Introduction:

Generally by the word “Bank” we can easily understand that the financial institutions that deal with money. But there are different types of banks like; Central Banks, Commercial Banks, Savings Banks, Investment Banks, Industrial Banks, Cooperative Banks etc.

When the term “Bank” without any prefix, or qualification it refers to the “Commercial Banks”. Commercial banks are the primary contributor to the economy of a country. As banks are profit earning concern; they collect deposit at the lowest possible cost and provide loans and advances at higher cost. The differences between two are the profit for the bank.

Banking sector is expanding its hand in different events every day. At the same time the banking process is becoming faster, easier and the banking area becoming wider. In order to survive in the competitive field of the banking sector, all banking organization are looking for better service opportunities to provide their fellow clients. As a result, it has become essential for every person to have some idea on the bank and banking procedure.

First Security Islami Bank Ltd (FSIBL) is one among the best and most important bank for the Banking system of Bangladesh who are trying to convey Islamic Banking services as well as doing commercial banking. Like other banks & financial intermediaries, they perform a critical function of facilitating the flow of funds from surplus units to deficit units. Like other banks FSIBL also have different sections such as section focusing on lending; a section helps in foreign trade, a section that collects deposits.

Origin of the Report:

The report entitled as “Foreign Exchange Operation of First security Islami Bank Ltd” and this report is the result of 3 months internship in “Mohakhali” branch of ‘First security Islami Bank Ltd’.

I have tried to prepare the report in such a way that it reflects what I learn during the orientation period. I tried to clarify my experience with practical knowledge on overall banking & customer service activities.

My course instructor ‘Mr. Muhammad Musharaf Hossain Mollah has authorized me to prepare a report on “Foreign Exchange Operation of First security Islami Bank Ltd”

Objectives of the study:

The main objective of education is to acquire knowledge. To acquired knowledge ultimately we must do some practical application in addition to theoretical knowledge. Through this report, I tried my level best present my practical knowledge as well as to find out-

1. Draw a general picture of foreign exchange operations in FSIBL.

2. The views of import & export sector of Bangladesh through FSIBL.

3. Find out the contribution in remittance of FSIBL.

Scope of the study:

The First Security Islami Bank Limited is one of the leading bank who operating Islamic banking. The scope of the study is quiet wide as this report has covered the overall banking activities. But it has been tried to emphasize on foreign exchange.

It also includes a brief overview of the organizational structure and policy of the First Security Islami Bank Limited. The study would focus on the following areas:

1. General banking, Credit Operation and Foreign Exchange of FSIBL.

2. Financial statement of FSIBL.

3. Credit appraisal system of FSIBL.

4. Organization structures and responsibilities of management of FSIBL.

Methodology:

The report is based on avalitative in nature. For preparing the report, I have undergone group discussion, collected data and asked some questions and have taken interviews of the bank officials. I have also gone through different brochure, manuals, magazines and annual report of the bank. However I have collected data from the following sources, which has helped me to make this report.

The “Primary Sources” are as follows:

- Face-to-face conversation with the respective officers and staffs of the Branch

- Informal conversation with the clients

- Practical work exposures from the different desks of the four departments of the Branch covered.

- Relevant file study as provided by the officers concerned.

The “Secondary Sources” of data and information are as follows:

- Annual Reports of FSIBL.

- Periodicals published by Bangladesh Bank

- Web site of the FSIBL

- Different related bank documents

- Prior research report

- Various books, articles, compilations etc. regarding general banking functions, foreign exchange operations and credit policies.

- Unpublished data received from branch.

- Different circular sent by head office of FSIBL.

The report has made with help of Microsoft Office tools – Microsoft Office Word-2007, Microsoft Office Exel-2007, Microsoft Office Picture Manager etc.

Limitations of the Study:

The main limitation here is as an internee I could not share all the information every time for the organization internal security. There are some other limitations these limitations are as follows:

- The major Problem was time constraints. The duration of my internship Program was only three months. But this allocated time is not enough for a complete and fruitful study.

- Bank is a sophisticated business sector. So Bank is not interested to provide me confidential data. As a result in my report there is a confidential data limitation.

- Bank is very busy organization in comparison to others. There is rush of people for about whole the day and the officers have to transact with them. So it is very tough and sometimes burden for them to allocate extra time for an Internee.

- The bank has very little adequate quality of readymade data and information. I have to find out different types of information from their files and other manuals. It was very much difficult and time consuming.

- Another problem was that it creates a lot of confusion regarding verification of data in case of interview from more than one person.

- Entrance to every nock and corner of the bank was not possible for me.

- Finally, I carried out such a study on Islamic bank for the first time. So, experience was one of the main constraints of the study.

Meaning of Export:

Export means lawful carrying out of anything from one country to another country for sale Export business handled by the FSIBL during 2009 stood at 1610.17 million, showing a growth of 73.30 percent from TK. 928.70 million during 2008.To become an exporter an ERC (exporter Registration Certificate) must be obedient from the office of CCI & E.

Definition of Exporter:

The importers and exporters trade of the country is regulated by the Importers Exporters control act 1950. No person / firm is allowed to export any thing from Bangladesh unless he is registered with CCI and E under the registration order (Importer and Exporter) 1952. To become an exporter an ERC (exporter Registration Certificate) must be obedient from the office of CCI & E.

Procedure for Maintaining Export Registration Certificate (ERC):

For obedient Export Registration Certificate (ERC), intending Bangladesh Exporters are required to apply to the CCI & E authority in the prescribed from along with the following documents:

- Nationality Certificate

- Copy of valid Trade License

- Income Tax Certificate

- Bank certificate

- Copy of rent receipt of the business firm

- Registered partnership deep in case of partnership concerns

- Memorandum of articles & association and incorporation certificate in

On satisfaction of the CCI & E the potential exporter is advised to deposit export registration fee of TK.1, 000 /- through treasure chalan to Bangladesh bank / sonali bank for enabling them to issue ERC. The ERC may be renewed every year on payment of renewal fee of TK.1, 000/- through treasury chalan as started.

Different Types of Export:

There are three types of export. Those are given below:

- Export under L/C

- Consignment basis export

- Export against advancement payment

Export under L/C:

Exporters are allowed to export the commodity under irrevocable letter of credit. Under this type of export, exporter will ship the goods as pr terms of the credit and will get payment as per arrangement as arrangement of the credit.

Consignment basis export:

Exports are allowed against firm contract. As per contract, importer will ship the goods and the buyer will make payment after selling the consignment.

Export against advancement payment:

Sometimes exporter receives payment in advanced. In that case Authorized dealer should obtain a declaration from the exporter.

General Rules for Export:

There are rules, which are mandatory for export of any goods form Bangladesh. The rules are under:

- No person can export any goods from Bangladesh unless he is duly registered as an exporter with the CCI & E.

- All export must be declared on the on the EXP form, which is consisting of 4 copies.

- Export much is against any of the following:

a. Export L/C.

b. Firm Contract

c. Advance Payment.

- Transport documents related to land route or sea and any other Authorized Dealer. The Airway Bill And Any Other documents of title to car 4 go may be drawn to the order of a bank in the country of import. However in case of advance payment transport document may be drawn to the order of Foreign Import Bank endorsement of transport documents is prohibited Directions under SI. No shall not apply in the following cases;

- Export of Trade sample

- Personal Effects.

- Goods Shipped under the order of Govt .

- Export of fresh fish vegetable and fruits.

- Gift package for less than Tk.50/-

- EXP” must be submitted to the Bank by the exported and Bank will submit the Duplicate Copy to the Bangladesh Bank within 14 days from the date of shipment.

- Payment for goods exported should be received through an authorized dealer in freely convertible currency.

- Export proceeds must be received by the export within 4 months.

- Overdue export bills statement to Bangladesh Bank should be submitted by the 15th of the month following quarter to which it relates.

Stages & Mechanism of Export:

There are some stages and mechanism of export. Those are given bellow:

- Exporter will make the goods ready for shipment.

- Arrangements have to be taken for inspection of goods by the competent authority as per credit terms.

- Exporter will declare on EXP form against export L/C firm contract /advance payment.

- Exporters have to arrange approval for export from custom authority on EXP from by submitting export L/C, export permission from CCI & E.

- After completion of custom formalities, shipping company will receive the goods and will issue B.L.

Export Document Checking:

After submission of export document by the exporter, FSIBL must check, whether the entire required document submitted or not. FSIBL must examine all document stipulated in the credit with reasonable care to ascertain or not they appear, on their face to be in compliance with the term and condition of the credit .Document not stipulated in the credit will not be examined by the FSIBL. To examine document FSIBL must follow the L.C term and international Banking practice.

Some Common discrepancies in export document:

- Late presentation

- Part shipmen effected

- Consignee/Notify party differs

- F. CR presented instead of B/L

- B/L shows “freight collect “instead freight prepaid

- B/L is clause

- Description of goods differs

- Unit price differs

- Per shipment inspection certificate absent

- Late shipment

Export Financing:

To meet up the cost of goods to be exported, the exporter may require Bank finance. Besides, he may require finance for go down rent, freight etc. Even after shipment of the goods, exporter may require Bank finance to meet-up his expenditure up o repatriation of the export proceeds. There are two type of export finance:

- Pre-shipment finance

- Post -shipment finance

Pre-shipment finance:

Per-shipment investment is finance, allowed by a Bank to an exporter, to meet the cost up to shipment of the goods to overseas buyer. The purpose of the investment is to purchase raw materials or finished goods or manufacturing processing, packing and transporting the goods.

Post-shipment finance:

There is time gape between exports of the goods and realization of the proceeds. So exporter may require finance in that period to continue his business. So Bank may finance against export document ensuring the following:

- Export document comply the credit terms.

- Buyer is Bona-fide.

- Parties past performance is satisfactory.

- Any other security in case of export under contract.

Security of Pre-Shipment Investment:

Security of pre-shipment investment is given bellow:

- FSIBL will mark on the related export L/C.

- FSIBL will finance against having sufficient time to procure the goods for export.

- Finance to be after arrival of the imported raw materials under Back to Back L/C.

- FSIBL will supervise the production from time to time ensure export of the goods in time.

- FSIBL will adjust the liability proportionately from related export documents.

EXP Requirement:

All export from Bangladesh must be declared by the shipper on EXP form to the FSIBL enabling them to submit the duplicate within 14 days from date of shipment. The shipper is required to repatriate the export proceeds within 4 months from the date of shipment otherwise penalty is imposed upon them A careful watch is to be ensure that the sale proceeds are received on due date. A due date diary must be maintained to pursue the individual case.

Inspection of Goods:

The goods should be kept ready for inspection of the competent authorities and issue a certificate of quality control required under regulation: for example:

- Export promotion Bureau.

- Custom Authorities who will inspect the goods under Sea customs Act.

- Chamber of commerce and industry.

- Other agencies authorized to inspect the goods before shipment.

Send shipping advice:

On shipment of goods and receipt of bill of lading and other documents from the clearing and forwarding agents send a shipping advice to the importer abroad so that the latter may stand making arrangement for taking delivery of the consignment.

Shipping Requirement of Exporter in the Context of Export:

Every exporter under foes certain sequential formalities when takes up the venture of exporting goods First of all the exporter comes into contact with the buyer and negotiate the commodity contract, while negating the commodity contract and exporter takes into consideration three resects:

- A Cost of the commodity

- Insurance.

- Freight component

Required Documents /Papers of L/C Stipulation:

There are different documents and papers of stipulation are given bellow:

- Commercial invoice

- Certificate of origin

- Negotiable bill of lading

- Pre-shipment inspection certificate.

