Introduction

1.1 Background of the Study

All over the world the dimension of Banking has been changing rapidly due to Deregulation, Technological innovation and Globalization. Banking in Bangladesh has to keep pace with the global change. Now Banks must compete in the market place both with local institutions as well as foreign ones. To survive and thrive in such a competitive banking world, two important requirements are development of appropriate financial infrastructure by the central bank and development of “professionalism” in the sense of developing an appropriate manpower structure and its expertise and experience. To introduce skilled Banker, only theoretical knowledge in the field of banking studies is not sufficient. An academic course of the study has a great value when it has practical application in real life situation. So, I need proper application of my knowledge to get some benefit from my theoretical knowledge make it more tactful.

In a simple word, Excellence is the Capacity of producing desired result. So, Excellence of customer is, how customers perceive services, how they assess whether they have experienced quality services and whether they are satisfied or not.

When it refers to Excellence of customer, we assume that the dimensions of services and the ways in which customer evaluate services are similar where the customer is internal & external of the organization.

1. 2 Problem Statement:

The topic of the report is “customer satisfaction on repayment Behavior: A case On Brac Bank Ltd”.

This topic serves dual purposes, number one is for my learning purpose and another one is, measuring the customers’ satisfaction on repayment Behavior toward Brac Bank Ltd. This report describes that in which factors customers are how much satisfied. And also an analysis as well as some recommendations for providing better service to the customers.

1.3 Objectives :

The objectives of the study are as follows:

Broad Objective:

To have an overview on “Customers’ satisfaction on repayment Behavior” A case on BRAC Bank Ltd.

Specific Objective:

To accomplish this objective, following specific objectives have been covered:

- To develop knowledge about repayment Behavior of loan

- To develop knowledge about General activities and SME Loan of Brac Bank Ltd

- To analyze the customers satisfaction in Brac Bank Ltd

- Find out the possible solution of repayment behavior.

- To identify the problems and weaknesses of Brac Bank Ltd

Methodology

2.1 Research Design: This research is used for finding out the satisfaction level of the customers’ of Brac Bank Ltd and submitting a recommendation making the processing easy towards better customer service for Brac Bank Ltd.This is a descriptive research.

2.2 Research Approach: To find out the level of customer satisfaction on repayment behavior the researcher collected data from the new and old customers who have take loan and repayment from Brac Bank. Not taken any opinion from the loan Brower because there is no similarity between taken loan and repayment. Then the research is qualitative in its approach.

2.3 Sampling Method:

This study was conducted by different people who have taken loan. And since 2001 to present approximately there are 85 loan Brower who have taken loan. Some of them are do not provided loan perfectly. As the number of loan taker is small so that the sample size was also small. From those I took 35 loan takers from different place as my sample size, non probability convenience sampling was taken to complete this research. The questionnaire was distributed to that loan taker and the percentage of response is 100%.

2.4 Survey Instruments: A structured questionnaire designed on the basis of Likert scale used for business research is the main instrument of this survey.

2.5 Data Collection:

- Primary Sources: Primary source of data is the face to face conversation with the loan taker. They answered the questions which mentioned in the questionnaire. And they wrote their suggestions according to their opinions. A questionnaire was designed for this survey to measure their satisfaction level.

- Secondary Sources: Annual reports and training, some data which has published and which hasn’t published yet of Brac Bank was the source of secondary data. Internet, newspaper and different websites were also used as a source of secondary data.

2.6 Data processing methodology: Collected data was entered in the research software called SPSS. Using SPSS, Frequency analysis and percentage was calculated for all questions and responses. Finally analysis of total output was used for recommendation.

2.7 Limitations of the Study:

The internship report is not free from limitations. The study has been conducted on the subject of A Report on “Customers’ Satisfaction on Repayment Behavior : A Study On Brac Bank Ltd” key limitations of the study are as follows:

- Some loan taker was not sincere because of their time limitation as most of them are businessman.

- Another limitation of the report is not to disclose some data and information to keep secrecy the Bank policy.

- Not able to collect information from all the clients.

- Time was the most important limitation in preparation of the internship report; that was very limited which disable many opportunities for a comprehensive study.

Organizational Background

3.1 History of Brac Bank Ltd (BBL):

Preamble: BRAC Bank Limited, with institutional shareholdings by BRAC, International Finance Corporation (IFC) and Shore cap International, has been the fastest growing Bank in 2004 and 2005. The Bank operates under a “double bottom line” agenda where profit and social responsibility go hand in hand as it strives towards a poverty-free, enlightened Bangladesh.

A fully operational Commercial Bank, BRAC Bank focuses on pursuing unexplored market niches in the Small and Medium Enterprise Business, which hitherto has remained largely untapped within the country. In the last five years of operation, the Bank has disbursed over BDT 1500 crore in loans to nearly 50,000 small and medium entrepreneurs. The management of the Bank believes that this sector of the economy can contribute the most to the rapid generation of employment in Bangladesh. Since inception in July 2001, the Bank’s footprint has grown to 26 branches, 350 SME unit offices and 19 ATM sites across the country, and the customer base has expanded to 200,000 deposit and 45,000 advance accounts. In the years ahead BRAC Bank expects to introduce many more services and products as well as add a wider network of SME unit offices, Retail Branches and ATMs and paid up capital of the same bank is Tk 500.million.

Background of the Organization: BRAC Bank Limited is a scheduled commercial bank in Bangladesh. It established in Bangladesh under the Banking Companies Act, 1991 and incorporated as private limited company on 20 May 1999 under the Companies Act, 1994. The primary objective of the Bank is to provide all kinds of banking business. At the very beginning the Bank faced some legal obligation because the High Court of Bangladesh suspended activity of the Bank and it could fail to start its operations till 03 June 2001. Eventually, the judgment of the High Court was set aside and dismissed by the Appellate Division of the Supreme Court on 04 June 2001 and the Bank has started its operations from July 04, 2001. The Chairman of the Bank is Mr. Fazle Hasan Abed. Now the Managing Director of the bank is Mr. Imran Rahman. The bank has made a reasonable progress due to its visionary management people and its appropriate policy and implementation.

Since its inception PR is giving emphasize on four things:

(a) Quality provide (in Loan)

(b) Commitment (for timely handover)

(c) Service (to the clients)

(d) Satisfaction (of the clients)

3.2 Organization Structure

Management Hierarchy:

Departments of BRAC Bank Ltd:

If the jobs are not organized according to their interrelationship and are not allocated in a particular department it would be very difficult to control the system effectively. If the departmentalization is not fitted for the particular works there would be haphazard situation and the efficiency of particular department will decline. BRAC Bank Ltd. has does this work properly. There are 18 departments in BRAC Bank Ltd. These departments are as follows:

- Human Resources Department

- Financial Administration Department

- Asset Operations Department

- Credit Division

- SME Division

- Internal Control & Compliance Department

- Marketing & Product Development Department

- Impaired Asset Management Department

- Remittance Operation Department

- Treasury Front

- Treasury Back

- General Infrastructure Service

- Information Technology Department

- Customer Service Delivery

- Cards Division

- Call Center

- Cash Management Department

- Secured Remittance Department

3.3 Mission, Vision, Goals, Objectives:

Corporate Mission:

Sustained growth in ‘small & Medium Enterprise’ sector

Continuous low cost deposit growth with controlled growth in Retained Assets

Corporate Assets to be funded through self-liability mobilization. Growth in Assets through Syndications and Investment in faster growing sectors

Continuous endeavor to increase fee based income

Keep our Debt Charges at 2% to maintain a steady profitable growth

Achieve efficient synergies between the bank’s Branches, SME Unit Offices and BRAC field offices for delivery of Remittance and Bank’s other products and services

Manage various lines of business in a fully controlled environment with no compromise on service quality

Keep a diverse, far flung team fully motivated and driven towards materializing the bank’s vision into reality

Aimed to assisting in the development of the housing sector and meet the demand by efficient use of resources.

Corporate Vision:

BRAC Bank will be a unique organization in Bangladesh. It will be a knowledge-based organization where the BRAC Bank professionals will learn continuously from their customers and colleagues worldwide to add value. They will work as a team, stretch themselves, innovate and break barriers to serve customers and create customer loyalty through a value chain of responsive and professional service delivery.

Continuous improvement, problem solution, excellence in service, business prudence, efficiency and adding value will be the operative words of the organization. BRAC Bank will serve its customers with respect and will work very hard to instill a strong customer service culture throughout the bank. It will treat its employees with dignity and will build a company of highly qualified professionals who have integrity and believe in the Bank’s vision and who are committed to its success. BRAC Bank will be a socially responsible institution that will not lend to businesses that have a detrimental impact on the environment and people. So Brac Bank operates following a specific vision like:

“Building a profitable and socially responsible financial institution focused on Markets and Business with growth potential, thereby assisting BRAC and stakeholders build a “just, enlightened, healthy, democratic and poverty free Bangladesh”.

Goals:

BRAC Bank will be the absolute market leader in the number of loans given to small and medium sized enterprises through out Bangladesh. It will be a world-class organization in terms of service quality and establishing relationships that help its customers to develop and grow successfully. It will be the Bank of choice both for its employees and its customers, the model bank in this part of the world.

Objectives:

Building a strong customer focus and relationship based on integrity, superior service.

To creating an honest, open and enabling environment

To value and respect people and make decisions based on merit

To strive for profit & sound growth.

To perform social responsibility for a happy future.

To satisfy clients by expert-oriented service.

To value the fact that they are the members of the BRAC family – committed to the creation of employment opportunities across Bangladesh.

To work as a team to serve the best interest of our owners

To relentless in pursuit of business innovation and improvement

To base recognition and reward on performance

To responsible, trustworthy and law-abiding in all that we do

To mobilize the savings and channeling it out as loan or advance as the company approve.

To establish, maintain, carry on, transact and undertake all kinds of investment and financial business including underwriting, managing and distributing the issue of stocks, debentures, and other securities.

To finance the international trade both in import and export.

To develop the standard of living of the limited income group by providing Consumer Credit.

To finance the industry, trade and commerce in both the conventional way and by offering customer friendly credit service.

To encourage the new entrepreneurs for investment and thus to develop the country’s industry sector and contribute to the economic development.

3.4 Markets:

BRAC Bank has a vision to develop human and economic position of a country. Its function is not limited only to providing and recovering of loan. But also try to develop socio-economic sector of the country.AndBrac Bank has one well operational Banking system and it is located at Niketon in Gulshan. They also have product name Small Medium Enterprise

(SME) to acquire interest from other people. SME plays a great role to remain this industry. SME Coverage many areas such as Dhaka, Bogra,Sherpur ,Sylhet,Jessore ,Barisal,Khulna etc

SME Network Coverage

3.5 Services / Products of BBL:

There are five different business units generating business BRAC Bank Limited:

Small & Medium Enterprise (SME)

Corporate Banking

Retail Banking

Treasury

Remittance Services

All the units are being operated in a centralized manner to minimize costs and risks.

Small & Medium Enterprise (SME):

For SME loan operation,

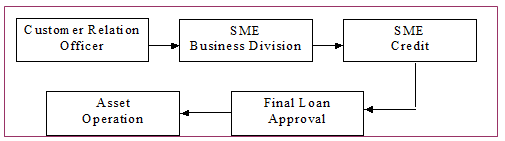

BRAC Bank Ltd has in total 900 unit offices, 80 zonal office, 12 territory and 1800 Customer Relationship Officers. These CROs work for the Bank to converge clients for getting the SME loan. Once CROs get the loan application and if it is less than 500,000 TK then zonal officer has the authority to approve the loan. But if it is above 500,000 then the CROs send it to Head Office for all necessary approval. After approving the loan then Asset Operation Department starts its work. As the scopes of businesses are growing, the amount of files and disbursement is getting bigger. In May 2007, AOD has processed 3249 files amounting Tk. 1,235,200,000. So SME Division’s success greatly relies on the performance.

SME Products-

1. Prothoma Rin.

2. Supplier Finance.

3. Anonno Rin.

4. Digoon Rin.

5. AroggoRin.

6. Pathshala Rin.

7. Opurbo Rin.

SME Loan process flow is shown below-

When a customer comes to the unit office for a loan request, first he/she meets with the customer relationship officer to discuss about the loan, which loan product is suitable for him/her. After then the following process takes place:

Corporate Banking:

Categories- the facilities our corporate Division offers to our customers are mainly of two-

Funded Facilities:-

Funded tells us that this type of facilities allows the customer to have money ‘on his hand’ for use i.e. he will get money as to meet his business demand. Examples are-

Working Capital Loan.

Over Draft Facility.

Term Loan.

Lease Finance.

Demand Loan.

Non-Funded Facilities-

Non-Funded facilities are those type of facilities where customers don’t get fund on their hand rather get Bank’s Guarantee service to do international trading-import and export. Letters of Credit, Bank guarantees etc. are the examples of the non-funded facilities.

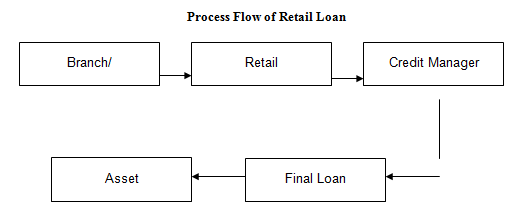

Retail Banking:

Retail Loans are consumers’ loan. Based on the customer demand these loans are given. BRAC Bank has a wide range of retail loan-

1. Car Loan. 2. Doctor’s Loan.

3. Secured Loan/OD. 4. High Flyer Loan.

5. Top Up Loan. 6. Credit Card Loan.

7. Study Loan. 8. Teacher’s Loan.

9. Now Loan. 10. Salary Loan.

BRAC Bank’s Retail Division is being operated centrally. Under the Retail Banking Division all the branches, which acts as sales & service center, are reportable to Head of Retail Banking. Different products of Retail Banking are as follows:

i) Deposit Products

ii) Lending Products

iii) Locker Services

iv) Remittance Services etc.

Treasury

Money Market Desk

BRAC Bank has a strong presence in the Treasury Market in Bangladesh. The Money Market Desk of the Treasury Division mainly deals in Bangladeshi Taka transactions. The basic activities undertaken by the Money Market Desk are:

- Management of Statutory Reserves viz. Cash Reserve Ratio (CRR) & Statutory Liquidity Ratio (SLR)

- Daily Funds & Liquidity Management

- Investment Management

Treasury Services

- Call/Overnight Lending & Borrowing

- Term Money Borrowing & Lending

- Repurchase Agreement

- Treasury Bills (T-Bills)

Monitoring:

Area of Monitoring-

The purpose is to know the entire business condition and all aspects of the borrowers so that mishap can be avoided.

i. Business Condition: The most important task of the CRO to monitor the business frequently, it will help him to understand whether the business is running well or not, and accordingly advice the borrower, whenever necessary. The frequency of monitoring should be at least once month if all things are in order.

ii. Production: The CRO will monitor the production activities of the business and if there is any problem in the production process, the CRO will try to help the entrepreneur to solve the problem. On the other hand the CRO can also stop the misuse of the loan other than for the purpose for which the loan was disbursed.

iii. Sales: Monitoring sales proceed is another important task of the CRO it will help him to forecast the monthly sales revenue, credit sales etc. which will ensure the recovery of the

monthly loan repayments from the enterprise as well as to take necessary steps for future loans.

iv. Investment: It is very important to ensure that the entire loan has been invested in the manner invented. If the money is utilized in other areas, then it may not be possible to recover the loan.

Terms and Conditions of SME Loan:

The SME department of BRAC Bank will provide small loans to potential borrower under the following terms and condition:

- The potential borrowers and enterprises have to fulfill the selection criteria

- The loan amount is between Tk 2 lacs to 30 lacs.

- SME will impose loan processing fees for evaluation/ processing a loan proposal as following:

- Loan can be repaid in two ways:

a) In equal monthly loan installment with monthly interest payment, or

b) By one single payment at maturity, with interest repayable a quarter end residual on maturity

- Loan may have various validates, such as, 3 months, 4 months, 6 months, 9 months, 12 months, 15 months, 18 months, 24 months, 30 months and 36 months.

- The borrower must open a bank account with the same bank and branch where the SME has its account

- Loan that approved will be disbursed to the client through that account by account payee cheque in the following manner: Borrower name, Account name, Banks name and Branch’s name

- The loan will be realized by 1st every months, starting from the very next months whatever the date of disbursement, through account payee cheque in favor of BRAC Bank Limited A/C. With Bank’s named and branches name

- The borrower will install a signboard in a visible place of business or manufacturing unit mentioned that financed by “BRAC Bank Limited”.

- The borrower has to give necessary and adequate collateral and other securities as per bank’s requirement and procedures.

- SME, BRAC Bank may provide 100% of the Net Required Working Capital but not exceeding 75% of the aggregate value of the Inventory and Account Receivables. Such loan may be given for periods not exceeding 18 months. Loan could also be considered for shorter periods including one time principal repayment facility, as stated in loan product sheet.

- In case of fixed asset Financing 50% of the acquisition cost of the fixed asset may be considered. While evaluating loans against fixed asset, adequate grace period may be considered depending on the cash generation after the installation of the fixed assets. Maximum period to be considered including grace period may be for 36 months.

Customer Handling (CH):

In our country currently 52 banks are working with the people through varieties of their attractive products and services and the competition among them is very high. For sustaining, they are offering various types of innovative product for better service for their valuable clients, so, to reach the closer best to the clients’ direct marketing gaining momentum in the country. In terms of SME, its targeted entrepreneurs are the subjects of dealings to achieve the objectives of BRAC Bank and its policy is to contact with clients directly with a confident manner. Some key activities of a CRO:

- Conducting Survey Properly

- Individual contact with entrepreneur for selecting potential borrower

- Deliver BRAC Bank’s products and other services

- Keeping in close touch with clients to develop mutually beneficial long term relationship

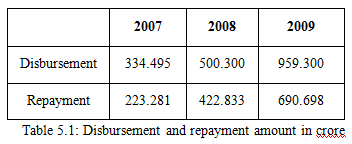

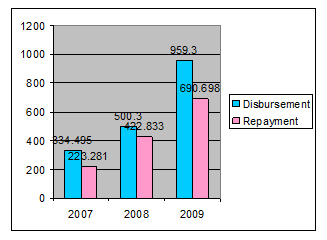

Disbursement & Repayment Status:

This status from 2007 to 2009 (Amounts in Crore) is shown as below:

Graphically-

For January 2009:

2009 | |

Disbursement | 87.908 |

Repayment | 76.084 |

We can see that the status of disbursement & repayment is increasing day by day. So it is hoped that in future, it will be increasing.

Competitors:

In terms of World Bank advice, most of the private banks are ready to provide small or micro credit loans to the clients because small loans are less risky than the corporate loan. At the recent trend, many banks like Standard Chartered, Islami Bank of Bangladesh, Eastern Bank Limited, Southeast Bank, Dutch Bangla Bank Limited etc are going to take many aggressive steps in terms of small loan to clients.Standard chartered bank already sent marketing troops surrounding the cities for providing loans and deposits. CITI Bank is going to start retail service business for capturing the market. So competitor’s analysis is important factor to carry out in the long run business for any organizations. Among these banks, many of them have lower interest rates but lots of hidden costs and services.

3.6 Performance of Brac Bank Ltd:

BRAC Bank Limited will be the most successful private sector commercial bank in our country, though it started its operation few years back. It has achieved the trust of the general people and made reasonable contribution to the economy of the country by helping the people investing allowing credit facility.

Capital Fund: The authorized and paid up capital of BBL is TK.1000 million and TK.500 million respectively. The paid up capital is one of the strongest in the banking industry. The bank is going to raise its paid up capital in the month September, 2006 by TK.500 million with issuing public share of 5, 00,000 of TK.100 each.

Date | 31/12/06 | 31/12/07 | 31/12/08 | 31/03/09 |

| Ordinary share | 405,020,000 | 500,000,000 | 500,000,000 | 500,000,000 |

| Preference share | 150,000,000 | |||

| Statutory reserve | 19,860,550 | 58,396,570 | 135,564,816 | |

| Surplus in profit | (9,095,940) | 70,346,259 | 224,490,340 | 226,006,069 |

| Total | 395,924,060 | 590,206,809 | 782,886,910 | 1,011,507,885 |

3.7 Analysis Turnover

3.8 SWOT analysis:

Strengths:

- The number of branches is more than any other bank in our country.

- Provide better loan service

- Brac bank Ltd has already established a favorable reputation in the banking industry of the country.

- A good number of experienced bankers in its management.

- The numbers of depositors are more than other bank in our country.

- Largest private sector commercial bank of Bangladesh.

- Management team is very qualified.

- Highest most profitable bank in Bangladesh.

Weaknesses:

- The activities of bank are maintained by manually in the rural area.

- Lack of employee satisfaction.

- Lack of modern information technology being practiced.

- Many competitors.

- Salary is fewer amounts other than competitors.

Opportunities:

- Many area SME network coverage

- Their network service is whole the country, so people get more service here.

- Brac Bank can collect deposit from rural area that other bank can not do because of their huge branches.

- The income of people is increasing day by day.

- People are interested in getting personal loan with lower interest rate.

- High contribution in economic development

- Money transfer easily in any branches of Bangladesh.

Threats:

- Many banks offer different type of product that people like than Brac Bank.

- Banking competitors are increasing.

- Some time the recruitment process is not effective.

3.9 Areas of improvement:

► Working process of CRO:

The working process that they are followed is not very speedy. All the process takes manual involvement. Another thing is sometimes organization remain busy for interest incresing. And before completing the interest they can’t provide the loan. And many of time they fill soil by truck. It’s a slow process.

► Facilities for employees:

BRAC Bank Ltd(BBL) tries to give all types of facilities that they want for better performance. But still there is some lacking like there is nothing to entertain. So that employees get bored. As well as the working hour is 10am to 7pm. It is also be shorted.

► Equipments:

They use computer, printer and papers as equipments. Computer that they are using is very old version and it is need to replace so that it can work effectively. On the other hand Data file that they use for identify the information is need to be updated because so many changes has happened in recent yea

Customer Satisfaction on Repayment behavior

4.1 Demographic profile of the respondents

This analysis part divided into two parts. Respondents were asked some general questions and beside this general questions they were also asked some questions to identify the customers satisfaction on Repayment Behavior of BRAC Bank Ltd. The analysis of general questions are given below.

Table 4.1: Gender

To complete this report the researcher had to conduct with 35 respondents where 32 respondents were male and rest of 3 were female. The ratio can be seen graphically in the pie chart.

Table 4.2: Level of Education

The study divided my respondents’ level of education into four classes. Among them less than SSC were 15 people. SSC were 10 persons. HSC were 5 persons. And BA/BSS/BSC/Honors were 5 persons. So I can say that most of the respondents are less than SSC. I can see the ratio of the different classes of people as follows on pie chat

Table 4.3: Occupation

After collecting the profession wise information we saw that Businessman is 14 respondents, Students 11 respondents, Service holder is 5 respondents and other is 5 respondents. Here we can see that mostly businessman and Students has take loan.

Table 4.4: Income

Table 4.7: Waiver based on repayment.

Q7: Taking loan from this bank is easy.

Table 4.5: Taking loan from this bank is easy.

| Frequency | Percent | |

| Strongly Agree | 18 | 51.4 |

| Agree | 8 | 22.9 |

| Neutral | 8 | 22.9 |

| Disagree | 1 | 2.9 |

| total | 35 | 100 |

Table shows 51% respondents strongly agreed that Taking loan from Brac bank is easy and 2.9% were disagreed. The mean is 4.23 (Appendix 1). This is the arithmetic average which is indicating most of the respondents marked between 5 and 4.The median is 5 (Appendix 1), that means the midpoint is 5.The mode is 5 (Appendix 1), that means 5 is the most repeated answer in this question. The calculated standard deviation is 0. (Appendix 1) It’s indicating the spread on the answers variability.

Q8:I am satisfied with the interest rate

Table 4.6: Satisfied with the interest rate

| Frequency | Percent | |

| Strongly Agree | 21 | 60 |

| Agree | 8 | 22.9 |

| Neutral | 6 | 17.1 |

| total | 35 | 100 |

Here Table shows that 60% respondents are strongly agreed and 22.9% respondents are agreed that they satisfied with the interest rate from this Bank because of its popularity. and 17.1% respondents are neutral with this question. The mean is 4.43 (Appendix 1). This is the average which is indicating most of the respondents marked between 5 and 4.The median is 5 (Appendix 1). The mode is 5 (Appendix 1), that means 5 is the most repeated answer in this question. The calculated standard deviation is 0.78 (Appendix 1) It’s indicating the spread on the answers variability.

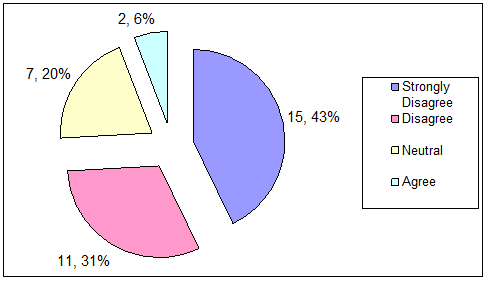

Q9: Customers get waiver based on repayment

Table 4.7: Waiver based on repayment.

| Frequency | Percent | |

| Strongly Agree | 13 | 37.1 |

| Agree | 7 | 20 |

| Neutral | 8 | 22.9 |

| Disagree | 5 | 14.3 |

| Strongly Disagree | 2 | 5.7 |

| total | 35 | 100 |

Customers get waiver based on repayment. Here analysis shows that 22.9 % respondents were neutral but 37.1 % respondents were Strongly agreed and only 14.3 % respondents were disagreed. And strongly disagreed persons were very few. The mean is 3.69 (Appendix 1). This is the average which is indicating most of the respondents marked between 5 and 3.The median is 4 (Appendix 1). The mode is 5 (Appendix 1), that means 5 is the most repeated answer in this question. The calculated standard deviation is 1.28 (Appendix 1) It’s indicating the spread on the answers variability.

Q10: Bank are nearby to my locality.

Table 4.8:Bank nearby to my locality

| Frequency | Percent | |

| Strongly Agree | 18 | 51.4 |

| Agree | 7 | 20 |

| Neutral | 9 | 25.7 |

| Strongly Disagree | 1 | 2.9 |

| total | 35 | 100 |

With this statement most of the respondents were strongly agreed. 9 people were neutral. 10 respondents were agreed and 1 people were strongly disagreed. The mean is 4.17 (Appendix 1). This is the average which is indicating most of the respondents marked 5.The median is 5 (Appendix 1). The mode is 5 (Appendix 1), the calculated standard deviation is 1.01 (Appendix 1).

Q11:I follow the rules and regulation of the loan.

Table 4.9: Rules and regulation of the loan

| Frequency | Percent | |

| Strongly Agree | 16 | 45.7 |

| Agree | 10 | 28.6 |

| Neutral | 8 | 22.9 |

| Strongly Disagree | 1 | 2.9 |

| total | 35 | 100 |

Here analysis shows that 45.7% respondents were strongly agree but 28.6 % respondents were agreed and 22.9% neutral and only 2.9 % respondents were strongly disagreed. The mean is 4.17 (Appendix 1). This is the average which is indicating most of the respondents marked between 4 and 5.The median is 4 (Appendix 1). The mode is 5 (Appendix 1), the calculated standard deviation is 0.89 (Appendix 1).

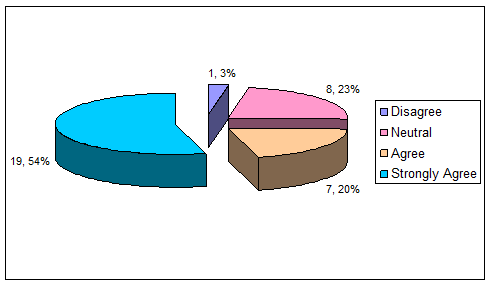

Q12: This bank provides competitive facilities.

Table 4.10: Bank provides competitive facilities

| Frequency | Percent | |

| Strongly Agree | 18 | 51.4 |

| Agree | 10 | 28.6 |

| Neutral | 6 | 17.1 |

| Disagree | 1 | 2.9 |

| Total | 35 | 100 |

Here analysis shows that 51.4% respondents are strongly agreed and 28.6% respondents are agreed that they satisfied with the competitive facilities from this Bank because of its popularity. And 17.1% respondents are neutral and only 2.9%respondents are disagree with this question. The mean is 4.29 (Appendix 1). This is the average which is indicating most of the respondents marked between 5 and 4.The median is 5 (Appendix 1). The mode is 5 (Appendix 1), that means 5 is the most repeated answer in this question. The calculated standard deviation is 0.86 (Appendix 1) It’s indicating the spread on the answers variability.

Q13: Customer relative officers (CRO) are very friendly

Table 4.11:CRO are very friendly

| Frequency | Percent | |

| Strongly Agree | 19 | 51.3 |

| Agree | 8 | 22.9 |

| Neutral | 8 | 22.9 |

| total | 35 | 100 |

According to frequency table 19 respondents says that the number of Customer relative officers (CRO) that are very friendly and customer is satisfactory. The calculated mean is 4.31 (Appendix 1). That means most of the respondents answered between 5 and 4. The median and mode are 5 (Appendix 1). The calculated standard deviation is 0.83 (Appendix 1)

Q14:I am satisfied with the repayment system of this bank.

Table4.12: Satisfiedwith the repayment system of this bank.

| Frequency | Percent | |

| Strongly Agree | 17 | 48.6 |

| Agree | 9 | 25.7 |

| Neutral | 9 | 25.7 |

| total | 35 | 100 |

Here analysis shows that 48.6% respondents are strongly agreed and 25.7% respondents are agreed that they satisfied with the repayment system of this bank. and 25.7% respondents are neutral with this question. The mean is 4.23 (Appendix 1). This is the average which is indicating most of the respondents marked between 5 and 3.The median is 4 (Appendix 1). The mode is 5 (Appendix 1), that means 5 is the most repeated answer in this question. The calculated standard deviation is 0.84 (Appendix 1) It’s indicating the spread on the answers variability.

Q15: I am satisfied with the terms and conditions of Small & Medium Enterprises (SME) that they provide.

Table 4.13: satisfied with the terms and conditions of SME

| Frequency | Percent | |

| Strongly Agree | 15 | 42.9 |

| Agree | 12 | 34.3 |

| Neutral | 8 | 22.9 |

| total | 35 | 100 |

The analysis shows 42.9% respondents strongly agreed that people satisfied with the terms and conditions of Small & Medium Enterprises (SME) that they provide. and 34.3% were agreed and 22.9% is neutral. The mean is 4.20 (Appendix 1). This is the arithmetic average which is indicating most of the respondents marked between 5 and 3.The median is 4 (Appendix 1).The mode is 5 (Appendix 1), that means 5 is the most repeated answer in this question. The calculated standard deviation is 0.80 (Appendix 1) It’s indicating the spread on the answers variability.

Q16: CRO give more practical suggestion to acquire knowledge of loan.

Table 4.14: CRO give more practical suggestion of loan.

| Frequency | Percent | |

| Strongly Agree | 3 | 8.6 |

| Agree | 2 | 5.7 |

| Neutral | 6 | 17.1 |

| Disagree | 12 | 34.3 |

| Strongly Disagree | 12 | 34.3 |

| total | 35 | 100 |

This analysis shows that most of the respondents are strongly disagreed that CRO give more practical suggestion to acquire knowledge of loan .So they are dissatisfactory. The mean is 2.20 (Appendix 1). This is the average which is indicating most of the respondents marked between 5 and 1.The median is 2 (Appendix 2). The mode is 1 (Appendix 2), that means 1 is the most repeated answer in this question. The calculated standard deviation is 1.23 (Appendix 1) It’s indicating the spread on the answers variability.

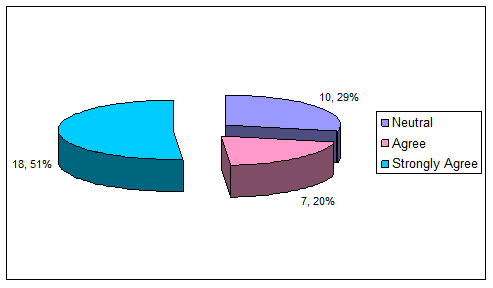

Q17: CRO are available during the consulting hour.

Table 4.15: CRO are available in the consulting hour

| Frequency | Percent | |

| Strongly Agree | 10 | 28.6 |

| Agree | 5 | 14.3 |

| Neutral | 7 | 20 |

| Disagree | 7 | 20 |

| Strongly Disagree | 6 | 17.1 |

| total | 35 | 100 |

With this statement most of the respondents were strongly agreed. Among the total of respondents 7 persons were neutral with this statement and 6 persons were strongly disagreed. The mean is 3.17 (Appendix 1). This is the average which is indicating most of the respondents marked between 1 and 5.The median is 3 (Appendix 1). The mode is 5 (Appendix 1), the calculated standard deviation is 1.48 (Appendix 1).

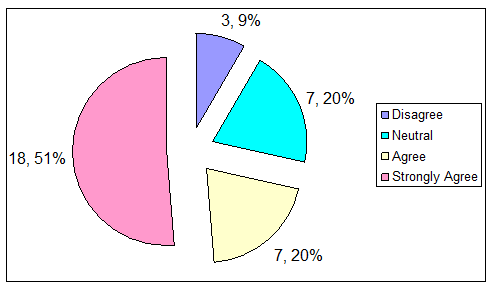

Q18: Overall loan facilities for the client are excellent.

Table 4.16: Overall loan facilities are excellent.

| Frequency | Percent | |

| Strongly Agree | 5 | 14.3 |

Agree12.9Neutral822.9Disagree925.7Strongly Disagree1234.3total35100

Here analysis shows that 12 persons were strongly disagreed with this statement that is 34.3 % and 8 people were neutral with the statement. 5 persons were strongly agreed and the rest were agreed. The calculated Mean is 2.37 (Appendix 1). This is the average of overall responses. The Median is 2 and Mode is also 1 (Appendix 3). The Standard deviation for this question is 1.37 (Appendix 1).

Q19: The loan they provide is proportionate to the asset I deposit

Table 4.17: They provide is proportionate to the asset.

| Frequency | Percent | |

| Agree | 2 | 5.7 |

| Neutral | 7 | 20 |

| Disagree | 11 | 31.4 |

| Strongly Disagree | 15 | 42.9 |

| total | 35 | 100 |

Most of the respondents strongly disagreed that BBL provide is proportionate to the asset o loan taker deposit. The percentage of strongly disagreed respondents is 42.9% and 31.4% is the percentage of disagreed respondents. The Calculated Mean for this question is 1.89 (Appendix 3). Mode is 2 and Median is 1 (Appendix 1), that representing most of the respondents marked 1. The Standard Deviation is 0.93 (Appendix 1).

Q20: There is uninterrupted loan supply in this bank

Table 4.18: There is continuous loan supply in this bank.

| Frequency | Percent | |

| Strongly Agree | 18 | 51.4 |

| Agree | 7 | 20 |

| Neutral | 10 | 28.6 |

| total | 35 | 100 |

Table shows that 51.4% respondents are strongly agreed and 20% respondents are agreed that they satisfied with the continuous loan supply in this bank. and 28.6% respondents are neutral with this question. The mean is 4.23 (Appendix 1). This is the average which is indicating most of the respondents marked 5 .The median is 5 (Appendix 1). The mode is 5 (Appendix 1), that means 5 is the most repeated answer in this question. The calculated standard deviation is 0.88 (Appendix 1) It’s indicating the spread on the answers variability.

Q21:I get loan in accordance with the nature of my business.

Table 4.19: Get loan in accordance of my business.

| Frequency | Percent | |

| Strongly Agree | 18 | 51.4 |

| Agree | 7 | 20 |

| Neutral | 7 | 20 |

| Disagree | 3 | 8.6 |

| total | 35 | 100 |

Most of the respondents strongly agreed. The percentage of strongly agreed respondents is 51.4% and 20% is the percentage of agreed respondents. Also the analysis showed that20 neutral and 8.6% disagreed. The mode and median of the question are 5 (Appendix 1). That means 5 is the number occurs most often.The calculated mean is 4.14 (Appendix 1) is supporting the statement that most of the respondents strongly agreed with the issue. The calculated standard deviation is 1.03. (Appendix 1) is representing the spread on variability of the distribution.

Q22: I satisfied to overall performance of this loan section

Table 4.20:Satisfied overall performance of this loan section

| Frequency | Percent | |

| Strongly Agree | 19 | 54.3 |

| Agree | 7 | 20 |

| Neutral | 8 | 22.9 |

| Disagree | 1 | 2.9 |

| total | 35 | 100 |

The analysis shows 54.3% respondents strongly agreed that loan taker satisfied to overall performance of this loan section. Also the analysis showed that neutral 22.9% and 2.9% disagreed. The mode and median of the question are 5 (Appendix 1). That means 5 is the number occurs most often and also 5 is the midpoint. The calculated mean is 4.26 (Appendix 1) is supporting the statement that most of the respondents strongly agreed with the issue. The calculated standard deviation is 0.92. (Appendix 1) is representing the spread on variability of the distribution.

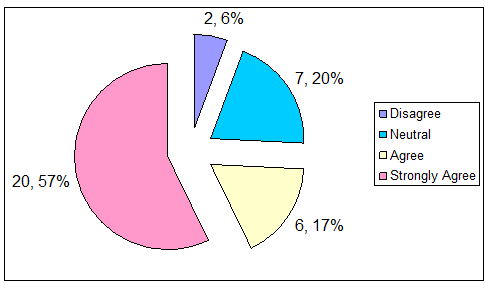

Q23:I will recommend to my relative to take loan in this bank.

Table 4.21:My relative to take loan in this bank.

| Frequency | Percent | |

| Strongly Agree | 20 | 57.1 |

| Agree | 6 | 17.1 |

| Neutral | 7 | 20 |

| Disagree | 2 | 5.7 |

| total | 35 | 100 |

With this statement most of the respondents were strongly agreed. And also strongly agreed respondents 57.1%.Among the total respondents 6 persons were agreed with this statement and 7 persons were neutral and 2 persons were disagreed. But there were no strongly disagreed people. The mean is 4.26 (Appendix 1). This is the average which is indicating most of the respondents marked 5.The median is 5 (Appendix 1). The mode is 5 (Appendix 1), the calculated standard deviation is 0.98 (Appendix 1).

Summery Of Findings

All over the world the dimension of Banking has been changing rapidly due to Deregulation, Technological innovation and Globalization. Banking in Bangladesh has to keep pace with the global change. Now Banks must compete in the market place both with local institutions as well as foreign ones. To survive and thrive in such a competitive banking world. So that a study has been made up on the customers’ of BRAC Bank to measure that how much satisfied they are. To complete this research a survey was conducted on 35 customers of BBL. The findings are as follows:

Among 35 respondents 32 respondents were male and rests of 3 were female. There are four categories level of education but most of the respondents are less than SSC-SSC. In occupation wise highest numbers of respondents are Businessman and Student. Most of the respondents are in income range of 75,001-1, 00,000. Among the 35 respondents most of them taken loan from BBL. After completing the survey we saw that respondents are strongly satisfied that taking loan from this bank is easy. Customers satisfied with the interest rate. After analysis this statement, the study show that most of the respondents give their opinion as a strongly agreed. Customers get waiver based on repayment. it does so. After analysis this statement, that most of the respondents are strongly agreed. Because of their reputation. The respondents are very satisfied about the bank are nearby to my locality. After analysis this statement I found that most of the respondents follow the rules and regulation of the loan. The respondents are very satisfied that this bank provides competitive facilities.

Customer relative officers (CRO) are very friendly. After analysis this statement, found that most of the respondents are strongly agreed. Because of their relation. Most of the respondents are very satisfied about the repayment system of the BBL.Respondents were strongly satisfied with the terms and conditions of Small & Medium Enterprises (SME) that they provide.CRO give more practical suggestion to acquire knowledge of loan. After analysis this statement, I found that most of the respondents are strongly agreed.

Most of the respondents are very satisfied because CRO are available during the consulting hour. Overall loan facilities for the client are excellent .after analysis this statement, found that most of the respondents give their opinion as a strongly disagreed. After completing the survey we saw that respondents are strongly dissatisfied that the loan they provide is proportionate to the asset customer deposit. Most of the respondents are strongly satisfied that there is uninterrupted loan supply in this bank. According to the nature of loan taker business that the respondents were very satisfied. Most of the respondents are strongly agree that overall performance of this loan section is better of BBL.This survey will recommend to my relative to take loan in this bank. After analysis this statement, found that most of the respondents are strongly agreed.

This bank is depending on the customers’ interest and satisfaction. So that BBL always concern about satisfaction of customers’. Finally observing all the factors we can include here that the customers of BBL is very much satisfied about the loan service of BRAC Bank.

Conclusion and Recommendations

6.1 Conclusion

In fact, BRAC Bank promotes broad-based participation in the Bangladesh economy through the provision of high quality and modern banking services. The research also found that loan has more priority in terms of selecting the different type of schemes according to the customer satisfaction on repayment. this report on the basis of the knowledge and experience gained during the internship period. Throughout the report my objective is to seek and find out the customer satisfaction on repayment behavior of Brac bank Ltd. From this report found that most of the customers of the bank are satisfied about the loan service of the bank. BRAC bank has established their image as one of the best loan service provider for its potential customers. And SME loan is one of such quality product through which they offer the small and mediocre entrepreneurs a quality banking services and earn the maximum profit as well. The recovery rate of this loan is 97%, which is extremely good in comparison to any other bank’s recovery rate. Brac Bank has made it possible as the loan is given to experienced, small and mediocre entrepreneurs most of whom are middle aged, slightly educated and having moderate income and this class of people is very loyal. But they can serve this class of customers with more commitment and loyalty and they can turn the recovery rate to 100%.

BRAC Bank Ltd started with a vision to be the most efficient financial intermediary in the country and it believes that the day is not far off when it will reach its desired goal.BRAC Bank Limited looks forward to a new horizon with a distinctive mission to become a highly competitive modern and transparent institution comparable to any of its kind at home and abroad.