Executive Summary:

Bangladesh Bank it is most important side of the bank. Bank is nothing but a middleman between lenders (surplus unit) and borrowers (deficit unit). To provide loan, a bank needs a huge amount of money from the depositors. General banking is the side where banks offer different alternatives to the clients to deposit and remit their money

Bangladesh bank would be prepared to consider approval for advance remittance against goods to be imported into Bangladesh where such goods are of specialized or capital nature. Application for approval in form IMP should be submitted in Bangladesh bang along with the Exchange Control copy of the relative LCAF, the contract in original entered into between the importers and the foreign manufacturer or supplier, and an undertaking on prescribed Performa.

In all cases of purchase of foreign currency an application must be made to an authorized Dealer and, where necessary to Bangladesh Bank. For payments against imports into Bangladesh, the prescribed application form, Form IMP is used and for other types of remittances form TM is used.

Exchange control copies of the LCAFs submitted by the importers, should, when fully utilized, is forwarded by the Authorized Dealer to the Bangladesh Bank. Exchange Control copies of LCAFs which remain unutilized for the full amount should also be surrendered by the Authorized Dealers to the Bangladesh Bank after expiry of the validity period for remittances.

Introduction:

1.1 Background of the Study

After completion of all the required courses of MBA program under Stamford UniversityBangladesh, it is an indispensable part of the study to get involved in a practical professional environment. I had joined with The Rupali Bank Ltd., Local Office, Dhaka for a three months period. Local Office, Dhaka, is the main branch of The Rupali Bank Ltd., and it performs the entire banking activities including General Banking, Loan & Advance and Foreign Trade Financing. As a result, one can easily learn all the simple and intricate banking operations from the activities of this branch. So I select Rupali Bank Ltd., Local Office, Dhaka, as sampling area to prepare this internship report. This report is the output of my practical experience which I gathered during intern life.

1.2 Origin of the Report

Theoretical sessions alone cannot make a business student efficient and perfect in handling the real life business situation. Therefore it is important for a student to comprehend the application of theoretical knowledge in practical fields through Internship program. This program may be divided into two phases:

£ Organizational part: To introduce the internee with the structure, functions, and performance of the organization.

£ The project part: Pertaining to a particular problem or a searching topic matching with internee’s capacity, interest of the organization’s requirements.

1.3 Objectives of the Study

Primary Objective:

£ Get the knowledge about report writings.

£ To make a study (theoretical & practical) and prepare a report that reflects our understandings and knowledge attained during the period.

Secondary Objective:

£ To know about the company and its products / services.

£ To get a good understanding of “Foreign Trade Financing” activities of the bank.

£ To make some findings and put forward some recommendations.

1.4 Methodology of the Study

The needed for conducting the study have been collected from the primary sources as well as secondary sources. In collecting the necessary data, care has been taken so that all the variables that may in some way can’t affect the objectives of the study. The information that I used in this study is collected from the following sources:

Primary data sources:

£ Personal interview with the employees

£ Practical desk work

£ Face to face conversation with the client

Secondary data sources:

£ Bulletin published by the bank

£ Annual statement of the bank

£ Previous research books and journals

£ Different books about banking

1.5 Scope and Rationale of the study

The main focus of the study is “Foreign Trade Financing” of RBL”. The topic is fixed. But the report has tried to cover overview of RBL objectives, functions, management, business policy and other things. This report has also mentioned some problems of RBL’s Operating systems and its solutions. The empirical part includes only the published information and current practices of the Rupali Bank Limited.

1.6 Limitations of the Report

Like every other studies, I too faced some constraints during my project period which otherwise would have enabled me in making my study more appropriate and logical. The limitation is from both side the bank as well as myself. The followings are some of the shortcoming, I came across:

£ I had to go to almost every Department of RBL as part of the internship program. There is a very short span of time to get in-depth knowledge about a massive organization like RBL.

£ Officials of RBL maintain a very busy schedule. So they are not always able to provide enough time to enlighten the internee students every time, even if they had the intention to do so.

£ The area covered by the report ” Foreign Trade Financing” of RBL concerns a huge number of activities and it is very difficult to sketch a total picture of the financial activities in a report of this scale.

£ Supply of more practical and contemporary data was another shortcoming.

£ Last but not least; the report would have more better and practical, as I too have shortcoming with time, knowledge and capacity.

£ The allocated time was not enough for getting a sound knowledge about the study.

Chapter – 2

An Overview of RBL

2.1 Introduction of Rupali Bank Limited:

Rupali Bank Ltd. was constituted with the merger of 3 (three) erstwhile commercial banks i.e. Muslim Commercial Bank Ltd., Australasia Bank Ltd. and Standard Bank Ltd. operated in the then Pakistan on March 26, 1972 under the Bangladesh Banks (Nationalization) Order 1972 (P.O. No. 26 of 1972), with all their assets, benefits, rights, powers, authorities, privileges, liabilities, borrowings and obligations. Rupali Bank worked as a nationalized commercial bank till December 13, 1986.

Rupali Bank Ltd. emerged as the largest Public Limited Banking Company of the country on December 14, 1986 under the order No. Ag / Awe / weK- 3 / 33 / 86 / 361 of the Govt. of the Peoples Republic of Bangladesh.

2.2 Mission of the Bank:

The bank participates actively in socio-economic development of the country by performing commercially viable and socially desirable banking functions.

2.3 Present Capital Structure:

| Authorized Capital | : | Tk. 7000 million (US$ 120.70 million) |

| Paid up Capital | : | Tk. 1250 million (US$ 21.55 million) |

| Reserve Fund | : | Tk. 1130.38 million (US$ 19.49 million) |

2.4 Break up of paid up Capital:

| (a)Government shareholding | : | 93.23% |

| (b) Private shareholding | : | 6.77% |

2.5 Board of Directors:

The Board of Directors is composed of 8 (eight) members comprised of representatives from both public and private sectors and shareholders. The members of the Board of Directors are appointed by the Govt. in the following manner:

Chairman | Managing Director | Directors |

1(one) | 1(one) | 6 (six) |

2.6 Chief Executive:

The Bank is headed by the Managing Director (Chief executive) who is a reputed professional Banker.

2.7 Organogram of Rupali Bank Ltd:

v Managing Director

v Deputy Managing Director

v General Manager

v Deputy General Manager

v Assistant General Manager

v Senior Principal Officer

v Principal Officer

v Senior Officer

v Officer

v 3rd Grade Staff (Supervisor/ Cashier/ Typist)

v 4th Grade Staff (Driver/ Guard/ MLSS)

2.8 No. of Branches:

Rupali Bank Ltd operates through 492 branches. It is linked to its foreign correspondents all over the world.

2.9 Numberof Zones and Corporate Offices:

The Corporate Head Office of the Bank is located at Dhaka with one local office (Main Branch), four corporate branches at Dhaka, one in Chittagong and twenty-five zonal offices all over the country.

2.10 Number of Employees:

The total number of employees is 4430.

2.11 International Banking:

Rupali Bank Ltd. engages itself in providing best international banking service to its valued clients by serving through 28 Authorized Dealer branch.

It has a good number of correspondent banks world-wide and it handles a big volume of export and import business. It is also engaged in collecting home-based remittances of the people and paying the same to the beneficiary promptly.

2.12 Products and Services:

- Export Credit (Pre-shipment & Post-shipment)

- Suppliers Credit

- Letter of Credit (Import)

- Guarantees in Foreign Currency

v Bid Bond

v Performance Guarantee

v Advance Payment Guarantee

- Bill purchasing/ discounting

- Remittance, Collection, Purchases & Sales of Foreign Currency & Traveler’s Cheques

- NRTA (Non-Resident Taka A/C )

- NFCD Account (Non-Resident Foreign Currency Deposit)

- RFCD Account (Resident Foreign Currency Deposit)

- Convertible & Non-convertible Taka Account

- Forward contracts

- Correspondent Banking Relations

2.13 Correspondent Banking:

- Rupali Bank Ltd’s aim is to increase its foreign exchange business.

- It is doing international banking with major banks of the world.

- It is attending to problems of the correspondent banks.

- It is maintaining agency arrangements and correspondent relationship with about 160 foreign correspondents.

2.14 Countrywise list of CorrespondentBanks are given bellow.

- Australia

- Canada

- China

- Croatia

- Denmark

- France

- Germany

- Hong Kong

- India

- Japan

- Jordan

- South Korea

- Kuwait

- Malaysia

- Nepal

- Netherlands (Holland)

- Oman

- Pakistan

- Qatar

- Russian Federation

- Saudi Arabia

- Singapore

- Sri Lanka

- Switzerland

- Sweden

- Thailand

- UAE

- U.K

- U.S.A

- Yugoslavia

Chapter – 3

Product & Services

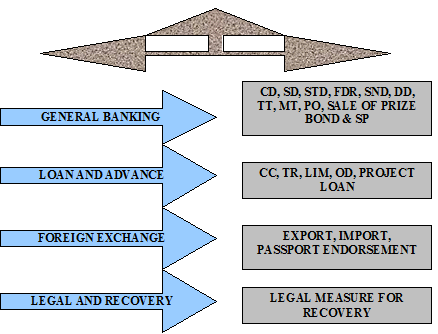

3.1 Line of Product & Services of Rupali Bank Limited, Local Office, Dhaka:

Local Office is the main branch of The Rupali Bank Ltd., situated at Ground floor & 1st floor of Rupali Bhavan, 34, Dilkusha C/A, Dhaka.The branch operating its overall business activities under the leadership of a Deputy General Manager, The branch provides above mentioned product & services to its clients through four departments namely:

£ General Banking

£ Loan & Advance

£ Foreign Exchange

£ Legal & Recovery

Head of the above departments are four Assistant General Manager the branch, who is directly responsible to the Deputy General Manager for the performances of their respective departments.

The products and services provided by the above departments of the branch to its clients are mentioned below:

3.2 Product and services:

RBL has a very broad line products under the various business group, from short term to long term deposits, various types loans and advances, account service, it provides finance for export and import, finance for working capital, project financing, capital investment, remittance service, trade service, foreign exchange service, online banking, cash management service, locker service, Profit & loss sharing and also has other miscellaneous product and services around the nation.

3.3 Product of Trade service:

3.3.1 Fund Based:

à Cash Credit (CC Hypo)

à Cash Credit (CC Pledge)

à Overdraft (OD)

à Trust Receipt (TR)

à Foreign Bill Purchase (FBP)

à Loan Against Important Merchandise (LIM)

3.3.2 Non-Fund Based:

à Letter of Credit (LC)

- o DA (Deferred)

- o DP (Sight)

à Letter of Guarantee (LG)

A limit (amount) is set by the bank that can be availed by a particular Customer based on his / her Credit worthiness and record of business transactions with the bank.

3.4 General Banking:

It is most important side of the bank. Bank is nothing but a middleman between lenders (surplus unit) and borrowers (deficit unit). To provide loan, a bank needs a huge amount of money from the depositors. General banking is the side where banks offer different alternatives to the clients to deposit and remit their money. To encourage the clients, bank offers different options in front of their clients. Most of these options are very much similar between the banks, but the customer services and facilities may not be the same.

General Banking of RBL is divided into 5 divisions:

I. Account opening

II. Remittance

III. Clearing

IV. Cash.

V. Account’s Department

3.4.1 Account Opening

The relationship between the banker and the customer begins with the opening of an account by the customer. Initially all the accounts are opened with a deposit money by the customer and hence these accounts are called deposit account. Usually a person needs to open an account ton take services form it. Without an opening an account, one can get only a few services from the bank. So the banking begins actually by opening an account with a bank. Generally, there are four types of accounts in our country’s banking system:

i. Current account or Demand Deposit(CD Account)

ii. Savings Deposit(SB Account)

iii. Fixed or Time Deposit(FDR)

i. Current Account

Current account is purely demand deposit account because the bank is bound to pay the amount to the account holder on demand at any time. It is running and active account, which may be operated upon any number of times during a working day. There is no restriction on the number and the amount of withdrawals from a current account. The special characteristics of a current account are as follows:

µ The primary objective of current is to serve big customers such as businessmen, joint stock companies, private limited companies, public limited companies etc. from the risk of handling cash by themselves.

µ The cost of providing current account facilities is considerable to the bank since they undertake to make payments and collects the bills, drafts, cheques for any number of times in a particular day. The bank therefore does not pay any interest on current deposit while on the other hand some banks charge for incidental charges on such account.

µ For opening of a current account minimum deposit of taka 1000/= is required. Introductory reference is also required for opening of such account.

Opening a Current Account

The following documentation and formalities are required for opening a current account:

Documentation of Opening a Current Account

Û For Proprietorship: Up-to-date copy of trade license, Introducer of a CD account holder, Two copies of passport size photographs of account holder, Seal, TIN, VAT certificate

Û For Partnership: up to date copy of trade License, Introducer of a CD account holder, Two copies of passport size photographs of account holder, Photocopy of partnership Deed, notarized by Notary Public, Account agreement (MF-06) and letter of partnership (MF-07), Seal, TIN, VAT certificate

Û For Private Limited Company: Up-to-date copy of trade license, Two copies of passport size photographs of account holder, Certified copy of Memorandum and Articles of Association, signed and sealed by the managing Director, Photocopy of the certified of Incorporation, List of directors as per return of joint stock company with signature ,Seal of each operating persons, Particulars of Directors, Resolution for opening account with the bank

Û For Public Limited Company: Up-to-date copy of trade license, Two copies of passport size photographs of account holder, Certified copy of Memorandum and Articles of Association, signed and sealed by the managing Director, Photocopy of the certified of Incorporation, Seal of each operating persons, Particulars of Directors, Resolution for opening account with the bank, Certificate of commencement of business, List of directors as per return of joint stock company with signature

Û For Societies, Clubs, Associations etc: Up-to-date copy of trade license, Registration from the concerned authority, By laws/ rules and regulations/ constitutions duly signed and sealed by chairman, Resolution for opening account with the bank, Introducer of a CD account holder, Seal of each operating persons.

Formalities of Opening a Current Account

v Application on the Prescribed Form

The person willing to open a current account with the bank has to make application in the prescribed form. This form must be properly filled up and signed by the applicants.

v Introduction to the Applicant

The applicant also required to furnish in the application form the names of the referees from whom the banker may make inquires regarding the character, integrity and respectability of the applicants. In most cases the introduction is done by the customer of the bank or some other person knows to the bank by signing on the application form with his/her account number (if any).

v Specimen signature

Every customer is required to supply to his banker with one or more specimens of his/her signature. These signatures are taken on cards, which are preserved by the banker, and his signature of the account holder on the cheques is compared with the Specimen signatures.

v Opening and operating the account

After the above formalities are over, the banker opens an account in the name of applicant. Generally the minimum amount to be deposited initially is tk. 1000/- for opening a current account. Then the bank provides the customer with:

- A pay in slip/deposit book

With a view of facilitate the receipt of credit items paid in by a customer, the bank will provide him/her pay in slip either loose or in a book forms. The customer has to fill up the pay in slip at the time of depositing the money with the bank. The cashier with his/her initials and stamps will return the counter foil to the customer on the receipt of the money.

- Cheque Book

To facilitate withdrawals and payments to third parties by the customer, the bank will also provide a cheque book to the customer. But it is noted that to get a cheque book, the customer has to dully fill up the cheque requisition slip to the banker.

ii. Savings account (SB)

A savings account is meant for the people of the lower and middle classes who wish to save a part of their incomes to meet their future need and intend to earn an income from their savings. It aims to encouraging savings of non trading persons, institutions, society and clubs etc. by depositing small amount of money in the bank. Both the elements of time and demand deposit are present in this account.

