Uttara Bank Limited is the leading bank in the private banking sector. It was incorporated as a banking company on 29.06.1983. It has now 211 branches all over the Bangladesh through which it carries out all its banking activities. Among 211 branches, 38 branches are Authorized Dealer (AD) branch, which deal with the foreign exchange business. Kalabagan Branch is one of the potential branches of Uttara Bank. As an Authorized Dealer branch, the branch has been continuing to extend special importance on foreign exchange business. With the enthusiastic endeavor of a good number of skilled officers the branch has been recording significant growth in its business during the last couple of years. There exists a congenial atmosphere among the officers in the branch. Historical data, customer profile and team spirit of the officers give hope to its management that the branch will see notable success in its future operation.

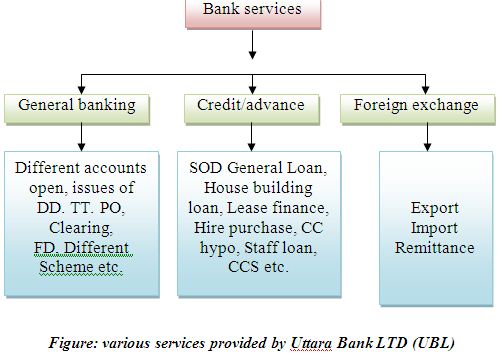

kalabagan branch of Uttara bank limited conducts all types of commercial business activities. such as rendering personal credits, local and foreign remittances and all types of foreign exchange business, loans and advance, bill receiving and collections. So the bank strategy is gradually cover total area of banking.

Foreign Exchange business is regarded as an emphatic field of a nation’s economic development activities and the commercial banks play immeasurable role to assist foreign exchange as well as international trade of the country. A bank’s foreign exchange section includes import, export, remittance and handling of foreign currency accounts.

Import means the flow of goods and services purchased by consumers, firms and government of one country from economic agents located in another country. Import is essential for the prosperity of the trading nations.

Export is one of the important activities to increase economic and social being, to build exchange reserve and to create wealth in a country. Export means transaction of goods and services from domestic economic agents to foreign economic agents for which domestic economic agents receive payment. Commercial banks extend financial support to the exporters in pre-shipment and post shipment stage which include export cash credit, packing credit, back to back L/C, advising and negotiation of export bills& so on.

Letter of Credit is an assurance of payment by the bank. Documentary Credit is an arrangement whereby bank (issuing bank) acting at the request and on the instruction of a customer (the applicant) or on its own behalf undertakes to make payment to or to the order of a third party (the beneficiary).

It is very much important to coincide the academic knowledge with the practical one. Keeping this view in mind, department of business administration of northern university of Bangladesh makes proper arrangement of practical orientation (internship) each year for the students of BBA program. I was placed in the Uttara bank limited kalabagan road branch for my internship program to have a practical working experience and have understanding of the real life with a closer look.

I have collected data from the two unique sources. In primary sources has collected data face to face conversation officers and office stuff and customers. In secondary sources, Annual reports of the bank and from the various sources. as well as the different books of journal. Objective of the reports has been highlighted that are such as General Banking activitiesof Uttara Bank Limited. Every study has some limitations, so this internship report is exceptional. Main constraints of the report are some internal data which bank does not publish for strong reason.

Uttara Bank Ltd. also provides the general banking service to the customer such as different categories of saving schemes, foreign exchange transactions, current account for business personal etc. at the time of my work at the branch I understood the gab between the practical and theoretical knowledge. I tried my best to make the report fruitful and my all efforts will be valuable if any one bets any sort of benefits from my report.

Finally, want to say that if any one has any suggestion or query about this report please let me know. Your suggestions will me to build up knowledge and my upcoming future.

Introduction:

Banking is one the most competitive industries of Bangladesh that has seen a huge amount of growth during the last decade. A large number of new banks have made their places in the industry and yet there are more to register in the list. In such a highly competitive service industry, the importance of customer satisfaction cannot be de-emphasized.

A commercial bank or business bank is a type of financial institution and intermediary. It is a bank that provides transactional, savings and money market accounts and that accepts deposits. Commercial banks are the deposits of individuals and business. The goal of modern banking system is to provide us with the primary contributors to the economy of the country. It is also profit making institutions that holds the best solution through consultation, design, superior hardware and software and ongoing professional support training.

To keep pace with this situation, we need banking knowledge for future career. If we want to build our career in banking area, only theoretical knowledge would not help us. As internship program is established to gather practical knowledge regarding various sector of economy, I chose to get practical knowledge regarding banking sector and I select Uttara Bank as my organization to work.

The duration of my program was 3months and during this period, I have learned many things. I observed that there is a great difference between theoretical knowledge and practical knowledge. I learned many terms, functions and nature of banking activities. I also get practical knowledge regarding organizational environment.

It covers the mission, strategy of the company and organizational structure, its functions and department of the company. Again I tried including some problems issues and industry analysis and the SWOT of the company.

Objective of the study:

The prime objectives of the report is to get practical exposure to organizational environment as well as to understand the system and methodology adopted in conducting day to day banking by The Uttara Bank Limited. Besides, this report has been composed to obtain the following objectives.

- To analyze the customer satisfaction of Uttara Bank Limited of the customer.

- To have an exposed on the banking environment of Bangladesh.

- To point out the tools of other tasks adopted by Uttara Bank Limited.

- To provide some suggestions and recommendations to improve their performances of marking.

- To gain knowledge about the company and its current functions.

- Historical background of the company.

- To gain knowledge about different jobs functions of banks.

- To have some practical experience of job life.

Area of investigation:

- Internal environment.

- Different branches.

- Corporate office of the bank.

- Customer and guest survey.

Origin of the report:

This report has been prepared for fulfilling the requirement of the internship program. Duration of the program was for 12 weeks, commencing on March 01, 2011 and finishing on may 30, and 2011.this report was assigned by the help of the supervisor and the employers of uttara bank.

The report title General Banking activities of Uttara Bank ltd.’ has been prepared as a partial fulfillment of BBA Program in Northern UniversityBangladesh. For this purpose each of the students is required to attach with an organization and has to undertake and involve in investigation on the organization for detailed study.

The basic purpose of this attachment is to expose the student to the real business world. This exposure acquaints his with the practices of modern business world. This exposure is very helpful is seeing for oneself how thing move and to find the gap as well as the similarities between theoretical and practical knowledge.

Background of the study:

Business world is becoming very much complex day by day. Without sufficient practical experience business becomes difficult and in some cases impossible. The whole world is moving because of business relation. Business plays a very important role in developing economy of a country. So, in the business world, practical experience is regarded as a media through whom we have an acquaintance with the real world.

The Bachelor of Business Administration (BBA) was introduced by Northern University Bangladesh with an objective to supply an adequate number of highly trained and educated graduates to the economy. As the BBA program is the integrated, theoretical and practical method of teaching students of this program are required to have practical exposure in own different major disciplines in the preceding years of their courses.

I was authorized to prepare a report on General Banking activities of Uttara Bank Ltd. for partial fulfillment of my course requirement.

Scope of the study:

This report covers the actual opinion of the customers or the potential customers and the guests who came through uttara bank of kalabagan branch. It also covers the banking activities, such as payment collection, loan against trust receipts, loans and advance, recovery of loans, reimbursement/C opening, advising, negotiating, and confirmation, foreign and local remittance of bank, bill receive and bill collections, issuing of D.D,P.O,M.T,T.T as well as problems in banking process.

Scope in this section is very broad to analyze, as information is very unavailable human resource department and customer care department are the major scope while doing this study and also the website has helped me also to collect data. Only problem that occurred while collecting the problem issues. This problem and performance analysis of kalabagan branch of Uttara Bank Limited was carried out to determine the progress of bank in the future.

Methodology:

This methodology was chosen to provide an initial rapid assessment of this complex and dynamic sector. Basically, this is a theoretical study. But there are some quantitative information incorporated to pin point the reality. Throughout the study, several subjects are highlighted requiring further study. The methodology of the report includes direct observation, oral communication with the employees of all departments of Uttara Bank Limited kalabagan branch, studying files, circulars etc as well as practical experience. This information of this report has been collected from two sources:

1. Primary sources:

*Practical desk work.

* Face to face conservation with the officers.

*Getting information from questionnaire survey on customers of satisfaction.

2. Secondary sources:

*Annual report of UBL.

*Website of UBL.

*Newspaper (financial express).

*Documents of UBL kalabagan branch.

*Bangladesh bank circular.

*Desk report of related department.

Business portfolio of uttara bank:

The aim of the Bank is to participate actively in the socio-economic development of the nation by operating a commercially sound Banking system. It provides credit to deserving borrowers and at the same time protects depositors’ interest and thereby earning more and more profit for the shareholders. In simple, to secure deposit from the customer and to lend the deposit again to customer is the Uttara business of Uttara Bank. Apart from traditional Banking activities, Uttara Bank facilitates its clients with extending credit to traders to boost up their business, to finance export import trade, to finance industrial sector and to support financially to different priority sectors. Financing small and medium enterprise with particular attention to export business and agro based industry has been focused. Small loan scheme for small entrepreneur is an innovation in the credit scenario of Uttara Bank. Here are the main activities of Uttara Bank described briefly.

Limitation:

There are many factors which affected me on my way making the report General Banking activities of UBL; I have much personal limitation for which I failed to prepare a better report. Some Limitation which affect me are given below-

- I have no of previous experience which is hampers my work.

- For the Lacking of sufficient data I am failed to make the report highly informative.

- To prepare this report I have faced a lot of problems such as time limitation.

- Less co- operation from respondent etc.

- They do not use modern equipment to record the databases regarding the customers and clients.

- As there are not any report, literature, publication on the past so collection of different data may not Wholly representative.

Overview of Uttara Bank Ltd

Uttara Bank Ltd. had been a nationalized bank in the name of Uttara Bank under the Bangladesh Bank (nationalization) order 1972, formerly known as the Eastern Banking Corporation Limited. The Bank started functioning on and from 28.01.1965. The government of Bangladesh nationalized all the banks of the country under president’s order no 26th of 1972 for the purpose of exerting social control over the resource of the country. They undertaking of the existing banks was renamed. As a result Uttara Bank Ltd was formed. Uttara Bank Ltd. formed talking over all the assets and liabilities of the “Eastern Banking Corporation Limited” of former East Pakistan.

It was the only Bengali own private bank in East Pakistan. Uttara Bank Ltd. Converted as a public Limited company in the year 1983. The Uttara Bank Ltd. Was incorporated as a banking company on 29.06.1983. Uttara Bank Ltd. Was incorporated as a company with an Authorized capital of Tk.20, 00, 00,000 dividend into 20, 00,000 shares of Tk.100 each. The bank obtained business commencement certificate on 21.8.1983. The bank floated its shares in the year 1984. It has now 211 branches all over the Bangladesh through which it carries out all its banking activities. The bank listed in Dhaka Stock Exchange Ltd. and Chittagong Stock Exchange Ltd. as a publicly quoted company for trading of its shares.

Vision Statement:

To stand out as a pioneer banking institution in Bangladesh and contribute significantly to the national economy.

Mission Statement:

- High quality financial services with the help of the latest technology.

- Fast and accurate customer services

- Balance growth strategy

- High standard business ethics.

- Steady return on shareholders’ equity.

- Innovative banking at a competitive price.

- Quality human resource.

- Firm commitment to the society and the growth of national economy.

Organizational Structures of Uttara of Bank Limited:

Truly organizational form follows function, for Banks usually are organized to carry out the roles assigned to them as efficiently as possible. Bank size is also a significant factor in determining how Banks are organized. However, a Bank’s role and size are not the only determinants of how it is organized or how well it performs. Government regulation too has played a major role in shaping the performance and diversity of banking organizations that operate around the globe. The organizational structure of Uttara Bank Ltd. is as under:

Credit Risk Management:

Credit risk is the possibility that borrowers may fall to meet their obligation in accordance with the agreed terms. So, it is essential that banks have robust Credit Risk Management policies and procedures. UBL always acknowledge that effective risk management is the key to steady and stable growth for the bank. The loan application assessment process starts at the branch level by the relationship managers through zonal office and ends at Credit Risk Management approval unit. CRM Unit analyses the proposal from different perspectives in line with lending policy of the bank. Then if the proposal is found business worthy CRM unit place sit to the credit committee and the concerned authority approves the loan.

Foreign Correspondents and Exchange Houses:

The bank kept on developing and maintaining correspondent banking relationship with the reputed deserving Banks. The expansion of network has helped the Bank to increase its foreign business. The network covers most of the important business and trade centers in the world. After enlistment of the bank as a member of SWIFT and for effective expansion of its networks the inter-bank remittance has been increased and as a result the bank is able to remit the fund the customer quickly.

The total number of Foreign Correspondents and Agents of the Bank was 696 as on 31-12-2011 which was increased by 48 than to previous year. At the same time the Bank handled Foreign Remittance business through 55 Exchange Houses one among them, named “Arabian Exchange Co. W.L.L” of Doha at Qatar has been functioning under Bank’s own Management. On the other hand Bank has tied with contract with America based international money remitting organization named “Money Gram” through which expatriates can remit their money to home from any corner of the world. Payee gets the proceeds through their 207 branches with their best efforts in short time.

Foreign Remittance and Products:

Uttara Bank Ltd. has been a successful year in 2009 in terms of expansion of its remittance business with its foreign correspondent and exchange houses. The volume of foreign remittance in the year 2009 stood at Tk. 29, 575.3 million as compared to the volume of Tk. 28,728.1 million in preceding year registering an increase of 2.95 percent. In order to keep pace with the time a scheme namely “Express Payment Scheme” has been introduced for inward remittance by using modern equipment. Under this scheme a payee having his account with any branch of Uttara Bank Ltd. Gets the proceeds of remittance sent from any part of the world within 2(Two) hours. Besides, in order to ensure speedy and improved service the Bank has also introduced “Instant Cash Scheme” for payment of foreign remittance in cash to the customers who have no account with the Bank on submission of Passport/Driving license/Remittance card (issued by this Bank)/Voter ID card/ Credit card etc. as identity. Under the scheme the Bank will make payment of the proceeds in cash if the Bangladeshi expatriates send their money furnishing the passport/card holder’s name and number of the passport/card. Under prior arrangement, the remitting company remits their drafts printed at International Division through the web site and delivered the same to the beneficiary’s home address for payment of money equivalent to foreign currency under a scheme named “Instant Draft”.

Training and Human Resources:

The bank give utmost importance for making continues investment in Research and Development and d training to achieve operational efficiency in the competitive global banking scenario. The bank’s human resource policy is to recruit and build up quality manpower having skill and professional expertise. Skilled human resource is life blood for development of any service industry. The Training Institute of the Bank situated at Eastern Plus, Dhaka which is nicely decorated and equipped with the sophisticated instruments has been striving to bring about a qualitative change in human resources of the Bank by imparting continuous different training throughout the whole year. Besides’ this, a number of executives and officers were sent to various Training Institutions including Bangladesh Institute of Bank Management (BIBM) and abroad for higher training. During the year 2009 the training Institute of the Bank arranged 17 different training courses for the officers and members of the staff of the Bank in which as many as 807 officers and members of the staff of the Bank participated. At the same time 229 officers and members of the staff of the Bank attended training courses/workshops/seminars conducted by BIBM, 30 officers received training from Bangladesh Bank, 8 officers obtained training from other training Institute and 12 officers obtained training from abroad.

| (a) Executive (Asst. General Manager & above) | 147 | 4.23% |

| (b) Officers | 2,225 | 64.01% |

| (c) I Asst. Officers | 327 | 9.41% |

| (d) Others | 777 | 22.35% |

Total: | 3,476 | 100.00% |

Audit and Inspection:

Under Internal Control and Compliance the bank has separate Audit and Inspection Unit engaged in identify lapse and irregularities in the field level and also to find corrective measures. Experienced Officials regularly audit and inspect the activities of the Bank throughout the year. During the year 2009 Bangladesh Bank Audit & Inspection Team undertook Audit & Inspection works in 19 Authorized Dealer branches, 64 other branches and Head Office.

Commercial Banking:

Uttara Bank is largely involves in commercial Banking operation. Besides providing quality services to customer, priority has been given to expand free-generating business and low-risk products.

Corporate Banking:

The Bank’s corporate division department has successful in developing project finance business, and the Bank has been involved in many key project finance operated in Bangladesh. The Bank has institute several initiatives in the corporate Banking department to improve asset quality. These initiatives include an independent review of all credit proposals by Risk Management Department and use of risk rating system to improve objectivity in the evaluation of credit proposal.

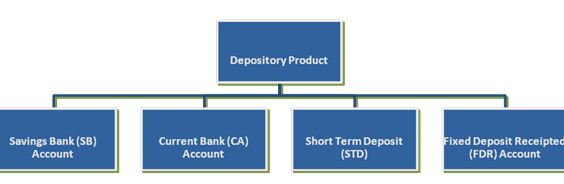

Products and Services (Financial Product):

The products and services of Uttara Bank Limited can be broadly classifies into two groups. i.e. depository products, loan products. These are given below.

Retail Banking:

The Bank’s retail banking business continues to be very active. The Bank has a network of Two hundred two (202) branches in the country. The Bank has sharply focused on key customer segments to profitable deliver a well tailored set of products and services through expanded distribution channel with high levels of efficiency and productivity. During the last three years, Uttara Bank has also created a few field sales and service organization for expanded customer reach.

Loan Products:

The Uttara Bank Limited is offering the following loan and advances products to the client for financing different purposes that fulfill the requirements of the Bank and have good return to the investment as well satisfy clients.

Management of the Bank:

Board of directors is the sole authority to take decision about the affairs of the business. There are 12 directors in management of the Bank. All the directors have good academic background and have huge experience in the business. The Boards of directors hold meeting on a regular basis. There are different committees in the Bank for the efficient management of the Bank.

- Board of directors.

- Policy committee.

- Executive committee.

- Credit committee.

General Banking:

General banking is the heart of the banking operations as it is involved in drawing deposits from the surplus units for creating assets of the bank; so that these assets can be utilized by providing loans and advances to deficit units, which is the major source of bank’s earning. This department provides everyday services to the customers and thus, it is also known as Retail banking. The major functions of general banking are: accept deposits, provide cash by honoring checks on customers’ demand, remit funds, open account, issue checks etc. These functions are further elaborated in the subsequent paragraphs.

Account Opening, Transfer and Closing:

Customer relationship with the bank begins with the opening of account and if builds the first impression of customers on the banking services. Thus, general banking has very important role of building customer attraction. The account opening is done on an application of the customer with due investigation of the personal accounts and identification of another account holder of the same bank. Any person except minor, insolvent, bankrupt, lunatic can open bank account.

Account Transfer and Closure:

In UBL, transfer.4.2 Account of account is allowed from one branch to another on request of the account holder duly justified. In this case, the original signature card is transferred to the new branch, when the manager approves the transfer, when customer desires so, the account is inoperative for long time, in case of customers’ death, insanity or insolvency or on court order. To close an account, the account holder must return the checkbook and pay taka 200 as closing charge.

Issuing Check Book:

Checkbooks are issued to account holder on opening new account or as replenishment of old checkbook to old account holders against requisition on the prescribed application form. For security purpose, a security number is generated for every leaf of the book by the manager or authorized person and necessary entries are made in Check Issue Register. In case of lost checkbook, duplicate book is issued duly verified in respect of signature.

Depository Products and Services

Corporate branch accepts both demand and time deposits. To make deposit transactions, the branch offers the following types of accounts:

Ancillary Services (Local Remittance):

Customers’ Remittances from one place to another within country is costly and risky. Thus, the bank remits funds on behalf of the customer for commission and providing service to the customer through its network of branches. There are the following modes of remitting funds locally:

• Pay Order (PO).

• Demand Draft (DID).

• Mail/Telegraphic Transfer (MT/TT)

■Pay Order

Pay order is an instrument, used to remit fund within a clearing zone. Unlike check, there is no possibility of dishonoring a PO. The PO can only be encased through the branch that has issued the instrument. This instrument is prepared by the bank on payment of money in cash or check by the customer and in consideration for commission and necessary postage charges. For obtaining this service, a customer usually should have account with the bank

Issuing PO. Parties may purchase pays order by cash, by account or by transfer of money. PO is not paid over the counter (OTC); rather money is transferred to the payee’s account.

■ Demand Draft (DD)

DID, also called ‘Banker’s Draft’, is an instrument, issued by a particular branch, drawn on another branch of the same bank, instructing to pay certain sum of money. DID is issued in favor of a customer who has an account with UBL branch issuing DID. If DID amount is more than Taka 50,000, a test code is given on inter bank credit advice (IBCA) for security reason. On receipt of instrument by the payee, paying branch will make payment debiting Head Office account of issuing bank and crediting party account. A commission @ .15% is (minimum Tk 0.50) and postage charge of Tk. 20 is charged from the customer. DID cancellation charge is Tk 50.

■ Telegraphic Transfer (TT)/Mall Transfer (MT)

TT and MT differ in speed and mode of delivery, although now a days mail transfer is seldom used. For speedy rerpittacice of funds different modes of communication like telegram, telephone, Telex or Fox is used, although telephone is the most usual. No instrument is issued and the .paying branch through telegraphic instruction of the drawing branch makes payment to the customer. For MT/TT the drawer and the payee usually should have account with UBL. Inter Branch Debit Advice (IBDA) is prepared by the drawing bank and sent to respondent branch for response and reconciliation department of Head Office. A test number is given for security reason, which is verified by the respondent branch before payment. TT/MT is issued against cash, check and letter of instruction. A commission @ .15% and telex charge is debited from the customer for f his service.

■ Call Deposit Receipt (COR)

CDR is also an instrument, issued by a particular branch, drawn on another branch of the same bank, instructing to pay a certain sum of money to a person or his order and not OTC. It is similar to a PO, but differs in the manner that PO is a bill payable and CDR is a sundry deposit. This service is limited and the customer is charged with only a fixed amount for this service.

■ Collection and Clearing

Customers pay and receive bills as a result of transaction, be it for business, official or personal that is known as Collection. Commercial banks are responsible to collect bills on behalf of their customers. There are two types of bills for collection: Outward Bills for Collection (OBC) and Inward Bills for Collection (IBC).

Clearing Section:

According to the Article 37 (2) of Bangladesh Bank Order, 1972, the banks, which are members of clearinghouse, are called scheduled banks. UBL is one of the scheduled banks and is a member of clearinghouse. The scheduled banks clear the checks drawn upon one another through the clearinghouse. This is an arrangement by the central bank where every day the representative of the member banks arranges to * clear the checks. There is clearing department in every bank. This department receives checks, drafts and like instruments from its customers for the purpose of collection with a deposit slip over the counter crediting their accounts.

Inward and Outward clearing of checks is done through the clearinghouse in Bangladesh Bank. Clearinghouse opens at 10:00 am and closes at 5:00 pm. Inward Clearing bills are drawn on UBL Corporate Branch, received, from other banks in the clearinghouse by their representative and settled through respective branches, main branch on which check/instrument is drawn and Bangladesh Bank. Outward clearing bills are instruments, drawn on the other banks by UBL Corporate branch. Standard I settlement process is followed through clearinghouse.

Cash Section:

This is the most sensitive section of any bank. This section deals with all types of negotiable instruments and is responsible for receipt and payment of cash. The vault, the most secured store for cash and instruments, store money enough to maintain liquidity of the bank and as decided by the manager of the branch. Cash officer and second officer of the bank are responsible for opening and closing and accountability of the vault. The amount of opening cash balance is entered into a register and after whole day’s transaction, the surplus money balance from receipt and payment of cash is stored in the vault. This closing balance is also entered into the register.

Cash Receipt:

On depositor’s filled in deposit-in-Slip, money is received from the customer and signs with bank seal and date and the receipt is entered into the register. The Second officer of the bank on behalf of the manager signs the slip and he updates his register. The customer’s account is updated through computer posting.

Cash Payment:

The cash officer, on receipt of the check, verifies authentic of the check to prevent fraudulent encashment. He then verifies the account balance through computer operator, verifies signature with the specimen signature card, debits customer’s account through computer posting, verifies signature of the bearer of the check overleaf and if satisfied, he then sends the check to the cashier for payment. For just ified reason the cash officer may dishonor the check stating the reason and empowered to make a penalty of Tk 100, if dishonor is due to insufficient fund position.

Loans and Advances:

The making of loans and advances has always been prominent and profitable function of a bank. Sanctioning credit to customers and others out of the funds at its disposal is one of the principal services of a modern bank. Advances by commercial banks are made in different forms, such as, loans, overdrafts, cash credits; bills purchased and discounted, consumer credit etc. They usually grant short-term advances which are utilized to meet the working capital requirements of the borrower. Only a small portion of a bank’s demand and time liabilities is advanced on long-term basis where the banker usually insists on a regular repayment by the borrower in installments.

Performance of the Branch:

The Branch has been performing well in terms of Deposit, Advance and Profit from the very beginning .

Three year performance at a glance:

2010 2009(tk in lacs) 2008

| Target | Achievement | Target | Achievement | Target | Achievement | |

| 1.Deposit | 6500.00 5487.37 | 6000.00 5957.91 | 5700.00 5832.52 | |||

| 2.Loans and Advances | 3500.00 3200.55 | 2800.00 2841.64 | 2600.00 2296.72 | |||

| 3. Import. | 4000.00 3765.65 | 3500.00 3370.68 | 3000.00 2725.59 | |||

| 4. Export. | ——– ——— | ——– ——— | ———- ———– | |||

| 5.Guarantee | 3000.00 2866.61 | 2730.00 2661.93 | 5000.00 1313.27 | |||

| 6.Remittance | 5600.00 5504.47 | 5500.00 5149.93 | 6400.00 8185.39 | |||

| 7.Profit | 250.00 168.09 | 200.00 126.48 | 175.00 142.85 | |||

Customer Profile:

UBL, Kalabagan Branch is coordinately welcome all people with different occupation to transact their business through their branch .Employees of the branch are hardworking to satisfy their valued customers wants and needs. They try their best to solve their customers’ problem so quickly. The branch’s customer profile is given below:

- Cell Phone & accessories.

- Electronic goods dealers (Wholesaler, retailer and importer.)

- Medicine (Wholesaler, retailer and importer.)

- Medical Instruments importer.

Introduction of Investment Division:

Uttara Bank is a private bank. it is committed to provide high quality financial services/products to contribute to the growth of G. d. p of the country through stimulating trade & commerce, accelerating the pace of industrialization, boosting up export, creating employment opportunity for the educated youth, poverty alleviation, raising standard of living of limited income group and over all sustainable socio-economic development of the country. In achieving the aforesaid objective of the bank, investment operation of the bank is of paramount importance as the greatest share of total revenue of the band is generated from it, maximum risk is centered in it and even the very existence of band depends on prudent management of its investment portfolio. The failure of a commercial bank is usually associated with the problem in investment portfolio and is less often the result of shrinkage in the value of other assets. As such investment portfolio not only features dominant in the assets structure of the, it is critically important to the success of the bank also.

Customer Satisfaction:

Customer satisfaction refers to the extent to which customers are happy with the products and services provided by a business. Customer satisfaction levels can be measured using survey techniques and questionnaires. Gaining high levels of customer satisfaction is very important to a business because satisfied customers are most likely to be loyal and to make repeat orders and to use a wide range of services offered by a business.

In a competitive marketplace where businesses compete for customers, customer satisfaction is seen as a key differentiator and increasingly has become a key element of business strategy. It is seen as a key performance indicator within business and is part of the four of a Balanced Scorecard.

There are many factors which lead to high levels of customer satisfaction including:

Products and services which are customer focused and thence provide high levels of value for money.

Customer service giving personal attention to the needs of individual customers.

After sales service – following up the original purchase with after sales support such as maintenance and updating (for example in the updating of computer packages).

Customer satisfaction is that customers are most likely to appreciate the goods and services that they buy if they are made to feel special. This occurs when they feel that the goods and services that they buy have been specially produced for them or for people like them.

Customer Satisfaction Survey:

Customer Satisfaction Survey:

Myself I was survey the customer in this segment; here I saw most of the customer have a long time relationship with Uttara bank ltd. I am survey total 20 people. Sex was divided into two groups Male & Female. In here the number of male was 15 & female was 5. Most of the customers in this bank are service holder but there are also open account another profession’s people, The respondent occupations are divided into 5 groups. These are Service, Business, Student, Housewife and Others. Among the number of respondents occupation Service are 10 respondents, Business are 5 respondents, Students are 2 respondents, Housewife are 3 respondents, Others are 0 respondent. The customers of UBL, age are differing customer to customer. I saw that the age groups ranged from 18 years to 60 years or older are divided into 6 groups. These are 18-25, 26-35, 36-45, 46-55, and 55-65, 66 or older. Among the number of respondents age range 18-25 are 2 respondents, 26-35 are 2 respondents, 36-45 are 5 respondents, 46-55 are 6 respondents, 55-65 are 3 respondents, 66 or older are 2 respondents.

The customer of Uttara bank ltd are very much satisfied about that the procedure of account opening but the back dated technology are confused them to do their banking. UBL has a fresh environment to satisfy their customers but when some customers are comparing with other bank environment then their not properly satisfied. Most of the customers demand is to introduce on line banking & internet banking but they don’t have that service. UBL recently lounge their ATM services in the city but their both is not sufficient. They don’t have any POS outlet; it’s very much needed for their customers. UBL have a lot of human resource but they have not enough knowledge & smartness to serve the customers, some time they done rude behave to customers like government bank. Most of the employees of UBL are not attentive to their job for this reason the customers are decline. As a privet bank the advantage is that UBL have highest number of branch in all over the country. The service charge is less then other privet banks. UBL have high volume of transaction regularly specially business purpose of customers. The loan & advance facilities of UBL are much more flexible, recently UBL start to provide small female investor loan. Customers are feeling very safe for their transaction with UBL.

Conclusion: Thank for your time and talking part in this survey. I would like to remind you that your opinion is valuable for our study, as part of our quality control procedures. All the information received will be kept confidential and will be used for academic purpose only. Your kind consideration will be highly appreciated. Thanks for your nice cooperation.

Findings:

- In Uttara Bank Ltd. the coordination among lower, mid, and top level management is very good.

- In Uttara Bank Ltd. the prompt decision making by the management among there own super vision.

- It is found that in Uttara Bank Ltd. “Zero” default during the last five years foreign exchange performance report, which is very favorable in competitive market.

- In Uttara Bank Ltd. the lagging behind technologically.

- Improper record keeping system found by the employers or employees by Uttara Bank Ltd.

- Lack of job rotation. Only a selected number of officers are involved or engaged in foreign exchange department. So that in case of emergency other officer can not handle the foreign exchange department.

- Very poor in the field of export during the last couple of years.

- In Uttara Bank Ltd. there is huge network with correspondent banks abroad, it means it worked all over Bangladesh as well as the other country.

- In Uttara Bank Ltd. the experienced and skilled officers in foreign exchange department as well as some other department.

- There is no record of opening a student file in the branch which is one of the potential businesses for a bank/branch.

- In banking sector this bank’s well reputation in international arena.

- The bank was the pioneer in inward foreign remittance of our non-resident expatriates.

- Increasing inflow of foreign remittance due to widespread branch network in the rural areas and quality customer services.

- Competitive cost of foreign currency.

- In Uttara Bank Ltd. there is Integrated treasury management that is known to all.

- Potential customers’ switching to other banks consequent upon considerable number of employees turnover.

- In Uttara Bank Ltd. there is unusual expectation and bargaining from customers’ side.

- In Uttara Bank Ltd. the increasing demand from the corporate customers for discount in service charges.

SWOT Analysis of UBL:

The Bank’s strength and competitive capabilities can be shown by the SWOT analysis .The SWOT analysis is grounded in the basic principle that strategy –making efforts must aim at producing good fit between a company resources capability and its internal situation.

Strengths:

- UBL has already established a favorable reputation in the banking industry of the country. It is one the leading private sector commercial banks in Bangladesh. The bank has already shown a tremendous growth in the profits and deposit sector.

- UBL has provided its banking service with a top leadership and management position.

- UBL has already achieved a high growth rate accompanied by an impressive profit growth rate in 2001. The number of deposit and the loans advances are also increasing rapidly.

- UBL has an interactive corporate culture. The working environment is very friendly, interactive and informal. And, there are no hidden barriers or boundaries culture provides as a great motivation factor among the employees.

- UBL has the reputation of being the provider of good quality services too its. potential customers.

- Uttara Bank Ltd. Trained young and energetic human resources that the can be highly expert in banking sector.

- Uttara Bank Ltd. has nation wide branch network that customers feel vary free to be an account holder.

- Uttara Bank Ltd. has good image that is very trust worthy to the corporate level as well the general customers.

- Uttara Bank Ltd. provide better and quick service quality by the expert and they can be goods solutions to their customers.

- Uttara Bank Ltd. branches are well decorated and furnished that the employees can move easily from one department to another departmen

Weaknesses:

- The main important thing is that the bank has no clear mission statement and strategic plan. The bank doesn’t have any long-term strategies of whether it wants to focus on retail banking or become a corporate bank. The path of the future should be determined now with a strong feasible strategic plan.

- The bank failed to provide a strong quality-recruitment policy in the lower and some mid level position. As a result the Services of the bank seem to be Deus in the present days.

- Uttara Bank Ltd. has existence of trade union that can raised ones voice can be problem to the other.

- Some of the job in UBL has no growth or advancement path. So lack of motivation exists in persons filling those positions. This is a weakness of UBL that it is having a group of unsatisfied employees.

- In terms of promotional sector, UBL has to more emphasize on that they have to follow aggressive marketing campaign.

- The default risk of all terms loans have to be minimized in order to sustain in the financial market. UBL has to remain vigilant about this problem so that proactive strategies are taken to minimize this problem if not eliminate.

Opportunities;

- In order to reduce the business risk, UBL has to expand their business portfolio. The management can consider options of starting merchant banking or diversify into leasing and insurance sector.

- The activity in the secondary financial market has direct impact on the primary financial market. Banks operate in the primary financial market. Investment in the secondary market governs the national economic activity. Activity in the national economy controls the business of the bank.

- Opportunity in retail banking lies in the fact that country’s increased population is middle class. Different types of retail lending products have great appeal to this class. Different types of retail lending products has a very large and easily pregnable market.

- A large number of private banks coming into the market in the recent time. In this competitive environment UBL must expand its product line to enhance its sustainable competitive advantage. In that product line, they can introduce credit card and debit card system for their potential customer.

- As its branches are situated all over the country, it is a comparative advantage to bring all the branches under computer network.

- Now inflow of foreign remittance is increasing so it will very favorable for Uttara Bank Ltd.

- Uttara Bank Ltd. has comparatively low cost fund then new bank that can be very helpful for the customers.

- Uttara Bank Ltd. taking advantage of emerging new technologies in Banking, especially online Banking, ATM etc. it will be a successive method to get fame.

Threats;

- All Sustaining multinational banks and upcoming foreign and private banks pose significant threats to UBL. If that happens the intensity of competition will rise further and bank will have to develop strategies to compete against these local and foreign banks.

- Other commercial banks are offering higher salary that may create problem for UBL to retain their experienced managers and executives.

- Others are coming with hi-tech technology is the great problem for Uttara Bank Ltd.

- Public expectation from bank changing and bargaining power of customer is increasing.

Conclusion:

Banks and other financial institutions have been playing key role in boosting economic activities in the Bangladesh economy. In Bangladesh, at present there are 50 banks of which there are 30 private commercial banks, 10 foreign commercial banks and 9 nationalized commercial and specialized banks. Since 2000, banking has made revolutionary change in the financial sector of Bangladesh. According to banking Company Act 1991, many policies have been adopted to regulate and monitor the banking sector of Bangladesh. Bangladesh Bank is the key institution to adopt policy making in Bangladesh.

Foreign Exchange has always been regarded as an esoteric field of a bank as it involves international trade, multiple currencies, different legal systems and different sovereign countries. It covers a wide range of sections such as remittances, import, exports, accounting standards, exchange controls etc. A bank can earn huge profit from its foreign exchange operations.

Uttara Bank is one of the largest private commercial banks in Bangladesh. It has a strong branch based network in Bangladesh and widespread correspondent relationship in international arena. It has also sound reputation to different international banking sectors for its committed transactions. Its strong earning and profitability reflects its ability to support its present and future operation.

Kalabagan Branch is one of the biggest and oldest branches of Uttara Bank. Its sound management, suitable location, efficient dealings and above all, proper marketing approach made it one of the successful branches of the Bank. Yet, there are ample opportunities for its operational boost up in near future.

Recommendations:

Foreign exchange is a multifarious track of a banks operational activity. Uttara Bank as one of the oldest banks of the country has attained experienced management, skilled human resources, huge customer based, and longer international channel. However, since a large number of private commercial banks came forward to complete the race it is not so easy for a bank to run business smoothly. because every private bank is growing rapidly by dint of strategic management, marketing management, asset liability and risk management. On the other hand, the growth in connection with return on asset, return on equity, networking, human resource development, technological advancement in Uttara Bank is not so significant. As far as possible the bank should take steps to strengthen its position in the competitive banking sector of Bangladesh which may include:

- To offer specialized and quality services to the customers.

- To launch realistic and attractive service products in order to maximization of profit.

- To commence on-line banking as part of sound financial services and transactions.

- Time oriented loan pricing setting interest rate for deposits and service charges.

- Enhance promotional activities to focus its marketing strategy.

- Arrangement of training for potential employees.

To ensure allied services related to foreign exchange operation at every AD branches like buying and selling of cash foreign currency and travelers cheques, opening of student file and opening of Foreign Currency accounts of the eligible people.

Method of internal communication and decision making should be reconstructed in order to protect waste of time, energy and papers.

Pursue a strong and effective recruitment system to ensure expected human resources in the institution.