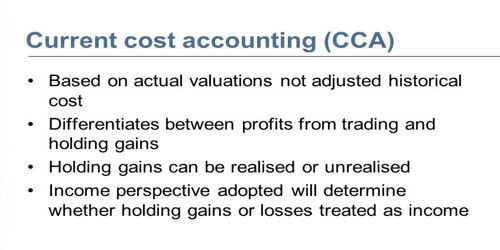

This system takes into account price changes relevant to the particular firm or industry rather than the economy as a whole. The system concerns operating profits and, naturally, operating capital employed and seeks to make a clear distinction between profits that emerge according to present-day terms through operations and profits and those that arise only because of an increase in prices, i.e., holding gains. It seeks to arrive at a profit which can be safely distributed as a dividend without impairing the operational capability of the firm.

“The current Cost Accounting approach is similar to those accounting requirements that apply to certain classes of investments owned by companies such as marketable securities held for trading purposes.”

Objectives of the Current Cost Accounting (CCA) Approach

Current Cost Accounting (CCA) aims to maintain the capital of a business enterprise in terms of its operating capability. Operating capability is denoted by the net operating assets of the enterprise in terms of share-holders funds.

(1) The objective of the current cost accounting method is to report the financial assets and liabilities of a company at their fair market value rather than historical cost.

(2) To provide correct and reliable financial information based on the current replacement cost.

(3) To calculate the profit without changing the historical profit.

(4) To protect the business in the event of a normal inflationary situation.

(5) To keep the level of capital in a very balanced position by making the valuation of assets in proper value based on replacement value.

(6) To provide realistic information to the management, investors, creditors, government, and to other interested parties.

(7) To prepare the financial statement at the end of the year on the basis of the current value of such items.

(8) This approach is similar to those accounting requirements that apply to certain classes of investments owned by companies such as marketable securities held for trading purposes.

Current cost accounting is not a generally accepted accounting principle for primary financial statements. A change in the input prices of goods and services used and financed by the business will affect the number of funds required to maintain the operating capability of the business enterprise. Therefore, maintaining the operating capability is the objective that is attempted to be achieved under CCA while preparing a profit and loss account and balance sheet.