Opening a Saving Account

For opening a savings account following documentation and formalities are required:

Documentation’s

(a)

v Two copies of passport size photographs of account holder.

v Photograph of the nominee

v Introducer’s reference

v Employer certificate

(b)

v Two copies of passport size photographs of account holder.

v Photograph of the nominee

v Photocopy of passport ( first four pages)

v Introducer’s reference

v Employer certificate

Formalities of Opening

v Application on the prescribed form: The person willing to open a savings account with the bank has to make application in the prescribed form. This form must be properly filled up and signed by the applicants.

v Introduction to the Applicant: The applicant also required to furnish in the application form the names of the referees from whom the banker may make inquires regarding the character, integrity and respectability of the applicants. In most cases the customer of the bank does the introduction or some other person knows to the bank by signing on the application form with his/her account number (if any).

v Specimen signature: Every customer is required to supply to his banker with one or more specimens of his/her signature. These signatures are taken on cards, which are preserved by the banker, and his signature of the account holder on the cheques is compared with the Specimen signatures.

v Opening and operating the account: After the above formalities are over, the banker opens an account in the name of applicant. Generally the minimum amount to be deposited initially is tk. 1000/- for opening a current account.

Then the bank provides the customer with:

A pay in slip/deposit book: With a view of facilitate the receipt of credit items paid in by a customer, the bank will provide him/her pay in slip either loose or in a book forms. The customer has to fill up the pay in slip at the time of depositing the money with the bank. The cashier with his/her initials and stamps will return the counter foil to the customer on the receipt of the money.

Cheque Book: To facilitate withdrawals and payments to third parties by the customer, the bank will also provide a cheque book to the customer. But it is noted that to get a cheque book, the customer has to dully fill up the cheque requisition slip to the bank.

iii. Fixed Deposit Receipts (FDR)

These are the deposits, which are made with the bank for fixed period specified in advance. It is purely a time deposit account. The bank doesn’t maintain cash reserves against these deposits and therefore the bank offers higher rates of interest on such deposits. At present the rate of interest for fixed deposit Receipt (FDR) in the First Security Bank Limited are as follows:

Rate of interest for fixed deposit Receipt (FDR)

Time period | Interest rate |

| For 3(three month) | 7.5% |

| For 6(six month) | 7.75% |

| For 1(one year) | 8% |

| For 2(two year) | 8.5% |

| For 3(three year) | 8.5% |

Source: Bank Circular

3.4.2 Remittance

Remittance of funds is ancillary services of RBL. It aids to remit fund from one place to another place on behalf of its customers as Ill as non- customers of Bank. RBL has its branches in the major cities of the country and therefore, it serves as one of the best mediums for remittance of funds from one place to another. The main instruments used by RBL:-

i. Payment Order Issue/Collection

ii. Demand Draft Issue/Collection

iii. T.T. Issue/Collection

iv. Locker Service:

v. Mail Transfer Advice (MTA)

i. Payment Order:

The pay order is an instrument issued by bank, instructing itself a certain amount of money mentioned in the instrument taking amount of money and commission when it is presented in bank. Only the branch of the bank that has issued it will make the payment of pay order.

Issuing of Pay Order:

The procedures for issuing a Pay Order are as follows:

▫ Deposit money by the customer along with application form.

▫ Give necessary entry in the bills payable (Pay Order) register where payee’s name, date, PO no, etc is mentioned.

▫ Prepared the instrument.

▫ After scrutinizing and approval of the instrument by the authority, it is delivered to customer. Signature of customer is taken on the counterpart.

Different modes of PO when a customer can purchase:

By cash:

Cash A/C Debit

Bills payable (PO) A/C Credit.

Income on commission A/C Credit.

By account:

Customer’s A/C Debit

Bills payable (PO) A/C Credit.

Income on commission A/C Credit.

By transfer:

RBL General/ other Dept Clients A/C Debit

Bills payable (PO) A/C Credit.

Income on commission A/C Credit.

PO A/C is the current liabilities of bank, which is acquired to be discharged by beneficiaries against cash or through an account.

Settlement of a PO:

When PO submitted by collecting bank through clearing house, the issuing bank gives payment.

Bills payable (PO) A/C Debit

RBL General A/C Credit.

But before giving payment it is duty for issuing to observe whether endorsement was given by the collecting bank or not, then the instrument is dishonored and marking ‘Endorsement required’.

Bills payable (PO) —————Dr.

Customer A/C———————Cr.

ii. Demand Draft:

The person intending to remit the money through a Demand Draft (DD) has to deposit the money to be remitted with the commission which the banker charges for its services. The amount of commission depends on the amount to be remitted. On issue of the DD, the remitter does not remain a party to the instrument:

à Drawer branch

à Drawn branch

à Payee.

This is treated as the current liability of the bank as the banker on the presentation of the instrument should pay the money. The banker event on receiving instructions from the remitter cannot stop the payment of the instrument. Stop payment can be done in the following cases:

Loss of draft before endorsement: In this case, “Draft reported to be lost, payee’s endorsement requires verification” is marked.

Loss of draft after endorsement: In this case, the branch first satisfies itself about the claimant and the endorsement in his favor.

Accounting treatment:

In case of issuing of the instrument:

Cash/ customer’s A/C———————Dr.

RBL General A/C (Drawn on branch)———-Cr.

Income A/C commission—————————Cr.

After giving these entries an Inter Bank Credit Advice is prepared which contains the controlling number, depicting that the branch is credited to whom it is issued.

An IBCA implies the following entries,

RBL General A/C Issuing Branch ——-Dr.

Drawn on branch————————————Cr.

iii. Telegraphic or Telephonic Transfer (TT)

This Method transfers money to one place to another place by telegraphic message. The sender branch will request another branch to pay required money to the required payee on demand. Generally for such kind of transfer payee should have account with the paying bank. Otherwise it is very difficult for the paying bank to recognize the exact payee.

When sending money is urgent then the bank uses telephone for remittance. This service is only provided for valued customers, who is very reliable and with which banks have long standing relationship.

TT (Issue):

- Customer fills up the TT form and pays the amount along with commission in cash or by cheque.

- The respected officer issues a cost memo after receiving the TT form with payment seal, then signs it and at last give it to the customer.

- Next a TT confirmation slip is issued and its entry is given in the TT issue register.

- A test number is also put on the face of the slip. Two authorized officer signs this slip.

- The respective officer transfers the message to the drawee branch mentioning the amount, name of the payee, name of the issuing branch, date, test number and his her power of attorney (P.A.) number.

- The confirmation slip is send by post.

Payment Process of TT:

- Test confirmation

- Confirm issuing branch

- Confirm payee’s account.

- Confirm amount

- Make payment

- Advice sends to the Head Office for reconciliation.

Test Arrangement of TT & DD

Test is the security code by decoding which any branch can be sure that the TT or DD is not forged one. Only the authorized officers know the test code. Each bank maintains secret code for this. That is the test arrangement is the combination of different secret codes

iv. Locker Service:

RBL, Local Office, Dhaka is providing facility of locker service for the purpose of safeguarding the valuable property of customers. The person or organization that has any account in bank branch can enjoy this service. They keep their valuable assets in banker’s custody. Customers have right to look after with a key of their individual locker provided by bank. FSBL maintains the following types of lockers:

▫ Large locker.

▫ Medium locker.

▫ Small locker.

For enjoying this service, clients have to give charge yearly Tk.2500/-, Tk.2000/- and Tk.1500/- for large, medium and small locker respectively.

v. Mail Transfer Advice (MTA)

Where the remitter desires the banker to remit the funds to the payee instead of purchasing a draft himself the banker does it through a mail transfer advice. The payee must have an account with the paying office as the amount remitted in such a manner is meant for credit to the payee’s account and not for cash payment. it is the least used technique for transferring fund. Where there is no telex machine or telephone line then this method is used.

3.4.3 Clearing

Clearing house is an assembly of the locally operating scheduled banks for exchange of cheques, drafts, pay orders and other demand instruments drawn on each other and received from their respective customers for collection. The house meets at the appointed hour on all working days under the supervision of two central bank officers or its agent as the case may be, and works within the regulations framed therefore on the basis of prevailing banking practices. in Bangladesh, clearing house sites at Bangladesh bank where there is no office of the Bangladesh bank, sonali bank acts as agent of Bangladesh bank.

There are mainly two types of clearing systems in Bangladesh, such as:

v internal clearing or inter branch clearing or inward clearing

v external clearing or inter banks clearing or outward clearing

] What is clearing House?

In Bangladesh Bank, there is a very large room, which contains fifty (50) or more tables for each bank that is called the clearing house.

] Nature of clearing house:

1st Clearing House

Return Clearing House

] Clearing House Process:

Every bank has an officer of clearinghouse who works with Bangladesh Bank clearing house. Now a day’s most of clients deposit in their account cheques of different banks. Clearing officer check all the cheques and deposit slip very carefully and then he received the cheque. Then the clearing officer posted all the cheques in computer software which is recognized through computer department of Bangladesh Bank. Clearing officer then seal all the cheques in advance date, makes endorsement on all the cheques.

All the cheques are posted in the computer branch wise, then officer print the entire document and staple all the cheques branch wise, which is called schedule of clearing house. It is a very difficult job to staple all the cheques, because some time’s the cheques are huge in quantity, it may be 250 to 400, this is very vital job, Because every cheque must have to staple very carefully, it means cheque amount and the print sheet amount and cheque branch must have to be same.

If the cheques staple in wrong direction, the cheque may be return from another bank, that’s why FSBL not to be able to credited party account.

Then the clearinghouse officer copying the entire document in two floppy dist as per Bangladesh Bank requirement. When the clearing officers enter the clearinghouse, his first job is that the floppy delivered to the Bangladesh Bank computer department.

All of the procedure the clearing in charge goes to the Bangladesh Bank clearing house before 10 am in the morning. The clearing officer check all the bank’s cheque and he put all the cheques in bank wise, like as this another bank’s delivered there cheques in RBL desk. Then the officers of RBL have to calculate all the cheques by using calculator machine, Staple pin remover, and then he divided all the cheques as RBL Branch wise.

] Types of Clearing Cheque:

RBL Local Office, Dhaka performs the clearing function through Bangladesh Bank. RBL Local Office, Dhaka acts as the agent of all RBL branches for the clearing house of the Bangladesh Bank. There are two types of cheque which are-

1. Inward clearing cheque

2. Outward clearing cheque.

Inward clearing Cheques:

Inward clearing cheques are those ones which have drawn on the other branches of RBL, which will be cleared / honored through the internal clearing system of RBL operated by the Local Office of RBL.

Outward clearing Cheques:

Outward clearing cheques are those ones, which have drawn on the other bank branches which are presented on the concerned branch for collection through clearing house of Bangladesh Bank.

] Reason for the Return Cheques:

Memorandum.

Rupali BANK LIMITED

__________ Branch Date: _____________

Cheque(s) No: _________________ for Taka ________________

Is/are returned un-paid for reason(s) no_____________________

not arrange for

Effects not cleared may be present again.

Exceeds arrangement.

Full neither covers nor received.

Payments stopped by draft.

________ Payee’s endorsement irregular requires bank’s confirmation.

________ Payee’s endorsement irregular, illegible / required.

Draft signature differs / required.

Alteration in Date / figures / words required draft’s full signature.

Cheque is post dated / out of date / mutilated.

Amount in word and figure differs.

Crossed cheque must be presented through a Bank.

clearing stamps required.

Addition to Bank discharge should b authenticated.

Cheque crossed “Account’s Payees Only”.

Collecting Bank discharge irregular.

] Software:

Software called NIKASH supplied by Bangladesh Bank is used in clearing of the cheques and other instruments. The in-charge of clearing section make clearing slip for each cheque through computer using NIKASH and finally this cheques are send to the Bangladesh Bank Clearing –House sorting bank wise.

] OBC/IBC:

By OBC, I mean that those cheques drawn on other banks which are not within the same clearing house. Officer gives OBC seal on this type of cheques and later sends a letter to the manager of the branch of the some Bank located in the branch on which cheque has been drawn. After collection of that bill branch advises the concerned branch in which cheques has been presented to credit the customer account through Inter Branch Credit Advice (IBCA).

In absence of the branch of the same bank, officer sends letter to manager of the bank on which the cheques is drawn. That bank will send pay order in the name of the branch. This is the procedure of OBC mechanism.

Actually OBC comes from the out side bank’s branch, or inter branches. Suppose AGRANI Bank, Jatrabari Branch sent a Cheque, which no: 012536, Tk. 5, 00,000/- to FSBL against AGRANI Bank Motijheel Corp. Branch. So this cheque could be an OBC. Now what FSBL has to do? FSBL tries to collect this cheque through Bangladesh Bank Clearing House, and credited clients account.

3.4.4 Cash

The cash section of any branch plays very significant role in Banking Section. Because, it deals with most liquid assets the RBL, Local Office has an equipped cash section. This section receives cash from depositors and pay cash against cheque, draft, PO, and pay in slip over the counter. Every Bank must have a cash counter where customer withdrawn and deposit there money. When the valued client’s deposit their money at the cash counter they must have to full fill the deposit slip his/her own, then they sing as the depositor option’s then they deposit their money through cash officer at the cash counter.

Several Types of Deposit Slip

There are several types of deposit slip as follows:

Current Deposit A/C Slip,

Saving’s Deposit A/C Slip,

Fixed or Time Deposit A/C Slip,

Other Types of Deposit A/C Slip,

Pay order Slip,

Demand Draft Slip,

T.T. Slip.

After paying this kind’s of slip, the valued client waits for the deposit slip book out side of the cash counter. The cash officer deposit the money in there account through computer software, while the depositors account credited, then the cash officer put a seal in the deposit slip and return it to the client.

Receiving Cash:

Any people who want to have deposit money will fill up the deposit slip and give the form along with the money to the cash officer over the counter. The cash officer counts the cash and compares with the figure written in the deposit slip. Then he put his signature on the slip along with the ‘cash received’ seal and records in the cash receive register book against A/C number.

At the end of the procedure, the cash officer passes the deposit slip to the counter section for posting purpose and delivers duplicate slip to the clients.

Account treatment:

Cash A/C——————— Dr.

Customer’s A/C————- Cr.

Disbursing Cash:

The client who wants to receive money against cheque comes to the payment counter and presents his cheque to the officer. He verifies the following information:

▫ Date of the cheque

▫ Signature of the A/C holder

▫ Material alteration

▫ whether the cheque is crossed or not

▫ whether the cheque is endorsed or not

▫ Whether the amount in figure and in word correspondent or not

Then he checks the cheque from computer for further verification. Here the following information is checked:

▫ whether there is sufficient balance or not

▫ whether there is stop payment instruction or not

▫ whether there is any legal obstruction (Garnishee Order) or not

After checking everything, if all are in order the cash officer gives amount to the holder and records in the paid register.

Account treatment:

Customer’s A/C Dr.

Cash A/C Cr.

The cash section of RBL deals with all types of negotiable instruments, cash and other instruments and treated as a sensitive section of the bank. It includes the vault which is used as the store of cash instruments. The cash limit of the branch is 6 % of demand liability of the branch lack. If the cash stock goes beyond this limit, the excess cash is then transferred to Bangladesh Bank, Dhaka.

3.4.5 Accounts Department

Accounts Department is play most vital role in Banking. Accounts Department is a department with which each and every department is related. It records the profit & loss A/C and statement of assets and liabilities by applying “Golden Rules” of book-keeping. The functions of it are theoretical & computerized based. RBL Local Office records its accounts daily, Weekly and monthly every record.

Functions Provided By Accounts Department:

Like all other Banks, in RBL Accounts Department is regarded as the nerve Center of the bank. In banking business, transactions are done every day and these transactions are to be recorded properly and systematically as the banks deal with the depositors’ money. Any deviation in proper recording may hamper public confidence and the bank has to suffer a lot otherwise. Improper recording of transactions will lead to the mismatch in the debit side and in the credit side. To avoid these mishaps, the bank provides a separate department whose function is to check the mistakes in passing vouchers or wrong entries or fraud or forgery. This department is called as Accounts Department.

Besides the above, the Bank has to prepare some internal statements as Ill as some statutory statements which are to be submitted to the central bank. Accounts Department prepares these statements also. The department has to submit some statements to the Head Office, which is also consolidated by the Head Office late on.

The tasks of the Accounts Department of RBL, Local Office may be seen in two different angles:

(1)Daily Tasks:

The routine daily tasks of the Accounts Departments are as follows——–

o Recording the daily transactions in the cashbook.

o Recording the daily transactions in general and subsidiary ledgers.

o Preparing the daily position of the branch comprising of deposit and cash.

o Preparing the daily Statement of Affairs showing all the assets and liability of the branch as per General Ledger and Subsidiary Ledger separately.

o Making payment of all the expenses of the Branch.

o Recording inter branch fund transfer and providing accounting treatment in this regard.

o Checking whether all the vouchers are correctly passed to ensure the conformity with the ‘Activity Report’; if otherwise making it correct by calling the respective official to rectify the voucher.

o Recording of the vouchers in the Voucher Register.

o Packing of the correct vouchers according to the debit voucher and the credit voucher.

(2)Periodical Tasks:

The routine periodical tasks performed by the department are as follows:

o Preparing the monthly salary statements for the employees.

o Publishing the basic data of the branch.

o Preparing the weekly position for the branch which is sent to the Head Office to maintain Cash Reserve Requirement (C.R.R).

o Preparing the monthly position for the branch which is sent to the Head Office to maintain Statutory Liquidity Requirement (C.R.R).

o Preparing the weekly position for the branch comprising of the break up of sector-wise deposit, credit etc.

o Preparing the weekly position for the branch comprising of the denomination wise statement of cash in tills.

o Preparing the quarterly statements (SBS-2 and SBS-3) where SBS-2 shows “classification of deposits excluding inter bank deposits, deposits under wage earner’s scheme and withdrawals from deposits accounts” and SBS-3 shows “classification of advances (excluding inter bank) and classification of bills purchased and discounted” during the quarter.

o Preparing the budget for the branch by fixing the target regarding profit and deposit so as to take necessary steps to generate and mobilize deposit.

- Preparing an ‘Extract’ which is a summary of all the transactions of the Head Office account with the branch to reconcile all the transaction held among the accounts of all the branches.

Other Activities of Accounts Department:

Transfer

Transfer is not a critical sector in banking but it is very important. Transfers play a vital role in banking sector. So now I have to know what transfer is: basically transfer is a type of register maintaining matter. In this register officer write down every day transactions in Debit and Credit side then the officer calculate both the side of the register if both side shown same amount, it means that the total day’s transaction is completely okay.

Extract:

Extract is a statement of all originating and responding transactions among inter–branches through inter branches debit and credit advice. At the end of the day, all the debit and credit advices of different department come to accounts department. It makes extract in light of all advices.

Actually extract shows the balance of RBL, Local Office general A/C. The objective of preparing it is to know how many transactions have been originated and responded by the respective branch per day. Branch has to send it its Head Office keeping one photocopy.

Statement of affairs:

Accounts section prepares the statement of affairs for finding the profit /loss as Ill as amount of assets and liabilities of concerned branch per day. Theoretically; it is called financial statement and has two parts:

Income and Expenditure A/C.

Statement of assets & liabilities.

Other Parts of General Banking

Transferring account

Account holder may transfer his account from one branch to another branch. For this he must apply to the manager of the branch where he is maintaining his account. Then the manager sends a request to the manager of the branch where the account holder wants to transfer his account for opening the account.

Know your Customer (KYC) Concept.

The officer related to account opening formalities must know details of their customers (depositors and borrowers) because of the guidelines provided by the Central Bank to identify the source(s) of money and use of credit.

It is said in the view of bank that, the banker-customer relationship is commenced through opening CD/STD/SB account. During the period of account opening, the customers must complete the KYC Profile which includes residence address, business address photographs, signatories, photocopy of valid passport, trade license, source of money, TI Number, photocopy of VAT Certificate, In case of company: photocopy of Memorandum of Association, certificate of incorporation, certificate of Board of Investment, list of directors, etc as per requirement of the bank.

Information regarding business pattern, nature of business, and volume of business etc. also to be discovered. Any suspicious transaction must be addressed and find out to take corrective measures as per regulation of the Central Bank.

Dormant account

If any account is inoperative for more then one year is called dormant account. To operate this accounts manager’s permission is necessary.

Crossing

Crossing cheque is written across the face of the cheque within two parallel lines. This practice becomes common even outside of clearing house, as an element of safety.

Normally two types of cheque used in the bank. Such as:

v Open cheque: A cheque, which capable of being paid over the counter in cash is known as open cheque

v Crossed cheque: A cheque, which can only be paid to the banker for crediting the proceeds to the amount of its payee.

Purpose of crossing

v To avoid possible loss that may occur by open cheques getting into the hands of wrong parties

v Crossing is a direction to the paying bank to pay the money generally to a bank or a particular bank, so that,

v It can be easily traced out for whose use the money was received.

Forms of crossing

General crossing

not negotiable

and company and co

not transferable

Special crossing

payees A/C only

not negotiable

Dispatch

Dispatch includes all correspondence, letter, statements and returns and telegrams. this dispatch is also known as Mail. Dispatch is primarily divided into two categories:

Inward: It means what are receives from the outside.

Outward: It means what are sent to the outside.

This dispatch also divided into

(A) ordinary.

(B) Registered and

(C) Local.

Every correspondence should have an office copy and one additional copy is also retained in the Master file of the office.

3.5 Loan and Advances

3.5.1 Cash Credit (Hypothecation):

Hypothecation is a charge on a company for a debt but neither ownership nor possession passes to the creditors. In hypothecation, both ownership and possession remains with the debtor. The change is created by the debtor to the lender on his execution of the document (Letter of Hypothecation). In the said document the debtor binds himself to give possession of the hypothecated goods to the lender, if the lender so requires.

As per the goods remain in the possession of the borrower, bank grant hypothecation facility normally to first party. The bank may also demand security from the party before making advance. It depends mainly upon the trust worthy of the party. Advance is generally allowed against hypothecation of the following:

Raw materials

Stock-in-trade

Finished products

Book debt of the debtor

3.5.2 Cash Credit (Pledge):

Cash credit allowed against pledge of goods is known as CC (pledge).

A letter of pledge is signed by the borrower in favor of the bank.

Pledge means bailment of goods as a security for repayment of debt or performance of a promise.

The bailment must be made by the debtor or indenting debtor of his duly authorized agent.

The ownership of goods remains with the borrower while possession of the goods is transferred to the bank until the debt is repaid.

3.5.3 Overdraft (OD):

The overdraft is a kind of advance always allow on a current account operated upon by cheque. The customer may be sanctioned a certain limit upon which he can overdraw his current account within a stipulated time. The agreed interest is calculated and charged on the debit balances on daily product basis.

3.5.4 Loan Against Trust Receipt (LTR):

This type of loan is allowed to the importer to retire documents and release the consignments from the authority against a trust receipt. The bank get the TR signed by the customer, agreeing to hold the goods or their sale proceeds in trust, for the banker, so long as the entire amount, due to the borrower is not paid off. Validity of LTR may be allowed for 60-90 days time to make payments. Interest is charged on the amount due.

3.6 Project loan

These types of loan are allowed to different industrial units who are interested to establish high profile manufacturing industries. RBL, Local Office, Dhaka generally acts as disbursing agent of RBL, Head Office. After getting proposal from clients to sanction project loan in a specific industrial sector, RBL, Local Office forward the proposal with its recommendation to concern department of RBL, Head Office for approval. If concern department of RBL, Head Office approves the proposal and then they send approval letter to RBL, Local Office. After observing all the formalities, terms and conditions of the approval letter RBL, Local Office then disburses project loan to the deserving client.

3.7 Foreign Exchange

3.7.1 Letter of Credit (L/C):

Documentary credit (DC) is a written undertaking by a bank (Issuing Bank, Opening Bank) to a seller (Beneficiary, exporter) at the request and on the instruction of the buyer (Applicant, Importer) to pay either at sight, if it is a sight bill, DP (Sight) or a determinable future date, if it a term bill, DA (Usance), a stated some of money against stipulated documents and fulfillment of all the term and condition in the DC.

RBL, Local Office, Dhaka provides two types of service on Letter of Credit. They are:

a) Issuance of Import Letter of Credit: At the request of its clients RBL, Local Office issues import L/C for procurement of industrial raw materials and other consumable items.

b) Advising of Export Letter of Credit: RBL, Local Office advises Export Letter of Credit to its exporter clients received from abroad.

3.7.2 Loan against Imported Merchandise (LIM):

In this case advance is made to the importer based on the imported goods as security. When the goods under a documentary credit arrives but where the customer does not wish to effect immediate payment, he can request the bank to effect payment for him and arrange to have the goods stored in the go down under the name of the bank. In case the customer wants to have the goods, he can arrange with the bank to take the delivery of the goods against payment to the bank or against trust receipt.

3.7.3 Foreign Bill Purchased (FBP):

This loan is given to the exporter, after shipment of goods, the exporter present the documents to the banker for negotiation. Sight bill or Term bill might be negotiated by the exporter’s bank. The bill with the shipping documents will be handed to the bank, which will then pay the exporter, but retaining a right of resource of to the exporter in the event that the bills are dishonored.

3.8 Endorsements of passports:

An endorsement is the mode of negotiating, a negotiable instrument. According to the section 15 of the Negotiation Instruments Act, 1881, an endorsement is “when the maker or holder of a negotiable instrument sign the same, otherwise then as such maker, for the purpose of negotiation, on the back of face thereof or on a slip of paper annexed there to….he is said to endorse the same and is called the endorser”

RBL endorses US$ in passports. To endorse US Dollar, the client has to apply in the prescribed from (TM Form).

The following entries are given in this regard:

Cash or Customers’ A/C—————–Dr.

Foreign Currency on Hand< Dollar Special> ———Cr.

3.9 Legal and recovery

This is an important department which plays a vital role for the branch. This department takes initiative for recovery of long outstanding loans or bad loans of the branch. In the process of recovery the department starts communication through correspondents and as well as physically with the defaulter borrowers and let them try convinced to adjust the loans. If this procedure fails to bring fruitful results for the branch, then takes legal measure against the borrowers for recovery of loan.

3.10 SWOT Analysis

SWOT Analysis is basic principle that strategy making efforts must aim at producing a good fit between a company’s resource capabilities (as reflected by its balance of resource strengths and weakness) and its external situation (as reflected by bank and competitive conditions, the bank’s own market opportunity and specific external threats to the bank’s profitability and market standing). Perceptive understanding of a bank’s resource capabilities and deficiencies, its market opportunities and the external threats to its future Ill-being is essential to good strategy-making.

Internal Area | Competitive Strengths and weakness | |

Finance | + | Easy availability of funds from corporate branch for financing trade |

+ | Good turnover | |

– | Deposit is short as compared to loan and advances | |

Management | + | Business efficiency has been achieved by years of experience. |

+ | well trained & skillful employees. | |

+ | Narrow organization structure | |

– | Lack of accountability | |

– | Only few employees possess in-depth competencies | |

Product & Service | + | Competitive interest rate and smooth service |

– | Very few product are available for general customer / narrow product line | |

+ | Efficient in trade services & possess flexible | |

– | No ILC, which can enhance the trade business further | |

– | No online banking service | |

– | Branch has no authority in granting advances without the prior approval from head office or corporate office | |

Control & Communication | + | Low record of defaulters as the advances are made after close scrutiny and proper collateral is obtained |

+ | Regular audit from Head Office & Bangladesh Bank | |

+ | Maintain KYC (Know your Customer) | |

+ | Follow informal communication | |

Technology | + | Computerized Banking |

– | No ATM technology | |

+ | Uses SWIFT | |

+ | Foreign remittance facility through internet | |

+ | Communication facility through e-mail & Internet | |

– | No use of secured data based programmed i.e. SQL/ Oracle | |

Note: “+” indicates Strengths & “-” indicates weakness

External Area | Competitive Opportunities and Threats | |

Economics | + | A strong financial source and ample resources to grow the business |

+ | Increase in trade and remittances | |

– | Commercial activities are not increasing as expected | |

+ | Rapid grow of small & medium enterprises | |

Market & Competition | – | Emergence of more new commercial banks and their branches |

+ | Ability to take advantage of economies of scale and/or learning curve effects, resulting in low cost | |

– | Other banks have competitive standing in terms of creating new product and services | |

– | Follow niche marketing, as such customer base is small | |

+ | Increase the product line can bring more customer | |

+ | Strong brand loyalty among the existing customer | |

Social Communication | + | Better social relationship with clients, not only priority customer but also others |

– | Less media focus (Ad. on TV or Dailies) | |

Technology | + | ATM & online banking service can enhance the existing customer services |

+ | Soon the bank will use MOBS (Multi-user Online Banking Service) thus increasing the security and operation efficiency | |

Branches & Location | + | Center of business area |

Note: “+” indicates Opportunity & “-” indicates Threat

Chapter – 4

Foreign Exchange

4.1 Definition of Foreign Exchange:

Foreign Exchange is a process which is converted one national currency into another and transferred money from one country to another country.

According to Mr. H. E. Evitt. Foreign Exchange is that section of economic science which deals with the means and method by which right to wealth in one country’s currency are converted into rights to wealth in terms of another country’s currency. It involved the investigation of the method by which the currency of one country is exchanged for that of another, the causes which rented such exchange necessary the forms which exchange may take and the ratio or equivalent values at which such exchanges are effected.

Foreign exchange is the rate of exchange in the both country’s currency.

4.2 Foreign Trade and Foreign Exchange:

International trade refers to trade between the residents of two different countries.

Each country functions as a sovereign State with its set of regulations and currency. The difference in the national of the exporter and the importer presents certain peculiar problems in the conduct of international trade and settlement of the transactions arising there from. Important among such problems are:

(a) Different countries have different monetary units;

(b) Restrictions imposed by countries on import and export

Of goods;

(c) Restrictions imposed by nations on payment from and

into their countries;

(d) Differences in legal practices in different countries.

4.3 Foreign exchange means foreign currency and includes:

I. All deposits, credits and balances payable in any foreign Currency and any drafts, traveler’s cheques, letters of credit and bills of exchange, expressed or drawn in local currency but payable in any foreign currency;

II. Any instrument payable, at the option of the drawee or holder thereof or any other party thereto. Either in local currency or in foreign currency or partly in one and partly in the other. Thus, foreign exchange includes foreign currency; balances kept abroad and instruments payable in foreign currency.

4.4 Principles of Foreign Exchange:

The following principles are involved in Foreign exchange:

i) The entire system

ii) The media used

iii) The monetary unit.

4.5 Functions of Foreign Exchange:

The Bank actions as a media for the system of foreign exchange policy. For this reason, the employee who is related of the bank to foreign exchange, especially foreign business should have knowledge of these following functions:

(i) Rate of exchange.

(ii) How the rate of exchange works.

(iii) Forward and spot rate.

(iv) Methods of quoting exchange rate.

(v) Premium and discount.

(vi) Risk of exchange rate.

(vii) Causes of exchange rate.

(viii) Exchange control.

(ix) Convertibility.

(x) Exchange position.

(xi) Intervention money.

(xii) Foreign exchange transaction.

(xiii) Foreign exchange trading.

(xiv) Export and import letter of credit.

(xv) Non-commercial letter of trade.

(xvi) Financing of foreign trade.

(xvii) Nature and function of foreign exchange market.

(xviii) Rules and Regulation used in foreign trade.

(xix) Exchange Arithmetic.

Chapter –5

Letter of Credit (L/C)

5.1 Definition of L/C:

On behalf of the importer if the Bank undertakes to make payment to the foreign bank is known as documentary credit or letter of credit.

A letter of credit is an instrument issued by a bank to a customer placing at the later disposal such agreed sums in foreign currency as stipulated. An importer in a country requests his bank to open a credit in foreign currency in favor of his exporter at a bank in the later country. The letter of credit is issued against payment of amount by the importer or against satisfactory security. The L/C authorizes the exporter to draw a draft under L/Cs terms and sell to a specified bank in his country. He has to hand over to the bank the Bill of exchange, shipping documents and such other papers as may be agreed upon between the exporter and the importer. The exporter is assured of his payment because of the credit while the importer is protected because documents in respect of export of goods have to be delivered by the exporter to the paying bank before the payment is made.

5.2 From of Letter of Credit

A letter of credit (L/C) may be two forms. These are as below:

(i) Revocable letter of credit.

(ii) Irrevocable letter of credit.

5.2.1 Revocable L/C:

If any letter of credit can be amended or canceled by the exporter and without prior consent of importer is known as revocable letter of credit.

A revocable letter of credit can be amended or canceled by the issuing bank at any time without prior notice to the beneficiary. It does not constitute a legally binding undertaking by the bank to make payment. Revocation is possible only until the documents have been honored by the issuing bank or its correspondent. Thus a revocable credit does not usually provide adequate security for the beneficiary.

5.2.2 Irrevocable L/C:

If any letter of credit can not be cancelled or amendment without the consent of both the importer and the exporter is known as irrevocable letter of credit.

An irrevocable credit constitution a firm undertaking by the issuing bank to make payment. It therefore, gives the beneficiary a high degree of assurance that he will paid to his goods or services provide he complies with terms of the credit.

5.3 Types of Letter of Credit:

Letter of Credit is classified into various types according to the method of settlement employed. All credits must clearly indicate in major categories.

(i) Sight payment credit.

(ii) Deferred payment credit.

(iii) Acceptance credit.

(iv) Negotiation credit.

(v) Red close credit.

(vi) Revolving credit.

(vii) Stand by credit.

(viii) Transferable credit.

5.3.1 Sight payment credit :

The most commonly used credits are sight payment credits. These provide for payment to be made to the beneficiary immodestly after presentation of the stipulated documents on the condition that the terms of the credit have been complied with. The banks are allowed reasonable time to examine the documents.

5.3.2 Deferred payment credit :

Under a deferred payment credit the beneficiary does not receive payment when he presents the documents but at a later date specified in the credit. On presenting the required documents, he received the authorized banks written undertaking to make payment of maturity. In this way the importer gains possession of the documents before being debited for the amount involved.

In terms of its economic effect a deterred payment credit is equivalent to an acceptance credit, except that there is no bill of exchange and therefore no possibility of obtaining money immediately through a descant transaction. In certain circumstances, however, the banks payment undertaking can be used as collateral for an advance, though such advance will normally only be available form the issuing or confirming bank. A discountable bill offers wider scope.

5.3.3 Acceptance Credit:

With an acceptance credit payment is made in the form of a term bill of exchange drawn on the issuing Bank. Once he has fulfilled the credit requirements, the beneficiary can demand that the bill of exchange be accepted and returned to him. Thus the accepted bill takes the place of a cash payment.

The beneficiary can present the accepted bill to his own bank for payment at maturity or for discounting, depending on whether or not he wants cash immediately. For simplicities sake the beneficiary usually gives on instruction that the accepted bill should be left in the safekeeping of one of the banks involved until it matures. Bill of exchange drawn under acceptances credit usually has a term of 60-180 days.

The purpose of an acceptance is to give the importer time to make payment. It he sells the goods before payments fall due, he can use the proceeds to meet the bill of Exchange in this way, he does not have to borrow money to finance the transaction.

5.3.4 Negotiation credit:

Negotiation means the purchase and sale of bill of exchange or other marketable instruments. A negotiation credit is a commercial letter of credit opened by the issuing bank in the currency of its own country and addressed directly to the beneficiary. The letter is usually delivered to the addressee by a correspondent bank. This credit is sometimes also as Hand on credit.

The letter of credit empowers the beneficiary to draw a bill of exchange on the using bank, on any other named drawer or on the applicant for the credit. The beneficiary can they present this bill to a bank for negotiation, together with the original letter of credit and the documents stipulated therein.

Payment of the bill of exchange is guaranteed by the issuing bank on the condition that the documents presented by the beneficiary are in order. The most common form of negotiation credit permits negotiation by any bank. In rare case the choice is limited to specified banks.

5.3.5 Red clause credit:

In the case of a red clauses credit, the seller can obtain an advance for an agreed amount from the correspondent bank, goods that are going to be delivered under the documentary credit. On receiving the advances, the beneficiary must give a receipt and provide a written undertaking to present the required documents before the credit expires.

The advance is paid by the correspondent bank, but it is the using bank that assumes liability. If the sellers does not present the required documents in time and fails to refund the advance, the correspondent bank debits the issuing bank with the amount of the advance plus interest. The issuing bank, in turn, has reveres to the applicant, who therefore bears the risk for the advance and the interest accursed.

The clause permitting the correspondent bank to make an advance used to be written on red in home the name red clause credit.

5.3.6 Revolving Credit:

Revolving credit can be used when goods are to be delivered in installment at specified intervals. The amount available at any one time is equivalent to the value of one partial delivery.

A revolving credit can be cumulative or non-cumulative means that amount from unused or incompletely used portions can be carried forward to subsequent period. If a credit is non-cumulative, portions not used in the prescribing period case to be available.

5.3.7 Stand by credit:

Stand by credit are encountered principally in the US. Under the laws of most US states, banks are prohibited from issuing regular quarantines, so credits are used instead. In Europe, too the use of this type of credit is increasing by virtue of their documentary credit, stand-by credit are governed by the UCP. However, their function is that of a grantee.

The types of payment and performance that can be guaranteed by stand-by credits include the following:

– Payment of thorium bill of exchange

– Repayment of bank advance

– Payment of goods delivered.

– Delivery of goods in accordance wets contract and

– Execution of construction contracts, supply and install contracts.

In order to enforce payment by the bank, the beneficiary merely presents a declaration stating that the applicant for the credit has failed to meet his contractual obligation. This declaration may have to be accompanied by other documents.

5.3.8 Transferable Credit:

Transferable credits are particularly well adapted to the requirements of international trade. A trader who receives payment from a buyer in the form of a transferable documentary credit can use that credit to pay his own supplier. This enables him to carry out the transaction with only a limited and lay of his own funds.

The buyer supplies for an irrecoverable credit issued in the traders favour. The issuing bank must expressly designate the credit as transferable. As soon as the trader receives the confirmation of credit he can request the bank to transfer the credit to his supplier. The bank is under no obligation to affect the transfer except in so far as it has expressly consented to do so. The costs of the transfer are usually charged to the trader and the transferring bank is entitled to delete them in advance.

