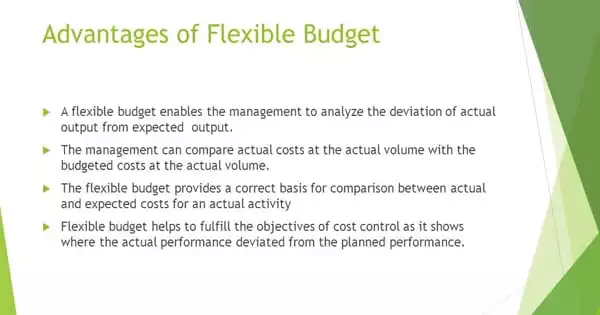

A flexible budget is a budget that is mostly used as a static budget and basically changes with changes in the volume or activity held in production; it is also useful for increasing the manager’s efficiency and effectiveness because it is set to benchmark for the company’s actual performance.

Advantages of a flexible budget –

A flexible budget can have many advantages for companies. The following are a few of the benefits that a business may experience when using a flexible budget:

- Adjustments based on profit margins and costs

A flexible budget allows businesses to have a more realistic idea of their budgets as costs and profit margins change. A static budget remains the same when it is created at the start of a new year, whereas a flexible budget accounts for decreased or increased costs and assists businesses in making adjustments to compensate. It can aid in the calculation of sales, costs, and profits at various levels of operating capacity. It aids in determining the quantity/amount of output to be produced in order to assist the company in achieving the desired profit level.

- Usage in variable cost environment

The flexible budget is especially useful in businesses where costs are closely aligned with the level of business activity, such as retail, where overhead can be segregated and treated as a fixed cost, while merchandise costs are directly related to revenues. The most significant benefit of this budget is that it assists the company’s management in determining the production level in various market and business conditions.

- Potential to maximize revenue

Flexible budgets, as opposed to static budgets, change to reflect an increase in sales. As a result, a company may be better able to see where it can increase marketing or other efforts when revenue increases. It also aids in the reclassification of various levels of budgeted costs as well as sales, allowing managers to easily identify profit areas and act accordingly.

- Budgeting efficiency

Flexible budgeting can be used to more easily update a budget that has not yet been finalized in terms of revenue or other activity figures. Managers give their approval for all fixed expenses, as well as variable expenses as a percentage of revenues or other activity measures, under this approach. The remainder of the budget is then completed by the budgeting staff, which flows through the formulas in the flexible budget and automatically alters expenditure levels.

- Increased cost controls

A flexible budget enables a company to determine when it is necessary to make changes to certain costs. For example, if projected sales are lower than expected, a flexible budget will show updated percentages of each category, allowing a company to adjust its spending to compensate for lower sales.

- Performance measurement

Because the flexible budget restructures itself based on activity levels, it is an excellent tool for evaluating manager performance – the budget should closely align to expectations at any number of activity levels. This budget can be recalculated based on activity levels. It is not constrained.

These factors combine to make the flexible budget an appealing model for advanced budget users. However, before making the switch to a flexible budget, consider the following issues.