The main objective of this report is to evaluate Overall Banking System of Mercantile Bank Limited, here main focus on the performance in the area of credit and foreign exchange risk management. Other objectives are to identify the factors influencing risk associated with banking operations and evaluate foreign exchange risk management of Mercantile Bank Limited. Finally suggest some policy measures for the improvement of risk management program of Mercantile Bank Limited.

Objectives of this report

The Principal objective of the study is to evaluate of the risk management practice of Mercantile Bank Limited (MBL). To accomplish this objective following objectives have been cover:

- To highlight the policies and strategies of Mercantile Bank limited for managing risk associated with banking operations.

- To identify the factors influencing risk associated with banking operations.

- To evaluate credit risk management practice of Mercantile bank

- To evaluate foreign exchange risk management of Mercantile Bank Limited.

- To suggest some policy measures for the improvement of risk management program of Mercantile Bank Limited.

Methodology of the Study:

All the information incorporated in this report has been collected both from the primary sources, internal sources and secondary sources.

Primary Source of Data

Collecting data directly from the practical field is called primary source of data. The method that was used to collect the primary data is as follows:

- Discussion with officials of MBL;

- Practical work experience in different desks;

- Information that are collected through questionnaire;

- Face to face conversation with the clients;

Internal Sources of Data

- Circular of Bangladesh Bank that keep as internal record of the branch.

- Circular of Mercantile Bank Limited.

- Internal record of branch.

Secondary Sources of Data

The data which have collected for some other different purpose rather than this and which have passed through the statistical process. The method that was used to collect the primary data is as follows:

- Annual Review of MBL.

- Various publications MBL

- Brochures of different product of MBL

- Various books related with the subject.

Policy Guidelines For Credit Risk Management (Lending) In MBL:

This section details fundamental credit risk management policies that are recommended for adoption by all banks in Bangladesh. The guidelines contained herein outline general principles that are designed to govern the implementation of more detailed lending procedures and risk grading systems within individual banks. MBL is following this guideline in managing credit risk.

Lending Guidelines: –

All banks should have established Credit Policies (“Lending Guidelines”) that clearly outline the senior management’s view of business development priorities and the terms and conditions that should be adhered to in order for loans to be approved. The Lending Guidelines should be updated at least annually to reflect changes in the economic outlook and the evolution of the bank’s loan portfolio, and be distributed to all lending/marketing officers. The Lending Guidelines should be approved by the Managing Director/CEO & Board of Directors of the bank based on the endorsement of the bank’s Head of Credit Risk Management and the Head of Corporate/Commercial Banking.

Any departure or deviation from the Lending Guidelines should be explicitly identified in credit applications and a justification for approval provided. Approval of loans that do not comply with Lending Guidelines should be restricted to the bank’s Head of Credit or Managing Director/CEO & Board of Directors.

The Lending Guidelines should provide the key foundations for account officers/relationship managers (RM) to formulate their recommendations for approval, and should include the following:

- Industry and Business Segment Focus

The Lending Guidelines should clearly identify the business/industry sectors that should constitute the majority of the bank’s loan portfolio. For each sector, a clear indication of the bank’s appetite for growth should be indicated (as an example, Textiles: Grow, Cement: Maintain, Construction: Shrink). This will provide necessary direction to the bank’s marketing staff.

- Types of Loan Facilities

The type of loans that are permitted should be clearly indicated, such as Working Capital, Trade Finance, Term Loan, etc.

- Single Borrower/Group Limits/Syndication

Details of the bank’s Single Borrower/Group limits should be included as per Bangladesh Bank guidelines. Banks may wish to establish more conservative criteria in this regard.

- Lending Caps

Banks should establish a specific industry sector exposure cap to avoid over concentration in any one industry sector.

- Discouraged Business Types

Banks should outline industries or lending activities that are discouraged. As a minimum, the following should be discouraged:

- Military Equipment/Weapons Finance

- Highly Leveraged Transactions

- Finance of Speculative Investments

- Logging, Mineral Extraction/Mining, or other activity that is Ethically or Environmentally Sensitive

- Lending to companies listed on CIB black list or known defaulters

- Counterparties in countries subject to UN sanctions

- Share Lending

- Taking an Equity Stake in Borrowers

- Lending to Holding Companies

- Bridge Loans relying on equity/debt issuance as a source of repayment.

- Loan Facility Parameters

Facility parameters (e.g., maximum size, maximum tenor, and covenant and security requirements) should be clearly stated. As a minimum, the following parameters should be adopted:

- Banks should not grant facilities where the bank’s security position is inferior to that of any other financial institution.

- Assets pledged as security should be properly insured.

- Valuations of property taken as security should be performed prior to loans being granted. A recognized 3rd party professional valuation firm should be appointed to conduct valuations

- Cross Border Risk

Risk associated with cross border lending. Borrowers of a particular country may be unable or unwilling to fulfill principle and/or interest obligations. Distinguished from ordinary credit risk because the difficulty arises from a political event, such as suspension of external payment

- Synonymous with political & sovereign risk

- Third world debt crisis

Policy guidelines for Foreign exchange risk management:

All foreign exchange transactions invariably involve two or more parties and two or more currencies. Commercial banks act as intermediaries for settling payments between parties located in different countries. Commercial bank dealing in foreign exchange has a specialized department know as the Foreign Exchange Department, manned by one or more senior officials who are specialists in this purpose. The function of this department is primarily to convert foreign currency into home currency and vice versa for customers and for other banks with which the bank concerned my enter into deals for certain business purposes.

A transaction involving foreign exchange i.e., conversion or exchange of currencies is known as “Foreign Exchange Transaction”. The policy guidelines that a bank needs to follow in foreign exchange can be given as:

Dealing Limit: –

As a dealer develops his/ her expertise and dealing instincts over time, it is the management’s responsibility to assess his/ her dealing capabilities and based on that a specific dealing limit can be allocated to an individual dealer. In doing this, the management also keeps in mind the dealer’s dealing limit requirement in relation to the market and according to the organization’s own size, need and market risk appetite.

Mandatory Leave: –

The dealing functions are extremely sensitive involving wholesale and large amounts with exposures to adverse market movements. There is also risk of mistakes not being unearthed. As a result, for a particular dealer’s functions to be run by a different dealer, all dealers are required to be away from their desks for a certain period of time at one stretch during a year. During this period, dealers are not expected to be in contact with their colleagues in the treasury area. Typically, this period is defined as a continuous two weeks period.

Position Reconciliation: –

All dealers’ positions must be reconciled with the positions provided by the treasury back-office. This must be done daily prior to commencement of the day’s business. Unreconciled positions may lead to real differences in actual positions exposing the organization to adverse market changes and real losses.

Nostro-Account Reconciliation: –

Banks maintain various nostro accounts in order to conduct operations in different currencies including BDT. The senior operations manager of the organizations set limits for handling nostro account transactions that include time limits for the settlements of transactions over the various nostro accounts and the time and amount limits for items that require immediate investigation after receipt of the account statements.

Overdraft interest for “our accounts” must be calculated for each day the branch is in overdraft in accordance with its records. The operations manager sets the time and amount limits for liquidation of open items or differences found unreconcilable. These items must be investigated as far as is practicable and if they are found unreconcilable, the operations manager may authorize liquidation through appropriate entries as established as per their accounting policies.

However, the items in question must be amply identified and corrective steps taken to prevent recurring differences. At least quarterly, a comprehensive review of all “our accounts” must be made by an officer independent of transaction processing and authorization functions to ensure that each account continues to be operated with a valid business purpose and that reconciliations and other controls continue to be in place and are effective.

After-hours Dealing: –

After-hours dealing is that which initiated when the dealer’s own trading room is closed. For specific business reasons, an organization may decide to allow its treasury to engage in after-hours dealing. In such cases the organization must have properly laid down procedures detailing the extent to which they want to take risk during after-hours and which dealers to have dealing authority and upto what limits they can deal during after hours.

Off-premises Dealing: –

A dealing transaction done by a dealer who is not physically located in the dealing premises (irrespective of the time of day) is an off-premises deal. An off-premises deal needs to be treated separately from a deal done from within the dealing room due to it being done using communication tools that are not as special as those of the dealing room. For example, an off-premises deal done on the phone is generally not recorded and thus there is no record in case of any future dispute. Also, deals done from within the dealing room get recorded immediately updating positions and allowing treasury back-office to take immediate actions (confirmation, settlement etc.), which is not the case for off premises deals.

As such, an organization must have detailed laid down procedures for the off-premises deals describing how these deals would be accounted for with least possible delay. Typically, organizations would designate particular dealer(s) with the authority for off-premises dealings in case they decide to carry out such activity for some specific business reason/ justification.

Stop Loss Limits: –

Based on the comfort on each dealer and/ or the treasury as a whole, the management allocates dealing limits. However, there is always risk of adverse market movements and no organization is in a position to absorb/ accept unlimited losses. This results in organizations putting in place “stop loss limits”. As a result of this and considering the company’s own financial strengths, the management determines loss limits for particular positions and/ or for a portfolio of positions, where the dealer must close the position or the portfolio and book the loss and stop incurring further losses. Stop loss limit can both be dealer specific and specific to the treasury as a whole.

Mark-to-Market: –

This is a process through which the treasury back-office values all outstanding positions at the current market rate to determine the current market value of these. This exercise also provides the profitability of the outstanding contracts. The treasury back office gathers the market rates from an independent source i.e. other than dealers of the same organization which is required to avoid any conflict of interest. Treasury back-office to take immediate actions (confirmation, settlement etc.), which is not the case for off premises deals.

Valuations: –

The process of revaluing all positions at a pre-specified interval is known as valuation. Though this exercise, an organization determines that if they are to liquidate all the positions at a given time, at what profit or loss they would be able to do so. This function is carried out by the treasury back-office by gathering revaluation rates. Ideally, the treasury back-office should gather such rates from sources other than from the dealers of the same organization to avoid any conflict of interest. Dealers’ are required to have their own P&L estimate which must be tallied with the ones provided by the treasury back-office. Any unacceptable difference between these two must be reconciled to an acceptable level.

Model Control Policy:

Any banking organization and particularly the treasuries use models for the following reasons:

- To generate valuations used in the various financial statements

- To produce market risk measurements used by independent risk management to monitor risk exposures

All financial models that are used for updating the organization’s independent risk monitoring, must be validated and per ideally reviewed by qualified personnel independent of the area that creates such models.

Model Validation is the process through which models are independently and comprehensively evaluated by reviewing underlying assumptions, verifying mathematical formulae, testing the models to verify proper implementation and assessing any weaknesses and ensuring appropriate application. The validation process of a model reduces the risk associated with using a model that has flaws in the underlying assumptions, errors in its implementation and/or is used inappropriately.

A model validation process is not applicable to financial models which only performs simple arithmetic operations. These may include, but are not limited to, value-at-close calculations, earnings-at-risk calculations, interest accrual calculations, and aggregation or consolidation of risk exposures to compare against risk limits.

Internal Audit:

Considering the complexities of the foreign exchange business, a process for an internal audit has widely been accepted as a check point to review the adequacy of the key control issues. This function can include checking for adherence to various limits, compliance requirements, statutory management etc. In addition to regular audits at specified intervals, a concurrent audit process can be put in place to ensure the treasury’s functioning in an appropriate manner on a day-to-day basis.

Factors of Risk:

Risk is inherent in all aspects of a commercial operation; however for Banks and financial institutions, credit risk and foreign exchange risk are essential factors that need to be managed. Before minimizing the risk a bank should know what are factors are influencing their risks.

Factors Influencing Credit Risk:

Different factors influencing the credit of a bank like Mercantile Bank can be given as:

- Default nature of borrower: -Risk of credit with the borrower differentiation. Different types of borrower contain different sort of risk. Default nature of the borrower influence the risk in a large extent.

- Industry size and Structure: The key risk factors of the borrower’s industry should be Different industry contain different sort of risk and this factors have to consider before proceeding loan.

- Financial position of the borrower: Financial position of the borrower also affect in the credit risk. If a borrower has enough current and fixed assets to support the loan then it is safe to precede loan to him than who don’t.

- Project of the Loan: – The project for which the loan is taking is also an important factor in credit risk management. Future of the loan settlement depends on the attractiveness of the project success. That is why in determining credit risk project attractiveness must be evaluated.

- Accounts conduct: – For existing borrowers, the historic performance in meeting repayment obligations (trade payments, cheques, interest and principal payments, etc) should be assessed.

- Margin Sustainability or Volatility: – Margin of the project or the existing margin of the business is stable or volatile is also important in determining risk of credit. Obviously bank will not prefer a volatile project for their business.

- High Debt Load: – Amount of debt currently the firm or the borrower has also a considering factor in credit management. If the firm or the person has fewer current assets than the loan amount proceed than it will be a risky decision to precede loan.

- Growth Rate: – acquisition or expansion rate: Growth, acquisition or good expansion rate of the borrower business give a positive signal for the loan settlement.

- Loan Structure: – The amounts and tenors of financing proposed should be justified based on the projected repayment ability and loan purpose. Excessive tenor or amount relative to business needs increases the risk of fund diversion and may adversely impact the borrower’s repayment ability.

- Security: – A current valuation of collateral should be obtained and the quality and priority of security being proposed should be assessed. Loans should not be granted based solely on security. Adequacy and the extent of the insurance coverage should be assessed.

- Guarantors’ strength: – When there are strong guarantors or a strong guarantor then the future of the loan more secure than a loan with weak guarantors or guarantors. Thus guarantors’ strength is also influencing factor in determining risk of credit.

Factors Influencing Foreign Exchange Risk:

Major factors that influence the foreign exchange risk are: –

Exchange rate risk Political risk and Country risk

Exchange rate risk refers the chance fluctuating the exchange rate of foreign currency more frequently. Political risk arises from political unrest in national and international territory. For politically unstable situation foreign direct investment reduce, export reduces and country depend more on import. On the other hand country risk is the risk that arises from doing business in a particular country. It affects most in MNC.

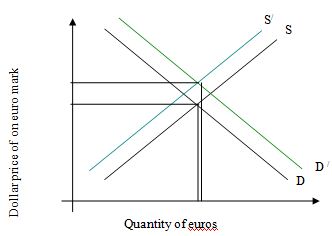

The risk of foreign exchange incur form the change of the equilibrium exchange rate and the factors that affect the foreign exchange rate can be given as:-

a. Relative inflation rate: – Suppose that the supply of dollars increases relative to its demand. This excess growth in the money supply will cause inflation in the United States, which means that U.S price will begin to rise relative price of German goods and services. German consumers are likely to buy fewer S. products and begin switching to German substitutes, leading to a decrease shift in the euro supply curve to S/ as shown in the following curve.

Similarly, higher price in the United States will lead American consumers to substitute German imports for US products, resulting in an increase in the demand for euros as depicted by D / . In effects, both Germans and Americans are searching for the best deals worldwide and will switch their purchases accordingly. Hence, a higher rate of inflation in the United States then in Germany will simultaneously increase German exports to the United States an d reduce U.S exports to the Germany.

Relative Interest Rates: -Interest rate differentials will also affect the equilibrium exchange rate. A rise in U.S interest rate relative to German rates, all else being equal, will cause investors in both nations to switch form euro to dollar-denominated securities to take advantage of the higher dollar rates. The net result will be depreciation of the euro in the absence of government intervention.

Relative Economic Growth Rates: – Similarly, a nation with strong economic growth will attract investment capital seeking to acquire domestic assets, in turn, results in an increased demand. For the domestic currency and a stronger currency, other things being equal. Empirical evidence supports the hypothesis that economic growth should lead to a stronger currency. Conversely, nations with poor growth prospects will see an exodus of capital and weaker currencies.

Political and Economic Risk: – Other factors that can influence exchange rates include political and economic risks. Investors prefer to hold lesser amounts of riskier assets; thus, low risk currencies- those associated with more politically and economically stable nations- are more highly valued than high currencies.

These are factors that affect equilibrium as well as foreign exchange risk. On the basis of these factors we studied the opinion of five officials of the Mercantile Bank Limited, Khatungonj Branch. Their responses about these factors can be summarizing as:

| Factors | No. of respondents | Percentage of respondents Believe that factor influence risk |

| Exchange rate risk | 5 | 100 % |

| Industry size and Structure | 5 | 80 % |

| Financial position of the borrower | 5 | 20 % |

Thus we can say that 100% respondent believe that Exchange rate risk influence foreign exchange risk where 80 % and 20 % respondents believe that industry size and structure, financial position of the borrower respectively affect the foreign exchange risk.

Process of Managing Credit Risk:

Process of managing credit risk means how the risk of credit is managed. Likewise other bank MBL also follows the rules and regulation that are prescribed by Bangladesh Bank in managing risk. Different process of risk management of credit can be given as:

Credit Assessment & Risk Grading

(a) Credit Assessment

A thorough credit and risk assessment should be conducted prior to the granting of loans, and at least annually thereafter for all facilities. The results of this assessment should be presented in a Credit Application that originates from the relationship manager/account officer (“RM”), and is approved by Credit Risk Management (CRM). The RM should be the owner of the customer relationship, and must be held responsible to ensure the accuracy of the entire credit application submitted for approval. RMs must be familiar with the bank’s Lending Guidelines and should conduct due diligence on new borrowers, principals, and guarantors.

All banks should have established Know Your Customer (KYC) and Money Laundering guidelines which should be adhered to at all times.

Credit Applications should summaries the results of the RMs risk assessment and include, as a minimum, the following details:

- Amount and type of loan(s) proposed.

- Purpose of loans.

- Loan Structure (Tenor, Covenants, Repayment Schedule, Interest)

- Security Arrangements

In addition, the following risk areas should be addressed:

- Borrower Analysis.

- Industry Analysis.

- Supplier/Buyer Analysis.

- Projected Financial Performance.

- Account Conduct

- Adherence to Lending Guidelines

- Mitigating Factors. .

- Loan Structure.

- Name Lending.

(b) Risk Grading

All Banks should adopt a credit risk grading system. The system should define the risk profile of borrower’s to ensure that account management, structure and pricing are commensurate with the risk involved. Risk grading is a key measurement of a Bank’s asset quality, and as such, it is essential that grading is a robust process. All facilities should be assigned a risk grade. Where deterioration in risk is noted, the Risk Grade assigned to a borrower and its facilities should be immediately changed. Borrower Risk Grades should be clearly stated on Credit Applications.

The following Risk Grade Matrix is provided as an example. The more conservative risk grade (higher) should be applied if there is a difference between the personal judgment and the Risk Grade Scorecard results. It is recognized that the banks may have more or less Risk Grades; however, monitoring standards and account management must be appropriate given the assigned Risk Grade:

| Risk Rating | Grade |

| Superior – Low Risk | 1 |

| Good – Satisfactory Risk | 2 |

| Acceptable – Fair Risk | 3 |

| Marginal – Watch list | 4 |

| Special Mention | 5 |

| Substandard | 6 |

| Doubtful and Bad (non-performing) | 7 |

| Loss (non-performing) | 8 |

At least top twenty five clients/obligors of the Bank may preferably be rated by an outside credit rating agency.

After approval, the report should be forwarded to Credit Administration, who is responsible to ensure the correct facility/borrower Risk Grades are updated on the system. The downgrading of an account should be done immediately when adverse information is noted, and should not be postponed until the annual review process

Approval Authority:

The authority to sanction/approve loans must be clearly delegated to senior credit executives by the Managing Director/CEO & Board based on the executive’s knowledge and experience. Approval authority should be delegated to individual executives and not to committees to ensure accountability in the approval process. The following guidelines should apply in the approval/sanctioning of loans:

- Credit approval authority must be delegated in writing from the MD/CEO & Board (as appropriate), acknowledged by recipients, and records of all delegation retained in CRM.

- Delegated approval authorities must be reviewed annually by MD/CEO/Board.

- The credit approval function should be separate from the marketing/relationship management (RM) function.

- The role of Credit Committee may be restricted to only review of proposals i.e. recommendations or review of bank’s loan portfolios.

- Approvals must be evidenced in writing, or by electronic signature. Approval records must be kept on file with the Credit Applications.

- All credit risks must be authorized by executives within the authority limit delegated to them by the MD/CEO. The “pooling” or combining of authority limits should not be permitted.

- Credit approval should be centralised within the CRM function. Regional credit centres may be established, however, all large loans must be approved by the Head of Credit and Risk Management or Managing Director/CEO/Board or delegated Head Office credit executive.

- The aggregate exposure to any borrower or borrowing group must be used to determine the approval authority required.

- Any credit proposal that does not comply with Lending Guidelines, regardless of amount, should be referred to Head Office for Approval

- MD/Head of Credit Risk Management must approve and monitor any cross-border exposure risk.

- Any breaches of lending authority should be reported to MD/CEO, Head of Internal Control, and Head of CRM.

- It is essential that executives charged with approving loans have relevant training and experience to carry out their responsibilities effectively. As a

- A monthly summary of all new facilities approved, renewed, enhanced, and a list of proposals declined stating reasons thereof should be reported by CRM to the CEO/MD.

Segregation of Duties

Banks should aim to segregate the following lending functions:

- Credit Approval/Risk Management

- Relationship Management/Marketing

- Credit Administration

The purpose of the segregation is to improve the knowledge levels and expertise in each department, to impose controls over the disbursement of authorized loan facilities and obtain an objective and independent judgment of credit proposals.

Internal Audit

Banks should have a segregated internal audit/control department charged with conducting audits of all departments. Audits should be carried out annually, and should ensure compliance with regulatory guidelines, internal procedures, and Lending Guidelines and Bangladesh Bank requirements.

Methods Of Risk Assessment:

Now a day’s different modern method of risk assessment is used in different financial institution. Some modern concepts of credit risk analysis are:

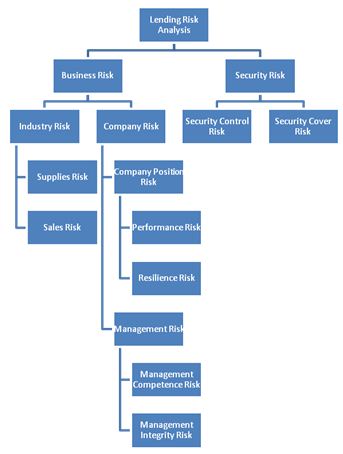

- Lending Risk Analysis

- Financial Statement, Spread Sheet & Credit Scoring System

- Fund Flow and Cash Flow Statement.

- Ratio Analysis.

- Credit Risk Grading (CRG)

Now the short description of the above concepts can be given as:

Lending Risk Analysis (LRA)

LRA is a management and operational tool for improving operational and judgment efficiency of bank. Since lending involves risks, the primary concern of branch manager/sanctioning authority has to assess the relative risks of credit as to minimize possibility of loan losses by identifying the weak/risky areas of a proposal and side by side will also point out the areas of strength and profitability. Thus this exercise not only support approval/rejection of a proposal but also helps determining lending rate and price based on risk rating. Board of divisions of LRA is shown below:

Financial Spread Sheet (FSS)

Financial Statement Sheet is a process that provides quick methods of assessing business trends and efficiency of an organization. It helps to assess borrowers’ ability to repay. Realistically shows business trends and allow comparisons to be made within industry. It is an important tool in a disciplines organized approach to credit analysis. The historic financial company are primary indicator of its financial position. Spread Sheet allows proper analysis of financial statement. It is a means of presenting the main between similar figures on different dates. It also includes cash flow statement and ratio analysis.

Credit Score System:

There are two types of credit score system

- Z-Score.

- Y-Score.

Z-Score: – It is used for those companies who are the listed company of Stock Exchange and whose capital is more that 500 millions. The formula to calculate the Z-Score is as follows:

Z = .012 X1+.014X2+.033X3+.006X4+.99X5

Where,

X1 = Working Capital / Total Assets.

X2 = Retained Earnings/ Total Assets.

X3 = Earnings before interest & taxes/ Total Assets.

X4 = Equity/ Total Liabilities

X5 = Sales/ Total Assets.

Y-Score: – It is used for all trading companies who are not belongs the above category. The formula calculates 5 ratios. These are:

Current Ratio (CR) = Current Assets/ Current Liabilities.

Quick Ratio (QR) = [(Cash + Equivalents +Accounts Receivable)/ Current Liabilities]

Asset Ratio (AR) = Total Asset / Total Liabilities.

Return on Equity (REO) = Net Profit for the year / Ending Net Worth.

Fund Flow & Cash Flow Statement:

Funds from operation indicate the extent to which an enterprise generates funds or uses funds in its operation whereas cash from operation is the cash generation solely from the operating activities of the company. Balance sheet tells us the position of the company at a point in time. Fund flow statement describes the changes that have taken place between the current balance sheet and the previous one. It has two parts:

The statement of cash flows reports inflows and outflows of cash during the accounting period in the categories of operating, investing and financial activities are discussed below;

Operating Activities:

Starts with net profit after tax of current year. Here all current assets and liabilities are covered to calculate the net result. Rules for date entry are:

- Increase in current asset assets will decrease the cash and decrease in CA will increase the cash.

- Increase in CL will increase in cash and decrease in CL will decrease in cash.

Investing Activities:

All information related sales out or procurement of non-current assets are covered here. The rules are:

- Increase in non-current assets will decrease in cash and decrease in non-current assets will increase in cash.

- Financial Activities:

All information related to non-current liabilities and short term financing and equity are covered here the rules are:

- Increase in non-current liabilities and items related to short term financing and owners’ equity will lead to increase in cash.

Ratio Analysis: –

Ratio analysis is a tool used to measure and evaluate the financial condition and operating effectiveness of business enterprise. Absolute figures do not serve the purpose as these are not fit for comparison.

Bank analyzes the financial statement of the borrowers so that it can minimize the risk and evaluate the financial condition of the borrowers. Bank analyzes the liquidity, profitability, assets utilization and debt utilization ratio. These ratios are as follows: –

Liquidity Ratio: – Liquidity refers to the ability to meet a firm’s short term ability when an as they fall due. The liquidity ratio is to measure the position of a firm’s liquidity or short term solvency.

Profitability Ratio: – This ratio is measure the ability of firm to generate revenue in excess of expenses.

Assets Utilization Ratio: This ratio is also known as turn over ratio. This ratio indicates the efficiency in utilization assets such as CA, FA and TA.

Debt Utilization Ratio: This ratio is also known as leverage ratio or capital structure ratio which measure the financial leverage or the extent to which non- equity capital us used to finance the assets of the firm.

Debt Service Coverage Ratio: Ratio to measure the ability of an entity to service interest payment from its operations that are due to non equity suppliers of fund.

Credit Risk grading (CRG):

Definition Of Credit Risk Grading (CRG)

The Credit Risk Grading (CRG) is a collective definition based on the pre specified scale and reflects the underlying credit-risk for a given exposure. A Credit Risk Grading deploys a number/ alphabet/ symbol as a primary summary indicator of risks associated with a credit exposure. Credit Risk Grading is the basic module for developing a Credit Risk Management System.

Functions Of Credit Risk Grading

Well-managed credit risk grading systems promote bank safety and soundness by facilitating informed decision-making. Grading systems measure credit risk and differentiate individual credits and groups of credits by the risk they pose. This allows bank management and examiners to monitor changes and trends in risk levels. The process also allows bank management to manage risk to optimize returns.

Use Of Credit Risk Grading

- The Credit Risk Grading matrix allows application of uniform standards to credits to ensure a common standardized approach to assess the quality of individual obligor, credit portfolio of a unit, line of business, the branch or the Bank as a whole.

- As evident, the CRG outputs would be relevant for individual credit selection, wherein either a borrower or a particular exposure/facility is rated. The other decisions would be related to pricing (credit-spread) and specific features of the credit facility. These would largely constitute obligor level analysis.

- Risk grading would also be relevant for surveillance and monitoring, internal MIS and assessing the aggregate risk profile of a Bank. It is also relevant for portfolio level analysis.

Credit Risk Grading Definitions

A clear definition of the different categories of Credit Risk Grading is given as follows:

Superior – (SUP) – 1

- Credit facilities, which are fully secured i.e. fully cash covered.

- Credit facilities fully covered by government guarantee.

- Credit facilities fully covered by the guarantee of a top tier international Bank.

Good – (GD) – 2

- Strong repayment capacity of the borrower

- The borrower has excellent liquidity and low leverage.

- The Company demonstrates consistently strong earnings and cash flow.

- Borrower has well established, strong market share.

- Very good management skill & expertise.

- All security documentation should be in place.

- Credit facilities fully covered by the guarantee of a top tier local Bank.

- Aggregate Score of 85 or greater based on the Risk Grade Score Sheet

Acceptable – (ACCPT) – 3

- These borrowers are not as strong as GOOD Grade borrowers, but still demonstrate consistent earnings, cash flow and have a good track record.

- Borrowers have adequate liquidity, cash flow and earnings.

- Credit in this grade would normally be secured by acceptable collateral

(1st charge over inventory / receivables / equipment / property).

- Acceptable management

- Acceptable parent/sister company guarantee

- Aggregate Score of 75-84 based on the Risk Grade Score Sheet

Marginal/Watch list – (MG/WL) – 4

- This grade warrants greater attention due to conditions affecting the borrower, the industry or the economic environment.

- These borrowers have an above average risk due to strained liquidity, higher than normal leverage, thin cash flow and/or inconsistent earnings.

- Weaker business credit & early warning signals of emerging business credit detected.

- The borrower incurs a loss

- Loan repayments routinely fall past due

- Account conduct is poor, or other untoward factors are present.

- Credit requires attention

- Aggregate Score of 65-74 based on the Risk Grade Score Sheet

Special Mention – (SM) – 5

- This grade has potential weaknesses that deserve management’s close attention. If left uncorrected, these weaknesses may result in a deterioration of the repayment prospects of the borrower.

- Severe management problems exist.

- Facilities should be downgraded to this grade if sustained deterioration in financial condition is noted (consecutive losses, negative net worth, excessive leverage),

- An Aggregate Score of 55-64 based on the Risk Grade Score Sheet.

Substandard – (SS) – 6

- Financial condition is weak and capacity or inclination to repay is in doubt.

- These weaknesses jeopardize the full settlement of loans.

- Bangladesh Bank criteria for sub-standard credit shall apply..

Doubtful – (DF) – 7

- Full repayment of principal and interest is unlikely and the possibility of loss is extremely high.

- However, due to specifically identifiable pending factors, such as litigation, liquidation procedures or capital injection, the asset is not yet classified as Bad & Loss.

- Bangladesh Bank criteria for doubtful credit shall apply.

- An Aggregate Score of 35-44 based on the Risk Grade Score Sheet.

Bad & Loss – (BL) – 8

- Credit of this grade has long outstanding with no progress in obtaining repayment or on the verge of wind up/liquidation.

- Prospect of recovery is poor and legal options have been pursued.

- Proceeds expected from the liquidation or realization of security may be awaited. The continuance of the loan as a bankable asset is not warranted, and the anticipated loss should have been provided for.

- This classification reflects that it is not practical or desirable to defer writing off this basically valueless asset even though partial recovery may be affected in the future. Bangladesh Bank guidelines for timely write off of bad loans must be adhered to. Legal procedures/suit initiated.

- Bangladesh Bank criteria for bad & loss credit shall apply.

- An Aggregate Score of less than 35 based on the Risk Grade Score Sheet.

Procedural Guidelines:

This section outlines of the main procedures that are needed to ensure compliance with the policies contained in Section 1.0 of these guidelines.

- Approval Process

The approval process must reinforce the segregation of Relationship Management/Marketing from the approving authority. The responsibility for preparing the Credit Application should rest with the RM within the corporate/commercial banking department. Credit Applications should be recommended for approval by the RM team and forwarded to the approval team within CRM and approved by individual executives. Banks may wish to establish various thresholds, above which, the recommendation of the Head of Corporate/Commercial Banking is required prior to onward recommendation to CRM for approval. In addition, banks may wish to establish regional credit centres within the approval team to handle routine approvals. Executives in head office CRM should approve all large loans.

The recommending or approving executives should take responsibility for and be held accountable for their recommendations or approval. Delegation of approval limits should be such that all proposals where the facilities are up to 15% of the bank’s capital should be approved at the CRM level, facilities up to 25% of capital should be approved by CEO/MD, with proposals in excess of 25% of capital to be approved by the EC/Board only after recommendation of CRM, Corporate Banking and MD/CEO.

Credit Administration

The Credit Administration function is critical in ensuring that proper documentation and approvals are in place prior to the disbursement of loan facilities. For this reason, it is essential that the functions of Credit Administration be strictly segregated from Relationship Management/Marketing in order to avoid the possibility of controls being compromised or issues not being highlighted at the appropriate level.

Credit Monitoring

To minimize credit losses, monitoring procedures and systems should be in place that provides an early indication of the deteriorating financial health of a borrower. At a minimum, systems should be in place to report the following exceptions to relevant executives in CRM and RM team:

- Past due principal or interest payments, past due trade bills, account excesses, and breach of loan covenants;

- Loan terms and conditions are monitored, financial statements are received on a regular basis, and any covenant breaches or exceptions are referred to CRM and the RM team for timely follow-up.

- Timely corrective action is taken to address findings of any internal, external or regulator inspection/audit.

- All borrower relationships/loan facilities are reviewed and approved through the submission of a Credit Application at least annually

Computer systems must be able to produce the above information for central/head office as well as local review. Where automated systems are not available, a manual process should have the capability to produce accurate exception reports. Exceptions should be followed up on and corrective action taken in a timely manner before the account deteriorates further.

Credit Recovery

The Recovery Unit (RU) of CRM should directly manage accounts with sustained deterioration (a Risk Rating of Sub Standard (6) or worse). Banks may wish to transfer EXIT accounts graded 4-5 to the RU for efficient exit based on recommendation of CRM and Corporate Banking. Whenever an account is handed over from Relationship.Management to RU, a Handover/Downgrade Checklist should be completed.

The RU’s primary functions are:

- Determine Account Action Plan/Recovery Strategy

- Pursue all options to maximize recovery, including placing customers into receivership or liquidation as appropriate.

- Ensure adequate and timely loan loss provisions are made based on actual and expected losses.

- Regular review of grade 6 or worse accounts.

The management of problem loans (NPLs) must be a dynamic process, and the associated strategy together with the adequacy of provisions must be regularly reviewed. A process should be established to share the lessons learned from the experience of credit losses in order to update the lending guidelines.

NPL Account Management

All NPLs should be assigned to an Account Manager within the RU, who is responsible for coordinating and administering the action plan/recovery of the account, and should serve as the primary customer contact after the account is downgraded to substandard. Whilst some assistance from Corporate Banking/Relationship Management may be sought, it is essential that the autonomy of the RU be maintained to ensure appropriate recovery strategies are implemented.

Account Transfer Procedures

Within 7 days of an account being downgraded to substandard (grade 6), a Request for Action) and a handover/downgrade checklist (should be completed by the RM and forwarded to RU for acknowledgment. The account should be assigned to an account manager within the RU, who should review all documentation, meet the customer, and prepare a Classified Loan Review Report within 15 days of the transfer. The CLR should be approved by the Head of Credit, and copied to the Head of Corporate Banking and to the Branch/office where the loan was originally sanctioned. This initial CLR should highlight any documentation issues, loan structuring weaknesses, proposed workout strategy, and should seek approval for any loan loss provisions that are necessary.

Recovery Units should ensure that the following is carried out when an account is classified as Sub Standard or worse:

- Facilities are withdrawn or repayment is demanded as appropriate. Any drawings or advances should be restricted, and only approved after careful scrutiny and approval from appropriate executives within CRM.

- CIB reporting is updated according to Bangladesh Bank guidelines and the borrower’s Risk Grade is changed as appropriate.

- Loan loss provisions are taken based on Force Sale Value (FSV).

- Loans are only rescheduled in conjunction with the Large Loan Rescheduling guidelines of Bangladesh Bank. Any rescheduling should be based on projected future cash flows, and should be strictly monitored.

- Prompt legal action is taken if the borrower is uncooperative.

Non Performing Loan (NPL) Monitoring

On a quarterly basis, a Classified Loan Review (CLR) should be prepared by the RU Account Manager to update the status of the action/recovery plan, review and assess the adequacy of provisions, and modify the bank’s strategy as appropriate. The Head of Credit should approve the CLR for NPLs up to 15% of the banks capital, with MD/CEO approval needed for NPLs in excess of 15%. The CLR’s for NPLs above 25% of capital should be approved by the MD/CEO, with a copy received by the Board.

NPL Provisioning and Write Off

The guidelines established by Bangladesh Bank for CIB reporting, provisioning and write off of bad and doubtful debts, and suspension of interest should be followed in all cases. These requirements are the minimum, and Banks are encouraged to adopt more stringent provisioning/write off policies. Regardless of the length of time a loan is past due, provisions should be raised against the actual and expected losses at the time they are estimated. The approval to take provisions, write offs, or release of provisions/upgrade of an account should be restricted to the Head of Credit or MD/CEO based on recommendation from the Recovery Unit. The Request for Action (RFA) or CLR reporting format should be used to recommend provisions, write-offs or release/upgrades.

The RU Account Manager should determine the Force Sale Value (FSV) for accounts grade 6 or worse. Force Sale Value is generally the amount that is expected to be realized through the liquidation of collateral held as security or through the available operating cash flows of the business, net of any realization costs. Any shortfall of the Force Sale Value compared to total loan outstanding should be fully provided for once an account is downgraded to grade 7. Where the customer in not cooperative, no value should be assigned to the operating cash flow in determining Force Sale Value.

Different Types of Foreign Exchange Risk:

Foreign Exchange risks are mainly three types:

- Exchange rate risk.

- Political risk

- Country risk

Exchange rate risk refers the chance fluctuating the exchange rate of foreign currency more frequently.

Political risk arises from political unrest in national and international territory. For politically unstable situation foreign direct investment reduce, export reduces and country depend more on import.

Country risk is the risk that arises from doing business in a particular country. This risk is a vital factor for Multination Corporation.

Though political and country risk influence in a large extent but Exchange rate risk is the main type of foreign exchange risk upon which firms profit or loss depends. Again foreign exchange risk influenced by: –

- Relative inflation rate

- Relative economic growth rate

- Relative interest rate

Theories of Exchange Rate Determination:

Different theories are developed for determining foreign exchange rate determination that are: Arbitrage and the Law of One Price, Purchasing Power Parity, The Fisher Effect, The International Fisher Effect, Interest Rate Parity Theory, Forward Rates As Unbiased Predictors of Future Spot rate.

Purchasing Power Parity (PPP): – This theory states that spot exchange rate between currencies will change to the differential in inflation rates between countries. There are two popular form of PPP theory a) Absolute Form of PPP. b) Relative form of PPP.

Absolute Purchasing Parity refers that price levels adjusted for exchange rates should be equal between countries. One unit of currency has same purchasing power globally.

Relative Purchasing Power Parity states that the exchange rate of one currency against another will adjust to reflect change in the price levels of the two countries.

The Fisher Effect: – Fisher Effect states that the nominal interest differential between two countries should equal the inflation differential of those countries. Virtually all financial contracts are stated in nominal terms, the real interest rate must be adjusted to reflect expected inflation. Where real rate of interest is the net increase in wealth that people expect to achieve when they save and invest their current income.

The Fisher Effect states that the nominal interest rate r is made up of two components a real require rate of return and a premium for inflation expectation.

r = a + I

Where, a = real require rate of return.

I = premium for inflation expectation.

International Fisher Effect: – International Fisher Effect states that inter differential between two countries should be an unbiased predictor of the future change in the spot rate.

The spot rate adjusts to the interest rate differential between two countries. International Fisher Effect combines purchasing power of money and fisher effect.

IFE = PPM + FE

where, IFE = International Fisher Effect

PPM = Purchasing Power of Money.

Interest Rate Parity (IRP): – IRP a condition where by the interest differential between two currencies is equal to the forward and spot rate differential between two countries. It states that the forward rate differ from the spot rate at equilibrium by an amount equal to the interest rate differential between two countries. According to this theory, the currency of the country with a lower interest rate should be at a forward premium in terms of currency of the country with the higher rate. According to this theory Forward premium or discount equals to the interest rate differentials.

Forward Rate – Spot Rate

Spot Rate = Home Rate – Foreign Rate

Methods Of Measuring Risk:

Measuring foreign exchange risk means the method used to determining the different types of foreign exchange risk.

Proposed method determining foreign exchange risk can be given as: –

For exchange rate risk well known methods are: –

- Volatility and Correlation Calculation.

- Value-At-Risk determination (VAR)

- Market Performance Analysis.

For Country risk measurement available measurements are:

- Expropriation or Nationalization.

- Political Stability Analysis.

- Economic Factor Analysis.

- Subjective Factors Analysis.

- Capital Flight Rate Calculation.

For Political risk analysis the necessary measurements are:

- Number of Strike work in a year.

- Sustainability of the Government.

- Relationship with other country or international relationship etc.

Some developed product for minimizing foreign exchange risk:

Though foreign exchange risk can not be removed completely because the factors that effect the exchange risk in large extent uncontrollable but we can use some derivative products that can minimize this risk. Some such products are:

- Option

- Forwards

- Futures

- Swap

Option: – An option is a contract between two parties a buyer and a seller that gives the buyer the right but not the obligation to purchase or sell something at a later date at a price agreed upon today.

The option buyer pays the seller a sum of money called the price or premium. The option seller stands ready to sell or buy according to the contract terms if and when the buyer so desires. An option to buy something is referred to as a call, and option to sell something is called a put. Options trade in organized markets, much like the stock market that you may already be familiar with contracting with each other may be preferable to a public transaction on the exchange. This type of market called an over the counter market was actually the first type of options market.

Forwards: – A forward contract as it occurs in both forward futures markets always involves a contract initiated at one time; performance in accordance with the terms of the contract occurs at a subsequent time. Further the type of forward contracting to be considered here always involves an initial contracting. Actual payment and delivery of the goods occur latter. So defined, almost all market player of the financial market engaged in some kind of forward contract.

Swap: – Although options, forwards and futures compose the set of basic instruments in derivative markets. There are many more combinations and variations. One of the most popular is called a wasp. A Swap is a contract in which two parties agrees to exchange cash flows. Swap operation is the traditional and most important method for adjusting the fund position without affecting overall currency position. Whenever a bank buys or sells forward, the forward position should be covered at once by a spot operation in the opposite direction. Later, at a convenient moment, the resulting spot forward commitment is offset by a swap operation.

- Methods Followed By MBL in managing Foreign Exchange Risk:

From the study of the related official of the bank, Mercantile Bank is using all the risk measurement that is practiced in out country. But all risk assessment done by Head Office and the measured result and necessary instructions send to all branches and branch do according to the instruction.

From the answer of the respondents of MBL officials they are using following products for minimizing risk: –

| Name | Number of respondents. | Comment of Respondents |

| Forward contract | 5 | 100% says that they using this product. |

| Future contract | 5 | 100% says that they using this product. |

| Swap | 5 | 100% says that they using this product. |

| Options | 5 | 100% says that they using this product. |

Comment: – All the respondents say that they are using the all the derivative products noted above for minimizing foreign exchange risk. But it is notable all the practice limited in Head Office, Branch involvement in decision making of hedging risk is very limited and they are the followers of Head Office instruction.

Separate Trading And Risk Management Units And Its Duties:

MBL also maintain a Separate trading and risk management units. The roles and responsibilities of these two departments in term of controlling and managing risk are:

Traders/ Risk-Taking Units:

- Maintain compliance with the market risk limits policies and remains within their approved independent market risk limit framework at all times.

- Ensure no limit breaches and arrange for pre-approval of any higher limit requirements

- Inform the market risk management unit of any shifts in strategy or product mix that may necessitate a change in the market risk limit framework

- Seek approval from the market risk management unit prior to engaging in trading in any new product

Market Risk Management:

- Review policy at least annually and update as required

- Independently identify all relevant market risk factors for each risk taking unit

- Develop proposals for the independent market risk limits/ triggers, in conjunction with the risk-taking units

- Ensure that limits/ triggers are appropriately established

- Independently monitor compliance with established market risk limits/ triggers

- Ensure ongoing applicability of the market risk limits/ triggers; formally review framework at least annually

- If applicable, review and approve limit frameworks, as well as limit change requirements

- Review and approve any temporary limit requirements

- Recommend corrective actions for any limit excesses

- Maintain documentation of limit breaches, including corrective action and resolution date.

Overall Practice Of Foreign Exchange In MBL:

Organization Chart:

Considering the above and in relation to the local market, an appropriate organization chart has been drawn. The proposed structure has been drawn bearing in mind all possible roles and functions that are currently applicable to our market. In organizations where it does not justify employment of full time employees for each of the functions, a single employee or department can be used for more than one function. The proposed organization Chart has been detailed on annexure I

From the organization structures shown on annexure III, it is evident that the reporting lines for the officers managing the treasury and the treasury back office are different. This is an ideal structure that needs to be in place for control reasons. In our domestic market, organizations according to their existing structure/ policy, would best determine in which of their departments the treasury would report and in which the treasury back office would.

Job Descriptions:

Based on the organizational structure proposed on annexure III, following is an overview of the various jobs depicting the key roles of each of these for an ideal treasury and a treasury back-office:

a – TREASURY:

Head of Treasury:

- Overall responsibility of all treasury activities

- Responsible for the treasury financial plan

- Determine overall treasury business and risk strategy within internal and regulatory limits

- Set individual dealer dealing limits

- Monitor all dealers’ positions and ensure dealers adhere to all internal, regulatory as well as dealer specific limits

- Decide on particular positions during adverse situations

- Continuous development of systems, processes, business strategies etc.

- Member of the ALCO

- Propose overall balance sheet strategy to the ALCO

Cross Currency Dealer:

- Forming Market Views

- Monitoring exchange positions

- Counterparty limits monitoring

- Collating all the cross currency exchange positions

- Remaining within all given internal and regulatory limits

- Remaining within all counterparty limits at all times

- Profitably trading/ squaring the positions

USD/BDT Dealer:

- Trading spot and forward positions arising from import/ export/ remittances etc.

- Collating the whole Bank’s USD/BDT positions

- Remaining within all given internal and regulatory limits

- Remaining within all counterparty limits at all times

- Profitably trading/ squaring the positions

Securities and Statutory Management Dealer:

- Maintenance of CRR and SLR

- Investment in Treasury Bills Portfolio

- Repo activities

- Propose to the ALCO (through the head of treasury) of statutory investments

Lcy & Fcy Money Market Dealer:

- Overnight/ Call money activities

- Term market activities

- Currency swaps

- Fcy placements

- MM pricing of Fcy

- Nostro funding

- Spot any arbitrage opportunities and take advantage

- Remaining within all counterparty limits at all times

- Operating within all given balance sheet gap limits

- Profitably trading/ squaring the positions

Balance Sheet Manager:

- Managing all balance sheet gaps

- Monitoring of market factors

- Interest rate and market forecasts

- Analysis of risk reports for presentation to ALCO

- Daily reports to senior management

b – TREASURY BACK-OFFICE:

Manager – Local Currency Nostro Reconciliation:

- Reconcile all local currency nostro accounts on a day-to-day basis

- Immediately advise money market dealer and balance sheet manager of any discrepancy

- Track for reconcilement of any unmatched item

- Claim or arrange payment of good value date effects for any late settlements

- Send chasers for any unsettled items until it is settled

Manager – Foreign Currency Nostro Reconciliation:

- Reconcile all foreign currency nostro accounts on a day-to-day basis

- Immediately advise USD/BDT or cross currency dealer of any discrepancy

- Track for reconcilement of any unmatched item

- Claim or arrange payment of good value date effects for any late settlements

- Send chasers for any unsettled items until it is settled

Manager – Foreign Currency Position Reconciliation:

- Receive copies of USD/BDT and cross currency dealers position blotters

- Reconcile all foreign currency positions between accounted for records and USD/BDT & cross currency dealers blotters on a day-to-day basis

- Immediately advise USD/BDT or cross currency dealer of any position discrepancy

- Investigate and match unreconciled amounts

- Advise USD/BDT and cross currency dealer of correct currencypositions prior to commencement of day’s dealing activities

Manager – Local Currency Position Reconciliation:

- Receive copies of position blotters from money market dealer

- Reconcile all local currency positions between accounted for records and money market dealers blotters on a day-to-day basis

- Immediately advise money market dealer of any position discrepancy

- Investigate and match unmatched amounts

- Advise money market dealer of correct positions prior to commencement of day’s dealing activities

Manager – Foreign Currency Settlements:

- Settle for all foreign currency deals done by USD/BDT, cross currency and the Fcy money market dealers

- Send and receive confirmations of all deals done by USD/BDT, cross currency and Fcy money market dealers

- Check foreign currency nostro statements for settlements of major items

- Advise dealers of any discrepancy in settlement for the prior dealing day

- All related accounting entries

- Generate various MIS

Manager – Local Currency Settlements:

- Settle for all local currency deals done by Lcy money market dealers

- Send and receive confirmations of all deals done by Lcy money market dealers

- Check local currency nostro statements for settlements of major items

- Advise dealers of any discrepancy in settlement for the prior dealing day

- All related accounting entries

- Generate various MIS

Manager – Regulatory reporting:

- Send all required regulatory reports at required intervals

- Respond to various queries from regulators regarding reports

- Coordinate with other departments in receiving required information for reporting purpose

- Create awareness among various related departments of the importance of effective and accurate reporting

Manager – Risk Reporting:

- Monitor limit utilizations against all internal and regulatory risk limits

- Reporting of limit excesses etc.

- Stop loss/ cumulative loss limits monitoring and reporting

- Monitoring of daily P&L

- Generate various MIS

Process:

In a proper treasury setup, a dealer strikes a deal in the market and maintains his/ her own record for monitoring the exchange position. Within a reasonable time, s/he passes on the detailed information of the deal to the treasury back office. The back office arranges for the deal confirmation with the counterparty, arranges settlement, reconciles exchange positions and advises to treasury and runs the valuation on a periodic basis. A detailed flowchart of this function has been shown on annexure V.

The dealing function requires the dealers to make very quick decisions either for taking advantages of any market movements or for unwinding an unfavorable position. Also, the treasury dealing is a wholesale function that involves large lots. These together make the job of a dealer requiring:

- Proper information sources e.g. Reuters Money 2000, Bloomberg, financial TV channels etc.

- Adequate and dedicated communication tools e.g. Reuters Dealing System, telephone, fax, telex etc.

- Specially designed dealing desks to appropriately accommodate the various information and communication tools

- High level of dealing skills

- Quick decision making authority

- Independent decision making authority

- Specific task allocations

In order to achieve the optimum level of efficiency, returns and most importantly controls, there are certain processes that the organization’s management must put in place. The very basic ones of these that would be related to our market are explained below:

Dealing Room:

Since the dealers have access to global live prices of various products through their various communication tools, their desks are required to be access restricted. As a result, dealers are typically housed inside a covered room known as the “dealing room” where the access is generally restricted only to the dealers and the related personnel.

Taped Conversations:

In many occasions, the dealers conclude deals over the phone. This is particularly applicable where deals are done on the local market where dealers are mostly known to each other and they feel comfortable dealing by talking to other dealers over phone. Such deals over the phone do not have any hard evidence and in a fast dealing environment, there is risk of mistakes (of rates, amounts or value dates etc.) As a result, all telephonic conversations taking place in the dealing room are required to be taped. Taped conversations can assist in resolution of any disputes that may arise.

As such, all telephone lines of the dealing rooms, may it be a direct line or a connection through the PABX, must be taped. This means that dealing over the mobile phones must be restricted. However, if the management feels that there is any specific need for dealing on mobile phone(s), this must be properly documented where specific dealer(s) may be allowed to engage in dealing on mobile phone(s) under specific circumstances.

In some jurisdictions, it is required to advise all dealers (of other organizations) beforehand that their conversation would be taped.

Deal Recording:

The job nature of a dealer is highly demanding and the environment of a dealing room is very active. In such an environment when a dealer continues to deal, his/ her focus remains on the market. As such there is a risk of a dealer completely forgetting about a deal or part of a deal or making mistake in recording that deal.

To eliminate this risk, a dealer must record the deal immediately after it is concluded with the counterparty. The deal recording needs to be done in two ways:

Position Blotter: Immediately after a deal is done, the dealer should record the deal on the position blotter and update his position. It is of utmost importance to a dealer to remain aware of his/ her position at all times. This is required to capture any immediate opportunity or to be in a position to immediately react to any adverse situation.

Deal Slip:

A dealer must, at the earliest possible time, record the details of the deal on a slip or memo which is known as the deal slip or deal ticket. In some organizations, the deal slips are electronic and are through inputs into their automated systems. A typical deal slip would contain details such as, payment instruction, value date, currencies, amounts etc. The deal slip should be passed on to the treasury back-office at the earliest for their further processing of the deal. Ideally, all deal slips should be pre-numbered for control reasons and the treasury back-office must monitor for any breakage in sequence. Where pre-numbered deal slips are in place, any cancelled deal slips must also be forwarded to treasury back-office for appropriate record keeping/ filling.

Deal Delay:

All deals done by dealers are required to be processed by the treasury back-office for which they need to be informed of the details of the deals within a certain time. In this process dealers raise deal tickets that need to be sent across to the treasury back-office within shortest possible time. The timeliness of raising deal slips/ inputting into the automated system as well as passing them on to the back-office is not only sound business practice but also critical for monitoring of credit risk, price risk and regulatory compliance.

Findings:

- For achieving profit target they sanctioned the loan in lack of mortgage. For that reason borrower not willing to pay their loan in due time. They have lack of monitoring to the borrower.

- Inaccurate data of creditors when MBL sanction loan, it require financial statement of borrower but borrowers not prepare their financial statement accurately. Collection and compilation of these data are very labourious. So analysis of performances of risk and borrower are difficult.

- The credit scheme of the MBL is not enough in number to satisfy the demand of consumer. Thats why they can not minimize the cost of financing from head office.

- Most of the employee do not have enough knowledge about the modern product that is used to protect risk on the ground of credit and foreign exchange risk.

- Rate determination is not based on demand and supply of foreign exchange in a large extent. In that case Bank policy is not same with the government policy.

- All shorts of banking activities have not yet been computerised.

Policy Implications of the Bank:

From the study of the management practice of MBL in determining foreign exchange risk, credit risk and risk management there are some problems facing the branch for which following policy implications can be taken for better performance.

- Bank should increase their credit scheme.

- Bank should follow more easy procedure in sanction of loan and advances.

- There is no marketing initiation in the bank. So bank can improve its marketing and promotional activities.

- Bank can offer SME loan in minimum term and condition.

- The procedure of online banking of MBL is much more long. Here they have an opportunity of time managing to develop the system.

- Bank can minimize too much paper formalities. This can be done computerizing the banking activities to a large extent, by which bank will also be able to ensure quality and efficiency.

- Bank can set up more correspondent relationship & Branch network in potential areas.

- Some banks are offering 24 hours banking facility. MBL also can offer it to market.

Conclusion:

From the whole study of the risk management of Mercantile Bank Limited it is clear that risk management is the most sensitive decision of the firm and it should be carefully determined because upon this decision current profits as well as future prospect of the firm depend.

At present Bank are using some but not all risk management tools in determining risk. For more profitability and ensuring safe future growth bank should follow all modern tools for minimizing risk.

It is the senior management’s responsibility to ensure appointment of the appropriate and deserving personnel as treasury and treasury-back office staff. They should also on a continuous basis, identify the dealers training and development requirement and arrange for the same. The management should also put in place an overall trading policy for its treasury defining the scopes, policies, risk-limits as well as their control mechanisms.

The management must appreciate that the nature of a treasury environment is ever changing where new market dynamics, products and as a result, new risks are evolving on a continuous basis. Internal policies and structures must be designed in such a manner that identification of new risk and control areas is possible at the earliest where control mechanisms can be implemented prior to taking up any significant.