Once considered a fancy gadget for the elite, the mobile phone has been transformed into an essential tool for all. Mobile phones are now empowering people from all groups in all areas of Bangladesh. And this revolution was first brought about by Grameenphone Ltd.

Grameenphone Ltd., the largest telecommunications service provider in Bangladesh, received its operating license in November 1996 and started its service from March 26, 1997, the Independence Day of Bangladesh. Now, after 10 years of successful operations, Grameenphone is the largest mobile phone service provider in Bangladesh, with more than 22 million subscribers as of July 2010. Grameenphone provides services to rural and urban customers across Bangladesh, where mobile telephony is acknowledged as a significant driver of socio-economic development, both for individuals and the nation.

Grameenphone Ltd. is incorporated in Bangladesh as a private limited company and now it is the market leader in mobile connectivity in Bangladesh. The current market share of GP is around 46%, almost three times more than its nearest competitor, Banglalink. Grameenphone (GP) has been established to provide high-quality GSM cellular service in Bangladesh at affordable prices. Serving the mass market is one of GP’s primary goals. By serving the general public as opposed to niche markets, the Company plans to achieve economies of scale and healthy profits. But serving the mass population is never easy. Organizing the distribution and collection channel for over 14 million clients is a daunting task indeed. That is why Grameenphone has always tried to be innovative in introducing newer and easier channels both for its distribution and collection network to work more efficiently.

The total subscriber number of Grameenphone is currently 22 million. Among them 5 lacs (3%) are post-paid subscribers. These subscribers mainly pay through – Banks, ERS (Flexi Load) and Scratch Card. Banks used to be the main collection mode but recently ERS is more popular whereas Scratch Cards are the least used mode of collection. This report will be explain and make comparative analysis between the different modes of payments through banks such as – ATM, Auto Debit etc. The introduction of ERS for collection of air-time has revolutionized the whole process. This report will also include a cost-benefit analysis of using ERS as a collection method and judge its effectiveness and efficiency.

Title of the Report:

This report will be titled as “The Investment policy of grameenphone ltd.( fund management).” The report will be divided into three basic parts like overview of grameenphone, the investment procedure of grameenphone in different banks, the investment procedure of grameenphone to extend their business.

Objective:

In this report, I would try to endow how grameenphone ltd. craft their decisions in making their investment. Here I would basically talk about the activities of the department of corporate finance and treasury under finance division and their decision making procedures and techiniques to invest in commercial banks and to extend their own business. Therefore the objective of the report can be summarized as follows:

Broad objective: To give a picture of the department of corporate finance, treasury and fund management in respect to investment policy.

Specific objective:

- To emphasize the brief description of finance division.

- To summarize the activities of the deparment of corporate finance and treasury.

- To know deeply how the concerned department make their investment decisions in banks.

- To know the factors and tools they rely on when making investment decisions in banks.

- To focus on the factors the consider when making investment to extend their business.

- To specify some findings from my analysis.

- To make some recommendations for the sectors which can be improved.

Significance of the study:

The finance division is the most vital division of any organization. They have to always deal with money i.e. how to invest money, how to collect money, what will be the sources of the money etc. The department of corporate finance and treasury is again very crucial department under finance division. They have to manage the fund coming in to grameenphone ltd. As an undergraduate student, I think I need to know how giant companies like grameenphone make their investment decisions. This study would help me in following aspects :

- It will help me to work in finance division of giant companies in future as I would learn their investment policy.

- As I would learn the investment decision making process, it would help me to make my own investment decision if I become an entrepenuer in future.

- The research will show the performance of different banks and their ratings which is again important in case of investment decision.

- This form of research will encouage me to do further researches in Bangladesh or other countries in the same area of interests.

Research Methodology:

The project will require primary and secondary data. I will collect the secondary data by going through different books, journals, online sources etc. The sources will be clearly mentioned in the references according to APA format. There will primary data sources as well because to do my analysis I will require some primary data which I will collect by interviewing different officials of finance division of Grameenphone Ltd.

Limitations of the study:

Grameenphone is a public Ltd. Comapany. Some their financial data is very sensitive to reveal in the public. Therefore I would not be provided with those financial data. So, in case of that I have to do the research with the data available in my hand and in some cases with some hypothetical data.

Grameenphone Limited

Grameenphone Ltd. received its operating license in November 1996 and started its service from March 26, 1997, the Independence Day of Bangladesh. The shareholders established the company realizing the important role telecommunications can play in economic development: Connectivity translates into productivity. They also made a commitment that “Good Development is Good Business”.

Grameenphone is a unique international joint venture between Telenor (62%), a leading telecommunications company of Norway, and Grameen Telecom (38%), a not-for-profit company in Bangladesh, working in close collaboration with the micro-credit pioneers Grameen Bank and Professor Muhammad Yunus, the Nobel Peace Prize winners in 2006. Entrepreneur Iqbal Quadir first had the idea of providing mobile telephony to the poor of Bangladesh. His early discussions with Professor Yunus later resulted in launching the internationally acclaimed Village Phone Program, coupling micro-credit with mobile telephony to make telecommunications accessible to the rural poor. The shareholders also contributed with their unique strengths. Being at the forefront of developing and delivering modern telecommunications facilities for more than 150 years, Telenor provided the managerial expertise and technological know-how to set up a world-class mobile phone operation in an emerging market. On the other hand, Grameen Telecom provided the knowledge and deep understanding of the local economy. At present GP has coverage all over Bangladesh as well as in 100 foreign countries of 6 continents through 250 international roaming partner operators.

Founding Partners of Grameenphone Ltd.

Initially Grameenphone was a joint venture company comprising of four companies from four different countries: Telenor of Norway, Grameen Telecom of Bangladesh, Marubeni Corporation of Japan and Gonofone Development Corporation of USA.

Telenor

Telenor is a state-owned telecommunication company from Norway. It is amongst the oldest, most sophisticated, and diversified telecom companies in the world. The company has a long history of successful cooperation with other operators and governments in and out of Norway. It has operations in Russia, Hungary, Montenegro, Ireland, Bangladesh, Greece, Germany, Germany, Australia, Malaysia etc. Telenor’s home base, Norway, has the highest density of mobile phones in the world and one of the most competitive markets in the field. Telenor has been playing a pioneering role in the development of GSM, one the latest and most successful versions of cellular technologies.

Grameen Telecom

Grameen Telecom, a sister concern of Grameen Bank, has been established to organize and assist the borrowers of Grameen bank. It was established in 1995 as a not-for-profit company for improving the standard of living and eradication of poverty from rural Bangladesh by extending the benefits of information revolution. Grameen Telecom’s objectives are to provide easy access to GSM cellular services in rural Bangladesh, creating new opportunities for income generation through self-employment by providing villagers with access to modern information and communication based technologies.

Marubeni Corporation

Marubeni Corporation is a leading investment and trading company from Japan. It is involved in the operations of import, export and offshore trading. It has major investments in numerous developing countries throughout Asia, Africa and Latin America.

Gonofone Development Corporation

Gonofone Development Corporation is a New York-based telecommunication development company having investments in many companies in USA, Russia and other parts of Europe. It was established in 1994 in New York for organizing the concept of Grameenphone.

These four companies owned shares of Grameenphone in the following manner:

Table-: Founding Partners of Grameenphone Ltd.

| Share Holders | % of share |

Telenor | 51.0 |

| Grameen Telecom | 35.0 |

| Marubeni Corporation | 9.5 |

| Gonofone | 4.5 |

Existing Shareholding Structure of Grameenphone Ltd.

It is a joint venture enterprise between Telenor (55.8%), the largest telecommunications service provider in Norway with mobile phone operations in 12 other countries, and Grameen Telecom Corporation (34.2% ), a non-profit sister concern of the internationally acclaimed micro-credit pioneer Grameen Bank. The other 10% shares belong to 10% to general retail and institutional investors

About Grameenphone Ltd.

Company Vision

The vision of Grameenphone Ltd. is “We are here to help”. Grameenphone exists to help its customers get the full benefit of communications services in their daily lives. It wants to make it easy for customers to get what they want, when they want it.

Company Mission

The vision will be achieved by the following missions:

- Connecting Bangladesh with ease and care

- Being user-friendly cellular phone service provider

- Providing value for money

- Providing simple and timely connections

- Having a right and understandable process

Company Values

Grameenphone Ltd. intends to portray its corporate values in all its functions, products and service. These values are:

- Make it easy

- Keep promises

- Be inspiring

- Be respectful

Company Objectives

The main objective of Grameenphone Ltd. is “Good Business, Good Development”. Grameenphone believes in providing service that leads to good business and good development. Telephony helps people to be better connected, work together, and thus raises productivity. This gain in productivity is development, which in turn enables them to afford services that Grameenphone offers, generating a good business. Thus development and business go together.

Serving the mass market is one of GP’s primary goals. By serving the general public as opposed to niche markets, the company plans to achieve economies of scale and healthy profits. At the same time, service to the general public means connectivity to a wider population and results in the economic development of the country. The company has devised its strategies so that it earns healthy returns for its shareholders and at the same time, contributes to genuine development of the country. In short, it pursues a dual strategy of good business and good development.

They say that everything starts with a dream. They started their history with a dream to bring change. The dream of changing the future with the strength of technology, of changing lives with the power of innovation.

Key Success Factors

Grameenphone Ltd. started operating in a monopoly market. Since then the market has turned competitive day by day. But it has retained its position as the market leader. Parameters identified as success factors for this continuous development are:

- Nationwide coverage

- Satisfied customers

- Easy availability

- Customer care

- Value added services

- Continuous investment

- Continuous innovation

- A group of enthusiastic employees

To maintain its place as the market leader, GP plans to deliver new products and new features to the market, which have been and will be planned keeping in mind the need, purchasing power, and usage pattern of different segments in the market.

Products and Services of GP

By bringing electronic connectivity to both urban and rural Bangladesh, Grameenphone is bringing the digital revolution to the country. The products of Grameenphone are categorized in four different segments four different kinds of users. They are:

- General Users

- Business Users

- Youth Segment

- Rural Users

General Users

For general users Grameenphone offers two types of products

- Prepaid

- Postpaid

Prepaid product- “Smile”

Introduction of Grameenphone’s Pre-Paid Service is a revolution of mobile telephony in Bangladesh. More than 95% of GP’s subscribers are prepaid users. Smile connections are of two types namely, “Smile” and “Smile PSTN”. The former is only mobile-to-mobile, while Smile PSTN connects to BTTB local, BTTB-NWD (Nationwide Dialing), ISD (International Standard Dialing), all Grameenphone mobiles, and other mobiles and receives calls from the same. It frees the subscriber from the hassles of paying bills, security deposits and line rents. A wide range of value added services are offered with this connection, namely – news updates, downloadable ringtones, wallpapers, data transfer, internet browsing etc.

Postpaid Product- “Xplore” Packages

Grameenphone has around 500,000 postpaid subscribers. For these subscribers it offers two types of postpaid connection – Xplore-1 & 2. “Xplore-1” connects to BTTB local, BTTB-NWD (Nationwide Dialing), all Grameenphone mobiles, other mobiles and receives calls from the same. It has National Roaming facility. “Xplore-2” also gives the same facilities as “Xplore-1” with some additional value added service. Another difference is it gives ISD (International Standard Dialing) facilities. But as it is a post-paid connection so a subscriber has to deposit some security money and pay the bill with a flat line rent

Business Users

Business Solutions is a complete, quality business communications service from Grameenphone – designed especially for the business community in Bangladesh. The Business Solutions team provides the business users customized telecommunications solutions through consultation with them.

The newest attraction in Grameenphone’s Business Solutions portfolio is BlackBerry, a complete solution for the business users. BlackBerry smartphones enable users to access the proven BlackBerry wireless services with support of email, phone, internet, instant messaging, organizer and much more. This enables the business users to create a much needed balance between work and personal life. There are two different services depending on the need of the user:

BlackBerry Enterprise Service (BES) – Complete wireless solution for the enterprise:

BlackBerry Enterprise Service (BES) is a unique and totally integrated service that offers corporate mail integration, secure administration, advanced wireless devices, desktop tools and more. It ensures mobility of workplace by connecting the user to customers, colleagues, and information that drive business. Wireless connectivity allows the user to stay in touch with business contacts at both home and abroad.

BlackBerry Internet Service (BIS) – Complete wireless solution for individuals/professionals:

BlackBerry Internet Service (BIS) is the easiest and the most affordable way for individuals to start using BlackBerry smartphones. It is an out-of-the-box service which when integrated with ISP mail service, provides the user with seamless mobile extension to his/her existing email service.

Business Solutions offers services like – International roaming, Internet and data services, business news, business SMS, missed calls alert and many more. This allows business people to stay connected – At office or on the move.

Youth Segment Product – Djuice

Djuice is a niche prepaid Service designed specially for the youth segment. It was introduced as a Youth Product on ‘Pahela Boishakh’ in April 2005. The core target market of Djuice comprises of 19 to 26 years old youth having a socially active and outgoing lifestyle. Extensions of the core target group are the two secondary groups, 13 to 18 and 27 to 30 years old, people pursuing the same lifestyle benefits from their mobile subscription.

The vision of Djuice is to become an integrated part of youth life and help them get more out of it. The brand identity of Djuice in Bangladesh has been developed based on some core values such as Original, Entertaining, Trustworthy, Refreshing, Empathetic, Dynamic, Socially active and Challenging. The call rate of Djuice is low and has lower pulse to attract the young generation.

Djuice offers a unique range of value added services for its unique group of subscribers. XTRA Khatir, dDuniya, drockstar are some of those.

Rural Users – Village Phone Program

Commencing its operation in March 1997, the Village Phone Program is a unique initiative to provide telecommunications facilities in remote, rural areas. It has brought about a quiet revolution in mobile telephony in Bangladesh, by putting cell phones in the hands of the rural poor, many of them women, who had never seen a telephone before.

The Village Phones work as an owner-operated pay phone. It has created a good income-earning opportunity for the VP operators, mostly poor women who are borrower members of Grameen Bank. Typically, a member of Grameen Bank takes a loan to buy a handset and a GP subscription and she is trained by Grameen Telecom on how to operate it. As of today, there are more than 260,000 VP operators in over 50,000 villages in 439 Upazilas (sub-districts) of the country. Amongst GP subscribers, VP operators yielded the highest average revenue per month.

VPP has received many international awards while it has also been extensively featured in the international media over the years and documented by researchers both at home and abroad. It was given the “GSM in the Community Award” by the GSM Association at the GSM Congress in Cannes, France in February 2000. It also received the “Commonwealth Innovation Award” in 2003 and the “Petersburg Prize” awarded by the Gateway Foundation in 2005.

The Village Phone Program has also been replicated in a number of countries including Uganda and Rwanda in Africa.

SWOT Analysis

Description of Different Divisions and Departments

Currently Grameenphone has 11 divisions and 5 departments to run its operations smoothly. The divisions are:

- Customer Management Division

- Finance Division

- Information Technology Division

- Sales and Distribution Division

- Human Resource Division

- Fiber Optic Network Division

- Regulatory and Corporate Affairs Division

- Technical Division

- Projects Division

- New Business Division

- Marketing Division

The departments are independent from any divisions. The names of 5 departments are:

- Administration Department

- Revenue Assurance and Fraud Management Department

- Information Department

- Internal Audit Department

- Legal and Compliance Department

There are also two projects running under observation of Deputy Managing Director. The projects are independent of Projects division. These are, CHQ Project and Efficiency Project.

Among them the respective directors head ten divisions. Marketing division is headed by a deputy director. A General Manager heads Information Department. He has to report direct to the Managing Director. Head of supply chain management has to report directly to the director of Finance Division. This responsibility is added recently to the Director, Finance Division.

CUSTOMER MANAGEMENT DIVISION

Customer Relations Division is the bridge between the customers and the company. People here are always serving the clients. A total of 210 people in this division providing customer service are strengthening the relationship of GP with its valued customers. This division can be subdivided into three major parts-call center, billing department and trainee development department.

Call center responds to customers’ query. 150 to 190 people working in shifting basis in call center provide 24 hours service to the customers through telephones. They receive queries and complaints related to GP service and network, solve them, provide different types of information to the clients etc.

Billing department is mainly responsible for billing customers for the service and collecting the revenue from them. This department works with the help of its eight units. The units are distribution unit, general banking unit, bank reconciliation unit, bank communication unit, collection unit, credit recovery unit, fraud management unit and revenue assurance unit.

Trainee development department arranges all sorts of in-house and overseas training programs for the employees. Experts from within the GP family conduct in-house training programs. These programs include orientation for new employees, team-building workshops, customized training for the senior managers on management style, motivation, and project management and handling difficult situations. Many GP employees are sent to foreign countries for overseas training, workshops and seminars. All the organization and formalities concerning these programs are done through this department.

SALES & DISTRIBUTION DIVISION

Sales and distribution division has the opportunity to have direct interface with the customers. The number of employees working in this division is 1588. This division is subdivided into two part- sales department and distribution department. The responsibility of sales department is to sell the products and services of Grameenphone. Therefore they have to work in close collaboration with Marketing Division for their success in selling. They also need to keep good relationship with the sellers and also with customers. The responsibilities of the part or the distribution department includes instant delivery of products and services, maintaining relationship with dealers, serving the corporate clients with extra care, follow up existing subscribers and building relationship with new and existing subscribers. One of the most important tasks of sales department is sales-forecast.

INFORMATION TECHNOLOGY DIVISION

The Information Technology Division became a separate division in 2003. Till then it was under the wing of Personnel & Organization Division.

The IT Division comprises the following departments:

- Core Systems

- IT Operations

- Information Security

- Business Processes and Architecture

- Project and Change Management

The description of each department is given below.

Core Systems

- Development/integration of business critical systems

- Maintenance of business critical systems

IT Operations

- Access control, accessibility and stability for end- and IT-users

- Operations, planning of operations and monitoring

- Security

- Readiness

Information Security

- Design, develop and deploy a security infrastructure including intrusion detection, protection, assessment and management

- Publish, monitor and enforce information and computer security policies

- Supervise and/or conduct periodic security assessments

- Manage long-term projects to improve security posture and capabilities

Business Processes and Architecture

- Overall IT architecture

- Management of business process framework

- Business process modeling

- Exception handling

HUMAN RESOURCES DIVISION

Human resource department plays a very important role in the functioning of the organization. The main tasks of this department are employee recruitment, selection, transfer, promotion, training, performance appraisal, manpower planning etc. Different divisions send theirpersonnel requirement to HR department. Then HRD sets target, prepare recruitment planning and go for the recruitment process. When an employee is recruited a separate employee file is opened comprising of all information of the particular employee which is regularly upgraded by HRD. This department is also responsible for performance appraisal, manpower planning etc. Different divisions send their personnel requirement to HR department. Then HRD sets target, prepare recruitment planning and go for the recruitment process. When an employee is recruited a separate employee file is opened comprising of all information of the particular employee which is regularly upgraded by HRD. This department is also responsible for performance appraisal of employees that is very important for the confirmation, increment, promotion, transfer of employees. This is done through job analysis, setting up of performance standard and appraisal interview.

REGULATORY & CORP. AFFAIRS DIVISION

This division looks after the regulatory and interconnection issues. It is responsible for maintaining close relationship with BTRC, MOPT, PSTN operators and mobile operators for matters related to interconnection with fixed and mobile operators, and interconnection & Revenue Sharing Agreement.

This division is also responsible for maintaining relationships with Ministries, the National Parliamentary Telecom Committee, Government agencies like the Board of Investment (BOI), the National Board of Revenue (NBR), and law-enforcing agencies.

TECHNICAL DIVISION

The Technical Division can be considered as the brain of this organization. This division has the highest number of employees, which are 1077 at present. This division is split into three departments- planning department, implementation department and operations department. People working in planning department build the technology while people working in operations department maintain the technology. Implementation is between the two. Most of the people in the technical division are from the engineering and technological educational background.

People in planning department are responsible for planning the network and equipment, taking decision about new expansion, enhancement and up-gradation and closely monitoring network performance. They are also engaged with BSC (Base Station Controller) and MSC (Mobile Switch center) related planning, timely supply of equipment, making roaming agreements with other countries and negotiating with home owners for building base stations on the roofs. This department has three parts: switch planning, radio planning and transmission planning.

The people of implementation department are responsible for the construction and acquisition of base station room, antenna pipe, and power supply etc., installation of new base station hardware, start-up and pilot operation of base station. It is also divided to three units: site acquisition, civil works and roll-out.

Operations department is responsible for smooth operations and maintenance of the network. Their main tasks are operation, maintenance and overall management of the networks, fault detection and fault handling of networks. This department always closely monitors the network performance.

FIBER OPTIC NETWORK DIVISION

The Fiber Optic Network (FON) Division is a full-fledged Division under Deputy Managing Director. It manages the nationwide Fiber Optic Network, and to create and sell the Transmission Capacity commercially to prospective business units/clients. The division shares use of FON capacity with third parties such as other telecom operators, ISP’s DDN service provider etc. Grameenphone is capable of offering point to point full E1 connectivity within GP Transmission Network for their sub-lease clients.

MARKETING DIVISION

Marketing is responsible for all types of Product development and launch, Branding and communication, International Roaming, Value Added Services and all types of Research activities. The Division comprises the following departments: Product and Market Development Department (PMD), Market Research and Planning Department (MRP), Market Communications Department, Brand Development and Management Department International Business Department, Value Added Services Department.

The Product and Market development Department includes Products & Prices Section (Business Solution, Djuice and, Mass), New Product development and Innovation lab, and Forecasting and Analysis Section. Market Research and Planning Department includes Segmentation, Research & Planning Section and Market Intelligence – acting as a central research point for Grameenphone. The International Business Department is involved in international roaming services while the Value Added Services Department includes Service Development and Management Section, Content Provider / Aggregator Management Section, CPA/CSF Platform Section and Advanced Services section. The Market Communication Department deals with media management, event management and regional marketing.

PROJECTS DIVISION

The responsibility of projects division is to manage the process of initializing, prioritization, monitoring of execution of all major change request (projects). This division is responsible for overall performance, measure and report of IT in delivering project-based services. This division develops, maintains, and evolves standards, tools, templates, and documented processes for project management within IT. Another responsibility of this division is to develop tools to assess the effectiveness of project management efforts within IT. This division gathers project information and maintains a list of current project activity for IT including project timeframes and resource utilization.

NEW BUSINESS DIVISION

New business is the newest division in the Grameenphone Ltd. Mr. Kafil H.S. Muyeed is the director of this division. To seek new business opportunity in the telecommunication industry is the main objective of this department.

ADMINISTRATION DEPARTMENT

This department headed by an AGM has three units. They are office, security and transport. The office unit looks after the furniture and general maintenance of the office premises. The security unit is responsible for managing the security of office, TBS, switches and BTS. The transport unit determines the transport routes; transport related costs and hires cars and microbuses for GP officials.

REVENUE ASSURANCE & FRAUD MANAGEMENT DEPARTMENT

Revenue Assurance and Fraud Management (RAFM) function in Grameenphone is responsible to stop revenue leakage in any form (intentional & unintentional) across the complete business chain (Internal & External). RAFM focus includes core business processes, support processes, systems, people and organizations involved with GP business in any form. RAFM as a principle, highly emphasize on cross functional cooperation based on smart & effective processes.

INTERNAL AUDIT DEPARTMENT

This department, with a direct reporting to the Managing Director, is responsible for monitoring the activities in the light of policies or procedures set by the Board of Directors and/or the Management Team. In addition, this unit has to follow the Group Internal Auditing Guideline as a part of subsidiary of Telenor Mobile. On the basis of reports of the Internal Auditor, actions are taken to bring about developments and rectifications of systems or policies and procedures.

LEGAL AND COMPLIANCE DEPARTMENT

This is a one unit department whose major functions comprise as follows:

- To ensure sufficient legal coverage and minimum exposure to risk

- To establish high standards of corporate governance

- To build GP’s image as a compliant organization both among its customers its other stakeholders.

INFORMATION DEPARTMENT

Information department is managing the efficient flow of information. It is responsible to manage the relationship with media and newspapers, publish news bulletins regarding different events of the company. It is also publishes monthly newsletters of GP. It also publishes the GP Annual Report. It determines the contents of Grameenphone websites and Grameenphone@work intranet site.

Industry Overview

Telecom Industry in Bangladesh

The telecommunication sector in Bangladesh is poised for rapid growth in the coming years. The concept of mobile telephone has become largely familiar and phenomenal in Bangladesh from the early 90s. The sector, particularly which of mobile phones, is one of the fastest growing areas of the economy. The growth potentials will continue to remain robust for the foreseeable future.

There are six mobile telephone operators in Bangladesh at the moment. Among them one is Government owned telephone operator: Bangladesh Telegraph and Telephone Board (BTTB) and the other five are privately owned companies namely Grameenphone Ltd., Telecom Malaysia International Bangladesh (TMIB), Orascom Telecom Bangladesh Ltd., Pacific Bangladesh Telecom Ltd. (PBTL) and Warid Telecom Bangladesh Ltd.

Grameenphone Limited

Grameenphone Ltd. is the market leader in the telecommunication sector in Bangladesh. It is a joint venture of four different companies in four different countries. Starting operating from 26th March, 1997, Grameenphone Ltd. has recently completed its 11th year of dominant present in the market. It is now able to say that it has the largest network, the widest coverage, the biggest subscriber base and more value added services than any other mobile phone operators in Bangladesh. GP has a very strong competitive position in the telephone industry in the country.

Orascom Telecom Bangladesh Limited (Banglalink)

Banglalink was previously known as Sheba Telecom which began operation in 1998. It was a joint venture between a Malaysian Conglomerate, Technology Resources Industries Berhad and a local firm named Integrated Services Ltd. (ISL). In 2005 Orascom Telecom Holding (OTH) acquired Sheba Telecom and gave a new trading name ‘Banglalink’.

When banglalink entered the Bangladesh telecom industry in February 2005, the scenario changed overnight with mobile telephony becoming an extremely useful and affordable communication tool for people across all segments. Within one year of operation, banglalink became the fastest growing mobile operator of the country with a growth rate of 257%. This milestone was achieved with innovative and attractive products and services targeting the different market segments; aggressive improvement of network quality and dedicated customer care; and effective communication that emotionally connected customers with banglalink. At present it is holding the 2nd position in the cell- phone industry with respect to market share.

Telecom Malaysia International Bangladesh (Aktel)

Telecom Malaysia International Bangladesh (TMIB) commenced their venture in 1997, the same year when Grameenphone inaugurated its business. TMIB is a joint venture between Telecom Malaysia and A. K. Khan and Co. The company used GSM network technology and its brand name is Aktel. It has now become the third largest mobile phone operator in Bangladesh in terms of revenue and subscribers (7.57 million as of April, 2008) unable to hold its 2nd position due to fierce competition from Banglalink. AKTEL has the widest international roaming service in the market, connecting 315 operators across 170 countries. It is the first operator in the country to introduce GPRS to its subscribers

Warid Telecom Bangladesh Ltd.

Warid Telecom Bangladesh Limited is a GSM-based cellular operator in Bangladesh. It is the sixed mobile phone carrier to enter the Bangladesh market. It is wholly owned subsidiary of Warid Telecom International LLC which is the part of The Dabi Group based in the UAE.

In May 10th, 2007, Warid Telecom launched its commercial operations in Bangladesh with a network encompassing 26 districts. By November 2007, the network had been expanded to cover 61 districts and being used by 2 million customers. Based on the NGN (Next-Generation) network, Warid Telecom’s operational activities in Bangladesh aim to achieve a new and modern corporate identity, which is congruent with the dynamic changes taking place in the telecom industry today. With a reflection of a new strategy, Warid aim to be perceived not only as a telecommunication operator of voice services, but also as a universal provider of comprehensive communications services for both residential and business customers.

Pacific Bangladesh Telecom Limited (Citycell)

Among the other four mobile phone operating companies who are running their businesses in the private sector, Pacific Bangladesh Telecom Ltd. (PBTL) is the pioneer. In 1990 Hutchison Bangladesh Telecom Ltd. was formed as a joint venture of Bangladesh Telecom Ltd. (BTL) and Hutchison Whampoa of Hong Kong. The company began their operations as the analog cellular operator using the CDMA technology in 1993. In 1996 this company was renamed as pacific Bangladesh Telecom Ltd. (PBTL) with brand name of Citycell. At present the ownership of PBTL belongs to the Pacific Telecom Ltd. a concern of the Pacific Group and Hutchison Whampoa Ltd. a Hong Kong based diversified multinational conglomerate.

Teletalk Bangladesh Limited

Teletalk Bangladesh Limited is a public limited company owned by Bangladesh Telegraph and Telephone Board (BTTB) in other words by the Government of the Peoples Republic of Bangladesh. It was incorporated on 26 December, 2004 being the only government sponsored mobile telephone company in the country. Teletalk Bangladesh limited was established keeping a specific role in mind. It has forged ahead and strengthened its path over the years and achieved some feats truly to be proud of, as the only Bangladeshi mobile operator and the only operator with 100% native technical and engineering human resource base, Teletalk thrives to become the true people’s phone – “Amader Phone”.

Market Scenario

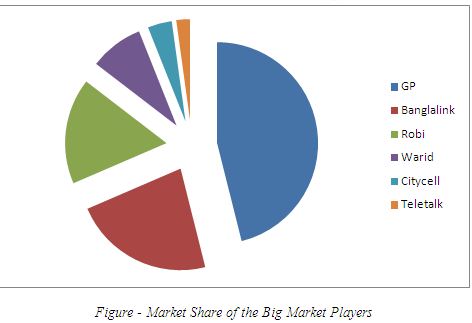

Telco industry in Bangladesh is intensely competitive. According to Bangladesh Telecommunication Regulatory Commission (BTRC) the total number of subscribers in the telecom industry of Bangladesh is 40.34 million as of April, 2008.

Table – Subscriber base of the Mobile Operators in Bangladesh

| Telecom Operator | Subscribers (in millions) |

GP | 20.82 |

| Banglalink | 10.14 |

| Robi | 7.63 |

| Warid | 3.86 |

| Citycell | 1.74 |

| Teletalk | 0.99 |

Source – Bangladesh Telecommunication Regulatory Commission (BRTC)

Figure– Subscriber base of the Mobile Operators in Bangladesh

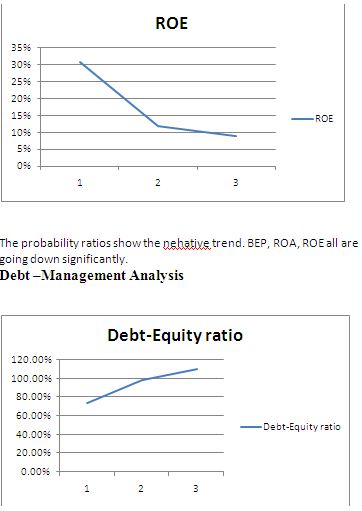

From illustration 2.1 and 2.2 it can be clearly seen that Grameenphone Ltd. dominates the market with a subscriber base of 18.60 million having 46.12% market share. Its nearest competitor is Banglalink with a subscriber base of 6.64 million and 21.42% market share, closely followed by Aktel. Other three players are Warid, Citycell and Teletalk. Among its competitors Banglalink and Warid pose the greatest threat. Banglalink is turning out to be the fastest growing mobile operator where as the growth of Warid is also threatening. All this players together make the telecom market very competitive in nature.

Industry Analysis

Although Grameenphone dominates the market with around 46% of market share, the nature of the industry is oligopolistic in nature. It is characterized by price transparency, very little product differentiation and intense competition in the market. For a competitive environment analysis, Porter’s 5 forces model is most useful.

Porter’s 5 Forces Model

Competitive Rivalry

The mobile telecom industry is fiercely competitive. Even a few years back the industry was not as robust as it is now. Initially, Citycell enjoyed total monopoly in this sector. After the entry of Grameenphone and Aktel, the industry condition changed. Citycell lost its place as a monopoly player as Grameenphone took over most of the market share and Aktel took the second position.

The scenario further changed with the entry of Orascom Telecom, the mobile giant from the Middle East. They entered the market by acquiring 100% shares of Sheba Telecom and re-launching the brand as Banglalink. Aggressive marketing and promotion were one of their main entry strategies and it worked. The airtime rates and connection prices came down because of the competition. This was an awakening call for the other operators. Grameenphone and Aktel, who were quietly enjoying their market positions, suddenly became aggressive as well. There was a huge increase in promotional activities of all mobile operators. The prices also started climbing downhill.

Companies focused on segment marketing as well as mass marketing. GP launched its youth brand Djuice to cater to the needs of young generation. Citycell came up with their Aalap Super and Aalap Super Plus providing free airtime whole night. Aktel also came up with new offers like Aktel JOY that catered to the need of couples. Overall, the industry became a hubbub of activities.

Threat of New Entrants

Although the industry is fiercely competitive, the overall mobile penetration rate is only 21.66% of the whole population. This huge untapped market makes the sector quite lucrative for big investors. Foreign investors are quite keen in investing in this segment. Infact, all the current players are either partially or fully foreign owned – 62% of Grameenphone is owned by Telenor from Norway; Telecom Malaysia owns around 70% of Aktel and Banglalink is 100% owned by Egyptian Orascom Telecom. Singapore Telecom (Singtel) has entered the market by acquiring 45% share in Pacific Bangladesh Telecom. Warid Telecom of Abu Dhabi has got the license and has already started their operation. And now the US giant Vodafone is investing in the mobile telecom sector of Bangladesh by acquiring significant share of Aktel.

This plethora of foreign investors shows that the threat of new entrants is very high. However, the barrier to entry and exit are also high. High setup cost and high level of sunk cost acts as a screening for small investors from crowding the sector.

Threat of Substitutes

Mobile industry is a technology based industry and like any other technology has the danger of becoming obsolete by new technology. Thus, the threat of potential substitutes is always there.

Currently, the biggest substitute of mobiles is land phone. The land phone market, until very recently, had been a government monopoly. Private land phone licenses were issued in 2005 and the PSTN (land phone) companies are yet to capture a significant portion of the market. Moreover, it was found that people keep mobile phones even if they have land phone connection. Thus, the threat from land phones is not that high.

Another threat to the mobile phone industry is the expansion of broadband technology. People, especially youngsters, are finding it cheaper to chat online with their friends rather than talking. Broadband provides with quite a few advantages over mobile phones: chance to communicate with more than one person, cheaper rate are a few examples. However, lack of proper infrastructure is acting as a barrier to expansion of broadband countrywide. Thus, it is yet to materialize as a real threat to the mobile industry.

Bargaining Power of Suppliers

The bargaining power of suppliers is moderate in this industry. Since the number of mobile phone companies are limited the suppliers cannot switch frequently or pressurize the buyers. On the other hand suppliers like Ericsson, Nokia, Siemens and Motorola are pretty big player themselves and have specialized sales units. Thus, there was always a good understanding between the suppliers and buyers. This situation is now tipped a little bit in the favor of the mobile phone companies by the entry of the Chinese company Huawei. They are offering to supply at lower rates than the previous suppliers. As a result, companies now have the option to go for cheaper suppliers.

Bargaining Power of Buyers

Initially, the mobile market was a sellers market. When Pacific Telecom first introduced their brand Citycell, the startup connection used to sell for more than Tk.100,000. The airtime was over Tk.16 per minute. However, with the increase in competition, buyers gained more power. Currently, it is now a market mainly dominated by buyers. The prices have come down a lot. The low level of product differentiation and very low cost of startup connections have led the buyers to switch operators very frequently. Companies are undertaking various promotional and product strategies to reduce churn.

The middlemen played a major role in the determining the buyer power. Previously all the companies used external dealers to ensure the smooth flow of their distribution. The commission paid to dealers was very high. However, the dealers paid a very low level of commission to retailers, thus controlling the market to a great extent. Grameenphone is the first company to deal with this situation. They have started their own distribution network. This has not only reduced cost in the form of dealer commission but also increased satisfaction of retailers. Thus, in a market with strong buyer power, a self-owned distribution network can only help GP in maintaining its market leader position.

The investment policy of Grameenphone Ltd.

Overview of Finance Division

The Finance Division holds 330 employees in its various departments. The Division encompasses all financial activities – both internal and external. The purpose of each of the activities is given as follows:

Financial Statement Analysis

- Business plan

- Strategic plan

- Budgeting

- Product profitability analysis

- Statistical analysis-financial

- Revenue analysis

- Telenor quarterly review

- Adhoc reporting to board, Telenor management and other related parties

- Presentation- company, BM, OCM and related parties

Investment Control

- Review new investment proposal as project or programs

- Prepare business case

- Advice management and investment committee

- Re-rank the investment options

Financial Control

- Implementation of IFRS in preparing the financial statements

- Maintain and develop internal control structure aiming at the Sarbanes Oxley Act 2002 (Section 404)

- Check compliance of financial and procurement policies

- Compliance with tax related issues

- Review policies and procedure in place and pass suggestion for continuous improvement

Strategy and Training

- Develop and follow-up strategy of Finance Division

- Coordinate recruitments in Finance Division

- Coordinate training for Finance Division employees

- Follow-up IVC of Finance Division

Payroll and Taxation

- Payroll management

- Corporate tax management

- VAT management

- Board of Investment (BOI), Bangladesh Bank and others regulatory affairs

Capital Market

- Coordinate overall financing function

- Ensure and monitor compliance to the financing agreement

- Responsible to lender, Telenor and Bangladesh Bank related to financing issues

- Liaison with foreign lenders, sponsors, bankers and regulators

Reporting & Accounting & System Administration

- Financial reporting to Management, Telenor, OCM and Board

- Financial and management accounting- actual and budget

- Budgeting (preparation/implementation/monitoring)

Assets and Insurance

- Asset addition

- Capitalization WIP

- Land and land advance

- Insurance – fire and business interruption

International Settlement & Insurance

- Letter of Credit for all imports

- Leasing, insurance and contracts

- International roaming and receivables, payables and invoicing

- All foreign payment and employee foreign travel and training payments and advances

Treasury

- Fund management

- Cash rolling forecast

- Local payments

- Bank reconciliations

- Employee gratuity and provident fund

Revenue Accounting

- Collection of prepaid, post-paid and international roaming bill from subscribers

- Recognition of prepaid, post paid revenue and revenue from all sub leases

- Reconciliation of all collections

- Handset payment management

- Banking arrangement for collection

- Costing of inventories

- Invoicing to subleases and collection

- Participation in revenue assurance activities

Gr ameenphone Ltd. Invest their money for two purposes-

- 1.To extend their business

- 2.Invest in banks to get profit.

Investment for business extension:

Base Station

Grameenphone has almost 12000 base stations through out the country. They have to invest huge amount of money to set up a base station. The expenses include : purchase of land and the cost of equipments. They incur this cost only when they find a potential market of subscribers, basically based on the population and probable mobile users.

Fixed Asset purchase

Grameenphone has huge amount of fixed asset in different offices of them and they have a certain department for fixed asset management. Grameenphone invests huge amount of money to buy this fixed assets.

Customer care opening

Grameenphone has established around 500 grameenphone centres(GPC) and many other GPSD where curtomers get gets direct services from GP. GP invests lot of money to establish such customer cares to facile their customers.

Investing in banks:

Grameeen invest in different locally operating banks.Like;UCB,EBL,One BANK,AB BANK,NATIONAL BANK LTD, DUTCH BANGLA BANK,STANDARD CHARTERED BANK, HSBC BANK, SOUTH EAST BANK ETC. Out of all these let me explain how do they make their investment decision???

They do sort of research and analysis before making their investment. What they consider for their invest are as follows:

Interest rate

When investing money in any bank grameenphone always do severe analysis regarding interest rate provided by different banks and even they get customized interest rate proposal from banks.

Stability of the bank

Before making the investment GP considers which bank is more stable. They check their financial statements and credit rating report. They do it to forecast whether bank will be able to repay them according to the condition.

Financial status of the bank

GP always check the financial summery of the banks before making their investment decisions. They check what was the financial performance in last few years of the bank. They also see what is probablity that a certain bank will go bankrupt.

The City Bank Ltd.

City Bank is one of the oldest private Commercial Banks operating in Bangladesh. It is a top bank among the oldest five Commercial Banks in the country which started their operations in 1983. The Bank started its journey on 27th March 1983 through opening its first branch at B. B. Avenue Branch in the capital, Dhaka city. It was the visionary entrepreneurship of around 13 local businessmen who braved the immense uncertainties and risks with courage and zeal that made the establishment & forward march of the bank possible. Those sponsor directors commenced the journey with only Taka 3.4 crore worth of Capital, which now is a respectable Taka 330.77 crore as capital & reserve.

City Bank is among the very few local banks which do not follow the traditional, decentralized, geographically managed, branch based business or profit model. Instead the bank manages its business and operation vertically from the head office through 4 distinct business divisions namely

- Corporate & Investment Banking;

- Retail Banking (including Cards);

- SME Banking; &

- Treasury & Market Risks.

Under a real-time online banking platform, these 4 business divisions are supported at the back by a robust service delivery or operations setup and also a smart IT Backbone. Such centralized business segment based business & operating model ensure specialized treatment and services to the bank’s different customer segments.

The bank currently has 87 online branches and 10 SME service centers spread across the length & breadth of the country that include a full fledged Islami Banking branch. Besides these traditional delivery points, the bank is also very active in the alternative delivery area. It currently has 46 ATMs of its own; and ATM sharing arrangement with a partner bank that has more than 550 ATMs in place; SMS Banking; Interest Banking and so on. It already started its Customer Call Center operation. The bank has a plan to end the current year with 100 own ATMs.

City Bank is the first bank in Bangladesh to have issued Dual Currency Credit Card. The bank is a principal member of VISA international and it issues both Local Currency (Taka) & Foreign Currency (US Dollar) card limits in a single plastic. VISA Debit Card is another popular product which the bank is pushing hard in order to ease out the queues at the branch created by its astounding base of some 400,000 retail customers. The launch of VISA Prepaid Card for the travel sector is currently underway.

City Bank has launched American Express Credit Card and American Express Gold Credit card in November 2009. City Bank is the local caretaker of the brand and is responsible for all operations supporting the issuing of the new credit cards, including billing and accounting, customer service, credit management and charge authorizations, as well as marketing the cards in Bangladesh. Both cards are international cards and accepted by the millions of merchants operating on the American Express global merchant network in over 200 countries and territories including Bangladesh. City Bank also introduced exclusive privileges for the card members under the American Express Selects program in Bangladesh. This will entitled any American Express card members to enjoy fantastic savings on retail and dining at some of the finest establishment in Bangladesh. It also provides incredible privileges all over the globe with more than 13,000 offers at over 10,000 merchants in 75 countries.

City Bank prides itself in offering a very personalized and friendly customer service. It has in place a customized service excellence model called CRP that focuses on ensuring happy customers through setting benchmarks for the bank’s employees’ attitude, behavior, readiness level, accuracy and timelines of service quality.

Financial summary:

| Operating performance ratio |

2005 |

2006 |

2007 |

2008 |

2009 |

| credit deposit ratio | 76.11% | 75.31% | 66.08% | 76.43% | 69.71% |

| cost to income ratio | 40.81% | 43.60% | 51.17% | 48.08% | 48.36% |

| total operating income per employee | 1.15 m | 1.33 m | 1.29 m | 1.58 m | 1.80 m |

| operting profit per employee | 0.66 m | 0.75 m | 0.63 m | 0.82 m | 0.93 m |

| cost of funds | 5.34% | 6.94% | 7.55% | 6.90% | 6.08% |

| yield on loans and advance | 12.67% | 13.30% | 13.15% | 13.50% | 13.07% |

| return on asset | 1.75% | 0.58% | 0.71% | 0.75% | 1.23% |

| return on equity | 32.05% | 10.69% | 12.71% | 11.23% | 16.24% |

| Fixed Deposit | ||

| 1 (one) month | 4.00 | |

| 3 (Three) months | 8.00 | |

| 6 (Six) months | 8.00 | |

| 01 (One) year | ||

| – Below Tk. 50.00 Crore | 8.00 | |

| – Tk. 50.00 Crore & above | 8.00 | |

| 02 (Two) & 03 (Three) years | 8.00 | |

| 01(One) year City Nokshi | 7.00 | |

Rating Report The City Bank Ltd.

Credit Rating Agency of Bangladesh (CRAB) limited has upgraded the long term rating of the city bank ltd to A1 and retained short term rating to ST-2 CRAB performed the rating surveillance based on financial statements upto 31st december 2009 and other relevant information.

Commercial bank rated ‘A1’ have strong capacity to meet their financial commitments but are somewhat more susceptible to the adverse effects of change in circumstances and economic conditions than commercial banks in higher rated categories. A1 is judged to be of high quality and are subject to low credit risk.

Commercial banks rated ST-2 are considered to have strong capacity for timely repayment . Commercial banks rated in this category are characterized with commendable position in terms of liquidity, internal fund generation, and access to alternative sources of funds.

CBL as one of the first generation private commercial banks has a large branch network of 88 branches and 10 SME centers. The revenue of the bank reasonably diversified having 47.41% revenue from net interest income which has a growth of 37.46% in 2009. On the other hand, 30.34% revenue was generated from investment income and 16.42% from commission, exchange and brokerage income.

National Bank Ltd.

National Bank Limited is one of the leading private commercial bank having a spread network of 121 branches and 10 SME centers across Bangladesh and plans to open few more branches to cover the important commercial areas in Dhaka, Chittagong, Sylhet and other areas in 2009.

National Bank Limited has been licensed by the Government of Bangladesh as a Scheduled commercial bank in the private sector in pursuance of the policy of liberalisation of banking and financial services and facilities in Bangladesh. In view of the above, the Bank within a period of 25 years of its operation achieved a remarkable success and met up capital adequacy requirement of Bangladesh Bank.

National Bank Limited is a customer oriented financial institution. It remains dedicated to meet up with the ever growing expectations of the customer because at National Bank, customer is always at the center.

Financial Summary

| credit deposit ratio | 81.92% | 81.06% | 76.05% | 84.18% | 84.76% |

| cost of funds | 5.31% | 6.15% | 6.35% | 6.76% | 6.45% |

| yield on loans and advance | 9.15% | 11.53% | 11.46% | 12.65% | 11.42% |

| return on asset | 0.74% | 1.19% | 2.40% | 2.36% | 2.52% |

| return on equity | 11.82% | 16.89% | 31.57% | 28.38% | 27.53% |

| EPS | 43.85 | 63.01 | 66.11 | 53.31 | 72.74 |

| Net Asset Value per share | 441.36 | 406.50 | 378.12 | 327.13 | 313.25 |

| Capital Adequecy | 10.45% | 10.10% | 13.11% | 13.42% | 13.56% |

Rating Report National Bank Ltd

Credit Rating Agency of Bangladesh (CRAB) ltd. Has affirmed A1 rating in the long term and ST-2 rating in the short term to National bank Ltd based on audited financials as at 31st December 2009 and other relevant information.

Commercial banks rated in the long term A1 belong to ‘strong capacity and high quality’ cohort. Banks rated ‘A1’ have strong capacity to meet their financial commitments but are somewhat more susceptible to the adverse effects of change in circumstances and economic conditions. A1 is judged to be of high quality and is subject to low credit risk.

Commercial banks rated in the short term ‘ST-2’ category are considered to have the strong capacity for timely repayment of obligations. Banks rated in this category are characterized with commendable position in terms of liquidity, internal fund generation, and access to alternative sources of funds.

National bank Ltd one of the first generation private sector banks in Bangladesh, commenced its commercial operations from March 1983 with paid up capital of BDT 44.oo million. Banks paid up capital as of 31 December 2009 stood at BDT 2,846.54 million. NBL offers both corporate and retail banking services with a strong trade finance focus. NBL had wide range of branch network across the country with 121 branches and 10 SME service centres in 2009.

Net interest income of NBL dominated the revenue stream in 2009 with 37% of total income (2008: 41%) followed by investment income (27%) and commission & exchange (22%). Higher investment income helped the bank to offset the lower growth in interest income in 2009. NBL’s cost to income ratio shot up by 6.93 percentage points and stood at 47.96% resulted from higher expenses in branch expansion and automation as well as higher staff cost.

All the profitability ratios (before tax) of the bank dropped in 2009 after having an increasing trend in the last few years. NBL’s return on average assets (ROAA) before tax in 2009 reduced by 0.52 percentage points resulted from reduced net profit margin whereas ROAA after tax in 2009 increased marginally by 0.14 percentage points on the back of lower tax rate as well as income from offshore unit. Net interest margin (NIM) also reduced by 0.79 percentage points in 2009.

The bank was mainly funded by customer deposit and internal capital generation. About 29% of total deposits of the bank comprised current and savings deposits. In 2009, advances to deposit ratio of the bank was 81.34% (monthly average). The bank was the net lender to the call money market throughout in 2009.

NBL experienced substantial growth (28.22%) in loans and advances portfolio considering the industry scenario and reached BDT 64,962.31 million by the end of 2009. But higher loan growth may deteriorate loan quality in future. The bank’s credit portfolio was reasonably diversified in terms of intrinsic and concentration risk. However, NBL’s top 50 funded loans hold 30.13% of total loan portfolio.

NBL’s total non-performing loans (NPL) increased to BDT 3880.30 million and gross NPL ratio also increased to 5.97% in 2009 (2008: 5.50%) resulted from fresh NPL generation of BDT 2,470.50 million. The bank also wrote off BDT 974.1 BDT million in 2009. However, special mention accounts (SMA) to total loans & advances ratio of the Bank reduced to 1% in 2009 (2008: 1.93%).

The bank was reasonably capitalised in terms of capital adequacy ratio (13.56%) by the end of 2009 against regulatory requirement 10%. However, this ratio was 8.61% under Basel II which was running parallel of Basel I in 2009.

NBL has its strength in liquidity position and capital generation. On the other hand, principal concern of the bank is higher growth in non performing loans.

AB Bank Ltd.

AB Bank Limited, the first private sector bank was incorporated in Bangladesh on 31st December 1981 as Arab Bangladesh Bank Limited and started its operation with effect from April 12, 1982.

AB Bank is known as one of leading bank of the country since its commencement 28 years ago. It continues to remain updated with the latest products and services, considering consumer and client perspectives. AB Bank has thus been able to keep their consumer’s and client’s trust while upholding their reliability, across time.

During the last 28 years, AB Bank Limited has opened 77 Branches in different Business Centers of the country, one foreign Branch in Mumbai, India and also established a wholly owned Subsidiary Finance Company in Hong Kong in the name of AB International Finance Limited. To facilitate cross border trade and payment related services, the Bank has correspondent relationship with over 220 international banks of repute across 58 countries of the World.

In spite of adverse market conditions, AB Bank Limited which turned 28 this year, concluded the 2008 financial year with good results. The Bank’s consolidated profit after taxes amounted to Taka 230 cr which is 21% higher than that of 2007. The asset base of AB grew by 32% from 2007 to stand at over Tk 8,400 cr as at the end of 2008.

The Bank showed strong growth in loans and deposits. Deposit of the Bank rose by Tk. 1518 cr ie., 28.45% while the diversified Loan Portfolio grew by over 30% during the year and recorded a Tk 1579 cr increase. Foreign Trade Business handled was Tk 9,898 cr indicating a growth of over 40% in 2008.

The Bank maintained its sound credit rating in 2008 to that of the previous year. The Credit Rating Agency of Bangladesh Limited (CRAB) awarded the Bank an A1 rating in the long term and ST-2 rating in the short Term.

AB Bank believes in modernization. The bank took a conscious decision to rejuvenate its past identity – an identity that the bank carried as Arab Bangladesh Bank Limited for twenty five long years. As a result of this decision, the bank chose to rename itself as AB Bank Limited and the Bangladesh Bank put its affirmative stamp on November 14, 2007.

The Bank decided to change its traditional color and logo to bring about a fresh approach in the financial world; an approach, which like its new logo is based on bonding, and trust. The bank has developed its logo considering the contemporary time. The new logo represents our cultural “Sheetal pati” as it reflects the bonding with its clientele and fulfilling their every need. Thus the new spirit of AB is “Bonding”. The Logo of the bank is primarily “red”, as red represents velocity of speed and purity. Our new logo innovates, bonding of affiliates that generate changes considering its customer demand. AB Bank launched the new Logo on its 25th Anniversary year.

AB Bank commits to nation to take a lead in the Banking sector through not only its strong financial position, but also through innovation of products and services. It also ensures creating higher value for its respected customers and shareholders. The bank has focused to bring services at the doorstep of its customers, and to bring millions into banking channels those who are outside the mainstream banking arena. Innovative products and services were introduced in the field of Small and Medium Enterprise (SME) credit, Women’s Entrepreneur, Consumer Loans, Debit and Credit Cards (Local & International), ATMs, Internet and SMS Banking, Remittance Services, Treasury Products and Services, Structured Finance for Corporate, strengthening and expanding its Islamic Banking activities, Investment Banking, specialized products and services for NRBs, Priority Banking, and Customer Care. The Bank has successfully completed its automation project in mid 2008. It envisages enabling customers to get banking services within the comfort of their homes and offices.

AB Bank has continuously invests into its biggest asset, the human resource to drive forward with its mission “to be the best performing bank in the country.” The bank has introduced Dress Code for its employees. Male employees wear designed ties and females wear Sharee or Salwar Kamiz, all the dresses are consisted with the unique AB Bank logo. AB is recognized as the people’s choice, catering to the satisfaction of its cliental. Their satisfaction is AB’s success.

Financial Summary

| Return on asset | 0.50% | 1.31% | 3.41% | 3.12% | 3.52% |

| return on equity | 11.73% | 20.61% | 42.19% | 40.96% | 40.01% |

| cost of fund | 8.60% | 10.04% | 10.54% | 11.09% | 10.31% |

| Eps | 6.34 | 20.75 | 74.23 | 89.72 | 131.13 |

| Capital adequecy ratio | 9.17% | 9.23% | 10.75% | 12.84% | 13.78% |

| Net asset value per share | 294 | 452 | 607 | 301 | 393 |

Rating Report AB Bank Limited

Credit rating agency of Bangladesh limited has affirmed AA3 rating in the long term and ST-1 rating in the short term of AB bank Ltd. Based on audited financial of 31 dec,2009 and other relevant information.

Commercial Banks rate AA3 in the long term belong to “very strong capacity and very high quality” cohort. Banks rate “ AA3” have very strong capacity to meet their financial commitments. AA3 rated banks are judged to be of high quality and are subject to low credit risk.

Commercial Banks rated in the short term “ST-1” category are considered to have highest capacity for timely repayment of obligations. Commercial banks rated in this category are characterized with excellent position in terms of liquidity, internal fund generation, and access to alternative sources of funds.

AB bank Ltd, first private sector bank of the country commenced its operation on april 12,1982 and presently the bank has 77 branches and 11 SME business centers across the country. The paid up capital of the bank reached BDT2564.25 million as of 31st December 2009 against the authorized capital of BDT6000 million.

CRAB assigned AA3 in the long term to AB bank Ltd. Considering year on year high profit growth ( profit after tax reached BDT 3,362.56 million in 2009 from BDT 2,300.62 million in 2008, registering a growth of46.16%); high asset growth, improvement in asset quality (gross NPL reduced to 2.75% in2009 from 2.99% in 2008) and adequate liquidity.

The revenue stream of the Bank was diversified having 35% revenue from both net interest income and investment income followed by income from commission & exchanges (in 2009: 22% of total operating income). The higher growth of the major contributing sector (interest income and investment income) helped the bank achieve a high growth of net interest income as well as operating income. The Bank managed to reduce its cost to income ratio by 0.27 percentage points on the back of higher growth of operating income.

In 2009, the Return on Average Asset (ROAA) increased by 0.40 percentage points whereas Return on Average Equity (ROAE) decreased by 0.95 percentage points. Net interest margin (NIM) of the Bank increased to 4.30% in 2009 compared to 3.93% in 2008. ABBL’s after tax return on average risk weighted asset (RWA) also witnessed an upsurge in 2009.

The Bank is mainly funded by customer deposit. Current and savings deposit accounted for 44% of total deposits in 2009 (2008: 32%) which reflect the stable deposit base of the Bank and helped the Bank to reduce its cost of deposit and borrowing from 8.40% to 7.63% in 2009. AB Bank maintained satisfactory liquidity position in 2009. Average loans to deposit ratio of the Bank was 82.22%. The Bank was net borrower in the call market throughout the year.

AB Bank experienced a reasonable growth (24.99%) in loans and advances and reached BDT 70,879.93 million by the end of 2009. The Bank’s loan portfolio was reasonably diversified in terms of intrinsic and concentration risk. The Bank’s top 50 funded loans in 2009 held 24.55% of total loan portfolio.

The overall asset quality trend of the Bank shows an improving trend in the last couple of years. Total non-performing loans (NPL) decreased to BDT 1,949.17 million in 2009 (2008: 1,695.38 million). The gross NPL ratio reduced to 2.75% in 2009 (2008:2.99%) resulted from rescheduling and loan written off. In 2009, AB Bank had BDT 88.91 million excess provisions against non-performing loans. Special Mention Accounts (SMA) to total loans and advances ratio of the Bank was also reduced to 0.19% in 2009 from 0.40% in 2008.

The Bank was well capitalized in terms of risk weighted capital adequacy ratio which was

13.78% by the end of 2009, against regulatory requirement of 10%. The risk weighted capital adequacy ratio was 11.09% under Basel II for the same period.

Investment income of ABBL increased by 35.80% on back of 43.64% increase in investment portfolio. Investment in quoted shares accounted for 38.78% of total investment in 2009.

The rating reflects the Bank’s strength in earning diversity, satisfactory liquidity as well as capital adequacy. On the other hand, principal concerns of the Bank are low recovery of classified asset and higher rate of fresh NPL generation as well as high investment in shares.

Investment Decision

Looking at the interest rate , credit rating and history of banks grameenphone will choose AB Bank to invest their money as according to credit rating AB bank is the best among these three bank and at same time they are providing higher interest rate for both short term and long term investment. Again AB bank is a very stable bank. It would clearly understood if we check the rations and their background.

Findings

- Grameenphone Ltd. Acute calculations before making their invetments in banks and other financial institutions.

- The financial performance of grameenphone was not that good in last three years compare to previous years.

- Grameenphone often try to get special interest rate from banks for their investment.

Recommendations

- Grameenphone can invest their money in comparatively less stable banks for short term because they earn higher interest from those banks but in case of long term investment financial stability is more important to get their money back.

- Grameenphone should invest their in dfferent terms so that they can earn interest of every single day from bank and at the same time they don’t suffer from liqudity crisis i.e. they should invest their money in such a manner which will help them not to keep their money idol for a single day and at the same they get cash at hand at the right time.

Conclusion

Bangladesh is a country of immense opportunities. With a huge population density and only 22% penetration rate, there is a big untapped market waiting to be discovered. Grameenphone is the biggest market player in the telecommunication industry and should think about these opportunities for retaining the market leader position.

Grameenphone Ltd. is a huge organization. Corporate finance & Treasury department is a very small department. However, regardless of its size, it performs a very important activity for the organization. By doing my internship there I learned a lot of things about revenue collection and investing that money. The employees there were very helpful and friendly to me. This internship experience really helped me to be prepared for the upcoming future.