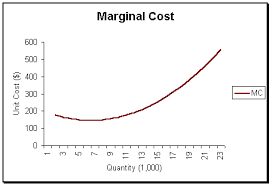

Marginal Cost is the increase or reduction in the total cost of an production run for producing one additional unit associated with an item. It is computed in situations in which the breakeven point may be reached: the fixed costs have been completely absorbed by the particular produced items in support of the direct costs must be accounted for. In economics, marginal cost means the change in the complete cost that arises when the quantity produced posseses an increment by unit.

Marginal Cost Definition