Introduction

Originally the word “BANK” we can easily understand the financial institution that deals with money. But there are different types of banks like; Central Banks, Commercial Banks, Savings Banks, Investment Banks, Industrial Banks, Co-operative Banks etc. But when we use the term “Bank” without any prefix, or qualification, it refers to the ‘Commercial banks’. Commercial banks are the primary contributors to the economy of a country. So we can say Commercial banks are a profit-making institution that holds the deposits of individuals & business in checking & savings accounts and then uses these funds to make loans. For these people and the government is very much dependent on these banks as the financial intermediary. As banks are profit -earning concern; they collect deposit at the lowest possible cost and provide loans and advances at higher cost. The differences between two are the profit for the bank.

Banking sector is expanding its hand in different financial events every day. At the same time the banking process is becoming faster, easier and the banking arena is becoming wider. As the demand for better service increases day by day, they are coming with different innovative ideas & products. In order to survive in the competitive field of the banking sector, all banking organizations are looking for better service opportunities to provide their fellow clients. As a result, it has become essential for every person to have some idea on the bank and banking procedure.

Thesis program is essential for every student, especially for the students of Business Administration, which helps them to know the real life situation. For this reason a student takes the thesis program at the last stage of the Master’s degree, to launch a career with some practical experience.

The report entitled “Performance Evaluation of Dutch Bangla bank Limited” has been prepared as a partial fulfillment of BBA program authorized by the Department supervisor, Department of BBA program, Faculty of Business Administration, IBAIS University Bangladesh.

OBJECTIVES OF THE RESEARCH

The initial objective of this report is to obey with the requirement of the DBBL. But the objectives is not limited with in above, behind this study is something broader. Objectives of the study are summarized in the following manner:

To measure the overall performance of DBBL.

To apply the critical knowledge in the practical field.

To make a bridge between the theories and practical procedures of banking day-to-day operations.

To gain practical knowledge by working in different desks of Local office branch of DBBL.

To observe the working environment in commercial banks.

To study existing banker-customer relationship.

To know the overall functioning of DBBL.

To have some practical exposures that will be helpful for my future career.

METHODOLOGY

In order to make the report more meaningful and presentable, two sources of data and information have been used widely.

The “Primary Sources” are as follows:

Face-to-face conversation with the respective officers and staffs of the Branch.

Informal conversation with the clients.

Practical work exposures from the different desks of the departments of the Branch covered.

Relevant file study as provided by the officers concerned.

The “Secondary Sources” of data and information are:

Annual Report of DBBL.

Various books, articles, compilations etc. regarding general banking functions, foreign exchange operations and credit policies.

Different ‘Procedure Manual’, published by DBBL.

Different circular sent by Head Office of DBBL and Bangladesh Bank.

Data Collection procedure:

In order to collect the data a questionnaire which is a combination of both open ended and close ended has been used. Group discussion and personal interview also used to collect the data.

Data Processing:

In order to process the data MS Excel has been used to analyze the data and to prepare the graphical presentation.

LIMITATIONS OF THE RESEARCH

Limitation the time, between someday, was one of the most important factors to know all activities of the branch and prepare the report.

It was very difficult to collect the information from various personnel for their job constraint.

Every organization has their own secrecy that is not revealed to others. While collecting data i.e. interviewing the employees, they did not disclose much information for the sake of the confidentiality of the organization.

Another limitation of this report is Bank’s policy of not disclosing some data and information for obvious reason, which could be very much useful.

Because of the limitation of information, some assumption was made. So there may be some personal mistake in the report

6. I carried out such a study for the first time, so inexperience is one of the main constraints of the study.

CHEPTER-2

o DBBL RETROSPECT

Capital Structure

Deposit

Loans & Advances

Investment

Functions of DBBL

DBBL Operational Branches

CHAPTER -2

RETTROSPECT OF DBBL

Dutch Bangla Bank Limited (the Bank, DBBL) is a scheduled joint venture commercial bank between local Bangladeshi parties spearheaded by M Sahabuddin Ahmed (Founder & Chairman) and the Dutch company FMO. DBBL was established under the Bank Companies Act 1991 and incorporated as a public limited company under the Companies Act 1994 in Bangladesh with the primary objective to carry on all kinds of banking business in Bangladesh. The Bank is listed with the Dhaka Stock Exchange Limited and Chittagong Stock Exchange Limited.

DBBL commenced formal operation from June 3, 1996. The head office of the Bank is located at Sena Kalyan Bhaban (4th floor),195, Motijheel C/A, Dhaka, Bangladesh. The Bank commenced its banking business with one branch on 4 July 1996.

The bank is often colloquially referred to as “DBBL”, “Dutch Bangla” and “Dutch Bangla Bank”.

After instability and frequent management changes in its initial years, DBBL overcame these obstacles to establish itself as a market leader. It has grown its reputation through social work rather than profits. The bank’s conservative nature, long-term strategies, hefty social donations and technology investments have always led to modest but steady profits.

Due to investor confidence, DBBL share prices has steadily climbed in value. In January 2008, DBBL share prices reached Tk. 9,450 .00 in the Dhaka Stock Exchange, setting the record for the highest stock price in the history of Bangladesh. It is also one of the few banks that does not participate in merchant banking (which can lead to sporadic growth). DBBL has branded itself as a trusted bank through its banking practices and social commitments.

Dutch Bangla Bank is the first and only local bank in Bangladesh to have an automated banking system. The bank has spent over Tk. 1 Billion in automation upgrades (first bank in Bangladesh to do so). This automation took place in 2003 whereby services of the bank were available uniformly though any branch, ATM and internet. Banking was a paper based until DBBL, with its wide local network, delivered banking automation and modern banking services to the masses. This effectively introduced the ‘plastic money’ concept into the Bangladeshi society.

MISSION

Dutch-Bangla Bank engineers enterprise and creativity in business and industry with a commitment to social responsibility. “Profits alone” do not hold a central focus in the Bank’s operation; because “man does not live by bread and butter alone”.

VISION

Dutch-Bangla Bank dreams of better Bangladesh, where arts and letters, sports and athletics, music and entertainment, science and education, health and hygiene, clean and pollution free environment and above all a society based on morality and ethics make all our lives worth living. DBBL’s essence and ethos rest on a cosmos of creativity and the marvel-magic of a charmed life that abounds with spirit of life and adventures that contributes towards human development

CORE OBJECTIVE

Dutch-Bangla Bank believes in its uncompromising commitment to fulfill its customer needs and satisfaction and to become their first choice in banking. Taking cue from its pool esteemed clientele, Dutch-Bangla Bank intends to pave the way for a new era in banking that upholds and epitomizes its vaunted marques “Your Trusted Partner”.

SERVICES AND PRODUCTS

Deposit

Savings Deposit Account

Current Deposit Account

Short Term Deposit Account

Resident Foreign Currency Deposit

Foreign Currency Deposit

Convertible Taka Account

Non-Convertible Taka Account

Exporter’s FC Deposit(FBPAR)

Current Deposit Account-Bank

Short Term Deposit Account-Bank

Loan & Advances

Life Line (a complete series of personnel credit facility)

Loan agst. Trust ReceiptTransport Loan

Real Estate Loan (Res. & Comm.)Loan Agst.

CAPITAL

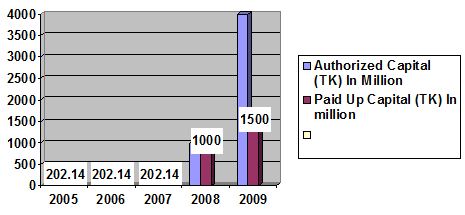

The bank started with an authorized capital of Tk.400.00 million in 1996 and as on 31st December 2009 paid up capital stood at Tk. 1,500 million. The total capital stood at Tk.5,899.79 million as on 31st December 2009, which was Tk. 4,587.48 million as on 31st December 2008. In 2009 Capital surplus Tk. 808.44 million which was Tk. 376.10 million

Analysis of capital structure:

Capital structure of DBBL has changed from year to year. The components of the capital structure are paid-up capital; proposed issue of dividend, share premium, statutory reserve, proposed cash dividend, retained earnings and other reserve

Authorized and paid up capital of DBBL:

| Authorized Capital (TK) In Million | Year | Paid Up Capital (Tk) In Million |

| 400.00 | 2005 | 202.14 |

| 400.00 | 2006 | 202.14 |

| 400.00 | 2007 | 202.14 |

| 1000.00 | 2008 | 1000.00 |

| 4000.00 | 2009 | 4000.00 |

Capital position of DBBL

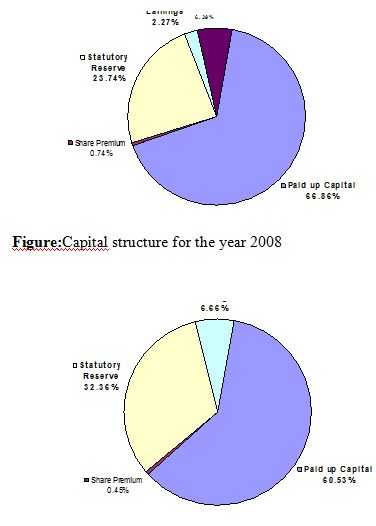

Components of capital structure and correspondent contributions:

Figures of different components of the capital structure for the year 2006 and 2007 are shown below.

Tk in million

| Components of capital structure | 2008 | 2009 |

| Paid-up capital | 1000 | 1500 |

| Proposed issue of bonus share | …….. | 500 |

| Share premium | 11.07 | 11.07 |

| Statutory reserve | 355 | 802 |

| Other reserves | ……… | |

| Proposed cash dividend | 95.53 | ……… |

| Retained earnings

| 34 | 165 |

| Total

| 1400.07(100%) | 2992.81(100%) |

In the annual report of the year 2009, capital structure did not contain any value for the component of proposed issue of bonus share, but in the annual report of the year 2009, it was mentioned that proposed issue of bonus share was 500 million taka. On the other hand proposed cash dividend did not contain any value in 2009, which was 95.53 in 2008.

Capital structure:

Pie chart of capital structure for the base year 2008 and the year 2009 has been shown below:

Fig: Capital structure for the base year 2009.

The above figures are showing the comparison between different components of capital structure of the base year 2008 and the year 2009. In the base year 2008, there was no proposed issue of bonus share proposed cash dividend and in the year 2009.

DEPOSIT

The total deposit of DBBL Tk. 67,788.53 million as on December 31, 2009, which was Tk 51575.67 in 2008. The DBBL remains committed to increasing deposit base by growing low cost personal and business accounts, and thereby lowering the banks over all cost of fund. So the deposit amount of DBBL is increasing year by year.

Deposit Position of DBBL:

Amount of Deposit (Tk In Million)

| Year | DBBL | SOUTH EAST BANK | BRAC BANK |

| 2009 | 67,788.53 | 55,065.54 | 37,368.41 |

| 2008 | 51,575.67 | 46,056.18 | 23,001.92 |

| 2007 | 42,110.15 | 38,258.15 | 13,409.01 |

| 2006 | 40,111.54 | 27,930.84 | 8,168.98 |

| 2005 | 27,241.11 | 19,618.82 | 3,497.30 |

Deposit in DBBL:

From the above chart we see that the deposit amount of south east bank is higher than other two in 2009. This is a upward slopping .The amount of deposited amount increased year by year.

LOANS AND ADVANCES

The advance portfolio of the bank is well diversified and broad based covering various sectors of the economy. Credit facilities were extended to the private sector for trade, project financing as well as to meet working capital requirements. During the year under review the Bank also extended credit facilities under lease facilities financing as well as syndication arrangements with other Bank and financial institutions.

In 2008 the loans and advance was Tk 41698.32 million. But in 2009 is stated Tk 48411.00 million. The interest on loan advance increased in 2009 13.85%,which was 13.80% in 2008.

Loan and Advance Position of DBBL:

Amount (TK. in Million)

| Year | DBBL | BRAC BANK |

| 2009 | 48411.00 | 32461.10 |

| 2008 | 41698.32 | 19557.17 |

| 2007 | 28369.58 | 11791.31 |

| 2006 | 28325.34 | 5819.79 |

| 2005 | 11431.32 | 2870.11 |

From the above table and figure we can say that, customers have a response to the loans & advances department of DBBL. So the position of this department is very good. Loans and Advances of the Bank stood at Tk.48411.00.million as on 31ST Dec 2009 againstTk.41698.32 million as on 31st Dec 2008, showing an increase growth rate.

Loans and advances are the core asset of a Bank. The Bank gives emphasis to acquire quality assets and does appropriate lending risk analysis while improving commercial and trade loans to clients

Mode of Advances:

PROFIT AND OPERATING RESULTS

In year 2008 a growth in operating profit of the bank was Tk.7275.75 million and in 2009 the profit reached to 8914.28 million which is more than Tk 1638.53 million than the previous year.

INVESTMENT

At the end of 2009 investment of DBBL is Tk 1137.70 million, which was Tk 821.62 million. Out of total investment Tk 5887.32 (99.63% of total investment) is concentrated in Govt. Treasury bills and bonds to maintain CRR and SLR of the bank comfortably and use to our surplus fund in a cost effective means. Income from Treasury bills increased 10% to 11.30% in 2009. DBBL invest in over night market, which was Tk 560.00million in 2008 and in 2009 it is Tk 2050.00 million.

Investment Activities of DBBL:

Amount (Tk In Million)

SWIFT SERVICES

The SWIFT services helped the bank in sending and receiving the messages and instructions related to our NOSTRO account operations and L/C related matters. We have brought most of our Branches under SWIFT network. Other Branches will come under the network hopefully by the year 2008. SWIFT: DBBL BD DH

FUNCTIONS OF DBBL

• To maintain all types of deposit A/Cs.

• To make investment.

• To conduct foreign exchange business.

• To conduct other Banking services.

• To conduct social welfare activities.

• To work for continues business innovation and improvements.

VALUES OF DBBL

To be one DBBL by holding and guiding the following values:

To have a strong customer focus and to build relationship based on integrity, superior service and mutual benefit.

To strive for private and sound growth.

To work as a team to serve the best interests of the organization.

To work for continues business innovation and improvements.

OPERATIONAL BRANCHES OF DBBL

DHAKA

HEAD OFFICE

LOCAL OFFICE

BANANI BRANCH

NABABPUR BRANCH

MOTIJHEEL (FOREIGN EXCHANGE) BRANCH

KAWRAN BAZAR BRANCH

SHANTINAGAR BRANCH

UTTARA BRANCH

DHANMONDI BRANCH

MIRPURBRANCH

MOHAKHALIBRANCH

GULSHANBRANCH

DANIA BRANCH

DHAKA EPZ BRANCH

BOARDBAZAR BRANCH

ELEPHANTROAD BRANCH

JOYPARA BRANCH

NAYABAZAR BRANCH

SAVARBAZAR BRANCH

GAZIPUR CHOWRASTA BRANCH

IMAMGONJ BRANCH

BASHUNDHARA BRANCH

MANIKGONJ BRANCH

Narayangonj

NARAYANGONJ BRANCH

B.B.ROAD BRANCH

NETAIGONJ BRANCH

SHIMRAIL BRANCH

Narsingdi

BABURHAT BRANCH

Comilla

COMILLA BRANCH

Chittagong

AGRABAD BRANCH

PATHERHAT BRANCH

HATHAZARI BRANCH

CDA AVENUE BRANCH

KADAMTOLI BRANCH

COX’SBAZAR BRANCH

LOHAGARA BRANCH

Sylhet

SYLHETBRANCH

BISWANATH BRANCH

MOULVIBAZAR BRANCH

GOLAPGONJ BRANCH

Khulna

KHULNA BRANCH

Bogra

BOGRA BRANCH

Barisal

BARISAL BRANCH

Rajshahi

RAJSHAHI BRANCH

Feni

FENI BRANCH

Tangail

MIRZAPUR BRANCH

Management of DBBL:

For any financial and non-financial organization, Management is the most valuable and important resources of any kind of organization. And, a well-organize management provides the organization to reach its ultimate goal. Management means planning, organizing, staffing, directing and controlling of all financial and non-financial resources of an organization. Different aspects of management practice in DBBL are discussed below.

