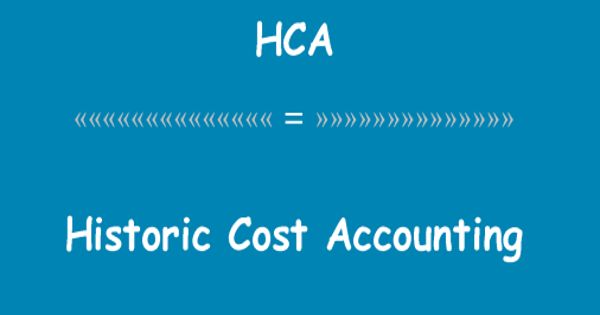

Limitation of Historical Cost Accounting (HCA)

Historical Cost Accounting (HCA), records transactions appearing in both the balance sheet and the profit and loss account in monetary amounts which reflect their historical costs, i.e., prices that are generally the result of arm’s length transactions. In order to trace the impact of inflation on the financial statements, it becomes necessary to pinpoint the limitations of the conventional statements conveying historical financial information for end-users within an organization and also outsiders.

Limitations of historical cost accounting Financial statements prepared on the historical cost basis do not necessarily lead to a true and fair presentation of an entity’s performance or future potential if capital is not being maintained. Financial statements prepared under the historical accounting system suffer from a number of limitations, which are as follows:

(1) No Consideration of Price Level Changes

Changes in the price level are not taken into account. The financial statements prepared under the conventional system are merely statements of historical facts. Financial statements prepared under historical cost accounting are merely statements of historical facts. Changes in the value of money as a result of changes in the general level of price are not taken into account. This instability has resulted in a number of distortions in the financial statements and is the most serious limitation of historical accounting. Hence, they fail to give a true and fair picture of the state of affairs of the organization.

(2) Unrealistic Fixed Assets Value

Fixed assets are shown in the position statement at the cost at which they were acquired. In historical cost accounting, fixed assets are recorded and presented at the price at which they are acquired. Changes in the market value of such assets are ignored.

(3) Insufficient Provision for Depreciation

Depreciation is charged on the historical cost of the asset. Depreciation is a mechanism of generating funds to replace the fixed assets when the replacement becomes due. It is the charge of the cost of the used up value of the asset against revenue. In historical cost accounting, depreciation is charged on the basis of the historical cost of fixed assets, not at the price at which the same assets are acquired. It is a mechanism of generating funds for the replacement of fixed assets when the replacement becomes due. The provision made by way of depreciation charge on the original cost will not be sufficient for the replacement of assets.

(4) Mixing Up of Holding and Operating Gain

In historical cost accounting, gain or loss on account of holding inventories may be mixed up with operating gain or losses. In conventional accounting gains (or losses) on account of holding inventories may be mixed up with operating gains (or losses). Holding gain or losses should be segregated from operating gain or losses to determine the true operating performance.

(5) Fails to Present a Fair Value of Financial Position

The balance sheet consists of monetary and non-monetary items. Monetary items like cash, loan, debtors, creditors, etc. are shown at their current monetary value. Non-monetary items like inventory, building, land, etc. are shown at historical costing, not at current value. The reported profits are overstated and assets are understated under inflationary conditions. During periods of inflation, non-monetary items are understated. Thus, the balance sheet fails to present a fair value financial position.