Executive Summary

Now-a-days, retail banking is the most sophisticated issue in the banking sector. From the word retail we know it is one kind of individual banking. Through retail banking a bank may provide differentiated banking product to the customer. The service or facilities under the retail banking are numerous types of deposit schemes and loans, ATM, Debit Card, Credit Card, Online Banking/internet Banking, online automated clearing house etc. everyday new and newer banking product are introduced to the market to fulfill latest demand of the consumer. In Bangladesh banking sector is the most emerging sector of the economy. Not only Bangladesh but also the whole world is on the demand of the banking sector for its diversified usage. Our selected “One Bank” has also delivered its retail banking facilities to the customer through 30 branches. To compete with the toughest competitor “One Bank” provided some types of deposit schemes to the consumer, such as Edusave, Marrysave, Pensave also some loans- Carloans,Consumer loans etc. In time of issuing such facilities, the bank faced so many challenges from the government & competitor in the market, such as-government intervention in providing car & consumer loan & the interest rate (spread).In providing modern banking facilities; such as-ATM booth, Debit card, and Credit card. One Bank is lagged behind to the competitor in the market. Not only in modern banking product but also in performing social responsibility, the bank is far behind from the competitor in the market, such as – Dutch Bangla Bank, Dhaka Bank, Standard Chartered Bank, Brac Bank etc.

Introduction

Now-a-days, the issue of retail banking is extremely important and topical. Across the globe, retail banking has been a spectacular innovation in the commercial banking sector in recent years. The growth of retail banking, especially in emerging economies, is attributable to the rapid advances in information technology. Following the global market, Bangladeshi Banks have not lagged behind. Specially One Bank offers typical retail banking products to the customer with great attention. Customers are always the top priority at One Bank. That’s why the retail banking division offers a range of solution driven and cost effective products and services that cater to the different needs of individual clients, ensuring that the personal touch is not merely a slogan but a practice that is very much a part of every transaction we make with One Bank. Our modern and convenient banking solutions ensure that One Bank offers us a unique approach to Retail Banking. By combining our preferred method of banking with the products and services available, One Bank can help the customer save time and effort and make our banking experience as effortless and cost effective as possible.

The Term Bank And Banker

A banker or bank is a financial institution whose primary activity is to act as a payment agent for customers and to borrow and lend money.

The first modern bank was founded in Italy in Genoa in 1406, its name was Banco di San Giorgio (Bank of St. George).

Many other financial activities were added over time. For example banks are important players in financial markets and offer financial services such as investment funds. In some countries such as Germany, banks are the primary owners of industrial corporations while in other countries such as the United States banks are prohibited from owning non-financial companies. In Japan, banks are usually the nexus of cross share holding entity known as zaibatsu. In France “Bancassurance” is highly present, as most banks offer insurance services (and now real estate services) to their clients.

Types of banks

Banks’ activities can be divided into following categories-

Retail banking- Dealsdirectly with individuals and small businesses.

Business banking- Provides services to mid-market business; corporate banking, directed at large business entities.

Private banking-providing wealth management services to high net worth individuals and families.

Investment banking- Relates activities on the financial markets. Most banks are profit-making, private enterprises. However, some are owned by government, or are non-profits.

Central Bank-Normally government owned banks, often charged with quasi-regulatory responsibilities, e.g. supervising commercial banks, or controlling the cash interest rate. They generally provide liquidity to the banking system and act as the lender of last resort in event of a crisis.

Our purpose is to focus on Retail Banking. So let’s have a look on retial banking.

Retail Banking

Retail banking refers to banking in which banking institutions execute transactions directly with consumers, rather than corporations or other banks. Services offered include: savings and checking accounts, mortgages, personal loans, debit cards, credit cards, and so forth.

Types of retail banks – Retail Banking is of following types-

Commercial bank: The term used for a normal bank to distinguish it from an investment bank. The term”commercial bank” refers to a bank or a division of a bank that mostly deals with deposits and loans from corporations or large businesses.

Community Banks: Locally operated financial institutions that empower employees to make local decisions to serve their customers and the partners

Private banks: Manage the assets of high net worth individuals.

Offshore banks: Banks located in jurisdictions with low taxation and regulation. Many offshore banks are essentially private banks.

Savings bank: In some countries, savings banks were created on public initiative, while in others socially committed individuals created foundations to put in place the necessary infrastructure. Nowadays, European savings banks have kept their focus on retail banking: payments, savings products, credits and insurances for individuals or small and medium-sized enterprises. Apart from this retail focus, they also differ from commercial banks by their broadly decentralised distribution network, providing local and regional outreach and by their socially responsible approach to business and society.

Community development banks: Regulated banks that provide financial services and credit to under-served markets or populations.

Postal savings banks: Savings banks associated with national postal systems.

Building societies and Landesbanks: Conduct retail banking.

Ethical banks: Banks that prioritize the transparency of all operations and make only what they consider to be socially-responsible investments.

Islamic Banks :Banks that transact according to Islamic principles.

COMPANY OVERVIEW

About One Bank

One Bank Limited incorporated in Bangladesh as a public limited company was established in 1999 under the COMPANIES ACT 1994. It started banking operations on 14 July 1999.

Authorized and Paid up capital – Tk 1,000 million and 202.5 million respectively. The capital is divided into ordinary shares of Tk 100 each. Fifty percent of its total share capital is reserved for the promoters designated as Group-A shareholders and the remaining 50% for general public designated as Group-B shareholders.

The head office of the bank is at Dhaka. A 10-member board of directors including the chairman and a vice-chairman governs the overall affairs of the bank. The managing director is its chief executive. In 2001, it had 73 employees, and 4 branches, all in urban areas.

Functions of the bank are deposit mobilization, lending, investment, foreign exchange business and other traditional banking services. Total deposits of the bank amounted to Tk 2,261.2 million in December 2000 and the deposit-mix comprised term deposits, savings bank deposits and current and contingency accounts, etc. As a new bank, it could not reach break-even and therefore, could not create any reserve funds till 31 December 2000.

Foreign exchange business handled by the bank in 2000 accounted for Tk 574 million covering export servicing, import financing and remittance facilities. The bank established foreign correspondent relationships with 33 international banks/bank offices.

Loans and advances made by the bank in 2000 were Tk 1,630.1 million. Its lending during 1999-2000 was limited to medium and large-scale industries, working capital finance, export credit, commercial loans and other activities. Investments of the bank in 2000 were Tk 240.26 million, which was made mainly in government TREASURY BILLs, from which it earned interest incomes of Tk 10.66 million.

Products And Services Provided By One Bank

Products and services provided by ONE BANK are-

Service of the Professional Personal

The Officers of ONE Bank Limited have, to their credit, decades of banking experience with National/ international banks at home and abroad. They are suitably equipped to meet customer expectations and are available at all times to provide a single-window customized and confidential service.

A State-Of-The-Art Technology Banking

The Bank will provide a state-of-the-art technology banking such as Any Branch Banking, ATM Services, Home-Banking, Tele-Banking, Mobile-Banking etc.

Retail Banking

ONE Bank limited offers individuals the best services, including the following, to provide complete customer satisfaction:

Deposit services.

Current Account in both Taka and major foreign currencies.

Convertible Taka Accounts.

Local and foreign currency remittances.

Various types of financing to cater to the banking requirements of multinational clients.

Institutional Banking

ONE Bank Limited will offer various services to foreign missions, NGOs and voluntary organizations, consultants, airlines, shipping lines, contractors, schools, colleges and universities. The services include mainly the following:

Deposit services.

Current Account in both Taka and major foreign currencies.

Convertible Taka Accounts.

Local and foreign currency remittances.

Various types of financing to cater to the banking requirements of multinational clients.

Corporate Banking

ONE Bank Limited caters to the needs of the corporate clients and provides a comprehensive range of financial services, which include:

Corporate Deposit Accounts.

Project & Infrastructure Finance, Investment Business Counseling, Working Capital and other finances.

Bonds and Guarantees.

Commercial Banking

Being a commercial bank, ONE Bank Limited provides comprehensive banking services to all. types of commercial concerns. Some of the services are:

Trade Finance.

Commodity Finance.

Issuance of Import L/Cs.

Advising and confirming Export L/Cs. – Bonds and Guarantees.

Investment advice.

ONE Bank Limited will provide specialized services to Ministries, Autonomous and Semi-autonomous bodies.

On-Line Banking

ONE Bank Limited offers ‘Any Branch’ banking service that facilitates its customers to deposit, withdraw and transfer funds through the counters of any of its branches within the country.

RETAIL BANKING PRODUCTS OF

ONE BANK LTD.

Deposit Schemes

Modern Banking system is becoming sophostiated day by day. To attract the customers One Bank is providing various facilities to sustain in the competitive market. Deposit schemes offerred by One Bank are –

One -2-3 scheme

Edusave

Marrysave

Pensave

Let’s have a discussion about these schemes-

One -2- 3 Scheme – One-2-3 Scheme will make customer’s deposit Double in 6 years, 2.5 times in 8.5 years and Triple in 11 years.

ONE-2-3 Scheme is a lucrative offer from ONE Bank Limited making customer’s deposits grows by folds over a certain period of time.This Scheme requires a fixed deposit of Tk. 5,000/- or its multiple for your chosen tenor.

More about ONE-2-3Customers can go for one or more schemes, even with different deposit amounts and tenors. In the event of premature encashment, One Bank will still give customers attractive interest rates.

Edusave Education is getting more and more expensive day by day. Hence Edusave is a far-sighted scheme that bridges customer’s dream and reality. Edusave can support customer’s expenditure for higher study at home or abroad. Edusave is a Deposit Scheme that offers customer to select from monthly installment amounts of TK. 500 / 1 ,000 / 1 ,500 / 2,000 and a tenor of 5 / 8 / 10 years, as they feel convenient

Marrysave Marrysave is a special designed scheme for the socially conscious citizens. This saving scheme will provide the financial security during customer’s marriage. Marrysave can support their expenditure during your marriage.

Pensave Pensave is a specially designed scheme for the socially conscious citizens. This scheme provides financial security during client’s retirement days. This scheme provides financial security after retirement.

Common features of EDUSAVE, MARRYSAVE AND PENSAVE SCHEME-

Customers have to open an account with One Bank and have to pay monthly installments.

Customers are free to choose more than one scheme with different installment amounts and tenors.

If any customer is the lucky winner of our monthly raffle draw, ONE Bank will contribute to that customer’s account next month’s installment

In the event of premature encashment One Bank will still give Customers interest at their Savings Deposit rate.

Customer will receive the amount mentioned in the table on maturity-

| Installment | Tk. 500 | Tk. 1,000 | Tk. 1,500 | Tk. 2,000 |

| Tenor | Amount Payable on Maturity | |||

| 5 Years | Tk. 41,243 | Tk. 82,486 | Tk. 1,23,730 | Tk. 1,64,973 |

| 8 Years | Tk. 80,763 | Tk. 1,61,527 | Tk. 2,42,290 | Tk. 3,23,053 |

| 10 Years | Tk. 1,16,170 | Tk. 2,32,339 | Tk. 3,48,509 | Tk. 4,64,678 |

Loans and Advances

ONE BANK Professional Loan:

This loan is a facility to support small-scale purchase of different equipments, tools and small machineries for installation at the business Sites/Offices.

Loan may be provided to purchase-

• X-ray Machines

• Medical Beds

• Ultra Sonogram Machines

• Engineering/Mechanical Tools

Loan can also be availed to purchase-

• Refrigerator

• Freezer

• Air conditioner

• Office Furniture

• Small generators

• IPS

• Personal Computers

• Printers

• Other Office Appliances

Loan Amount:

| Rural Area | TK. 30,000 to TK. 300,000 only |

| Urban Area | TK. 50,000 to TK. 360,000 only |

• Loan may be availed up to a maximum of 12 times of our gross monthly income

• Under special conditions, loan amount may be enhanced up to TK. 10,00,000 only.

Eligibility:

Bangladeshi nationals between the ages of 21-54 years, a monthly income of at least TK. 8,000 and having a minimum of two years working or business experience (reputed local corporate, multinational firms, government organizations, and autonomous bodies, engaged in business or a self employed professional).

Repayment:

Based on our convenience we may choose from 12,24,36 or 48 equated monthly installments (EMI) to repay the loan.

How we can apply:

First we need to collect loan application form. We fill up the loan application form with required supporting documents. Completed application will be processed on a priority basis.

One Bank Master Card (Gold & Silver)

ONE BANK CREDIT CARDS are widely accepted at department stores, shops, restaurants, hotels, airlines, travel agencies, hospitals, diagnostic centers etc. across the country wherever the MASTER CARD logo is displayed. We issue MASTER CARD in two versions: Gold and Silver.

Credit Limit:

Assigned Credit Limits are dependent on various criteria like applicant’s age, income and profession. Once approved our credit limit will be communicated to us.

Credit period:

Cardholder may enjoy between 15 and 45 days of interest free credit, from the date of each transaction. On receipt of the monthly statement the options are to either pay in full or only 10% of the current balance indicated. If our current balance is less than BDT 500, then we may pay in full.

Credit Interest:

Outstanding amount of monthly statement will attract interest @ 2.5% per month and will be calculated on a daily basis in the card account from the posting date.

Who can apply for a card:

If we are between 21 and 60 years of age and have a steady job or income that pays us at least BDT 120,000 annually (gross), we can apply for a ONE BANK MASTER CARD.

Card Annual Fee:

ONE BANK MASTER CARD GOLD: BDT 2,000.00 and ONE BANK MASTER CARD SILVER: BDT 1,000.00. These prices are excluding applicable VAT.

Cash Advance Facility:

ONE BANK MASTER CARD allows the facility to draw cash up to the extent of 50% of our credit limit. Cash advance is available at ONE BANK branches and ATMs displaying the MASTER CARD logo. Availing cash advance attracts applicable fee and amount withdrawn will be subject to interest from the transaction date.

Cash Back Reward Scheme:

Cardholders may enjoy the benefit of cash back reward scheme. Cardholders will earn 1 reward point for every purchase worth BDT 200.00 and cash back of BDT 0.50 will be given for each reward point earned. The earned cash back amount will be credited to card account upon receipt of a request from cardholder in the month of January and July each year.

For Lost/Stolen Card:

If the card is lost or stolen, simply we an call ONE Bank’s 24 hour Help Desk. Also we should report to the bank about the loss by fax to ONE BANK LTD. within 24 hours. These steps are essential to prevent fraudulent transactions on the lost card.

Account with ONE BANK:

The credit card holders are recommended to maintain an account (not mandatory) with ONE BANK LTD., thereby enabling convenience of auto monthly settlement of their bills, by filling a ‘Standing Instruction’ to this effect.

Apply for the Card:

We should just visit any ONE BANK branch or contact ONE BANK LTD, Retail Banking division, Card Service for more information.

One bank Car loan: The loan serves to fulfill our life style aspirations. Attractive interest rates and the equated monthly installment repayment make decision very easy and straightforward.

With one bank car loan we can purchase:

A brand new vehicle of any brand.

Reconditioned vehicle.

One bank will finance up to 80% for a brand new and 70% for a reconditioned vehicles quoted price.

Loan amount:

Minimum: taka 300000

Maximum: Taka 2000000 only.

Loan can be availed up to 18 times of gross monthly income. Additionally if quashi cash or other securities acceptable to the bank are provided, the bank at its discretion may allow preferential interest rates.

Eligibility:

Bangladeshi nationals between the ages of 21-54 years a monthly income of at least Taka 30000 and having a minimum of two years working or business experience (reputed local corporates,multinational firms, government organizations, engaged in business or a self employed professionals.)

Repayment:

the maximum repayment period is 60 months for a brand new car and 48 months for a reconditioned car. Based on our convenience we may choose from 12,24,36,48 or 60 equated monthly installments.

How we can apply:

First we need to collect loan application form. We fill up the loan application form with required supporting documents. Completed application will be processed on a priority basis.

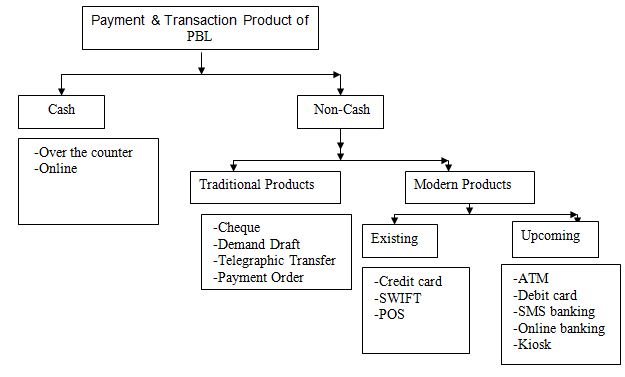

Payment & transaction product of ONE BANK

One bank commitment to excellent customer services delivery to their customer. This bank adopted various payment & transaction products & services for smooth payments & transactions for the customers. This includes both traditional & modern products. Though modern products demand is increasing traditional banking product is still dominating. The payment and transaction product of one bank is given below:

Payment & transaction product Of ONE BANK

Marketing Strategies of the retail banking services

Differentiated products

One bank introducing their retail banking through differentiating their products as customer oriented and the patterns of essentiality and demand. This product differentiation has brought out the maximum coverage of their retail banking in a shortest time. These products differentiation is designed mainly the demand and the nature of services that customers want.

Goodwill

The bank has its long experience of rural banking before commencing the ongoing banking services. Utilizing the experience of working with the vast rural sector, the ONE Bank using its goodwill to operate the retail banking thus, made it success in the field of modern competitive retail banking.

High exposure

One bank penetrated the market with the strategy of a big bang in the market. It’s taken the followings media to capture the market

• Media

• Sponsorship

• Beautification

• Other social responsibility

Available of modern technology

In general, ONE bank always tends to make a difference in their technological advancement. They inaugurated various technical supports to make easier their banking service and almost to provide the utmost satisfaction to their customer.

Service oriented banking

ONE bank has set up a new dimension to provide the customer services. It emphasizes “customer first” cares and to protect the value of their customer through hassle free banking services. It also arranges the well decorated premises for their banking services and related facilities to their customers

Risk Management

The risk of ONE BANK LTD. is defined as the possibility of losses, financial or otherwise. In today’s challenging financial & economic environment effective risk management is vital for sustainable growth of shareholders value. The major areas of risk in which the activities of the banking operation is exposed to are credit risk, market risk, interest rate risk & equity risk.

Risk Management Process:

One bank activities involve analysis evaluation, acceptance 7 management of some risk or combination of risks. Risk management is emphasized not only for regulatory purpose but also to improve operational & financial performance of the bank.

The risk management policy of the bank operates under 5 broad principles-

• Oversight by the board committee. Board approves policies & processes of risk management recommended by the management & executive committee approves the credit proposals submitted by the management.

• Audit committee of the board reviews the internal audit reports of the bank & risk management covering credit risk.

• Dedicated independent risk management units viz credit risk management units, credit administration units, and credit monitoring & recovery unit.

• Dedicated committee at the management level has been set up to monitor risk viz. credit risk through Credit Review Committee & Risk Management Division, Operational Risk through management committee & Internal Control & Compliance division.

Market Risk:

Market risk is defined as the potential change in the earnings due to changes in the rate of interest, foreign exchange rate & equity prices. Treasury Division manages the market risk & monitors the activities of treasury division in managing the risk.

Interest Rate Risk:

Treasury Division reviews the trend analysis of market movement particularly peer group analysis & economic outlook closely & prepares the gap position for proper management of interest rate movement. The estimated impact of 1 percent change in interest rate was within the tolerable limit of the bank. The bills held for the maturity had positive PV, as such it had favorable affect in banks equity position. As per policy of Bangladesh Bank the revaluation gain or loss are shown against changes in equity.

Foreign Exchange Risk Management:

Foreign Exchange risk are measured & monitored by treasury department. Foreign exchange risk is defined as the potential change in earnings arising due to change in market prices. Treasury division monitors the FX price changes. The foreign exchange risk of the Bank is insignificants all the transactions are carried out on behalf of the customers against underlying L/C commitments & other remittance requirements. No dealing on banks accounts was conducted during the period.

Equity Risk:

Equity risk is defined as loss due to change in market price of equity held. To measure & identify the risk, market to market valuation of the share investment portfolios are done. Mark to market valuations is done a predetermined cut loss limit. Investment account where margin loan is allowed is monitored very closely against predetermined margin requirement & margin ratio. Diversification is enforced as per Bank’s own policy. At the time providing margin loan following factors are taken into consideration.

• Security of Investment

• Fundamentals of the security

• Liquidity of the securities

• Reliability of earnings

• Capital appreciation

• Risk factors

• Implication of taxes

Operational Risk Management:

Operational risk is the risk of loss arising from fraud forgery, unauthorized activities, omission, inefficiency, system failure from inadequate or failed internal process & external event. It is inherent in every business organization & covers a wide spectrum of issues. Operation risk my be caused based, effect based & event based.

Liquidity Risk Management:

The object of liquidity risk management is to ensure that all foreseeable funding commitments & deposits withdrawals can be met when due. To this end, PBL maintains diversified & stable funding base comprising of core retail, corporate & institutional deposits. It maintained sufficient liquid assets for meeting the funding requirements. The principle responsibility of the liquidity risk management of the bank rests with Treasury Division. Treasury Division maintains liquidity based on historical requirements, current liquidity position, anticipated future funding requirement, sources of fund, option for reducing fund needs, present & anticipated asset quality, present & future earning capacity.

Social Commitments

In todays corporate world the financial institutions perform many activities for the society to sustain in the competitive market. ONE Bank is also performing different kinds of activities. They are as follows-

Bangladesh Flood 2004

ONE Bank tried to mitigate the sufferings of the flood stricken people in the villages of Meradia/ Shatarkul (Dhaka), by distributing Family Bags amongst 1,100 families. Each bag contained the following items: Rice: 3 Kg, Pulses: 1 Kg, Salt: 1Kg, Molasses (Gur): 1 Kg, Two pieces of Sari & 2 pieces of Lungi (one large and one small). The recipients very much appreciated our endeavor.111 new houses constructed for the flood affected families at Sylhet and DoharThe Bank spent around Taka three million in flood related relief activities.

Cricket

ONE Bank has been actively supporting the flourishing of Cricket in Bangladesh. To facilitate the movement of cricket officials, the Bank has presented one microbus to the Bangladesh Cricket Control Board.In addition, your bank has been the official tickets sponsor for the New Zealand, India and Zimbabwe cricket (Test and ODI) series, during the year 2004.

Comparison part

Prime bank limited

Vs

Comparison of Strategy

ONE BANK VS. PRIME BANK

Product line of retail banking of ONE BANK consists of few deposit and loan scheme. On the other hand product line of Prime bank consists of many products. Prime bank not only develop different products but also provide these services to achieve their ultimate goal.

Competitive advantage on competitive financial market of Bangladesh:

In Bangladesh, 30 Commercial Banks are operating in Bangladesh. So we can say that our financial market as well as commercial banking sector is competitive. In competitive financial market PBL expanding their product and business, where OBL operating their less product and branches. To compare with these two branches we may easily conclude that PBL has comparative advantage on OBL.

Wide banking network through Branches and and E-Banking:

OBL is operating their business through 31 branches. PBL doing their business through – branches.PBL expanding their business around our country, where One Bank’s maximum branches located in Dhaka, Chittagong and Sylhet city. In this perception PBL’s strategy is better than One Bank.PBL collected deposits from the whole country and invested this money in different sectors also in retail banking. They collect fund from individuals with their branches that increases their productivity in retail banking sector.OBL can differentiate their product and can achieve productivity through retail banking.

Social responsibilities:

Retail banking activities are concerned with individuals. Now a days people are looking for not only business activities but also their social responsibilities. In competitive market social activities of business work regard as their marketing activities. This up growing social responsibilities attract individual to be linked with business.PBL contribute much in social responsibilities, than OBL.PBL recently sponsors theBAFOFA.But OBL’s social activities is lower in compare with PBL.OBL should increases it’s social responsibilities which will be benefited for our society and also OBL’s business.

Creating market demand through advertising:

Advertising of products and services is an important tool to create an increase market demand. In our country different commercial banks advertise their banking retail products through newspapers and electronic medias. Prime Bank is also advertising their retail banking products with the features and facilities. But OBL does not have any strategy to advertise their retail banking scheme.

Risk management strategy:

Risk management is very important because firm always seeking for maximizing their profit by minimizing risk. In case of banks it is very important because they operate business with others money. ONE BANK & PRIME BANK are managing their risk efficiently but to be more efficient risk management they have to diversify their risk. Most of the branches of OBL located in the Dhaka (16 out of 31) and they have no branch in Rajshahi, khulna & Barishal. To be more efficient risk management ONE BANK Ltd. has to diversify their risk by opening branch on those areas.

Maintenance of the Regulation of the Central Bank:

Bangladesh Bank as a central bank of our country makes legislation for the commercial banks. When Bangladesh Bank makes any regulation it must be implemented by commercial banks. Few months ago, B.B. announced for the scheduled banks to reduce interest rate of loans. But some scheme of OBL is carrying interest rate of 16.5%- 18.5%Though Prime Bank’s interest rate is not below the 15% but a little bit lower than OBL. These two banks should reduce their interest rate according to the regulation of Bangladesh Bank.

Challenges faced by one bank

Regulation of central bank:

• Car Loan: Car Loan is the prime earning source for the ONE BANK. Mainly it provides this loan facility to the upper middle and middle class family. But for rising price the amount of loan default is increasing. At the same time, for buying more cars it creates traffic congestion which compels the central bank to enforce some regulations like reducing the loan facility on car. So it becomes a challenge for this bank.

• Consumer Loan: Another thing is that ONE BANK provides more and more consumer loan. It is profitable for this bank. But from the greater perspective, it is not effective for the country. Because for not providing loans in the industrial sector output is not increasing at all. As a result govt. pressures banks to provide more loans in the industrial sector.

• Use of Credit Card: Consumers are using credit cards on buying daily necessary goods. Govt. restricts on using credit card in this case to encourage consumer to engage in greater transaction.

Challenges in competitive market:

• Modern Facilities: Compared to other banks ONE BANK provides less modern facilities to the customers like ATM services as well as internet banking facilities. As a result ONE BANK looses their customers for getting these facilities from other banks.

• SME Banking: ONE BANK does not provide SME banking facilities which is provided by other modern banks.

• Differentiated Products: Most of the modern banks provide differentiated products but ONE BANK does not provide these types of products and for this reason it does not attract the customers.

• Branch Banking: ONE BANK has fewer branches compared to other banks. So customers do not get banking services at any moment.

• Using consumer loan for business purpose: Sometimes businessmen are unable to get industrial loan for want of proper banking statement. So they use consumer loan for this purpose. As a result ONE BANK cannot expand its business.

• Weak Advertisement Policy: ONE BANK has not any focusing advertisement policy to promote the products. As a result, the expansion of this bank is slower than other banks.

Recommendation

We can now justify about retail banking activities from the above discussion of retail banking in Bangladesh & the retail banking activities of One Bank. We can now recommend some initiatives relevant to the banking activities of one bank.

Expansion of its business:-Getting information from one bank and its website as well as its market situation, we see that it has little exposure. On the basis of above analysis, One Bank should expand its business through establishing more branches.

Providing more modern retail banking product:-Today, Bangladeshi banking sector is the most competitive sector in the market. Every numerous banking facilities are being delivered specially retail banking products are being introduced to the banking customers. In order to cope with the changing market, One Bank should produce more retail banking products in the market, i.e.- SME banking, some innovative deposit scheme etc.

Modern Banking Facilities: Bangladesh, as a new born baby in modern banking sector, we refer ATM., online banking & POS as modern banking services served by One Bank. But in this sector the performance of One Bank is very poor. In order to develop this sector, it has to provide-

• More ATM booth services

• Internet Banking & SMS banking

• Point of Sale(POS)

Loan for the appropriate person or sector: Now days we feel that the loan seeker for industrial purpose are more interested in consumer loan because of its availability. As a result, for which purpose the bank provide the loan, is not specific rather than it is vague in the user of loan. So, the bank cares about its loan facilities & be strategic in lending sector. And also suggested that loans in industrial sector should be increased & flexibility in the process of lending industrial loan like on consumer loan.

Research & Development for customer satisfaction: In this competitive business environment, Research & Development activities are thought to enrich the banks with new & improved products, process & business avenues. In this pursuit One Bank should recruit team for research by which they can achieve better customer satisfaction.

[/starlist]