Background of the report

Mutual Trust Bank is the largest local commercial bank operating in Bangladesh. They have a huge customer base that is ever growing. Mutual Trust Bank is mainly providing two types of service.

1) Corporate Financial Services

2) Consumer Financial Services.

Consumer financial services include account opening, card services, loan facilities, and so on. General Banking is one of the parts of customer financial service. General banking consists of account opening for various types of deposit and saving scheme, card issue, chequebook issue, receiving foreign remittance, and such which will be discussed on the following chapters.

Origin of the report

The BBA internship program is a mandatory requirement for the students who are graduating from the BBA programme of Stamford University Bangladesh. In the internship program, I was attached to a host organization named ‘Mutual Trust Bank Ltd.’ Fulbaria branch for 12 weeks. During this period I learned how the host organization works with the help of the internal supervisor. As a result I have decided to make a report on “General Banking and Financial Performance of MTBL”.

Objective of the report

- To identify the level of customer satisfaction of MTBL.

- To recommend ways of improving the service standard that accommodates a rapidly growing customer volume.

- To find out what are the major factors that hamper satisfaction among General banking service in MTBL.

- To see if inclusion of some necessary product or documentation feature that is currently absent, or improvement of some existing facility can act to increase customer satisfaction.

Scope

The report will be limited to the level of customer satisfaction in the General banking service of MTBL. The focus of this report will be only on General banking and financial performance analysis of MTBL. The report is developed on the basis of my work in general banking with MTBL, Fulbaria Branch.

Methodology

I have got all the relevant information from my working experience with MTBL, their Annual report, some circular, various brochures, MTBL web site and such. Some information is taken from some of my teachers.

Primary data:

The primary data of this report is the information, which is gathered from MTBL while I worked with them.

Secondary data:

The secondary data of this report is collected from MTBL Annual report, some circular, various vouchers, web site, also some reports from which I got idea about the way of writing a report.

Benefit of the report

As a student, I have learned about a bank; I also have learned the report writing, as a great deal of theory is included in this report. It will be also benefited for the people who are interested to know about MTBL.

Limitations

The main limitation for conducting this report is time limitation and resources. Three months is not enough to understand all the activities of a bank and how they handle their clients. Lack of experience has also acted a constraint for the exploration of the topic.

MTB background

The Company was incorporated on September 29, 1999 under the Companies Act 1994 as a public company limited by shares for carrying out all kinds of banking activities with Authorized Capital of Tk. 38,00,000,000 divided into 38,000,000 ordinary shares of Tk.100 each.

The Company was also issued Certificate for Commencement of Business on the same day and was granted license on October 05, 1999 by Bangladesh Bank under the Banking Companies Act 1991 and started its banking operation on October 24, 1999. As envisaged in the Memorandum of Association and as licensed by Bangladesh Bank under the provisions of the Banking Companies Act 1991, the Company started its banking operation and entitled to carry out the following types of banking business

- All types of commercial banking activities including Money Market operations.

- Investment in Merchant Banking activities.

- Investment in Company activities.

- Financiers, Promoters, Capitalists etc.

- Financial Intermediary Services.

- Any related Financial Services.

The Company (Bank) operates through its Head Office at Dhaka and 30 branches. The Company/Bank carries out international business through a Global Network of Foreign Correspondent Banks.

The Registered Office of the Bank is:

68, Dilkusha C/A, Dhaka

Phone: 717 0138, 7170139, 7170140

Fax: 880-2-956 9762,

SWIFT-MTBL BD DH

Telex: 632173 MTB HO BJ E-mail: mtbl@bangla.net

Mission & Vision

Mission

MTBL aspire to be the most admired financial institution in the country, recognized as a dynamic, innovative and client focused company that offers an array of products and services in the search for excellence and to create an impressive economic value.

Vision

To be the bank of first choice by creating exceptional value for their clients, investor and employees alike.

MTB Branches

MTBL is operating all over the country with 30 branches. Most of branch are in Dhaka but they have braches in all main city like- chittagong, sylhet, khulna, Barishal , pabna and such.

MTB Online Banking

The ServiceMutual Trust Bank is playing a pioneering role among its competitors in providing real time online banking facilities to its customers. Mutual Trust Bank online banking offers a customer to deposit or withdraw any sum of money from any branch anywhere. Any account holder having a checking account with the bank can avail this service.

MTB Consumer Product & Services

- Brick by Brick

- Monthly Benefit plan

- Save everyday plan

- Children education plan

- MTB Double saver plan

- MTB Triple saver plan

- MTB Millionaire plan

- Unique saver plan

- Consumer Loan Scheme

- Small Business loan scheme

- House loan Scheme

- Home repair/ renovation loan scheme

- Auto loan scheme

- Visa electron debit card

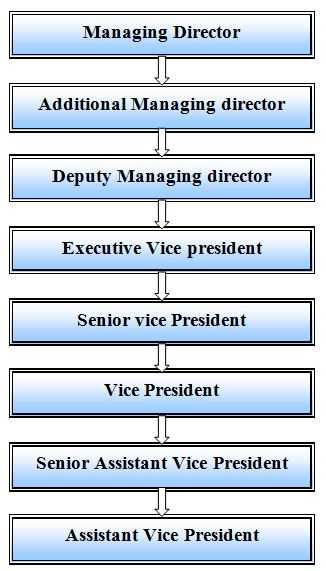

MTB Management hierarchy

MTB decision making & risk management

Risk is inherent in all the core business areas of a bank. Managing risks properly is one of the main pillars of banking business. To ensure sustainable growth and performance, proper and sound risk management practice is vital importance, as a commercial band Mutual Trust Bank Ltd (MTBL) attaches fill importance to manage the risk involved in its business. The risk management of the bank covers a wide spectrum of risk issue but the five core areas of Banking are—Credit risk, Foreign Exchange risk, Internal control and Compliance risk, Laundering risk and asset liability management. The principle objective of risk management is to safeguard the bank’s capital, financial resources, profitability and market reputation. To this effect, the bank took the following steps under guidelines of Bangladesh bank:

1. Credit Risk Management: Credit risk is the possibility that borrower or counter party will fail to meet its obligations in accordance with agrees terms. The failure may result from unwillingness of the counter party or decline in his/ her financial condition. Credit risk, therefore, arises from the bank’s dealing with or lending to corporate, individuals, other banks or financials institutions. A separate credit division has been formed at head office since the inspection of the bank, which is assigned with the duties of marketing and assessment of credit products, maintaining effective relationship with the customer and exploring new business opportunities. The credit risk management includes borrower risk analysis, financial statement analysis, industrial analysis, and historical performance of the customer, security of the proposed credit facility and market reputation of the borrower. MTB takes its lending decision based on the credit risk assessment report by appraisal team.

2. Foreign Exchange Risk: Foreign exchange risk is defined as the potential change in earning arising due to change in market prices. The market directly affects each country bond, equities, private property, manufacturing and all assets that are available to foreign investors. Foreign exchange rates also play a major role in determining who finance government deficits, which buys equities in companies and literally affects and influences the economic scenario. Due to high risk market the role of treasury operations is crucial. As per Bangladesh Bank guidelines the bank has segregated the front and back office for treasury operations. Front office independently conducts the transactions and the Back Office is responsible for verification of the deals and passing of their entries in books of accounts. All nostro accounts are reconciled on monthly basis and all foreign exchange transactions are revalued at Market-to- Market rate as determined by Bangladesh Bank

3. Internal Control and Compliance Risk Management: Internal control and compliance (ICC) is a critical component of bank management and foundation of the safe and sound operation of banking organization. A system of strong internal control and compliance can help to ensure that the goals and objectives of a banking organization will be met, that the bank will achieve long term profitability targets, and maintain reliable financial and managerial reporting. Operational loss may arise from error and fraud due to lack of strong internal control and compliance culture. Effective internal control and compliance can help to ensure that the bank will comply with laws and regulation as well policies, plans, internal rules and procedures, and decreases the risk of unexpected losses or damage to the bank’s reputation. To this effect, the bank an ICC Division headed by senior executives. The ICC Division has been segregated to three departments, which are Audit& Inspection Dept, Compliance Dept and Monitoring Dept. The bank has also developed an internal control and compliance policy duty approved by the board of directors. The Audit & Inspection team undertakes periodic and special audit. The audit committee of Board of Directors plays an effective role in providing between the board and management. The committee reviews the financial reporting prices, the system of internal control, the audit process and the bank’s process for compliance with laws, regulations and code of conduct.

4. Money Laundering prevention: Money laundering has been identified as a major thereat to the financial services community, it is important that the management of banks and other financial instructions view prevention of money laundering as part of their risk management strategies and not simply as a stand alone requirement that is being imposed by the legislation. The management of MTB is fully aware that the financial system shall not be and cannot be used as channel for criminal activities. Therefore, co-ordination and co-operation between concerned parties are essential for its success. The bank has designated Chief Anti Money Laundering Compliance Officer (CAMLCO) at head office and compliance officers at braches to review the transactions of the accounts to identify suspicious transaction profile (TP) has been incorporated in the Account Opening Form (AOF) along with other KYC related issues.

5. Asset Management: Asset/liability management has become al almost universally accepted approach to risk management. Since capital and profitability are intimately linked, Mutual Trust Bank Ltd. Is managing its asset/liability in order to ensure sustained profitability so that the bank can maintain and augment its capital resources. The assets/liability management committee (ALCO) usually makes decisions, which is reasonable for the financial direction of the bank. The ALCO’s goal is to manage the sources and uses of funds, identify balance sheet management issues like balance sheet gaps, interest rate gap. ALCO also reviews liquidity contingency plan and implements liability pricing strategy for the bank.

MTB human resources

MTB sincerely recognize the importance of skilled human resources for overall growth of the bank. The bank believes that a congenial working environment and people related policies generate team sprit and promotes a high level of integrity, loyalty, commitment and devotion among the employees. In order to maintain transparency, the bank engaged reputed and independent institution to conduct competitive written tests for recruitment of direct officers for the bank. The experienced officers are recruited through a selection committee upholding justice to the deserving candidates. The bank particularly stresses the need of training to the employees for their professional improvement. MTB Training institute conduct foundation course, workshop and seminar.

MTB five years at a glance

Figure in Million

| ITEMS

| 2006 | 2005 | 2004 | 2003 | 2002 |

| Authorized Capital

| 1,000.00 | 1,000.00 | 1,000.00 | 1,000.00 | 1,000.00 |

| Paid up Capital

| 950.40 | 864.00 | 720.00 | 600.00 | 200.00 |

| Shareholder’s equity

| 1,904.80 | 1,547.48 | 1,217.55 | 970.35 | 320.02 |

| Total Capital

| 2,114.53 | 1,692.52 | 1,335.08 | 1,030.38 | 355.05 |

| Total Assets

| 26,217.99 | 19,306.99 | 15,931.03 | 9,037.53 | 5,832.10 |

| Total Deposits

| 22,264.05 | 16,098.54 | 13,164.13 | 7,163.67 | 5,158.11 |

| Total Loans and Advances

| 18,591.52 | 14.373.26 | 11,692.97 | 5,904.18 | 3,432.13 |

| Total Investments

| 3,055.69 | 2,495.98 | 1,676.21 | 5,904.18 | 3,437.13 |

| Export

| 12,943.29 | 8,810.00 | 5924.00 | 3,523.92 | 2,142.67 |

| Import

| 26,255.29 | 17,660.00 | 17,355.90 | 11,284.41 | 6,393.53 |

| Total Contingent liabilities | 9,671.39 | 7,498.27 | 5,474.58 | 3,887.90 | 1,315.14 |

| Operating Income

| 1,284,86 | 877.01 | 686.00 | 489.15 | 252.78 |

| Operating Expenditure

| 315.39 | 225.17 | 179.06 | 118.09 | 71.59 |

| Profit before provision and tax | 969.47 | 651.85 | 506.94 | 371.07 | 181.19 |

| Net profit after provision and tax | 478.28 | 336.17 | 274.19 | 190.34 | 98.52 |

| Total provision maintained

| 239.98 | 145.00 | 117.50 | 60.00 | 35.00 |

| Earning Assets

| 23,575.83 | 17,419.05 | 14,779.16 | 8,300.61 | 5,369.61 |

| Non- interest Earning Assets

| 2,642.16 | 1887.94 | 1,151.87 | 736.92 | 462.49 |

| Earning per share (Figure in taka) | 50.32 | 35.37 | 34.33 | 43.37 | 49.26 |

| Book value per share (Figure in taka) | 200.42 | 180.66 | 169.10 | 161.73 | 160.01 |

| Dividend cash

| 20% | 14% | – | – | 20% |

| Bonus share

| 5% | 10% | 20% | 20% | – |

| Return on Equity

| 25.11% | 22.00% | 20.30% | 19.62% | 30.79% |

| Return on Assets

| 1.82% | 1.74% | 1.55% | 2.11% | 1.69% |

| Lending- Deposit Ratio

| 83.50% | 89.28% | 88.82% | 82.42% | 66.64% |

| Capital adequacy Ratio

| 11.83% | 12.55% | 11.87% | 17.33% | 10.81% |

| Price –Earning Ratio (Times) | 6.80 | 11.35 | 17.10 | 5.14 | – |

| No. Of Branches

| 25 | 20 | 16 | 13 | 8 |

| No. Of Employees

| 470 | 376 | 298 | 228 | 142 |

General Banking Sections, Types of Accounts, Products

General Banking

Financial institution/ intermediary that mediates or stands between ultimate borrowers and ultimate lenders is knows as banking financial institution. Banks perform this function in two ways- taking deposits from various areas in different forms and lending that accumulated amount of money to the potential investors in other different forms. General Banking is the starting point of all the banking operating and aids in taking deposits and simultaneously provides some ancillaries services. It provides those customers who come frequently and those customers who come one time in banking for enjoying ancillary services. In some general banking activities, there is no relation between banker and customers who will take only one service form Bank.. Since bank in confined to provide the service everyday general banking is also known as retail banking.

General Banking consists of the many sections in the branch.

Customer Service.

Account Opening/Closing.

Remittance.

▫ Payment Order Issue

▫ Demand Draft Issue/Collection

▫ T.T. Issue/Collection

▫ Endorsements

▫ IBC/OBC Collection.

Deposit Department.

Locker Service.

Account’s Department.

▫ Clearing. ▫ Transfer. ▫ Cash.

Customer Services of MUTUAL TRUST BANK LIMITED: Professional merit and Competency, Flexibility, Determination and Dedication are the core resources that MTBL consider to be of paramount importance for building a client oriented modern banking. Customer satisfaction is MTBL foremost professional undertaking. Therefore, a satisfied client is MTBL precious product and they consider them MTBL ambassador in the market.

Account Opening of MTBL:

Under this department, MTBL officer opens different types of account on the request of clients. The procedure of opening account is given bellow:

Types of Accounts:

General Products are:

Current Deposit:

Interest Rate 0.00%

▫ Individual Account

▫ Joint Account

▫ Proprietor Ship Account

▫ Limited Company Account

Savings Deposits:

Interest Rate 6.25%

▫ Individual Account

▫ Joint Account

▫ Proprietor Ship Account

▫ Limited Company Account

Short Term Deposits:

Interest Rate 6.00%

▫ Individual Account

▫ Joint Account

▫ Proprietor Ship Account

▫ Limited Company Account

Fixed Deposits:

Fixed deposit is one, which is repayable after the expiry of a predetermined period fixed by him. The period varies form 1 month to 12 months. These deposits are not repayable on demand but they are withdraw able subject to a period of notice. Hence, it is a popularly known as ‘Time Deposit’ or ‘Time Liabilities”. Normally the money on a fixed deposit is not repayable before the expiry of a fixed period.

Before opening a Fixed Deposit Account a customer has to fill up an application form which contains the followings:

▫ Amount in figures

▫ Beneficiary’s name and address

▫ Period

▫ Rate of interest

▫ Date of issue

▫ Date of maturity

▫ Instructions:

– To be renewed automatically with interest for the next period.

– Not to be renewed for next period.

– Pay interest to account no. (——-) on maturity

▫ Special instruction

▫ How the account will be operated (singly or jointly)

▫ Signature (s)

▫ FDR no.

Then a FDR account is opened and it is recorded in the FDR Register which contains the following information,-

▫ FDR A/C no.

▫ FDR (Fixed Deposit Receipt) no.

▫ Name of the FDR Holder with address

▫ Maturity period

▫ Maturity date

▫ Interest rate

In case of Fixed Deposit Account the Bank needs to maintain a cash reserve. So MTBL offers a high interest rate in Fixed Deposit accounts. The interest rates followed by MTBL in Fixed Deposit accounts are:

Interest Rate:

1 months and above but less than 3 months: 8.50%

3 months and above but less than 6 months: 11.00%

6 months and above but less than 12 months: 11.25%

12 months and above: 11.75%

Source: GB Department & Banking Operations Division, circular REF: IC#BOD/21/07, Date: 04-06-2007

Festival Sanchay Prokalpa are:

Eid-Ul-Azha Sanchaya Prokalpa:

Interest Rate 10.00%

Eid-Ul-Fitre Sanchaya Prokalpa:

Interest Rate 10.00%

Durga-Puja Sanchaya Prokalpa:

Interest Rate 10.00%

Buddha-Purnima Sanchaya Prokalpa:

Interest Rate 10.00%

Boro-Din Sanchaya Prokalpa:

Interest Rate 10.00%

MTBL Consumer Banking Products are:

1. Brick by Brick Savings Scheme

2. Monthly Benefit Plan

3. Save Everyday Plan

4. Childrens Education Plan

5. Consumer Credit Scheme

6. BestInvest Plan

7. Unique Savings Plan

Some of MTBL Consumer Products

1. Brick By Brick Savings Scheme:

Monthly Installment 5 Years* 8 Years* 10 Years*

* The maturity value is an indicative figure. Tax/Excise Duty will be deducted as per govt. rules. 90% Loan Advantage on deposited amount. Thereafter in multiples of Tk. 5000 up to a limit of Tk. 100,000.

2. MTB Monthly Benefit Plan:

Deposit Amount Income Amount for 3-year plan* Income Amount for 5-year plan*

* The maturity value is an indicative figure. Tax/Excise Duty will be deducted as per govt. rules. 90% Loan Advantage on deposited amount.

3. Save Everyday Plan:

Saving money for the future is a common practice in any society. Savings help you to build a better tomorrow. Regular saving makes a man become disciplined, self confident and successful.

MTBL offers you “Save Everyday” Plan. The primary advantage of this plan is that you are absolutely free to choose your own time for depositing money into this account. You can deposit daily, weekly or monthly. The choice is yours, but the transactions will have to be within the Bank’s transaction hour.

This is a 5 year plan and you will be required to open the account with an initial deposit of Tk. 2500/= only. We offer you very attractive interest rate which is accrued in this account on a daily basis.

4. MTB Education Plan:

Monthly Installment 4 Years* 7 Years* 9 Years*

* The maturity value is an indicative figure. Tax/Excise Duty will be deducted as per govt. rules. 90% Loan Advantage on deposited amount.

5.Consumer Credit Scheme:

In order to make a significant contribution in the living standards of the people of medium and low income category, MTBL has introduced a scheme called “Consumer Credit Scheme”. With a view to materialize the dreams of those who are unable to make one time investment from their own savings, one can now afford to buy necessary household equipments and thus improve the standard of living.

All sorts of household durables eg. Television, Refrigerators, Computers, Air Conditioners, Video Cameras, Washing/ Drying Machines and Furnitures are allowed under this scheme. One can buy Motorcycle too under this programme.

The collateral security is minimum and the interest rates are one of the lowest in the market. Please contact the nearest branch for details.

6. Best Invest:

Best Invest offers you efficient high return investment plan. This plan helps you to build up a sizeable income in easy and affordable installments. This plan allows you to own 5 times the initial invested amount. Best Invest offers two separate and convenient term deposit periods for 4 years and 6 years respectively.

Best Invest is available in units worth Tk.50,000/- each. You will invest Tk.10,000/- as down payment for purchasing 1 (one) unit and the Bank will provide loan for Tk.40,000/-. The customer also has the option to buy units in multiples of Tk. 50,000/- but maximum unto Tk. 1,00,00,000/- (one crore).

This is a unique high return plan catering to all income group. So do not miss the opportunity.

Customized Products are:

MTB Double Saver Plan:

Deposit Amount Maturity Value after 6 Years*

* The maturity value is an indicative figure. Tax/Excise Duty will be deducted as per govt. rules. 90% Loan Advantage on deposited amount.

MTB Triple Saver Plan:

Deposit Amount Maturity Value after 11 Years*

* The maturity value is an indicative figure. Tax/Excise Duty will be deducted as per govt. rules. 90% Loan Advantage on deposited amount.

MTB Millionaire Plan:

Monthly Installment Year Maturity Value*

* The maturity value is an indicative figure. Tax/Excise Duty will be deducted as per govt. rules. 90% Loan Advantage on deposited amount.

7. MTB Unique Savings Plan:

Unique Savings Plan is an any day, any amount savings plan. The beauty of this plan is that a customer can deposit any day, any time and any amount.

Unique Savings Plan offers you to deposit any amount of your choice but not less than Tk. 500/- for 3/4/5 years. This is a high income plan with withdrawal facilities. The withdrawal facility will help you at the time of any emergency. You can withdraw 50% of the deposited balance for once a month. At maturity you will get a handsome amount.

Procedure of Account Opening, Interest Posting, Cheque Book Issues & Account Closing

Procedure of Account Opening:

Account Opening (Normal Account):

▫ Collect an Account opening form from the Bank.

▫ Fill all the requirements of the form.

▫ Nominee is must be specified.

▫ Photograph is most important for any account.

▫ The account holder sign of his/her own self in front or the specific bank principle Officer in the account opening form.

Account Opening (Saving Account):

▫ Collect an Account opening form from the Bank.

▫ Fill all the requirements of the form.

▫ Nominee is must be specified.

▫ Photograph is most important for any account.

▫ The account holder sign of his/her own self in front or the specific bank principle Officer in the account opening form.

▫ To open this account the most important things is that Passport Photocopy or the Word Commissioner Certificate must have to add with the account opening form.

Account Opening (Current Deposit Account):

▫ Collect an Account opening form from the Bank.

▫ Fill all the requirements of the form.

▫ Nominee is must be specified.

▫ Photograph is most important for any account.

▫ To open this account the most important things is that Passport Photocopy or the Word Commissioner Certificate must have to add with the account opening form and also enclose the form 12 with the account opening form.

Checklist of Documents to be obtained for various types of ACCOUNTS:

Sole Proprietorship:

1. Signature Card.

2. Photograph of signatories attested by introducer.

3. Copy of valid Trade License.

4. TIN Certificate.

5. 18-A permission from Bangladesh Bank (for GSA & Agents only).

Partnership:

1. Signature Card.

2. Photography of signatories attested by introducer.

3. Partnership Deed.

4. Partners letter of authority to open account and authorization for operation.

5. Copy of valid Trade License.

6. 18-A permission from Bangladesh Bank (for GSA & Agents only).

Limited Liability Company:

1. Signature Card.

2. Photograph of signatories attested by introducer.

3. Copy of Memorandum and Articles of Association (Certified by RJSC).

4. Copy of Certificate of Incorporation and commencement of business (In case of public Ltd. Co.).

5. Copy of Board Resolution to open the account and authorization for operation.

6. List of Directors and signatories along with addresses.

7. Latest copy of From XII.

Association/Trust/Society:

1. Signature Card.

2. Photograph of signatories attested by introducer.

3. Copy of Resolution of governing body to open the account and authorization for operation.

4. Copy of consolation / bylaws/ rules.

5. Certificate of registration.

6. List of authorized signatories and members of the governing bodies along with address.

7. Trust Deed (for Trust account only).

Interest Posting to Client’s account:

Bangladesh Government has circulated that, 10% deduction from the Bank’s Internal Account’s. This 10% tax deduction from the client’s interest.

Other wise another circulation is that, from the OBC collection every bank cut off there OBC commission as income account, here Bangladesh Bank said that 15% money cut off from the OBC collection as Vat on Others.

Cheque Book Issues:

Types of Cheque Book’s:

▫ Savings Account – 10 Leaves

▫ Current Deposit Account – 10 Leaves

▫ Current Deposit Account – 25 Leaves (CDTF)

▫ Current Deposit Account – 50 Leaves (CDF)

NB: CDTF: Current Deposit Twenty Five

CDF: Current Deposit Fifty

Cheque Issuing is Two Types:

Direct requisition slips

Cheque Book’s requisition slip

Customers Service Officer receives these types of slip from the client’s and gives the cheque books under processing. Processing means Cheque Book’s collect from the VOLT and the put account number in the cheque book, write down the serial number of the cheque book in the requisition slip and cheque book register, then Verified client signature. After all this things the Principal officer sign in the cheque leaves and sent the cheque book to another Principal officer for sign, after his sign the client receive the cheque book. These things the Principal Officer for sign, after his sign the client receive the cheque book. Then Principal Officer posting that cheque books leaves number in the computer data processing system.

A cover file containing the requisition slip is effectively preserved as vouchers. If any defect is noticed by the ledger keeper, he makes a remark to that effect on the requisition slip and forward it to the cancellation officer to decide whether a new checkbook to be issued to the customer or not.

Account Closing:

For two reasons, one can be closed. One is by banker and other is by the customer.

By banker: If any customer doesn’t maintain any transaction within six years and the A/C balance becomes lower than the minimum balance, banker has the right to close an A/C.

By customer: If the customer wants to close his A/C, he writes an application to the manager urging him to close his A/C.

Different procedures are followed in cash of different types of A/C to close:

Fixed deposit A/C is closed after the termination of the period.

Brick by Brick A/C is very easily closing if one of the clients didn’t pay his/her monthly installment at the bank three months one after one, in this way three months.

Another account’s will be closed on the parties advice, if they want to close any one of the account clients must have to submit an A/C closing letter through des pass. Then the Sr. Principal Officer checks it out and closes the A/C.

Closing process for current & savings A/C:

After receiving customer’s application the officer verifies the balance of the A/C.

He then calculates interest and other charges accumulated on the A/C.

If it bears a credit balance, the officer writes advice voucher. He gives necessary accounting entries post to accounts section.

The balance is returned to the customer. And lastly the A/C is closed.

But in practice, normally the customers don’t close A/C willingly. At times, customers don’t maintain any transaction for long time. Is this situation at first, the A/C becomes dormant and ultimately it is closed by the bank.

Remittance, Main instruments, Payment Order & Demand Draft Issue, Cancellation, Charges, Duplica

Remittance:

Remittance of funds is ancillary services of MTBL. It aids to remit fund from one place to another place on behalf of its customers as well as non- customers of Bank. MTBL has its branches in the major cities of the country and therefore, it serves as one of the best mediums for remittance of funds from one place to another.

The main instruments used by MTBL, Dilkusha Branch for remittance of funds.

▫ Payment Order Issue/Collection

▫ Demand Draft Issue/Collection

▫ T.T. Issue/Collection

▫ Endorsements

▫ Travelers Cheque Issuance

▫ IBC/OBC Collection.

Payment Order Issue/Collection: The pay order is an instrument issued by bank, instructing itself a certain amount of money mentioned in the instrument taking amount of money and commission when it is presented in bank. Only the branch of the bank that has issued it will make the payment of pay order.

Issuing of Pay Order:

The procedures for issuing a Pay Order are as follows:

▫ Deposit money by the customer along with application form.

▫ Give necessary entry in the bills payable (Pay Order) register where payee’s name, date, PO no, etc is mentioned.

▫ Prepared the instrument.

▫ After scrutinizing and approval of the instrument by the authority, it is delivered to customer. Signature of customer is taken on the counterpart.

Demand Draft Issue/Collection:

The person intending to remit the money through a Demand Draft (DD) has to deposit the money to be remitted with the commission which the banker charges for its services. The amount of commission depends on the amount to be remitted. On issue of the DD, the remitter does not remain a party to the instrument: i) Drawer branch ii) Drawee branch iii) Payee. This is treated as the current liability of the bank as the banker on the presentation of the instrument should pay the money. The banker event on receiving instructions from the remitter cannot stop the payment of the instrument. Stop payment can be done in the following cases:

Loss of draft before endorsement: In this case, “Draft reported to be lost, payee’s endorsement requires verification” is marked.

Loss of draft after endorsement: In this case, the branch first satisfies itself about the claimant and the endorsement in his favor.

Issuing of Duplicate DD:

If the customer wants to issue a duplicate DD, than customer is asked to do the following formalities:

Making a general diary (GD) in the nearest Police Station.

Furnishing an Indemnity Bond in Tk.50/= stamp

The banker immediately marks “stop payment” in the register after receiving the application from the customer and a duplicate DD is issued.

T.T. Issue Collection, Accounting entries, Procedures, Endorsements, IBC & OBC, Locker Service

T.T. Issue/Collection:

Telex transfer (TT) is another widely used mode for remittances of funds. In case of telex transfer the message for transfer of funds is communicated through tested telex. MTBL generally recovers from the telex charges in addition to the usual service charges.

Issuing of TT:

MTBL follows the following procedures:

The customer deposits money with MTBL to be sent.

The customer obtains a cash memo containing TT serial number.

TT serial number, notifying part name is mentioned in the telex message.

The Telex Department confirms transmission of the telex.

IBC/OBC:

By OBC, we mean that those cheques drawn on other banks which are not within the same clearing house. Officer gives OBC seal on this type of cheques and later sends a letter to the manager of the branch of the some Bank located in the branch on which cheque has been drawn. After collection of that bill branch advises the concerned branch in which cheques has been presented to credit the customer account through Inter Branch Credit Advice (IBCA).

In absence of the branch of the same bank, officer sends letter to manager of the bank on which the cheques is drawn. That bank will send pay order in the name of the branch. This is the procedure of OBC mechanism.

Actually OBC comes from the out side bank’s branch, or inter branches. Suppose AGRANI Bank, Jatrabari Branch sent a Cheque, which no: 012536, Tk. 5,00,000/- to Mutual Trust Bank Limited against AGRANI Bank Motijheel Corp. Branch. So this cheque could be an OBC. Now what Mutual Trust Bank Limited has to do? MTBL tries to collect this cheque through Bangladesh Bank Clearing House, and credited clients account.

OBC Collection Process:

Create a Voucher against OBC: S/D A/C OBC Tk. 5,00,000/-

.10% Cut off as Commission on OBC Tk. 500

15% Cut off as Vat on Others Tk. 75

Tk. 20/- Cut off as Postage Recovery Tk. 20

Total Tk. 595/-

In this condition MTBL got the cheque amount of Tk. 5,00,000/-, but after cut off the commission, vat and postage recovery MTBL will be credited the amount Tk. (5,00,000 – 595)= Tk. 4,99,405/- in party account.

Bangladesh Bank Circulation about OBC:

Bangladesh Bank has circulated some things about OBC. These are given below:

If the cheque amount will be under Tk. 1,00,000/- then bank’s OBC commission will be charged at .15%.

If the cheque amount will be above Tk. 1,00,000/- to Tk. 5,00,000/- then Bank’s OBC commission will be charged at .10%.

If the cheque amount will be above Tk. 5,00,000/- then Bank’s OBC commission will be charged at .5%.

Against the OBC the Government Tax will be realized on 15% on Commission Amount.

Postage Recovery will be realized Tk. 20/- for each OBC.

Locker Service:

MTBL Dilkusha Branch is providing facility of locker service for the purpose of safeguarding the valuable property of customers. The person or organization that has any account in bank branch can enjoy this service. They keep their valuable assets in banker’s custody. Customers have right to look after with a key of their individual locker provided by bank. MTBL maintains the following types of lockers:

▫ Large locker.

▫ Medium locker.

▫ Small locker.

For enjoying this service, clients have to give charge yearly Tk.2500/-, Tk.2000/- and Tk.1500/- for large, medium and small locker respectively.

Accounts Department of a bank branch – Cash, Clearing & Transfer, deposit slip

Accounts Department

Accounts Department is play most vital role in Banking. Accounts Department is a department with which each and every department is related. It records the profit & loss A/C and statement of assets and liabilities by applying “Golden Rules” of book-keeping. The functions of it are theoretical & computerized based. MTBL Dilkusha Branch records its accounts daily, weekly, and monthly every record. MTBL Dilkusha Branch Accounts Department in Charge: Mr. Kazi Imamul Haque, Sr. Executive Officer (having 12 years of experience in banking sector). Another officer’s are: Mr. Tarek, (Officer), Mr. Hamid (Teller-Officer), Mr. Sohel(Teller-Officer).

This entire executive’s helps me a lot in my internship program at MTBL. They didn’t guide me as an Internee; they guide me as a training officer of MTBL to gather practical knowledge about Banking. They tried there best to inform me every thing about accounts department. I hope I knew every thing that gave me as a new comer in banking sector.

Basically Accounts Department is not alone. Accounts department is a mix of as follows:

1. Cash

2. Transfer

3. Clearing

CASH

Mr. Kazi Imamul Haque, Sr. Executive Officer and Mr. Md. Tarek (Officer) is the cash in charge. Both of the two senior executives help’s me lot to get practical knowledge and prepare this report.

The cash section of any branch plays very significant role in Accounts Department. Because, it deals with most liquid assets the MTBL Dilkusha Branch has an equipped cash section. This section receives cash from depositors and pay cash against cheque, draft, PO, and pay in slip over the counter. Every Bank must have a cash counter where customer withdrawn and deposit there money. When the valued client’s deposit their money at the cash counter they must have to full fill the deposit slip his/her own, then they sing as the depositor option’s then they deposit their money through cash officer at the cash counter.

SEVERAL TYPES OF DEPOSIT SLIP :

There are several types of deposit slip as follows:

Current Deposit A/C Slip,

Saving’s Deposit A/C Slip,

Festival Deposit A/C Slip,

Brick By Brick Deposit A/C Slip,

Pay order Slip,

Demand Draft Slip,

T.T. Slip.

After paying this kind’s of slip, the valued client waits for the deposit slip book out side of the cash counter. The cash officer deposit the money in there account through computer software, while the depositors account credited, then the cash officer put a seal in the deposit slip and return it to the client.

RECEIVING CASH:

Any people who want to deposit money will fill up the deposit slip and give the form along with the money to the cash officer over the counter. The cash officer counts the cash and compares with the figure written in the deposit slip. Then he put his signature on the slip along with the ‘cash received’ seal and records in the cash receive register book against A/C number.

At the end of the procedure, the cash officer passes the deposit slip to the counter section for posting purpose and delivers duplicate slip to the clients.

DISBURSING CASH:

The drawn who wants to receive money against cheque comes to the payment counter and presents his cheque to the officer. He verifies the following information:

▫ Date of the cheque

▫ Signature of the A/C holder

▫ Material alteration

▫ Whether the cheque is crossed or not

▫ Whether the cheque is endorsed or not

▫ Whether the amount in figure and in word correspondent or not

Then he checks the cheque from computer for further verification. Here the following information is checked:

▫ Whether there is sufficient balance or not

▫ Whether there is stop payment instruction or not

▫ Whether there is any legal obstruction (Garnishee Order) or not

After checking everything, if all are in order the cash officer gives amount to the holder and records in the paid register.

The cash section of MTBL deals with all types of negotiable instruments, cash and other instruments and treated as a sensitive section of the bank. It includes the vault which is used as the store of cash instruments. The vault is insured up to Tk. 60 lacs. If the cash stock goes beyond this limit, the excess cash is then transferred to Principle Branch Office. When the excess cash is transferred to MTBL Principle Branch Office the cash officer issues IBDA.

Account treatment:

MTBL General A/C Dr.

Cash A/C Cr.

When cash is brought from MTBL Principle Branch Office.

Transfer, Clearing, Clearing House Process, types, Clearing Cheque

TRANSFER

Transfer is not a critical sector in banking but it is very important. Transfers play a vital role in banking sector. So now we have to know what transfer is: basically transfer is a type of register maintaining matter. In this register officer write down every day transactions in Debit and Credit side then the officer calculate both the side of the register if both side shown same amount, it means that the total day’s transaction is completely okay.

CLEARING

Clearing is one of the magical parts of banking. I really enjoyed this part of the accounts department and banking sector. In Mutual Trust Bank Limited clearing in charges Mr. Md. Jahir Ahmed (Officer), I did work with him. I went Bangladesh Bank lot’s of time with Mr. Md. Jahir Ahmed.

What is Clearing House?

In Bangladesh Bank, there is a very large room, which contains fifty (50) or more tables for each bank that is called the clearing house.

Nature of clearing house:

1st Clearing House

Return Clearing House

Clearing House Process:

Every bank has an officer of clearinghouse who is work with Bangladesh Bank clearing house. Acutally most of major client deposit their account in different kinds of bank cheques. Clearing officer check all the cheques and deposit slip very carefully and then he received the cheque. After that the clearing officer posting all the cheques in computer software which is recognized through Bankgladesh bank computer department. Then clearing officer seal all the cheques in advance date after that the officer endorsement all the cheques and sign all the cheques. All the cheques are posted in the computer by branch wise, then officer print the entire document and staple all the cheques by branch wise this is called schedule of clearing house. It is a very difficult job to staple all the cheques, because some time’s the cheques are huge in quantity, it may be 250 to 400, this is very vital job because every cheque must have to staple very carefully, it means cheque amount and the print sheet amount and cheque branch must have to be same. If the cheques staple in wrong direction, the cheque may be return from another bank, that’s why MTBL not to be able to credited party account.

Then the clearinghouse officer copying all the document in two floppy dist as per Bangladesh Bank requirement. When the clearing officers enter the clearinghouse, his first job is that the floppy dlivered to the Bangladesh Bank computer department.

All of the procedure the clearing in charge goes to the Bangladesh Bank clearing house before 10 am in the morning. The clearing officer check all the bank’s cheque and he put all the cheques in bank wise, like as this another bank’s delivered there cheques in MTBL desk. Then the officers of MTBL have to calculate all the cheques by using calculator machine, Staple pin remover, and then he divided all the cheques as MTBL Branch wise.

Types of Clearing Cheque:

MTBL Dilkusha Branch performs the bill clearing function through Bangladesh Bank. MTBL Dilkusha Branch acts as the agent of all MTBL branches for the clearing house of the Bangladesh Bank. There are two types of cheque which are-

1. Inward clearing cheque

2. Outward clearing cheque.

INWARD CHEQUES:

Inward cheques are those ones drawn the respective branch which have been presented on other banks and will be cleared / honored through the clearing house of Bangladesh Bank. Then the cheque is called inward cheque of MTBL Dilkusha Branch.

OUTWARD CHEQUES:

Outward cheques are those ones drawn on other bank branches which are presented on the concerned branch for collection through clearing house of Bangladesh Bank. These cheques are called outward clearing cheques.

RECOGNIZED BANK’S AS THE MEMBER OF BANGLADESH BANK CLEARING HOUSE WITH THEIR CLEARINGHOUSE CODE:

SL No. | Name of Bank | Code |

1 | Agrani Bank | 11 |

2 | Al-Baraka Bank Bangladesh Limited | 49 |

3 | Al-Arafah Islami Bank Limited | 57 |

4 | Arab Bangladesh Bank Limited | 41 |

5 | Bangladesh Bank | 10 |

6 | Bangladesh Commerce Bank | 64 |

7 | Bangladesh Krishi Bank | 31 |

8 | Bangladesh Shilpho Bank | 32 |

9 | Bangladesh Shilpo Rin Sangstha | 34 |

10 | Bank Asia Limited | 51 |

11 | Brac Bank Limited | 72 |

12 | Citi N.A Bank Limited | 26 |

13 | Cradit Agricole Indosuez | 27 |

14 | Dhaka Bank Limited | 56 |

15 | Dutch Bangla Bank Limited | 59 |

16 | Eastern Bank Limited | 52 |

17 | First Security Bank Limited | 67 |

18 | Habib Bank Limited | 25 |

19 | HSBC Limited | 83 |

20 | IFIC Bank Limited | 45 |

21 | Islami Bank Bangladesh Limited | 42 |

22 | Jamuna Bank Limited | 71 |

23 | Janata Bank | 12 |

24 | Marcentile Bank Limited | 60 |

25 | Mutual Trust Bank Limited | 65 |

26 | National Bank Limited | 43 |

27 | National Bank of Pakistan | 28 |

28 | National Credit and Commerce Bank Limited | 53 |

29 | One Bank Limited | 62 |

30 | Prime Bank Limited | 54 |

31 | Pubali Bank Limited | 47 |

32 | RAKUB |

Cash receipt & payment

The cash section of any branch plays very significant role in Accounts Department. Because, it deals with most liquid assets the MTBL has an equipped cash section. This section receives cash from depositors and pay cash against cheque, draft, PO, and pay in slip over the counter. Every bank must have a cash counter where customer withdrawn and deposit there money. When the valued client’s deposit their money at the cash counter they must have to full fill the deposit slip his/her own, then they sing as the depositor option’s then they deposit their money through cash officer at the cash counter.

Cash receipt

Any people who want to deposit money will fill up the deposit slip and give the form along with the money to the cash officer over the counter. The cash officer counts the cash and compares with the figure written in the deposit slip. Then he put his signature on the slip along with the ‘cash received’ seal and records in the cash receive register book against A/C number. The cash officer deposit the money in there account through computer software, while the depositors account credited, then the cash officer put a seal in the deposit slip and return it to the client There are several types of deposit slip as follows:

- Current Deposit A/C Slip

- Saving’s Deposit A/C Slip

- Festival Deposit A/C Slip

- Brick By Brick Deposit A/C Slip

- Pay order Slip

- Demand Draft Slip

- T.T. Slip.

Legal requirements

- Account number

- Account name

- Amount

- Date

- Branch name

Cash payment

The drawn who wants to receive money against cheque comes to the payment counter and presents his cheque to the officer. He verifies the following information:

- Date of the cheque

- Signature of the A/C holder

- Material alteration

- Whether the cheque is crossed or not

- Whether the cheque is endorsed or not

- Whether the amount in figure and in word correspondent or not

Then he checks the cheque from computer for further verification. Here the following information is checked:

- Whether there is sufficient balance or not

- Whether there is stop payment instruction or not

- Whether there is any legal obstruction (Garnishee Order) or not

After checking everything, if all are in order the cash officer gives amount to the holder and records in the paid register.