5.4 Parties of Letter of Credit:

A letter of credit is issued by a Bank at the request of an importer in favour of an exporter from whom he has contracted to purchases some commodity or commodities. The importer, the exporter and the issuing bank are parties to the letter of credit. There are however, one or more than one banks that are involved in various capacities and at various stages to play an important role in the total operation of the credit.

5.4.1 The opening Bank.

5.4.2 The Advising Bank.

5.4.3 The Buyer and the Beneficiary.

5.4.4 The paying Bank.

5.4.5 The negotiating Bank.

5.5.6 The confirming Bank.

5.4.1 The opening Bank:

The opening Bank is one that issues the letter of credit at the request of the buyer. By issuing a letter of credit it takes upon itself the liability to pay the bills drawn under the credit. If the drafts are negotiated by the another bank, the opening Bank reimburses that Bank. As soon as the opening Bank, issuing a letter of credit (L/C), it express its undertaking to pay the bill or bills as and when they are drawn by the beneficiary under the credit. When the bills are presented to or when antic is received that bills have been presented to a paying or negotiating Banks its liability matures.

5.4.2 The Advising Bank:

The letter of credit is often transmitted to the beneficiary through a bank in the letters country. The bank may be a branch or a correspondent of the opening bank. The credit is some times advised to this bank by cable and is then transmitted by it to the beneficiary on its own special form. On the other occasions, the letter is sent to the bank by mail or telex and forwarded by it to the exporter. The bank providing this services is known as the advising bank. The advising bank undertakes the responsibility of prompt advice of credit to the beneficiary and has to be careful in communicating all its details.

5.4.3 The Buyer and the Beneficiary:

The importer at whose request a letter of credit is issued is known as the buyer. On the strength of the contract that he makes with the exporter for the purchase of some goods that the letter of credit is opened by the opening bank.

The exporter in whose favour the credit is opened and to whom the letter of credit is addressed is known as the beneficiary. As the seller of goods he is entitled to receive payment which he does by drawing bills under the letter of credit (L/C). As soon as he has shipped the goods and has collected the required documents, he draws a set of papers and presents it with the documents to the opening bank or some other bank mentioned in the L/C.

5.4.4 The paying Bank:

The paying bank only pays the drafts drawn under the credit but under takes no opening bank, by debating the latters accounts with it if there is such an account or by any other measured up, between the two bankers. As soon as the beneficiary has received payment for the draft, he is out of the picture and the rest of the operation concerns only the paying bank and the opening bank.

5.4.5 The Negotiating Bank :

The negotiating bank has to be careful in scrutinize that the drafts and the documents attached there to are in conformity with the condition laid down in the L/C. Any discrepancy may result in refused on the part of the opening bank to honor the instruments is such an eventuality the negotiating bank has to look back to the beneficiary for refund of the amounts paid to him.

5.4.6 The Confirming Bank:

Sometimes an exporter stipulates that a L/C issued in his favour be confirm by a bank in his own country. The opening this country to add its confirming to the credit the bank confirming the credit is known as the confirming bank and the credit is known as confirmed credit.

5.5 Contents of the Letter of Credit:

Banks normally issued letter of credit (L/C) on forms which clearly indicate the banks name and extent of the banks obligation under the credit. The contents of the L/C of different Banks may be different .In general L/C contains the following information:-

5.5.1 Name of the buyer:

Who is also known as the accounted since it is for his account that the credit has been opened.

5.5.2 Nameof the seller:

Who is also known as the beneficiary of the credit?

5.5.3 Amount of the credit:

Which should be the value of the merchandise plus any shipping charges intent to be paid under the credit?

5.5.4 Trade terms:

Such as F.O.B and CIF

5.5.5 Tenor

Tenor of the Draft which is normally dependent upon the requirements of the buyer.

5.5.6 Expiration date:

This is specified the latest date documents may be presented. In this manner or by including additionally a latest shipping date, the buyer may exercise control over the time of shipment.

5.5.7 Documents required:

Which will normally include commercial invoice consular or customer’s invoice, insurance policies as certificates, if the source is to be effected by the beneficiary and original bills of lading?

5.5.8 General description of the merchandise:

This briefly and in a general manner duly describes the merchandise covered by a letter of credit.

Chapter – 6

Foreign Trade Financing(Import) of RBL

6.1 Import trade control & registration With C.C.I & E

In almost all the countries of the world there is import trade control in one form or other which supervises the import into the country and controls certain items of exports depending upon national exigencies. The main object of the import trade control is to conserve the scarce foreign exchange resources of the country with a view to meeting the needs of development of its expending economy. In Bangladesh the import of goods is regulated by the Ministry of commerce in terms of import and export (Control) Act, 1950; with import policy orders issued which is valid for five years, and Public Notices issued from time to time by Chief Controller of Imports and Exports (C.C.I & E), while payments of these imports are regulated by Central Bank, i.e., Bangladesh Bank, through its Exchange Control Policy Department. So, Import Trade Control and Exchange Control are complementary and supplementary to each other.

According to the Imports and Exports (Control) Act, 1950 as adopted in Bangladesh, any one willing to carry import business needs registration with the licensing authority, i.e., Chief Controller of Imports and Exports and its offices at the important trade centers of the country.

The following documents are required to be submitted to the licensing authority for registration as importers.

I. Questionnaire form duly filled in and signed

II. Tax Identification Number (TIN) certificate

III. Trade License from the City/Municipal Corporation or Local Authority

IV. Bank solvency certificate

V. Nationality certificate

VI. Partnership Deed where applicable

VII. Certificate of Registration with the Registrar of Joint Stock Companies and Memorandum & Article of Association in case of Private and Public Ltd. Co.

VIII. Membership Certificate from the Chamber of Commerce/Registered Trade Association

IX. Ownership documents or rent receipts of the place of business

X. Any other documents required under the relevant import policy.

On receipt of the application along with relative documents, the Chief Controller of Imports and Exports and its regional offices scrutinizes the documents and conducts physical verification (if considered necessary) and on being satisfied, requests the applicant to pay fees towards registration through treasury challan.

After submission of the above documents and payment of requisite fees, if the documents are found in order and the C.C.I& E are satisfied, the Import Registration Certificate (IRC) is issued to the applicant I.E. Importer.

The IRC is a security document issued under embossing seal and duly signed by authorized officials of C.C.I & E and to be kept under safe custody. The IRC is required to be renewed every year on payment of usual fees.

6.2 Licensing for import

Most imports into Bangladesh require a license from the licensing authority; from 1983-84 shipping period the procedure have been liberalized. Commercial Banks have been entrusted with the responsibility of licensing imports in both industrial and commercial sectors. Licensing is done by commercial banks by means of specially designed from known as Letter of Credit Authorization Forms simply LCAF. LCA Forms are security documents printed by the respective bank. Bankers must not hand over these to others. This form is in reality a substitute for the conventional import license.

The following documents are required to be submitted by the importer to his banker for licensing:

I. The LCA Form properly filled in quintuplicate signed by the importer.

II. L/C Application duly signed by the importer.

III. Purchase contract, i.e., indent for the goods issued by an indentor or proforma invoice as the case may be.

IV. Insurance cover note.

V. Membership certificate from a recognized Chamber of Commerce and Industry or Town Association or registered Trade Association.

VI. Proof of payment of renewal fees for the Import Registration Certificate.

VII. A declaration in triplicate, that the importer has paid income-tax or submitted income-tax return for the preceding year.

VIII. In case of Public Sector, attested photocopy of allocation letter issued by the allocation authority, Administrative Ministry or Division specifying the source, amount, purpose, validity, and other terms and conditions against the imports.

IX. Any such documents as may be required as per instruction issued/ to be issued by Chief Controller of Imports & Exports from time to time.