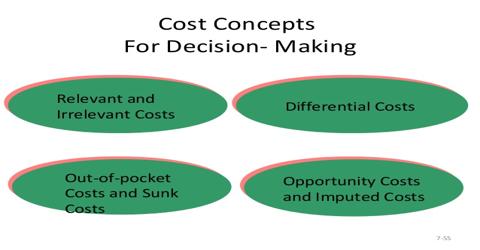

Prime purpose of this lecture is to present on Relevant Costs for Decision Making. Making decisions is one of the basic functions of a manager. To be successful in decision making, managers must be able to tell the difference between relevant and irrelevant data and must be able to correctly use the relevant data in analyzing alternatives. The purpose of this chapter is to develop these skills by illustrating their use in a wide range of decision-making situations. Two broad categories of costs are never relevant in any decision. They include: Sunk costs and Future costs that do not differ between the alternatives.

Relevant Costs for Decision Making