Transfer& clearing

TRANSFER

Transfer is not a critical sector in banking but it is very important. Transfers play a vital role in banking sector. So, basically transfer is a type of register maintaining matter. In this register officer write down every day transactions in Debit and Credit side then the officer calculate both the side of the register if both side shown same amount, it means that the total day’s transaction is completely okay.

CLEARING

Clearing is one of the magical parts of banking. Every bank has an officer of clearinghouse who is work with Bangladesh Bank clearing house. Actually most of major client deposit their account in different kinds of bank cheques. Clearing officer check all the cheques and deposit slip very carefully and then he received the cheque. After that, the clearing officer gives posting all the cheques in computer software, which is recognized through Bangladesh bank computer department. Then clearing officer seal all the cheques in advance date after that the officer endorsement all the cheques and sign all the cheques. All the cheques are posted in the computer by branch wise, then officer print the entire document and staple all the cheques by branch wise this is called schedule of clearing house. It is a very difficult job to staple all the cheques, because some time’s the cheques are huge in quantity, it may be 250 to 400, this is very vital job because every cheque must have to staple very carefully, it means cheque amount and the print sheet amount and cheque branch must have to be same. If the cheques staple in wrong direction, the cheque may be return from another bank, that’s why MTBL not to be able to credited party account.

Then the clearinghouse officer copies the entire document in two floppy disk as per Bangladesh Bank requirement. When the clearing officers enter the clearinghouse, his first job is that the floppy delivered to the Bangladesh Bank computer department. All of the procedure the clearing in charge goes to the Bangladesh Bank clearing house before 10 am in the morning. The clearing officer checks all the bank’s cheque and he put all the cheques in bank wise, like as this another bank’s delivered their cheques in MTBL desk.

Foreign trade

MTB provides a wide range of banking services to all types of commercial concerns such as Import & Export Finance and Services, Investment Advice, Foreign Remittance and other specialized services as required. Although we are a private commercial Bank, they have a strong global network that helps them to undertake international trade smoothly and efficiently

Import Business

Mutual Trust Bank supports its customers by providing facilities throughout the import process to ensure smooth running of their business. The facilities are:

a. Import Letter of Credit

b. Post Import Financing (LIM, LTR etc)

c. Import collection services & Shipping Guarantees

Export Business

Mutual Trust Bank offers extra cover to its customers for the entire export process to speed up Receipt Of proceeds. The Facilities are:

a. Export Letters of Credit advising

b. Pre-shipment Export Financing

c. Export documents negotiation

d. Letters of Credit confirmation

MTBL nine branches are their authorized dealers

Loan and Advance

Consumer Loan Scheme:

In order to make a significant contribution in the living standards of the people of medium and low-income category, Mutual Trust Bank has introduced a scheme called “Consumer Loan Scheme”. With a view to materialize the dreams of those who are unable to make one time investment from their own savings, one can now afford to buy necessary household equipments and thus improve the standard of living.

All sorts of household durables like- Television, Refrigerators, Computers, Air Conditioners, Video Cameras, Washing/ Drying Machines and Furnitures are allowed under this scheme. One can buy Motorcycle too under this programme.

The collateral security is minimum and the interest rates are one of the lowest in the market.

Small Business Loan scheme

With the objective of extending financial support to small businessmen, this loan scheme has been introduced. It has been designed to get business loans on easy terms and without any hassle. Only the genuine businessmen having entrepreneurship quality and honesty, to run and expand their business smoothly. Maximum loan under the scheme will be up to Tk. 50 lac. No collateral security is required up to Tk. 5 lac. Collateral security is required for loan above 5 lac.

Home Loan Scheme

Home Loan Scheme has been introduced to facilitate people to fulfill their dream of a home of their own. It has been designed o help people to get home loans on easy terms and without any hassle. Loan amount under this scheme is maximum Tk. 50 lac. Salaried executives, professionals, businessmen and govt. officials are eligible to avail this loan scheme. The loan is to be repaid by monthly equal installments including interest within the period ranging from 5 years to 15 years depending on the size of loan.

Home Repair/ Renovation Loan Scheme

Home Repair/ Renovation Loan Scheme has been designed with a view to help the owners of house/ building/ flat to mitigate their financial need for repair/ renovation of their house/ building/ flat. Only the genuine residential house owners will be eligible to avail the loan facilities to repair or renovate their own house/ building/ flats according to their needs. Maximum loan under the scheme will be up to Tk. 5.00 lac commiserating the monthly income. The loan is to be repaid by monthly equal installments including interest within maximum 60 Months.

Auto Loan Scheme

To own a car is everyone’s dream as well as a part of todays living, which enhances standard and quality of life. Auto Loan scheme has been designed to help materialize your long cherished dream of a car of your own. Purchase of new/-reconditioned cars is allowed under this scheme. Salaried executives, professionals, businessmen, govt. officials or self-employed persons are eligible to avail this loan. Loan amount under this scheme is 70% of car value but maximum of Tk. 20 lac.

Correspondence banking

The objective of our correspondent banking operations is to strengthen our existing relationships with foreign banks and financial institutions around the globe as well as exploring new relationships. In addition to that, we provide assistance in marketing the products of the correspondent banks. At present MTB is maintaining relationships with 30 (thirty) foreign correspondents and the number is growing everyday. Currently the bank has 18 (eighteen) NOSTRO A/Cs with large foreign banks abroad. The bank is a “SWIFT” member and its Bank Identification Number or BIC is ‘MTBL BDD

List of Major Foreign Correspondent Banks:

|

List of Nostro Accounts (SSI)

|

Vertical/ Common size Analysis

Vertical/Common size statements came from the problems in comparing the financial statements of firms that differ in size. In the balance sheet, for example, the assets as well as the liabilities and equity are each expressed as a 100% and each item in these categories is expressed as a percentage of the respective totals. In the common size income statement, turnover is expressed as 100% and every item in the income statement is expressed as a percentage of turnover (sales). Here bank has no sales so that I have considered the operating as 100%.

Balance sheet As on December 31, 2006 & 2005 | Common size Balance sheet | |||

Particulars | 2006 | 2005 | 2006 | 2005 |

Property and assets Cash: Cash in hand Balance with Bangladesh bank& agent bank |

233,425,245 1,413,425,408 |

147,594,334 841,125,960 |

0.90% 5.38% |

0.72% 4.35% |

| 1,646,850,653 | 988,720,294 | 6.28% | 5.12% |

Balance with other banks & financial Institutions: In Bangladesh Outside Bangladesh

|

783,960,394 175,569,497 |

255,207,335 165,359,702 |

2.99% 0.66%

|

1.32% 0.85% |

| 959,529,891 | 420,567,037 | 3.65% | 2.17% |

Money at call and short notice | 970,000,000 | 130,000,000 | 3.69% | 0.67% |

Investments: Government Others |

2,990,909,400 64,778,000 |

2,370,760,000 125,220,000 |

11.40% 0.25% |

12.28% 0.64% |

| 3,055,687,400 | 2,495,980,000 | 11.65% | 12.92% |

Loan and advance: Loans, cash credit, overdrafts Bills purchase and discounts

|

16,356,416,377 2,235,104,254 |

12,207,542,738 2,165,713,795 |

62.38% 8.52% |

63.22% 11.21% |

| 18,591,520,631 | 14,373,256,533 | 70.91% | 74.44% |

Fixed assets including premises, furniture & fixture Other assets |

276,186,202 718,210,820 |

236,559,678 661,907,204 |

1.05% 2.78% |

1.22% 3.42% |

Total property and assets | 26,217,985,597 | 19,306,990,566 | 100% | 100%

|

Liabilities and Capital Deposits and other accounts: Current deposit & other accounts Bills payable Savings deposits Fixed deposits Deposits products |

2,804,119,941 196,727,245 1,439,402,890 16,519,124,214 1,304,671,699

|

1,973,668,293 179,504,030 914,722,524 12,119,174,327 911,472,249 |

10.69% 0.75% 5.49% 63.00% 4.98% |

10.22% 0.92% 4.73% 62.77% 4.72% |

| 22,264,045,989 | 16,098,541,423 | 84.92% | 83.38% |

Other Liabilities | 2,049,135,387 | 1,660,964,321 | 7.81% | 8.60% |

Total liabilities | 24,313,181,376 | 17,759,505,744 | 92.73% | 91.98% |

Capital/ shareholders equity: Paid up capital Share premium Statutory reserve General reserve Retained earnings |

950,400,000 100,000,000 511,124,778 39,894,467 303,384,976 |

864,000,000 100,000,000 336,230,355 35,949,091 211,305,448 |

3.63% 0.39% 1.94% 0.15% 1.15% |

4.47% 0.39% 1.74% 0.18% 1.09% |

Total stockholder’s equity | 1,904,804,221 | 1,547,484,822 | 7.27% | 8.01% |

Total liabilities and stockholder’s equity | 26,217,985,597 | 19,306,990,566 | 100% | 100% |

From the vertical analysis above, we can compare the percentage mark-up of asset items and how they have been financed. The strategies may include increase/decrease the holding of certain assets. The analyst may as well observe the trend of the increase in the assets and liabilities over several years. It can be observed that there is an increase in the holding of the current assets of the company. The management can seek the reasons of why the holding of these assets is continuously increasing. Though both the assets and liabilities are increasing but proportionately liabilities were a little higher than the assets, which may make some ratio lower. The above analysis also shows that total liabilities has increase but stock holder’s equity has decreased, which indicates that MTBL is more debt financed than the equity.

Profit and Loss Account For the year ended December 31, 2006 & 2005 | Common size Profit and Loss Account | |||

Particulars | 2006 | 2005 | 2006 | 2005 |

Net Interest Income | 632,333,889 | 430,173,317 | 49.21% | 49.04% |

Income from investments Commission, exchange & brokerage Other operating income | 184,398,535 401,448,414 66,684,925 | 139,970,967 271,401,289 35,467,093 | 14.35% 31.35% 5.20% | 15.96% 30.95% 4.05% |

| 652,532,874 | 446,839,349 | 50.79% | 50.96% |

Total operation income | 1,284,865,759 | 877,012,666 | 100% | 100% |

Less: Operating expenditure Salary & allowances Managing director’s remuneration Director’s fees Rent, tax, insurance, electricity Legal expenses Postage, stamps, telegram& telephone Audit fee Printing, stationary, advertising Depreciation on & repairs to banks property Other expenditure |

158,532,358 2,400,000 425,000 40,192,847 525,393 12,665,039 60,000 13,126,422 28,336,491

59,129,548 |

102,675,527 2,400,000 382,500 28,974,686 205,010 8,739,014 40,000 14,369,739 21,822,952

45,556,988 |

12.34% 0.18% 0.03% 3.12% 0.42% 0.98% 0.004% 1.02% 2.20%

4.60% |

11.70% 0.27% 0.04% 3.30% 0.02% 0.99% 0.004% 1.63% 2.48%

5.19% |

Total operating expenditure | 315,393,644 | 225,166,416 | 24.54% | 25.67% |

Profit Before provision | 969,472,115 | 651,846,250 | 75.46% | 74.33% |

Less: Provision against loans & advances | 95,000,000 | 275,000,000 | 7.39% | 3.135 |

Profit before Tax | 874,472,115 | 624,346,250 | 68.07% | 71.20% |

Less: Provision for tax current Deferred | 393,512,452 2,680,264 | 287,578,298 593,254 | 30.62% 0.21% | 32.79% 0.06% |

| 396,192,716 | 288,171,552 | 30.83% | 32.85% |

Net profit after tax | 487,279,399 | 336,174,698 | 37.24% | 38.35% |

Add: Retained surplus, brought forward | 211, 305,448 | 157,304,137 | 16.45% | 17.93% |

| 689,584,847 | 493,478,835 | 53.69% | 56.28% |

A second method of common size analysis is a means of comparing figures within a single P & L. A common size profit and loss statement, for example, compares all components of the P & L to total operating income. In other words, Total operating income is defined as “100%” and all other figures on the statement are expressed as a percentage of that. In this way, we not only get an automatic indication of approximate profit margin, we also can see the importance of all of your costs and expenses relative to operating income. Vertical analysis can also be done on these common size percentages in order to identify trends in the relative sizes of categories like costs, expenses, or margins. The above analysis shows that MTBL has higher net interest income than 2005 to 2006. But after tax net profit has decreased because they paid more provision against loan and advances. On the other hand they paid lower tax in 2006. In the year 2006 MTBL has comparatively higher expenditure, but marginally lower percentage, which was not good signal for the bank.

Horizontal/ Trend Analysis

It is conducted by setting consecutive balance sheet, income statement or statement of cash flow side-by-side and reviewing changes in individual categories on a year-to-year or multiyear basis. The most important item revealed by comparative financial statement analysis is trend. # Percentage change= (recent year-previous year)/previous year

MTBL performance for 2006 compared to 2005 & 2005 compared to 2004

ITEMS (Figure in million) | 2006 | % | 2005 | % | 2004 |

Paid up Capital | 950.40 | 9.95% | 864.00 | 2.00% | 720.00 |

Shareholder’s equity | 1,904.80 | 23.09% | 1,547.48 | 27.09% | 1,217.55 |

Total Capital | 2,114.53 | 24.93% | 1,692.52 | 26.77% | 1,335.08 |

Total Assets | 26,217.99 | 35.79% | 19,306.99 | 21.19% | 15,931.03 |

Total Deposits | 22,264.05 | 38.29% | 16,098.54 | 22.29% | 13,164.13 |

Total Loans and Advances | 18,591.52 | 29.34% | 14.373.26 | 22.92% | 11,692.97 |

Total Investments | 3,055.69 | 22.42% | 2,495.98 | 48.90% | 1,676.21 |

Export | 12,943.29 | 46.91% | 8,810.00 | 48.71% | 5924.00 |

Import | 26,255.29 | 48.67% | 17,660.00 | 1.75% | 17,355.90 |

Total Contingent liabilities | 9,671.39 | 28.98% | 7,498.27 | 36.96% | 5,474.58 |

Operating Income | 1,284,86 | 46.50% | 877.01 | 27.84% | 686.00 |

Operating Expenditure | 315.39 | 40.06% | 225.17 | 25.75% | 179.06 |

Profit before provision and tax | 969.47 | 32.76% | 651.85 | 28.58% | 506.94 |

Net profit after provision and tax | 478.28 | 42.27% | 336.17 | 35.99% | 274.19 |

Total provision maintained | 239.98 | 65.50% | 145.00 | 23.40% | 117.50 |

Earning Assets | 23,575.83 | 35.34% | 17,419.05 | 17.86% | 14,779.16 |

Non- interest Earning Assets | 2,642.16 | 39.94% | 1887.94 | 63.90% | 1,151.87 |

A comparison of statements over several years reveals direction, speed and extent of a trend(s). The horizontal financial statements analysis is done by restating amount of each item or group of items as a percentage. Such percentages are calculated by selecting a base year and assign a weight of 100 to the amount of each item in the base year statement. Thereafter, the amounts of similar items or groups of items in prior or subsequent financial statements are expressed as a percentage of the base year amount. The resulting figures are called index numbers or trend ratios. The above analysis shows that MTBL performance trend is quite better in 2006, but somewhere it was not good. Their import was too higher, which is not good. Their capital was higher in 2006 but stockholders equity has decreased. As compared 2005 though their asset and deposit was higher but they had very low investment as well as MTBL was highly debt financed.

Ratio Analysis

Financial ratios are useful indicators of a firm’s performance and financial situation. Financial ratios can be used to analyze trends and to compare the firm’s financials to those of other firms. Ratio Analysis enables the business owner/manager to spot trends in a business and to compare its performance and condition with the average performance of similar businesses in the same industry. Financial ratios can be classified according to the information they provide. The following types of ratios frequently are used:

- Liquidity ratios

- Debt management ratios

- Profitability ratios

- Market value ratios

- Dividend policy ratios

1. Liquidity ratio

Liquidity ratios are the first ones to come in the picture. These ratios actually show the relationship of a firm’s cash and other current assets to its current liabilities. Two ratios are discussed under Liquidity ratios. They are:

Current ratio: This ratio indicates the extent to which current liabilities are covered by those assets expected to be converted to cash in the near future. Current assets normally include cash, marketable securities, accounts receivables, and inventories. Current liabilities consist of accounts payable, short-term notes payable, current maturities of long-term debt, accrued taxes, and other accrued expenses.

Current Ratio=Current Assets/Current Liabilities

| Year | 2006 | 2005 |

| Current ratio | 0.83 | 0.89 |

From the analysis, we can see that in 2005 the current assets were 0.89 times than the current liabilities that has not fluctuated much through out these years. A minimal decrease is seen in 2006.The reason for such stability can be there not investing remarkably on assets and not making any huge financing from outside. If we take a closer look on the balance sheet, this assumption gets a more realistic touch. Year by year assets have gone slightly up and the liabilities as well, but proportionately liabilities were a littler higher than the assets, which actually reflected as a marginal decrease in the ratio.

Quick ratio: This ratio indicates the firm’s liquidity position as well. It actually refers to the extent to which current liabilities are covered by those assets except inventories.

Quick Ratio= (Current Assets-Inventories)/Current Liabilities

Year | 2006 | 2005 |

Quick ratio | 0.07 | 0.06 |

This ratio portray the idea that MTBL has so far an almost constant liquidity position which is good at some point, but at the same token it can be said that they have not been able to improve them-selves. Standing at this point, we can make an assumption that may be their profit margin was not so high that they can make some investments paying off the liabilities that could result in an increase in assets and decrease in liabilities to make the liquidity position far better.

2. Debt management ratios

Debt management ratios reveal 1) the extent to which the firm is financed with debt and 2) its likelihood of defaulting on its debt obligations. These ratios include:

Debt to equity ratio: This ratio indicates how much the company is leveraged (in debt) by comparing what is owed to what is owned. A high debt to equity ratio could indicate that the company may be over-leveraged, and should look for ways to reduce its debt.

Debt to equity ratio = Total Debt / Total equity

Year | 2006 | 2005 |

Debt to equity ratio | 12.76% | 11.47% |

Equity and debt are two key figures on a financial statement, and lenders or investors often use the relationship of these two figures to evaluate risk. The ratio of the business’ equity to its long-term debt provides a window into how strong its finances are. Equity will include goods and property the business owns, plus any claims it has against other entities. Debts will include both current and long-term liabilities. The above analysis shows that MTBL has a strong finance.

Times-Interest-Earned (TIE) ratio: This ratio measures the extent to which operating income can decline before the firm is unable to meet its annual interest cost.

TIE ratio = EBIT / Interest Charges

Year | 2006 | 2005 |

TIE ratio | 11.30 times | 14.92 times |

We can see from this ratio analysis that, this company has covered their interest expenses 11 times in 2006, 14 times in 2005. It means they have performed pretty low in 2006. As in 2005 they issued a little high number of long-term loans and does not have good liquidity position, their EBIT became high thus making TIE a little high as well.

3. Profitability ratios

Profitability is the net result of a number of policies and decisions. Profitability ratios show the combined effects of liquidity, asset management and debt on operating results.

This ratio includes:

Return on Asset: This number tells how effective the business has been at putting its assets to work. The ROA is a test of capital utilization – how much profit (before interest and income tax) a business earned on the total capital used to make that profit. This ratio is most useful when compared with the interest rate paid on the company’s debt. For example, if the ROA is 15 percent and the interest rate paid on its debt was 10 percent, the business’s profit is 5 percentage points more than it paid in interest.

Return on Total Assets (ROA) = Net income available to total common shareholders / Total assets

Year | 2006 | 2005 |

ROA ratio | 1.82 % | 1.74 % |

Return on assets is an indicator of how profitable a company is. Use this ratio annually to compare the business’ performance to its norms. So, return on total assets increased gradually throughout the years. This may have occurred because MTBL did not used more debt financing in 2006 compared to 2005, which resulted in less Interest cost and brought the net income up.

Return on Equity: Return on Equity measures the amount of Net Income earned by utilizing each dollar of Total common equity. It is the most important of the “Bottom line” ratio. By this, we can find out how much the shareholders are going to get for their shares.

Return on Equity (ROE) = Net income available to common shareholders / Total common equity

Year | 2006 | 2005 |

ROE ratio | 25.11 % | 22.00 % |

The Return on Equity increased in 2006 than 2005. This again may have happened due to the issue of more long-term debt in 2005.

4. Market value ratios

The market value ratio relates the firm’s stock price to its earnings and book value per share. These ratios give management an indication of what investors think of the company’s past performance and future prospects. It includes:

Price/ Earnings ratio: The Price/ Earnings ratio (price-to-earnings ratio) of a stock is a measure of the price paid for a share relative to the income or profit earned by the firm per share.

P/E ratio – Price per share / earnings per share

Year | 2006 | 2005 |

| Price/ Earning ratio

| 6.80 times | 11.35 times |

The P/E ratio was 11.35 times in 2005 and decreased further to as low as 6.80 times in the next year, which is an alarming signal for the potential investors. The main reason behind the declination of P/E ratio is the fall of price per share. Price of share may fall for several reasons. Failing to meet market expectations is one of the main reasons for the market to lose interest in a share.

Market/ Book ratio: The ratio of book value to market value of stocks.

Market/Book ratio (M/B) = Market price per share / Book value per share

Year | 2006 | 2005 |

| Market/book ratio | 0.24 times | 0.27 times |

The M/B ratio was 0.27 times in 2005 and decreased further to 0.24 times in the following year, which was not as excellent as to draw the attention of investors.

5. Dividend Policy Ratios

It describes how a firm pays their dividend as they earn. On the other hand it also shows that a firm may earn and provide the dividend to its shareholders.

Dividend payout ratio: it is equals the percentage of earnings paid out as individuals.

Dividend payout=Dividend/Net income

Year | 2006 | 2005 |

| Dividend payout ratio

| 0.17 times | 0.00 times |

Generally, growth firms have low dividend payout ratios as they retain most of their income to finance future expansion. Here MTBL has a high pay out ratios, which indicates that it is a well-established bank.

Dividend yield: It indicates how much a firm earn dividend per share to give it to their shareholders.

Dividend yield =DPS/Market value per share

Year | 2006 | 2005 |

| Dividend Yield ratio | 0.80 times | 0.50 times |

From the above analysis we can see that, MTBL has a higher dividend yield ration, which indicates that they are earning more that will be paid to its shareholders.

SWOT Analysis

Strengths

- MTBL has a strong Human resource

- MTBL has a wide coverage all over the country

- MTBL has widest product suits, which includes—various deposit, saving scheme, various loan etc.

- Experienced and well organized top and mid level management

- Improvements in the performance in the recent years

Weaknesses

- Lesser degree of flexibility in sales and service in compared to competition

- HR policy not attractive enough to attract meritorious entries

- Some Officers are not well trained

- In MTBL there is lower marketing and promotional activities

- MTBL has no own ATM booth

Opportunities

- MTBL can Introduce more consumer banking products including credit cards

- MTBL can provide service to all level of consumers through its branch network

- MTBL can do Credit financing through its broad branch network

Threats

- Envisaged currency devaluation and shortcomings in foreign currency availability may impact on foreign currency exposure of the bank

- Excessive competition from other private & government banks, use of modern concepts and technologies in banking by competitors

Modern Commercial Banking is exacting business. The reward are modest, the penalties for bad looking are enormous. And Commercial banks are great monetary institutions, important to the general welfare of the economy more than any other financial institution. It has a vastly sobering and exacting responsibility. Mutual Trust Bank Ltd. (MTBL) playing a vital role in financing the people of the country. Without Bank’s co-operation, it is not possible to run any business or production activity in this age. So, The Mutual Trust Bank Limited (MTBL) has to clearly justify the customers from a neutral point and gather the current information about the market.

MTBL is regarded as a very reliable bank and the growing number of its customers indicates its increasing acceptance among clients. Since MTBL has been able to rapidly increase the total number of Account-holders, it now should focus the on the level of customer satisfaction. This is extremely important if MTBL wants to prevent loss of customers to numerous competing banks.

From the total analysis, we can summarize that Mutual Trust Bank Ltd. has been doing pretty good through out the years. It is true that last year there return did decline but it is still pretty much satisfactory. Therefore, I can conclude that, MTBL is a good enough company to invest on. One thing definitely worth mentioning is that all customers were highly satisfied at the attitude and product presentation and selling skills of all the officer of MTBL. This is a very good sign that all are very carefully trained. Since selling requires huge amounts of interpersonal skills, the responses of the customers show that MTBL has a competitive in terms of persuading the customers.

a. MTBL can modify product features so that customer can easily get whatever they need

- Some officers are not trained properly, which may become the cause of losing customer. So they need to train the officer efficiently

- Consumer is easily convinced when they will know the bank. To reach the customer bank need to do more advertising, where MTBL is a bit week. So MTBL should increase their marketing and advertising policy

- If a perfect and hard working officer is recruited then bank may be able to proceed quickly. For that MTBL need to be more realistic on HR policy

- To earn more profit it is necessary to the entire customer over the country. So MTBL can introduce more branch to cover all over the country

- MTBL customer sometimes feels uneasy to use other bank booth. To keep the customer MTBL need to introduce own ATM booth