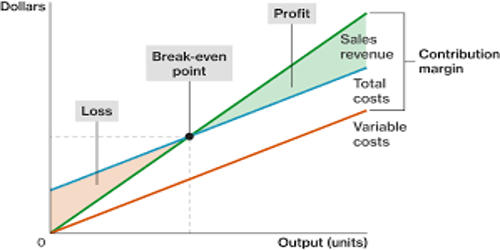

Operating risk refers to the risk of the firm not being able to cover its fixed operating costs. Operating Risk measurement is not the only target of the overall operational risk management process, but it is a fundamental phase as it defines its efficiency; furthermore, the need to measure operational risk comes from the capital regulatory framework. Effective risk management requires formal processes and controls as well as “good” risk culture. This is because pre-defined controls by definition will not address unknown risks and therefore staff must work in line with principles and values which guide their actions and decision making in unforeseen circumstances.

The measurement of operating risk can be done through the application of the concept of elasticity. Since operating leverage depends on fixed operating costs, larger fixed operating costs indicate a higher degree of operating leverage and thus, higher operating risk of the firm. High operating leverage is good when sales are rising but bad when they are falling. More specifically, we can use indicators such as the degree of operating leverage (DOL), which is a very popular indicator of operating risk.

The degree of operating leverage measures the sensitivity of operating income to the variations in units sold. It is measured as the percentage change in operating income divided by the percentage change in units sold:

DOL: [Percentage Change in Operating Income / Percentage Change in Units Sold]

For example, if we calculated the degree operating leverage for Company A and found a value of 3, it means that Company A would experience a 3% increase in operating income for every 1% of growth in units sold.

The Right Level of Operating Risk

- A company should neither generally minimize the level of operating risk nor maximize it. The right level of operating risk depends on several factors, such as:

- The characteristics of the industry: Businesses in some industries may need to bear a certain level of fixed costs to be efficient.

- The balance sheet’s health: Companies with bad balance sheets will approach operating risk differently from financially more stable companies.

- The overall strategy and level of risk aversion: As a higher level of operating risk amplifies both losses and profits, the management of some companies may willingly decide to take on higher operating risk, structurally or opportunistically, when some favorable conditions are identified.

Information Source: