INTRODUCTION OF TOPIC:

This internship is a part of the Bachelor of Business Administration (BBA) program that provides an acquaintance of real working environment to students. I was placed at Trust Bank Limited, Dhanmondi Branch as an internee for three months. My respective Supervisor has given me the topic “General Banking Operations of Trust Bank Limited.” This internship program was my very first on-the-job exposure and provided me with learning experience and knowledge in several areas. During the first few weeks of my internship period, I was able to get accustomed to the working environment of the bank. As the internship continued, I not only learned about the activities and operations of correspondent Bank, but I also gathered some knowledge about the basic business activities of banking in first one-month of my internship period.

Generally by the word “Bank” we can easily understand that the financial institution deals with money. But there are different types of banks such as; Central Banks, Commercial Banks, Savings Banks, Investment Banks, Industrial Banks, Co-operative Banks etc. But when we use the term “Bank” without any prefix, or qualification, it refers to the ‘Commercial banks’. Commercial banks are the primary contributors to the economy of a country. So we can say Commercial banks are a profit-making institution that holds the deposits of individuals & business in checking & savings accounts and then uses these funds to make loans. Both general public and the government are dependent on the services of banks as the financial intermediary. As, banks are profit-earning concern; they collect deposit at the lowest possible cost and provide loans and advances at higher cost. The differences between two are the profit for the bank.

Efficacy of customer service is related with progression of operation. We can identify the efficacy of customer service by studying the progress of “Trust Bank Ltd.” from starting to at present. The progress of “The Trust Bank Ltd.” is very rapid with the concern of its profit making and growth of its operation within the country towards the country’s economy.

Trust Bank Limited pursues decentralized management policies and gives adequate work freedom to the employees. This results in less pressure for the workers and acts as a motivational tool for them, which gives them, increased encouragement and inspiration to move up the ladder of success. Overall, I have experienced a very friendly and supporting environment at TBL, which gave me the pleasure and satisfaction to be a part of them for a while. While working in different departments of this branch I have found each and every employee too friendly to me to co-operate. They have discussed in details about their respective tasks. I have also participated with their works.

RATIONAL OF THE STUDY:

The BBA program is designed to focus on theoretical and professional development of the students to take up business as a profession as well as service as a career. It is designed with an excellent combination of theoretical and practical aspects. The Internship program provides the students to link their theoretical knowledge into practical fields.

Internship program is essential for every student, especially for the students of Business Administration, which helps them to know the real life situation. For this reason a student takes the internship program at the last stage of the degree, to launch a career with some practical experience. As a Complete fulfillment of Internship Program introduce the students with the real life business situation

This report is a part of my academic program. The internship program has been set for three (3) months period at “Trust Bank Ltd” as a part of my BBA program. In our BBA Program all courses based on theoretical and we have to learn practically. The program has helped me a lot to understand the organizational atmosphere and behavior and I gather some practical Knowledge about “General Banking Operation of Trust Bank Ltd.”

OBJECTIVE OF THE STUDY:

The objective of the Internship program is to familiarize students with the real market situation, to compare them with the business theories & at the last stage make a report on assigned task. The main objective of this report is to have an assessment about overall activities of “Trust Bank Ltd.”. How the Bank is providing facilities to its clients & to suggest remedial measure for the development of overall banking activities of “TBL”. In addition, the study seeks to achieve the following objectives:

SPECIFIC OBJECTIVE:

- To present an overview of “ Trust Bank Ltd. ”

- To get an overall idea of banking operation from banker’s point of view.

- To study deposit mobilization mechanism and the performance of “Trust Bank Ltd” in terms of deposit mobilization

- To study the investment mechanism and evaluate the performance of “TBL.”

- To understand the recent complexity of banking in Money Laundering. And

- To understand the issue of corporate governance in the banking sector and highlighting the product of “TBL”.

- To identify the limitations in the operation of “Trust Bank Ltd.”

- To recommending some guidelines to improve the overall banking performance of “TBL”

SCOPE OF THE REPORT:

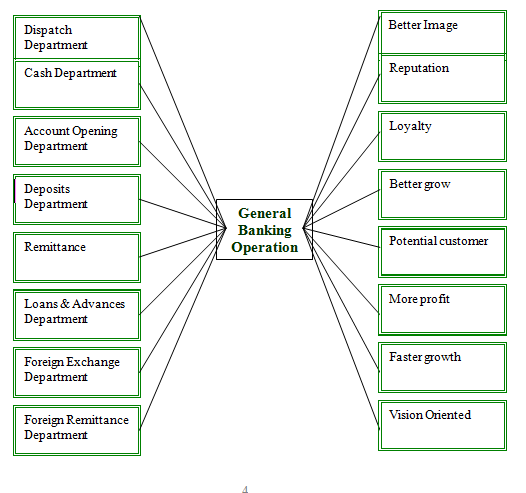

This internship report covers all the trade related products handled by the “Trust Bank Ltd.” such as Foreign Exchange, Cash Dept., Dispatch, Account Opening, Remittance, Accounts, Administration and Loans & Advances etc.

This report has been prepared through extensive discussion with bank employees and with the customers. While preparing this report, I had a great opportunity to have an in depth knowledge of all the banking activities practiced by the “Trust Bank Ltd.” It also helped me to acquire a first hand perspective of a leading private Bank in Bangladesh.

Data collection procedure:

This report is the output of 6 weeks long internship program by analyzing the qualitative information collected from secondary sources that contain past and present facts and figures, and conditions of the Trust Bank Limited. This report is based on both primary & secondary information. Majority of the information was collected from secondary sources.

Primary Sources:

- Conversations with officers & employees of the branch.

- Interactions with the customers at TBL.

Secondary sources:

- Annual reports,

- Official documents,

- Relevant books

- Journals, and other publications

- Term papers of TBL Training manuals

- Internet & various web sites of TBL.

- Prior research report.

CONCEPTUAL FRAMEWORK OF THE REPORT:

LIMITATIONS:

The present study was not out of limitations. But it was a great opportunity for me to know the banking activities of Bangladesh specially “Trust Bank Ltd.” Some constraints are appended bellow—

- The main constraint of the study is inadequate access to information, which has hampered the scope of analysis required for the study. As it is a new bank it could not start all its operation, it was unable to provide some formatted documents data for the study.

- Due to time limitations many of the aspects could not be discussed in the present report.

- Every organization has their own secrecy that is not revealed to others. While collecting data i.e. interviewing the employees, they did not disclose much information for the sake of the confidentiality of the organization.

- Another problem is that creates a lot of confusions regarding verification of data.

- The clients were too busy to provide me much time for interview.

- I have had no opportunity to compare the general banking system of the TBL with that of other contemporary and common size banks. It was mainly because of the shortage of time and internship nature.

CHAPTER TWO

COMPANY OVERVIEW:

BACKGROUND OF “TRUST BANK LTD:

The Trust Bank Ltd. is a private, commercial, scheduled Bank, which obtained license from Bangladesh Bank on July 15, 1999. Presently Army Welfare Trust is the major shareholder. The authorized capital of the Bank is Taka two thousand million and paid-up capital of Taka five hundred million. The Bank was formally inaugurated and listed as a scheduled Bank on November 1999.

The idea of setting up a Bank by Bangladesh Army was first conceived in 1987 and on November 29, 1999 the first branch of the Trust Bank Ltd came in to operation.

Composition of the Board of TBL consists of Ex-officio Directors of in-service senior Army personnel, with the Chief of Army Staff as its Chairman and the Adjutant General as its Vice-Chairman.

The Trust Bank Ltd. having a spread network of 35 branches across Bangladesh and plans to open few more branches to cover the important commercial areas in Dhaka, Chittagong, Sylhet and other areas in 2008. The Bank sponsored by the Army Welfare Trust (AWT), is first of its kind in the country with a wide range of modern corporate and consumer financial products. The Trust Bank Ltd. has been operating in Bangladesh since 1999 and has achieved public confidence as a sound and stable Bank.

In addition to ensuring quality Customer services related to general banking the bank also deals in Foreign Exchange transactions. In the mean time the bank has extended credit facilities to almost all the sector of the country’s economy. The bank has plans to invest extensively in the country’s industrial and agricultural sectors in the coming days.

It has also plans to promote the agro-based industries of the country. The bank has already participated in syndicated loan agreement with other banks to promote textile sectors of the country. Such participation would continue in the future for greater interest of the overall economy. Keeping in mind the client’s financial and banking needs, the bank is engaged in constantly improving its services to the clients and launching new and innovative products to provide better services towards fulfillment of growing demands of its customers.

CORPORATE INFORMATION AT A GLANCE:

- Banking License received on : 15th July. 1999

- Certificate of incorporation received on : 17th June 1999

- Certificate of Commencement of business received on : 17th June 1999

- First branch licenses on : 9th August 1999

- Formal inauguration on : 29th November 1999

- Sponsor Shareholders : Army Welfare Trust

- Number of Branch : 35

NATURE OF BUSINESS:

The Trust Bank Ltd offers full range of banking services that include:-

- Deposit banking

- Loans & advances

- Export

- Import

- Financing inland

- International remittance facilities

The bank offers a full scale commercial banking includes:–

- Foreign Exchange transactions

- Personal

- Credit

- Consumer & Corporate Banking

The bank has plans to invest extensively in the country’s industrial and agricultural sectors in the coming days. The bank has participated in syndicated loan agreement with other banks. Such participation would continue in the further for greater interest of the overall economy. The bank is keen to constantly improve its services to the clients and launching new & innovative products to provide better services towards fulfillment of growing demands of its customers.

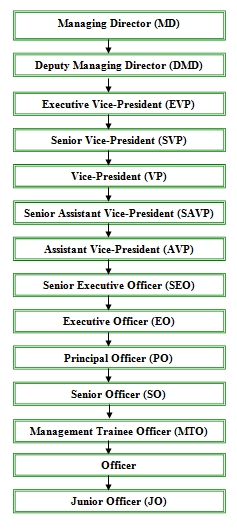

BOARD OF DIRECTORS:

Chairman

General Moeen U Ahmed, ndc, psc

Chief of Army Staff, Bangladesh Army

Vice Chairman

Maj Gen Md Matiur Rahman, ndu, psc

Adjutant General, Bangladesh Army

Directors:

Brig Gen Md Zillur Rahman, MCPS, MSC

Brig Gen S M Mahbubul Karim

Brig Gen Md Rafiqul Islam, ndc, psc

Brig Gen Mohd Mahbubul Hasan, ndc, psc

Brig Gen Md Aminul Hasan, ndc, psc

Professor Md. Abdullah

Managing Director:

Mr. Iqbal U Ahmed

Company Secretary:

Mr. Farhad Uddin

Organizational Structure of Trust Bank Ltd.

Vision Statement of “Trust Bank Limited:

- To build a sustainable and respectable financial institution.

- To be a leading Commercial Bank, with a social focus, assisting in the economic development of the country.

- The Profit of the bank used for the Socio-economic development of the members of the Bangladesh Army and thereby the nation as a whole.

Mission Statement of “Trust Bank Limited:

- Achieving sound and profitable growth in Assets & Liabilities, with focus to maintain non-performing assets at acceptable levels.

- To build long-lasting, credible and mutually dependable relationships with customers.

- Efficiently managing interest and operating costs.

- To excel in rendering superior customer service.

- To be the preferred employer among Banks in Bangladesh.

Branches:

The bank now continues its operation with 35 branches across the country mainly in Dhaka, Chittagong, Jessore, Sylhet, Sirajgong and Mymensingh. The district wise pictorial presentation of the branches appears as follows:

Thirty Five branches of Trust Bank Limited are located in the following areas:

Branch ID | Branch Name | Branch Address | Branch Phone Number |

0001 | Head Office | Peoples Insurance bhaban | 9570261,9570263, |

0002 | Principal Branch (PB) | 98 Shaheed Sarani, | 9871074,9871095,9888068 |

0003 | Sena Kalyan Bhaban (SKB) | Sena Kalyan Bhaban, 195, Motijheel C/A, Dhaka-1000 | Chief Manager : 7121263 |

0004 | Bogra Cantonment Branch | Bogra Cantonment, | 01730-056422, |

0005 | Comilla Cantonment Branch | Comilla Cantonment, | 01713-102834, |

0006 | CTG Cantonment Branch | Bangladesh Tea Board Bhaban | 031-2581170(T&T-PABX) 031-2581171(T&T-PABX) 031-2581172(Fax) 031-683680(Direct) 031-681551-9,Ext-3178(Army) 01914403178(Mobile) 01713400503(Mobile) |

0007 | Rangpur Cantonment Branch | Rangpur Cantonment, | 01713-201661,0521-66653 |

0008 | Jessore Cantonment Branch | Jessore Cantonment | 01713-400503,0421 61043 |

0009 | Mymensingh Cantonment Branch | Mymensingh Cantonment Branch Mymensingh. | 01713-039178,091 55601-3 |

0010 | Saver Cantonment Branch | Saver Cantonment, Saver, Dhaka | 01713-034198, 01715407266, |

0011 | Jalalabad Cantonment Branch | Jalalabad Cantonment Branch | 01713-046337,0821-2872135, 710001-6 |

0012 | Agrabad Branch | 109 Shilpa Bank Bhaban , Chittagong | 01713-104241, 031-720188, 031 814462-3 |

0013 | Shaheed Salauddin Cantonment Branch | Shaheed Salauddin Cantonment, | 01713-007399, |

0014 | Dhanmondhi Branch | BDR Gate No – 4, PeelKhana , BDR | 0171-3014641 |

0015 | Khatungonj Branch | 205, Main Road, Plot No- 218, | 01713-103481,031 627860, |

0016 | Gulshan Corporate Branch | 110 Gulshan Avenue, Dhaka | 0171-30360174, 8828088, |

0017 | Dilkusha Corporate Branch | Peoples Insurance Bhaban | 0171-3062127, 9560944 |

0018 | Raddisson Branch | Airport Road, Joar Sahara, Dhaka | 07173-090078, 8752066, |

0019 | Khaja Yunnis Ali Medical College & Hospital Branch | Enayetpur, Sirajgonj | 01713-047399, 01710660415 |

0020 | CDA Avenue Branch | Holding No – 1827(New), | 01713- 043157, |

0021 | Sylhet Corporate Branch | BMA Bhaban, Chowatta, Kotoewali, | 0171- 3300298, |

0022 | Millenium Branch | Beer Shrestho ShaheedJahangir | 01713-034197, 02 87120756, |

0023 | Uttara Branch | Holding 111/A (Ground & 1st floor) | 07173-062127, 8911052 |

0024 | Halishahar Branch | Monirat Plaza, 230/A, Block – G | 01819-313708, |

0025 | Biani Bazar Branch | Al Amin Super Market | 01716-929400 |

0026 | Moulovibazar Branch | Holding-10, Court Road, | 01713-129265, |

0027 | Goala Bazar Branch | Hazi Nasirullah Market (1st floor) | 0171068371, 01715-747091 |

0028 | Mirpur Branch | Road – 3 Block – A, Section – 11 | 9008310, 9008218, 9008310 |

0029 | Naval Base | BNC, Isha Khan, naval Base | 0171-3452830, 031 747833, 741834 |

0030 | Kawran Bazar | Zenith Tower, 40, Kawran Bazar | 0171- 3041420 |

0031 | Feni | Kazi Center , Holding – 106 | 0171- 1123463, 033163535 |

0032 | Joypara Branch | Ashan Ali Moshan Ali Shooping Complex , | 01716 – 274920, 03894680402, |

0033 | Joydebpur Branch | Vaowal Point | 01713007399 |

0034 | Narsingdi Branch | Salam Mension, Holding 13/9 | 01713- 0057305 |

0035 | Narayangonj Branch | 1 No.B.B. Road, Alam Khan Road (ist & 2nd Florr ) | 7648283 |

CHAPTER THREE

OVERALL BANKING ACTIVITIES OF TRUST BANK LTD.

General Banking:

General banking department is the heart of all banking activities. This is the busiest and important department of a branch, because funds are mobilized, cash transactions are made; clearing, remittance and accounting activities are done here.Since bank is confined to provide the services everyday, Following departments are under general banking section.

1) Account opening section

2) Deposit section

3) Cash section

4) Remittance section

5) Clearing section

ACCOUNT OPENING DEPARTMENT:

A bank has to maintain different types of accounts for different purposes. Trust Bank limited (TBL) offers the general deposit products in the form of various accounts.

Account Opening Procedure in a flow chart:

3.1.2 SAVINGS ACCOUNT (SB)

Savings bank deposit is popular account maintained in Banks. The different matters relating SB account are described in the following discussion. The summary of the rules and regulations to open a savings account is as follows:-

- Any person or persons of more than 18 years having sound mind can open and operate this account singly or jointly.

- In case of a minor (a person below 18 years), a guardian can open and operate this account on his or her behalf.

- Clubs, Societies, Sole Proprietorship firms, Partnership firms, Limited Companies either public or private and other similar organization are eligible to open such account.

- More than one account cannot be opened in the same name.

- A minimum initial deposit of Tk. 1000.00 is required to open such account. And the interest rate of SB account is 7.00%

- Money will be withdrawn through cheque. Withdrawal cannot be more than twice a week and generally the amount will not be more than 25% of the balance available, subject to maximum Tk. 20,000.00.

- In case of closure of any account, the bank deducts Tk. 100.00 as closing charge.

CURRENT ACCOUNT AND SHORT TERM DEPOSIT (STD) ACCOUNT:

Most businessmen maintain Current Deposit accounts in order to make their daily business activities. This account’s funds change most frequently than any other accounts because customers use to withdraw and deposit funds in regular basis. The summary of the rules and regulations to open a current account & short term deposit (STD) account as follows:-

- A minimum deposit of Tk. 5000.00 is needed to open a current account.

- The bank charges an incidental charge of Tk 150.00 for every six (6) months for the maintenance of the account.

- In case of the closure, the bank charges Tk. 100.00 as closing charge of the account.

- Withdrawal of money is allowed only through the leaves of the cheque book issued by the bank.

FIXED DEPOSIT ACCOUNT:

The bank allows people to keep their idle money secured and profitable as Fixed Deposit. The interest rate that the bank offers to the fixed depositors is as follows:

SL No | Amount or Slab wise Deposit | Interest rate on Deposit: Maturity wise but based on amount | |||

1 Month | 3 Months | 6 months | 1 Year and above | ||

| 01. | Any amount but less than Tk 5 crore. | 10.00% | 11.50% | 12.00% | 12.00% |

| 02. | Tk 5 crore & above but less than Tk. 10 crore. | 11.00% | 11.25% | 12.00% | 12.00% |

| 03. | Tk 10 crore & above but less than Tk. 25 crore | 11.00% | 11.25% | 12.00% | 12.00% |

| 04. | Tk. 25 crore and above | 11.00% | 11.25% | 12.00% | 12.00% |

| * Subject to 10% government tax on interest earnings.

| |||||

The Bank deducts the Excise duty, the compulsory levy of the government, on the interest earnings in the following structure:

Minimum Deposit | Maximum Deposit | Excise Duty |

10,001 | 1,00,000 | 120.00 |

1,00,001 | 10,00,000 | 250.00 |

10,00,001 | 1,00,00,000 | 550.00 |

1,00,00,001 | 5,00,00,000 | 2500.00 |

5,00,00,001 | 99,99,99,99,999 | 5000.00 |

DOCUMENTS REQUIRED FOR OPENING ACCOUNT:

To open a savings, current, STD account, the following documents are mandatory:

a) FOR INDIVIDUAL ACCOINT:

- Two copies of Passport size Photograph of the Clients (Attested by introducer or Verified with Passports)

- Passports/ National Identity Card / Employer’s Certificate of the Proprietor.

- Customer Profile.

- Transaction Profile.

- Photograph of the Nominee(s) attested by the account holder.

- TIN Certificate.

- Introducer.

b) FOR JOINT ACCOUNT:

- Passports/ National Identity Card / Employer’s Certificate of the Proprietor.

- Two copies of Passport size Photograph of the Clients.

- Customer Profile.

- Transaction Profile.

- Photograph of the Nominee(s) attested by the account holder.

- TIN Certificate.

- Relationship between the account holders.

- Purpose of opening of the Joint account.

- Introducer.

c) FOR PROPRIETORSHIP ACCOUNT:

- Two copies of Passport size Photograph of the proprietor

(Attested by introducer or Verified with Passports)

- Passports/ National Identity Card / Employer’s Certificate of the Proprietor.

- Customer Profile.

- Transaction Profile.

- Photograph of the Nominee(s) attested by the account holder.

- TIN Certificate.

- Trade License.

- VAT Registration (if available)

d) FOR PERTNERSHIP CONCERN:

- Two copies of Passport size Photograph of each partner (Attested by introducer or Verified with Passports)

- Passports/ National Identity Card.

- Company Profile.

- Transaction Profile of the concern.

- Personal Profile of the partners.

- Photograph of the Nominee(s) attested by the account holder.

- TIN Certificate.

- Trade License of the concern.

- VAT Registration (if available)

- Relationship between the partners.

- Attested Photocopy of the Partnership Deed (Deed on Tk 1000.00 stamp)

- Resolution regarding opening and operation of the account.

e) FOR COMPANY ACCOUNT:

- Attested or Certified copy of the Memorandum and Articles of Association.

- Certificate of Incorporation.

- Certificate of Commencement of Business.

- Two copies of Passport size Photograph of all Directors (Attested by introducer or Verified with Passports)

- Passports/ National Identity Card of all Directors of the company.

- Company Profile.

- Transaction Profile of the company.

- Personal Profile of all Directors as per enclosed sheet in the Company’s letterhead pad.

- TIN Certificate.

- Trade License.

- VAT Registration (if available).

- Board resolution of the company regarding opening and operation of the account.

f) FOR PRIVATE SCHOOL/COLLEGE/MADRASA:

- Attested or Certified copy of the Constitution.

- Registration Certificate.

- List of all Executive Members (as per enclosed format).

- Two copies of Passport size Photograph of the account operators (Attested by introducer or Verified with Passports)

- Passports/ National Identity Card of the account operators.

- Personal Profile of all members of the governing body and Managing Committee.

- Board resolution regarding opening and operation of the account.

g) FOR NGO/ CLUB-SOCIETY/CO-OPERATIVE ACCOUNT:

- Registration Certificate from the Joint Stock Company/ Ministry of Social Welfare.

- List of all Executive Members (as per enclosed format).

- Board resolution as per Memorandum regarding opening and operation of the account.

- Attested or Certified copy of the Constitution/Bylaws.

- Two copies of Passport size Photograph of all Members (Attested by introducer or Verified with Passports)

- Passports/ National Identity Card of all Members.

- Profile of the Firm.

h) Minor’s Account:

- Putting the word “MINOR” after the title of the account (with red color).

- Recording of the special instruction of operation of the account.

The AOF is to be filled in and signed by either the parents or the legal guardian appointed by the court of law and not by the minor.

“No Objection Certificate” from the Ministry of Social Welfare.

Issuing Cheque Book to the Customer:

(A) Issue of fresh checkbook:

Fresh checkbook is issued to the account holder only against requisition on the prescribed requisition slip attached with the checkbook issued earlier, after proper verification of the signature of the account holder personally or to his duly authorized representative against proper acknowledgment.

Procedure of issuance of a fresh chequebook:

A customer who opened a new a/c initially deposits minimum required money in the account.

The account opening form is sent for issuance of a chequebook

Respected Officer first draws a chequebook

Officer then sealed it with branch name.

In-charge officer enters the number of the cheque Book in Cheque Issue Register.

Officer also entry the customer’s name and the account number in the same Register.

Account number is then writing down on the face of the Cheque Book and on every leaf of the Chequebook including Requisition Slip.

There is a special technique to sign every leaf of the chequebook with the help of carbon paper. So officer’s signature prints the reverse side of the leaf.

The name of the customer is also written down on the face of the Chequebook and on the Requisition slip.

Issue of Duplicate checkbook:

Duplicate checkbook instead of lost one should be issued only when an A/C holder personally approaches the Bank with an application Letter of Indemnity in the prescribed Performa agreeing to indemnify the Bank for the lost checkbook. Fresh check Book in lieu of lost one should be issued after verification of the signature of the Account holder from the Specimen signature card and on realization of required Excise duty only with prior approval of manager of the branch. Check series number of the new checkbook should be recorded in ledger card and signature card as usual. Series number of lost checkbook should be recorded in the stop payment register and caution should be exercised to guard against fraudulent payment.

Issue of New Cheque book (FOR OLD ACCOUNT):

All the procedure for issuing a new Chequebook for old account is same as the procedure of new account. Only difference is that customer has to submit the requisition slip of the old Chequebook with date, signature and his/her address. Computer posting is then given to the requisition slip to know the position of account and to know how many leaf/leaves still not used. The number of new Chequebook is entered on the back of the old requisition slip and is signed by the officer.

Procedure of issuance of a new chequebook:

If the cheque is handed over to any other person then the account holder the bank addressing the account holder with details of the Chequebook issues an acknowledgement slip. This acknowledgement slip must be signed by the account holder and returned to the bank. Otherwise the bank will not honor any cheque from this chequebook. At the end of the day all the requisition slips and application forms are sent to the computer section to give entry to these new cheque.

NEW DEPOSIT PRODUCTS:

To keep in touch with competitive market, the bank has recently introduced four attractive deposit products. The products having their distinctive have already gained and are gaining the response from the existing and prospective clients. The products are as follows:

TRUST SMART SAVERS SCHEME (TSSS):

Under the TSSS, the following category of deposit and maturity payment has been declared:

Monthly Deposit | Amount Payable at Maturity (3 years) | Amount Payable at Maturity (5 years) | Amount Payable at Maturity (7 years) | Amount Payable at Maturity (10 years) |

500 | 20,897 | 38,514 | 59,801 | 1,00,000 |

1,000 | 41,794 | 77,027 | 1,19,601 | 2,00,000 |

2,000 | 83,588 | 1,54,055 | 2,39,202 | 4,00,000 |

3,000 | 1,25,380 | 2,31,100 | 3,58,800 | 6,00,000 |

4,000 | 1,67,170 | 3,08,100 | 4,78,400 | 8,00,000 |

5,000 | 2,08,970 | 3,85,100 | 5,98,000 | 10,00,000 |

RULES AND REGULATION:

- The maximum number of TSSS account from a single family can not exceed five.

- The first installment is to be deposited on any date of the month but the subsequent installment is to be deposited by the 10th day.

- Advance payment of three installments is acceptable.

- One copy of Passport size Photograph of the account holder is needed to open TSSS.

- One copy of Passport size Photograph of the Nominee(s) [attested by the account holder] is also required.

- In the event of failure of to pay installment, the arrear installment(s) should be paid before or along with the next due installment subject to the penalty of Tk. 50.00 for per installment to be paid.

- In case of premature closure of the account, Tk 100.00 is charged as closing charge.

- Loan may be allowed up to 80% of the deposited amount but not below Tk 1, 00,000.00 against lien or pledge of the same account.

- Any account can be transferred from any branch to another subject to Tk. 25.00 as Account transfer fee.

In any installment remains unpaid for six consecutive months, the account will be closed automatically and the account will be settled as below:

| Different duration Treatment | Applied rate of Interest |

| Less than six month | No interest |

| More than six month but less than three years | Prevailing interest rate on Savings Account |

| More than three years but Less than five years | Matured value of three years and rest as per the prevailing interest rate on Savings Account |

| More than five years but Less than seven years | Matured value of five years and rest as per the prevailing interest rate on Savings Account |

| More than seven years but Less than ten years | Matured value of seven years and rest as per the prevailing interest rate on Savings Account |

TRUST DIGOON LAABH SCHEME (TDLS):

Under the Scheme, the amount deposited at the very inception is doubled in 7 years. The basic structure of this Scheme is as follows:

Deposit Value | Matured Value | Year | Effective Rate of Interest (EAI) |

| 10,000.00 or multiple thereof | Double of the deposited amount | 7 years | 10.40% |

SOURCE: From interview with the In-charge of FDR department of Trust Bank Ltd, Dhanmondi Branch.

The bank lags behind in this project. Other contemporary banks offer the scheme with a maturity period of 6 years that result in the Effective Interest Rate (EAI) of 12.25%.

TRUST MONEY MAKING SCHEME (TMMS):

Under the Scheme, the client has to pay a down payment of Tk 7,500.00 or multiple thereof and the bank contributes Tk 42,500.00 or multiple thereof to form a fixed deposit of Tk 50,000.00 or multiple thereof with the bank. The client is allowed an interest rate of 10.00% on that deposit. The client has to pay the amount due to the bank through monthly equal installment of Tk 855.00 or multiple thereof in 6 years. The client is entitled to get the interest on FDR.

Summary of the scheme

| Client’s Own Deposit | Tk 7,500.00 or multiple thereof |

| Bank’s Contribution | Tk 42,500.00 or multiple thereof |

| FDR Value | Tk 50,000.00 or multiple thereof |

| Tenor | 6 years |

| Installment Size | Tk 855.00 or multiple thereof |

| Interest Size | 10.00% |

TRUST EDUCATION SCHEME (TES):

The TES has been introduced to assist the poor students financially and chronologically. Under the scheme, a student may deposit Tk 10,000.00 for a period of three or five years. After the maturity period he or she may get a lump-sum amount of Tk 13,400.00 (for three years maturity) or Tk 16,000.00 c or he/she may get monthly education allowance of Tk 430.00 (for three years maturity) or Tk 520.00 (for three years maturity) for a period of three years after maturity.

Summary of the scheme:

Term | Deposit Amount | Monthly education allowance after maturity of 3 years continuity | lump-sum amount payable at maturity |

3 years | Tk. 10,000.00 | Tk. 430.00 | Tk. 13,400.00 |

5 years | Tk. 10,000.00 | Tk. 520.00 | Tk. 16,000.00 |

CASH DEPARTMENT:

- Opening of Cash: Beginning balance is used to start daily transaction.

- Maintenance of Receipt and Payment Registers while receiving & paying

- Different amount of cash.

- Previously issued cheque will be paid if issued 6 months before.

- Advance issued cheque cannot be made payment even one day before.

- Evening Banking: Can only receive cash. No payment can be made except

- Some special cases.

- TBL Dhanmondi Branch provides “Sheba Service” in this branch

REMITTANCE & BILLS DEPARTMENT:

Local remittance is one of the main components of general banking.The components of local remittance are-

Telegraphic Transfer,

Demand Draft issue,

Saving Certificate Issue (Sanchaypatra issue),

Pay order.

REMITTANCE & BILL SECTIONS ARE:

- Issue and payment of Pay Order, Pay Slip, Demand Draft, etc.

- Execution of Inward and Outward Telegraphic Transfer

- Non client services like T.T. and Pay Order

- Follow up with clients

- Internal and local collection of cheque and bills.

i. Telegraphic Transfer (TT):

It is an order from the issuing branch to the drawee bank / branch for payment of a certain sum of money to the beneficiary. The payment instruction is sent by telephone and funds are paid to the beneficiary through his account maintained with the drawee branch or through a pay order if no account is maintained with the drawee branch. No charge is required for TT.

ii. Demand Draft (DD) Issue:

Sometimes customers use demand draft for the transfer of money from one place to another. It is must need for sending money out side Dhaka city. For getting a demand draft, customer has to fill up an application form. The form contains date, name and address of the applicant, signature of the applicant, cheque number (if cheque is given for issuing the DD), draft number, name of the payee, name of the branch on which the DD will be drawn and the amount of the DD. The form will be duly signed by the applicant and by the authorized officer. TBL charges 15% commission on the face value of DD as service charge.

iii. Shanchaya Patra:

Shanchaya patra is received from Bangladesh bank (BB). People purchasing these bonds by depositing money in this branch and payment are made on maturity to customers from this branch only. Every transaction is reported to Bangladesh bank. In case of issuance, report to be reached to BB within 48 hours, otherwise penalty is imposed. Money is realized from BB after making payment to customer.

Various types of Shanchaya Patras are sold here. They are as follows:

- Ø 5 years Bangladesh Bank Shanchaya patra (5 BSP):

Duration of this Shanchaya patra is 5 years. Any person who purchases this Shanchaya patra can withdraw his/her interest only after 5 years at the time of maturity along with capital. Any single individual can buy Bangladesh Bank Shanchaya patra for up to TK. 50 lac. And jointly can buy for up to TK.1 Crore. Interest Rate: 12.5% After 5 years.

- Month Profit Based Sanchaya patra(3MPBSP):

Duration of this Shanchaya patra is 3 years. Any person who purchases this Shanchaya patra can withdraw his/her interest in every 3 month but capital can be withdrawn after the maturity period. Any single individual can buy 3 MPB Shanchaya patra up to TK. 50 lac. And jointly can buy for up to TK.1 Crore.

Interest Rate: 11.5% after 3 year

After every three (03) month 2,875/= Tk. will be given against 1 Lac. Taka as interest.

- Pensioner’s Sanchaypatra:

Duration of this Shanchaya patra is 5 years. Any person (Retired) who purchases this Shanchaya patra can withdraw his/her interest in every 3 month but capital can be withdrawn after the maturity period. Any single individual can buy Pensioner’s Sanchaypatra up to TK. 30 lac.

Interest Rate: 12.50% after 5 year

After every three (03) month 3,125/= Tk. will be given against 1 Lac. Taka.

iv. Pay Order

For issuing a pay order, the client has to submit an application in the prescribed form. This form should be properly filled up and signed. The procedure of the issuing pay order is similar to that of the Telegraphic transfer. For issuing pay order TBL charges commission on the following rate—

|

| Pay Order [Local] issuance | No charge for account holder Tk. 20/- for non-customers/clients |

| Pay Order[Local] cancellation | Tk. 20/- per instrument

| |

| Issuance of Duplicate Instrument | Tk. 100/- per instrument plus stamp charges for indemnity at actual. |

PAYMENT OF PAY ORDER:

The pay order is presented to the bank either through clearance or for credit to the client’s account. While payment, relative entry is given in the pay order register with the date of payment.

In case of collecting DD, P0, PS following things are to be carefully checked:

- Instrument of TBL

- Crossing Seal

- Clearing Seal

- Branch Name

- Amount same in word & figure

- Signature verification

- Avoid the stop order PO, DD

- Test key verification. Every TT must have test key.

- DD over Tk.50000/- must have test key

- Maintenance of PO/TT/DD issue & payable books

- Balancing at the end of the month.

PRODUCTS & SCHEMES :

DEPOSIT PRODUCTS:

- Current Deposit Account

- Savings Deposit Account (interest calculated on monthly minimum balance of Tk.2000 and above)

- Fixed Deposit (3 months to 3 years term)

- Savings Certificate

- Trust Smart Savers Scheme(TSS)

- Trust Digoon Laav Scheme(TDLS)

- Trust Money Making Scheme(TMMS)

- Trust Education Scheme(TES)

- Corporate Financing

- Trust Consumer Durable Scheme (TCDS)

- Trust Marriage Loan Scheme (TMLS)

- Trust Car Loan Scheme (TCLS)

- Trust House Building Loan Scheme (THLS)

- Trust Micro Credit for Renovation & Reconstruction of Dwelling Houses

INVESTMENT PRODUCTS:

INTERNATIONAL TRADE:

- International Banking

- Private Foreign Currency Accounts

- Non Resident Foreign Currency Deposit Account

- Resident Foreign Currency Deposit Account

- Travelers’ Endorsement (Cash and Travelers Cheque)

- Remittance of Foreign Currency

- Import and Export Transaction

- Foreign Exchange Dealing

- Purchase of Foreign Currency Drafts, Cheque, Travelers Cheque

- Wage Earner’s Development Bond

OTHER SERVICES:

There are two services offered by the bank exclusively on distinguishable terms and conditions. The aforesaid services are-

Locker Service:

There are some more than 500 lockers at the Dhanmondi Branch of TBL. The lockers are now rented on Security Deposit Basis instead of yearly or monthly rental Basis. The lockers are allotted on most flexible term and meager Security Deposit refundable at the time of closing the locker.

Size of Locker

| Size | ||||||||

| Small | Medium | Large | ||||||

| Height | Width | Length | Height | Width | Length | Height | Width | Length

|

| 4.5” | 7” | 21.5” | 4.5” | 14” | 21.5” | 9” | 14” | 21.5”

|

Security Deposit of Locker

Floor | Security Deposit | ||

Small | Medium | Large | |

| Ground Floor | 7,500 | 10,000 | 15,000

|

| First Floor | 5,000 | 7,500 | 10,000

|

Debit Card:

The bank offers its clients Debit Card. To be a holder of the Card the person needs nothing but to be a client or account holder of the bank. The bank charges no initial card processing cost. The yearly service charge of a debit card is Tk300.00. It seems to be a value added service to the clients.

DISPATCH DEPARTMENT:

Dispatch is one of the primary departments of banking activities. Dispatch can be categorized into two parts:

3.4.1 Inward Register

3.4.2 Outward Register – (a) Courier

(b) By Post

Inward Register :

In inward register all the incoming documents are received and registered according to date. Then, Documents are transferred to different departments according to their destiny.

Outward Register:

The documents, which are needed to mail to different branches of TBL in Bangladesh or outside Bangladesh, are registered in outward register and mailed by courier or by post, which one is suitable.

LOANS AND ADVANCES DEPARTMENT:

The bank lends the deposited money on different sectors and at different rates. A summary of sector wise lending and lending rate is as follows:

There are two types of Loan:

1) Short-Term Loans: Time period is less than 1 year

2) Long -Term Loans: Time period is 1 year & above

Loans and advances Department is the most important department of a bank. Banks borrows money from the public by accepting Deposits from them and then lending it to a borrower for a specific period of time to be repaid with a certain amount of interest. This Dept. is one of the main sources of TBL’s profits.

When bank wants to give loans of advances to a borrower, first of all he has to do LRA (Lending Risk Analysis) and when loan amount is 20, 00,000 & above this analysis is compulsory. Because the amount, which is given to, a borrower, actually comes from the public and it is repayable on demand. So, bank has to be careful when giving loans and advances. When banks can not collect the loan amount with interest, they have to bear losses.

If TBL agrees to give loans and advances to a borrower after analyzing all sorts of risk, then the borrower writes an application addressing the manager and the amount, business types, securities etc. also are mentioned in the application. After getting the application the manager scrutinizes it for justifying all information whether genuine or not. and after doing this he sanctions the loan. He can also collect the borrower’s credit report from CIB(Credit Information Bureau ) Department of Bangladesh Bank (If the borrower takes loans above Tk. 1,00,000 from any bank, that bank will send this credit reports to the Bangladesh Bank.

The manager can sanction specific amount of loans and advances (In this branch it is Tk. 15, 00,000). If the loan amount crosses this limit, then he will recommend it to regional office. Regional manager also has limit for sanctioning loans and advances. If the amount of loans and advances above his limit, he will recommend it to the head office. Then head office will sanction that loans and advances.

TBL sanctions loans and advances under certain terms of conditions. When the borrower‘s loan is sanctioned, he is known through intimation/ a copy of sanction letter. If he accepts all terms of conditions, then he has to come within 3, 7, or 15 days whatever mentioned in the sanction letter.

- § Selection of Borrower:

In extension of bank credit, nothing is more significant than selection of borrower. While choosing a borrower, bank must study three things: Character, Capacity and in Capital or in other words Reliability, Responsibility, Resourcefulness of a party.

LENDING SCHEMES:

The bank lends the deposited money on different sectors:

a) TRUST CONSUMER DURABLE SCHEME :

Loans up to Tk, 60,000.00 available for purchase of household durable. Tenure ranges from 6 months to 24 months.

b) TRUST MARRIAGE LOAN SCHEME:

Bank Provides loan up to Tk. 1,00,000.00 for marriage. Easy monthly installment for a maximum period of 48 months.

c) TRUST CAR LOAN SCHEME:

Loan up to Tk. 3,00,000.00 available for purchase of car. Maximum period for repayment is 48 months only.

d) TRUST HOUSING LOAN SCHEME (THLS):

House Building loan up to Tk. 12.50 lac available for expansion of residential buildings. Easy monthly installment for a maximum period of 07 years.

e) TRUST MICRO CREDIT FOR RENOVATION & RECONSTRUCTION OF DWELLING HOUSE:

Small loans of Tk. 20,000.00 Tk. 30,000.00 and Tk. 40,000.00 are given to the low-income group for improving standard and quality of living.

RETAIL PRODUCTS:

- TBL Car Loan,

- TBL House Hold Durables Loan,

- TBL Doctors Loan,

- TBL Advance Against Salary Loan,

- TBL Any Purpose Loan,

- TBL Hospitalization Loan,

- TBL Education Loan,

- TBL Travel Loan,

- TBL Marriage Loan,

- TBL CNG Conversion Loan,

- TBL Apon Nibash Loan

Retail Products Details:

Retail Banking:

Banking services for individual customer. It is different from general credit section. It provides many attractive services to its client. Day by day it becomes more popular to an individual client. An individual can take any loan in easy way. The retails products of Trust Bank Ltd. are as follows:

- Household Durables Loan:

Needs are constantly changing phenomena in human life to improve the standard of living. Sometimes your saving is not good enough to meet your requirements. At, Trust Bank, we take care of your financing needs and you can trust on us as your financial partner indeed.

- Doctors’ Loan:

Medical is a noble profession, which is evolving fast. In a country like ours it is important to be a part of those changes, as we cannot ender leg behind. Keeping that in mind and with a vision to support and promote health services, TBL is at your side with our Doctor’s Loan.

- Educational Loan:

A substantial amount of finance is required to give child the best education or to get a higher degree either at home or abroad.

- Travel Loan

When you plan to travel local or global exotic location, financing is the key issue. Don’t be worried; TBL Travel loan is ready to provide instant financial support

- Hospitalization Loan:

Crises come at anytime and well-being comes at a prices. When the urgency comes for medical treatment of your family, there can never be any compromise. At any urgency, please remember us to provide financial support through our “Hospitalization Loan” scheme.

- Any Purpose Loan:

We have so many needs, some are attainable with our means & standing and some are unattainable. The unattainable needs can be met by TBL “Any Purpose Loan”

- Apon Nibash Loan:

TBL offers Apon Nibash Loan (House Finance) to you with easy repayment schedule matching your affordability. You have unlimited options of choosing your home with limited means and standing. Here, TBL Apon Nibash helps you to match your long cherished dream.

- CNG Conversion Loan:

Driving a car is no longer a burden as our TBL Conversion Loan makes it easily affordable.

- Marriage Loan

Tying the marital knot is an event of a lifetime and memories should last forever. TBL “Marriage Loan” will help you to arrange celebrate the marriage in style.

- Advance against Salary

Life is continuously facing unforeseen events. For which sudden financial support is essential. We are at your side to meet up your urgency at any moment through our “Advance against Salary.”

INTERNATIONAL BANKING:

Trust Bank Limited, with its wide correspondent relationship with major banks in the world is totally capable to meet your needs of foreign currency transactions and foreign trade services. You can open and maintain Accounts in foreign currencies like US Dollar, Pound Sterling, and Japanese Yen and even in Euro with us. With its own Dealing Room, TBL is able to offer competitive Exchange Rate for all major currencies of the world.

- FA Account (Foreign Nationals)

- FC Account (Bangladeshi Nationals)

FOREIGN EXCHANGE DEPARTMENT:

Foreign exchange means the exchange of currency in terms of goods from one country to another. This is the most well-known and well-organized business uniform in world business. Foreign exchange mainly has two parties:

Import Operations:

There are different other parties who are also related to this foreign exchange process. But Bank is the most important of all the other parties. Bank works as intermediary in case of foreign exchange. So, we can say that the foreign exchange is nothing but the combination of export and import in international platform.

If an importer wants to buy goods from foreign countries he has to communicate with the exporter or he may also communicate through indenting firms.

EXPORT OPEATIONS:

- § For becoming an Exporter a person needs:-

- Current A/C in TBL

- ERC (Export Registration Certificate) issued by CCI & E (Chief Controller of Import & Export).

- Permission from sponsoring Authority such as Board of Investment for industries, Department of Textile for garments etc.

- Traders Association’s certificate

- VAT (Value Added Tax) & TIN (Tax Identification Number) certificates.

CREDIT DEPARTMENT:

Credit is an arrangement whereby bank acting at the request and on the instructions of a customer or on its own behalf to make a payment to or to the order of a third party or is to accept and pay bills of exchange drawn by the beneficiary. In an economy banks play the role of an intermediary that channels resources from the surplus group to the deficit group. So, one of the core functions of Commercial banks is to sanction credit facility to its customers as per requirement. Trust Bank Limited Mission is to actively participate in the growth and expansion of our national economy by providing credit to variable borrowers in most efficient way of delivery and at a competitive price.

Bank can lend up to 15% of its capital fund without having any approval from Bangladesh bank. The maximum limit can go up to 100% of the bank’s capital fund. Trust Bank Limited complies with the ceiling set by Bangladesh Bank.

PRINCIPAL OF CREDIT:

Basic principle governs the extension of credit. These principles are strictly maintained to shape and define the acceptable risk profile of Trust Bank and guides to respond business opportunities as they arise. Basic lending principles are;

- Know your customer

- Liquidity of the customer

- Safety

- Security

- Profitability (from both bank’s and customer’s purpose of the loan’s perspective)

- Diversification

- National interest

Types Of Loans And Advances Offered By Trust Bank:

Basically Trust Bank offers both funded and non-funded credit facilities.

Funded Loan Facility:

Any type of credit facility which involves direct outflow of Bank’s fund on account of borrower is termed as funded credit facility, the funded facilities of loans and advances are:

CASH CREDIT:

Cash credit is a continuous credit facility usually provided for working capital fund requirements purpose of the customer. Cash credit is generally given to traders, Industrialist for meeting up their working capital requirements. Cash Credit can be given on Hypothecation of goods or pledge. Trust Bank only practices Cash Credit on Hypothecation.

Features of Cash Credit:

- A certain limit of credit amount is set at the time of initiation of Cash Credit facility.

- An expiration date is set, which is not more then one year.

- The drawings are subject to drawing power.

- A service charge, which in effect an interest charge is normally made as a percentage of the value of purchases.

- The primary security of Cash credit facility is stock of goods, which maybe hypothecated to Trust Bank as collateral.

OVER DRAFT:

Over draft facility is also a continues loan arrangement on a customer’s current account permitting him to overdraw up to a certain approved limit for an agreed period. Here the withdrawal of deposits can be made any number of times at the convenience of the borrower, provided that the total overdrawn does not exceed the agreed limit.

Customer can return any amount at any time within the pre-fixed time of the facility. Turn over of an OD facility is the most important phenomenon on which renewal of the facility depends. Over draft facility is given to the businessman for financing working capital requirement and high net worth individual to overcome temporary liquidity crisis.

TERM LOAN:

Term loans are given to finance the acquisition of capital asset. Loan agreements often contain restrictive covenant and loan is repayable in accordance to amortization schedule. Collateral is must for term loan.

Under term loan there are three categories:

- Short term loan – less then 1 year falls with this category

- Midterm – this loan facility is extended for more then 1 year but less the 3 year. Trust Bank encourages midterm loan.

- Long term – tenure of long term loan is more then 5 years

- Inland Bill Purchased (IBP)

- House Building Loan

- Marriage Loan

- Car loan (Staff & Others)

- Consumer Durable Scheme (CDS)

- Loan Against Trust Receipt (LTR)

- Any Purpose Loan

Non-funded facilities:

Non-funded facilities also known as “contingent facilities” are those where bank fund is not required directly. A non-funded facility can turned to a funded facility as per situation creates. Bank receives commission rather than interest income by providing non-funded facilities.

Guarantee:

Trust Bank offers guarantee for its reliable and valuable customer as per requirements. This is also a Credit facility in contingent liabilities from extended for participation in development work like supply of goods and services.

Features of Bank Guarantee;

- It is a written document on non-judicial stamp

- Expiry date is mentioned specifically with other terms and conditions

- Trust Bank receives commission quarterly @ 0.50% of the guaranteed amount.

Credit Planning at different level of Trust Bank:

Credit Planning implies estimating first the total lend able resources that are likely to be available within the given period and then allocating the same amongst various alternative uses in conformity with national plan and priorities.

Necessity of credit planning in context:

- Demand for Credit is much more than its supply.

- Providing credit at right person at right time at right quantity.

- Getting maximum output as a result of credit allocation.

- Ensuring the best of alternative investment opportunities

Achieving declared objective such as providing credit to priority sectors.

Lending Risk Analysis (LRA): A Risk Mgt. Technique by Trust Bank (CRG):

Lending Risk Analysis (LRA) are based on two important pillars –

- Business risk pillar

- Security risk pillar

These are for addressing two frequently asked questions of the bankers. The questions are –

- Is the business good enough to ensure regular repayment of my loan?

- Do the securities cover adequate exposure, if the business fails to produce returns?

In answering these two basic questions, business risk and security risk have been examined with their different parameters of risk, as business risk is nothing but the Combination of the risk of different parameters of business and industry and so is for security risk, under LRA forms with a view to reaching the ultimate Security risk pillar and Business risk pillar. In this regard, the FSRP authorities have prescribed a total 11 forms, for the bankers for facilitation their decision-making.

Source: Primary

Modes of Charging Securities by Trust Bank:

Securities are the cover against loans and advances. On the other hand it ensures recovery of loans and advances from the borrowers who offer properties to the lending banker as security. Properties are converted into securities. But for conversion some conditions are to be full filled as required by the Trust Bank and these are as follows:

a) The properties are to be acceptable to the lending bankers for securities.

b) Creation of the charge on the concerned properties.

- The Acceptability of properties as securities are mainly depends on:

1. Value of property must cover the loan amount with margin.

2. Consideration of different qualities of properties

3. Free from credit restrictions of Bangladesh Bank (if any).

- Within the credit policy of the bank.

- There are two types of securities i.e. primary and collateral.

- Modes of Creation of chares are of different types. These are dependable on the basis of nature of loans and advances and nature of properties for securities.

- Charges may be of different types like legal Charge, Equitable charges, fixed charges, floating charges etc.

- Following are the different modes of creation of charges by the bank:

- Pledge

- Hypothecation

- Mortgage

- Lien

Pledge:

When goods and produces are handed over to the lending banker by the trader or manufacturer who borrow against those goods and produces for short term i.e. for working capital. But if any goods and produces are kept with the bank for security purposes will not be treated as pledge. In otherwise it is the Bailment of goods as per Bailment of goods act. In case of Pledge, control and possession of goods and produces will remain with bank but ownership will remain with borrower. There will be a storehouse either of banks or rented for safe keeping of goods. Insurance of pledged goods are compulsory. And all related expenses would be born by borrower.

Hypothecation:

Hypothecation is just opposite of pledge. When a borrower ownership, control and possession of trading goods but legal right and indirect control is created by lending banker for security against short term advances i.e. Equitable charge is created is known as Hypothecation. Just control and possession of trading goods are kept under borrower. In these types of securities lending banker generally asks for collateral securities. This type of mode of securities is allowed only for the case of first class borrowers.

Mortgage:

When bank create charge on immovable property in the form of mortgage against any lending to the borrower. Therefore a mortgage is a transfer of interest of a specific immovable property. The immovable property means land and the property attached to land but not grass, trees and crops. Mortgage is to be created for securing loan or performing any contract. And there will be a Mortgagor, Mortgagee, Mortgaged Property and Mortgage deed.

Lien:

A lien is defined as the right to retain property belonging to a debtor until he has discharged a debt due to the retainer of the property. Lien may be of two types, General Lien and Particular Lien.

A particular Lien confers a right to retain a property in respect of a particular debt involved in connection with a particular transaction.

But a General Lien confers a right to retain goods not only in respect of a debt incurred in connection with a particular transaction but also in respect of any general balance arising out of the general dealing between two parties.

Banker’s Lien is defined as an implied pledge. An ordinary lien does not imply a power of sale, but a pledge implies a power of sale. A banker’s right of sale is generally regarded as extending only to fully negotiable instrument, with regard to other securities.

LOAN PRICING TECHNIQUES BY TRUST BANK:

Loan Pricing:

- The price of a loan is the “interest rate” that the borrowers must pay to the bank; in addition to the amount borrows (principal)

- The price or the “Interest rate” of a loan is determined by the true cost of the loan to the bank (base rate) plus profit/risk premium for the bank’s services land acceptance of the risk.

- The components of the true cost of a loan are:

- Interest expense

- Administrative cost

- Cost of capital

These three components add-up to the bank’s “base rate”.

- Interest Expense = Deposit Interest + Central Bank Borrowing cost

- Administrative cost = Deposit as well as Loan administrative cost.

- Cost of capital = Return on capital or the Rate of Return investors would expect to receive from their investment in a bank.

- Risk is the measurable possibility of loosing or not gaining value.

- The Primary risk of making loan is Repayment Risk, which is the measurable possibility that a borrower will not repay their obligation as agreed.

- The Price a borrower must pay to the bank for assessing and accepting the risk is called the risk premium.

- Since past performance of a sector, industry or company is a strong indicator of the future performance, risk premium is generally based on the historical, quantifiable amount of losses in that category.

- Interest Rate Charge = Base Rate + Risk Premium.

Interest Rate Charged at Different Credit Scheme:

| SL# | Particulars | Rate of Interest |

| 1. | Agriculture loan including raw jute | 11.00% P.A. |

| 2. | Term loan (project loan) | 15.00% P.A. |

| 3. | Working capital loan (except jute) | 16.00% P.A. |

| 4. | Export loan (packing credit, export cash credit) | 7.00% P.A.

|

| 5. | Commercial loans (cash credit, hire- purchase, LTR, IBP etc.) | 15.00% P.A. |

| 7. | Small & cottage industry loan (Without subsidy of Bangladesh Bank) | 15.00% P.A. |

| 8. | Loans under various credit schemes such as consumer’s credit, small loan, Doctor’s credit, rural development credit etc. | 15.00% P.A. |

| 10. | Secured overdraft (SOD) | |

| SOD against financial obligation (PSP, BSP, ICB unit certificate etc) | 14.00% P.A. | |

| SOD against FDR of MBL | 3.00% above of the FDR rate | |

| SOD against deposit of various savings instruments of MBL | 15.00% P.A. | |

| SOD against shares / work order / export bills / quota etc | 15.00% P.A. | |

| SOD (General) | 15.00% P.A. |

Loan Classifications and Provisioning By Trust Bank:

Loan Classifications:

Loan classification is required to have a real picture of the loan and advances provided by the Bank. It helps to monitor and take appropriate decision regarding each loan account like other banks, all types of loans of BA fall into following four scales:

Unclassified: Repayment is regular

Substandard: Repayment is stopped or irregular but has reasonable prospect of improvement.

Doubtful debt: Unlikely to be repaid but special collection efforts may result in partial recover.

Bad/Loss: Very little chance of recovery.

Table – CL Statement:

| Loan Type | Unclassified (Month | Substandard (Month) | Doubtful (Month) | Bad (Month) |

| Continuous Loan Demand Loan | Expiry up to 5 month | 6 to 8 month | 9 to 11 month | 12 month+ |

| Term loan up to 5 year | 0 to 5 month | 6 to 11 month | 12 to 17 month | 18 month+ |

| Term Loan more then 5 years | 0 to 11 month | 12 to 17 month | 18 to 23 month | 24 month+ |

| Micro Credit | 0 to 11 month | 12 to 13 month | 36 to 59 month | 60 month+ |

Source: Publication of Trust Bank:

Loan Provisioning:

A Certain amount of money is kept for the purpose of provisioning. This percentage is set following Bangladesh Bank rules.

| Type of Classification | Rate of Provision |

| Unclassified | 1% |

| Substandard | 20% |

| Doubtful | 50% |

| Bad debt | 100% |

Source: Publication of Trust Bank:

Statement Send by Credit Department To Bangladesh Bank:

Statements are sent to Bangladesh bank on monthly, quarterly, half yearly and yearly basis. These statements are based on advance and inland Bill purchase/Discounted, Statement over due advances, CIB Statement, Statement of Credit, and Monthly Statement of deposit, Monthly Statement of Bank Loan & advances and other as per central bank time-to-time requirement.

Financial Analysis:

Performance of the Bank:

Profit and Operating Results: The bank earned as operating profit Tk. 853,713,506 during 2007 after all provisions including the 1% general provision on unclassified Loan & Advances. Provision for income tax for the year amounted to Tk. 340,741,773 resulting into a net profit after tax of Tk. 239,028,693

Deposit: A strong deposit base is necessary for the success of a Bank. During the year 2002 the Bank mobilized a substantial amount of deposit from mid-level income group people under Deposit Savings Scheme. After critical handling the Bank mobilized total Deposit Tk. 27,101,585,101 as at December 31, 2007, thus recording an increase of 42.75% in comparison with Tk. 18,985,951,094 as at December 31, 2006. The significant growth in deposit enabled the Bank to expand its business, performing assets and also had an impact on the profit position of the Bank.

q Advance: The Bank Loans & Advance portfolio also indicates an impressive growth. Total Loan and Advances amount to Tk. 18,682,164,654 in 2007 against Tk. 13,188,092,885 in 2006 and the growth being 41.66% TBL’s Advance portfolio is well diversified and covers a wide range of businesses and industries. The sectors financed include Manufacturing, Trading, Construction, Transport, Agriculture, Fishing & Forestry, Information Technology, and Consumer Credit amongst others.

Advances constitute the most significant indicator of the health of a Bank. The Bank has formulated its policy to give priority to SMES (Small and Medium Enterprise) and at the same time the Bank is financing large-scale enterprises through consortium of Banks. The Trust Bank Limited is committed to maintain a very high quality of assets. Close monitoring and efficient asset management has resulted in minimal creation of classified loans to total Loans and Advances.

Foreign Exchange Business: International Trade constitutes the main stream of business activities of the Trust Bank. Trust Bank Limited offer a full range of trade and services namely, issue, advice and confirmation of Documentary Credit; arranging forward exchange coverage; pre-shipment and post-shipment finance; negotiation and purchase of export bills; discounting bill of exchange; collection of bills, inward and outward remittance etc.

Import Business: The Bank established Letter of Credit amounting to Tk. 17,683.17 million during 2007; compared to the volume of Tk. 9,746.00 million in the year 2005.

q Foreign Correspondents: The number of foreign correspondents and agents of Trust Bank Limited is increasing day by day. The Bank has maintained excellent relationship with leading international Banks and has successfully established credit lines with major Banks to support global Foreign Trade Business.

Financial Highlights:

| Sl No | Particulars | Base | 2007 | 2006 | 2005 |

| 1 | Paid up capital | Taka | 1,166,670,000 | 500,000,000 | 500,000,000 |

| 2 | Total Capital | Taka | 2421322741 | 1310210320 | 1,115,068,646 |

| 3 | Capital surplus/ (deficit) | Taka | 464001641 | 44108286 | 311,749,871 |

| 4 | Total Assets | Taka | 30382222281 | 21197592200 | 14,807,905,231 |

| 5 | Total Deposits | Taka | 27101585101 | 18985951094 | 12,704,902,083 |

| 6 | Total loans & Advances | Taka | 18682164654 | 13188092885 | 9,738,323,349 |

| 7 | Total contingent liabilities and commitments | Taka | 8764455749 | 7885364349 | 4,681,077,063 |

| 8 | Credit deposit ratio | % | 68.93 | 69.46 | 76.65 |

| 9 | % of classified loans against total loans and advances | % | 2.71 | 1.32 | 1.32 |

| 10 | Profit after tax & provision | Taka | 239028693 | 262695349 | 121,286,368 |

| 11 | Amount of classified loans during current year | Taka | 332279970 | 45402353 | 28,617,561 |

| 12 | Provisions kept against classified loans | Taka | 225837248 | 63676000 | 58,000,000 |

| 13 | Provision surplus/ debit | Taka | – | – | 2,315,796 |

| 14 | Cost of funds ( Deposit Cost & Administrative cost) | % | 8.43 | 8.28 | 9.23 |

| 15 | Interest earning Assets | Taka | 27636293247 | 18608058132 | 13,401,393,133 |

| 16 | Non-interest earning Assets | Taka | 2745929034 | 2589534068 | 1,406,512,098 |

| 17 | Return on investment (ROI) | % | 9.87 | 20.05 | 10.88 |

| 18 | Return on Assets (ROA) | % | 0.79 | 1.24 | 0.82 |

| 19 | Income from Investment | Taka | 299490240 | 170817002 | 194,479,592 |

| 20 | Earning per share | Taka | 28.28 | 52.45 | 24.26 |

| 21 | Net Income per Share | Taka | 28.28 | 52.45 | 24.26 |

| 22 | Price earning Ratio | % | 3.04 | N/A | N/A |

Total Deposit:

The Total Deposit of the bank was-

2007 | 2006 | 2005 |

27,101,585,101 | 18,985,951,094 | 12,704,902,083 |

The pictorial graph and the subsequent numerical figure show that the deposit collection was more than double than that of 2005. In 2007, total deposit was increased by 113.32%, which stands at Tk. 27,101,585,101 than the deposit of accumulated in 2005. So it is vivid from the viewpoint of deposit collection the performance of the bank in 2007 was far better than 2005.

Loans and Advances:

Loans and advances of the bank constitute different purpose loans (repair and maintenance of dwelling house, customer durable loan scheme, car loan, term loan, loans against Trust Receipt etc), cash credit (cash credit, cash collateral) and overdraft (normal overdraft, secured overdraft). The total loans, cash credits and overdrafts for the three years was as follows-

2007 | 2006 | 2005 |

18,682,164,654 | 13,188,092,885 | 9,738,323,349 |

The graphical and numerical presentation depicts that loans and advances increased by in 35.42% 2006 and 91.84% in 2007 (taking 2005 as the base year).

ð Net Profit or Loss after Tax:

2007 | 2006 | 2005 |

239,028,693 | 262,695,349 | 121,286,368 |

PROFIT AND LOSS ACCOUNT:

2007 | 2006 | |||

| Interest Income Less: Interest Paid on Deposits and Borrowings |

|

| ||

| Net Interest Income | 667804877 | 400001365 | ||

| Income from Investments Commission, Exchange and Brokerage Other Operating Income |

|

| ||

660226888 | 444186672 | |||

| Total Operating Income | 1328031765 | 844188037 | ||

| Salaries and Allowances Rent, Taxes, Insurance, Electricity, etc. Legal Expenses Postage, Stamps, Telecommunications, etc, Stationery, Printing, Advertisement etc, Managing Director’s salary and benefits Directors’ Fees Auditors’ Fees Charges on loan losses Depreciation and repair of Bank Assets Others Expenses |

|

| ||

| Total Operating Expenses | 474318259 | 297288541 | ||

| Profit before Provisions | 853713506 | 546899496 | ||

| Provision for Loans and Advances | 229445936 | 38555000 | ||

| Provision for diminution in value of investment | – | 649147 | ||

| Other Provision | 44497104 | – | ||

| Total Profit before Income Taxes | 579770466 | 507695349 | ||

| Provision for Taxation | 340500000 | 245000000 | ||

| Current Tax | 241773 | (455135) | ||

| Deferred Tax | 340741773 | 244544865 | ||

| Net Profit after Taxation Appropriations: | 239028693 | 263150484 | ||

| Statutory Reserve @ 20% on profit before Tax General reserve |

|

| ||

| Retained surplus | 123074600 | 161611414 | ||

| Earning per share (EPS) (value per share: Tk;100;2003:Tk.1000) | 28.28 | 52.63 |

Foreign Remittance Department:

For reimbursement in foreign exchange businesses different banks that are intermediary between importers and exporters maintain internationally three types of account. These accounts are:

(a) NOSTRO A/C:

Our accounts with them. This means TBL maintains its accounts in different banks outside Bangladesh for reimbursement in foreign exchange businesses.

(b)VOSTRO A/C:

Their accounts with us. This means different banks outside Bangladesh maintain their accounts in TBL for reimbursement in foreign exchange businesses.

(c) LORO A/C:

Your accounts with me. When two banks from one country maintain their A/C’s in one bank outside their country.Ex. Suppose TBL and IFIC have A/C’s in American Express Bank (AMEX) in New York. Then, TBL’s A/C maintaining in AMEX is LORO to IFIC Bank. IFIC’s A/C maintaining in AMEX is LORO to TBL

PERFORMANCE OF THE BANK: AS A WHOLE:

The comparative performance of the bank among different years appears as follows:

TREND ANALYSIS:

ANALYSIS FROM THE BALANCE SHEET:

For the purpose of analysis the financial data of 2003, 2004 and 2005 have been taken based on the availability of the data. The key points of the financial statements take the following figure:

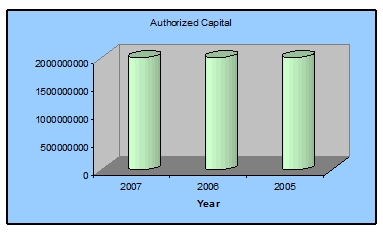

Particulars | 2007 | 2006 | 2005 |

| Authorized Capital | 2000000000 | 2000000000 | 2000000000 |

| Paid-up Capital | 1166670000 | 500000000 | 500000000 |

| Statutory Reserve | 330632079 | 214677986 | 113138916 |

| Shareholders’ Equity | 2154291716 | 1154999391 | 991972309 |

| Fixed Assets | 194224790 | 146054811 | 110616082 |

| Total Assets | 30382222281 | 21060771167 | 14807905231 |

| Investment | 3785450925 | 3122814158 | 2447953778 |

In Year 2005, Year 2006 and also in Year 2007 the authorized capital stands for the same worth of Tk. 200.00 crore. It is due to the bank’s future expansion philosophy and to keep rein with the market competitiveness.