• Planning:

DBBL has done its planning within the purview of the corporate plan. The overall planning approach in DBBL is top-down. Each branch can plan according to the goal imposed by the corporate level. It doesn’t plan independently. And, DBBL has a planning division. This department is mainly responsible for the overall planning.

• Organizing:

DBBL is organized as per the existing business locations. It has nineteen branches, each of which is a separate entity. Each unit is responsible for own performance and a Senior Vice President (SVP) followed by Manager heads each. He is directly responsible for the performance of their unit. Within each branch it is organized functionally.

• Staffing:

The recruitment in DBBL is done in two ways. One as a “Probationary Officer” for the management program and it has a probation period of one year. Another one is non- management level as “Trainee Officers”. Probationary Officer is recruited in officer category and their career path is headed towards different managerial jobs.

• Directing and controlling:

The management approach in DBBL is top-down or authoritative. Information just seeks through lower management layer. Works are designed in such a way that one cannot leave without clearing the tasks as he is assigned for a day. Sitting arrangement in all office is done in a way that the superior can monitor the subordinate all time. Budgeting, rewarding, punishing, etc. are also practiced as control mechanism.

Human Resources Practices in DBBL:

Employees are the core resources of any organization. Without them, one cannot run their organization. And, human resources approach is concerned with the growth and development of people toward higher level of competency, creativity and fulfillment. It helps employees become better, more responsible persons, and then it tries to create a climate in which they may contribute to the limits of their improved abilities. It assumes that expanded capabilities and opportunities for people will lead directly to improvements in operating effectiveness. Essentially, the human resources approach means that better people achieve better results.

CHEPTAR-3

o COMMERCIAL BANKING

Account Opening

Deposit Section

Cash Section

Local Remittance

Clearing Section

Accounting Section

CHAPTER-3

COMMERCIAL BANKING

Commercial banking department is the heart of all banking activities. This is the busiest and important department of a branch, because funds are mobilized, cash transactions are made; clearing, remittance and accounting activities are done here.

Since bank is confined to provide the services everyday, commercial banking is also known as ‘retail banking’. In DBBL Principal Branch, the following departments are under general banking section:

o Account opening section

o Deposit section

o Cash section

o Remittance section

o Clearing section

o Accounts section

ACCOUNT OPENING SECTION:

Account opening is the gateway for clients to enter into business with bank. It is the foundation of banker customer relationship. This is one of the most important sections of a branch, because by opening accounts bank mobilizes funds for investment. Various rules and regulations are maintained and various documents are taken while opening an account. A customer can open different types of accounts through this department. Such as:

o Current account.

o Savings (SB) account.

o Short Term Deposit (STD)

Types of Accounts with Terms and Conditions

Current Account:

Current account is purely a demand deposit account. There is no restriction on withdrawing money from the account. It is basically justified when funds are to be collected and money is to be paid at frequent interval.

Some Important Points are as follows-

Minimum opening deposit of TK.2000/- is required;

There is no withdrawal limit.

No interest is given upon the deposited money;

Minimum Tk.1000/= balance must always maintain all the time;

Savings (SB) Account:

This deposit is primarily for small-scale savers. Hence, there is a restriction on withdrawals in a month. Heavy withdrawals are permitted only against prior notice. Some Important Points are as follows-

Minimum opening deposit of Tk.2000/= is required;

Minimum Tk. 1000/= balance must always maintain all the time;

Withdrawal amount should not be more than 1/4th of the total balance at a time and limit twice in a month.

If withdrawal amount exceed 1/4th of the total balance at a time no interest is given upon the deposited money for that month.

Proprietorship account:

Attested copy of valid Trade license

attested copy of passport of the proprietor

Company seal and Tin certificate

Partnership account:

Partnership letter.

Copy of notarized partnership deed certified by all partners or registered partnership deed of join stock companies and firms duly certified by the register of join stock companies and firms.

Partnership Resolution signed by all the partners to open account with DBBL indicating type of account and mode of operation.

Club / societies account:

Certified copy of registration Certificate

Certified copy charter /Bye laws and regulation/Constitution of the relevant organization.

Copy resolution of managing committee/Executive committee for opening account with DBBL and operation of account-duty certified by chairmen /secretary.

List of members of the managing committee /Executive committee- duty certified by chairmen /secretary.

Private /public limited company account:

Memorandum and articles of association duly certified by the register of join stock companies and firms.

Certificate of incorporation duly certified by the register of join stock companies and firms.

Board resolution duly certified by the Chairman/Sectary of the company.

Form XII and schedule X duly certified by the register of join stock companies and firms.

Certificate of commencement of business duly certified by the register of join stock companies and firms.

Non-Govt. School/College/University/Madrasa/Muktab:

Certified copy of Registration certificate.

Copy resolution of managing committee/Executive committee for opening account with DBBL and operation of account-duty certified by chairmen /secretary.

List of members of the managing committee /Executive committee- duty certified by a Gazette officer.

Sector Corporation:

• Certified by relevant Presidential order/ Act of Parliament establishing the corporation.

• Resolution of board of directors /competent authority to open account with DBBL.

• Certified list of Board of Directors.

DEPOSIT SECTION

Deposit is the lifeblood of a bank. From the history and origin of the banking system we know that deposit collection is the main function of a bank.

Accepting deposits:

The deposits that are accepted by DBBL like other banks may be classified in to,—

o Demand Deposits

o Time Deposits

Demand deposits:

These deposits are withdrawn able without notice, e.g. current deposits. DBBL accepts demand deposits through the opening of,-

current account

Savings account

Call deposits from the fellow bankers

Time deposits:

A deposit which is payable at a fixed date or after a period of notice is a time deposit. DBBL accepts time deposits through Fixed Deposit Receipt (FDR), Short Term Deposit (STD) and Bearer Certificate Deposit (BCD) etc.

While accepting these deposits, a contract is done between the bank and the customer. When the banker opens an account in the name of a customer, there arises a contract between the two. This contract will be valid one only when both the parties are competent to enter into contracts. As account opening initiates the fundamental relationship & since the banker has to deal with different kinds of persons with different legal status, DBBL officials remain very much careful about the competency of the customers.

CASH SECTION:

Banks, as a financial institution, accept surplus money from the people as deposit and give them opportunity to withdraw the same by cheque, etc. But among the banking activities, cash department play an important role. It does the main function of a commercial bank i.e. receiving the deposit and paying the cash on demand. As this department deals directly with the customers, the reputation of the bank depends much on it. The functions of a cash department are described bellow:

Functions of Cash Department:

Cash Payment Cash payment is made only against cheque

This is the unique function of the banking system which is known as “payment on demand”

It makes payment only against its printed valid Cheque

Cash Receipt It receives deposits from the depositors in form of cash

So it is the “mobilization unit” of the banking system

It collects money only its receipts forms

Cash packing:

After the banking hour cash is packed according to the denomination. Notes are counted and packed in bundles and stamped with initial.

Allocation of currency:

Before starting the banking hour all tellers give requisition of money through “Teller cash proof sheet”. The head teller writes the number of the packet denomination wise in “Reserve sheet” at the end of the day, all the notes remained are recorded in the sheet.

LOCAL REMITTANCE

Carrying cash money is troublesome and risky. That’s why money can be transferred from one place to another through banking channel. This is called remittance. Remittances of funds are one of the most important aspects of the Commercial Banks in rendering services to its customers.

Types of remittance:

Between banks and non banks customer

Between banks in the same country

Between banks in the different centers.

Between banks and central bank in the same country

The main instruments used by the DBBL of remittance of funds are

Payment order ( PO)

Demand Draft ( DD)

Telegraphic Transfer (TT)

So the basic three types of local remittances are discussed below:

| Points | Pay Order | Demand Draft | TT |

| Explanation | Pay Order gives the payee the right to claim payment from the issuing bank | Demand Draft is an order of issuing bank on another branch of the same bank to pay specified sum of money to payee on demand. | Issuing branch requests another branch to pay specified money to the specific payee on demand by Telegraph /Telephone |

| Payment from | Payment from issuing branch only | Payment from ordered branch | Payment from ordered branch |

| Generally used to Remit fund | Within the clearinghouse area of issuing branch. | Outside the clearinghouse area of issuing branch. Payee can also be the purchaser. | Anywhere in the country |

| Payment Process of the paying bank | Payment is made through clearing | Confirm that the DD is not forged one.2.Confirm with sent advice 3.Check the ‘Test Code’ 4.Make payment | 1.Confirm issuing branch2.Confirm Payee A/C 3.Confirm amount 4.Make payment 5.Receive advice |

| Charge | Only commission | Commission + telex charge | Commission +Telephone |

Payment of interest: It is usually paid on maturity of the fixed deposit. DBBL calculates interest at each maturity date and provision is made on that “miscellaneous creditor expenditure payable accounts” is debited for the accrued interest.

Encashment of FDR: In case of premature FDR< DBBL is not bound to accept surrender of the deposit before its maturity date. In order to deter such a tendency the interest on such a fixed deposit is made cut a certain percentage less the agreed rate. Normally savings bank deposit is allowed.

Loss of FDR: In case of lost of FDR the customer is asked to record a GD (general diary) in the nearest police station. After that the customer has to furnish an Indemnity Bond to DBBL a duplicate FDR is then issued to the customer by the bank.

CLEARING SECTION

The amount of Cheques, Pay Order (P.O), and Demand Draft (D.D.) Collection of amount of other banks on behalf of its customer is a basic function of a Clearing Department.

Clearing:

Clearing is a system by which a bank can collect customers fund from one bank to another through clearing house.

Clearing House:

Clearing House is a place where the representatives of different banks get together to receive and deliver cheque with another banks.

Normally, Bangladesh Bank performs the Clearing House in Dhaka, Chittagong, Rajshahi, and Khulna & Bogra. Where there is no branch of Bangladesh Bank, Sonali bank arranges this function.

Member of Clearing House:

DBBL. is a scheduled Bank. According to the Article 37(2) of Bangladesh Bank Order, 1972, the banks, which are the member of the clearinghouse, are called as Scheduled Banks. The scheduled banks clear the cheque drawn upon one another through the clearinghouse.

Types of Clearing:

Outward Clearing: When the Branches of a Bank receive cheque from its customers drawn on the other Banks within the local clearing zone for collection through Clearing House, it is Outward Clearing.

Inward Clearing: When the Banks receive cheque drawn on them from other Banks in the Clearing House, it is Inward Clearing.

Types of clearing house:

There are two type of clearing house: Those are

Normal clearing house

Same day clearing house

Normal clearing house:

1st house: 1st house normally stands at 10 a.m. to 11a.m

2nd house: 2nd house normally stands after 3 p.m. and it is known as return house.

Same day clearing house:

1st house: 1st house normally stands at 11 a.m. to 12 p.m

2) 2nd house: 2nd house normally stands after 2 p.m. and it is known as return house.

Who will deposit cheque for Clearing: Only the regular customers i.e. who have Savings, Current, STD & Loan Account in the bank can deposit cheque for collection of fund through clearing house.

Precaution at the time of cheque receiving for Clearing, Collection of LBC, OBC & Transfer:

Return house:

Return House means 2nd house where the representatives of the Bank meet after 3 p.m. to receive and deliver dishonored cheque, which placed in the 1st Clearing House.

Cheque may be dishonored for any one of the following reasons:

Insufficient fund.

Amount in figure and word differs.

Cheque out of date/ post- dated.

Payment stopped by the drawer.

………….Payee’s endorsement irregular / illegible / required.

Drawer’s signature differs / required.

Crossed cheque to be presented through a bank.

Responsibility of the concerned officer for the Clearing Cheque:

Crossing of the cheque.

(Computer) posting of the cheque.

Clearing seal & proper endorsement of the cheque.

Separation of cheque from deposit slip.

Sorting of cheque 1st bank wise and then on branch wise.

Computer print 1st branch wise & then bank wise.

Preparation of 1st Clearing House computer validation sheet.

ACCOUNTS SECTION

Bills Collection:

In modern banking the mechanism has become complex as far as smooth transaction and safety is concerned. Customer does pay and receive bill from their counterpart as a result of transaction. Commercial bank’s duty is to collect bills on behalf of their customer.

Types of Bills for Collection

Outward Bills for Collection (OBC).

Inward Bills for Collection (IBC).

Outward Bills for Collection (OBC)

OBC means Outward Bills for Collection .OBC exists with different branches of different banks outside the local clearing house. Normally two types of OBC:

o OBC with different branches of other banks

o OBC with different branches of the same bank

Procedure of OBC:

Entry in the OBC register.

Put OBC number in the cheque.

“Crossing seal” on the left corner of the cheque & “payees account will be credited on realization “seal on the back of the cheque with signature of the concerned officer.

Despatch the OBC cheque with forwarding.

Reserve the photocopy of the cheque, carbon copy of the forwarding and deposit slip of the cheque in the OBC file.

Commission for collection:

Up to 1 lac ———————————————- 0.15%

Above 1 lac———————————————- 0.10%

Above 5lac ———————————————- 0.05%

Inward bills for collection (IBC)

When the banks collect bills as an agent of the collecting branch, the system is known as IBC. In this case the bank will work as an agent of the collection bank. The branch receives a forwarding letter and the bill.

CHEPTER-4

o FOREIGN EXCHANGE OPERATIONS

Name of Exchange

Import

Export

Foreign Remittance

CHAPTER-4

FOREIGN EXCHANGE

OPERATION:

Name of the Exchange Companies and Banks

| Sl No. | Name of Exchange House | Service Available | Presence |

| 01 | UAE Exchange Centre LLC | Taka Draft ArrangementXpress Money (Agent network) TT Arrangement | Global |

| 02 | Al Ahalia Money Exchange Bureau | TT Arrangement.Taka Draft Arrangement | UAE |

| 03 | Dollarco Exchange Co. | TT Arrangement.Taka Draft Arrangement | Kuwait |

| 04 | Kuwait Asian International Exchange Co. | TT Arrangement.Taka Draft Arrangement | Kuwait |

| 05 | East Bengal Exchange Inc. | TT Arrangement. | Canada |

| 06 | Janata Express Corporation | TT Arrangement. | USA |

| 07 | Western Union Services Singapore Pte Ltd. | Instant Cash Payment. | Global |

| 08 | Wall Street Finance L.L.C | EFT Arrangement | USA |

| 09 | Choice Money Transfer | EFT Arrangement | USA |

FOREIGN EXCHANGE STEPS

Foreign exchange is the means and methods by which rights to wealth in a country’s currency are converted into rights to wealth in another country’s currency. In banks when we talk of foreign exchange, we refer to the general mechanism by which a bank converts currency of one country into that of another. Foreign Exchange Department (FED) is the international department Bangladesh Bank issues license to scheduled banks to deal with foreign exchange. These banks are known as Authorized Dealers. If the branch is authorized dealer in foreign exchange market, it can remit foreign exchange from local country to foreign countries. So DBBL, Principal branch is an authorized dealer.

There are three kinds of foreign exchange transaction:

- Import

- Export

- Remittance.

IMPORT:

To import, a person should be competent to be and importer’. According to Import and Export Control Act, 1950, the Office of Chief Controller of Import and Export provides the registration (IRC) to the importer. In an international business environment, buyers and sellers are generally unknown to each other. So seller of goods always seeks security for the payment of his exported goods. Bank gives export guarantee that it will pay for the goods on behalf of the buyer if the buyer does not pay. This guarantee is called Letter of Credit. Thus the contract between importer and exporter is given a legal shape by the banker by ‘Letter of Credit’

.Import Finance

DBBL extends finance to the importers in the form of:

- Opening of Import L/C

- Credit against Trust Receipt for retirement of import bills.

- Short term & medium term loans for installation of imported machineries & production thereof.

- Payment against document

Letter of Credit:

Definition:

A letter of credit is a letter issued by a bank (know as the opening or the issuing bank) at the instance of its customer (known as the opener) addressed to a person (beneficiary) undertaking that the bills drawn by the beneficiary will be duly honored by it (opening bank) provided certain conditions mentioned in the letter gave been complied with.

Parties to the L/C:

| Importer | Who applies for L/C |

| Issuing Bank | It is the bank which opens/issues a L/C on behalf of the importer. |

| Confirming Bank | It is the bank, which adds its confirmation to the credit and it, is done at the request of issuing bank. Confirming bank may or may not be advising bank. |

| Advising or Notifying Bank | It is the bank through which the L/C is advised to the exporters. This bank is actually situated in exporter’s country. It may also assume the role of confirming and / or negotiating bank depending upon the condition of the credit. |

| Negotiating Bank | It is the bank, which negotiates the bill and pays the amount of the beneficiary. The advising bank and the negotiating bank may or may not be the same. Sometimes it can also be confirming bank. |

| Accepting Bank | It is the bank on which the bill will be drawn (as per condition of the credit). Usually it is the issuing bank. |

| Reimbursing Bank | It is the bank, which would reimburse the negotiating bank after getting payment – instructions from issuing bank. |

Steps for import L/C Operation – 8 steps operation:

Step 1 – Registration with CCI&E:

- For engaging in international trade, every trader must be first registered with the Chief Controller of Import and Export.

- By paying specified registration fees to the CCI&E. the trader will get IRC/ERC (Import/Export Registration Certificate), to open L/C with bank, this IRC is must.

Step 2 – Determination terms of credit:

The terms of the letter of credit are depending upon the contract between the importer and exporter. The terms of the credit specify the amount of credit, name and address of the beneficiary and opener, tenor of the bill of exchange, period and mode of shipment and of destination, nature of credit, expiry date, name and number of sets of shipping documents etc.

Step 3 -Proposal for Opening of L/C:

To have an import LC limit an importer submits an application to department to DBBL. The proposal contains the following particulars:

- Full particulars of the bank account

- Nature of business

- Required amount of limit

- Payment terms and conditions

- Goods to be imported

- Offered security

- Repayment schedule

Step 4 – Application by importer to the banker to open letter of credit:

For opening L/C, the importer is required to fill up a prescribed application form provided by the banker along with the following documents:

| 1. L/C Application form | 7. Authority to debit account |

| 2. Filled up LCA form | 8. Filled up amendment request Form |

| 3. Demand Promissory Note | 9. IMP form |

| 4. pro-forma invoice | 10. Insurance cover note and money receipt. |

| 5. Tax Identification number | 11. Membership certificate |

| 6.Import registration certificate | 12. Rate fluctuation undertaking |

Step 5 – Opening of L/C by the bank for the opener:

- Taking filled up application form from the importer.

- Collects credit report of exporter from exporter’s country through his foreign correspondence there.

Step 6 – Shipment of goods and lodgment of documents by exporter:

- Then exporter ships the goods to the destination of the importer country

- Sends the documents to the L/C opening bank through his negotiating bank. Generally the following documents are sent to the Opening Banker with L/C:

Step 7 – Lodgment of Documents by the opening Bank from the negotiating bank:

After receiving the documents, the opening banker scrutinizes the documents. If any discrepancy found, it informs the importer. If importer accepts the fault, then opening bankers call importer retiring the document. At this time many thing can happen. These are indicated in the following:

- Discrepancy found but the importer accepts – no problem occurs in lodgment.

- Discrepancy found and importer not agreed to accept – In this case, importer protest and send back all the documents to the exporter and request his to make in the specified manner. Here banker is not bound to pay because the documents send by exporter is not in accordance with the terms of L/C.

- Everything is O.K. but importer fails to clear goods from the port and request bank to clear – In this case banks clear the goods and takes delivery of the same by paying customs duty and sales tax etc. So, this expenditure is debited to the importer’s account and in banking it is called LIM.

Step 8 – Retirement:

The importer receives the intimation and gives necessary instruction to the bank for retirement of the import bills or for the disposal of the shipping document to clear the imported goods from the customs authority. The importer may instruct the bank to retire the documents by debiting his account with the bank or may ask for LTR (Loan against Trust Receipt).

Accounting Procedure in case of L/C Opening:

When the officer thinks fit the application to open a L/C, giving the following entries- creates the following charges-

| Particulars | Debit/ Credit | Charges in Taka |

| Customer’s A/C | Debit | |

| L/C Margin A/C | Credit | |

| Commission A/C on L/C | Credit | 50% |

| VAT | Credit | 15% on commission |

| SWIFT Charge | Credit | 3000/= |

| Datamax | Credit | 1000/= |

| Stamp | Credit | 300/= |

| Postage | Credit | 300/= |

| DHL/Courier | Credit | 1500 |

Amendment of L/C:

After opening of L/C some time’s alteration to the original terms and conditions become necessary. These amendments involve changes in

- Unit price

- Extension of validity o the L/C

- Documentary requirements etc.

Such amendments can be affected only if all the concerned parties agree i.e. the beneficiary, the importer, the issuing bank and the advising bank.

For any amendment the importer must request the issuing bank in writing duly supported by revised indent/ Performa invoice. The issuing bank then advises the required amendment to the advising bank. L/C amendment commission including postage is charged to the clients A/C.

Loan against Trust Receipts (LTR):

- § Advance against a Trust Receipt obtained from the Customers are allowed to only first class tested parties when the documents covering an import shipment or other goods pledged to the Bank as security are given without payment. However, for such advances prior permission/sanction from Head Office must be obtained.

The customer holds the goods or their sale-proceeds in trust for the Bank, till such time, the loan allowed against the Trust Receipts is fully paid off.

The Trust Receipt is a document that creates the Banker’s lien on the goods and practically amounts to hypothecation of the proceeds of sale in discharge of the lien.

Payment Procedure of Import Documents:

This is the most sensitive task of the Import Department. The officials have to be very much careful while making payment. This task constitutes the following:

|

|

Date of Payment:

Usually payment is made within seven days after the documents have been received. If the payment is become deferred, the negotiating bank may claim interest for making delay.

Preparing Sale Memo:

A sale memo is made at B.C rate to the customer. As the T.T & O.D rate is paid to the ID, the difference between these two rates is exchange trading. Finally, an Inter Branch Exchange Trading Credit Advice is sent to ID.

Requisition for the Foreign Currency:

For arranging necessary fund for payment, a requisition is sent to the International Department.

Transmission of Message:

Message is transmitted to the correspondent bank ensuring that payment is being made.

EXPORT

Understanding:

The goods and services sold by Bangladesh to foreign households, businessmen and Government are called export. The export trade of the country is regulated by the Imports and Exports (control) Act, 1950. There are a number of formalities, which an exporter has to fulfill before and after shipment of goods. The exports from Bangladesh are subject to export trade control exercised by the Ministry Of Commerce through Chief Controller of Imports and Exports (CCI & E). No exporter is allowed to export any commodity permissible for export from Bangladesh unless he is registered with CCI & E and holds valid Export Registration Certificate (ERC). The ERC is required to be renewed every year. The ERC number is to be incorporated on EXP forms and other documents connected with exports.

Export Finance

Pre-Shipment Finance

- Pre-Shipment finance in the form of:

- Opening of Back-to-Back L/C

- Export Cash Credit

Post-Shipment Finance

- Post-Shipment finance in the form of:

- Foreign/Local Documentary Bills Purchase

- Export Credit Guarantee

- Finance against cash incentive

The formalities and procedure are enumerated as follows:

- Obtaining exports LC: To get export LC form exporter issued by the importer.

- Submission of export documents: Exporter has to submit all necessary documents to the collecting bank after shipping of goods

- Checking of export documents: After getting the documents banker used to check the documents as per LC terms.

- Negotiation of export documents: If the bank accepts the document and pays the value draft to the exporter and forward the document to issuing bank that is called a negotiating bank. If the bank does buy the LC then the bank normally acts as collecting bank.

- Realization of proceeds: This is the period when the issuing bank has realized the payment.

Export operation:

Bangladesh exports a large quantity of goods and services to foreign households. Readymade textile garments (both knitted and woven), Jute, Jute-made products, frozen shrimps, tea are the main goods that Bangladeshi exporters exports to foreign countries. Garments sector is the largest sector that exports the lion share of the country’s export. Bangladesh exports most of its readymade garments products to U.S.A and European Community (EC) countries. Bangladesh exports about 40% of its readymade garments products to U.S.A. Most of the exporters who export through DBBL are readymade garment exporters. They open export L/Cs

Here to export their goods, which they open against the import L/Cs opened by their foreign importers.

Export L/C operation is just reverse of the import L/C operation. For exporting goods by the local exporter, bank may act as advising banks and collecting bank (negotiable bank) for the exporter.

As an advising bank:

It receives documents from the foreign importer and hands it over to the exporter. Sometimes it adds confirmation on the L/C on request from the Opening Bank. By adding confirmation, it assumes the responsibility to make payment to the exporter.

As Negotiating Bank:

It negotiates the bills and other shipping documents in favor of the exporter. That is, it collects the proceeds of the export-bill from the drawee and credits the exporter’s account for the same. Collection proceed from the export bill is deposited in the bank’s NOSTRO account in the importer’s country. Sometimes the bank purchases the bills at discount and waits till maturity of the bill. When the bill matures, bank presents it to the drawee to encash it.

In our country, Export and Import operation of bank is very much related with one another because of use of Back to Back and maturity of payment for Back-to-Back L/C is set in such that it can be paid out of export proceeds. .

Back-To-Back L/C:

It is simply issued to the clients against an import L/C. Back-to-Back mechanism involves two separates L/Cs. One is master Export L/C and another is Back-to-Back L/C. On the strength of Master Export L/C bank issues bank to Back L/C. Back-to-Back L/C is commonly known as Buying L/C. On the contrary, Master Export L/C is known as Selling L/C.

Features of Back-to-Back L/C:

- An Import L/C to procure goods /raw materials for further processing.

- It is opened based on Export L/C.

- It is a kind of Export Finance.

- Export L/C is at Sight but back to Back L/C is at Usance.

- No margin is required to open Back to back L/C

- Application is registered with CCI&E

- Applicant has bonded warehouse license.

- L/C value shall not exceed the admissible percentage of net FOB value of relative Master L/C.

- Usance period will be up to 180 days.

Documents Required for Opening a Back-to-back L/C:

- In DBBL Principal Branch, following papers/ documents are required for opening a back-to-back L/C-

- Master L/C

- Valid Import Registration Certificate (IRC) and Export Registration Certificate (ERC)

- L/C Application and LCAF duly filled in and signed

- Proforma Invoice or Indent

- Insurance Cover Note with money receipt

- IMP Form duly signed

- In addition to the above documents, the followings are also required to export oriented garment industries while requesting for opening a back-to-back L/C –

- Textile Permission

- Valid Bonded Warehouse License

- Quota Allocation Letter issued by the Export Promotion Bureau (EPB) in 2.

Checklist of exports L/C:

Following defective points are usually found in the Master L/C. So, the bank officials so much carefully check these points. These are:

- Name of the Advising Bank.

- Name of Transferring Bank

- Form of Doc. credit:

- Name of Issuing Bank

- Documentary Credit No. and issuing date

- Date of shipment

- Expiry date and place

- Applicant/ for order of/ On Account.

- Beneficiary/ Favoring

- Amount

- Availability of Credit

- Partial shipment/ Transshipment

- Payment condition /Draft Sight

- Category.

- Description of goods:

- Item

- Total Qty

- Unit price

- B/L Clause

- Reimbursement clause.

Payment of back-to-back L/C:

In case back to back as 60-90-120-180 days of maturity period, deferred payment is made. Payment is given after realizing export proceeds from the L/C issuing bank.

L/C under EDF:

Exporter development Fund is created by Bangladesh Bank to give encourages to the exporter in Bangladesh.

Generally Back-to-Back L/C is Usance L/C that is here bill of exchange is payable after some maturity date say 90 or 120 days after the date of acceptance/negotiation. But some foreign seller may require sight payment. Here import L/C matures first. In that case Bangladesh Bank gives the fund to the bank to pay the price of imported goods in favor of the local

purchaser of raw materials. When export proceeds come, first Bangladesh Bank loan to the importer is adjusted and remaining part goes to the importer of raw materials.

Negotiation of exports documents:

The most common method of financing exporters is negotiation of documents under L/C. It is a post-shipment credit. Here the bank acts as a negotiating bank. After the shipment of the goods, the exporter submits the relative documents to the branch for negotiation. The documents are to submit within the period mentioned in the L/C. after approval of negotiation of the bill the full particulars of the documents are entered into the Foreign bill Purchased (F.B.P) register. The documents are sent to the L/C opening branch with a forwarding letter. The branch claim reimbursement from the issuing bank or from the reimbursing bank, giving clear instructions to credit the proceeds of the bill to the DBBL head office NOSTRO A/C maintained with the named correspondent bank abroad under telex intimation to the Principal branch and Head Office (International Division).

Presentation of export documents for negotiation/Purchase:

After shipment, exporter submits the following documents to DBBL for negotiation.

- Bill of exchange

- Bill of Lading

- Invoice

- Insurance Policy/Certificate

- Certificate of Origin

- Inspection Certificate

- Consular Invoice

- Packing List

Foreign documentary bills for collection (FDBC)

DBBL forwards the documents for collection due to the following reasons,-

- If the documents have discrepancies.

- If the exporter is a new client.

FDBC signifies that the exporter will receive payment only when the issuing bank gives payment. DBBL make regular follow-up with the L/C opening Bank in case of any delay in getting payment.

Settlement of Local Bills:

- The settlement of local bills is done in the following ways, –

- The customer submits the L/C to DBBL along with the documents to negotiate

- DBBL official scrutinizes the documents to ensure the conformity with the terms and conditions.

- The documents are then forwarded to the L/C opening bank.

- The L/C issuing bank gives the acceptance and forwards an acceptance letter.

- Payment is given to the customer on either by collection basis or by purchasing the document.

Deferred payment Credit:

In deferred payment, the bank agrees to pay on a specified future date or event, after presentation of the export documents. No bill of exchange is involved. Payment is given to the party at the rate of D.A 60-90-120-180 as the case may be. But the Head office is paid at T.T clean rate. The difference between the two rates us the exchange trading for the branch.

Acceptance credit:

In acceptance credit, the exporter presents a bill of exchange payable to himself and drawn at the agreed tenor (that is, on a specified future date or event) on the bank that is to accept it. The bank signs its acceptance on the bill and returns it to the exporter. The exporter can then represent it for payment on maturity. Alternatively he can discount it in order to obtain immediate payment.

Negotiation Credit:

In Negotiation credit, the exporter has to present a bill of exchange payable to him in addition to other documents that the bank negotiates.

FOREIGN REMITTANCE

This bank is authorized dealer to deal in foreign exchange business. As an authorized dealer, a bank must provide some services to the clients regarding foreign exchange and this department provides these services.

The basic function of this department are outward and inward remittance of foreign exchange from one country to another country. In the process of providing this remittance service, it sells and buys foreign currency. The conversion of one currency into another takes place at an agreed rate of exchange, which the banker quotes, one for buying and another for selling. In such transactions the foreign currencies are like any other commodities offered for sales and purchase, the cost (convention value) being paid by the buyer in home currency, the legal tender

Remittance procedures of foreign currency:

There are two types of remittance:

- Inward remittance

- Outward remittance.

Inward Foreign Remittance:

Inward remittance covers purchase of foreign currency in the form of foreign T.T., D.D, and bills, T.C. etc. sent from abroad favoring a beneficiary in Bangladesh. Purchase of foreign exchange is to be reported to Exchange control Department of Bangladesh bank on Form-C.

Outward Foreign Remittance:

Outward remittance covers sales of foreign currency through issuing foreign T.T. Drafts, Travelers Check etc. as well as sell of foreign exchange under L/C and against import bills retired.

Working of this department:

- Issuance of TC, Cash Dollar /Pound

- Issuance of FDD, FTT & purchasing, Payment of the same.

- Passport endorsement.

- Encashment certificate.

- F/C Account opening &filing.

Modes:

The remittance process involves the following four modes:

| Cash RemittanceDollar/ Pound | Sell | Bank sells Dollar / Pound for using in abroad by the purchaser. The maximum amount of such sell is mentioned in the Bangladesh Bank publication of ‘Convertibility of Taka for Currency Transactions in Bangladesh’. |

| Purchase | Bank can purchase dollar from resident and non – resident Bangladeshi and Foreigner. Most dollars purchased comes from realization of Export Bill of Exchange. | |

| Traveler’s Cheque(TC) | Issue of TC | TC is useful to traveler abroad. Customers can encash the TC in abroad from the drawee bank. TC is alternative to holding cash and it provides better security than holding cash in hand. |

| BuyingOf TC | If any unused leaf of TC is surrendered bank buys it from the customer. All payments are made in local currency. Banks generally buy only those TC. | |

| Telex Transfer | Outward TT | It remits fund by tested TT via its foreign correspondence bank in which it is maintaining its NOSTRO Account. |

| Incoming TT | It also makes payment according to telegraphic message of its foreign correspondence bank from the corresponding VOSTRO Account. | |

| Foreign Demand Draft | Bank issue Demand Draft in favor of purchaser or any other according to instruction of purchaser. The payee can collect it for the drawee bank in which the Issuing bank of Demand Draft holds its NOSTRO Account. Bank also makes payment on DD drawn on this bank by its foreign correspondence bank through the VOSTRO Account. | |

Miscellaneous Services by This Department:

- Student File: Students who are desirous to study abroad can open file in the Bank. By opening this file, bank assures the remittance of funds in abroad for study.

- F.C Accounts: Foreign Currency Accounts opened in the names of Bangladeshi nationals or persons of Bangladeshi origin working or

selfemployed abroad can now are maintained as long as the account holders desires

Formalities for opening foreign currency (FC) Account:

The AD may without prior approval of the Bangladesh Bank open Foreign Currency

(FC) account in the name of:

- Bangladesh national residing abroad.

- Foreign nationals residing abroad/ in Bangladesh and also foreign firms

- Registered abroad and operating in Bangladesh and abstract foreign missions and their expatriate employees.

- Resident of Bangladesh nationals working with the foreign / international organization operating in Bangladesh provided their salary in paid in foreign currency.

Papers required:

Application duly billed in and signed.

- Photograph (two copies).

- Passport photocopy.

- Work permit from board investment. (In case of foreign nationals).

Rate of exchange:

It means the price of one currency expressed in terms of another currency. Rate of exchange is the rate by which the relation among different foreign currencies is established in terms of local currency of that country. Value at which one country currency can be converted into another’s country.

Spot rate:

It is quoted for transaction where the foreign currency bought or sold is to be received or delivered immediately. The current rate of exchange quoted in the foreign exchange market.

Forward rate: When a rate is applied to a future date it is called forward rate at which foreign exchange can be sold or bought for delivery at a future time.

Cross rate: The rate of exchange quoted expressing the quotation for any two currencies in term of a third.

SWAO: Sport rate against forward purchased or a spot purchase against forward rate.

Pence rate / direct quotation: Rates are quoted in term’s foreign currency per one unit of foreign currency.

Currency rate / indirect quotation: Rates are quoted in terms of foreign currency per one unit of home currency.

Buying rate: Authorized dealer applies this at the time of purchasing / negotiation of export document and payment against TT. MT, check and drafts required from abroad.

Selling rate: Authorized dealer applies this at the time of lodgment of import documents, realization of LC margin from importer and other foreign exchanges transaction on overseas bank.

Forward Rate at a discount: When forward rate is higher than that of spot rate.

Forward rate at a premium: When for ward rate is lower than that of spot rat

CHAPTER-5

- LOANS & INVESTMENT

Introduction

Lending Principles

Process of Investment

Types of Investment & Invest

Lending Authorities

Securities

SWOT Analysis

CHAPTER-5

LOANS & ADVANCES

This is the survival unit of the bank because until and unless the success of this department is attained, the survival is a question to every bank. If this section does not properly work the bank it may become bankrupt. This is important because this is the earning unit of the bank. Banks are accepting deposits from the depositors in condition of providing profit to them as well as safe keeping their profit. Now the question may gradually arise how the bank will provide profit to the clients and the simple answer is – Investments & Advance.

Why the bank provides Investment to the Borrowers?

- To earn profit from the borrowers and give the depositors profit.

- To accelerate economic development by providing different industrial as well as agricultural Investment.

- To create employment by providing industrial Investments.

- To pay the employees as well as meeting the profit groups.

Lending principles

The Principle of lending is a collection of certain accepted time tested standards, which ensure the proper use of Investment fund in a profitable way and its timely recovery. Different authors describe different principles for sound lending.S

- 1. Safety

- 2. Security

- 3. Liquidity

- 4. Adequate yield

- 5. Diversity

Process of Investment

| Heads | Characteristics |

| Application | Applicant applies for the Investment in the prescribed form of the bank describing the types and purpose of Investment. |

| Sanction |

|

| Documentation |

|

| Disbursement | An Investment Account is opened. Where customer A/C————————-Dr.Respective Investment A/C ——————————————–Cr. |

Types of Investments and Investment

The different types of Investments and Investment that DBBL offers are as follows:

- Secured Overdraft (SOD)

- Investment against Imported Merchandise (LIM)

- Investment against Trust Receipt (LTR)

- Payment Against Document (PAD)

- HouseBuilding Investment

- House Building Investment (staff)

Secured Overdraft (SOD):

It is a continue advance facility. By this agreement, the banker allows his customer to overdraft his current account up to his credit limits sanctioned by the bank. The profit is charged on the amount, which he withdraws, not on the sanctioned amount. DBBL sanctions SOD against different security.

SOD (general):

Advance allowed to individual/ firms against financial obligation (i.e. lien on FDR/PSP/BSP/ insurance policy share etc.) This may or may not be a continuous Credit.

SOD (others):

Investment allowed against assignment of work order or execution of contractual works falls under this head. This advance is generally allowed for a definite period and specific purpose i.e. it is not a continuous credit. It falls under the category “others”

LIM (Investment against Imported Merchandise):

Investment allowed for retirement of shipping documents and release of goods imported through L/C taking effective control over the goods by pledge in go downs under Banks lock & key fall under this type of advance. This is also a temporary advance connected with import, which is known as post‑import financing, falls under the category “commercial lending”.

LTR (Investment against trust receipt):

Advance allowed for retirement of shipping documents, release of goods imported through L/C falls under trust with the arrangement that sale proceed should be deposited to liquidate within a given period. This is also a temporary advance connected with import, which is known as post‑import financing, falls under the category “commercial lending”.

PAD (payment against document):

Payment made by the Bank against lodgment of shipping documents of goods imported through L/C falls under this head. It is an interim advance connected with import and is generally liquidated against payments usually made by the party for retirement of the documents for release of imported goods from the customer’s authority. It falls under the category “commercial Bank”.

House building Investment (General):

Investments allowed to individual/ enterprise construction of house (residential or commercial) fall under this of advance. The amount is repayable by monthly installment within a specified period, Investment is known as Investment (HBL‑GEN).

Collateral:

The land and the construction on the land are normally given as collateral. It may changes: –

- The documents to be obtained:

- DP note.

- Letter of disbursement

- Letter of installment.

- Letter of guarantee.

- Letter of under taking.

- Letter of agreement.

- Irrevocable general power of attorney.

- Memorandum of deposit of title deed.

- Any other documents if considered

House building Investments (staff):

Investments allowed to the Bank employees for purchase/construction of house shall be known as Staff Investment (HBFC‑STAFF).

Term Investment:

DBBL considers the Investments, which are sanctioned for more than one year as term Investment. Under this facility, an enterprise is financed from the starting to its finishing, i.e. from installation to its production.

Investment (general):

Short term and long term Investments allowed to individual/ firms / industries for a specific purpose but a definite period and generally repayable by the installments fall under this head. These types of lending are mainly allowed to accommodate financing under the categories.

Bank guarantee:

The bank is very often requested by his customer to issue guarantees on their behalf to a third party – committing to make an unconditional payment of certain amount of money to the third party, if the customer (on whose behalf it gives guarantee) becomes liable, or creates any loss or damage to the third party.

Export cash credit (ECC):

Financial accommodation allowed to customer for exports of goods falls under this head is categorized as “Export Credit “. The Investment must be liquidated out of export proceeds within 180 days.

Cash Credit (Hypothecation)

The mortgage of movable property for securing Investment is called hypothecation. Hypothecation is a legal transaction whereby goods are made available to the lending banker as security for a debt without transferring either the property in the goods or either possession. The banker has only equitable charge on stocks, which practically means nothing. Since the goods always remain in the physical possession of the borrower, there is much risk to the bank. So, it is granted to parties of undoubted means with the highest integrity.

The formalities for Opening cash credit:

The intending cash credit holder should submit the nd being fulfill properly:

- Stock report, Rent receipt.

- Trade license.

- Up to date income tax clearing certificate.

- Charge documents

- Letter of continuity

- Letter of arrangement

- DP (Demand promissory) note.

- Letter of guarantee.

- Letter lien.

- Limit sanctions advice.

LENDING AUTHORITY

As sure proper and orderly conduct of the business of the Bank, the Board of Directors’ will empower the Managing Director and other Executives of the Bank to lend up certain amount under certain terms and conditions at their discretion. The lending officer is broadly categorized as follows:

- Managing Director

- Deputy Managing Director

- Executive vice President asstt.

- Senior vice President

- Vice President

- Senior asstt. Vice President

- Asst. vice President.

SECURITIES

To make the Investment secured, charging sufficient security on the credit facilities is very important. The banker cannot afford to take the risk of non-recovery of the money lent. DBBL charges the following two types of security,

Primary security: These are the security taken by the ownership of the items for which bank provides the facility.

Collateral security: Collateral securities refer to the securities deposited by the third party to secure the advance for the borrower in narrow sense. In wider sense, it denotes any type of security on which the bank has a personal right of action on the debtor in respect of the advance.

MODES OF CHARGING SECURITY

There are different modes of charging the bank exercises security:

PLEDGE

Pledge is the bailment of the goods as security for payment of a debt or performance of a promise. A pledge may be in respect of goods including stocks and share as well as documents of title to goods such as railway receipt, bills of lading, dock warrants etc. duly endorsed in bank’s favor.

HYPOTHECATION

In case of hypothecation the possession and the ownership of the goods both rest the borrower. The borrower to the banker creates an equitable charge on the security. The borrower does this by executing a document known as Agreement of Hypothecation in favor of the lending bank.

LIEN

Lien is the right of the banker to retain the goods of the borrower until the Investment is repaid. The bankers’ lien is general lien. A banker can retain all securities in his possession till all claims against the concern person are satisfied.

MORTGAGE

According to section (58) of the Transfer of Property Act,1882 mortgage is the ‘’transfer of an profit in specific immovable property for the purpose of securing the payment of money advanced or to be advanced by way of Investment, existing or future debt or the performance of an engagement which may give rise to a pecuniary liability”. In this case the mortgagor dose not transfer the ownership of the specific immovable property to the mortgagee only transfers some of his rights as an owner. The banker exercises the equitable mortgage.

CREDIT DISBURSEMENT

Having completely and accurately prepared the necessary Investment documents, the Investment officer ready to disburse the Investment to the borrower’s Investment account. After disbursement, the Investment needs to be monitored to ensure whether the terms and conditions of the Investment fulfilled by both bank and client or not.

SWOT ANALYSIS

SWOT analysis is the detailed study of an organization’s exposure and potential in perspective of its strength, weakness, opportunity and threat. This facilitates the organization to make their existing line of performance and also foresee the future to improve their performance in comparison to their competitors. As though this tool, an organization can also study its current position, it can also be considered as an important tool for making changes in the strategic management of the organization.

Strengths:

- DBBL Limited has already established a favorable reputation in the banking industry of the country. It is one of the leading private sector commercial banks in Bangladesh. The bank has already shown a tremendous growth in the profits and deposits sector.

- DBBL has provided its banking service with a top leadership and management position. The Board of Directors headed by its Chairman Mr. Abul Hasnat and Md. Rashidul Islam is a skilled person in business world.

- DBBL Limited has already achieved a high growth rate accompanied by an impressive profit growth rate in 2007. The number of deposits and the loans and advances are also increasing rapidly.

- DBBL has an interactive corporate culture. The working environment is very friendly, interactive and informal. And, there are no hidden barriers or boundaries while communicate between the superior and the employees. This corporate culture provides as a great motivation factor among the employees.

- DBBL has the reputation of being the provider of good quality services too its, potential customers.

Weakness:

- The main important thing is that the bank has no clear mission statement and strategic plan. The banks not have any long-term strategies of whether it wants to focus on retail banking or become a corporate bank. The path of the future should be determined now with a strong feasible strategic plan.

- Some of the job in DBBL has no growth or advancement path. So lack of motivation exists in persons filling those positions. This is a weakness of DBBL that it is having a group of unsatisfied employees.

- In terms of promotional sector, DBBL has to more emphasize on that. They have to follow aggressive marketing campaign.

Opportunity:

- In order to reduce the business risk, DBBL has to expand their business portfolio. The management can consider options of starting merchant banking or diversify into leasing and insurance sector.

- The activity in the secondary financial market has direct impact on the primary financial market. Banks operate in the primary financial market. Investment in the secondary market governs the national economic activity. Activity in the national economy controls the business of the bank.

- Opportunity in retail banking lies in the fact that the country’s increased population is gradually learning to adopt consumer finance. The bulk of our population is middle class. Different types of retail lending products have great appeal to this class. So a wide variety of retail lending products has a very large and easily pregnable market.

- A large number of private banks coming into the market in the recent time. In this competitive environment DBBL must expand its product line to enhance its sustainable competitive advantage. In that product line, they can introduce the ATM to compete with the local and the foreign bank. They can introduce credit card and debit card system for their potential customer.

- In addition of those things, DBBL can introduce special corporate scheme for the corporate customer or officer who have an income level higher from the service holder. At the same time, they can introduce scheme or loan for various service holders. And the scheme should be separate according to the professions, such as engineers, lawyers, doctors etc.

Threats:

- All sustain multinational banks and upcoming foreign, private banks posse’s enormous threats to DBBL.If that happens the intensity of competition will rise further and banks will have to develop strategies to compete against an on slough of foreign the banks.

- The default risks of all terms of loan have to be minimizing in order to sustain in the financial market. Because default risk leads the organization towards to bankrupt. DBBL has to remain vigilant about this problem so that proactive strategies are taken to minimize this problem if not elimination.

- The low compensation package of the employees from mid level to lower level position threats the employee motivation. As a result, good quality employees leave the organization and it effects the organization as a whole.

CHAPTER –6

- RESEARCH & FINDINGS

DBBL Investment Project Study

Project Study Findings

Branch Manager Recommendation:

Mr. Md. Shanowar Hossain, Shathil is the proprietor of M/S. Anowara Trading Corporation. M/s. Anowara Trading Corporation is the retail and whole seller of Rod, Cement and C I sheet. Mr. MD. Shanowar Hossain, Shathil is an experienced businessman in this line. Mr. Md. Shanowar Hossain, Shathil has started this business in the year 2000. His monthly income is about TK.7,00,000.00(Gross) and net Income is TK.4,00,000.00(Four Lac) only as reported. M/s. Anowara Trading Corporation is a corporate client of our Branch and has been enjoying CC limit of Tk.700,000.00 (Seventy Lac) only and BG limit of Tk. 10,00,000.00 (Ten lac) only from our Bank, Now he has approached us to sanction of a Home Loan for Tk.5.0 (Five) million. To purchase a Fllat (B-6 Type) measuring 1255 sft on the 6tht floor of “DOM-INNO PLACER” at plot # 31, Road # 11, Sector # 6,Uttara model Town, Dhaka. The total price of the apartment including one car park is Tk.71,50,000,00. Mr. Md. Shanowar Hossain will also incur Tk. 26.76 lac for marble and other interior decoration of the said flat. He has submitted an estimate for Tk.26.76 lac. In this regard. Mr. Md. Shanowar Hossain has already paid Tk.12,50,000.00 the developer company.

In view of the above and considering the Personal net worth, integrity of the client , Scope of earnings from the proposed facility the facility is covered by land and building with acceptable nature and above all the client having good relation with us by enjoying corporate credit facilities from our Bank we strongly recommend for sanction of Home Loan of Tk.5,000,000/- (Taka Five Million) only to purchase a Flat measuring 1255 sft on the 6tht floor of “DOM-INNO PLACER” at plot # 31, Road # 11, Sector # 6, Uttara model Town, Dhaka for a period of 8(Eight) years in favor of Mr. Md. Shanowar Hossain Shathil with DBBL, Mirpur Circle-10 Branch, Dhaka.

Case 1:

Md. Shanowar Hossain (Shathil)