Executive Summary

The bank plays an important role in the economy of any country. The banking system of Bangladesh is composed of variety of banks working as nationalized commercial banks, Private Banks, foreign banks, specialized banks & development banks. However there are many private banks in Bangladesh. At present, among other banks Prime Bank Limited plays as a leading bank to provide efficient banking service with a view to accelerating socio-economic development of the country. Day by day, new competitors appear with better ideas & Products as well as service. “Consumer credit scheme” one of the new innovative idea which cater to the credit needs of the low & middle income groups for household durables. In a present time, few banks operate this scheme with short volume. Only Prime Bank Limited & a very few banks operate this scheme in a large volume. To make its position more strong, PBL wants to make this scheme more attractive to the customer. Consumer credit scheme provided by Prime Bank Limited are Car Loan: Car, Jeep, Station Jeep, Pick up Van, Cover Van, Bus, Truck, Ambulance and any other vehicle for own use. Doctors Loan: For the Doctors only. Advance against Salary: Any qualified person Education Loan: For Study purpose only. Travel Loan: For traveling purpose, Wedding loan: For wedding only. CNG Conversion Loan: To convert into CNG Any Purpose Loan: For emergency need Hospitalization Loan: For treatment in hospital. It is provided against personal Guarantee. It requires to a certain percent of equity investment it is to repaid by equal monthly installment.

It is to be repaid within a specific period. Any interested person within the age of 25 to 60 and having a permanent job or the permanent employees of the Govt./Semi-Givt. Autonomous, Private organization can apply for the CCS loan of Prime Bank Ltd. Under CCS program of Prime Bank Limited a borrower can get maximum of taka 40, 00,000 and minimum taka 10,000. The down payment is 10% of the loan for each product. The interest rate is 15% for the all products. And Prime Bank charges 1% service charge and 1% risk fund for all products other than for Car loan, Doctor’s loan, Advance against salary and CNG Conversion loan. Prime Bank Ltd has some problem in CCS those are Sometimes the down payment paid by CCS customers is very high with PBL. Interest rate and payback period are very important criteria for any kind of loan but most of the clients are not satisfied to PBL Consumer Credit interest rate and loan payment period. PBL should include more differentiate product in their CCS, such as – Teacher Loan, Shop Financing Scheme, Personal Loan for Women etc. to gain competitive advantage if they overcome those they became the 1st position in banking sector.

BACKGROUND OF THE STUDY:

The EMBA program requires a student to take 21 courses of 3 credit hours each and a project paper of 3 credit hours. As requirement for the fulfillment of the program I select my own organization, Prime Bank Limited. I have been working as a credit officer in our Motijheel branch so I choose the mentioned topic.

Now a days the retail credit is very much popular and is given more emphasis than corporate credit as well as traditional credit. Moreover the Central Bank has instructed to reduce the lending interest rate and fix up the maximum interest rate @13% recently. Mentionable that the consumer loan/ Retail loan is out of this instruction. So now a day the Retail Credit is the most important topic in Banking Arena.

TOPIC OF THE STUDY:

The topic of the report is –

“Consumer Credit Scheme of Prime Bank Limited: An Analysis”

OBJECTIVE OF THE STYUDY:

Broad objectives:

The Broad objective of the study is to know the overall performance of consumer credit scheme of Prime Bank Limited through different aspects of the banking sector & to evaluate how well bank is doing in its Consumer Credit Scheme.

Specific objectives:

In specific objective I have to prepare a sound report that must be reliable and dependable for the Bank’s officials.

The specific objectives to help in explaining the broad objectives are as follows:

- To trace the origin of the CCS of the PBL.

- To gather comprehensive knowledge on CCS.

- To understand the need & objective of credit Management Specially CCS.

- To acquire in depth knowledge on about PBL credit function

- To identify the competitive position of the Consumer Credit Scheme of Prime Bank Limited

- To identify weakness & Problem in CCS

LIMITATION OF THE REPORT:

There were some problems while I conducting the orientation program. A wholehearted effort was applied to conduct the orientation program and to bring a reliable and fruitful result. In spite of having the wholehearted effort, there exit some limitations, which acted as a barrier to conduct the program. The limitations were —

- One problem is concerned with data collection. PBL starts in 1995. So there are shortages of sufficient data for comparing. Moreover, the bank has supplied me the annual report only for three years.

- Learning all the banking functions about credit within just 45days was really tough.

- Another limitation of this report is Bank’s policy of not disclosing some data and information for obvious reason, which could be very much useful.

INCORPORATION OF THE ORGANIZATION

In the backdrop of economic liberalization and financial sector reforms, a group of highly successful local entrepreneurs conceived an idea of floating a commercial bank with a different outlook. For them it was competence, excellence and consistent delivery of reliable service with superior value products. Accordingly, Prime Bank Limited was created and commencement of business started on 17th April 1995.

Prime Bank Ltd. is operating as a scheduled bank under the banking license issued by Bangladesh Bank, the Central Bank of the country on April 17, 1995 through the opening of its Motijheel Branch at AdamjeeCourtAnnexBuilding, Motijheel commercial area, Dhaka-1000. PBL was actually registered under the Companies Act of 1913 with its registered office at 5, Rajuk Avenue, Motijheel commercial area, Dhaka-1000 which was later shifted to AdamjeeCourtAnnexBuilding, 119-120, Motijheel commercial area, Dhaka-1000.

As a fully licensed commercial bank, Prime Bank Limited has being managed by highly professional and dedicated team with long experience in banking. They constantly focus on understanding and anticipating customer needs. As the banking scenario undergoes changes so does the bank and it adjusts and repositions itself to the changed conditions.

In its 15th year of operation in 2010, Prime Bank has made substantial headway in terms of business growth, profitability and establishing its image as one of the leading private commercial banks. Its march towards reaching greater heights in operation continues with full vigor and enthusiasm. Prime Bank has made significant progress within a very short period of its existence. The bank has been graded as a top class bank in the country through internationally accepted CAMEL Rating. The bank has already occupied an enviable position among its competitors after achieving success in all areas of business operations.

Prime Bank Limited offers all kinds of commercial, corporate and personal banking services covering all segments of society within the framework of banking rules and regulations laid down by the Central Bank. Diversification of products and services include corporate banking, retail banking and consumer banking right from industry to agriculture, real state, software and other sectors. Prime Bank Limited is a fast growing private bank and it is already at the top slot in terms of quality service to the customers and value addition for the shareholder

NETWORKS:

Prime Bank has a large and well distributed network of branches in Bangladesh. It has 94 branches and 14 SME branches covering strategic financial centers. It has 3 Off-shore banking units at different EPZs in Bangladesh. It has fully owned exchange houses at Singapore and UK facilitating inward remittance to Bangladesh. It has active presence in Capitakl Market through Prime Bank Investment Limited.

COMMENCEMENT OF OPERATION:

Prime Bank Ltd. started its operation on 17th April 1995 with an authorized capital of Tk. 1000 million and paid up capital of Tk. 100 million by a group of highly successful entrepreneurs who are established in various fields of economic and business activities. PBL is a fully licensed scheduled commercial bank set up in private sector in pursuance of the Government of Bangladesh to liberalize banking and financial services

Currently, there are some proposed branches. The commercial and investment services of PBL range from small enterprises to big business loans to all type of customers. Besides this, the bank actively participates in socio-economic development of priority sectors like agriculture, industry, housing, self-employment, etc. PBL is also a pioneer in providing consumer loans as well as financing the industries and transport sector through attractive leasing and higher purchase scheme.

VISION OF PRIME BANK LTD.:

To be the best Private Commercial Bank in Bangladesh in terms of efficiency, capital adequacy, asset quality, sound management, and profitability having strong liquidity.

MISSION OF PRIME BANK LTD.:

To build Prime Bank Limited into an efficient. Market driven, customer focused institution with good corporate governance structure. Continuous improvement in Bank’s business policies, procedures and through integration of technology at all levels..

Slogan of PRIME BANK LTD.:

To keep continue the growth with reputation and social responsibility, it has it’s own slogan is, “a bank with a difference”

OBJECTIVE OF PRIME BANK LIMITED

Prime Bank aims to continuously update and develop its product line and range of services to cater to the needs of retail and corporate customers. To achieve this goal, efforts have been directed in three main areas:

Design and introduction of new products and services

Shaping and developing the system to face new challenges and emerging need of the market

Full implementation and utilization of the Bank’s excellence program which aims to provide service to customers.

While strengthening risk management and improving asset quality is the main focus of the bank, it is also aware of its responsibility to the society. With this noble intention, Prime Bank Foundation was established in 2001, which took part in diverse charitable and voluntary programs to alleviate poverty and community welfare.

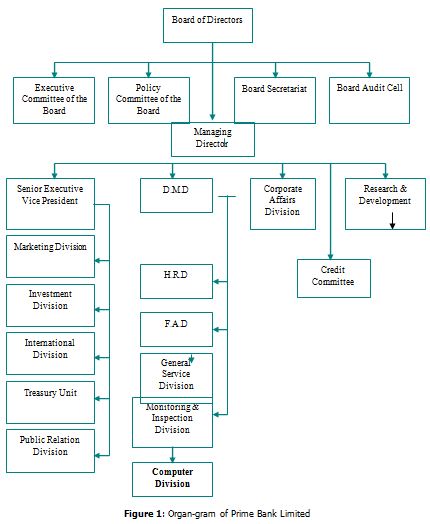

PRIME BANK’S ORGANIZATIONAL STRUCTURE:

Prime Bank had a rather large board (20 members in all) with representatives from all the major shareholders. Previously central bank norms prevented any one shareholder individually holding an equity stake of greater than 5% in the bank; this was the reason for the 20 directors sitting in the board. The central bank rules in this regard have undergone a slight change. Now the rules are that the individual holding has been enhanced to 10% and the size of the Board will now be restricted to 13 members, which should include at least two independent directors.

The bank’s board has a policy of rotating the Chairman’s position amongst various members; consequently the bank has a new Chairman every year. The executive management also appears a bit top-heavy (relative to the size of the bank) with one additional managing director besides the managing director, a Senior Executive Vice President, four Executive Vice Presidents and many Senior Vice Presidents. Prima-facie the rotating Chairman and the presence of effectively two managing directors may lead to some overlapping responsibilities and possible conflict; however this does not seem to have happened so far in the bank’s history and the bank continues to perform satisfactorily.

Organ-gram of Prime Bank Limited:

LOANS AND ADVANCES AND ITS GROWTH IN PRIME BANK LTD.:

Loans and advances/Investments of the Bank grew strongly. The Bank offered various types of Loan and Advances considering the need and wands of different category of customers of the diverse segment of people.

| Different types of Loans and Advances: |

|

Table 2: Loans and Advance Scenario of PBL

| Year | 2006 | 2007 | 2008 | 2009 | 2010 |

| Taka in Million | 45010 | 57683 | 75156 | 89252 | 11167 |

Source: Annual Report-2010

PERFORMANCE OF PRIME BANK LTD.:

a. Operating profit:

Wealth maximization is the main concern for every organization. The symbol for wealth maximization is the operating profit. As high the operating profit is good the organization is. So as to the operating profit concern Prime Bank is doing better and better day by day.

Table3: Operating Profit Scenario of PBL

Years | 2006 | 2007 | 2008 | 2009 | 20010 |

Taka in million | 2131 | 3257 | 3247 | 5289 | 6078 |

Source: Annual Report-2010

CONSUMER CREDIT SCHEME IN BANGLADESH:

a. Introduction:

Bangladesh is a third world developing country. Per capita income of our country is very poor. So, the majority of our population is forced to live a sub-standard life. The middle class and the disciplined professionals cannot afford to buy essential utility products at a time. As such, they cannot able to raise their living standard to an expected level. Different private sector banks and foreign commercial banks have introduced the household durable loan scheme known as “Consumers Credit Scheme” to fulfill the dreams and desires of middle class fixed income group by providing loan to purchase necessary products.

b. CCS in Bangladesh:

Consumer Credit Scheme is very much popular in most of the developed and developing countries of the world. This is designed to finance the fixed income group for buying essential commodities, which is to be repaid by monthly installment over a period in accordance with a contractual agreement. Consumer Credit Scheme is becoming very much popular in our country. A good number of financial institutions in our country are successfully operating this program. First of all Islami Bank Bangladesh Limited introduced this loan in 1993. Following their success other private banks like Prime Bank Ltd., Uttara Bank Ltd., Pubali Bank Ltd., Mercantile Bank Ltd., IFIC Bank Ltd. and other introduced this scheme later. Now about to every private sector banks offers this household durable loan. But among the foreign commercial banks this is not that much practiced. But very few banks offer this CCS loan extensively. Some other banks failed to operate CCS successfully as a result they bound to close-up this program like Dhaka Bank Limited.

CONSUMER CREDIT SCHEME OF PRIME BANK LIMITED

Bangladesh is a country having its population of above 140 million. When the world turns to be a “Global Village”, 36% of our people live below the poverty line. In this situation when all other banks are running after making profit, Prime Bank is committed to play a vital role in the overall socio economic development of our country. As per its commitment, it launched “Consumer Credit Scheme” in the Year 1995 to enhance the living standard of the people of limited and fixed income.

Prime Bank tries to establish the concept of “Relationship Banking”. It treats clients as its ‘Financial Partner’ and always intends to be a friend of rainy days by means of proving financial assistance in those days. Till the current fiscal period it provides financing for the following purposes:

To purchase different home appliances

To purchase equipments for medical services

To purchase motor vehicles

To meet up emergency or sudden needs

All of the above facilities were not available under the ‘Consumer Credit Scheme, launched in the year 1995. The new facilities are added with the Consumer Credit Scheme under the head of the “ Retail credit Scheme”. This new scheme has been introduced recently and it came to effect from the 1st March 2004.

OBJECTIVES OF THE SCHEMES:

- Prime Bank Limited started the Consumer Credit Scheme program with a view to fulfill its benevolent institutional objectives through financing the middle class limited income group.

- To ensure the credit facility to the both middle class Limited income group and upper class income group.

- To improve the living standard of limited income group through financing in purchasing necessary goods.

- To participate in the socio-economic development of the country.

ELIGIBILITY OF THE CUSTOMER:

Any interested person within the range of 25 to 60 and having a permanent job or the permanent employees of the following organization can apply for the CCS loan of Prime Bank.

- Government Organizations.

- Semi-Government and Autonomous Bodies.

- Banks, Insurances Companies or any other financial institutions.

- Armed Forces, B.D.R, Police and Ansar.

- Private Organizations having corporate structure.

- Teachers of Universities, Colleges and Schools.

- Permanent employees of locally established and renounced Public Limited Companies.

- Permanent employees of Multinational Companies.

- Permanent employees of Bank acceptable companies

- Professionals such as Doctors, Engineers, Lawyers, Architects, Chartered Accountants, Journalists, and self employed person etc.

DISCOURAGE LIST OF THE CUSTOMER:

The following are the people who should be discouraged in extending credit facilities under this scheme:

- The employees of frequently transferable services.

- The employees of enterprises which are not of good reputation.

- Employees having take home salary less than taka 10,000 per month.

PRODUCTS OF PRIME BANK LIMITED:

The products of Prime Bank with their financing items under CCS loan are given below:

Household Durable Loan: Motor Cycle, Personal Computer, Photocopier, Fax machine, Small PABX system, Television, Mobile Phone set, Refrigerator, Audio-video equipment, Other home electric appliances, Furniture and any other household items.

Car Loan: Car, Jeep, Station Jeep, Pick up Van, Cover Van, Bus, Truck, Abulance and any other vehicle for own use.

Doctors Loan: For the Doctors only.

Advance against Salary: Any qualified person

Education Loan: For Study purpose only

Travel Loan: For traveling purpose,

Wedding loan: For wedding only.

CNG Conversion Loan: To convert into CNG

Any Purpose Loan: For emergency need

Hospitalization Loan: For treatment in hospital

Home loan (Sawpna Neer): For buying, renovation and reconstruction of home.

CREDIT LIMIT, PERIOD OF LOAN AND DOWN PAYMENT:

Under CCS program of Prime Bank Limited a borrower can get maximum of taka 40, 00,000 and minimum taka 10,000. The down payment is 10% of the loan for all products except Car and Home Loan (Swapna Neer) loan which required 40%.

INTEREST AND OTHER CHARGES:

The interest rate is 15% for the all products except Home (Swapna Neer) Loan. The interest rate of Home (Swapna Neer) Loan is 13%. And Prime Bank charges 1% service charge and 1% risk fund for all products except Home (Swapna Neer) Loan for 0.50%.

APPLICATION PROCEDURE:

The intending client will have to apply for the credit in Bank’s printed application form, which is available in respective Branch on payment of Taka 10 only. Customers will submit the application form dully filed-in with 2(two) photograph and signed along with quotation for purchase of desired article or any other relevant documents.

The customers’ name/other name(s) including nickname, if any should be mentioned in every loan application.

PROCESSING OF APPLICATIONS:

On proper scrutiny of the application, branch will inform the initial decision (acceptable for processing /decline) to the applicant within 3(three) working days from the date of receiving application. Applicant will submit the above dully filed-in with the following additional papers:

- Salary certificate for service holders.

- Trade license and TIN Certificate (if any) for businessperson.

- TIN Certificate of applicants for vehicle loan (compulsory)

- Bank statement of last six month.

- Attested photocopies of current tax receipt, electric bill etc & lease agreement (if any) when the source of income is house rent as a land lord.

Branch will inspect the given information with respect to eligibility, feasibility and security. After completion of all necessary formalities, Branch shall disburse the loan or refuse the proposal within 7(seven) working days from receiving the additional papers. Price of the items (Down payment + loan amount) should be given to the respective supplier through Payment order (PO) after completion of necessary documentation.

MODE OF REPAYMENT:

Repayment of loans including accrued interest will be made by equal monthly installments, which will start from the following month of the disbursement of loan. Before disbursement of loan, the customer will deposit crossed cheque covering the total number of monthly installments in favor of Bank which will have to be presented for collection on the due date. Installment will be paid within 7th day of each month. However, prepayment is allowed.

OTHER CONDITIONS:

- Customer will bear the license fee, registration fee, insurance charge etc, if any, in respect of the articles.

- Customer will bear the expenses for necessary repair and maintenance of the articles during the period loan.

After delivery of the articles, the respective customer shall remain responsible if the articles are broken, stolen or damaged. The articles shall be used by the customer with optimum care, caution and prudence and he will be liable for

- Compensation or replacement etc. for any damaged caused due to this negligence, carelessness and inefficient handling. In the event of the articles being lost or totally damaged and become irreparable due to his negligence, careless ness and inefficient handling, he will be liable to adjust Bank’s due i.e. outstanding principal, interest and other charges on demand.

- Customer will inform the Bank of any Change of his address immediately after the change.

- The articles shall remain in sole control and custody of the customer who will not let out, lend, resell or transfer the possession or rights of the same to a third party under any circumstances.

- Customer will keep available all the articles supplied to him for inspection by the Bank officials or supervising agency as and when required.

- Default in payment of 3(three) consecutive installments shall render the customer liable to handover the articles of the Bank.

- In case of loan for purchase of Car loan, the registration of the vehicle loan shall be made in the sole name of the Bank/joint name of the Bank and the customer until full adjustment of the loan.

- The Registration, Blue book, Tax token, Fitness Certificate, etc for vehicles must always be kept up to date at the cost of the customer.

- The vehicles must be covered by comprehensive insurance policy to be taken by the customer on his own expenses.

- No additional amount will be paid by bank for repairing or any other purpose for which credit was allowed.

JUDGEMENT PROCESS OF CREDIT PROPOSAL UNDER THE CCS:

Loan and Advances are the main form of asset of a bank. It is very crucial for any bank because it generates the greatest part of revenue for a bank. Within the total credit portfolio consumer credit is the most popular form of credit because it is easily recoverable. To disburse the loan, the credit officer has to verify the potential borrower’s income, expenditure pattern, type of service etc to select the appropriate borrower. The factors which are considered in this process are stated below:

a. Borrower’s income:

It is the vital factor for selecting a borrower. To gather required information in his regard, the borrower is requested to allow the credit officer to verify the following subject matters:

- Place of employment

- The stated Salary

- The continuity of Existing job

- Income from part time employment

- Spouse’s income

- Income from rentals

- Dividend or interest

- Children’s support

Besides these the credit officer also verifies borrower’s income from the TIN certificate, tax return and salary statement etc.

b. Estimated Housing Expenses:

The credit officer tries to evaluate the expenditure pattern as well as monthly living expenditure with the help of the following information:

- Children’s educational expenses

- House rent

- Interest payment on previous borrowing

- Interest payment for the loan which is under consideration

c. Location:

The location of the borrower is an important factor for selecting any borrower. If the location of the borrower is far from the bank, the physical communication becomes tough for the bank. So bank likes to provide loan to those who stay near to the bank’s branch.

d. Assessment of credit History:

The credit officer evaluates the credit history of a potential borrower with the help of the CIB report and with the inquiry of his or her Business community subsequently verified by five outsourcing CPV (Contact Point Verification) agents namely Credit Ben Balance Consultancy, Snipers Secures Limited, Beacon Consultancy Services, Management Consultancy Limited and Prime Asset and Insight Management. Quality of a loan is heavily dependent on the reports provided by the low salaried employees of the outsource agents.

e. Social Status:

Social status of a borrower is to be verified from the following information:

- Ownership of a car

- Ownership of a House in the metropolitan area

- Holding a land phone in residence

- Holding a passport, TIN certificate

- Membership of a first club

- Marital status

- Guarantors status:

Under the CCS, credit is offered by taking personal guarantors from a third party. The guarantor will be liable for the default of loan. So guarantor’s designation, type of job, monthly salary, period of service, office address, and the consent of the guarantors regarding the matters are evaluated.

MONITORING AND RECOVERY:

The credit under this scheme is fully supervised and as such, the success of the scheme depends on proper and persistent supervision, follow up, persuasion and monitoring of the credits by the Branches. Branches shall maintain proper records of the applications received, loan sanctioned, disbursement and recovery made. It is worthwhile to mention here that optimum recovery can be ensured by developing relationship with the customers and the beneficiaries and maintaining supervision thereon without filing any suit/case. The mechanism of supervision and monitoring are as follows:

- Regular checking of the balance of the clients account

- Regular communication with the defaulting customer and guarantors physically/over telephone.

- Issuance of letter to customers immediately after dishonor of cheque.

- Issuance of letter to defaulting customers and respective guarantors.

- Contacting the employers of the defaulting customers (after there overdue installments)

- Issuance of legal notice to the customers and guarantors prior classification of loans.

- Periodical visit to the customer to maintain relationship and supervision of supplied goods/items.

- Call Center of Head Office Recovery Unit of Retail Banking Division is currently handling only Overdue (Standard) and SMA (Special Mention Account) files with the help of 79(Seventy Nine) Collection Executives. There are also six outsourcing agents such as Standard Credit Collection Agency, Smart Way, Quorum Financial Services Limited, Intelligent Credit Care Advance Business Snipers Secures Limited and Legal Care Services Limited also involved in recovery of overdue and all types of classified loans as referred to them by the Management.

- Legal actions to be taken after all possible efforts to recover the Bank’s dues have in vain.

STEPS AGAINST DEFAULTERS:

If a borrower fails to pay 3(three) installments consecutively he/she consider as a defaulter. Prime Bank Limited usually follows the following guidelines for treatment of its overdue installments.

- Telephone contact

- Cheque bounce Letter

- Overdue recover Letter

- Letter of guarantors

- Letter to authority

- Legal notice to borrower and guarantor

- Suit notice

LOAN AMORTIZATION:

Prime Bank uses the most common loan amortization method that is “Capital Recovery Method”. Under this method constant monthly payment is calculated on an original loan amount at affixed interest for a given term.

Example: Loan Amount: BDT 100,000 (PV)

Interest rate: 15 %( r)

Number of Installments (monthly): 24

So monthly install will be: PV/*MPVIFA@15%, 24months)

So Monthly installment: 100,000/20.62423451=BDT 4848.66/Month

*MPVIFA=Monthly Present Value Annuity Factor.

| Month (1) | Beginning Balance(2) | Monthly Interest (3)=(2)*(.15/12) | Monthly Payment (4) | Monthly Amortization (5)=(4)-(3) | Balance (6)=(2)-(5) |

| 1 | 100,000 | 1250 | 4848.66 | 3598.66 | 96,401.34 |

| 2 | 96,401.34 | 1205.02 | 4848.66 | 3643.65 | 92,757.69 |

| 3 | 92,757.69 | 1159.47 | 4848.66 | 3689.19 | 89,068.49 |

| 4 | 89,068.49 | 1113.36 | 4848.66 | 3735.31 | 85,333.18 |

PREPAYMENT:

Customers can repay the loan before maturity of the loan. In case of early payment bank has to face reinvestment risk. That is from the early payment of a loan bank gets an unanticipated fund that may or may not be invested at the previous rate, because interest tends to decline over time because of the growing competition among banks. But Prime Bank usually welcomes the early repayment of loan and offers a rebate of interest amount as well as no prepayment penalty is to be charged like other banks. The reason behind this is that Prime Bank tries to avoid classified loan even at the cost of losing some profit and receiving risk just to maintain its credit history and good CAMEL rating

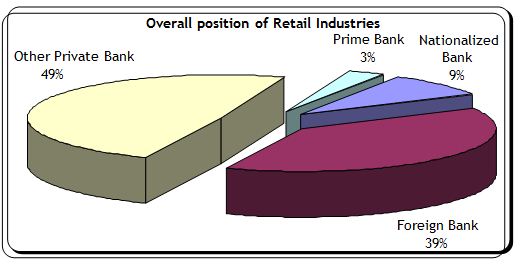

OVERALL POSITION OF RETAIL LOAN INDUSTRY:

The total portfolio of retail loan in Bangladesh is around 26,000 crore where Prime bank’s portfolio is 783.57 crore as on 31.06.2010 i.e. 3% of the industries. The overall position is as follows: –

PRESENT POSITION OF PRIME BANK RETAIL LOAN:

Position of retail loan as on 30.06.2010 is as follows: –

- Outstanding: BDT 783.57 crore involving 23522 accounts (8% of total advance of the bank)

- Target was BDT 1200 crore i.e. achieved 66%

- Average monthly disbursement in 2010: BDT 26.55 crore

- Average monthly recovery in 2010: 25.69 crore

- Overdue: BDT 72.63 crore involving 6632 accounts (9.12% of total portfolio)

- Classification: BDT 37.65 crore involving 2053 accounts (4.81% of total portfolio)

- Special Mention Account (SMA): BDT 27 crore involving 1083 accounts (4.6% of total portfolio)

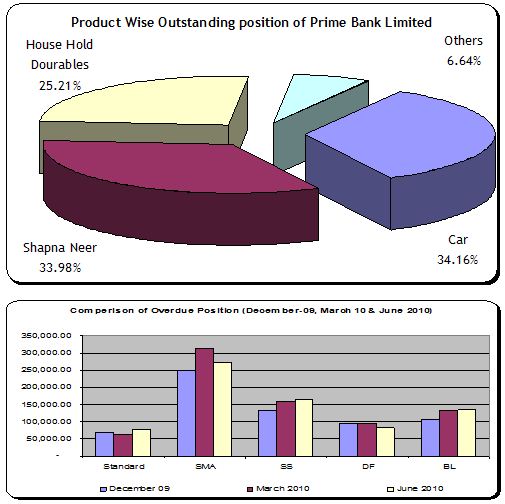

PRODUCT WISE POSITION OF PRIME RETAL:

Product wise position as on 30.06.2010 is as follows:

EVALUATION OF CCS OF PRIME BANK LIMITED:

Consumer Credit Scheme is one of the most attractive Schemes for both clients and bank. Because of the continuous improvement of the standard of living attractiveness of CCS is also increasing day by day. For this reason all of the banks are trying to improve their performance in CCS. Though CCS of every bank is similar but CCS sector of every bank have some strong and weak points that affect their performance to the customers. The current scenario of CCS of PBL in compare with other banks is discussed here.

PBL has high reputation as a bank that practices customer oriented banking among the local banks of Bangladesh. Besides, this year PBL has received SAFA (South Asian Federation of Accountants) award as the “Best Bank” and also received ICBA for “best presented accounts” and ICMAB for “best corporate governance” award.

Prime Bank has already launched every product available under CCS. Not any other bank except Prime bank has launched all of these schemes yet. This characteristic of CCS of PBL is positively considered by customers while taking decision of taking loan under CCS. Moreover no other banks are providing C.N.G. Conversion loan which is an exclusive scheme offered by Prime bank. In this aspect Prime bank has an absolute advantage over the other banks in this scheme.

Prime bank have a large number of branches all over the country. It already has 90 branches all over the country and the number is increasing day by day. As a result of these it has a large customer base. This huge customer base is very helpful for CCS because every customer of different schemes can be a possible customer of CCS.

PBL is very conservative in customer selection. Prime Bank Limited does not establish any link with any multinational company consists of huge employee base and salary amount. Multinational Banks earn huge profit from this type of liaison. For example, Standard Chartered Bank has link with Grameen phone and Bangla Link and HSBC has link with Robi and Citycell. The whole salary amounts of these companies provide a huge deposit for these banks. Prime bank does not practice priority banking. Whereas multinational banks often provides priority banking services. Banks usually provides priority banking services by preferential pricing on all products and charge-free banking services. For example, Standard Chartered bank treats Grameen Phone’s employees specially. Standard chartered charges only 50% or nil service charge from employees of GP and also allows rebate for them.

The well-behaved and generous employee base of CCS of Prime Bank is another positive side of CCS of PBL. Employees of CCS successfully build and maintain long term relationship with customers. Prime bank provides more prompt service than any other local bank. Telephone inquiries of consumers of PBL get highest response. But PBL does not practice job rotation adequately which causes few employees have versatile expertise in different banking sector which creates problem at the time of new posting.

The credit policy of Prime bank is not flexible but Prime Bank always tries to match their policy with the government policy and customer needs which increases its acceptability to customers.

PBL do not have any plan to practice fast track banking. Documents demanded by CCS of PBL are huge in compare with multinational bank. The loan sanctioning procedure of Prime Bank limited is lengthier than multinational banks. It will take 10-15 days for sanctioning a loan under CCS of PBL.

Like other local banks, PBL also can not practice proper employee selection, motivation & training for Consumer Credit Scheme (CCS). Assign right person at right place in right time is the main task of HRM. Like other private banks Prime Bank also appoint employee from internal sources. Some times this includes inefficient employees in the employee base. For these reason, lack of efficient employee in CCS department is becoming a problem for PBL like other local banks. Now-a-days all multinational and foreign banks preferred comparatively young persons as high officials. The reason behind this is the hypothesis that a young person can easily understand the current market situation and modern customers’ demand than an older official who is used to work within a backdated system for years after years. Like other local banks in Prime Bank absence of younger people as high officials has been seemed. Like other private banks and companies CCS of Prime Bank also suffers for shortage of manpower which reduces the efficiency of services.

Monitoring and recovery of CCS Loan in PBL is comparatively weak than other banks. For this weakness bank have to tolerate more overdue. Prime Bank disburses the loans on different dates of months and the last date of payment of installment is also different for different loans. So, it becomes very difficult to find out that exactly which loans’ installments are overdue and how many installments are overdue on a specific date. When defaulters are identified in the meantime a huge overdue amount has already piled up and collection of a huge amount is always difficult than that of a small amount.

Marketing Department of CCS department in PBL is weak. PBL is suffering for lack of efficient sales people like other local banks. The research and development sector of marketing in CCS is not much effective. R&D sector of CCS does not use enough primary sources in data collection while conducting a study. They usually use secondary sources of data that may be inaccurate, invalid and backdated. The current market situation of CCS is not clearly known to PBL because of its weak R&D sector. For this reason it can not compete with multinational banks and can not attract high profile customers.

Computer and IT department regarding CCS is really weak. For IT problem Service of CCS and other sector is affected negatively. The banking software used by Prime Bank Limited is T24. T24 is the latest banking software but Prime bank does not have enough capacity and expertise to customize this software according to their need regarding proper functioning of CCS. For this reason many problem arises. For example, accrual of interest after classification of a loan as Bad & Loss (Bad & Los refers to overdue of more than 12 monthly installments in case of CCS). The capacity of server is not enough for retail banking. In pick banking hours different problems arise like server become overloaded; IPs’ are conflicted with each other and stops printing. Though Prime Bank developed a website for its CCS customers and interested persons to inform about their products and services, it rarely updates its website. This kind of practice may misguide its customers about up-to-date information.

After all, it can be said that performance of CCS of PBL is satisfactory while comparing with other local banks but not at all satisfactory while comparing with multinational banks.

FINDINGS

- PBL does not use adequate primary sources of regarding Research & Development of Consumer Credit Scheme. For this reason they do not get enough appropriate information about market, customers’ demand, current situation, and competitors to contribute in decision making.

- PBL does not able to establish not establish any link with multinational companies who can be high profile customers.

- An important part of credit assessment is Contact Point Verification (CPV) which verifies the authenticity of all credit related information provided by the potential customers. At present the PBL has been executing this part through five Outsourcing Agents namely Credit Ben balance constancy, Snipers Secures Limited, Beacon Consultancy Services, Management Consultancy Limited and Prime Asset and Insight Management. Quality of a loan is heavily dependent on the reports provided by the low salaried employees of the outsourcing agents. On the other hand the bank has not the capability to verify all the information provided by the customers within the competitive time by its own resources at this moment. As a result, over dependency of outsourcing agents regarding verification of information may crease the default risk.

- Bank Account Statement especially for businessmen is one of the top most tools for assessing income of the customer since there is no practice of taking other business related documents for retail loan sanctioning in PBL. It is observed that assessing of income through verifying of bank account statement is problematic as the most of the business transactions of Small and Medium Enterprises are executed outside the Bank and maintaining of many Banks’ accounts by the businessmen who executed their business transaction through Bank.

- For salaried people it is very tough to find out the actual salary if the salary does not go to bank account as in most of the cases the salary statement is becoming manipulated.

- Credit Matrix for loan assessing is not being followed all time and sanctioning of loan period is sometimes delayed upto 10-15 days due to hold of sanctioning authority entirely by Head Office and delegation of hierarchy which is not appreciated by the vital clients.

- Lack of maintaining proper customer database which results loan duplication of default and ill customers.

- Payback period of different loans under CCS of Prime Bank is comparatively less than other banks

- PBL has able to establish a diversified product mix in their Consumer Credit Scheme to satisfy the various types of demand of different segment of people.

- Interest rate in consumer credit scheme of PBL is lower than industry average.

- The bank has achieved 18% growth compare to last year in retail loan outstanding which is the 8% of total Loans and Advance portfolio of the Bank.

- Car loan and Swapna Neer (Home Loan) is 68% of total retail portfolio which is in one sense good for the Bank as the above two products are more secured than other retail products. On the other hand, concentration in one or two products out of total retail portfolio is risky.

- The overdue, SMA and classification position of the bank is very much alarming. The trend of overdue. SMA and Classified loans are increasing.

- Call Center of Head Office Recovery Unit of Retail Banking Division is currently handling only Overdue (Standard) and SMA (Special Mention Account) files with the help of 79(Seventy Nine) Collection Executives. There are also six outsourcing agents such as Standard Credit Collection Agency, Smart Way, Quorum Financial Services Limited, Intelligent Credit Care Advance Business Snipers Secures Limited and Legal Care Services Limited also involved in recovery of overdue and all types of classified loans as referred to them by the Management. The performance of Recovery Unit is acceptable but the Recovery Agents performance is very poor.

- Recovery through legal action is not profitable to the Bank due to high cost involvement rather than claim amount.

- The key factor of success in Consumer Credit Scheme of PBL is well-behaved, skilled and service oriented employee base.

RECOMMEDATIONS:

- PBL should use more primary sources of data while conducting research. Then the studies will be more effective and will contribute more in decision making.

- For Strong MIS and Healthy portfolio Bank should go for a Retail Banking Software for Disbursement, Sales, Approval and Recovery purpose.

- Since the bank has been doing CPV (Contact Point Verification) through third party(s) so the bank official should involve in cross checking as much as possible.

- Without proper verification of bank statement no loan should be processed for businessman.

- For Salaried people only those applications should be considered where there is standard corporate culture.

- Credit Matrix for loan assessing should be followed always and credit sanctioning period should be reduced to 7 days.

- PBL should award the authority of sanctioning of CCS loan at a limited level to Branch.

- The bank may focus more on maintaining proper database so that default customers of the bank do not get any opportunity for availing of any further loan.

- PBL should be cautious in connection with the registration of vehicles with BRTA and do cross check the registration by their officers duly since a number customer submitted faked Blue Book, Tax token, Route Permit and Insurance certificate to different branches.

- No disbursement should be made before execution of Tripartite Agreement between client, Developer (must be a member of REHAB) and the Bank.

- Payback period should be enhanced considering the customers need.

- Risk fund which is being taken against most of the product may be refundable.

- The bank should give more focus on initial stage recovery strategy.

- RecoveryCenter of Head Office should be restructured and developed for handling all the delinquent customers of the bank.

- Bank should appoint Legal Officer for handling the legal activities in connection with the CCS.

- PBL should arrange regular training on technological changes for its employees to be familiar with modern technological changes so that they can take it as a challenge to convert technological changes into organizational advancement and maintain standard customer service.

CONCLUSION:

The Prime Bank Ltd. is one of the largest local banks in our country. For any kind of loan and advances PBL is always preferred by people who preferred local banks. The banking sector plays an important role in the success of economic development of the country. But this sector has been suffering from so many problems like corruptions, unsatisfactory performance level or overdue loan, poor recovery rate and unethical and illegal influences in decision-making process etc. These problems can be overcome through increasing employees’ efficiency by training & motivating, enhance recovery rate, strictly prohibiting unethical & illegal influences in decision making process etc. There is no alternative of skilled, trained and professional manpower. So, continuous training, learning and development are essential for Prime Bank Ltd. to enrich knowledge and develop skills and competences to succeed in today’s dynamic banking world and to compete with multinational banks. To reach its expected goals, Prime Bank Limited has to compete with multinational and foreign banks along with local bank. After all, PBL must put special attention to its employees, customer segmentation, service quality and IT and R&D sector.