- Quantity and Quality certificate.

- Fumigation certificate depending the nature of cargo

- Photo sanitary certificate depending the nature of cargo

Sending Export document on Collection:

If the documents are discrepant exporters Bank will send the document to the issuing Bank on collection, at the request a risk of the exporter. At the time of sending documents on collection the following voucher to passed.

- Dr. outward foreign bill lodged A/C

- Cr. outward foreign bill lodged A/C

After realization of the proceeds, above entries to reserve and the following voucher to be passed.

- Dr. IBG A/C IBW@ Mid rate (Bangladesh Banks buying rate +TT documentary /2)

- Party’s current account

- Cr. Party’s investment account

- Cr. Party’s investment income a/c

- Cr. Income a/c

- Cr.Telex charge

- Cr. F.C held against Back to Back L/C

Meaning of Remittance:

The word “Remittance” originates from the word “remit” which means to transmit money/ fund. In banking terminology, the work “remittance means transfer of fund one place to another. When money transferred from one country to another is called “Foreign Remittance”

Foreign Remittance:

The basic function of this department are outward and inward remittance of foreign exchange from one country to another country. In the process of providing this remittance services; it sells and buys foreign currency. The conversion of one currency into another takes place at an agreed rate of exchange in where the banker quotes, one for buying and another for selling. In such transactions the foreign currencies are like any other commodities offered for sales and purchase, the cost (convention value) being paid by the buyer in home currency, the legal tender

Function of the Remittance Section

- Handling of all incoming and outgoing foreign and local remittance is the major

- Function for this department.

- Handling of incoming and outgoing T.T.

- Outstation Cheque Collection.

- Outstation Cheque Purchase.

- Demand Draft Handling.

- Other assorted work

Remittance of Fund:

Remittance of fund is to be collected in two ways. First of all, it comes from inward basis and then, it happens outward.

Inward remittance:

Any person can remit funds to another through Inland remittance by using the following means of remitting funds with charges

- Pay Order (PO).

- Demand Draft (DD).

- Telegraphic Transfer (T.T).

- Mail Transfers

Pay Order (PO)

A pay order is a written under, issued by a branch of the Bank, to pay a certain sum of money to a specific person or a bank. It may be said as to be a banker’s cheque as it is issued by a bank and payable by itself.

Demand Draft (DD)

This is an instrument through which customers money is remitted to another person/Firm/organization in outstation (outside the clearing house area) form a branch of one Bank to an outstation branch of the same Bank or to a branch of another Bank (with prior arrangement between that Bank with the issuing branch).

Telegraphic Transfer (TT)

A Telegraphic Transfer is a method of remittance, which is effected by the banker through a coded telegram attested by secret cheek signal, on receipt of which, the paying office pay the amount to the payee by crediting his account.

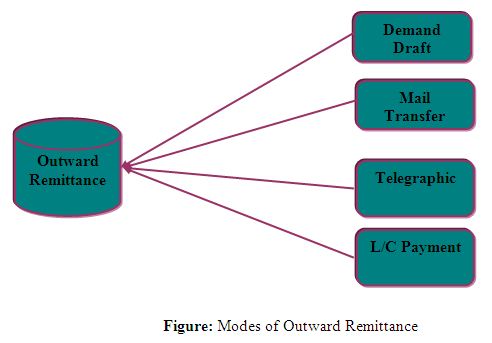

Outward Remittance:

Remittance from our country to foreign countries is called outward foreign remittance. On the other word, sales of foreign currency by the authorized dealer or formal channels may be addressed as outward remittance. The authorized dealers must utmost caution to ensure that foreign currencies remitted or released by them are used only for the purposes for which they are released. Out ward remittance may be made by appropriate method to the country to which remittance is authorized. Most outward remittance is approved by the authorized dealer on behalf of Bangladesh Bank. Outward remittance may be made for following purposes –

- Travel

- Medical treatment

- Educational purpose

- Attending seminar etc.

- Balance amount of F.C account.

- Profit of foreign companies.

- Technical assistance

- New exporters up to USD 6,000/- for business promotion

- F.C. remittance can be made for fare, exhibition from export retention quota.

Outward remittance in favor of beneficiaries outside Bangladesh may be made in any of the following manners:

SWOT Analysis:

Every organization is composed of some internal strengths and weaknesses and also has some external opportunities and threats in its whole life cycle. The following will briefly introduce the First Security Islami Bank Ltd. internal strengths and weaknesses, and external opportunities and threats.

STRENGTHS

- Superior Quality: First Security Islami Bank Ltd.. provides its customers excellent and consistent quality in every service. It is of priority that customer is totally satisfied.

- Dynamism: First Security Islami Bank Ltd.. draws its strength from the adaptability and dynamism it possesses. It has quickly adapted to world class standard in terms of banking services. It has also adapted state of the art technology to connect with the world for better communication to integrate facilities.

- Efficient Management: All the levels of the management of FSIBL are solely directed to maintain a culture for the betterment of the quality of the service and development of a corporate brand image in the market through organization wide team approach and open communication system.

- Experts: The key contributing factor behind the success First Security Islami Bank Ltd of is its employees, who are highly trained and most competent in their own field. FSIBL provides their employees training both in-house and out side job.

- Deposit income: The number of depositors through MMDS, MTDR and savings account is comparatively higher than other banks.

WEAKNESS

- Limited Workforce: FSIBL has limited human resources compared to its financial activities. As a result many of the employees are burdened with extra workloads and work late hours without any overtime facilities. This might cause high employee turnover that will prove to be too costly to avoid.

- Poor Technology Infrastructure: As previously mentioned, the world is advancing e-technology very rapidly. Though FSIBL has taken effort to join the stream of information technology, it is not possible to complete the mission due to the poor technological infrastructure of the country.

- Lack of ATM Booth: FSIBL has not their own ATM booth. They have to use the booth of Duch Bangla Bank.

OPPORTUNITIES

- Government Support: Government of Bangladesh has rendered its full support to the banking sector for a sound financial status of the country, as it has become one of the vital sources of employment in the country now. Such government concern will facilitate and support the long-term vision of FSIBL.

- Evolution of E-Banking: Emergence of e-banking will open more scope for the Bank to reach the clients not only in Bangladesh but also in the global banking arena. Although the bank has already entered the world of e-banking but yet to provide full electronic banking facilities to its customer.

- Information Technology: Banking and information technology might give the bank leverage to its competitors. Nevertheless there are ample opportunities for FSIBL to go for product innovation in line with the modern day need.

THREATS

- Mergers and Acquisition: The worldwide trend of merging and acquisition in financial institutions is causing concentration. The industry and competitors are increasing in power in their respective areas.

- Frequent Currency Devaluation: Frequent devaluation of Taka and exchange rate fluctuations and particularly South-East Asian currency crisis adversely affects the business globally.

- Emergence of Competitors: Due to high customer demand, more and more financial institutions are being introduced in the country. Many banks are entering the market with new and lucrative products.

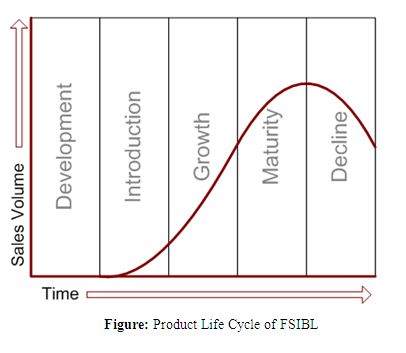

Product Life Cycle (PLC) For FSIBL:

From the figure of Product Life Cycle we see that the position of FSIBL is in Growth stage where market acceptance and profits increasing rapidly. The company uses several strategies to sustain rapid market growth as long as possible. They trying to improve their service quality and adds new features and models to provide the best services for their customers.