goods, like

- L.C.A Form

- Registration no of L.CA Form

- Description & Quantity of goods

- Invoice Value in foreign currency

- Country of Origin

- Port of importation

- Port of shipment

- Name of vessel

- Indenters name & address

- Indenters reg. no with CCI&E

Export section: Beside the import a large volume of profit is generated from Export. In this section I stayed many times and observed different Export related activities like advising L/C, writing forwarding letter, fill up the EXP form etc.

While fill up the EXP form than I need the following information

- LDBP/ FDBP bill no.

- Bill date

- Export L/C no & date

- L/C value

- Proceed of the invoice

- Realization date of payment

- Port of shipment

- Name of vessel

- Date of lading

- ERC number

- Exporter’s name and address

Remittance Section

In the remittance section I worked for 10 days, the purpose of remittance section is to ease the flow of funds between our country and abroad. When an international transaction is made the payment of the transaction is made through foreign currencies. Some major activities of remittance are: Telegraphic Mail form checking, verify the information of customer with the product, provide the payment to the customer.

General banking department is the “Heart” of the all-banking activities. It performs the core functions of bank, operates the day to day transactions. It is the storage point for all kinds of transaction of foreign exchange department, loans and advances department &itself. General Banking department generally deals with the following sections:-

- Account Opening Section

- Cash Section

- Bills & Clearing Section

- Remittance Section

Account Opening Section:

The relationship between banker and customer begins with the opening of an account by the customer. Opening an account binds the banker and customer into contractual Deposit Account relationship. In fact, all kinds of fraud and forgery start by opening an account. So the bank should take extreme caution in section customers.

Different Types of Account:-

- Current Deposit Account

- Saving Deposit Account

- Short term Deposit Account

- Monthly Saving Deposit Account

Current Account:

A current deposit account may be operated in several times during a working day. There is no restriction on the number and the amount of withdraws from a current account and the banker does not allow any interest on the current account.

As the banker is under an obligation to repay these deposits on demand, they called demand liabilities of a bank. To meet such liability the banker keeps sufficient cash reserves against such deposit.

A person can open a current a/c or any entity. The entity can be a partnership firm, limited company, proprietorship firm, association, clubs etc.

Saving Account:

A saving a/c is meant for the person of the lower and middle classes who wishes to save a part of their income to meet their future needs and intend to earn an income from their saving. The entire feature are like CD a/c except some restrictions imposed by the bank. The bank offers a reasonable rate of interest. The number of withdrawals over period of times is limited. Only two withdrawals are permitted per week, more than that no interest will be paid on rest of the amount for that month. The total amount of one or more withdrawals on any date should not exceed 25% of the balance in the a/c unless 7 days advance notice is given.

Short Term Deposit:

Special notice a/c which is commonly known as short term deposit a/c will be kept in the short term deposit ledger. The customer should dully sign a/c opening form and specimen signature card.

Monthly Saving Scheme:

It is a new project of NCCBL, which is a scheme like DPS in our bank it is called SSS. This scheme started from 1998. The installment payment is to be made to the bank within the first 10 days of each month. It can be opened for 5years and 10 years maturity for Tk. 500 and 1000.

| Monthly Installment | 5 Years | 10 Years |

| 500.00 | 40,000 | 1,12,000 |

| 1000.00 | 80,000 | 2,24000 |

Cash Department:

Cash section of any branch plays a very vital role in general banking department, because it deals with the most liquid assets. NCCBL has a very equipped cash section. This section receives cash from depositors and pays cash against check, draft, pay order, pay in slip, over the counter.

Cash Receive Section:

Any person to deposit money will fill up the deposit slip and give the form along the money to the cash officer over the counter. The cash officer counts the cash and compares with figure written in the deposit slip. Then he puts his signature on the slip along with the ‘cash received’ seal and record in the cash receive register book against the number. At the end of this procedure, the cash officer passes the deposit slip to the computer section for posting purpose and delivers the duplicate slip to the client.

Cash Disbursement:

The drawer who wants to receive money against check comes to the cash payment counter and presents his check to the officer. The officer verifies the following information:

- Date of the check,

- Signature of the a/c holder,

- Material alteration

- Where the check is crossed or not,

- Where the check is endorsed or not,

- Where the amount in figure and in word correspondent or not,

Then s/he sends the check to the computer for posting. If the computer officer finds everything in order, then s/he passes the check to the cash officer to payment by putting ‘pay cash’ seal on the check. The cash officer gives the cash amount to the holder.

Bills and Clearing:

As a service oriented organization, a bank has to per form some extra services on behalf of his customer. The main function of this section is to collect instruments on behalf of his customers through Bangladesh Bank clearinghouse. Outward Bills for Collection (OBC), inter branch clearing (IBC). Upon the receipt of the instruments this section examines the followings:

- Whether the paying bank within DhakaCity

- Whether the paying bank outside DhakaCity

- Whether the paying bank of their own branch

Local Remittance:

A lot of cash handling from one place to another is risky. So bank remits funds on behalf of the customers to save them from any awkward happening through the network of their branches. There are three ways of remitting fund from one place to another. There are as follows:-

- Pay Order (PO)

- Demand Draft (DD)

- Telegraphic Transfer (TT)/ Mail Transfer (MT)

Bank Draft:

A bank draft is an order to pay money drawn by one office of the bank upon other office of the same bank for a sum of money payable to order on demand.

Characteristics:

- It is drawn by one office of a bank upon some another office of the same bank

- It is payable on demand

- Its payment is to be made to the person whose name is mentioned therein or according to his order.

- It cannot be made payable to the bearer.

Commission:

0.10% commission of the principle amount and Postage charge Tk.15 plus 15% Tax on the commission amount.

Foreign Exchange:

Foreign exchange means to deal with foreign currency, so we can say that foreign exchange means all kind of transaction related to foreign currency, as well as currency instrument such as DD, FDD, and PO etc. Foreign Exchange Department of a bank is an important one that deals with import, export, and foreign remittance. Bank branch should be ‘Authorized Dealer’ with the approval of Bangladesh Bank to run foreign exchange business. To run foreign trade every bank should have some foreign exchange account. The accounts are

Foreign Exchange Accounts:

Loro account:

Loro account means “their account with you “. Account maintained by third party is known as Loro Account. This account may be either in foreign currency or home currency.

Nostro Account:

Nostro Account means “Our account with you. The account that a home bank maintains with a foreign bank is known as Nostro account. For example, NCC Bank’s US Dollar account maintained with HSBC USA is NOSTRO Account of NCC Bank.

Vostro Account:

Vostro Account means “your account with us”. The account maintained by a foreign bank is known as vostro account. We can term nostro account when referred to its account holder (foreign bank) by home bank as vostro account. For example, Standerd Chartered Bank’s taka account maintained with NCC Bank is a vostro account of NCC Bank.

Foreign exchange Dept. of NCC bank:

NCC bank foreign exchange dept. plays a vital role to earn the bank’s maximum profit. The dept. is classified according to their activities. The foreign exchange dept. consists of three sections: –

¨ Import section,

¨ Export section,

¨ Foreign remittance section.

Classification of L/C:

There are various kinds of L/C’s exists in different consideration, but usually all those types of L/C’s are not in use in our country. Only few of them are being used from the followings

- Revocable L/C

- Irrevocable L/C

- Back-to-Back L/C

- Revolving L/C

- Red clause L/C

- Green clause L/C

- Documentary L/C

Nature of L/C:

There are several types of L/C according to the nature of payment. The foreign trade department of NCC Bank has been practicing the following types of L/C

- Deferred L/C

- Sight L/C (Cash L/C)

- Sight Local L/C

- Usance L/C

Opening of L /C:

If an importer wants to import some goods from out side of Bangladesh, at first he has to apply to a bank for opening an L/C. Letter of Credit is a written undertaking of a bank written to the seller /exporter issued at the request of the buyer / importer to at site or a determinable future date. According to import policy unless otherwise specified, all import is to be made by opening irrevocable letter of credit. L/C can be opened against Performa Invoice, if the exporter has no agent and L / C can be opened against Indent if the foreign supplier has indenting agent.

Transmitting the L/C:

The L/C is transmitted to the advising bank for advising then L/C to the beneficiary. L/C is generally transmitted through three methods. They are:-

1) Courier,

2) SWIFT,

3) Telex or Fax

Before transmission, a final examination of the L/C contents is necessary for then issuing bank. It is customary to the beneficiary through an advising bank. Advising through a bank is a proof of apparent authenticity of the credit to the seller. Banks have corresponding relation or arrangement through the world by which the L/C is advised to the beneficiary. While advising, the advising bank does not undertake any liability. Before advising, the advising bank verifies the signature or test of the officers of the issuing bank. Advising bank is generally the nearest bank of the beneficiary’s county or of that country.

Conformation:

Very often advising bank receive request from the issuing bank to add their conformation while advising credit to the beneficiary. The advising bank can do it if there is prior arrangement between advising and issuing bank or if it feels that the issuing bank is a reputed and reliable institution and good enough to discharge its obligation. By being involved as a confirming agent, the agent the advising bank undertakes to negotiate beneficiary’s bill without recourse to him.

Import section:

Import of into Bangladesh is regulated by the Ministry of Commerce in terms of the import & export act 1950, with import policy orders issued periodically and public notices issued from time to time by the office of the Chief Controller of Import & Export (CCI&E). In terns of importers, exporters and indenters order 1981; no person can import goods into Bangladesh unless he is registered with the CCI&E. On the next step the importers applies to Bangladesh Bank through authorized dealers for import goods. In order to import a product from abroad, the importer needs to submit an application letter requesting for opening Letter of Credit (L.C) with the bank.

Registration of Importer:

To obtain Import Registration Certificate (IRC), the applicant have to submit documents to the CCI & E through the nominated bank.

- Trade license

- Membership certificate from chamber of commerce

- Nationality certificate

- TIN number

- Dully filled & signed questionnaire

By getting those documents the CCI & E issues IRC obtaining treasury challan to the importer.

Amendment of L/C:

Amendment of L/C is based on agreement between buyers and sellers. Any amendment they want to bring in L/C should be informed to the issuing bank. Issuing bank will transmit the amendment to the advising bank with test. In case of revocable L/C amendment can be brought without prior notice of the beneficiary or issuing bank. But in case of irrevocable L/C, Which is very much popular, can not be amendment with out informing beneficiary or the issuing bank. Usually L/C amendment for the following requirements:

- Extension of validity of credit,

- Change of price / unit price,

- L/C value increase or decrease,

- Change of documentary requirement,

Lodgment of Import Bills:

The word “Lodgment” means temporary stay. If import documents found in order it is to be made entry in the bill register and necessary voucher to be passed, putting the bill number on the document, this process is called the lodgment of bill. The documents stay at this stage for a very short time such as up to retirement of the documents. Bank must be lodgment the document within 7 working days after receiving the documents.

Retirement of Import Bills:

On the date of Lodgment of document the importer is being advised to retire the document against payment, with full particulars of shipment. Every week till retirement of the bill, subsequent reminders are to be given. If the importer fails to retire the bill within 21 days of arrival of the consignment, such bills are considered as overdue bill.

Payment of L/C:

The issuing bank gives the payment to the negotiating/advising bank. Usually payment is made within 7 days after the documents have been received. If the payment is become deferred, the negotiating bank may claim interest for making delay. A telex is transmitted to the correspondent bank ensuring that payment is being made.

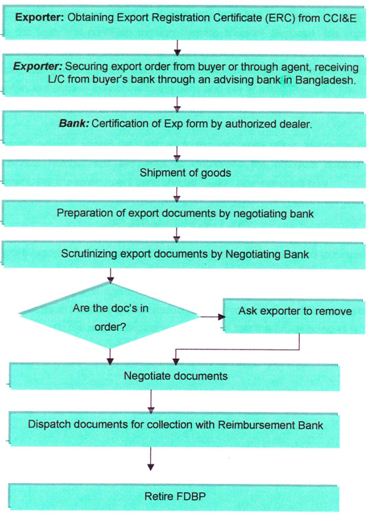

Export Section:

The export section of NCC bank of main branch is responsible for opening L/C negotiation of export documents, purchase of inland bill etc. As per Foreign Exchange Regulation Act, 1947, nobody can export by post and otherwise than by post any goods either directly or indirectly to any place outside Bangladesh, unless a declaration is furnished by the exporter to the collector of customer or to such other person as the Bangladesh Bank may specify in this behalf that foreign exchange representing the full export value of the goods has been or will be disposed by Bangladesh Bank.

Export Procedure:

Registration of Exporter:

No one can export any goods from Bangladesh unless he is duly registered as an exporter with the Chief Controller of Bangladesh authorized dears should therefore, ensure before certifying any export forms, as required, that the person is so registered. The registration number should be quoted on the relative export forms. Before the exporter with the customs authorities lodges the forms, they should get all the copies certify by an authorized dealer. After receipt of the EXP forms from the exporters for certification purposes, the authorized dealers will see and ensure that each set of the forms is duly filled in and signed by the authorized dealer.

The following documents are required to apply for registration of exports:

- Trade License

- Income clearance certificate,

- Nationality certificate,

- Bank solvency certificate,

- Asset certificate,

- Registration certificate,

- Memorandum of association,

- Rent receipt of business premises,

- Certificate of incorporation,

Advising of L / C:

The banker provides little import information for example: name of importer and exporter, description of goods, expiry date, and shipment date of L / C etc. The documents the bank receives in cable at first and letter in original. Bank records the details of the L / C and prepare advice after getting the original L / C. Advise is prepared for the beneficiary, issuing bank and for office.

Negotiation of Export Bills:

NCC bank, main branch checks all points in the export documents and if they are free of irregularity the bills are negotiated. Negotiation is nothing but making payment to the exporter and sending the paper to the importer bank for reimbursement. The conversion rate of foreign exchange of negotiating date is applied. The foreign bills negotiate a/c is debited and party’s a/c is credited. Transaction of foreign exchange are consolidated and sent to international division and accounts division of head office. The foreign bills negotiated a/c is credited by head office after the bills are realized.

Back to Back L / C:

It is nothing but a secondary letter of credit opened by the advising bank in favor of a domestic / foreign supplier on behalf of the beneficiary or original foreign L/ C as per original letter of credit of bank by importer letter; it is called Back to Back L / C. The secondary L / C is opened on the strength of the original / master L / C for a smaller amount i.e. Maximum 75% is kept under lien and 10% under packing credit. As per existing provision recognized export oriented units of the country are permitted to make import of their raw and packing material requirements under the back to back L / C arrangement where the importer payments are made out of the realized proceeds of export of the manufacture’s products. Number of Back to Back L / C party now in the NCC bank is increasing.

Back to Back Foreign L/C:

When the back to back L/C is opened in a foreign country supplier it is called back to back foreign. It is generally payable with in 120 days at sight.

Back to Back Local L / C:

When the back to back L/ C is opened local purchaser of materials, it is called back to back local L/ C. It is generally payable within 90 days at sight.

Payment under Back to Back L/C:

Deferred payment is made in case of back to back L/C as 60days, 90days, 120days, and 180days of maturity period. Payment will be given after realizing export proceeds from the L/C issuing bank abroad.

Foreign Remittance:

Foreign remittance means purchase and sale of freely convertible foreign currencies as admissible under Exchange Control Regulations of the country. Purchase of foreign currencies constitutes inward foreign remittance and sale of foreign currencies constitutes outward foreign remittance.

The transaction of the authorized dealer in foreign exchange involves either outward or inward remittances of foreign exchange from one country to another.

A customer is permitted to endorse maximum US $ 3000 per year for countries other than SAARC countries and US $ 1000 for SAARC countries. If SAARC countries are to be visited by road then per year US $500 can be endorsed per passport. At cash can not be endorsed over US $500.

NCC Bank issues following drafts:-

¨ Traveler’s Check,

¨ Foreign Demand Draft,

¨ Endorsement of Cash

Analysis

Import position of Foreign Exchange Branch:

| Year | NCCBL Import | NCCBL Growth | F. Ex Br. Import | F Ex BR. Growth | Contribution of F Ex Br. |

| 2007 | 28779.21 | 3092.3 | 10.74% | ||

| 2008 | 38796.8 | 34.8% | 4233.6 | 36.9% | 10.9% |

| 2009 | 19896.6 | – 48.7% | 2137.8 | – 49.5% | 10.7% |

| 2010 | 25069.7 | 27.89% | 2798.3 | 30.9% | 11.16% |

Sources: Financial statement of NCC Bank ltd, F Ex Br.

From the above diagram we can see that in 2009 there was the lowest amount of import through foreign exchange branch of NCC Bank Ltd which was TK.2137.8 million. We can see that from 2007 to 2008 the import was in growth In 2008 import was in highest position which is TK.4233.6 million in amount & the growth rate was 36.9% which is highest till now, but in the very next year of 2009 foreign exchange branch experienced a negative growth rate of – 49.5% and the import amount decreased to TK.2137.8 million. But in next year foreign exchange branch has recovered its position. It has achieved a positive growth rate and import increased to TK.2798.3 million.

In every year foreign exchange branch has contributed more than 10% of the NCC Banks total import. In 2009 it contributed 10.7% of total import even though in that year the bank experienced a negative growth.

From the above diagram we can see the growth comparison between NCC bank ltd aggregate import and Foreign Exchange Br. Import we see that in 2008 the F Ex. Branch growth was 36.9% which was higher than the NCC bank’s total growth of 34.8%. This was highest growth of Foreign Exchange branch. In 2009 the growth was negative and it was -49.5%, but the total growth of NCCBL was -48.7%. In 2010 the import businesses get back on the track, it gained a positive growth. Total bank growth was 27.89% where F. Ex branch growth was 30.9%.

Export position of Foreign Exchange Br.

| Year | NCCBL Export | NCCBL Growth | F Ex Br. Export | F Ex Br Growth | Contribution of F EX Br. |

| 2007 | 9577.92 | 814.12 | 8.5% | ||

| 2008 | 12522.4 | 30.74% | 1081.7 | 32.86% | 8.64% |

| 2009 | 7763.8 | -37.9% | 724.1 | -33.06% | 9.33% |

| 2010 | 9083.65 | 17% | 852.7 | 17.76% | 9.40% |

Source: Financial statement of NCC Bank Ltd, F Ex Br.

From the above diagram we can see that, last four year export trends shows a huge growth from year 2007 to 2008, but like import trend, in 2009 the export through Foreign Exchange Br. of NCC bank has also fall down and it was a negative growth in that year. If we compare it with the total position of NCC Bank Ltd, we find that in every year the contribution of Foreign Exchange Br. was more than 9% even though that year bank has experienced a negative growth.

From the above Diagram we can see the comparison of export growth between NCC Bank Ltd & F Ex Br. The highest growth of Foreign Exchange Br was 32.86% in 2008. The total bank growth was 30.74% in that year. In 2009 the growth was negative for both NCCBL and F Ex Br, but in 2010 the company gets back on track and it regained the positive growth.

Import VS Export

| Year | Import | Export |

| 2007 | 3092.3 | 814.12 |

| 2008 | 4233.6 | 1081.7 |

| 2009 | 2137.8 | 724.1 |

| 2010 | 2798.3 | 852.7 |

Source: Financial statement of NCC Bank Ltd, F EX Br.

From the above line diagram if we compare last four years growth trend of Import & Export of Foreign Exchange Br. of NCC Bank Ltd, we will see that in from the beginning there is a vast difference between import and export. From year2007 to 2008 both import & Export were increasing but in 2009 import & export both were decreasing. Also we can see that decrease in export was less than the decrease in import. In 2010 again both import &export was started to increase.

Remittance

| Year | Remittance | Growth rate |

| 2007 | 227.2 | |

| 2008 | 307.3 | 35% |

| 2009 | 341.1 | 11% |

| 2010 | 421.2 | 23.5% |

Source: Financial statement of NCC Bank Ltd, F Ex Br.

The above bar diagram is much more satisfactory for the Foreign Exchange Br of NCC Bank Ltd. We can see that unlike the Export and Import condition it is a purely upward sloping curve. It has maintained a consistent growth rate. In the year 2008 the growth rate was the highest and it was 31.96%. In 2009 the growth has been decreased to 11%. But in 2010 the growth increased to 23.5%.

Findings:

- In year 2008 import and its growth rate of foreign exchange branch of NCC Bank Ltd was in highest position where the amount was TK.4233.6 million and the growth rate was 36.9%.

- The impact of global recession has fallen on the import transaction in 2009 when the growth rate has turned negatively for NCC Bank Ltd & Foreign Exchange Br. which was -48.7% and -49.5% respectively. In 2009 F EX. Br was in better position in compare to the total banks growth.

- Up to the year 2008 the export through foreign exchange branch of NCC Bank Ltd was in good position. For NCC Bank and Foreign Exchange Br in 2008 there was a highest growth of 30.74% and 32.86% and it was TK 12522.4million and TK.1081.7 million.

- In 2009 the growth was negative for both the NCC Bank and as branch. Growth of bank was -37.9. % & for F Ex Br it was -33.06%.

- Inward remittance has not seriously affected by economic crisis as other foreign exchange activities. Though the growth rate has slightly decreased, still now it is representing a positive growth.

- The export of huge manpower in the different country is the main strength of the inward remittance that comes through NCC Bank Ltd.

- Accept the recession affected year of 2009, both the Import & Export condition of foreign exchange branch was in the growth.

- Total export of the branch is less then total import, if we express export as percentage of import than we can see Export is only 25% to 34% of import.

- Letter of credit (L/C) opening system for the importer is not a easy process. For processing of L/C document, it requires huge amount of time and money as well.

- The existing clients of Foreign Exchange activities of the bank get more benefit than newer.

- Though the maximum of the foreign exchange Foreign Exchange clients are giants in nature, the number of clients is very small in the foreign exchange branch.

- There has a lack of manpower in the foreign exchange division. Some important task of foreign exchange division are hampered, even some case not accomplished in due time only because of the crisis of manpower.

- The major sector of Import and Export the foreign exchange branch deal with is the product of readymade garments industry.

- The bank is circulating in a traditional way. The way of serving customer is not up to the mark.

- Number of ATM booth is very poor, customer have to use other banks booth.

Conclusion:

During the three months practical orientation program at various department of foreign exchange branch of NCC Bank Ltd, almost all the desks have been observed more or less. This practical orientation program, in first, has been arranged for gaining knowledge of practical banking and to compare to this practical knowledge with the theoretical knowledge. Comparing practical knowledge with theoretical involves identification of weakness in the department activities and making recommendation for solving the weakness identified. Though all sections of foreign exchange branch are covered in the internship program, it is not possible to go to the depth of each activities department because f time limitation. However highest effort has been given to achieve the objectives of the internship program.

Banking is a dynamic business. Today is beset by momentous changes in virtual every facet of industry activities. By assessing the current position of the bank, any hindrances must be seen as a challenge and not as a threat. Any such problems must be tackled accordingly.

The foreign exchange activities are performing by NCC Bank Ltd as well as the foreign exchange branch of NCCBL with successfully and a good reputation. The foreign exchange branch is continuously satisfying their customers through their efficient working force. The business position is also in a good position comparing to the other branches of the bank. The branch is also contributing significantly to the NCC Bank’s total performance. Through the foreign exchange operation and all other banking activities, NCC Bank Ltd is no doubt, playing a vital role in the economic sector of our country.

This report has attempted to explain the banking practice that are followed by the NCC Bank and also attempt to harmonize and link the theoretical knowledge, acquired in the program, with the experience gathered in the period practical orientation.

Recommendation:

The modern bank with vast and complex banking system operates its different commercial activities with some competitive strength and weakness. It is very difficult for me to recommend for a complex organization like commercial bank. As I have got an opportunity to work with NCC Bank Ltd for three months, I have got some practical experience about the banking sector as well as the NCCBL. On the basis of my observation, I would like to recommend the following suggestions

- The customer services need to improve in modern way for the purpose of adding some value and customer satisfaction.

- Some sort of customer needs and satisfaction related survey may be conducted to find innovative and better ways of customer satisfaction and it may increase the portion of customer loyalty.

- Card facilities including the ATM booths should be improved by NCCBL.

- In general banking division their need to give appoint much skilled, trained and smart employees.

- NCC Bank Ltd an emphasis on regular employees rather than casuals.

- Some extensive promotional activities should be taken to make the bank familiar to the society. In that case NCCBL can attend in social activities

- As a result of of global economic recession the growth of export was negative in 2009. Foreign Exchange Br of NCC Bank need to be more aggressive with their promotional activities, their service and charges to overcome this situation.

- In 2009 the import growth of F EX BR was also negative, so the bank should do something to overcome the situation.

- The branch may seek for new customers to recover the world economic crisis impact on its growth and to boost up its Import and Export position.

- The position of export is very poor in terms of import. Bank should take some necessary action to improve the export condition.