Definition of Journal –

The journal is the regular book to maintain daily transactions which are recorded for the first time when the transaction occurs. In this daily transactions are recorded orderly, so that it can be a reference for the future. In the journal entry, there have two highlighted columns one is debit and the other is credit. And the transaction is affected two sides are equal amount.

All accounting entries are sequentially recorded for the first time in the journal through accounting entries. It is the book of original entry. The accounts which are to be debited and credited are determined by adhering to golden rules of accounting that are prescribed for journalizing.

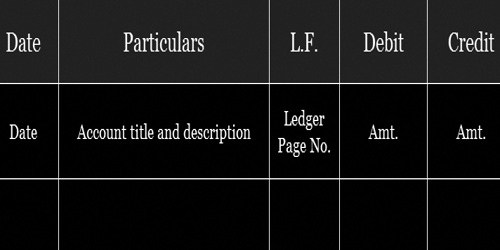

The journal entry form to five columns which is date, particulars, reference journal, debit amount, and credit amount. It can be two parts which are described below;

Single Entry: when the transaction occurs one debit and another credit amount is called single entry.

Combined Entry: When the transaction occurred more than debit and one credit amount or one debit and more than credit amount but the two sides are equal is called combined entry.

Each accounting entry must be supported by a narration that describes, in brief, the nature of the transaction record. The journal is the base book from which entries are posted to the ledger.

Definition of Ledger –

The ledger is a principal book wherein journal entries are classified as account wise and posted to individual accounts. It is essentially a set of all real, personal, and nominal accounts where transactions affecting them are recorded.

After that when a posting of accounts posted in the ledger accounts individual head of account opens for one account. The format of the ledger is ‘T’ form and having two sides of these types of accounts, one side is recorded in a debit account and another side is the credit name of an account.

Once all journal entries are posted to their individual ledger accounts, they are balanced and the balances are compiled in the form of a trial balance. This forms the base for preparing the financial statements such as profit and loss account and balance sheet.

Difference between journal and ledger –

The difference between journal and ledger have been detailed below:

Journal

- Journal is a book of accounting where daily records of business transactions are first recorded in a chronological order i.e. in the order of dates.

- It is known as the primary book of accounting or the book of original/first entry.

- It is prepared out of transaction proofs such as vouchers, receipts, bills, etc.

- A journal is not balanced like a ledger.

- The procedure of recording in a journal is known as journalizing, which performed in the form of a Journal Entry.

- It may be subdivided into a cash book, a sales daybook, sales return daybook, purchases daybook, purchases return daybook, B/R Book, B/P Book, Petty Cash Book.

- The format of a journal;

Ledger

- A ledger is an accounting book in which all similar transactions related to a particular person or thing are maintained in a summarized form.

- It is known as the principal book of accounting or the book of final entry.

- It is prepared with the help of a journal itself; therefore, it is the immediate step after recording a journal.

- Except for nominal accounts, all ledger accounts are balanced to find the net result.

- The procedure of recording in a ledger is known as posting.

- It may be sub-divided into the general ledger, debtors/sales ledger, and creditors/purchases ledger.

- The format of a ledger account;

In the above discussion about journal and ledger accounts, we can determine that the journal entry is the recording book of daily transactions known as journalizing and the transaction must have two effects as per double-entry rules. Then the transaction will be recorded in the recording process known as posting of a ledger. The posting is recorded as per head of accounts and after that, the balancing figure of two sides determines a balance, and the balance is carried forward to the preceding month as a beginning balance. This balance transferred to trial balance and the amount of trial balance is to prepare for the financial statement if the process is merely flaw then the financial statement is hard to prepare and the accounts will not be prepared for a particular period.

Information Sources: