PART THREE

BRANCH BANKING AND OPERATION OF DHAKA BANK

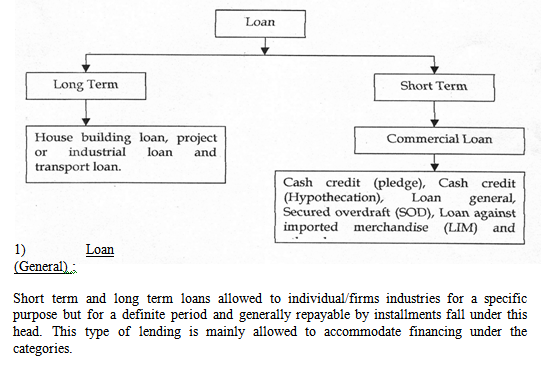

ADVANCE BANKING:

Advance banking is one of the significant schemes of the Dhaka Bank Limited. It contributes a huge portion in the Dhaka Bank’s total revenue. It provides different types of loans to its borrowers as a lender. The bank operates advance facilities through different branches but the entire loan sanction procedure is controlled and monitored by the Head Office.

Cet1ain terms and conditions are followed when the loan is sanctioned to the borrower. Now advance banking is discussed in detail.

Credit Policy:

Dhaka Bank is a new generation bank. It is committed to provide high quality financial services/products to contribute to the growth of G .D.P of the country through stimulating trade & commerce, accelerating the pace of industrialization, boosting export, creating employment opportunity for the educated youth, poverty alleviation, raising standard of living of limited income group and overall sustainable growth in the socioeconomic development of the country.

To achieve the aforesaid objectives of the bank credit operation of the bank is of paramount importance as the greatest share of total revenue of the Bank is generated from it, maximum risk

is centered in it and even the very episteme of the Bank depends on the prudent management of its credit port-folio. The failure of a commercial bank is usually associated with the problem in credit port-folio and is less often the result of shrinkage in the value of other assets. As such, credit portfolio not only features dominantly in the assets but also to the structure of the Bank.

To provide broad guideline for the credit operation towards achieving the objectives of the bank, for efficient and profitable deployment of its mobilized resources and to administer the credit portfolio in the most efficient way, a clearly defined, well planned, comprehensive and appropriate credit policy and control guidelines of the bank is a prerequisite.

In view of the above, this credit policy and guidelines of the bank has been prepared subject to amendment, revision, re-adjustment and refinement as and when required by the bank.

The purpose of this policy statement, which replaces all previous ones, is to set out the credit policies of the Board of Directors.

The policies are described as under:

Credit principles.

Global Credit Portfolio Limits.

Types of Credit Activities.

Credit Administration.

Credit Principle:

The following are the principles to be adopted for lending authority, approval, monitoring and control on the basis consistent with the global operational objectives and business strategies of the bank.

General:

The bank will provide suitable credit services and products for the markets in which it operates.

Loans and advances shall normally be financed from customers’ deposits and not out of temporary funds or borrowing from other banks. Credit will be allowed in a manner, which will in no way compromise the Bank’s standards of excellence and to customer who will complement such standards.

All credit extension must comply with the requirements of the Bank’s Memorandum & Articles of Association, Banking Companies Act 1991 as amended from time to time, Bangladesh Bank instructions and other applicable rules and regulations.

Structural:

The authority structure for extension of credit should enable effective adaptation to changes in the economic, technological, regulatory and competitive environment within which the bank operates.

Performance:

The conduct and administration of the loan portfolio should contribute, within defined risk limitation, to bank’s achievement of portfolio growth and superior return on the bank’s capital.

Credit advancement shall focus on the development and enhancement of customer relationship and shall be measured on the basis of the total yield for each relationship with a customer (on a global basis), through individual transactions should also be profitable.

Credit facilities will be extended to those companies/persons, which can make best use of them, thus helping to maximize our profits as well as leading economic growth of the country. To ensure achievement of this objective it will base its lending decision mainly on the borrower’s ability to repay.

Loan Pricing :

Interest on various lending categories will depend on the level of risk and type of security offered. It should be kept in mind that rate of interest is the reflection of risk in the transaction. The higher the risk, the higher the interest rate.

Interest may be reviewed at least once in 6 (six) months and more often when appropriate. Fixed interest rate should be discouraged; preferably all rates should vary with cost of funds fluctuation based on a spread for profit.

Effective yield can be enhanced to the extent borrowers are required to maintain deposits to support borrowing activities. Commitment fee and service charges should further improve yield where possible. All pricing of loans should however have relevance with market condition and be approved by the Executive Committee/Managing Director from time to time.

Administration/Monitoring:

The administration of the loan process shall ensure, compliance with all laws and regulations at both local and global levels including bank policy as set out in this document and the bank’s credit manual/circulars.

Proper analysis of credit proposal is complex and requires a high level of numerical as well as analytical ability and common sense. To ensure effective understanding of the concepts and thus common sense. To ensure effective understanding of the concepts and thus to make the overall credit portfolio of the bank healthy, proper staffing of the credit departments shall be done through placement of qualified officials who have got the right aptitude, formal training in finance, credit risk analysis, bank credit procedures as well as required experience.

Where repayment and interest servicing performance of a credit deteriorates it shall be identified at an early stage and closely monitored to avoid low losses.

Loans/Facilities where appropriate and related security shall be monitored and reviewed by a separate unit unconnected with the credit, approval process on a regular basis in order to assess the collection ability of the loan and effectiveness of the security. This unit will report to the Managing Director or his designated officer.

Exception of Loan Policy :

It is recognized that there will be exceptions to the state policy, which can be justified. However, the Board should approve these by the Executive Committee or/and the circumstances must be fully documented in the credit file.

Global Credit Portfolio Limits:

The nature of credit portfolio shall be governed within guidelines set down by the Head Office and regulatory requirements. These guidelines will however be consistent with the global limits identified below for the bank’s portfolio in aggregate. Criteria for exposure to customers are set as under:

Total Facilities:

The aggregate of all cash facilities shall not exceed 80% of the customer deposit. It is further governed by the statutory and liquidity reserve requirement of Bangladesh Bank.

Term facilities:

The aggregate loan term facilities shall not exceed 20% of the total credit portfolio. The facilities shall not be allowed for a period exceeding 5 years. Any exception will require the approval of Board of Directors.

Country/Cross Border Exposure:

Limits to be established by the Board for individual Country as well as for aggregate Bank Credit Exposures to different countries. These limits are to be reviewed from time to time with due regard to the political and economic environment in each country. The country exposure limits may be utilized up to maximum amounts for different maturities as follows:

For maturity up to one year: 100%

For maturity up to two years: Maximum 50 % of the limit.

For maturity up to three years: Maximum 25 % of the limit.

For maturity beyond three years: Maximum 10 % of the limit.

For exceptions, approval is required from the Board of Directors.

Exposure to Customer Groups:

Credit facilities in aggregate extended to anyone-customer group shall not normally exceed 15% of the capital fund or Tk. 10 (ten) crore whichever is lower. However, the Board of Directors may relax these limits in deserving cases. All proposals submitted to the Head Office will also be required to indicate the extent of the Bank’s global exposure to that customer group.

Sector-wise allocation:

Sector-wise allocation of credit shall be made annually with the approval of the Executive Committee Board of Directors. This will be reviewed from time to time.

Security :

Security is accepted against credit facilities but shall be properly valued and shall be affected in accordance with the laws of the country in which security is held. An appropriate margin of security will be taken to. reflect such factors as the disposal of costs or potential price movements of the underlying assets.

Types of Credit Activities:

Depending on the various nature of financing, all the lending activities have been brought under the following major heads:

a) Large and Medium Scale Industries.

b) Small and Cottage Industries. Very often term financing for agriculture and others

are also included here.

2. House Buildin2 Loan (General) :

Loans allowed to individual/enterprises, construction of house (residential or commercial) fall under this type of advance. The amount is repayable by monthly installment within a specified period, advances are known as Loan (HBL-GEN).

Introduction:

House Building loan is one of the common credit policies of banking sector. There was only one institution in our country, which is specified in HBFC, Bangladesh House Building Finance Corporation. Nowadays, besides this bank, many commercial banks and leasing companies provide house-building loans to the customers.

Interest rate:

Currently the interest rate is 16% but it may change from time to time depending on the market interest rate. From the customer’s point of view, these changes have an adverse impact on customers. Sometimes, if they have to bear a higher interest on the principal amount which causes a great burden on them.

But from the bank’s point of view, this is very good to maintain the markup. Because when the market interest rate rises by 1 %, than they are getting 1 % less markup. So for this clause of increasing interest rate, they can have the same markup by increasing the interest rate charging on the clients. So this is very effective for the bank to maintain markup.

Disbursement Procedure:

The disbursement procedure or timing of disbursement can be made in two or three stages or more depending on the above conditions.

Mode of repayment :

The loan shall be adjusted by monthly installment basis. The repayment will start from. 6 (six) months of the date of first disbursement (it may change according to the terms and conditions of the agreement).

Collateral:

The land and the construction on the land are normally given as collateral. It may change

The documents to be obtained:

a. DP note.

b. Letter of disbursement.

c. Letter of installment.

d. Letter of guarantee.

e. Letter of undertaking.

f. Letter of agreement.

g. Irrevocable general power of attorney.

h. Any other documents if considered.

House Building Loan (Staff)

Loans allowed to the Bank employees for purchase/construction of house shall be known as Staff Loan (HBFC-STAFF).

Other loan to Staff:

Loans allowed to employees other than for House Building shall be grouped under head Staff Loan (general).

Cash Credit (Hypo) :

Advances allowed to individual/firm for trading as w~1I as wholesale purpose or to industries to meet up the working capital requirements against hypothecation of goods as primary security fall under this type of lending. It is a continuous credit. It is allowed under the following categories.

“Commercial lending”- when the customer is other than an industry and “Working Capital” when the customer is an industry.

Cash credit (Pledge) :

Financial accommodations to individual/Firms for trading as well as wholesaler to in4ustries as working capital against Pledge of goods as primary security fall under this head of advance. It is also a continuous credit and like the above, allowed under the categories.

a) “Commercial Lending”

b) “Working Capital”

Hire-purchase:

Hire purchase is a type of installment credit under which the Hire-Purchaser agrees to take the goods on hire at a stated rental, which is inclusive of the repayment of principal as well as for adjustment of the loan within a specified period.

Lease Financing:

Lease financing is one of the most conventional sources of acquiring capital machinery and equipment whereby a client is given the opportunity to have an exclusive right to use an asset usually for an agreed period of time against payment of rent. It is a term financing repayable by installment.

Lease Finance of Dhaka Bank Ltd. :

Lease financing is a major financial instrument in the banking sector. As the Bank is a leading financial institution in the financial sector in our country, it is also involved in lease financing. But the procedure of lease financing is something different from the pure leasing companies. The procedure of the bank is called “Mixed Procedure of Lease Financing”. The bank at first started lease financing in conventional style in 1995 when it started its operation. After doing lease financing successfully for two consecutive years it switched to mixed mode of lease financing in 1997.

The bank generally provides vehicles and medical instruments. The vehicle class includes all the commercial vehicles like buses & trucks, cars and jeeps, prime movers, ship maker etc. The medical instruments are provided to the doctors and medical centers.

Interest Rate:

The interest of the bank is between 15% and 18%, depending on the party or clients. Mainly the interest rate changes subject to the amount of lease finance and the amount of collateral. Risk fluid provision and supervision cost is also charged to the clients. Here the interest rate is 2% in both cases.

Installments:

Lease rentals include the interest, risk fund, supervision cost etc. Normally there are 48 installments in a lease financing repayment.

Credit Scheme of Dhaka Bank ltd.

Introduction:

Consumer credit scheme is a major program of Dhaka Bank Ltd. In CCS the bank engages an agent who works on behalf of the bank. This agent performs all the work prior to the sanction of the CCS. They do the inspection and make all the documents necessary for CCS. For this purpose they get commission.

Clients:

The clients are service holders and businessmen. Service holders can be Government and Private enterprise employees. In case of government service holder, the client must be an officer in rank.

Products:

Electronic goods, cars, jeeps, microbuses, mobile telephone, T & T telephone, etc.

Interest Rate:

Interest rate is 16%. 2% risk fund, and 2% service charge.

Down payment :

Down payment is 20% of the CCS amount. It is considered as equity. The payment is 50% for vehicles.

Maturity and Loan Limit:

1-2 years for electronic goods. Here the limit is 1,00,000/=.3 years for vehicles. Here the limit is 3700,000/=.

The documents. which are demanded by the bank:

Two letters of guarantee.

Bank statements; the assets and liabilities of client

Assurance letter from the organization where he is currently working. Trade license for the businessman or Article of Association.

Non-J udicial stamp amounting to Tk. 300/=

Penalties:

2% penal interest is charged in the residual amount.

Recovery rate:

Recovery rate is 93%.

It is a special credit scheme of the finance purchase of consumers’ durables to the fixed income group to raise their standard of living. The customers are allowed the loans on soft terms against personal guarantee and deposit of specified percentage of equity. The loan is repayable by monthly installment within a fixed period.

SOD (Secured Overdraft) (General) :

Advances allowed to individual/firms against financial obligation (i.e. lien on FDRlPSP/BSP/ insurance policy/share etc.). This mayor may not be a continuous credit.

SOD (Secured Overdraft) (Others) :

Advances allowed against the assignment of work order or execution of contractual works falls under this head. This advance is generally allowed for a definite period and specific purpose ie. it is not a continuous credit. It falls under the category “others”.

SOD (Secured Overdraft) (Export) :

Advance allowed for purchasing foreign currency for payment against L/Cs (Back to Back) where the exports do not materialize before the date of import payment. This is also an advance for temporary period, which is known as export finance and under the category “Commercial Lending”.

PAD (Pavment ae:ainst documents) :

Payment made by bank against lodgment of shipping documents of goods imported through L/C falls under this head. It is an interim advance connected with import and is generally liquidated against payments usually made by the party for retirement of the documents for release of imported goods from the customer’s authority. It falls under the category “Commercial Bank”.

LIM (Loan against imported merchandise) :

Advance allowed for retirement of shipping documents and release of goods imported through L/C taking effective control over the goods by pledge in godowns under bank’s lock and key fall under this type of advance. This is also a temporary advance connected with import, which is known as post-import financing and falls under the category “Commercial Lending”.

L TR (Loan against trust receipt) :

Advance allowed for retirement of shipping documents and release of goods imported through L/C falls under trust with arrangement that sale proceeds should be deposited to liquidate the advances within a given period. This is also a temporary advance connected with import and known as post-import finance and falls under the category of “Commercial Banking”.

IBP (Inland bill purchased) :

Payment made through purchase of inland bills/cheque to meet urgent requirement of the customer falls under this type of credit facility. This temporary advance is adjustable from the proceeds of bill/cheque purchased for collection. It falls under the category “Commercial Lending”.

Export Cash Credit (ECC) :

Financial accommodation allowed to a customer for export of goods falls under this head and is categorized as “Export Credit”. The advances must be liquidated out of export proceeds within 180 days.

Packing: Credit (P.C.) :

Advance allowed to customer against specified LIC/Fine contract for processing/Packing of goods to be exported falls under this head and is categorized as “Packing Credit. “

The advances must be adjusted from proceeds of the relevant exports within 180 days. It falls under the category “Export Credit”.

FDBP (Forei2n documentary bill purchased) (Forei2n) :

Payment made to a customer through purchase/negotiation of a foreign documentary bills falls under this head. This temporary advance is adjustable from the proceeds of the shipping/export documents. It falls under the category “Export Credit”.

FDBP (Forei2n documentary bill purchased) (Local) :

Payment made against documents representing sales of goods, industries which are deemed as exports, and which is Currency/Foreign Currency falls under this head. This temporary liability is adjustable from proceeds of the bills.

FBP (Forei2n bill purchase) :

Payment made to a customer through purchase of Foreign Currency Cheques/Drafts falls under this head. This temporary advance is adjustable from the proceeds of the cheque/draft.

LDBP:

Payment made to a customer through purchase of inland documentary bills. This temporary liability is adjustable from proceeds of the bill.

Credit Administration:

The principal elements of bank credit administration are as follows:

A. Credit Approval.

B. Credit file maintenance.

C. Facility evidence maintenance. D. Credit monitoring and review.

Credit Approval:

The primary factor determining the quality of the bank’s credit portfolio is the ability of each borrower to honor, on a timely basis, all credit commitments made to the bank. The authorizing credit personnel prior to credit approval must accurately determine this.

The credit approval process shall be governed by the Bank Credit Policy framework, which can be summarized under the following:

1) Credit Evaluation Principles:

To have the optimum returns from the deployed funds in different kinds of lending, more emphasis shall be given on refund of loans and advances out of funds generated by the borrowers from their business activities (Cash Flow) in realization of money by disposing of the securities held against the advance which is very much uncertain and time consuming.

Accordingly the credit evaluation principles must be adhered to at every level of approval. The lending risk analysis of both the business risk and security risk provides overall ratings of risk in a particular to in under the following lending process:

· Assess risk of failure to repay.

· Decide whether to accept or reject a loan proposal. . Set price and terms.

· Obtain sanctioning documents and disburse loan.

· Monitor performance and ensure repayment/recovery.

The most significant part of the process is assessment of risk of failure to repay which deals with the overall lending risk combining the business risk and the security risk in a matrix derived out of six segments of the Business risk, viz.

Suppliers Risk

Sales Risk

Performance Risk

Resilience Risk

Management Competence Risk

Management Integrity Risk

The overall matrix provides four kinds of lending risks for decision-makers, viz.

Good

Accepted o Marginal and

Poor which are detailed in the Lending having an overall risk as “managerial” and

“poor” without proper justifications except for renewal of existing facilities under compelling circumstances or for other reason such as salvage, which shall also contain convenient future improvement of the position. All credit applications rated “Poor” shall require approval of the Board regardless of purpose, tenure or amount.

Credit Risk Evaluation/Assessment:

The importance of detailed and complete credit risk assessment for each facility and customer relationship cannot be over emphasized. The steps that should be followed in carrying out such an assessment are set out in the bank credit manual and the Head Office circulars issued from time to time. All proposals of credit facilities must be supported by a complete analysis of the proposed credit. A comprehensive and accurate appraisal of risk in every credit exposure of the bank is mandatory. No proposal can be put up for approval unless there has been a complete written analysis. It is the absolute responsibility of the proposal officer to ensure that all necessary proposal documentation is collected before the facility request is sent to the sanctioning officer.

Lending Authority :

Assure proper and orderly conduct of the business of the bank, the Board of Directors will empower the Managing Director and other Executives of the bank to lend upto certain amount under certain conditions at their discretion. The lending officer is broadly categorized as follows:

Managing Director.

Deputy Managing Director.

Executive Vice President

Senior Vice President.

Vice President.

Senior Asstt. Vice President.

Asstt. Vice President.

The amount and scope of each officer’s lending authority is a function of the amount only on the basis of his position. In other words, an officer does not automatically get lending authority by virtue of his corporate and/or functional title. Specified lending authority will be delegated by the Managing Director to various Executives after taking into consideration his proven credit judgment, knowledge and experience. The amount of lending authority approved by the Board for various Executives forms the upper limit of the authority that may be delegated to an officer holding corporate title. Each individual’s lending authority will be delegated to him in writing. Authorities given to an incumbent will not automatically be transferred to a replacement. The letter will have lending authorities delegated to him in writing and amount delegated will depend upon the individual.

The Managing Director with the Executive Committee/ Board will review all lending authorities periodically.

Approval under Dual Si2:nature :

All approval of credit facilities must be conveyed under dual signature, and ideally both the signatures must have the required lending authority. If however, two lending officers of the required lending authority are not available, one of the signatories must have the lending authority. .

The responsibility for the credit policy, procedure, approval & review shall vest amongst the following groups:

A) Board of Directors;

Establishing overall policies and procedures for approving & reviewing credits.

Delegating authority to approve and review credits.

Approving Credit for which authority is not delegated.

Approving all extensions of credit, which are contrary to bank’s written credit policies.

B) Executive Committee: Executive Committee of the Board shall be responsible for:

Approving credit facilities as delegated by the Board of Directors.

Supervising the implements of the Directives of the Board of

Directors.

Reviewing of each extension of credit approval by the Head Office

Credit Committee/Managing Director.

Keeping the Board of Directors informed covering all of the above.

C) Policy Committee:

Establishing Lending Policy.

Establishing policies & procedure for reviewing and analyzing extension of credit and loan portfolios.

DECLARA TION OF THE BORROWER (SPECIMEN)

I. Name:

2. Address:

3. Name of proprietor/partners/directors and his/her father’s name and present residential address.

4. Permanent address of the proprietor/partners/directors.

5. Date of establishment.

6. Nature of business.

7. Investment in the business or paid-up capital.

8. Movable and immovable properties (in detail) owned by the firm and/or company with valuation.

9. Movable and immovable properties'(in detail) owned by the proprietor/partners/directors with valuation.

10. Allied or subsidiary concerns, if any.

11. Their investment or paid-up capital in allied or subsidiary concern.

12. Purpose of borrowing.

13. Source of repayment.

14. Amount of income, Tax paid (last year).

15. Name of two references, either in service or in business, with full address.

16. Name of the previous banker.

17. Details of liability, if any, or with any other bank.

18. Brief history of the Proprietor/Managing partner/ Managing Director.

Latest Balance Sheet of the company or financial statement of the firm in duplicate is enclosed.

We, hereby confirm that the particulars given above are true and correct.

Signature of the Borrower Bank’s opinion:

Bank’s Opinion:

It is a well-established practice amongst banks to exchange opinion on customers confidentially. A request for a report on a customer other than from a bank should not be complied with. Information should only be supplied to another banker on his written request. It is, however, preferable to obtain the customer’s consent to send confidential reports on him to such bodies.

While giving credit reports, to another bank, it must be ensured that the report is carefully worded in general terms without details regarding balance or turnover of an account. It should be accurate, erring on the side of neither exaggeration nor under-estimation.

A banker is expected to do no more than give an honest answer on the basis of the facts known to him. It should embody the banker’s opinion on the general reputation and financial position of the party. Phrases like “maintains satisfactory accounts with us for the past so many years” are examples of reports in regard to general reputation of the customer.

The covering letter to the reply should be marked “confidential” and it should be expressly stated therein that the report of the bank, or any of its officers and on the condition that the reporting bank’s name will not be disclosed. The bank should not state units in its reply the worth of the customer as per its records but code words like “Small means”, “Moderate means”, “Fair means”, “Fairly good means”, “Good means”, “Large means”, and “Very large means” may be used while exchanging confidential reports with other banks regarding the means of the parties.

In case of a sole proprietorship, information will be given about the year the business was established, dealings with the bank and the proprietor’s means. If it is a partnership firm, particulars will be supplied about partners, their means, and experience, nature of business and their connections with the bank. In the case of a limited company, year of establishment, names of directors, capital structure, reserves, nature of business and company’s connections with the bank are given.

The bank which receives an opinion on a party from another bank should exercise care not to pass on the information to his customer and should not disclose the fact to him. The customer should be informed that it is confidential.

In reply to enquiries from the banker’s own branches, full information may be given regarding the constitution of the party, limit sanctioned, maximum, minimum and average balance in the account during the last 12 months, turnover in the account, experience of the branch in the conduct of the account, exact worth of the party, details of his business, names and places where the party has office and comments on his dealings. If the concern has any allied or connected business, relevant details should also be given.

Sometimes, foreign correspondents ask banks to send reports on their customers. In such cases, information should be supplied as much as may be possible but only in general terms. Thus, the reports to foreign banks generally embody more information than that contained in the reports to fellow bankers but a little less than that supplied to banker’s own branches.

Enquiries are often received from the Government or Semi-government institutions about customers who may have applied for being placed on the approval list as Government contractors. The information should be supplied in the same manner as to the bankers. It must be stated in the covering letter that the information is being given by the bank without any responsibility on the part of the bank or any of its officers and without any undertaking or guarantee, express or implied.

Capacity/Solvency Certificate etc. :

Customers sometimes approach banks to issue them capacity (or solvency) certificate while applying for import license to the Controller of Importers or similar other purpose. In this case, the bank may issue normal certificate in general terms quoting code words. Banks should also state in such certificate that the information is given by them without any responsibility on the part of the bank or any of its officers, etc.

Sometimes a certificate of turnover is required by customers for submission to Government departments. The bank has to state the particulars of the goods in which the customer deals and the approximate turnover of the customer’s account with the bank during previous year. Strict accuracy is needed when issuing such certificates. Too much reliance should not be placed on what the customer states or what is printed on his letterhead.

Analysis of Balance Sheet:

The first step in the analysis of balance sheet is the scrutiny and examination of different items of assets and liabilities and their classification into various categories. The left hand side of balance sheet displays capital and liabilities while the right hand side, property and assets.

1. Current Assets.

2. Cash in hand and bank balance.

3.Stock. .

4. Investment.

5.. Book Debts and Bills Receivable. 6. Fixed Assets.

Banker should, therefore, examine the following points while analyzing the fixed assets :

a) How the fixed assets are valued in Balance Sheet?

b) What is their current market value?

c) What is their forced sale value if put up for auction?

d) Date of purchase in relation to valuation and cost price according to current price level?

e) If imported, whether imported on cash licenses or under credit/grant on hire purchase system.

£) Whether sufficient depreciation has been provided or sufficient reserve has been created for the purpose?

g) Whether it is specialized machinery suitable for rare type of business activity.

VII) Land and Buildin2 :

It may be a factory, a farm, a hotel, a warehouse, office building, a block of houses etc. banker should ascertain their present realizable value. For this purpose, it is essential to know the type and situation of property and the manner in which the property is maintained in case emergency sale is necessary.

VIII) Plant and Machinery :

The age and type of machinery are important considerations. In the case of new machinery, suppliers usually erect it as a part of the bargain and guarantee its performance. In case the machinery is of a specialized nature, its marketability and value are greatly reduced. If the machinery is subject to hire purchase, the creditor is entitled to claim it back if stipulated installments are paid. It should be particularly investigated that no prior charge exists and reasonable depreciation is provided against these assets. It should be valued at cost price less depreciation.

IX) Furniture and Fixture:

Furniture and fixtures may not fetch much .price on a forced sale as they are usually of a specialized character and considerable expenses will be necessary before a prospective buyer can make use of them. These are to be valued at cost price less depreciation.

X) Tools:

Tools are valued similarly as machinery at cost price less depreciation.

XI) Intan2ible Assets:

Intangible assets, also called fictitious assets, do not represent any material asset or property. They are represented by either deferred revenue expenditure or expenditure which for the sake of prudence should not be taken to carry any value. They also include items, such as, Goodwill, Patents, Trade Marks, Designs, and Preliminary Expenses. Debit balance of profit and loss account, discount on shares or debentures etc. Intangible assets are non-physical and intangible in nature, but have quite a long period of usefulness to business.

LIABILITIES:

Liabilities of a business concern are broadly divided into two categories:

i) Current liabilities.

ii) Term liabilities. These are external liabilities.

Current Liabilities:

Current liabilities otherwise known as short-term liabilities include all liabilities which are payable quickly in a short term that is within a period of one year or less.

I) Borrowing: from banks:

These are usually in the nature of short-term credit. The banker should also know the term and conditions of the borrowings from other banks, viz., the amount, rate of interest, period of repayment and security charged are important points for the consideration of the lending banker.

II) Trade Creditors I Bills Payable:

The creditors should be well-spread; The banker should ascertain that the amount due to the trade creditors is not large., keeping in view the amount of purchases. These accounts should not be overdue for periods in excess of the usual period of credit granted in the trade concerned.

III) Early installments a2:ainst Long:-term Liabilities:

Term loans, deferred payment credits, debentures and redeemable preference shares are long-term liabilities but the installments thereof, which are repayable within one year, are included in the current liabilities, because hire payment is to be made like other current liabilities in the immediate future.

IV) Other Current Liabilities:

These include provision for taxation, interest on term-loans, debentures and other charges due,

rent insurance, wages, salaries unpaid etc.

V) Term Liabilities:

Term liabilities are those liabilities which are payable after a period of one year from the date of balance sheet.

NET WORTH:

Apart from the liabilities due to outsiders the rest of the terms on the liabilities side of the balance sheet are considered as the owned funds or the capital funds of the borrowing concern. A company’s own funds comprise mostly its share capital, general (or free) reserve, capital reserve, premium on shares and undistributed profits The own funds or, the ‘net worth’ of the borrowing concern, must be sufficient keeping in view of the requirement of the business. Moreover, the long-term needs of the business should be financed by the owned or long-term liabilities~ otherwise the business unit might experience difficulties in the repayment of the short debts. The concept of ‘net worth’ of the borrowing concern is very sufficient for the creditors and the bankers because it indicates the extent of the solvency of the borrower. The uncalled capital should be taken into’ account as it strengths the financial position of the company as, in case the company needs more funds, it can make calls on the shareholders. Again in the event of the company’s liquidation, the uncalled share capital would bring additional cash for the benefit of the creditors.

Contingent liabilities:

A contingent liability is a likely or possible liability. These liabilities do not exist at the time of balance sheet but it may arise in future.

PROFIT AND LOSS ACCOUNT:

The objective of studying the profit and loss account of a company for a particular financial year IS:

To know the trading results during the period; ii) to relate the profits to

a) The total capital (Share capital, reserves, etc., and long-term borrowings)

employed in the concern which will indicate its overall profitability;

b) The share capital which will indicate profitability of the share capital employed In business;

B. To find out the relation between profits and turnover. It should be seen if, with the

increase in sales, the same ratio of profitability has been maintained. In order compare trading results for different years, the banks should extract the profit or loss figures for each year separately.

RATIO ANALYSIS:

When a banker examines a balance sheet together with the profit and loss account, he usually makes certain comparisons between certain items of the balance sheet and also to some items in the profit and loss account. These relationships are called ‘Ratios’. The analysis of the balance sheet and working of different ratios assists the banker informing an opinion whether the

business is progressing, deteriorating or static. Ratio analysis is a useful and common method of determining and interpreting different items in the financial statements.

i) Financial Ratio.

ii) Turnover Ratio.

iii) Profitability Ratio.

Financial Ratios:

Financial ratios indicate about the financial position of the company. A company is deemed to be financially sound if it is in a position to carry on its business smoothly and meet all its obligations both long term as well as short term without strain. Thus, its financial position has to be judged from two angles — long term as well as short term. The ratio is expressed as follows:

Fixed Assets Ratio: Fixed Assets/Long Term Funds:

The ratio should not be more than one. If it is less than one, it shows that a part of working capital has been financed through long term funds.

Current Ratio:

This ratio is computed by dividing the current assets by current liabilities. It is expressed as follows:

Current Ratio: Current Assets/Current Liabilities:

If the current assets are excessively higher than the current liabilities, it would imply that the company has more finance than it needs and cannot, or does not, employ it profitably. The mere fact that current ratio is quite high does not mean that the company will be in a position to meet adequately its short-term liabilities. In fact, the current ratio should be seen in relation to the component of current assets and higher liquidity. If a large portion of current assets comprise the obsolete stocks or debtors outstanding for’ a long time, the company may fail even if the current ratio is higher than 2. The current ratio can also be manipulated very easily. This may be done either by postponing certain pressing payments or making payment of certain current liabilities. In both the cases, the position requires scrutiny. An ideal ratio is between 1.5 and 2. If the ratio is 2, the position of the concern is highly liquid, if it falls below 1, it may indicate shortage of working capital.

Quick Ratio/Acid Test Ratio:

This ratio is called the liquidity ratio. This ratio is determined by dividing quick assets by current liabilities. This ratio may be expressed as:

Quick Assets (Current Assets-Inventory) / Current Liabilities

By quick assets it means those current assets which are quickly and readily convertible into cash. Cash in hand and bank are of course quick assets. Marketable securities and receivables/book debts are also quick assets. Raw materials and finished products, as also stocks-in process, are not included in quick assets.

Current ratio and quick ratio are both very helpful in measuring the liquidity of a concern. If any of the ratios is below 1, the current liabilities exceed the current assets and the company may not be able to meet its obligations, if the occasion demands. The quick ratio, it must be remembered, is a better indication of the concern’s ability to meet its current liabilities at short notice. The current ratio and the quick ratio are also useful for comparing the liquidity of the concern on different dates.

iv) Debt-equity ratio:

This is very important ratio for the creditor including the bankers. The debt-equity ratio is determined to ascertain the soundness of the long term financial policy of the company. It is also known as external and internal equity ratio. It may be calculated as follows:

Debt -equity ratio = External equities/ Internal equities

The term external equities refer to total outside liabilities and term internal equities refers to shareholders’ fund or the tangible net worth. In case debt-equity ratio is to be calculated as a long term financial ratio, it may be calculated as follows:

Debt-equity ratio = Total long-term debt Shareholders’ fund

This ratio brings out the proportion of debt (long-term borrowed fund) to equity (Shareholders’ fund) by dividing the former by the latter. This ratio shows the extent to which the term liabilities are covered by the owned funds or the tangible net worth of the business. The ratio indicates the extent to which the firm/company depends upon outsiders for its existence.

A ratio of 1 : I is generally considered satisfactory as it indicates the safety of the funds lent to the business. If the debt exceeds the equity, or the borrowed funds exceed the company’s own funds, the debt equity ratio will exceed unity which is considered as an unhealthy feature. However, in a well-managed concern dealing in or manufacturing readily marketable products, a higher ratio may be acceptable.

v) Proprietary Ratio:

It is a variant of debt equity ratio. It establishes the relationship between the proprietors’ or shareholders’ funds and the total tangible assets. It may be expressed as:

Proprietary ratio = Shareholders’ Fund/Total Tangible Assets

This ratio focuses the attention on the general strength of the business enterprise. The ratio is of particular importance to the creditors who can find out the proportion of shareholders’ funds in the total assets employed in the business.

A high proprietary ratio will indicate a relatively little danger to the creditors, in the event of forced organization or winding up of the company. A low proprietary ratio indicates greater risk to the creditors since in the event of losses a part of their money may be lost to the proprietor of the business. The higher the ratio, the better it is.

TURNOVER RATIO:

The turnover ratios indicate the efficiency with which the capital employed is rotated. They are also, therefore, known as Activity or Efficiency Ratios. The overall profitability of the business depends on two factors:

(i) The rate of return of capital employed; and

(ii) The turnover i.e. the speed at which the capital employed in the business

rotates. Higher the rate or rotation, greater will be the profitability. In order to find out which part of capital is efficiently employed and which part not, different turnover ratios are calculated. These ratios are as follows:

I)Fixed Assets Turnover Ratio:

The ratio indicates the extent to which the investment in fixed assets contributes towards the sales. If compared with a previous period, it indicates whether the investment in fixed assets has been judicious or not. The ratio is calculated as follows:

Net sales/Fixed Assets (net)

iii) Working Capital Turnover Ratio:

The ratio indicates whether or not working capital has been effectively utilized in

making sales. The ratio is calculated as follows: .

Net sales! Net Working Capital:

Working capital turnover ratio may take different forms for different purposes. Some of them are being explained below:

Debtor’s turnover ratio (Debtors’ Velocity) :

Debtors constitute an important constituent of current assets and, therefore, the quality of debtors to a great extent determines a firm’s liquidity. This is used by financial analysis to judge the liquidity of the firm.

The debtor’s turnover ratio is calculated as under:

Credit sales/Average accounts receivable

The term’ account receivable’ includes ‘Trade Debtors’ and ‘Bills Receivable’.

b) Creditors’ turnover ratio (Creditors’ Velocity):

It is similar to Debtors’ Turnover Ratio. It indicates the speed with which the payments for credit purchase are made to the creditors. The ratio can be computed as follows:

Credit purchases/ Average accounts payable

The term “Accounts Payable” includes ‘Trade Creditors’ and ‘Bills Payable’. Both the creditors turnover ratio and the debt payment period enjoyed ratio indicate about promptness or otherwise in making payment of credit purchases. A ‘higher creditors’ turnover ratio’ or a ‘lower credit period enjoyed ratio’ signifies that the creditors are being paid promptly, thus enhancing the credit worthiness of the company. However, a very favorable ratio to this effect also shows that the business is not taking full advantage of credit facilities which can be allowed by the creditors.

c) Stock (Inventory) turnover ratio:

The ratio indicates whether investment in inventory is efficiently used or not. It, therefore, explains whether investment in inventories is within proper limits or not. The ratio is calculated by dividing the cost of goods sold by average stock held during the year. The ratio is calculated as follows:

Cost of goods sold during the year. Average inventory (stock)

Average inventory calculated by taking stock levels of raw materials, work-in-process, finished goods at the end of each month, adding them up and dividing by twelve.A high inventory turnover ratio indicates brisk sales. The ratio is, therefore, a measure to discover the possible trouble in the form of overstocking or over valuation. The stock position is known as graveyard of the balance sheet. If the sales are quick, such a position would not arise unless the stock consist of saleable items. Average inventory turnover ratio results in blocking of funds in inventory which may ultimately result in heavy losses due to the inventory becoming obsolete or deteriorating in quality. Then it would be necessary to further analyze this problem. It is difficult to establish a standard ratio of inventory because it will differ from industry to industry.

PROFITABILITY RATIOS:

i) Overall profitability Ratio:

It is also called as “Return on Investment” (ROT). It indicates the percentage of return on the total capital employed in the business. It is calculated on the basis of following formula.

Operating profit/Capital Employed x 100

The term “Operating Profit” means “Profit before Interest and Tax’. The term ‘Interest’ means ‘Interest on Long-term borrowings’ Interest on short term borrowings will be deducted for computing operating profit. Non-trading income such as interest on government securities or non-trading losses or expenses such as loss on account of fire etc. will also be excluded.

ii) Gross Profit Ratio:

The ratio is calculated by dividing profit before depreciation, taxation and other allocations, by the sales during the period. The ratio is usually expressed as a percentage.

This ratio expresses relationship between gross profit and net sales. Its formula is

Gross Profit / Net sales. 100

A comparison of this ratio for the last few years will show the trend in the profitability of the business operations, i.e., whether the profitability is increasing, decreasing or remaining constant. This ratio of the borrowing concern should be compared with that of other units in the same trade or industry to have a comparative views of the performance of the borrowing concern vis-a-vis similar other units.

There is no room for judging the Gross Profit Ratio; therefore, the evaluation of the business on its basis is a matter of judgment. However, the gross profit should be adequate to cover operating expenses and to provide for fixed charges, dividends and building up of reserves.

II) Net Profit Ratio:

This ratio is derived by dividing the net profit after depreciation but before taxation by the net worth of the company. The ratio so obtained will show the profitability of the total own funds of the company employed in the business. It is particularly useful from the point of view of investors who wish to invest their funds in the corporate securities. It may be calculated in the following way.

Net Operation Profit/ Net sales x 100

Net operating profit is arrived at by deducting operating expenses from Gross Profit.

The net profit can also be divided by the paid-up capital to calculate the profit earning capacity of the share capital employed in the business. A third way of judging the profitability of the concern is to divide the net profit by the total capital employed, i.e. share capital, reserve, and long-term borrowing.

iv) Fixed Charge Cover:

The ratio is very important from the lender’s point of view. It indicates whether the business would earn sufficient profits to pay periodically the interest charges. The higher the number, the most secured the lender is in respect of his periodical interest income. It is calculated as follows:

Income before interest and tax x 100 Interest charges

This ratio is also calculated as “Debt Service Ratio”.

The standard for this ratio for an industrial company is that charges should be covered six to seven times.

Limitations of Accounting Ratios:

i) Comparative study required.

ii) Limitations of financial statements. ill) Ratios alone are not adequate.

iv) Window-Dressing.

v) No fixed standards.

SECTION – C

PART ONE

PROJECT PART

Introduction:

In the modem business world, organizations apply a number of business strategies. Technological innovation has greatly changed the way of doing business today. And as more time goes by, people will definitely be exposed to newer systems of handling money and also get used to the benefits they get. In the general banking and export import operation, a bank must satisfy the customers in a way they want to be satisfied. So customer satisfaction is considered to be a key motto, as customers who are satisfied will definitely come back in future. Customer’s satisfaction proves to be the most significant strategy whatever may be the product, service or non-service, concerning business. In case of export import operation, clients demand more and more sophisticated privilege, because it is not a dealing for thousands rather it is the dealing for crores of amount. Service is the outcome of the Bank. It is widely acknowledged that customer service begins at the entrance of a customer into a Bank. The first person that represents the bank seems to be the sentry posted in front of a bank building, with his good wishes to a customer and a smiling face.

Origin of the Report :

As a requirement for my MBA practicum, I have conducted this Internship Program on “General Banking and Finance Operations on Export and Import of DHAKA BANK LIMITED”. My honorary sir Prof. Kayemuddin, Faculty of Business Administration, Dhaka International University, gave this topic and helped me a lot in my way to complete this report.

Rationale of the Study:

Due to free market economy, the competition among the nationalized, foreign and private commercial banks and the expectation of the customers is rapidly growing concerning the banking operation and how customer service becomes more attractive. Reciprocating the sentiment, commercial/private banks are trying to elevate their traditional banking service to a better standard, to meet the challenging needs. Side by side, these banks have now concentrated their attention towards diversification of their products for better performance and existence. Under the above circumstances, it has become necessary for DHAKA BANK LTD., one of the leading commercial banks, to focus its attention towards the improvement of the customer service. That’s why it is quite justified to make an in-depth study about its operation and evaluate the service provided by this bank and scope for its improvement. The s’tudy may help formulating policy regarding the ideas relating to the feelings of the customers and bankers. Further more, DHAKA BANK LTD. executives who are actually executing the policies undertaken by the top management will have a chance to communicate their feelings and will have the feedback about their dealings with the customers.

Objectives of the Study:

The primary objectives of the report are as follows:

To submit a report, for the fulfillment of my MBA practicum.

The main objective of this report is to find out the “General Banking and Finance

Operations on Export and Import of DHAKA BANK LTD.”

To gather comprehensive knowledge on overall banking functions and the

expectations of the customers regarding the service level of the bank.

Identify the factors contributing to the attractive and operative performance of

the local branch of the bank.

To make a study of the facts in order to arrive at certain conclusion about overall banking operation.

Critically analyze the functions and the operations of each level of the

organization of DHAKA BANK LTD.

To prevent current observation and unique aspects of the bank.

To familiarize with practical job environment.

To examine the profitability and productivity of the bank.

Scope of the Study:

The focus of the report is on general banking and finance operations to judge the performance of the existing service facilities provided by. DHAKA BANK LTD. Attempts have been made particularly to gather customer’s attitudes toward the service and quality provided by this bank.

Methodology :

The methodology of the report is stated below, which was appropriately exercised in achieving the above stated objectives.

Time period of the study:

For the fulfillment of the desired purpose following working days are spent in various departments:

Place & Location of Study:

DHAKA BANK Foreign Exchange Branch,

Division / Department | Working Days |

| General Banking Department | 18 Days |

| Export Department | 18 Days |

| Import Department | 18 Days |

| Accounts Department | 18 Days |

| Advance Department | 18 Days |

Sources of Data Collection

The inputs are collected from two sources:

Primary Sources:

D Discussion with bank officers.

D Personal observation.

D Desk work in different sections/ departments.

Secondary Sources:

1. Annual report of the DHAKA BANK LTD., 2000.

2. Brochures and leaflets of the Bank.

3. Consultations of related books and publications.

4. Different statements of branch.

5. Files, Balance sheet and various documents of DHAKA BANK.

6. Different report and journals of the bank.

Data Processing:

Collected information is processed by the use of computer system. Detailed analysis, working variables and working definitions are embodied in the report.

Limitation of the Study:

The study has suffered from a number of limitations:

Time constraint was a major drawback in this study.

It was difficult to communicate with the customer, as many of them were hesitant to

respond. As a result the sample size was not big.

Another limitation of this report is Bank’s policy of not disclosing some data and

information for obvious reason, which could be very much useful.

The outlet owners might have got a little biased on the fact, because they thought

that the study was being prepared for the particular department.

The clients were very busy. So they were unable to give me much time for interview.

For the sake of convenience, the survey had to be kept confined to the Foreign

Exchange Branch only.

SECTION – C

PART TWO

PROTECT PART

COMPETITIVE CONDITIONS, INDUSTRY ANALYSIS, STRENGTHS, WEAKNESSES, OPPORTUNITIES AND THREATS

COMPETITIVE CONDITIONS:

Almost all banks are in highly competitive positions since nowadays the number of banks is increasing at a rapid pace and it can be expected that it will be more in the future. However, the main sustainability again, depends on the bank’s number of clients and deposits and its income. So if there are steady customers; then banks usually don’t face downfalls. But recessions are unwanted in the economy and when they do take place bankers don’t have a choice but to pray for time for the economy to recover. The main competitors of this bank include all banks operating at the same level, such as Mercantile Bank, One Bank, NCC Bank, Bank Asia, Southeast Bank and some other banks which are of the same generation.

But the main important point remains that now the competitive climate overall is very poor ever since the bombing of the Twin Tower in the 11th of September, as mostly exports have fallen and these are consequences that almost all banks have to suffer. Large exporting firms are the ones who can survive but some of the new and small ones are getting abolished ever since the bombing.

Although there have been massive improvements, but fact remains that the consequences will be harsh on almost all banks.

INDUSTRY ANALYSIS:

The Bangladesh bank ranks all banks in order of which generation they have been operating. This rating is usually known as the CAMEL (Capita, Asset, Management, Efficiency and Liquidity) rating. Now last year, amongst the 3rd generation banks, Mercantile bank was ranked number 1, whereas DHAKA BANK was ranked number 2, this was in 2001. It cannot still be predicted as to what is ahead in the CAMEL rating in the year 2002. But however, the current performance of DHAKA BANK can always be considered to an upward sloping curve.

SWOT ANALYSIS

Strengths:

The directors of the board are a major strength as they themselves have a large finance base, and they have other businesses, so they can always invest a lot of capital in this bank.

Another important strength is the supervision of adviser and the directors of the bank.

Amongst the major strengths of the DHAKA BANK Foreign Exchange Branch, the pay structure of the employees and their motivation and devotion towards work is the biggest strength.

The senior Vice President and manager are the key individuals who have established active networking with the top corporate clients for which the bank is getting most deposits.

The employees are also actively collecting deposits with their contacts as a result of he quota that needs to be fulfilled, which .again, ends up in collection of deposits.

Weaknesses:

Amongst the weaknesses of this bank is the unavailability of A TM (Automated

Teller Machines), and credit cards which many customers today are demanding.

Another important weakness is the size of the credit division which needs to be

vastly increased for credit cards to be introduced.

Advertising of this bank should also be done on a more extensive basis which is not

so extensive now compared to other banks.

Requests about online banking is yet another concern as often customers after

hearing what other banks are offering often are interested in knowing whether

DHAKA BANK offers such facilities.

Opportunities:

More customers can be attracted if successful advertising can be done; resulting in

greater profits.

If ATM cards, and credit cards are introduced then that will result in a better customer

satisfaction level, and there will be more people who, because of these, might

become customers of the bank.

If there is a separate Department of the bank that emphasizes on simple consultations

regarding imports and exports then people can take advantage of that.

Furthermore, online banking should be introduced as most banks nowadays have

these services.

Threats:

In banking there is always a threat as to whether other banks will be able to offer higher interest rates on the customer’s deposits. So this is one big threat, as bankers often know that there can be other banks who can attract customers by saying that they will offer higher interest rates.

One of the biggest threats that has already taken place is the incident on the 11th of September, which includes the bombing of the World Trade Centre (WTO) which has led to some downfalls in the garments industry and in a way the bank is suffering as there were a lot of clients whose primary business was garments.

Government changes in regulations regarding loans, advances, and other formalities also remains a threat as especially customers might not react favorably to changes, and as a result blame it on the bank for the changes.

Since there are other banks which offer greater ranges of products such as A 1Ms, credit cards and online banking this remains a threat as many customers might want this services which they cannot get from this bank.

The economy as a whole poses a threat as now there is a downfall in almost all business because of the poor economic conditions, hence, during this period there are no alternatives but to pray for the economic conditions to get better.

STRATEGIC, OPERATIONAL AND LEGAL ISSUES AND PROBLEMS FACING THE COMPANY AND THE STRATEGIES AND TACTICS USED TO COPE WITH THEM

Throughout time almost all financial institutions face problems that are operational, strategic or legal. The challenge is how they can possibly cope up with them. There are operational problems such as forging of cheques, false notes, which eventually contribute to the bad debt of the bank. Strategic problems such as how reliable a party can be to release a loan, are issues that have to be coped up with constantly. And for these reasons; the Senior Vice President of our DHAKA BANK Foreign Exchange Branch and our respected Manager are always there to deal with these clients; but at higher levels; such as organizational levels; people higher in the hierarchy such as the Senior Vice President, Mangers, and directors have to deal with it.

Hence, problems arise and when it does the bank is always proactive about it; and tries and resolves disputes as soon as possible. And for that all the credit goes to the people working for the bank and others who are in favour of the bank.

SECTION – C

PART THREE

FINDINGS, RECOMMENDATIONS AND CONCLUSION

Findings:

1. Only the case section of the branch is computerized. Hopefully the management decided to provide computers for departments, which will bolster services of the bank.

2. When a joint stock company comes to open an account if the company happens to be an existing one, the banker should demand copies of the balance sheet and profit & loss account, which will reflect the financial growth of the company and its soundness. But in practice companies and the bankers, as well, don’t even bother.

3. Encoding and decoding process of test number eat up the lion’s share of the time of the officer who works in that desk. But a simple computer program could do the same if the desk were computerized.

4. Officers of the bank are competent. Even though many of them simply know the working procedure of what they are doing but don’t know the philosophy behind doing those.

5. Project loan requires testing of feasibility of project and judging the marketability of the product. It requires infusion of knowledge of both the fields – marketing and banking. But the bank has hardly any officer with this kind of ability.

6. Like most of the private banks, DHAKA BANK LTD. also imposes a target deposit for collection upon its employees. Every employee has to go out for the purpose of .deposit collection, which they call “development purpose”. It is an effective method no question about it, since many banks of our country relies on this method. But sometimes it affects negatively and causes job dissatisfaction. Officers of the desk, where workload is very high, hardly get the chance to go out for development purpose and always feel that their duties for the organization would not be evaluated unless they can show a good amount of deposit collection against their name.

Recommendation:

In order to get competitive advantage and to deliver quality service, top management should try to modify the services. .

* Rectify the Existing Problems :

1. The synergy of dedicated manpower, technology, and market opportunity can lead the organization to achieve the goal, a bank must establish and adhere to adequate policies, practices and procedures for evaluating the quality of asset and the adequacy of loan provision and reserve.

2. DHAKA BANK should train up their branch personnel about all sorts of

information regarding SWIFT and its service.

3. Due to lack of proper knowledge about the operation procedures and services provided to the customers by SWIFT, certain customers are facing problems, as they have to wait for a certain time to get the service. And sometimes personnel are not being able to operate SWIFT without confusion. They are not fully independent in handling SWIFT. Official training is the solution to this problem.

4. DHAKA BANK should always monitor the performance of its competitors in the field of Foreign Trade.

5. Mercantile Bank Ltd. Standard Bank Ltd., Mutual Trust Bank ltd., Premier Bank Ltd., First Security Bank Ltd., Eastern Bank Ltd., Bank Asia Ltd. and Exim Bank Ltd. and all other private banks are the emerging competitors of DHAKA BANK. They should continuously strive and try to introduce new products and services as access card and ATM with future improved quality services.

6.For customer’s convenience in Foreign Exchange Department of D~AKA BANK Ltd., the department should provide more personnel to deliver faster services to their honorable customer.

7. It seems to me that day-by-day customers operation is increasing; individual employee has to handle different types of jobs. But that is patting a back for an employee. As a result there might happen a big mistake by the employee and service is also time consuming and customer has to suffer for this situation. May be it would be the reason for employee’s de-motivation as well as the customer’s dissatisfaction.

8. DHAKA BANK LTD. should focus on their promotional activities.

9. They should also focus on the marketing aspects to let customers know about their products and offering more promotional services should be given to attract new customer.

10.DHAKA BANK LTD. must develop electronic banking system to modify the service. Technological advantage of a bank ensuring its competitive edge in the market place can only be achieved by efficient manpower. Electronic banking system also allows increased access to the financial system by its customers.

* Some other important factors that should be focused on the development

process are:

1. Time consumed at service level should be minimized at optimum level.

2. Evaluate customer’s needs from their perspective and explain logically the

shortcomings.

3. Customer’s convenience should receive priority.

4. Improve office atmosphere to give customers better feeling.

5. Use of effective management information systems.

6. Use appropriate techniques in evaluating customer’s need professionally.

7. To deliver quality service, top management should try to mitigate the gap

between customer’s expectation and employee’s perception.

* Comments :

A. The bank can offer to its customer better service if all of its departments are

computerized and incorporated under local area network (LAN).

B. At the entry position the bank should enroll more expert people to augment

. quality services.

C. Nowadays, conventional banking concept is outmoded. Now banks are, offering more ancillary services like credit card, on line services and many others. DHAKA BANK LTD. should differentiate its services adopting the modem facilities.

D. Bank is providing both internal and external training for the officers but bank should be scrupulous about the training facilities so that officials can implicate this in their job.

E. People are very choosy about environment nowadays, so bank premises should be well decorated and DHAKA BANK LTD. should look into the matter very seriously.

F. Bank should provide advances towards the true entrepreneur without reconsidering conventional system of security and collateral. Moreover, the whole process should be completed with in acceptable time.

CONCLUSION:

There are a number of nationalized and foreign banks operating in Bangladesh. The DHAKA BANK LTD. is a promising one among them. The growing competition bounds DHAKA BANK not only to compete with the other commercial banks but also with the public banks. For the future planning and the successful operation in achieving its prime goal in this current competitive environment this report can be a guideline.From the practical point of view I can declare boldly that I really enjoyed my internship at DHAKA BANK from my first day. Moreover, this internship program which is mandatory for my MBA program, although short-dated obviously has helped my further thinking about my career.

An evaluation of the customer service department and the scope for its advancement in a harmonious combination was the basic concern of my study and I completed this report on this basis that customer service department should be one of the most important departments of a bank. Customers obtain service directly from them. My central aim was to understand different services practiced by this department and explain it from my own point of view and also how their services can be improved.

Banks always contribute towards the economic development of a country. DHAKA BANK, compared with other banks is contributing more by investing most of their funds in fruitful projects leading to increase in production in the field of Export and Import Business. It is obvious that the right thinking of this bank including establishing a successful network over the country and increasing resources, will be able to play a considerable role in the portfolio of development of financing in a developing country like ours.

Glossary

H FDR -Fixed Deposit Rate

H FOB -Free On Board

H MSS -Monthly Savings Scheme

H MPPS -Monthly Profit Payable Scheme

H PO -Payment Order

H DD -Demand Draft

H TT -Telegraphic Transfer

H NFCD -Non Resident Foreign Currency Deposit

H RFCE -Resident Foreign Currency Deposit

H AD -Authorized Dealer

H TC -Travelers Cheque

H C&F -Cost & Freight

H FC -Foreign Currency

H STD -Short Term Deposit

H FER -Foreign Exchange Regulation

H GSP -Generalized System of Preference

H CAD -Cash Against Document

H D/P -Document Against Payment

H A/C -Account

H UCP -Uniform Customers and Practice for Documentary Credit

H IBP Inland Documentary Bills Purchased.

BILIOGRAPHY

- Annual report on DHAKA BANK LTD. 2000 and 2001.

- Brochures published by DHAKA BANK LTD.

- How to use your Bank by Warren Henry

- Design and operation of Customer service system by Paul S. Bender

- Foreign Exchange and Financing of Foreign Trade by Syed Asraf Ali.

- Financial Institutions and Markets- A global perspective Hazel Johnson.

- Managing Projects in Bangladesh by Skylark Chadha.

- The Management of Bank Funds (Second Edition) by Robinson.

- Financial Management and Policy (Tenth Edition) by Van Horne.

Some are parts:

General Banking and Finance Operations of Dhaka Bank Ltd (Part 1)

General Banking and Finance Operations of Dhaka Bank Ltd (Part 2)

General Banking and Finance Operations of Dhaka Bank Ltd (Part 3)