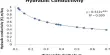

Time value is the main reason there is little exercising of options but a considerable amount of closing out, offsetting, covering, and selling of shares or contracts. It is basically the risk premium that the seller requires to provide the option buyer with the right to buy/sell the stock up to the expiration date. Think of this component as the “insurance premium” of the option.

When calculating time value, it is measured as any value of an option other than its intrinsic value.

Option Price – Intrinsic Value = Time Value

For example, if Company XYZ is trading for $25 and the XYZ 20 call option is trading at $7, then we would say that the option has an intrinsic value of $5 ($25 – $20 = $5), and the time value of $2 ($7 – $5 = $2).

Options that have zero intrinsic value are comprised entirely of time value.

The market determines this part of the premium but it is not a random assessment. Many factors come into play in the establishment of the time value of an option. For example, the Black-Scholes option pricing model relies on the interplay of five separate factors:

- Price of the underlying asset

- The strike price of the option

- The standard deviation of the underlying asset

- Time to expiration

- Risk-free rate

The Basics of Time Value –

The price (or cost) of an option is an amount of money known as the premium. An option buyer pays this premium to an option seller in exchange for the right granted by the option: the choice to exercise the option to buy or sell an asset or to allow it to expire worthlessly.

The intrinsic value is the difference between the price of the underlying asset (for example, the stock or commodity or whatever the option is being taken out on) and the strike price of the option. The intrinsic value for a call option (the right but not the obligation to buy an asset) is equal to the underlying price minus the strike price; the intrinsic value for a put option (the right to sell an asset) is equal to the strike price minus the underlying price. So, an option’s time value is equal to its premium (the cost of the option) minus its intrinsic value (the difference between the strike price and the price of the underlying asset).

Basically, an option’s time value is largely determined by the amount of volatility that the market believes the stock will exhibit before expiration. If the market does not expect the stock to move much, then the option’s time value will be relatively low.

Meanwhile, the opposite is true for stocks that are expected to be very volatile. High-beta stocks, or those that tend to be more volatile than the general market, usually have very high time values because of the uncertainty of the stock price prior to an options expiration.

Information Sources: