Process Costing:

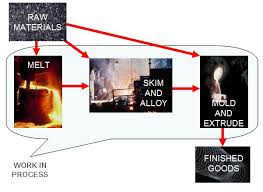

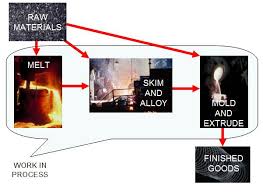

Process costing is a type of operation costing which is used to ascertain the cost of a product at each process or stage of manufacture. CIMA defines process costing as “The costing method applicable where goods or services result from a sequence of continuous or repetitive operations or processes. Costs are averaged over the units produced during the period”. Process costing is suitable for industries producing homogeneous products and where production is a continuous flow. A process can be referred to as the sub-unit of an organization specifically defined for cost collection purpose.

Procedure of Process Costing:

There are four basic steps in accounting for Process cost:

- Summarize the flow of physical units of output.

- Compute output in terms of equivalent units.

- Summarize total costs to account for and Compute equivalent unit costs.

- Assign total costs to units completed and to units in ending work in process inventory.

The journal entries for process costing are the same as those for job-order costing with one exception. The entry to transfer cost from one work-in-process account to another is:

Work-in-process inventory-second department Debit (Left)

Work-in-process-first department Credit (Right)

e.g.(1) Micro Labs Company produces house paint in two processing departments: the Mixing Department which mixes the paint colors and the Finishing Department which puts the paint in containers and labels them. The following information related to the company’s operation for October follows:

A) Raw materials were issued for use in production: Mixing department, $551,000, and the Finishing department, $629,000. B) Direct labor costs incurred: Mixing department $230,000, and Finishing department $270,000. C) Manufacturing overhead cost applied: Mixing department $665,000, and Finishing department, $405,000. D) The cost of the mixed paint transferred from the Mixing department to the Finishing department was $1,850,000. E) Paint that had been prepared for shipping was transferred from the Finishing department to Finished Goods. Cost of the transferred paint was $3,200,000.

Required: Prepare journal entries to record items A) through E) above.

Solution(1):

–Work in Process – Mixing 551,000 –Work in Process – Finishing 629,000 –Raw Materials 1,180,000 –Work in Process – Mixing 230,000 –Work in Process – Finishing 270,000 –Wages and Salaries Payable 500,000 –Work in Process – Mixing 665,000 –Work in Process – Finishing 405,000 –Manufacturing Overhead 1,070,000 –Work in Process – Finishing 1,850,000 –Work in Process – Mixing 1,850,000 –Finished Goods 3,200,000 –Work in Process – Finishing 3,200,000

e.g.(2) Larney Corporation uses process costing. A number of transactions that occurred in June are listed below. As follows:

A) Raw materials that cost $38,200 are withdrawn from the storeroom for use in the Mixing Department. B) Direct labor costs incurred $36,500,in the Mixing Department. C) Manufacturing overhead of $42,100 is applied in the Mixing Department. D) Units with a carrying cost of $112,400 finish processing in the Mixing Department and are transferred to the Drying Department for further processing. E) Units with a carrying cost of $143,800 finish processing in the Drying Department, the final step in the production process, and are transferred to the finished goods warehouse. F) Finished goods with a carrying cost of $138,500

Required: Prepare journal entries to record items A) through F).

Solution (2):

–work in process-mixing department $38,200 —raw materials $38,200 –work in process $36,500 –salaries/wages payable $36,500 –work in process-mixing department $42,100 –manufacturing overhead $42,100 –work in process-drying department. $112,400 –work in process mixing department $112,400 –finished goods $143,800 –work in process-drying department $143,800 -costs of goods sold $138,500 –finished goods $138,500

Operation cost in batch manufacturing

Batch costing is a modification of job costing. When production is repetitive nature and consists of a definite number of articles, batch is used. In batch costing, the most important problem is to determine the optimum size of the batch that follows the fact that production of two elements of costs:

- Set up costs which are generally fixed per batch.

- Carrying costs which vadetermination of batch quantity requires considerations of some factors:

- setting up costs per batch.

- cost of manufacturing such as (direct materials cost + direct wages + direct overhead) per piece.

- cost of storage.

- rate of interest on the capital invested in product and rate of demand for product.

References

- Jae K. Shim, Joel G. Siegel (2009,2000,1992). Modern Cost Management and Analysis 3rd Ed. Barron’s Education Series, Inc. ISBN 978-0-7641-4103-4.

- Bhabatosh Banerjee. Cost Accounting Theory And Practice 12Th Ed.