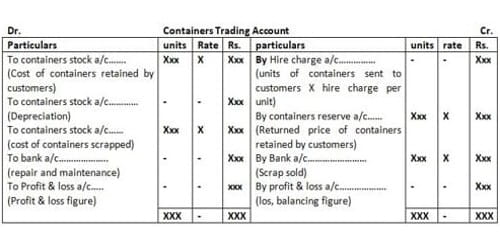

Concept of Containers Account

A container is anything in which goods are packed for sale. The word containers may be substituted for drums, boxes, packages, cases, crates, bottles, barrels, empties and cask is different and appropriate situations. The modern business can not be separated from containers. For most products, some sort of packaging is essential inasmuch as they cannot be sold without a container. Products need suitable containers before they are sold to customers. Certain other products require much stronger containers. Acid is stored and transported in non-corrosive cylinders. Normally, there are two types of containers viz. primary which is the part of the product and secondary which is the need for distribution of goods to the customers.

Accounting for containers is very important if you pack your product in containers before selling it to your consumers. When the containers are of primary nature its cost is included in the cost of production and there is no need to be returned by the customers. To calculate the cost of packaging and to record is very necessary. Therefore, no separate treatment is needed for such containers. But when the cost of the container is a significant portion of the total cost, the charge of the container is normally excluded in the price of a product to allow the seller to compete with other competitors. Therefore, the difference between the charged out the price for containers and the refunded price is known as ‘Hire charges’. The accounting treatment of containers regarded as expendable is different from the treatment of those who are not.

Objectives of Keeping Separate Accounts for Containers

Containers require investment. Hence, a separate account should be maintained for containers. A separate account is not necessary for non-returnable containers. But for returnable containers, a separate account is necessary for the following reasons.

- A separate account is necessary to control the movement of containers. Time to time it needs reconciliation and the regular incoming and outgoing of containers must be recorded.

- For an ascertainment of profit or loss arising out of containers also, the separate accounting is necessary. There are a regular inflow and outflow of containers, which demands reconciliation.

- A substantial amount is involved in the investment for containers.

Information Source: