To survive in this competitive market every business no matter it is production oriented or service oriented should make broaden their horizons. Their products must be diversified which can respond to the market demand easily. SIBL has a complete assortment of Commercial

Corporate and Personal banking service covering all segments of society. SIBL is very different from any other commercial banks and islami banks as well. It was an investment bank earlier so it knows the demand of the market more than other islami banks.

This report has been conducted to find out the possibility of ascertain the standard of SIBL in the higher level in terms of retail products. In this report the total portfolio of SIBL has been shown that indicated a positive growth trend in the retail credit amount disbursed. Nowadays more people are interested in Islamic banking system may be for the religious view. Islamic bank does not have any interest system. They only give profit upon the depository amount and receives profit from the investors by giving loans.

From the comparison with other commercial and Islamic banks, some problems and prospects are found in SIBL. They are offering diversified product portfolio and lowest rates and charges which are their strength to proceed further in the business.

Again, SIBL has some problems regarding target clients segments and promotional activities that should be rectified. The products and drawbacks of SIBL are described in the report. Some solutions are also covered in the report which can help the bank to minimize the risk of customer dissatisfaction.

Chapter: One

Rationale of the Study

A research is always formulated based on some requirements and enquiries. This research has been carried out as a part of the BBA program but this study might be very much helpful for banks or financial institutes or the related parties. At this competitive market every bank has some competitive objectives of their own. The Banks are now facing more competition than ever before which leads them to offer more customized and quality service to their customers to ensure customer’s satisfaction. Customer service of a bank is the main reason to become competitive.

Objective of the Study

The objective of the Internship report is to engage the students with the organizational functioning situation and this report is a result of such organizational involvement. The primary objective of this report is to explain the real life scenarios in the organizational working environment. But the objective behind this study may something be broader. Thus the objectives of the study are:

- To describe the retail banking system

- View the SIBL products and services

- Evaluate the performance

- Finding drawbacks in products and services

- Draw some solutions to the problems

- To apply theoretical knowledge in the practical field.

- To find out facilities that are provide by SIBL to its customers.

- How branches are dealing with the customers

- The process of working sections of a branch.

- To analyze the performance of SIBL.

- To have some practical experience that will be helpful for future career growth.

Methodology

To prepare this report I have assembled the data and information from both primary and secondary sources. Primary data and information were collected through:

- Interviewing the officials

- Discussion with clients

- Personal observation & intelligence

Data Collection Procedure

There should a particular process for collecting data for a report. The necessary data and information were collected in the following ways:

- Through discussion of the topic.

- Through a formal questionnaire.

- Though the papers of rules and regulations.

- Files containing product details.

- Through various journal of banks.

- Personal experience gained by visiting different desks.

- Study of old files.

- Personal investigation with bankers.

- Different circulars sent by Head Office of SIBL and Bangladesh Bank.

Chapter: Two

Introduction

In the modern world, banks are playing a key role for the development of an economy and the banks are no more divergent from any other consumer marketing corporation. The excellent service quality allows a bank to make them diverse from their competitors, provide an endurable competitive advantage, and augment efficiency.

Customer service is the process of ensuring customer satisfaction with a product or service.

Customer service takes place due to performing a transaction for the customer, such as making a sale or returning an item. In Banks customer service includes the processing of cheque, cash and direct debit payments and withdrawals, setting up and maintaining customers‟ accounts, selling financial products and services to customers, dealing with enquiries, promoting the products and using a computerized system to update account details, general administration tasks such as maintaining records, sending letters to customers, helping customers with loan and mortgage applications. This internship report restrains the fleeting study on Social Islami Bank Limited

The report is disseminated in many parts according to the structure of supervisor of report. Most of the banks have some distinct business divisions namely

- Corporate & Investment Banking;

- Treasury & Market Risks;

- Retail Banking (including Cards);

- SME Banking.

Under a real time online banking platform, these four business divisions are supported at the back by a vigorous service delivery or operations setup and also a smart IT Backbone. Such centralized business segment based business & operating model ensure specialized treatment and services to the bank’s different customer segments.

Chapter: Three

Retail Banking

Retail banking is a distinctive mass-market banking system in which individual customers use local branches of larger commercial banks. Services offered include savings and current accounts, mortgages, personal loans, debit/credit cards and certificates of deposit. This is a consumer oriented banking system where the organization deals with the customers directly.

Through retail banking customers can get financial services Retail banking is the division of a bank which deals with retail customers which defined as the process of identifying individual needs and satisfying them accordingly.

Objectives of Retail Banking

- To get better living standard certain segments of customer by giving collateral free loan

- To participate in the Scio-economic development of the country

- To ensure the access to credit by mass people

- To diversify loan portfolio to minimize risk

- To maximize bank profit as well as to minimize pressure on liquidity through quicker recycling but higher yielding loan operation

Target Market of Retail Banking

- Confirmed Officers of Government, Non–Government organizations/Institutes, Semi Government, Autonomous bodies & Corporations

- Professionals, Business Executives and Self Employed Persons who have regular monthly income with repayment capacity

- Any other individuals where the monthly installment size shall not exceed one third of their take home income.

Retail Banking Products and Services

Al-Wadiah current account

One of the most significant sources of depository amount is the Al–Wadiah current deposit .It has some similarities with the current account of conventional bank account. The term AlWadiah current deposit means deposit of money allowing somebody to sue it. Bank being a trustee preserve and keeps or in safe custody of what is deposited. Depositors feel safe in keeping their money with the bank and take transaction facilities.

- Features of this deposit

- Minimum TK 1000 is required to open this account.

- This account is operated under Al-Wadiah principle.

- Without any condition any amount can deposited to this account.

- A cheque book is provided for the account.

- Any amount can be withdrawn at any banking holder

Mudaraba Savings Deposit

Mudaraba savings Deposit (MSD) account is opened by the lower and middle classes people who wish to save a part of their incomes to meet their future intend to earn an income from their savings. It aims at encouraging savings of non-trading person(s), institution(s), society, etc by depositing small amount of money in the bank.

- Features of this deposit

- This account is operated under profit sharing principle. Here bank is Mudariba and depositors are Sahib al-mal.

- Cheque books are provided for this account.

- From this account money can be withdrawn four times a month.

- For this account an interim profit is provided in the month of June and December in each year.

- After preparing the final account at the end of each year the final profit is provided to the depositors.

Mudaraba Term Deposit

Mudaraba Term Deposits are opened by the bank with a sum of Tk. 5000 or above any amount from individuals (single and joint), firms (proprietorship/partnership), limited companies etc. This deposit is accepted by the period of 1, 3, 6, 12, 24 months. This account holder will share the profit of investment with Social Islami Bank Ltd, at the rate declared by the bank from time to time. The Bank reserves the right to invest the funds received in Mudaraba term deposit accounts, in its sole judgment, in any interest-free “Halal” business it deems fit.

Features of this deposit

Mudaraba Term Deposits are accepted by the bank with a sum of Tk. 10000 or above (multiple of 5000) from individuals (single and joint), firms (proprietorship/partnership), limited companies, autonomous bodies, charitable institutions, association, educational institution, local bodies, trusts, etc, against issuance of non transferable receipts in acknowledgement of MTD account may be opened in the names of minors jointly with

- Their guardians, for example:

- Received from Mr. X Guardian of Mister/Miss…………………. (Minor)

- The Mudaraba term deposits are accepted for periods of 1, 3,6,12 and 36 months. Weight age on the rate of return is given to deposits of longer maturity.

- The Bank reserves the right to invest the funds received in Mudaraba term deposit accounts, in its sole judgment, in any interest-free “Halal” business it deems fit.

- Mudaraba term deposit account holder will share the profit of investment with Social Islami Bank Ltd, at the rate declared by the bank from time to time.

- The account holder is not allowed to withdraw the amount before maturity date.

- MTD account holder may withdraw the profit amount annually if he so desires on condition the final adjustment

- If the profit amount is not withdrawn it will automatically be added to the principal amount annually and the entire amount will earn profit/loss.

- The bank retains the right of refusing to accept any deposit from any person in MTD account without assigning any reason.

Mudaraba Scheme Deposit

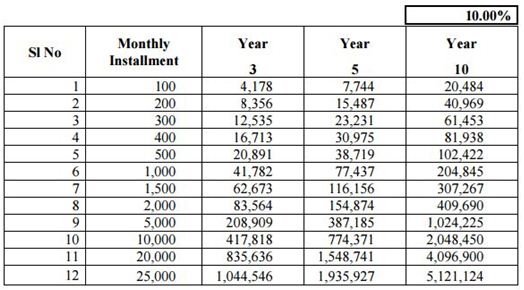

In SIBL they offer monthly depository scheme. In those account people deposit a certain amount of money every month for a predetermined period of time and gets profit at the current rate of profit. Now there rate is 10% for monthly deposit scheme. The installment and profits are given below:

A large number of scheme deposits are available in SIBL, the bank tried to meet customer need by using the following scheme

Mudaraba Hajj Saving Deposit

This scheme will be accounted under Mudaraba rules. The Bank as Mudarib and the account holder will be treated as Sahib-e-Mal. The duration of this scheme will be 1 to 20 years. An introducer must be there to open an account. Any installment size can be chosen during the opening of the account In case of closing the account before maturity profit will be given as per rules of Al-Wadiah Current account.

Features of this deposit

- This account shall be called as Hajj/Umrah Savings Scheme.

- Any Muslim Residing in Bangladesh may open an account under this scheme.

- In case of change of address the bank must have to be notified as soon as possible.

- An introducer must be there to open an account.

- In case of closing the account before maturity profit will be given as per rules of Al-Wadiah Current account. No profit will be given in case of closing the account before 6 (Six) months.

- Monthly installment of the account will be deposited within 10th day of each month. Any advance installment is always appreciable.

- In case of failing of 3 consecutive installments the account will be automatically changed to savings account.

Mudaraba Bashastan Savings scheme

The scheme is provided to facilitate the inhabitant. It helps to fulfill basic needs of housing.

- Features of this deposit

- The applicant has to fill the application form duly.

- An amount of Tk. 500/-, 1000/-, 1500/-, 2000/- or any amount multiple can be deposited under this scheme.

- The depositor will enjoy earnings from investments under Islami Shariah based Mudaraba rules.

- As per rules of Islami banking the actual amount may vary from the estimated amount.

- In case of failing of 3 (Three) consecutive installments the account will be closed.

In such cases profit will be given as per savings account rate, but no profit will be given if the account is closed within 6(Six) months. The account holder may choose any installment size on account opening, which cannot be changed later. Installment must be deposited within first 15 day of the month. Any amount deposited as advance installment is always welcome.

Mudaraba Pension Saving Deposit

To create awareness to deposit among income people this scheme is introduced. It facilitates the old aged people.

- Features of the deposit

- An amount of taka 100, 200, 300, 400, 500, and 1000 can be installed here.

- Any Bangladeshi person aged above 18 yrs and having sound mental condition can may open this scheme.

- To open this account there must be a signature of a valued introducer.

- Parents or legal guardians can open this scheme in the name of their underage children.

Mudaraba Millionaire Scheme

Thinking of the income generation of the people, Mudaraba Millionaire scheme is introduced by SIBL.

Features of the deposit

- 550/-, Tk. 1050/- or Tk. 2050/- is taken as monthly installment under Mudaraba principles of Islami Shariah.

- Duration of this scheme will be 5, 10 yrs.

- After starting of operation of this scheme size of installment cannot be changed.

- Any depositor may open one or more account in the same name in the same branch.

- If a depositor fails to deposit 4 consecutive installments then the account will be closed and profit will applied as per rate of Mudaraba Savings Rate. Profit for the first 06 (Six) months shall not be applied.

Mudaraba Monthly Profit scheme

It is a scheme which is introduced by SIBL to facilitate the people at a monthly basis.

- Features of this deposit

- The scheme provides monthly profit for service holders who may deposit the pension benefit.

- 1, 00,000/-, 1, 10,000/-, 1, 20,000/- or 1, 25,000/- or any amount multiple can be deposited under this scheme.

- The duration of the amount should be for Five years.

- The payable profit will become due after 1 month of deposit. But the amount will be deposited to account in the last week of the month.

- Generally, a depositor cannot withdraw the amount before 5 years. But, in unavoidable circumstances the depositor can withdraw the amount and in that case

- The depositor will have to submit the duly filled application form of the scheme.

- The depositor will have to maintain a Mudaraba Savings account in which the profit of the scheme will be deposited.

- In case of change of address the depositor must inform the bank as soon as possible.

- If the scheme is closed before 1 year then no profit will be given.

Issuing cheque books

After opening Al-Wadiah current account or Mudaraba Savings account, customer are provided with a cheque book. Customers can choose the leave limits starting from 25-100.Customers have to fill the requisition form, leave it to the prospective officer and can collect it after four working day. For a new cheque book there is a leave attached inside the cheque book. To collect a new one same procedure is repeated.

Issuing Pay orders

Pay order is an instrument, which is used to remit money with in a city through banking channel; the instruments are generally safe as most of them are crossed. SIBL charges different amount of commotions on the basis of payment order amount.

Providing bank statement

An account statement or a bank statement is a summary of all financial transactions occurring over a given period of time on a deposit account, a credit card, or any other type of account offered by the SIBL. Fixed amount of money is charged for Bank statement.TK 100/- is charged for every single time.

Providing bank solvency certificate

Bank provide bank solvency certificate to a client to declare either the client is financially solvent or not. There are two conditions; bank will issue a solvency certificate either to the amount of balance in the account or on fixed deposit or any other collateral security. Bank charge TK 100/- for this service.

Tele Banking

Social Islami Bank Limited (SIBL) provides the Tele Banking Service to its customers. Who lead very busy life or live far from bank or do not want experience crowd by telephone they can gather information what they want to know. They will have the convenience of requesting the services mentioned below-

- Balance Inquiry

- Exchange Rate Inquiry

- Request for Statements

- Information about interest on different types of deposits.

- Balance of the account

- Other Banking Information

Along with the Account opening section I worked at FDR section of General banking department. Both the Account opening section and General banking department helped me to fulfill the requirements to complete my assigned internship report.

Clearing Activities

According through the 37(2) of Bangladesh Bank Order 1972, which are the member of the clearinghouse, are called as Scheduled Bank. The scheduled banks clear the cheques drawn upon one another through the clearinghouse. Banks for credit of the proceeds to the customer’s account accept cheques and other similar instruments. The banks receive many such instruments during the from account holders.

The Clearing house sits for two times a working day. The members submit the climbable cheque in the respective desks of the banks and vice-versa. Consequently the debit and credit entries are given. Then the banks clear the balances through the cheque of Bangladesh Bank. The dishonored cheque are sorted and returned with return memo.

- Cheque is collected from customer throughout the day then it is crossed.

- At the end of collection one authorized officer signed on other side of the instruments.

- Then the deposit slip is separated from the instruments and has to put input in a register book, manually.

- After that all the instruments are organized as sill: High value and Regular value

Finally all the instruments are placed to a scanner and have to give commend on the computer and the scanner starts itself. Then the entire scanned image is to be verified after give input in Bangladesh Bank web side. When the input is finished reports of the input is generated and it is cross checked for any type of mistake. If everything is correct then the task is finished for the day. In the evening every day the returns report of the previous day is generated and it need to be collected and it‟s the duty of that officer to inform the party who submitted the instruments.

Organization-wide

These are the following responsibilities covered organization wide

Export Finance

Foreign Exchange Trade of SIBL is dealt with its 9 AD branches out of which 4 branches are in Dhaka and the remaining 5 are in Chittagong, Khulna, Sylhet, Rajshahi and Bogra. As a 21st Century Bank, it is providing the services in foreign trade through import and export finance and also playing significant role in the area of foreign remittance. To facilitate the import obligation of the Bank as well as considering the requirement of foreign currency of the country, potential exporters are encouraged to do their export business with SIBL. Competitive exchange rate is provided for foreign currency to valued exporters. In the last 3 years our export business performance is significant.

Import Finance

SIBL deal with import business and its import business is extended to commercial importers (traders) for import of various Shariah approved items and industrial importers (Users) for import of raw cotton, yarn, clinker, pharmaceutical raw materials, TV parts, Computer parts etc raw materials for their industries

Foreign Remittance

SIBL is playing important role in the Foreign Remittance sector also. It has correspondent relationship with almost all major 122 Banks of 109 countries of the world like Standard Chartered Bank, American Express Bank Limited, HSBC, HBZ Finance, Mashreq Bank PSC, Dresdner Bank AG and with local banks in Pakistan, India, Nepal and Bhutan etc with whom is plays role over advising, reimbursing and add confirming arrangement.

SWIFT

SIBL is the member of SWIFT and have 9 SWIFT workstations in all of 9 AD branches. Beside 96 branches are equipped with online banking. All the SWIFT workstations keep under online system. All correspondences of foreign trade both export and import is communicated through SWIFT. As a result foreign exchange trade becomes expeditious and instant.

Cash Section

Cash section deals with all kind of transaction in cash. This department starts day with cash in vault. This amount is called opening cash balance. Bank makes cash payment and takes cash receipts.net figure of cash receipt and payment added with opening cash balance .this figure is called closing balance. This closing balance is then added to the vault and this is the final cash balance figure for the bank at the end of a day.

Chapter: Four

Challenges and Proposed course of action Identified in the Organization

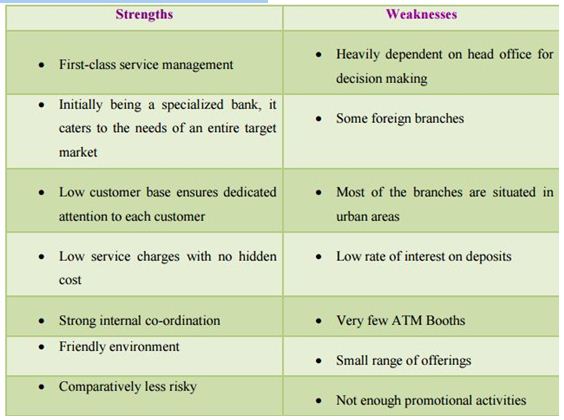

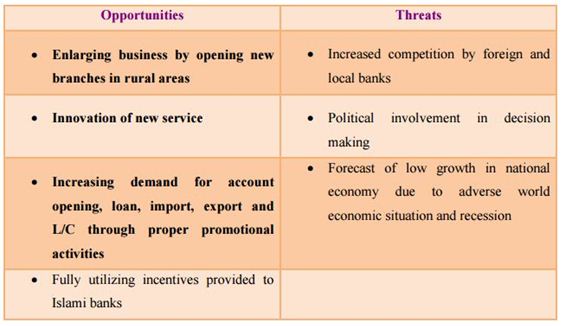

In my Internship period I observed my organization and found out some limitations of the organization. I have presented those by using a SWOT Analysis. The SWOT analysis comprises of the organization‟s internal strengths and weaknesses and external opportunities and threats. SWOT analysis helps to identify the current position of the organization. A SWOT analysis Social Islami Bank Ltd. has been done below:

Observation in the Organization

During my internship I have face few problems in this branch such as-

- Most of the bank officers were busy for their work, so they could not give me so much time for learning a topic.

- Many clients were uneducated, so I face some problems when I deal with those clients.

- All the bank officers were not helpful. But some officers help me a lot to learning about Islamic banking. System.

- In order to maintain secrecy they don‟t gave me all information.

Drawbacks of the Organization

In spite of the good management system and customer service the organization has lack of performance. There are some areas which require extensive improvement. To remain established in the completive market Social Islami Bank must solve their problems and improve their service. The drawbacks they must work on are:

Opportunities Threats

- Enlarging business by opening new branches in rural areas

- Increased competition by foreign and local banks

- Innovation of new service

- Political involvement in decision making

- Increasing demand for account opening, loan, import, export and L/C through proper promotional activities

- Forecast of low growth in national economy due to adverse world economic situation and recession

- Fully utilizing incentives provided to Islami banks

No enough ATM Booths

Social Islami bank does not have much ATM booths in Dhaka City and outside Dhaka as well. So the customer faces problems for withdrawal of money. Where the other commercial banks have emphasized on the ATM Boot, SIBL is far away from the competition.

To ensure the customer satisfaction SIBL must increase the number of ATM booth in whole Bangladesh.

Bad network of ATM Booth

During my internship period I have noticed many times that the customers are complaining about the ATM booths. Sometimes the clients can not withdraw their money from the booth in spite of having balance in the account. Service of ATM booths must be updated.

Captured card

The debit/credit card of Social Islami Bank Limited is the VISA debit card. So it can be used in other VISA Card booths. But sometimes the card gets captured by those booths. That’s why the client face hassles. They need to give application to recover the captured card. I think this is the responsibility of the card division of SIBL.

No Automatic Transaction Profile

Transaction Profile is the profile of the client of savings and current account in which they mention an approximate amount of money which can take place in every transaction or the total amount of transaction in a certain month. Sometimes the client may violate the Transaction profile where there transactions exceed that certain amount. In SIBL if the TP violates the software does not notify that. So in every month the offices need to check the transaction profile of every client which is very time consuming. To avoid this updated software is required.

No Circular for the changing rates of deposits and loans

The rate of deposits and loans are fluctuating all the time. Whenever the rate changes an updated chart of rate or installment is needed for the customers. For DPS the customers need a chart to know about the installments and profits from the certain period. When the rate changes, the installment amount and maturity changes as well. But there is no updated circular or chart for the depository amount or maturity.

The head office should provide a new chart for the deposits and loans to all the branches. So the customer will not face any confusion.

No updated form

The account opening forms are not updated enough. All the accounts have the same form which is very confusing for the clients and the officials. For better customer service, the forms need to be more updated.

No enough promotional activities

SIBL does not give enough emphasizes to the promotional activities which results less popularity of it. When more people will get to know about the services , more people would like to involve with it.

Less motivational activities

The motivational activities can increase the quality of the performa.nce and can take the organization in the higher position. To get better performance from the employees the motivational activities should be broaden. Such as:

- High-quality work environment

- Standard amount of salary

- Other beneficiary things

- Poor service quality

The customer service quality is not satisfactory enough according to the perceptions of the customers, in terms of responsiveness and assurance of the employees in comparison with other banks. Most of the employees are not aware of the segmentation of the customers, which results into dissatisfaction of those customers.

Lack of waiting place

Compared to the amount of customer the waiting place for them is too little. The branch Manager should pay more attention to the comfort of the customers.

Conclusion

The Banks always contribute towards the economic development of a country. Compared to other Banks SIBL is also playing a leading role in socio-economic development of the country. The bank is currently doing average. By analyzing its performance it is observed that a potential growth might be accelerated through effective implications of some policy. Being an old generation bank it has an advantage compared to newly established bank in the form of wide range of activities. However policy implication needs to be as fast as possible to grab the early mover advantage. The bank through years has been able to spread operation in mass banking rather than concentrating in niches. It can hedge poor performance of one sector by some other sector for its wide range of offering. Capital market operation has become a great potential for the bank to increase its profitability. SIBL is concentrating to establish new work stations in order to facilitate investor of remote places. The bank has been able to create a multi component portfolio. However none performing are a real challenge to the sound general banking management. Default is increasing for lack of monitoring. The bank is trying to increase its quality by accelerating its recovery policy.

Recommendation for Future Strategic Action

To satisfy customers it is very important to provide customer with better service and no service gaps. Work experience and observation help me to draw the following recommendation:

- Employees of SIBL should be more responsive in terms of service delivery. Proper training should be provided if needed.

- SIBL should identify the target customer group

- Branch location should be in more secure place to make the customers feel secure as well as the employees

- Adequate place should be there for all the departments and the customers to avoid crowd

- SIBL should create awareness and consciousness among the clients of the bank’s Current image

- Call centre can be established for receiving complains and suggestions.

- Telephone network should be developed

- All the tasks should be equally distributed to all the employees

- Evening bank should be introduced

- 5 pages cheque book can be provided with new account to avoid lengthiness

- Credit card holder customers should be informed few days before the card‟s expired

- Bar code can be used in cheque leaves to avoid fraudal activities.