An inventory write-off is a process of lowering the value of a company’s inventory to reflect the fact that it has no value. Either of the two methods can be used to document it. A stock discount might be discounted straightforwardly to the cost of goods sold (COGS) record, or it might balance the stock resource account in a contra resource account, regularly alluded to as the remittance for outdated stock or stock save. It can happen for a variety of reasons, including burglary, decay, damage in transit, misplacement, and so on. As an example, assume a company has a $1,000 product in stock that has had to be scrapped due to its defective state.

Inventory to be discounted when it becomes out of date or its market cost has tumbled to a level beneath the expense at which it is presently recorded in the bookkeeping records. The sum to be written down should be the difference between the inventory’s book value (cost) and the amount of cash the company will get from selling it in the most efficient way. The two strategies for writing off inventory incorporate the direct discount technique and the recompense strategy. On the off chance that stock just abatements in esteem, rather than losing it totally, it will be recorded rather than discounted.

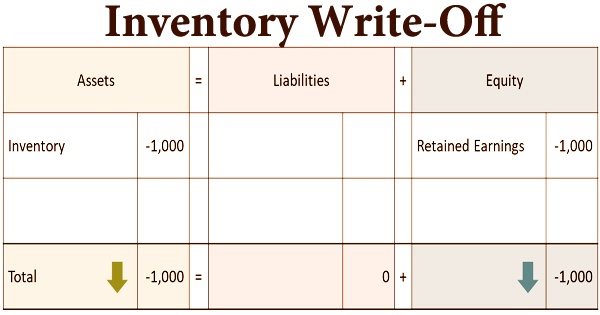

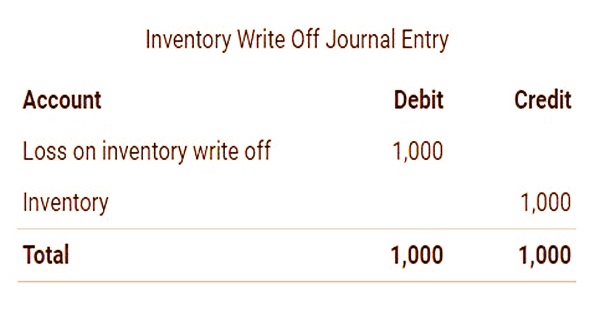

The inventory’s value has dropped by 1,000 dollars, and this must be reflected in the accounting reports. The following is the inventory write-off journal entry:

The inventory write-off cost is debited to the Loss on inventory write-off account in the journal entry above. If the inventory write-off is insignificant, the inventory write-off is frequently charged to the Cost of Goods Sold account. The issue with charging the add up to the expense of merchandise sold record is that it misshapes the gross edge of the business, as there is no comparing income entered for the offer of the item.

Any commodity that has a potential economic value to a business must be classified as an asset under generally accepted accounting principles (GAAP). Inventory is listed at cost on a company’s balance sheet under the section for current assets because it meets the criteria of an asset. An elective methodology when explicit stock things have not yet been recognized is to set up a hold for stock discounts. This is a contra account that is matched with the stock record. At the point when things are really discarded, the misfortune is charged against the hold account.

Assets = Liabilities + Owners Equity is an accounting equation that states that a company’s total assets are always equal to its total liabilities. This is valid whenever and applies to every exchange. The sum expressed in the contra account is a gauge of likely benefits, normally dependent on whatever recorded discount rate the organization has encountered. Sometimes, a stock may get out of date, ruin, become harmed, or be taken or lost. When this happens, a company’s inventory must be written off. The expense lowers the company’s net profits, which lowers the company’s retained earnings and, as a result, the owner’s equity.

It is also permissible to charge the sum to a separate inventory write offs account, rather than the cost of goods sold, if management wishes to monitor the amount of inventory write offs separately over time. There are two methods companies can use to write off inventory: the direct write-off, and the allowance method.

A company would report a credit to the inventory asset account and a debit to the expense account by using the direct write-off form. The expense account appears on the income statement, lowering the firm’s net income and therefore its retained earnings. A decline in held profit converts into a relating decline in the investors’ value segment of the asset report. On the off chance that the stock discount is unimportant, a business will frequently charge the stock discount to the cost of goods sold (COGS) account. The majority of inventory write-offs are one-time costs. A non-recurring loss can be described as a large inventory write-off (such as one caused by a warehouse fire).

When inventory can be fairly calculated to have lost value but has not yet been disposed of, the other form of writing off inventory, known as the allowance method, may be more suitable. Utilizing the recompense technique, a business will record a diary section with a worthy representative for a contra resource account, for example, stock save or the stipend for old stock. A counterbalancing charge will be made to a business ledger. The inventory account will be paid and the inventory reserve account will be debited to minimize both when the asset is finally disposed of. This is useful for maintaining the original inventory account’s historical expense.

A write off is like a record, then again, actually with a record, the resource is still left with a book esteem though with a discount the estimation of the resource is diminished to nothing. A central issue is that discounting stock doesn’t imply that dealers fundamentally need to toss out the stock simultaneously. Instead, it would make sense to keep the inventory in the hopes of increasing its value over time. It might also be appropriate to keep inventory on hand for a limited period of time while the buying department works out the best price for selling it.

In the event that the stock actually has an honest assessment yet that worth is not exactly the book esteem, it will be discounted instead of discounted. However, inventory that has been written off should not be kept for too long if it results in additional inventory storage costs or a cluttered warehouse area that interferes with regular warehousing operations. A write-off (or write-down) in inventory should be remembered right away. The misfortune or decrease in esteem can’t be spread and perceived over different periods, as this would suggest that there is some future advantage related with the stock thing.

Information Sources: